3-1–25

ATC 3-3

a.

The fiscal year-ends should be matched to the companies as follows:

February 2, is the closing date for Michaels. By January 31, the Christmas

rush is over.

July 31, is the closing date for Vail Resorts, Inc. Clearly, a ski resort company would

not want to close its books on December 31. Thus, before the ski season gets

3-1–26

ATC 3-3 (cont.)

b. Assuming a company chooses the slowest time of its year to close its

books, its balance sheet may not represent the remainder of its fiscal

year for the following reasons.

3-2–27

ATC 3-4

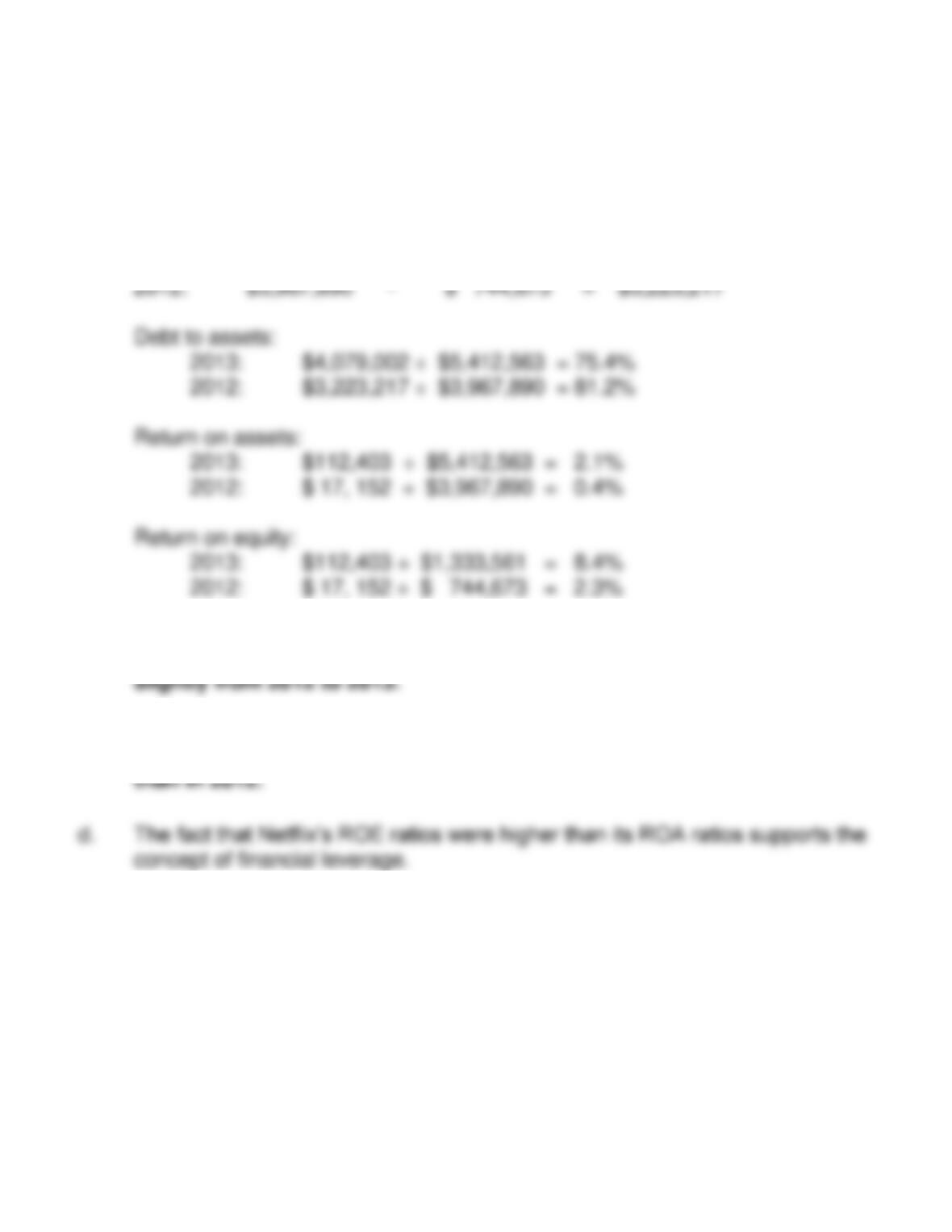

a. First compute Netflix’s liabilities:

