Archives

978-0078025907 Appendix D Solution Manual

Appendix D – Target Annual Report Solutions 1 Appendix D: 2013 Target Annual Report Solutions Management’s Discussion and Analysis 1. U.S. and Canadian 2. Significant Risk Factors include: a. If Target is unable to positively differentiate itself from other retailers, […]

978-0078025907 Appendix E Solution Manual

E-1 SOLUTIONS TO EXERCISES – APPENDIX E EXERCISE E1 Asset FMV LCM HC/AC Buildings X Available-for-Sale Securities X Office Equipment X Inventory X Supplies X Land X Trading Securities X CashIntangible Assets X X Held-to-Maturity Securities X Commented [ILP1]: You […]

978-0078025907 Appendix F Solution Manual

F-1 SOLUTIONS TO APPENDIX F EXERCISE F1 a. $30,000 x 2.158925 = $64,768 (Table I, 8%, 10 years) EXERCISE F2 a. Payment amount x 3.312127 = $25,000 (Table IV, 8%, 4 years) $25,000 3.312127 = $7,548 b. $8,000 x […]

978-0078025907 Chapter 1 Lecture Note Part 1

1-1 Chapter 1 An Introduction to Accounting General Comments for Chapter 1 Most students come to class the first day without a textbook. Even after students have the textbook, many of them do not read assigned chapters prior to attending […]

978-0078025907 Chapter 1 Lecture Note Part 2

1-12 Totals 14,600 + = 5,000 + 9,000 + 600 4,000 – 2,900 = 1,100 14,600 NC 2016 Assets = Liab. + Equity Rev. Ä Exp. = Net Inc. Cash Flow No. Cash + Land = Liab. + C. Stk. […]

978-0078025907 Chapter 1 Solution Manual Part 1

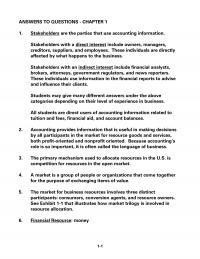

1-1 ANSWERS TO QUESTIONS – CHAPTER 1 1. Stakeholders are the parties that use accounting information. Stakeholders with a direct interest include owners, managers, creditors, suppliers, and employees. These individuals are directly 2. Accounting provides information that is useful in […]

978-0078025907 Chapter 1 Solution Manual Part 2

1-21 1-22 EXERCISE 1-12A (cont.) d. Harris Company Accounting Equation Event Assets = Liabilities + Stockholders’ Equity Acquired assets $7,800 $3,600 $4,200 Incurred loss (4,900) (700) (4,200) Balance $2,900 $2,900 ($ 0) While creditors get first priority to receive assets […]

978-0078025907 Chapter 1 Solution Manual Part 3

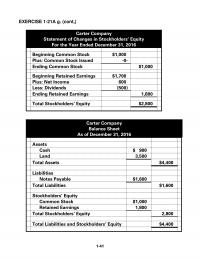

EXERCISE 1-21A g. (cont,) Carter Company Statement of Changes in Stockholders’ Equity For the Year Ended December 31, 2016 Beginning Common Stock $1,000 Plus: Common Stock Issued -0- Ending Common Stock $1,000 Beginning Retained Earnings $1,700 Plus: Net Income 600 […]

978-0078025907 Chapter 1 Solution Manual Part 4

1-61 PROBLEM 1-32A b. (cont.) Mark’s Consulting Services Balance Sheet As of December 31, 2017 Assets Cash $57,500 Land 30,000 Total Assets $87,500 Liabilities Notes Payable $10,000 Stockholders’ Equity Common Stock $44,000 Retained Earnings 33,500 Total Stockholders’ Equity 77,500 Total […]

978-0078025907 Chapter 1 Solution Manual Part 5

1-75 EXERCISE 1-12B e. Investors put assets into the company with the expectation of sharing profits. Creditors lend assets to the company with the expectation of repayment of the principal plus interest on the loan. f. Clayton Company Accounting Equation […]

978-0078025907 Chapter 1 Solution Manual Part 6

1-95 EXERCISE 1-21B (cont.) g. Zeke Company Accounting Equation as of December 31, 2016 Assets = Liabilities + Stockholders’ Equity Notes Common Retained Cash + Land = Payable + Stock + Earnings $200 $1,800 $600 $1,000 400 500 NA NA […]

978-0078025907 Chapter 1 Solution Manual Part 7

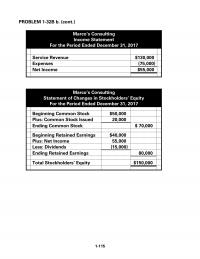

1-115 PROBLEM 1-32B b. (cont.) Marco’s Consulting Income Statement For the Period Ended December 31, 2017 Service Revenue $130,000 Expenses (75,000) Net Income $55,000 Marco’s Consulting Statement of Changes in Stockholders’ Equity For the Period Ended December 31, 2017 Beginning […]

978-0078025907 Chapter 10 Solution Manual Part 1

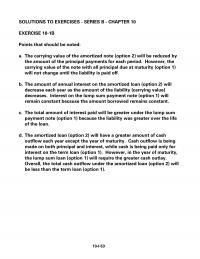

SOLUTIONS TO EXERCISES – SERIES B – CHAPTER 10 EXERCISE 10-1B Points that should be noted: a. The carrying value of the amortized note (option 2) will be reduced by the amount of the principal payments for each period. However, […]

978-0078025907 Chapter 10 Solution Manual Part 2

EXERCISE 10-16B Files Co. General Journal Date Account Titles Debit Credit 2016 Jan. 1 Cash1 388,000 Discount on Bonds Payable 12,000 Bonds Payable 400,000 Dec. 31 Interest Expense 26,400 Discount on Bonds Payable2 2,400 Cash3 24,000 2017 Dec. 31 Interest […]

978-0078025907 Chapter 10 Solution Manual Part 3

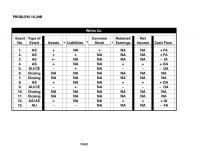

10–93 PROBLEM 10-29B White Co. Event No. Type of Event Assets = Liabilities + Common Stock + Retained Earnings Net Income Cash Flow 1. AS + NA + NA NA + FA 2. AS + + NA NA NA + […]

978-0078025907 Chapter 10 Solution Manual Part 4

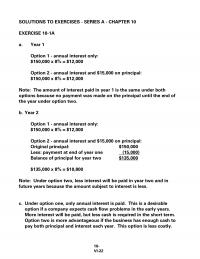

SOLUTIONS TO EXERCISES – SERIES A – CHAPTER 10 EXERCISE 10-1A a. Year 1 Option 1 – annual interest only: $150,000 x 8% = $12,000 Option 2 – annual interest and $15,000 on principal: $150,000 x 8% = $12,000 Note: […]

978-0078025907 Chapter 10 Solution Manual Part 5

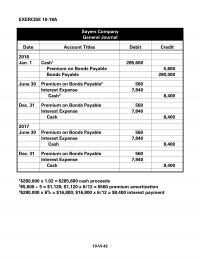

EXERCISE 10-18A Sayers Company General Journal Date Account Titles Debit Credit 2016 Jan. 1 Cash1 285,600 Premium on Bonds Payable 5,600 Bonds Payable 280,000 June 30 Premium on Bonds Payable2 560 Interest Expense 7,840 Cash3 8,400 Dec. 31 Premium on […]

