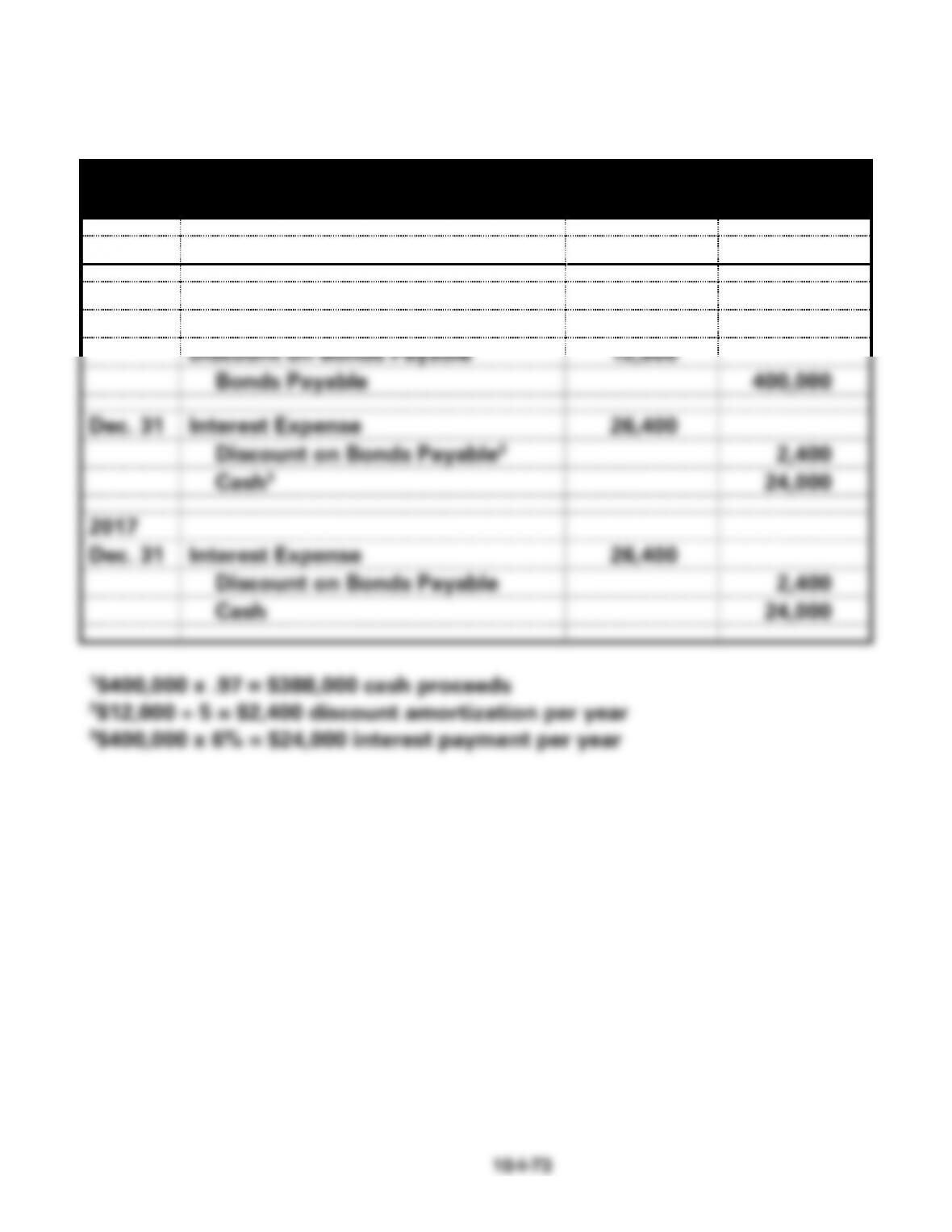

EXERCISE 10-16B

Files Co.