Stockholders’

Assets – Equity = Liabilities

2013: $5,412,563 – $1,333,561 = $4,079,002

1. b. Based on the debt to assets ratio Netflix’s financial risk decreased

2. c. Based on the ROA ratio Netflix managed its assets better in 2013

3-6–28

3. ATC 3-5

a. Debt to assets:

Biogen: $ 3,242 ÷ $11,863 = 27.3%

4. b. Based on the debt to assets ratio Amgen has the highest level of

5. c. Based on the ROA ratio Biogen managed its assets better than

Amgen.

6. d. Based on the ROE ratio Amgen’s owners received a slightly better

3-6–29

ATC 3-6

The following information should be contained in the memo:

a.

Present Return on Assets:

$425,000 $3,500,000 = 12.1%

If the asset is sold for $1,500,000:

ATC 3-7

a. This answer represents one acceptable solution out of many possible alternatives.

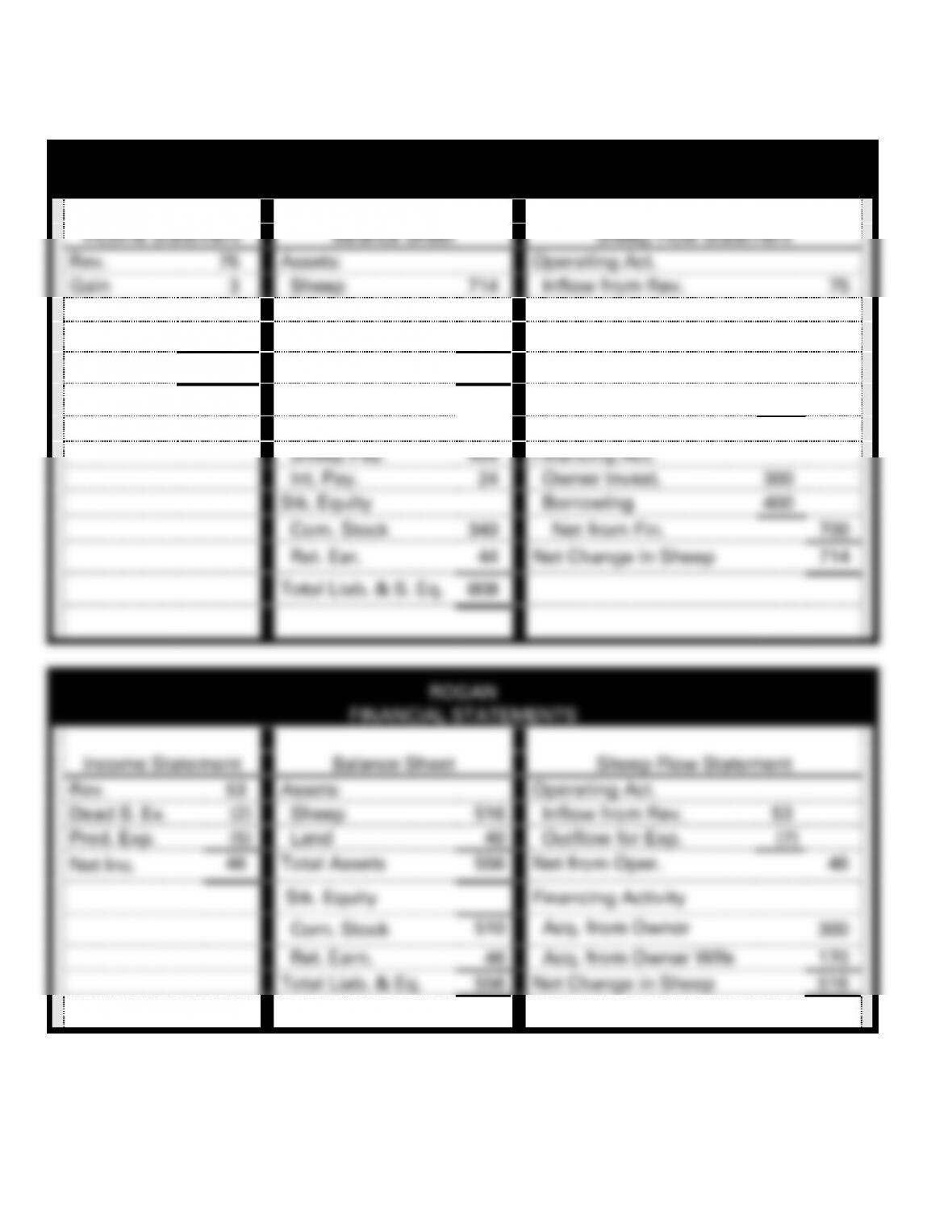

Eight identifiable events for Argon and seven for Rogan are shown below under

accounting equations. The financial statements on the following pages are drawn

3-6–31

ATC 3-7 a. (cont)

ARGON

FINANCIAL STATEMENTS

Income Statement

Balance Sheet

Sheep Flow Statement

Rev.

75

Assets:

Operating Act.

Gain

3

Sheep

714

Inflow from Rev.

75

Int. Exp.

(24)

Fence

40

Investing Act.

Fence Exp.

(10)

Land

54

Purchased Land

(20)

Net Inc.

44

Total Assets

808

Built Fence

(50)

Sold Land

9

Liabilities

Net from Inv.

(61)

Sheep Pay.

400

Financing Act.

Int. Pay.

24

Owner Invest.

300

Stk. Equity

Borrowing

400

Com. Stock

340

Net from Fin.

700

Ret. Ear.

44

Net Change in Sheep

714

Total Liab. & S. Eq.

808

ROGAN

FINANCIAL STATEMENTS

Income Statement

Balance Sheet

Sheep Flow Statement

Rev.

53

Assets:

Operating Act.

Dead S. Ex.

(2)

Sheep

516

Inflow from Rev.

53

Pred. Exp.

(5)

Land

40

Outflow for Exp.

(7)

Net Inc.

46

Total Assets

556

Net from Oper.

46

Stk. Equity

Financing Activity