978-0078025907 Chapter 10 Solution Manual Part 6

PROBLEM 10-31A Provided for the instructor’s use: Transactions: 1. Issued bonds at 96. Cash proceeds = $480,000; Discount = $20,000, 1/1/16. 2. Purchased land for $480,000, 1/1/16. 3. Land rental, $60,000 per year, for 2016, 2017, 2018. 4. Interest payments […]

978-0078025907 Chapter 10 Solution Manual Part 7

10–73 ATC 10-2 a. (1)(a) Cash Proceeds (1)(b) Interest Paid: Car, Inc.: Interest paid = $100,000 x 8% = $8,000 per year. Kim, Inc.: Interest paid = $100,000 x 8% = $8,000 per year. Jay, Inc.: Interest paid = $100,000 […]

978-0078025907 Chapter 11 Lecture Note

11-1 Chapter 11 Proprietorships, Partnerships, and Corporations General Comments for Chapter 11 Introductory accounting courses often consist of students who are trying to determine a major or are majoring in something other than accounting. This chapter provides information that is […]

978-0078025907 Chapter 11 Solution Manual Part 1

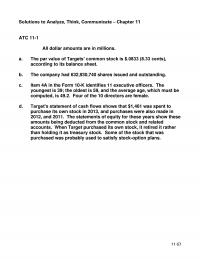

11–57 Solutions to Analyze, Think, Communicate – Chapter 11 ATC 11-1 All dollar amounts are in millions. a. The par value of Targets’ common stock is $.0833 (8.33 cents), according to its balance sheet. b. The company had 632,930,740 shares […]

978-0078025907 Chapter 11 Solution Manual Part 2

11–77 EXERCISE 11-3B (cont.) Bozeman Corporation Financial Statements Balance Sheet As of December 31, 2016 Assets Cash $179,500 Total Assets $179,500 Liabilities $ -0- Stockholders’ Equity Common Stock, $10 par value, 10,000 shares issued and outstanding $100,000 Paid-In Capital in […]

978-0078025907 Chapter 11 Solution Manual Part 3

11–97 11–98 PROBLEM 11-19B (cont.) b. Partnership Best Auto Parts Company Financial Statements For the Year Ended December 31, 2016 Income Statement Revenues $80,000 Expenses (56,000) Net Income $24,000 Capital Statement Beginning Capital Balance $ -0- Plus: Capital Acquired from […]

978-0078025907 Chapter 11 Solution Manual Part 4

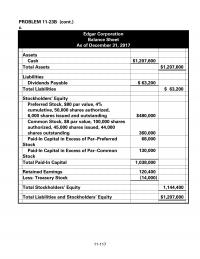

11-117 PROBLEM 11-23B (cont.) c. Edgar Corporation Balance Sheet As of December 31, 2017 Assets Cash $1,207,600 Total Assets $1,207,600 Liabilities Dividends Payable $ 63,200 Total Liabilities $ 63,200 Stockholders’ Equity Preferred Stock, $80 par value, 4% cumulative, 50,000 shares […]

978-0078025907 Chapter 11 Solution Manual Part 5

11–24 EXERCISE 11-2A (cont.) B&B Partnership Financial Statements Balance Sheet As of December 31, 2016 Assets Cash $129,100 Total Assets $129,100 Liabilities $ -0- Equity F. Busby, Capital $51,440 J. Beatty, Capital 77,660 Total Equity 129,100 Total Liabilities and Equity […]

978-0078025907 Chapter 11 Solution Manual Part 6

11–44 EXERCISE 11-18A The memo should contain a definition of the price-earnings ratio. It is one of the most commonly reported measures of a company’s value. It is of $0.01 whose stock is trading at $0.50 has a P/E ratio […]

978-0078025907 Chapter 11 Solution Manual Part 7

11–60 PROBLEM 11-22A (cont.) c. Brice Company December 31, 2016 Stockholders’ Equity Preferred Stock, $20 par value, 6%, 8,000 shares issued and outstanding $160,000 Common Stock, no par value, 88,000 shares issued and outstanding 448,000 Total Paid-In Capital $608,000 Retained […]

978-0078025907 Chapter 12 Lecture Note Part 1

12-1 Chapter 12 Statement of Cash Flows General Comments for Chapter 12 For instructors who prefer the T-account approach to explaining accrual to cash conversions under the direct method, we have included an alternate detailed lesson plan; it follows the […]

978-0078025907 Chapter 12 Lecture Note Part 2

12–16 Demonstration Problem 12-1 Solution, part b., Direct Method Cash Flows from Operating Activities Rules provided for reference: Rules for Computing Cash Flow from Operating Activities, Direct Method Rule 1 Revenue, plus decreases, minus increases in related current assets (accrued […]

978-0078025907 Chapter 12 Solution Manual Part 1

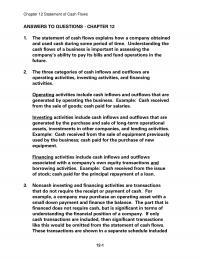

Chapter 12 Statement of Cash Flows 12-1 1. The statement of cash flows explains how a company obtained and used cash during some period of time. Understanding the cash flows of a business is important in assessing the company’s ability […]

978-0078025907 Chapter 12 Solution Manual Part 2

Chapter 12 Statement of Cash Flows 12–21 EXERCISE 12–12A a. Reconciliation of Common Stock Account Beginning balance $150,000 Increase due to issuing common stock ? = 25,000 Ending balance $175,000 Cash Flows from Financing Activities Proceeds from issue of common […]

978-0078025907 Chapter 12 Solution Manual Part 3

Chapter 12 Statement of Cash Flows 12–41 Chapter 12 Statement of Cash Flows 12–42 PROBLEM 12-20A (cont.) (10) Reconciliation of Common Stock Account Beginning balance $120,000 Increase due to issuing common stock ? = 40,000 Ending balance $160,000 This cash […]

978-0078025907 Chapter 12 Solution Manual Part 4

Chapter 12 Statement of Cash Flows 12–61 EXERCISE 12–8B a. Reconciliation of Land Account Beginning balance $178,000 Increase due to purchasing land ? = $103,000 Decrease due to selling land (71,000) Ending balance $210,000 Cash Flows from Investing Activities Proceeds […]

978-0078025907 Chapter 12 Solution Manual Part 5

Chapter 12 Statement of Cash Flows 12–81 PROBLEM 12-17B Item Type of Activity Add or Subtract a. Operating Subtract b. Investing Subtract c. Operating Subtract d. Operating Add e. Financing Subtract f. Operating Subtract g. Financing Subtract h. Financing Add […]

978-0078025907 Chapter 12 Solution Manual Part 6

Chapter 12 Statement of Cash Flows 12–95 PROBLEM 12–21B (1) Reconciliation of Accounts Receivable Beginning balance $ 60,000 Increase due to revenue recognized on account 450,000 Decrease due to cash collections from customers ? = (438,000) Ending balance $ 72,000 […]