General Journal

Date

Account Titles

Debit

Credit

2016

Jan. 1

Cash1

388,000

Discount on Bonds Payable

12,000

Bonds Payable

400,000

Dec. 31

Interest Expense

26,400

Discount on Bonds Payable2

2,400

Cash3

24,000

2017

Dec. 31

Interest Expense

26,400

Discount on Bonds Payable

2,400

Cash

24,000

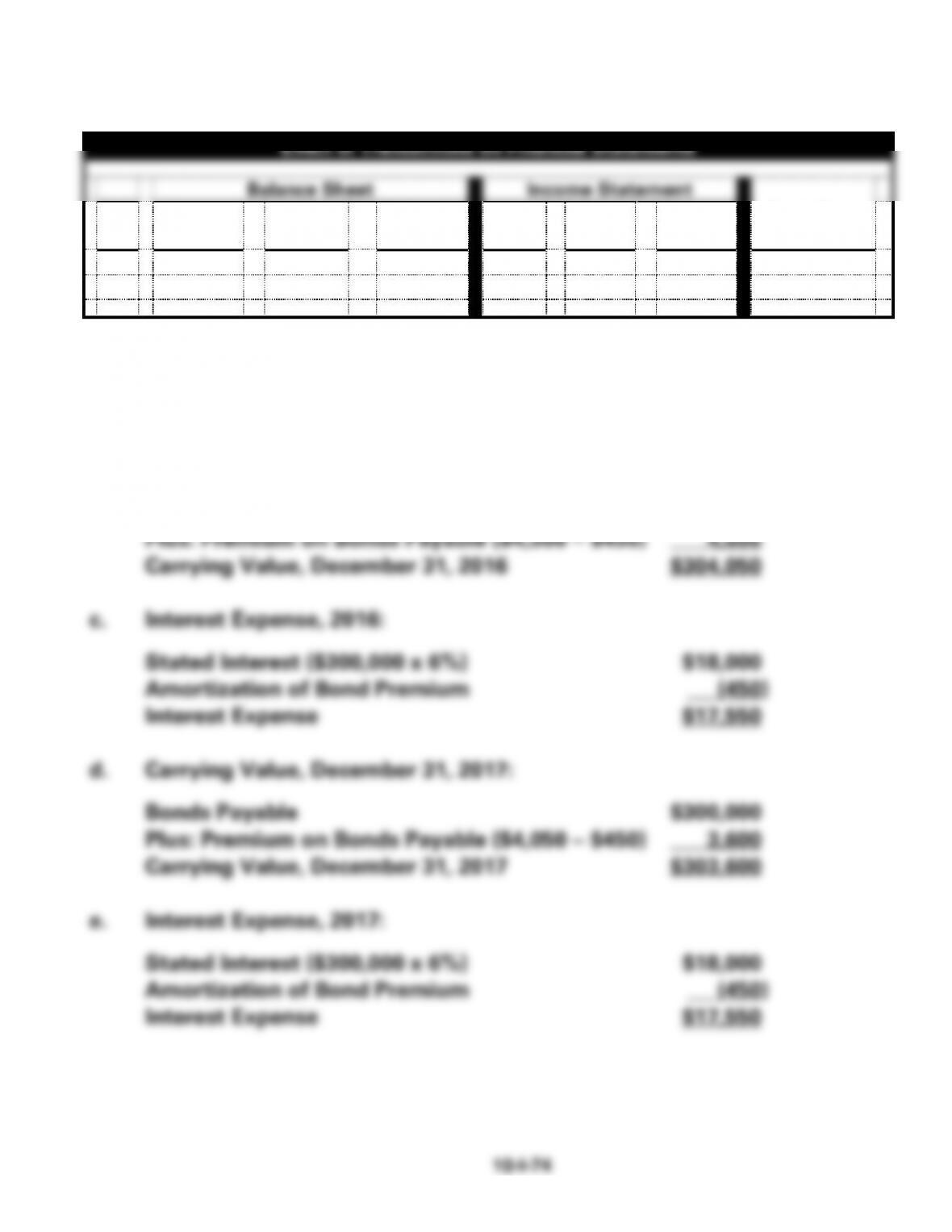

EXERCISE 10-17B

a.

Effect of Transactions on Financial Statements

Balance Sheet

Income Statement

No

.

Assets

=

Liab.

+

S. Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

1.

+

+

NA

NA

NA

NA

+ FA

2a.

−

−

−

NA

+

−

− OA

b. Bond Premium: $300,000 x 1.5% = $4,500

Amortization of bond premium: $4,500 10 = $450 per year

Carrying Value, December 31, 2016:

Bonds Payable $300,000

EXERCISE 10-18B

Chen Company

General Journal

Date

Account Titles

Debit

Credit

2016

Jan. 1

Cash1

303,000

Premium on Bonds Payable

3,000

Bonds Payable

300,000

Dec. 31

Premium on Bonds Payable2

600

Interest Expense3

17,400

Cash4

18,000

2017

Dec. 31

Premium on Bonds Payable

600

Interest Expense

17,400

Cash

18,000

EXERCISE 10-19B

a.

Face Value

−

Bond Price

=

Discount

$250,000

−

$219,277

=

$30,723

b.

Carrying Value

x

Effective Rate

=

Interest Expense

$219,277

x

.10

=

$21,928

c. Compute the Ending Balance in the Discount Account

Face Value

x

Stated Rate

=

Cash Payment

$250,000

x

.08

=

$20,000

Interest Expense

−

Cash Payment

=

Amortization

$21,928

−

$20,000

=

$1,928

Beginning Discount

−

Amortization

=

Ending Discount

$30,723

−

$1,928

=

$28,795

Bond Carrying Value as of December 31, 2016

Bond Payable (Face Value)

$250,000

Discount on Bonds Payable

28,795

Carrying Value

$221,205

d.

Account Titles

Debit

Credit

Interest Expense

21,928

Bond Discount

1,928

Cash

20,000

EXERCISE 10-20B

a.

Date

Cash

Payment

Interest

Expense

Discount

Amortization

Carrying

Value

January 1, 2016

57,666

December 31, 2016

4,800

5,190*

390

58,056

December 31, 2017

4,800

5,225

425

58,481

December 31, 2018

4,800

5,263

463

58,944

December 31, 2019

4,800

5,305

505

59,449

December 31, 2020

4,800

5,351**

551**

60,000

Totals

24,000

26,334

2,334

Bond liability

$60,000

Less: Bond discount

1,519*

Carrying value

$58,481

*Total discount, $2,334

Amortized 2016 (390)

Amortized 2017 __(425)

Balance $1,519

c. The income statement would show $5,225 of interest expense.

d. The statement of cash flows would show a $4,800 cash outflow for

interest in the operating activities section.

EXERCISE 10-21B

a.

Bond Price

−

Face Value

=

Premium

$215,443

−

$200,000

=

$15,443

b.