Com. Stock

510

Acq. from Owner

300

Ret. Earn.

46

Acq. from Owner Wife

170

Total Liab. & Eq.

556

Net Change in Sheep

516

3-6–32

ATC 3-7 (cont.)

1. Rogan’s equity is larger with a total of 556 compared to Argon’s total of

384.

2. Rogan produced the larger amount of net income with a total of 46

3. Based on conventional accounting standards Rogan would be assigned

heir to the family fortune.

c. Argon has seven more acres of land than Rogan (27 v. 20). Remember that

Argon purchased an additional ten acres and sold three of them. Since the

land has increased in value by one sheep per acre, the gain on Argon’s

3-6–33

ATC 3-7 (cont.)

e. Rogan lost approximately 1% of his herd to predators (i.e., 5 516). Applying

this percentage to Argon’s herd suggests that he saved approximately 7 sheep

(i.e. 714 x .01) by building the fence. Since the fence cost approximately 10

sheep per year of useful life (i.e. 50 5) the decision to build the fence appears

debt of 424 sheep. Rogan would lose 258 sheep (i.e., 516 2). However, since

he has no debt, he would also retain an equity base of 258 sheep. Accordingly,

Argon would be bankrupt but Rogan would still be in business. Financial risk is

shown in financial statements by reporting the amount of liabilities that

companies have incurred. The level of this risk can be measured with a debt-

3-6–34

ATC 3-8

This solution is based on Nike’s May 31, 2013 Form 10-K. Dollar amounts are

(1)Liabilities must be computed:

Assets − Shareholders’ Equity = Liabilities

3-6–35

SOLUTION TO COMPREHENSIVE PROBLEM – CHAPTER 3

a.

Pacilio Security Services, Inc.

General Journal, 2013

Event

Account title

Debit

Credit

1.

Salaries Payable

1,200

Cash

1,200

2.

Notes Payable

2,000

Cash

2,000

3.

Cash

11,000

Accounts Receivable

21,000

Security Service Revenue

32,000

4.

Prepaid Rent

3,000

Cash

3,000

5.