978-0078025907 Chapter 13 Solution Manual Part 1

Answers to Questions 1. Ratios and trends are useful tools for analyzing financial statements because they give the analyst a basis for comparing 2. “Liquidity” is the short-term ability to convert assets to cash or some form useful for executing […]

978-0078025907 Chapter 13 Solution Manual Part 2

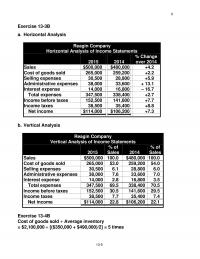

9 13-9 Exercise 13-3B a. Horizontal Analysis Reagin Company Horizontal Analysis of Income Statements 2015 2014 % Change over 2014 Sales $500,000 $480,000 +4.2 Cost of goods sold 265,000 259,200 +2.2 Selling expenses 30,500 28,800 +5.9 Administrative expenses 38,000 33,600 […]

978-0078025907 Chapter 13 Solution Manual Part 3

13–24 Problem 13-24B = 1.96:1 c. Accounts receivables turnover = Net sales ÷ Average A/R = $180,000,000 ÷ $45,500,000 = 3.96 times Days in receivables = 365 ÷ Turnover = 365 ÷ 3.96 = 92.17 d. Cost of goods sold […]

978-0078025907 Chapter 2 Lecture Note Part 1

2-1 Chapter 2 Accounting for Accruals and Deferrals General Comments for Chapter 2 This chapter introduces accrual accounting. A key concept in this chapter is for the student to understand that revenues earned must be matched with expenses incurred to […]

978-0078025907 Chapter 2 Lecture Note Part 2

2-12 Demonstration Problem 2-1B Solution, part 2. Financial Statements Jackson Legal Services Financial Statements Income Statements For the Years Ended December 31, 2014 2015 Fees revenue $ 3,000 $ 9,000 Expenses 0 0 Net income $ 3,000 $ 9,000 Statements […]

978-0078025907 Chapter 2 Solution Manual Part 1

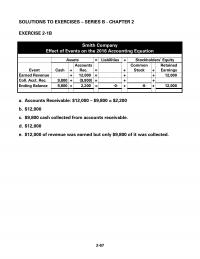

2-67 SOLUTIONS TO EXERCISES – SERIES B – CHAPTER 2 EXERCISE 2-1B Smith Company Effect of Events on the 2016 Accounting Equation Assets = Liabilities + Stockholders’ Equity Event Cash + Accounts Rec. = + Common Stock + Retained Earnings […]

978-0078025907 Chapter 2 Solution Manual Part 2

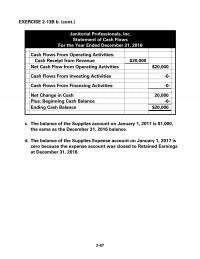

2-87 EXERCISE 2-13B b. (cont.) Janitorial Professionals, Inc. Statement of Cash Flows For the Year Ended December 31, 2016 Cash Flows From Operating Activities: Cash Receipt from Revenue $20,000 Net Cash Flow from Operating Activities $20,000 Cash Flows From Investing […]

978-0078025907 Chapter 2 Solution Manual Part 3

2–107 EXERCISE 2-30B Note: These are only sample transactions. Other similar transactions will satisfy the requirements of this exercise. a. Payment of rent expense; payment of other operating expense. b. Payment of accounts payable; payment of dividends. c. Received a […]

978-0078025907 Chapter 2 Solution Manual Part 4

2-127 PROBLEM 2-42B (cont.) FOR THE YEARS 2016 2017 2018 Statements of Cash Flows Cash flows from oper. activities: Cash receipts from revenue (j)$ 400 $ 500 (v) $ 800 Cash payments for expenses (k) (250) (400) (w) (425) Net […]

978-0078025907 Chapter 2 Solution Manual Part 5

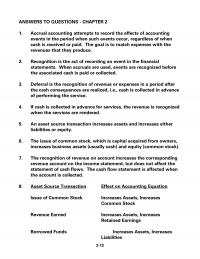

2-12 ANSWERS TO QUESTIONS – CHAPTER 2 1. Accrual accounting attempts to record the effects of accounting 2. Recognition is the act of recording an event in the financial statements. When accruals are used, events are recognized before the associated […]

978-0078025907 Chapter 2 Solution Manual Part 6

2-32 EXERCISE 2-11A a. Examples of expenses that would be matched directly with revenue: Sales commissions Salaries expense b. An example of a period cost that is difficult to match with revenue: Advertising expense – A company can not be […]

978-0078025907 Chapter 2 Solution Manual Part 7

2–52 Ending Cash Balance $55,300 EXERCISE 2-26A Item/Account Statement Item/Account Statement a. Supplies BS u. Rent Exp. IS b. Cash Flow from Financing Act. CF v. P/E Ratio NA c. “As of” Date Notation BS w. Taxes Payable BS d. […]

978-0078025907 Chapter 2 Solution Manual Part 8

2–69 m. Beg. RE $47,500 + NI $20,850 − Div. $2,000 = Ending retained earnings $66,350 2–70 PROBLEM 2-41A Barker Company Financial Statements For the Year Ended December 31, 2016 Income Statement Revenue Service Revenue $65,200 Total Revenue $65,200 Expenses […]

978-0078025907 Chapter 3 Lecture Note Part 1

3-1 Chapter 3 The Double-Entry Accounting System General Comments for Chapter 3 Chapter 3 introduces recording procedures at a level designed to serve students who plan to major in accounting as well as those who do not. Although advances in […]

978-0078025907 Chapter 3 Lecture Note Part 2

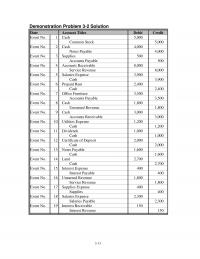

3-13 Demonstration Problem 3-2 Solution Date Account Titles Debit Credit Event No. 1 Cash 5,000 Common Stock 5,000 Event No. 2 Cash 4,000 Notes Payable 4,000 Event No. 3 Supplies 500 Accounts Payable 500 Event No. 4 Accounts Receivable 8,000 […]

978-0078025907 Chapter 3 Solution Manual Part 1

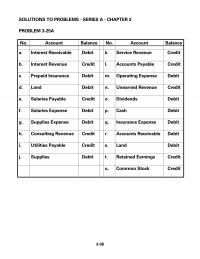

3-38 SOLUTIONS TO PROBLEMS – SERIES A – CHAPTER 3 PROBLEM 3-25A No. Account Balance No. Account Balance a. Interest Receivable Debit k. Service Revenue Credit b. Interest Revenue Credit l. Accounts Payable Credit c. Prepaid Insurance Debit m. Operating […]

978-0078025907 Chapter 3 Solution Manual Part 10

EXERCISE 3-14B a. Account Title Debit Credit Accounts Receivable 50,000 Service Revenue 50,000 Assets = Liab. + Equity Rev. − Exp. = Net Inc. Cash Flows 50,000 NA 50,000 50,000 NA 50,000 NA b. Account Title Debit Credit Operating Expenses […]