Carrying Value

x

Effective Rate

=

Interest Expense

$215,443

x

.05

=

$10,772

c. Compute the Ending Balance in the Premium Account

Face Value

x

Stated Rate

=

Cash Payment

$200,000

x

.06

=

$12,000

Cash Payment

−

Interest Expense

=

Amortization

$12,000

−

$10,772

=

$1,228

Beginning Premium

−

Amortization

=

Ending Premium

$15,443

−

$1,228

=

$14,215

Bond Carrying Value as of December 31, 20163

Bond Payable (Face Value)

$200,000

Premium on Bonds Payable

14,215

Carrying Value

$214,215

d.

Account Titles

Debit

Credit

Interest Expense

10,772

Bond Premium

1,228

Cash

12,000

EXERCISE 10-22B

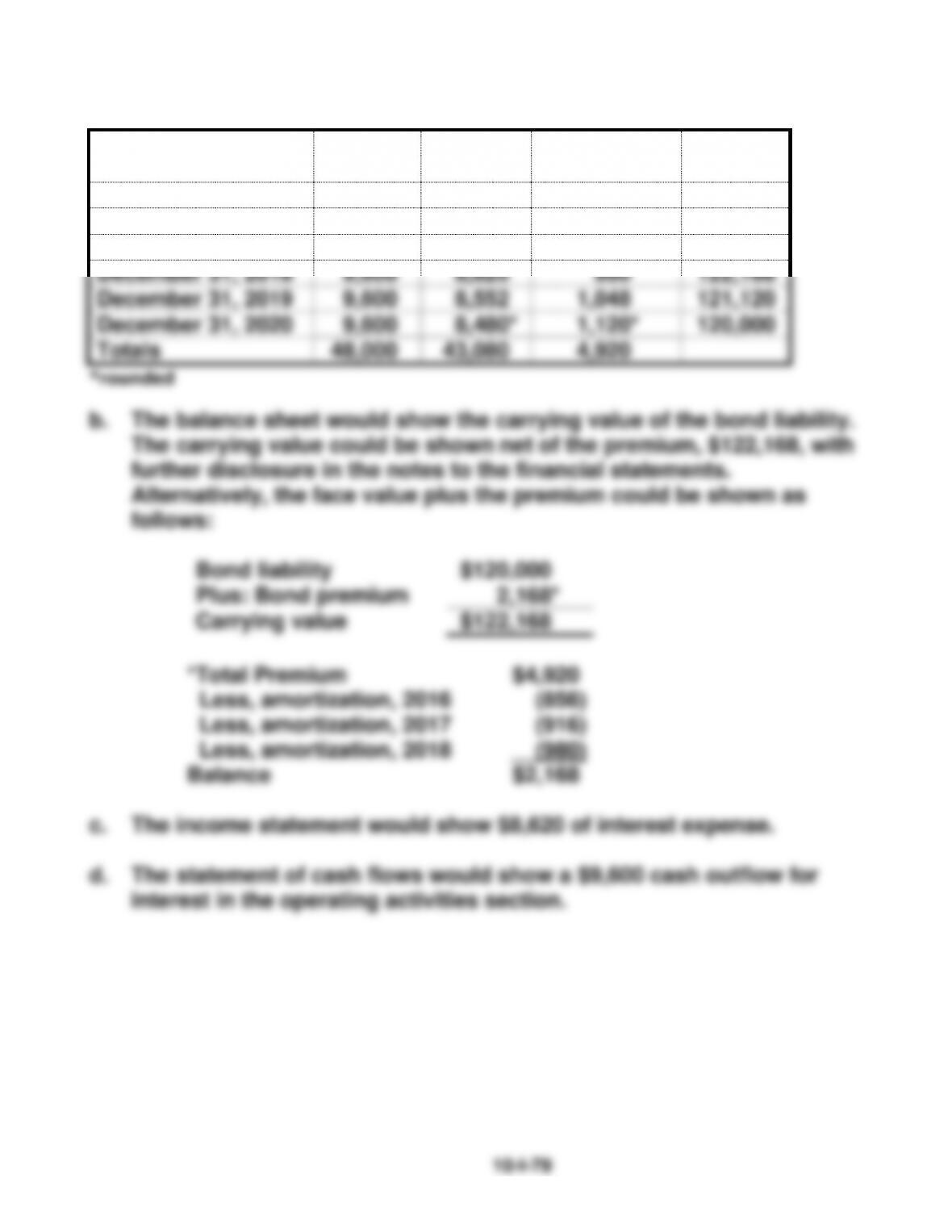

a.

Date

Cash

Payment

Interest

Expense

Premium

Amortization

Carrying

Value

January 1, 2016

124,920

December 31, 2016

9,600

8,744

856

124,064

December 31, 2017

9,600

8,684

916

123,148

December 31, 2018

9,600

8,620

980

122,168

December 31, 2019

9,600

8,552

1,048

121,120

December 31, 2020

9,600

8,480*

1,120*

120,000

Totals

48,000

43,080

4,920

*rounded

b. The balance sheet would show the carrying value of the bond liability.

The carrying value could be shown net of the premium, $122,168, with

further disclosure in the notes to the financial statements.