Supplies

700

Accounts Payable

700

6.

Salaries Expense

9,000

Cash

9,000

7.

Other Operating Expense

4,200

Accounts Payable

4,200

8.

Cash

1,200

Unearned Revenue

1,200

9.

Cash

19,000

Accounts Receivable

19,000

10.

Accounts Payable

5,950

Cash

5,950

11.

Advertising Expense

1,800

Cash

1,800

12.

Dividends

4,650

Cash

4,650

3-6–36

3-6–37

COMPREHENSIVE PROBLEM – CHAPTER 3 a. (cont.)

Pacilio Security Services, Inc.

General Journal, 2013

Event

Account title

Debit

Credit

13.

No Entry

14.

Supplies Expense ($65 + $700 − $120)

645

Supplies

645

15.

Rent Expense1

2,800

Prepaid Rent

2,800

16.

Unearned Revenue2

500

Security Services Revenue

500

17.

Salaries Expense

1,000

Salaries Payable

1,000

3-6–38

COMPREHENSIVE PROBLEM – CHAPTER 3 (cont.)

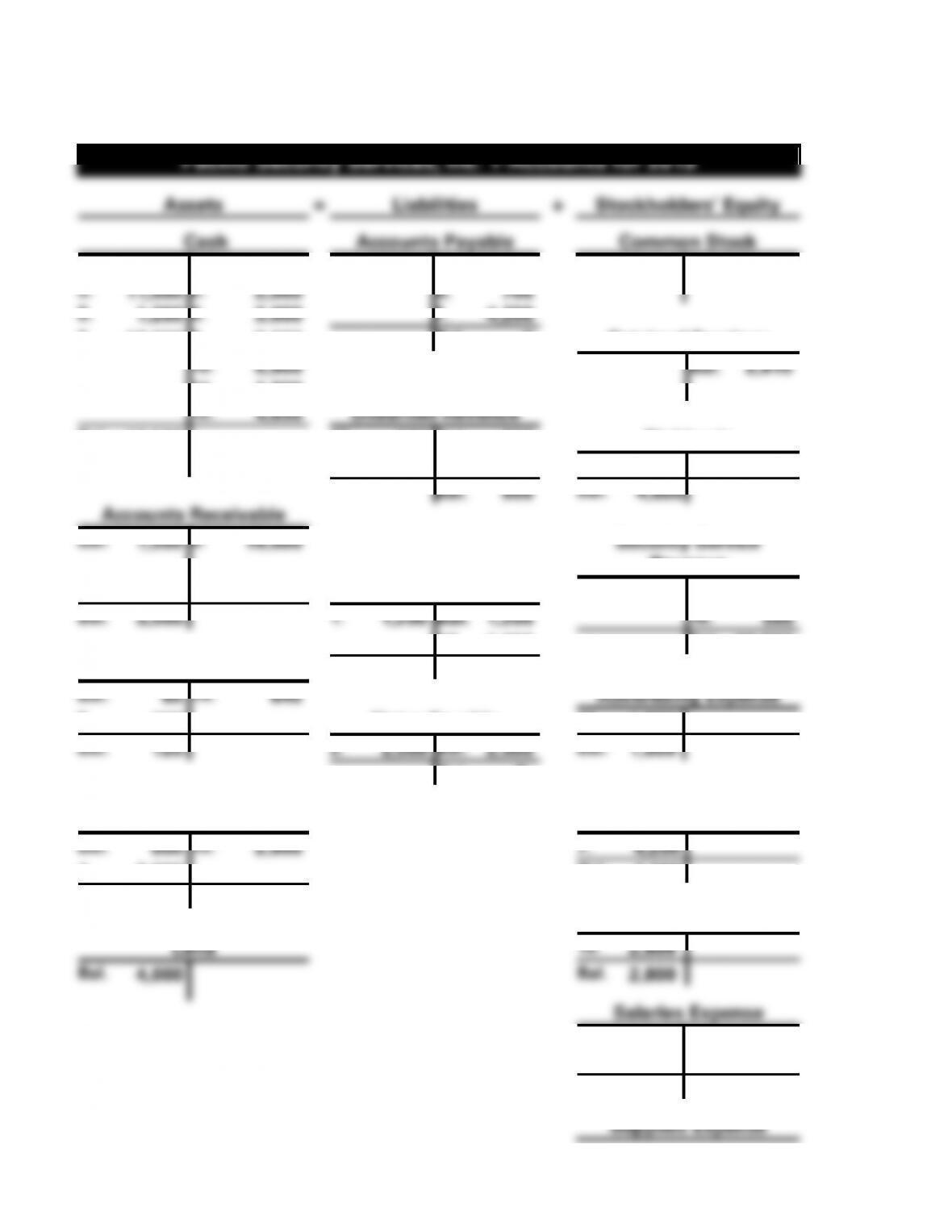

b.

Pacilio Security Services, Inc. T-Accounts for 2013

Assets

=

Liabilities

+

Stockholders’ Equity

Cash

Accounts Payable

Common Stock

Bal.

8,900

1.

1,200

10.

5,950

Bal.

1,050

Bal.

8,000

3.

11,000

2.

2,000

5.

700

8.

1,200

4.

3,000

7.

4,200

9.

19,000

6.

9,000

Bal.

-0-

Retained Earnings

10.

5,950

Bal.

2,815

11.

1,800

12.

4,650

Unearned Revenue

Bal.

12,500

16.

500