978-0078025907 Chapter 3 Solution Manual Part 11

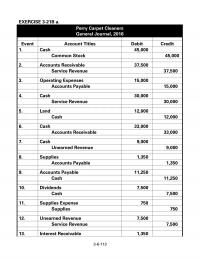

3-6–113 EXERCISE 3-21B a. Perry Carpet Cleaners General Journal, 2016 Event Account Titles Debit Credit 1. Cash 45,000 Common Stock 45,000 2. Accounts Receivable 37,500 Service Revenue 37,500 3. Operating Expenses 15,000 Accounts Payable 15,000 4. Cash 30,000 Service Revenue […]

978-0078025907 Chapter 3 Solution Manual Part 2

3-58 PROBLEM 3-33A (cont.) b. Colton Enterprises T-Accounts – 2016 Assets = Liabilities + Stockholders’ Equity Cash Accounts Pay. Common Stock 1. 35,000 2. 12,000 7. 28,000 4. 35,000 1. 35,000 5. 55,500 6. 21,000 Bal. 7,000 Bal. 35,000 7. […]

978-0078025907 Chapter 3 Solution Manual Part 3

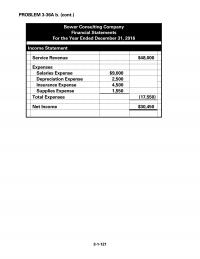

3-1–121 PROBLEM 3-36A b. (cont.) Bower Consulting Company Financial Statements For the Year Ended December 31, 2016 Income Statement Service Revenue $48,000 Expenses Salaries Expense $9,000 Depreciation Expense 2,500 Insurance Expense 4,500 Supplies Expense 1,550 Total Expenses (17,550) Net Income […]

978-0078025907 Chapter 3 Solution Manual Part 4

3-141 PROBLEM 3-32B (cont.) e. Price Corporation Closing Entries, 2016 Date Account Titles Debit Credit Dec. 31 Service Revenue 29,400 Retained Earnings 29,400 Dec. 31 Retained Earnings 22,950 Salaries Expense 19,100 Rent Expense 3,500 Supplies Expense 350 Dec. 31 Retained […]

978-0078025907 Chapter 3 Solution Manual Part 5

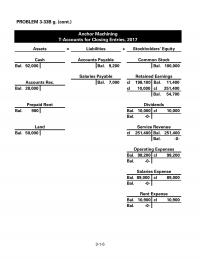

3-1–5 PROBLEM 3-33B g. (cont.) Anchor Machining T-Accounts for Closing Entries, 2017 Assets = Liabilities + Stockholders’ Equity Cash Accounts Payable Common Stock Bal. 92,000 Bal. 9,200 Bal. 100,000 Salaries Payable Retained Earnings Accounts Rec. Bal. 7,000 cl 198,100 Bal. […]

978-0078025907 Chapter 3 Solution Manual Part 6

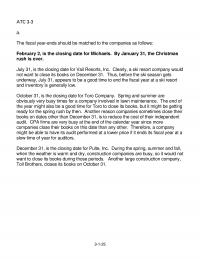

3-1–25 ATC 3-3 a. The fiscal year-ends should be matched to the companies as follows: February 2, is the closing date for Michaels. By January 31, the Christmas rush is over. July 31, is the closing date for Vail Resorts, […]

978-0078025907 Chapter 3 Solution Manual Part 7

3-6–45 COMPREHENSIVE PROBLEM – CHAPTER 3 (cont.) e. Pacilio Security Services, Inc. T-Accounts for 2013 Assets = Liabilities + Stockholders’ Equity Cash Accounts Payable Common Stock Bal. 12,500 Bal. -0- Bal. 8,000 Retained Earnings Accounts Receivable Unearned Revenue cl 19,445 […]

978-0078025907 Chapter 3 Solution Manual Part 8

3-65 3-66 EXERCISE 3-14A a. Account Title Debit Credit Accounts Receivable 8,200 Service Revenue 8,200 Assets = Liab. + Equity Rev. − Exp. = Net Inc. Cash Flow 8,200 NA 8,200 8,200 NA 8,200 NA b. Account Title Debit Credit […]

978-0078025907 Chapter 3 Solution Manual Part 9

3-6–82 3-6–83 EXERCISE 3-23A a. Company Total Debt Total Assets = Debt to Assets Ratio Ever-Well $ 96,000 $320,000 = 30.0% Eat-Right $280,000 $700,000 = 40.0% b. Based only on the debt to assets ratio, Eat-Right has […]

978-0078025907 Chapter 4 Lecture Note Part 1

4-1 Chapter 4 Accounting for Merchandising Businesses General Comments for Chapter 4 Chapter 4 introduces accounting for inventory transactions using the perpetual method. In today’s high-technology environment, the perpetual system has become the predominant method of accounting for inventories. Because […]

978-0078025907 Chapter 4 Lecture Note Part 2

4-12 Demonstration Problem 4-3 Solution Lisa’s Dress Supply Schedule of Cost of Goods Sold Beginning inventory $ 0 Purchases 54,000 Purchase returns and allowances (4,000) Purchase discounts (1,000) Transportation-in 1,000 Cost of goods available for sale $50,000 Ending inventory (10,800) […]

978-0078025907 Chapter 4 Solution Manual Part 1

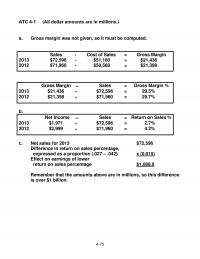

4-75 ATC 4-1 (All dollar amounts are in millions.) a. Gross margin was not given, so it must be computed. Sales – Cost of Sales = Gross Margin 2013 $72,596 – $51,160 = $21,436 2012 $71,960 – $50,568 = $21,398 […]

978-0078025907 Chapter 4 Solution Manual Part 2

4-95 Net Cash Flow from Operating Activities $ 4,500 4-96 EXERCISE 4-3B (cont.) f. Net income is $11,000 and net cash flow from operating activities is $4,500. Revenue earned amounted to $50,000 but only $38,000 was collected. Expenses actually incurred […]

978-0078025907 Chapter 4 Solution Manual Part 3

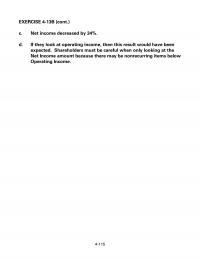

4-115 EXERCISE 4-13B (cont.) c. Net income decreased by 34%. d. If they look at operating income, then this result would have been expected. Shareholders must be careful when only looking at the Net Income amount because there may be […]

978-0078025907 Chapter 4 Solution Manual Part 4

4-135 4-136 EXERCISE 4-22B (cont.) d. Sally’s Gift Shop General Journal Date Account Titles Debit Credit Closing Entries cl Sales Revenue 98,300 Retained Earnings 98,300 cl Retained Earnings 59,900 Cost of Goods Sold 43,400 Advertising Expense 4,500 Salaries Expense 12,000 […]