Alternatively, the face value plus the premium could be shown as

follows:

Bond liability

$120,000

Plus: Bond premium

2,168*

Carrying value

$122,168

*Total Premium $4,920

Less, amortization, 2016 (856)

Less, amortization, 2017 (916)

Less, amortization, 2018 __(980)

Balance $2,168

c. The income statement would show $8,620 of interest expense.

d. The statement of cash flows would show a $9,600 cash outflow for

interest in the operating activities section.

EXERCISE 10-23B

Since the stated rate of interest is lower than the effective interest rate the

bonds will sell at a discount. Because the effective interest rate method

EXERCISE 10-24B

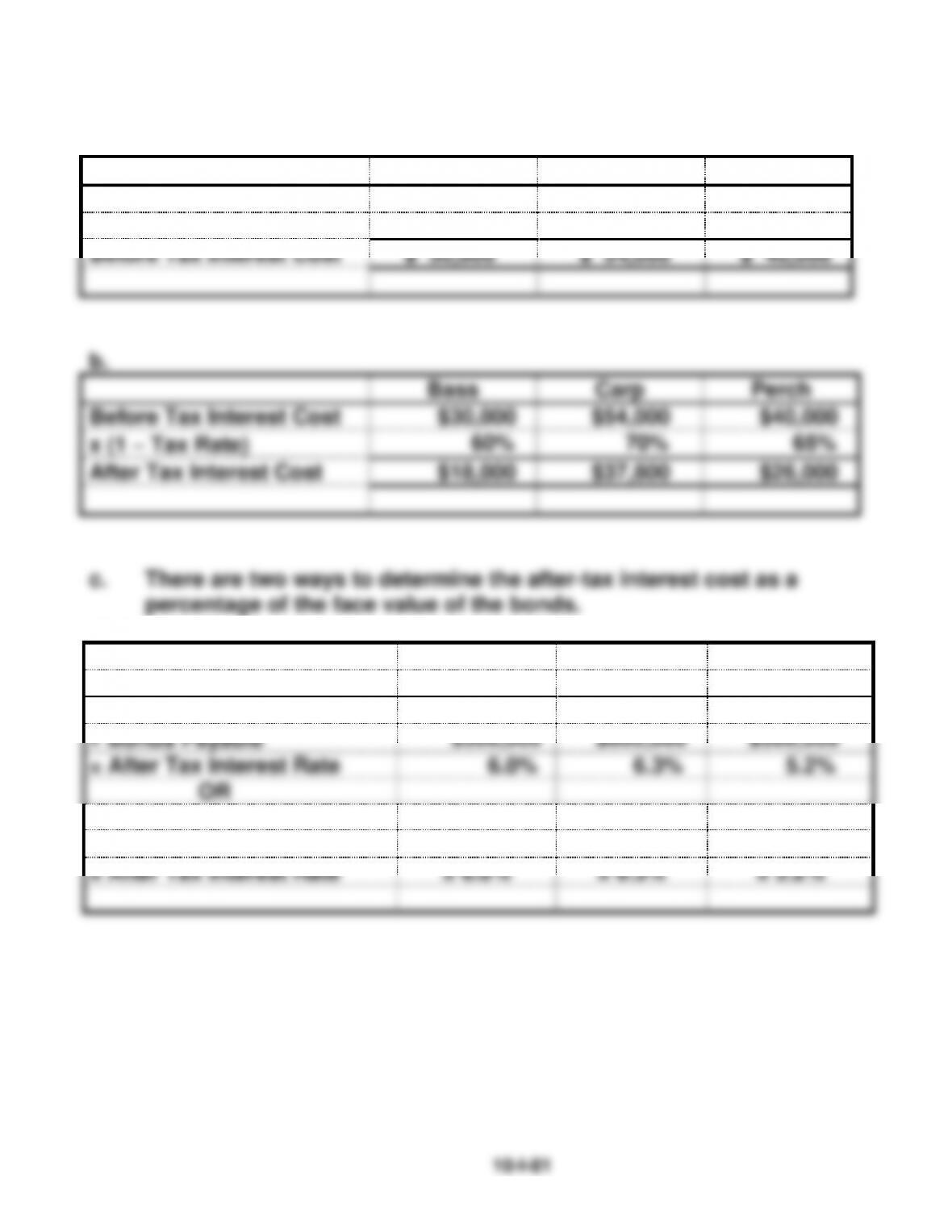

a.

Bass

Carp

Perch

Bonds Payable

$300,000

$600,000

$500,000

Interest Rate

10%

9%

8%

Before Tax Interest Cost

$ 30,000

$ 54,000

$ 40,000

b.

Bass

Carp

Perch

Before Tax Interest Cost

$30,000

$54,000

$40,000

x (1 − Tax Rate)

60%

70%

65%

After Tax Interest Cost

$18,000

$37,800

$26,000

1.

Bass

Carp

Perch

After Tax Interest Cost

$ 18,000

$ 37,800

$ 26,000

Bonds Payable

$300,000

$600,000

$500,000

= After Tax Interest Rate

6.0%

6.3%

5.2%

OR

2.

Interest Rate x (1 − Tax Rate)

.10 x ( 1−.4)

.09 x (1 − .3)

.08 x (1 − .35)

= After Tax Interest Rate

= 6.0%

= 6.3%

= 5.2%

EXERCISE 10-25B

a. Note to Instructor: Students may be able to solve this problem more

easily if they first prepare a table showing the balances in current

assets, total assets, current liabilities, and total liabilities for each

situation. Then, they can more easily compute the new ratios and

SOLUTIONS TO PROBLEMS – SERIES B – CHAPTER 10

PROBLEM 10-26B

a.