Bal.

200

Dividends

8.

1,200

12.

4,650

Bal.

900

Bal.

4,650

Accounts Receivable

Bal.

1,500

9.

19,000

Security Service

Revenue

3.

21,000

Salaries Payable

3.

32,000

Bal.

3,500

1.

1,200

Bal.

1,200

16.

500

17.

1,000

Bal.

32,500

Supplies

Bal.

1,000

Bal.

65

14.

645

Advertising Expense

5.

700

Notes Payable

11.

1,800

Bal.

120

2.

2,000

Bal.

2,000

Bal.

1,800

Bal.

-0-

Prepaid Rent

Other Operating

Expense

Bal.

800

15.

2,800

7.

4,200

4.

3,000

Bal.

4,200

Bal.

1,000

Rent Expense

Land

15.

2,800

Bal.

4,000

Bal.

2,800

Salaries Expense

6.

9,000

17.

1,000

Bal.

10,000

Supplies Expense

3-6–39

14.

645

Bal.

645

3-6–40

COMPREHENSIVE PROBLEM – CHAPTER 3 (cont.)

c.

Pacilio Security Services, Inc.

Trial Balance

December 31, 2013

Cash

$ 12,500

Accounts Receivable

3,500

Supplies

120

Prepaid Rent

1,000

Land

4,000

Unearned Revenue

$ 900

Salaries Payable

1,000

Common Stock

8,000

Retained Earnings

2,815

Dividends

4,650

Security Service Revenue

32,500

Advertising Expense

1,800

Other Operating Expense

4,200

Rent Expense

2,800

Salaries Expense

10,000

Supplies Expense

645

Totals

$45,215

$45,215

3-6–41

COMPREHENSIVE PROBLEM – CHAPTER 3 (cont.)

d.