978-0078025907 Chapter 4 Solution Manual Part 5

4-155 PROBLEM 4-28B (cont.) (Appendix) b. Multistep income statement Hogan Sales Co. Income Statement For the Year Ended December 31, 2016 Sales Sales Revenue $640,000 Sales Returns and Allowances (16,000) Net Sales $624,000 Cost of Goods Sold (302,800) Gross Margin […]

978-0078025907 Chapter 4 Solution Manual Part 6

4-21 EXERCISE 4-1Aa. (cont.) Sports Clothing Statement of Cash Flows For the Year Ended December 31, 2016 Cash Flows From Operating Activities: Cash Inflow from Customers 50,000 Cash Outflow for Inventory (50,000) Cash Outflow for Expenses (8,000) Net Cash Flow […]

978-0078025907 Chapter 4 Solution Manual Part 7

4-41 EXERCISE 4-12A b. (cont.) Ho Designs Balance Sheet As of December 31, 2016 Assets Cash $85,200 Merchandise Inventory 3,200 Total Assets $88,400 Liabilities $ -0- Stockholders’ Equity Common Stock $70,000 Retained Earnings 18,400 Total Stockholders’ Equity 88,400 Total Liab. […]

978-0078025907 Chapter 4 Solution Manual Part 8

4-61 EXERCISE 4-22A (cont.) (Appendix) b. Bob’s Bike Shop T-Accounts for 2016 Assets = Liabilities + Stockholders’ Equity Cash Accounts Payable Common Stock 1. 35,000 4. 2,800 7. 65,000 3. 85,000 1. 35,000 5. 165,000 6. 28,000 Bal. 20,000 2. […]

978-0078025907 Chapter 4 Solution Manual Part 9

4-77 Bal. -0- 4-78 PROBLEM 4-26A (Cont.) d. Redd Company Financial Statements For the Year Ended December 31, 2016 Income Statement Net Sales $10,178 Cost of Goods Sold (6,542) Gross Margin 3,636 Operating Expenses Transportation–out (140) Operating Income 3,496 Nonoperating […]

978-0078025907 Chapter 5 Lecture Note Part 1

5-1 Chapter 5 Accounting for Inventories General Comments for Chapter 5 This chapter explains inventory valuation methods, how to determine cost of goods sold, and other accounting issues related to inventory. It shows students that a company may report certain […]

978-0078025907 Chapter 5 Lecture Note Part 2

5-13 Demonstration Problem 5-3 Solution Determination of Ending Inventory at Lower of Cost or Market Type Quantity Unit Cost Unit Market Total Cost Total Market Lower of C or M A 100 $12.00 $15.00 $ 1,200 $ 1,500 $ 1,200 […]

978-0078025907 Chapter 5 Solution Manual Part 1

5-6 ANSWERS TO QUESTIONS – CHAPTER 5 1. (1.) Specific Identification – The inventory cost flow method that (2.) First In, First Out – The inventory cost flow method that assumes that the first items purchased are the first items […]

978-0078025907 Chapter 5 Solution Manual Part 2

5-26 EXERCISE 5-6A (cont.) c. Income tax paid using FIFO: $32,430 Income tax paid using LIFO: $31,710 d. Parvin Company Cash Flows from Operating Activities FIFO LIFO Cash Flows From Operating Activities: Cash Inflow from Customers $243,000 $243,000 Cash Outflow […]

978-0078025907 Chapter 5 Solution Manual Part 3

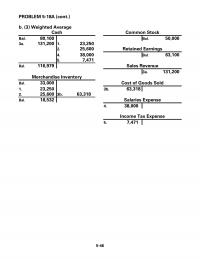

5-46 PROBLEM 5-18A (cont.) b. (3) Weighted Average Cash Common Stock Bal. 80,100 Bal. 50,000 3a. 131,200 1. 23,250 2. 25,600 Retained Earnings 4. 38,000 Bal. 63,100 5. 7,471 Bal. 116,979 Sales Revenue 3a. 131,200 Merchandise Inventory Bal. 33,000 Cost […]

978-0078025907 Chapter 5 Solution Manual Part 4

EXERCISE 5-2B Harris Co. First Purchase $3,600 Second Purchase 4,200 Total $7,800 (a) (b) (c) FIFO LIFO W. AVG. Cost of Goods Sold $3,600 $4,200 $3,900* Ending Inventory 4,200 3,600 3,900* *Average Cost per Unit: $7,800 2 = $3,900 […]

978-0078025907 Chapter 5 Solution Manual Part 5

5-87 EXERCISE 5-11B a. a. b. c. d. e. f. g. Item Quantity Cost Per Unit Mkt. Value Per Unit Unit Lower Cost/Mkt. Total Cost Total Lower Cost/Mkt. (b x c) (b x e) A 400 $20 $18 $18 $8,000 […]

978-0078025907 Chapter 5 Solution Manual Part 6

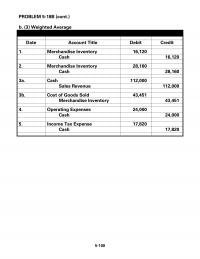

PROBLEM 5-18B (cont.) 5-100 b. (3) Weighted Average Date Account Title Debit Credit 1. Merchandise Inventory 16,120 Cash 16,120 2. Merchandise Inventory 28,160 Cash 28,160 3a. Cash 112,000 Sales Revenue 112,000 3b. Cost of Goods Sold 43,451 Merchandise Inventory 43,451 […]

978-0078025907 Chapter 6 Lecture Note

Copyright © McGraw-Hill Education. Permission required for reproduction or display. 6-1 Chapter 6 Internal Control and Accounting for Cash General Comments for Chapter 6 Most students find the concepts in this chapter less difficult than those in the two previous […]

978-0078025907 Chapter 6 Solution Manual Part 1

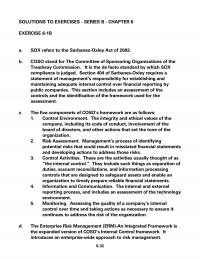

6-32 SOLUTIONS TO EXERCISES – SERIES B – CHAPTER 6 EXERCISE 6-1B a. SOX refers to the Sarbanes-Oxley Act of 2002. b. COSO stand for The Committee of Sponsoring Organizations of the 1. Control Environment. The integrity and ethical values […]

978-0078025907 Chapter 6 Solution Manual Part 2

6-52 PROBLEM 6-21B a. Pyle Garage Bank Reconciliation March 31, 2016 Unadjusted Bank Balance, March 31, 2016 $16,000.00 Add: Deposit in Transit 2,000.00 Less: Outstanding Checks #1469 $1,500.00 1470 102.00 (1,602.00) True Cash Balance, March 31, 2016 $16,398.00 Unadjusted Book […]

978-0078025907 Chapter 6 Solution Manual Part 3

6-22 EXERCISE 6-7A a. & c. Han’s Supplies Statements Model Assets = Liab. + S. Equity Rev. − Exp. = Net Inc. Cash Flow Cash + Acct. Rec. (a) (270) + 270 = NA + NA NA − NA = […]

978-0078025907 Chapter 6 Solution Manual Part 4

6-37 PROBLEM 6-23A a. Account Title Debit Credit Accounts Receivable 1,800 Cash 1,800 b. The clerk has collected cash from a customer on account. This required a book entry debiting cash and crediting accounts receivable. Instead of depositing the money, […]