Kramer Co.

Amortization Schedule

$90,000, 3-Yr. Term Note, 7% Interest Rate

Year

Prin. Bal.

on Jan 1

Cash Pay.

Dec. 31

Applied to

Interest

Applied

to

Principal

Prin. Bal.

End of Period

2016

$90,000

$34,295

$6,300

$27,995

$62,005

2017

62,005

34,295

4,340

29,955

32,050

2018

32,050

34,295

2,245*

32,050

-0-

*rounded for final year

PROBLEM 10-26B (cont.)

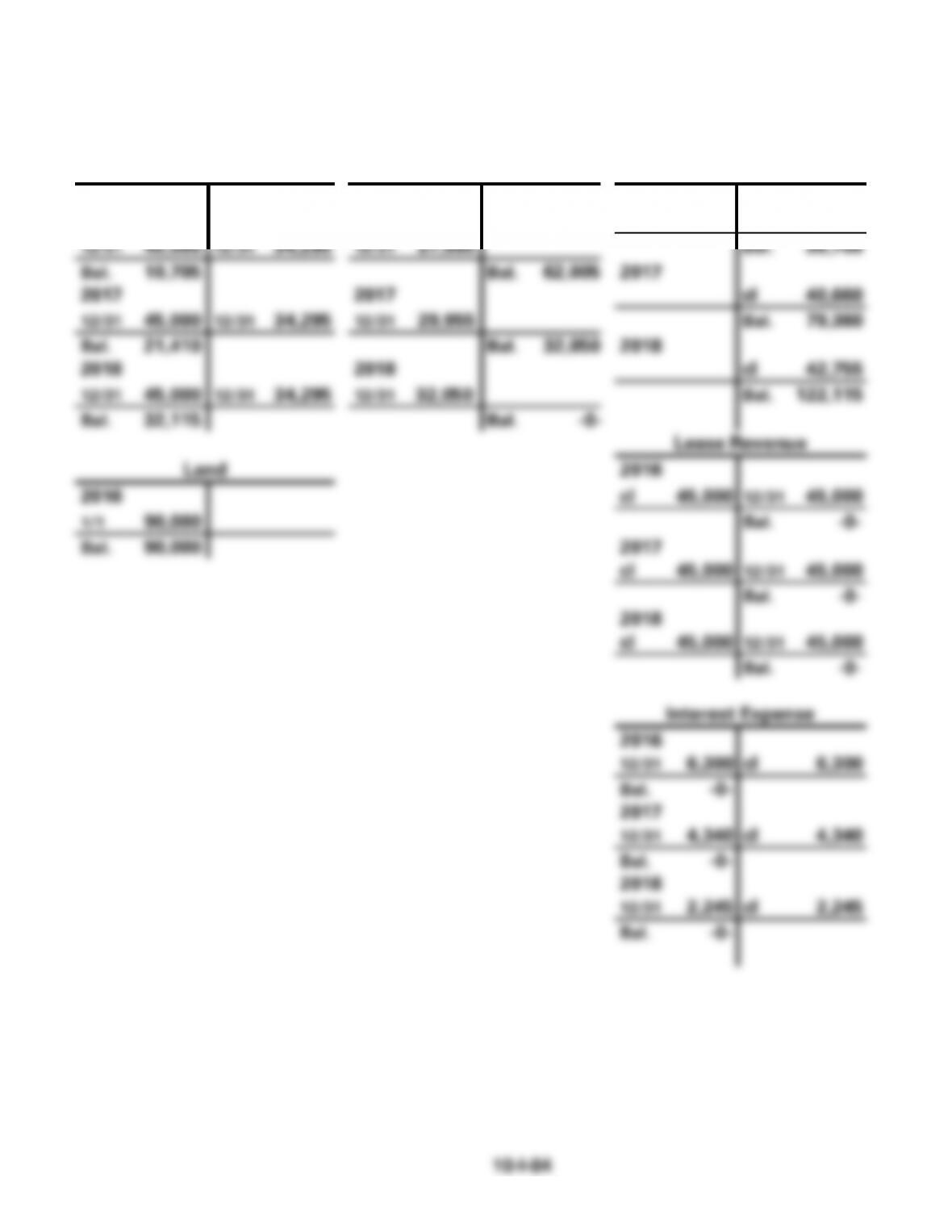

b. Provided for the use of the Instructor:

Cash

Notes Payable

Retained Earnings

2016

2016

2016

1/1 90,000

1/1 90,000

1/1 90,000

cl 38,700

12/31 45,000

12/31 34,295

12/31 27,995

Bal. 38,700

Bal. 10,705

Bal. 62,005

2017

2017

2017

cl 40,660

12/31 45,000

12/31 34,295

12/31 29,955

Bal. 79,360

Bal. 21,410

Bal. 32,050

2018

2018

2018

cl 42,755

12/31 45,000

12/31 34,295

12/31 32,050

Bal. 122,115

Bal. 32,115

Bal. -0-

Lease Revenue

Land

2016

2016

cl 45,000

12/31 45,000

1/1 90,000

Bal. -0-

Bal. 90,000

2017

cl 45,000

12/31 45,000

Bal. -0-

2018

cl 45,000

12/31 45,000

Bal. -0-

Interest Expense

2016

12/31 6,300

cl 6,300

Bal. -0-

2017

12/31 4,340

cl 4,340

Bal. -0-

2018

12/31 2,245

cl 2,245

Bal. -0-

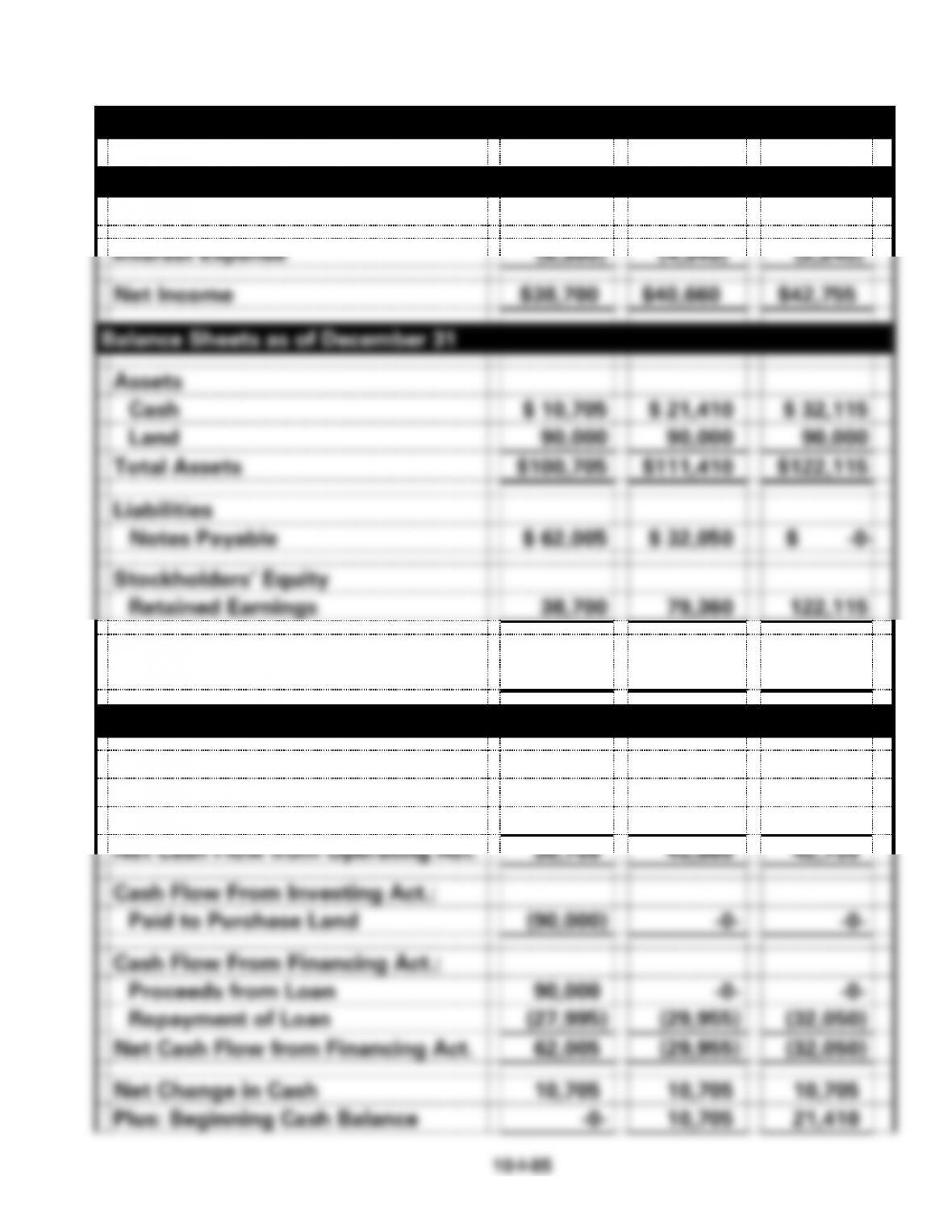

PROBLEM 10-26B b. (cont.)

Kramer Co.

Financial Statements

2016

2017

2018

Income Statements for the Year Ended December 31

Lease Revenue

$45,000

$45,000

$45,000

Interest Expense

(6,300)

(4,340)

(2,245)

Net Income

$38,700

$40,660

$42,755

Balance Sheets as of December 31

Assets

Cash

$ 10,705

$ 21,410

$ 32,115

Land

90,000

90,000

90,000

Total Assets

$100,705

$111,410

$122,115

Liabilities

Notes Payable

$ 62,005

$ 32,050

$ -0-

Stockholders’ Equity

Retained Earnings

38,700

79,360

122,115

Total Liab. and Stockholders’

Equity

$100,705

$111,410

$122,115

Statements of Cash Flows for the Year Ended December 31

Cash Flows From Operating Act.:

Receipts from Rental

$45,000

$45,000

$45,000

Paid for Interest

(6,300)

(4,340)

(2,245)

Net Cash Flow from Operating Act.

38,700

40,660

42,755

Cash Flow From Investing Act.:

Paid to Purchase Land

(90,000)

-0-

-0-

Cash Flow From Financing Act.:

Proceeds from Loan

90,000

-0-

-0-

Repayment of Loan

(27,995)

(29,955)

(32,050)

Net Cash Flow from Financing Act.