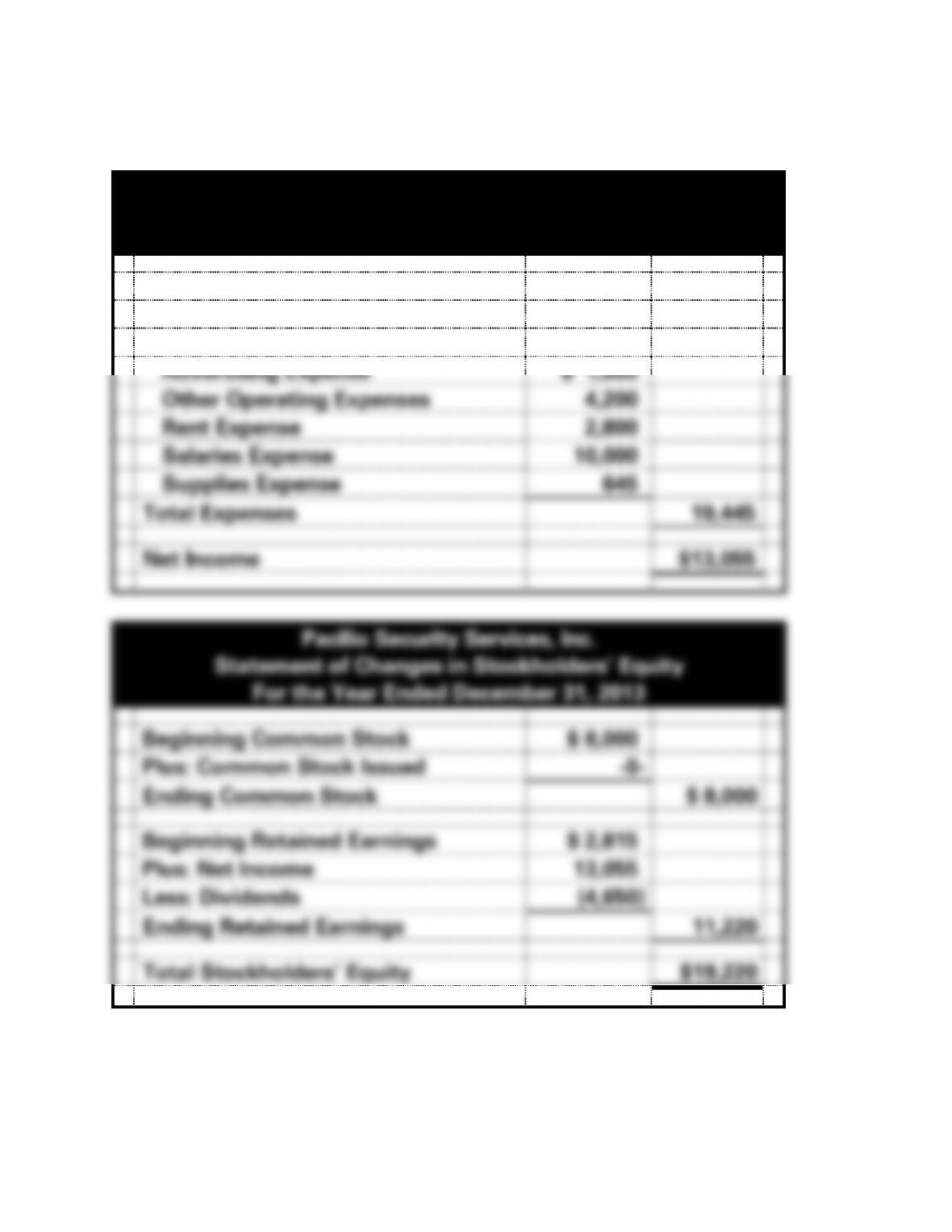

Pacilio Security Services, Inc.

Income Statement

For the Year Ended December 31, 2013

Service Revenue

$32,500

Expenses

Advertising Expense

$ 1,800

Other Operating Expenses

4,200

Rent Expense

2,800

Salaries Expense

10,000

Supplies Expense

645

Total Expenses

19,445

Net Income

$13,055

Pacilio Security Services, Inc.

Statement of Changes in Stockholders’ Equity

For the Year Ended December 31, 2013

Beginning Common Stock

$ 8,000

Plus: Common Stock Issued

-0-

Ending Common Stock

$ 8,000

Beginning Retained Earnings

$ 2,815

Plus: Net Income

13,055

Less: Dividends

(4,650)

Ending Retained Earnings

11,220

Total Stockholders’ Equity

$19,220

3-6–42

COMPREHENSIVE PROBLEM – CHAPTER 3 d. (cont.)