978-0078025907 Chapter 7 Lecture Note Part 1

7-1 Chapter 7 Accounting for Receivables General Comments for Chapter 7 This chapter focuses on accounting for receivables – both collectible and uncollectible. This chapter also includes accounting for credit card sales and discount notes. You can begin this chapter […]

978-0078025907 Chapter 7 Lecture Note Part 2

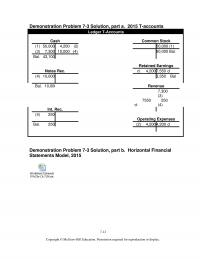

7-12 Demonstration Problem 7-3 Solution, part a. 2015 T-accounts Ledger T-Accounts Cash Common Stock (1) 50,000 4,200 (2) 50,000 (1) (3) 7,300 10,000 (4) 50,000 Bal. Bal. 43,100 Retained Earnings Notes Rec. cl. 4,200 7,550 cl (4) 10,000 3,350 Bal […]

978-0078025907 Chapter 7 Solution Manual Part 1

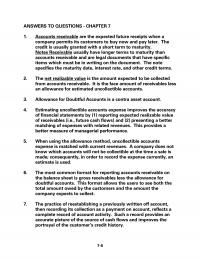

7–6 ANSWERS TO QUESTIONS – CHAPTER 7 1. Accounts receivable are the expected future receipts when a company permits its customers to buy now and pay later. The 2. The net realizable value is the amount expected to be collected […]

978-0078025907 Chapter 7 Solution Manual Part 2

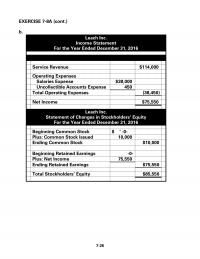

7–26 EXERCISE 7-8A (cont.) b. Leach Inc. Income Statement For the Year Ended December 31, 2016 Service Revenue $114,000 Operating Expenses Salaries Expense $38,000 Uncollectible Accounts Expense 450 Total Operating Expenses (38,450) Net Income $75,550 Leach Inc. Statement of Changes […]

978-0078025907 Chapter 7 Solution Manual Part 3

7–46 SOLUTIONS TO PROBLEMS – SERIES A – CHAPTER 7 PROBLEM 7-17A a. Event Number Type of Transaction 2016 1, Asset Source 2. Asset Source 3. Asset Exchange 4. Asset Use 5. Asset Use 2017 1. Asset Source 2. Asset […]

978-0078025907 Chapter 7 Solution Manual Part 4

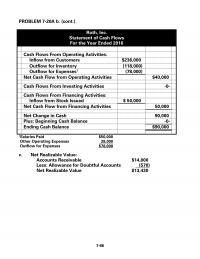

7-66 PROBLEM 7-20A b. (cont.) Roth, Inc. Statement of Cash Flows For the Year Ended 2016 Cash Flows From Operating Activities: Inflow from Customers $236,000 Outflow for Inventory (118,000) Outflow for Expenses1 (78,000) Net Cash Flow from Operating Activities $40,000 […]

978-0078025907 Chapter 7 Solution Manual Part 5

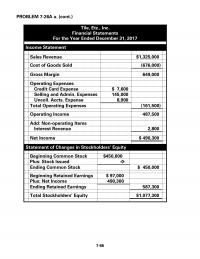

7-86 PROBLEM 7-26A a. (cont.) Tile, Etc., Inc. Financial Statements For the Year Ended December 31, 2017 Income Statement Sales Revenue $1,325,000 Cost of Goods Sold (676,000) Gross Margin 649,000 Operating Expenses Credit Card Expense $ 7,600 Selling and Admin. […]

978-0078025907 Chapter 7 Solution Manual Part 6

7-100 EXERCISE 7-4B a. & c. (cont.) Reliable Auto Service T-Accounts Assets = Liabilities + Stockholders’ Equity Cash Retained Earnings 2016 2016 2. 32,000 5. cl 450 4. cl 45,000 Bal. 32,000 Bal. 44,550 2017 3. 66,000 Service Revenue Bal. […]

978-0078025907 Chapter 7 Solution Manual Part 7

7-120 EXERCISE 7-12B a. $18,000 x 5% x 10/12 = $750 b. Total Receivables at December 31, 2016: Notes Receivable $18,000 Interest Receivable 750 Total Receivables $18,750 c. Investing Activities: Outflow for Note Receivable ($18,000) Interest is not reported on […]

978-0078025907 Chapter 7 Solution Manual Part 8

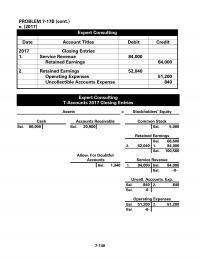

7-140 PROBLEM 7-17B (cont.) e. (2017) Expert Consulting Date Account Titles Debit Credit 2017 Closing Entries 1. Service Revenue 84,000 Retained Earnings 84,000 2. Retained Earnings 52,040 Operating Expenses 51,200 Uncollectible Accounts Expense 840 Expert Consulting T-Accounts 2017 Closing Entries […]

978-0078025907 Chapter 7 Solution Manual Part 9

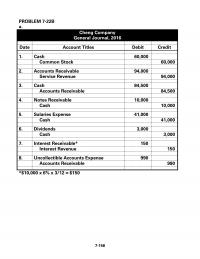

7-156 PROBLEM 7-22B a. Cheng Company General Journal, 2016 Date Account Titles Debit Credit 1. Cash 60,000 Common Stock 60,000 2. Accounts Receivable 94,000 Service Revenue 94,000 3. Cash 84,500 Accounts Receivable 84,500 4. Notes Receivable 10,000 Cash 10,000 5. […]

978-0078025907 Chapter 8 Lecture Note Part 1

8-1 Chapter 8 Accounting for Long-Term Operational Assets General Comments for Chapter 8 This chapter introduces the concepts of current, long-term, tangible, and intangible assets and also explains how acquiring, using, and disposing of long-term operational assets affects fi- nancial […]

978-0078025907 Chapter 8 Lecture Note Part 2

8-14 Ending cash balance $9,000 $13,800 $23,400 $29,800 $34,100 Copyright © McGraw-Hill Education. Permission required for reproduction or display. 8-15 Demonstration Problem 8-2 Solution 1. Paid $1,000 cash for maintenance cost. Assets = Liab. + Equity Rev. – Exp. = […]

978-0078025907 Chapter 8 Solution Manual Part 1

8-121 ATC 8-1 All dollar amounts are in millions. a. Straight-line. See Note 12 of the annual report. b. Note 14 of the annual report refers to “goodwill and intangible assets.” Other than mentioning “goodwill” and “leasehold acquisition costs,” no […]

978-0078025907 Chapter 8 Solution Manual Part 2

8-65 EXERCISE 8-7B a. (cont.) The Soda Shop T-Accounts for 2016 Assets = Stockholders’ Equity Cash Common Stock Service Revenue 1. 20,000 2. 20,000 1. 20,000 3. 36,000 3. 36,000 4. 21,000 Bal. 20,000 Bal. 36,000 5. 6,000 Bal. 9,000 […]