62,005

(29,955)

(32,050)

Net Change in Cash

10,705

10,705

10,705

Plus: Beginning Cash Balance

-0-

10,705

21,410

Ending Cash Balance

$10,705

$21,410

$32,115

PROBLEM 10-26B (cont.)

c. Because the company is making both principal and interest

payments on the loan each year, the amount paid on the principal

PROBLEM 10-27B

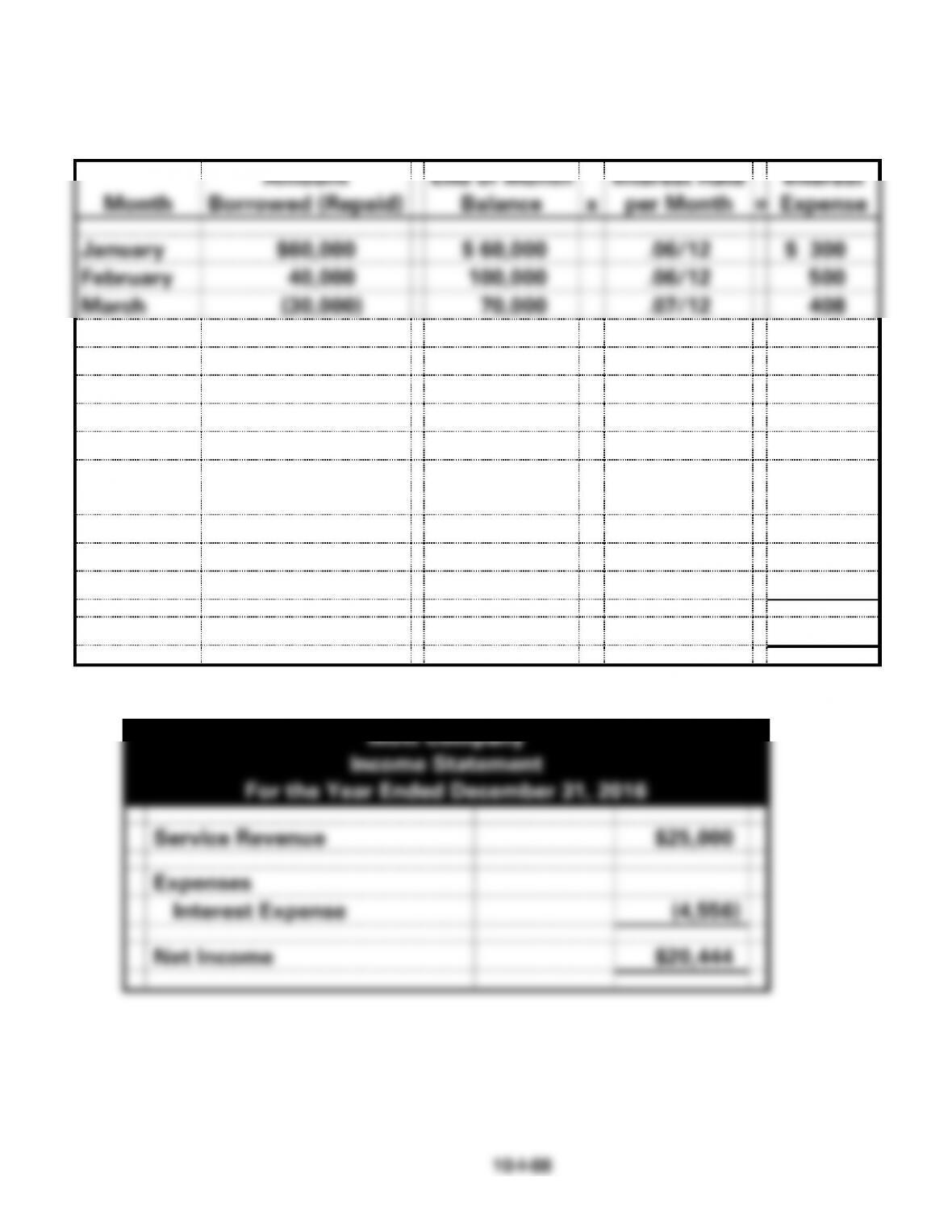

Computation of Interest Expense

Month

Amount

Borrowed (Repaid)

End of Month

Balance

x

Interest Rate

per Month

=

Interest

Expense

January

$60,000

$ 60,000

.06/12

$ 300

February

40,000

100,000

.06/12

500

March

(30,000)

70,000

.07/12

408

April

-0-

70,000

.07/12

408

May

-0-

70,000

.07/12

408

June

-0-

70,000

.07/12

408

July

-0-

70,000

.07/12

408

August

-0-

70,000

.07/12

408

Septembe

r

-0-

70,000

.07/12

408

October

-0-

70,000

.07/12

408

November

(20,000)

50,000

.07/12

292

December

(10,000)