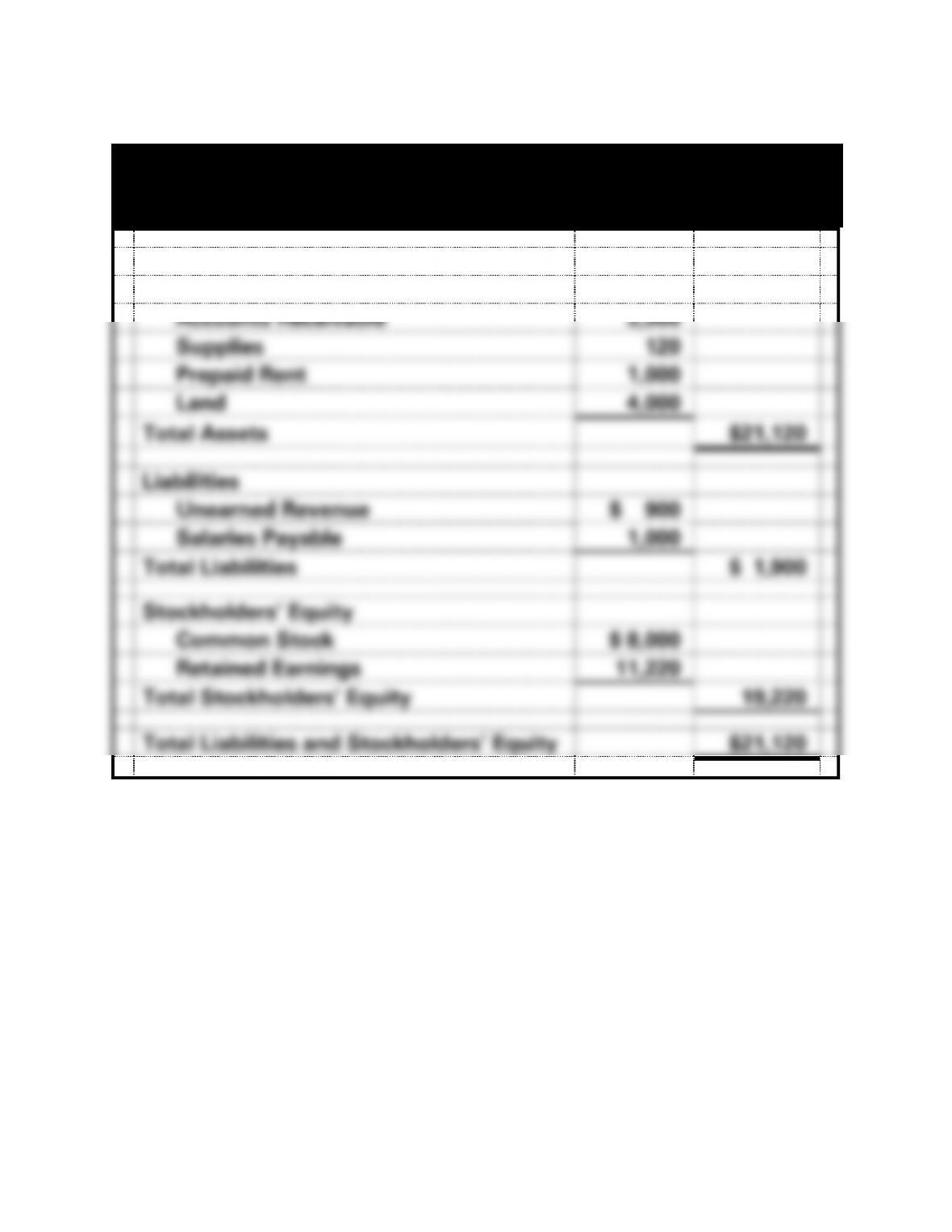

Pacilio Security Services, Inc.

Balance Sheet

As of December 31, 2013

Assets

Cash

$12,500

Accounts Receivable

3,500

Supplies

120

Prepaid Rent

1,000

Land

4,000

Total Assets

$21,120

Liabilities

Unearned Revenue

$ 900

Salaries Payable

1,000

Total Liabilities

$ 1,900

Stockholders’ Equity

Common Stock

$ 8,000

Retained Earnings

11,220

Total Stockholders’ Equity

19,220

Total Liabilities and Stockholders’ Equity

$21,120

3-6–43

COMPREHENSIVE PROBLEM – CHAPTER 3 d. (cont.)