978-0078025907 Chapter 8 Solution Manual Part 3

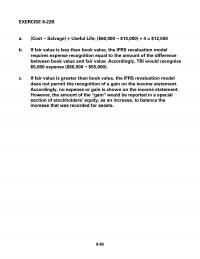

8-85 EXERCISE 8-22B a. (Cost − Salvage) ÷ Useful Life; ($60,000 − $10,000) ÷ 4 = $12,500 b. If fair value is less than book value, the IFRS revaluation model requires expense recognition equal to the amount of the difference […]

978-0078025907 Chapter 8 Solution Manual Part 4

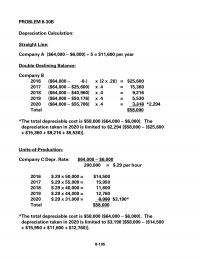

8-105 PROBLEM 8–30B Depreciation Calculation: Straight Line: Company A ($64,000 − $6,000) 5 = $11,600 per year Double-Declining Balance: Company B 2016 ($64,000 − -0-) x (2 x .20) = $25,600 2017 ($64,000 − $25,600) x .4 = 15,360 […]

978-0078025907 Chapter 8 Solution Manual Part 5

8-18 plant, and equipment in total assets amd thus more depreciation expense relative to sales than a labor-intensive company. 8-19 EXERCISE 8-1A Note: There are many possibilities for answers to this question. The answers given are only a few examples […]

978-0078025907 Chapter 8 Solution Manual Part 6

8-38 EXERCISE 8-14A a. MACRS depreciation = Cost x MACRS Table % EXERCISE 8-15A Depreciation Expense 2016: $42,000 − $3,000 = $39,000; $39,000 3 = $13,000 2017: (Same as year 2016.) $13,000 2018: Cost $42,000 Less: Acc.Depr. (26,000) Book […]

978-0078025907 Chapter 8 Solution Manual Part 7

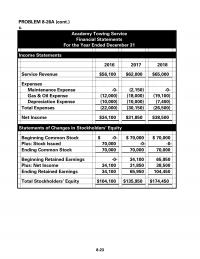

8-23 PROBLEM 8-26A (cont.) c. Academy Towing Service Financial Statements For the Year Ended December 31 Income Statements 2016 2017 2018 Service Revenue $56,100 $62,000 $65,000 Expenses Maintenance Expense -0- (2,150) -0- Gas & Oil Expense (12,000) (18,000) (19,100) Depreciation […]

978-0078025907 Chapter 8 Solution Manual Part 8

8-35 PROBLEM 8-30A (cont.) d. Sales (four years) $160,000 Depreciation (four years) (45,000) Retained Earnings $115,000 All companies have the same retained earnings because over the four- year period, the total depreciation is the same. e. The cash flow from […]

978-0078025907 Chapter 9 Lecture Note

Copyright © McGraw-Hill Education. Permission required for reproduction or display. 9-1 Chapter 9 Accounting for Liabilities and Payroll General Comments for Chapter 9 Students were initially introduced to the concept of accounts payable in Chapter 2. Chapter 9 looks at […]

978-0078025907 Chapter 9 Solution Manual Part 1

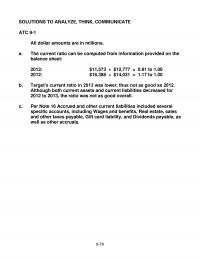

9-70 SOLUTIONS TO ANALYZE, THINK, COMMUNICATE ATC 9-1 All dollar amounts are in millions. a. The current ratio can be computed from information provided on the balance sheet: 2013: $11,573 ÷ $12,777 = 0.91 to 1.00 2012: $16,388 ÷ $14,031 […]

978-0078025907 Chapter 9 Solution Manual Part 2

9–90 EXERCISE 9-6B (cont.) c. Owens Computers Financial Statements Income Statement Sales Revenue $280,000 Cost of Goods Sold (150,000) Gross Margin 130,000 Warranty Expense (14,000) Net Income $ 116,000 Statement of Cash Flows Cash Flows From Operating Activities: Inflow from […]

978-0078025907 Chapter 9 Solution Manual Part 3

9–110 EXERCISE 9-13B a. Ritter Co. General Journal for 2016 Event Account Titles Debit Credit 1. Cash 40,000 Common Stock 40,000 2. Merchandise Inventory 128,000 Accounts Payable 128,000 3a. Cash 210,000 Sales Revenue 200,000 Sales Tax Payable ($200,000 x 5%) […]

978-0078025907 Chapter 9 Solution Manual Part 4

9–130 Ending Cash Balance $107,800 9–131 PROBLEM 9-20B (cont.) d. Barclay Co. General Journal for 2016 Event Account Title Debit Credit Closing Entries cl Service Revenue 140,000 Retained Earnings 140,000 cl Retained Earnings 85,875 Operating Expenses 84,000 Interest Expense 1,875 […]

978-0078025907 Chapter 9 Solution Manual Part 5

9–150 PROBLEM 9-25B (cont.) Brown Company Balance Sheet As of December 31, 2016 Assets Current Assets Cash $ 46,000 Accounts Receivable $88,000 Less: Allow. for Doubtful Accounts (14,000) 74,000 Merchandise Inventory 126,000 Interest Receivable 1,600 Prepaid Rent 18,000 Supplies 4,500 […]

978-0078025907 Chapter 9 Solution Manual Part 6

9-16 EXERCISE 9-5A 1. Probable and can be reasonably estimated. This category of contingent liabilities is recognized in the financial statements. 2. Reasonably possible, or probable but cannot be reasonably estimated. This category of contingent liabilities is disclosed in the […]

978-0078025907 Chapter 9 Solution Manual Part 7

9-36 EXERCISE 9-11A (cont.) b. (3) Assume gross salary is $9,600: Sky Co. payroll tax expense – January: Employer FICA Social Security tax ($9,600 x 6%) $ 576 Employer FICA Medicare tax ($9,600 x 1.5%) 144 Employer unemployment tax ($7,000 […]

978-0078025907 Chapter 9 Solution Manual Part 8

9-56 Bal. 50,000 Bal. 2,250 9-57 PROBLEM 9-20A (cont.) c. Walnut Enterprises Income Statement For the Year Ended December 31, 2016 Service Revenue $130,000 Expenses Operating Expenses $62,000 Total Operating Expenses (62,000) Operating Income 68,000 Interest Expense (2,250) Net Income […]

978-0078025907 Chapter 9 Solution Manual Part 9

9-74 PROBLEM 9-23A Electronics Services Co. General Journal Date Account Title Debit Credit a. 12/31 Administrative Salaries Expense 96,000 Sales Salaries Expense 57,000 Office Salaries Expense 38,000 Employee Fed. Income Tax Payable 21,500 Employee State Income Tax Pay. 11,200 FICA […]

AC 15873

Indicate whether each of the following statements regarding internal controls is true or false. _____ a) The Sarbanes-Oxley Act of 2002 requires public companies to evaluate their internal controls and report those findings with SEC filings. _____ b) The Sarbanes-Oxley […]