40,000

.06/12

200

Total

$4,556

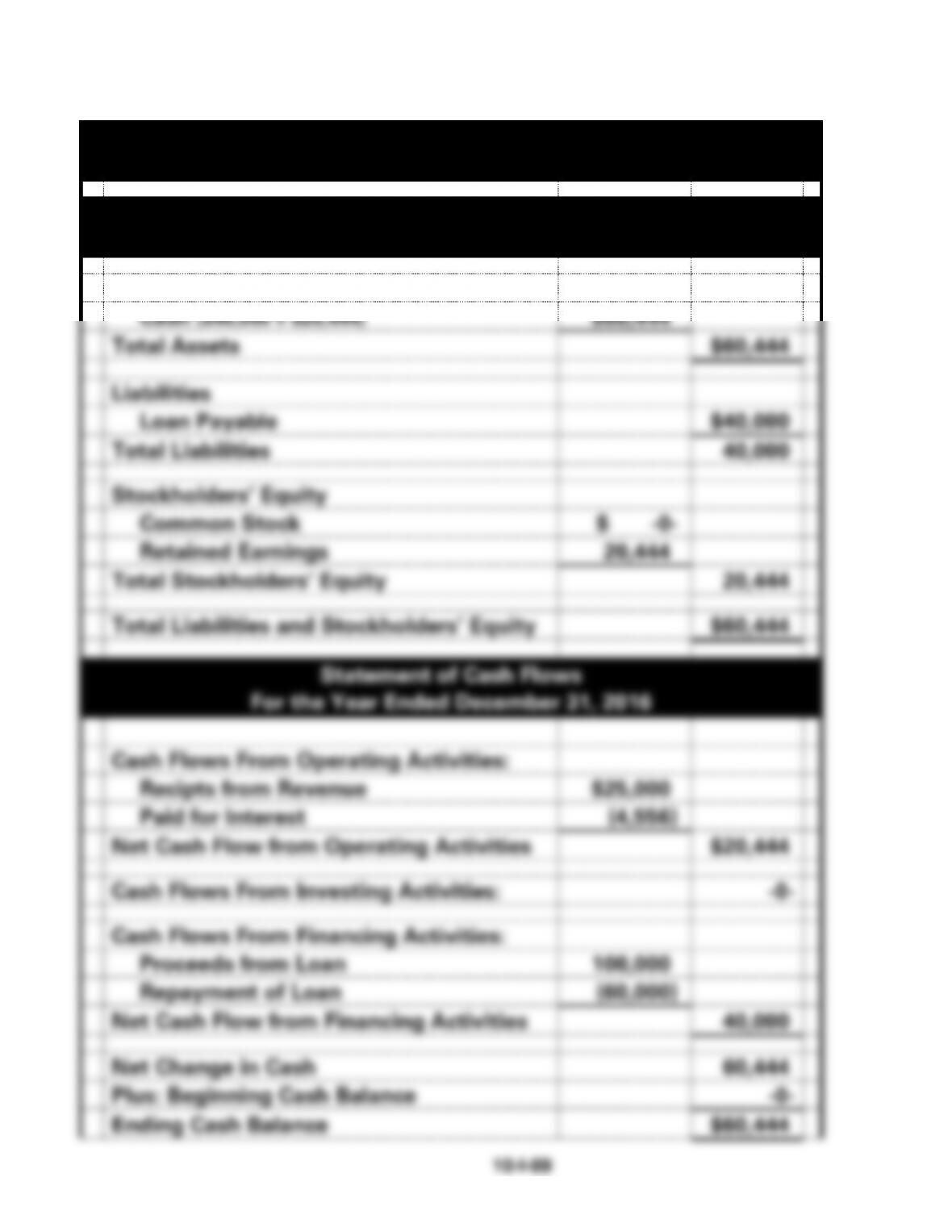

a.

Mott Company

Income Statement

For the Year Ended December 31, 2016

Service Revenue

$25,000

Expenses

Interest Expense

(4,556)

Net Income

$20,444

PROBLEM 10-27B a. (cont.)

Mott Company

Financial Statements

Balance Sheet

As of December 31, 2016

Assets

Cash ($40,000 + $20,444)

$60,444

Total Assets

$60,444

Liabilities

Loan Payable

$40,000

Total Liabilities

40,000

Stockholders’ Equity

Common Stock

$ -0-

Retained Earnings

20,444

Total Stockholders’ Equity

20,444

Total Liabilities and Stockholders’ Equity

$60,444

Statement of Cash Flows

For the Year Ended December 31, 2016

Cash Flows From Operating Activities:

Recipts from Revenue

$25,000

Paid for Interest

(4,556)

Net Cash Flow from Operating Activities

$20,444

Cash Flows From Investing Activities:

-0-

Cash Flows From Financing Activities:

Proceeds from Loan

100,000

Repayment of Loan

(60,000)

Net Cash Flow from Financing Activities

40,000

Net Change in Cash

60,444

Plus: Beginning Cash Balance

-0-

Ending Cash Balance

$60,444

PROBLEM 10-27B (cont.)

PROBLEM 10-28B

a.

Effect of Transactions on Financial Statements

No

.

Assets

=

Liab.

+

S.

Equity

Rev.

Gain

−

Exp./

Loss

=

Net Inc.

Cash Flow

1

250,000

=

250,000

+

NA

NA

−

NA

=

NA

250,000 FA

2.

(15,000)

=

NA

+

(15,000)

NA

−

15,000

=

(15,000)

(15,000) OA

3.

(253,750)

=

(250,000)

+

(3,750)

NA

−

3,750

=

(3,750)

(253,750) FA

b.

Date

Account Titles

Debit

Credit

1.

Cash

250,000

Bonds Payable

250,000

2.

Interest Expense1

15,000

Cash

15,000

3.

Bonds Payable

250,000

Loss on Redemption of Bonds

3,750

Cash2

253,750