AC 27069

What event and inventory method may have produced the following journal entry? A.A return of goods by a customer under the perpetual inventory method. B.A sale of goods under the periodic inventory method. C.A return of goods by a customer […]

ACC 11449

Indicate whether each of the following statements about financial statement analysis is true or false. _____ a) Both dividends and earnings performance are indicators of the value of a company’s stock. _____ b) The most widely quoted measure of a […]

ACC 28267

For a company that uses the allowance method, the write-off of an uncollectible account receivable is an asset use transaction. Preparing a bank reconciliation is a requirement to obtain an unqualified audit opinion, but is not an important internal control […]

Acc 38398

A debit entry A.increases assets. B.increases expenses. C.decreases liabilities. D.increases assets, expenses, and liabilities. Under what condition should a pending lawsuit be recognized as a liability on a company’s balance sheet? A.The amount can be reasonably estimated. B.The outcome is […]

Acc 50272

On January 1, 2016, The Hanover Corporation issued $70,500 of 8%, 5-year bonds at 97. Hanover uses the straight-line method of bond discount amortization. The interest payments are due on December 31 each year. The journal entry used to record […]

Acc 51538

Indicate whether each of the following statements about financial statement analysis is true or false. _____ a) Comparing percentages derived from financial statement analysis has the drawback of varying materiality levels. _____ b) The materiality of accounting information refers to […]

ACC 80344

In the reconciliation of the June bank statement, a deposit made on June 30 did not appear on the June bank statement. In preparing the bank reconciliation, this deposit in transit should be: A.subtracted from the unadjusted book balance. B.added […]

Acc 98780

Kier Company issued $200,000 in bonds on January 1, 2016. The bonds were issued at face value and carried a 4-year term to maturity. They had a 6 % stated rate of interest that was payable in cash on December […]

Accounting 11588

Dividends paid by a company are shown on the A.income statement. B.statement of changes in stockholders’ equity. C.statement of cash flows. D.the statement of changes in stockholders’ equity and the statement of cash flows. Indicate whether each of the following […]

Accounting 64262

Using the allowance method of accounting for uncollectible receivables requires an estimate of the amount of receivables that will not be collected. In preparing a bank reconciliation, typical adjustments to the bank balance are deposits in transit and outstanding checks. […]

Accounting 76301

When the direct method is used to prepare the operating activities section of the statement of cash flows, cash inflows from customers and cash outflows for depreciation are among the categories of cash flows likely to be reported. The cost […]

ACCT 31678

Wholesale companies sell goods primarily to other businesses. The indirect method for preparing the operating activities section of the statement of cash flows begins with the amount of sales revenue reported on the income statement. Answer: False Feedback: The indirect […]

ACCT 37697

The operating cycle is the length of time that a company spends acquiring inventory to sell. Merchandising businesses include retail companies and manufacturing companies. Answer: False After closing, all income statement accounts have non-zero balances. Answer: False The debt to […]

Acct 40166

For 2016, The Oscar Company records depreciation expense of $12,000 on its income statement and $9,000 of MACRS depreciation on its tax return. Which of the following answers is correct regarding the difference between the two figures? A.Net income is […]

ACCT 45471

All journal entries made related to bank reconciliations include an expense or revenue account. Two of the steps in the accounting cycle are adjusting the accounts and closing the accounts. Answer: True Net sales is calculated by subtracting cost of […]

ACCT 48466

Blake Company loaned Jiminez Corporation $18,000 on October 1, 2016. The 8-month note carried a 6% rate of interest. Required: a) How will Blake report the note and interest on its 2016 income statement, balance sheet, and statement of cash […]

ACCT 59956

Statler Corporation has beginning and ending accounts payable balances of $400 and $800, respectively. Inventory had beginning and ending balances of $700 and $600, respectively. If cost of goods sold was $2,800, how much cash was spent to purchase inventory? […]

ACCT 90277

Assume that you are considering purchasing some of a company’s long-term bonds as an investment. Which of the company’s financial statement ratios would you probably be most interested in? A. Debt to assets ratio B. Debt to equity C. Plant […]

Acct 91114

Assume the perpetual inventory method is used. 1) Green Company purchased merchandise inventory that cost $64,000 under terms of 2/10, n/30 and FOB shipping point. 2) The company paid freight cost of $2,400 to have the merchandise delivered. 3) Payment […]

Acct 94211

Posting is the process of determining the balance in an account by subtracting debits and credits. A benefit of corporations is that they are free from double taxation. Answer: False Feedback: Double taxation is a disadvantage of corporations. For many […]

ACT 38667

Davis Corporation borrowed $50,000 on January 1, 2016. The loan is for a ten-year period and has an annual interest rate of 9%. At the end of each year, Davis will make a payment of $7,791, which includes both principal […]

ACT 51559

On January 1, 2016, Kincaid Company’s Accounts Receivable and the Allowance for Doubtful Accounts carried balances of $31,000 and $500, respectively. During the year Kincaid reported $72,500 of credit sales. Kincaid wrote off $550 of receivables as uncollectible in 2016. […]

ACT 68822

Indicate whether each of the following statements is true or false. _____ a) Financial statement ratios permit comparisons over time and among different companies. _____ b) Knowledge of financial statement analysis techniques is useful to stockholders and creditors but not […]

ACT 95328

The Cost of Goods Sold account is classified as: A.a liability. B.an asset. C.a contra asset. D.an expense. Jing Company was started on January 1, 2016 when it issued common stock for $50,000 cash. Also, on January 1, 2016 the […]

MET MG 10648

Oregon Company provided the following income statement for 2014 and 2015: Required: (a) Perform vertical analysis on Oregon’s income statements for 2014 and 2015. (b) Comment on the results, comparing 2014 to 2015. Phipps Corporation overstated its ending inventory on […]

MET MG 22451

Victor Company issued bonds with a $250,000 face value and a 6% stated rate of interest on January 1, 2016. The bonds carried a 5-year term and sold for 95. Victor uses the straight-line method of amortization. Interest is payable […]

MET MG 79914

The following balance sheet information is provided for Victor Company: What is the company’s working capital? A.$3,810 B.$9,810 C.$18,610 D.$26,840 Compute the amount of cash a company will receive from the following bond issues. a) _______________ Issued $200,000 of 5-yr, […]

Nelson Company Experienced The Following Transactions During Year 1

Hernandez Company began business operations and experienced the following transactions during 2016: 1) Issued common stock for $50,000 cash. 2) Provided services to customers for $125,000 on account. 3) Purchased $2,500 of supplies on account. 4) Paid $30,000 cash to […]

SMG AC 46249

The party that issues a promissory note is known as the A.lender. B.maker. C.borrower. D.lender and maker. Total debt is accounts payable ($4,310) salaries payable ($10,030) and bonds payable ($9,000); total assets are equal to total liabilities and stockholders’ equity: […]

SMG AC 75054

Gomez Co. had beginning inventory of $2,400 and ending inventory of $1,200. The cost of goods sold was $9,600. Based on this information, Gomez Co. must have purchased inventory amounting to: A.$8,400. B.$9,600. C.$10,800. D.$13,200. Hartford Company borrowed $20,000 on […]