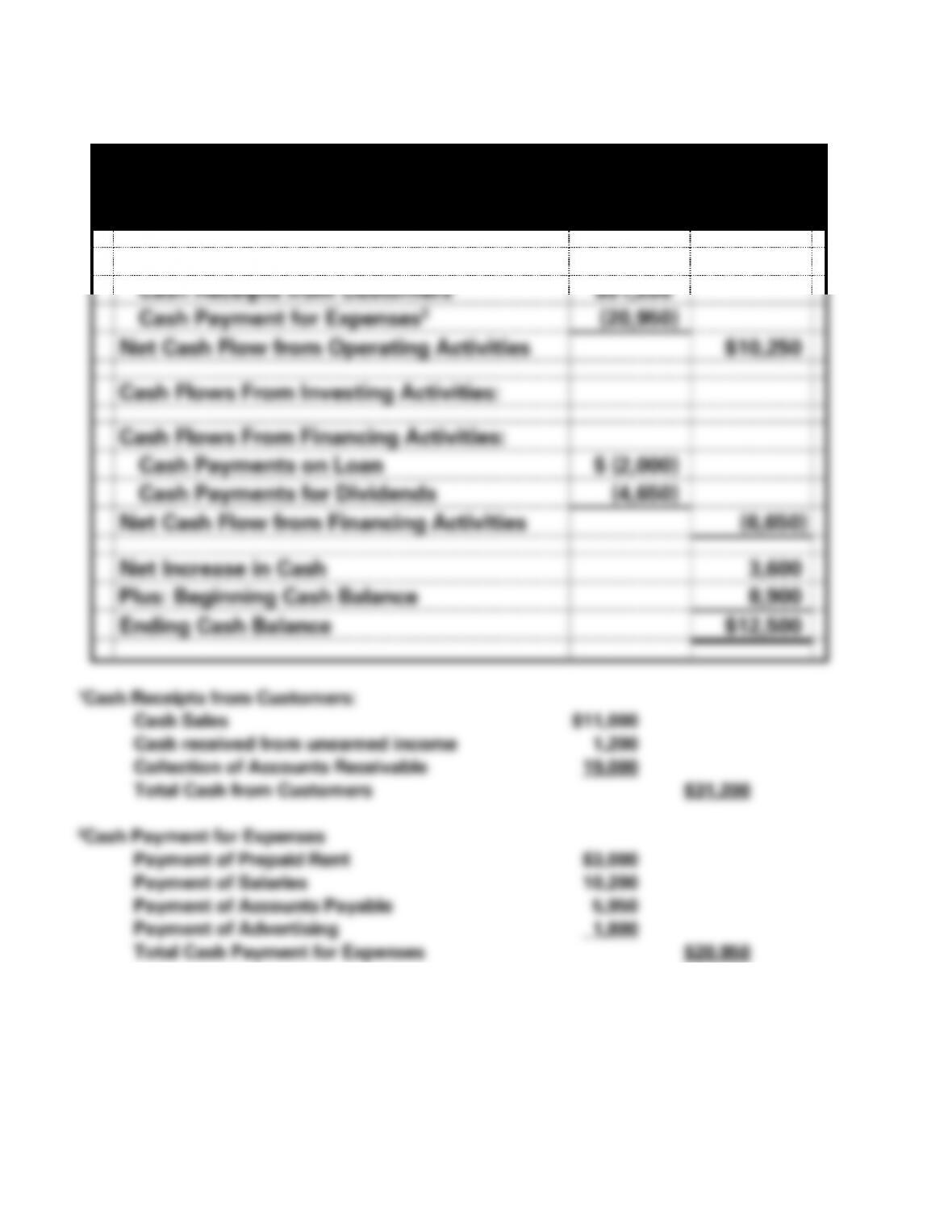

Pacilio Security Services, Inc.

Statement of Cash Flows

For the Year Ended December 31, 2013

Cash Flows From Operating Activities:

Cash Receipts from Customers1

$31,200

Cash Payment for Expenses2

(20,950)

Net Cash Flow from Operating Activities

$10,250

Cash Flows From Investing Activities:

Cash Flows From Financing Activities:

Cash Payments on Loan

$ (2,000)

Cash Payments for Dividends

(4,650)

Net Cash Flow from Financing Activities

(6,650)

Net Increase in Cash

3,600

Plus: Beginning Cash Balance

8,900

Ending Cash Balance

$12,500

3-6–44

COMPREHENSIVE PROBLEM – CHAPTER 3 (cont.)

e.

Date

Account Titles

Debit

Credit

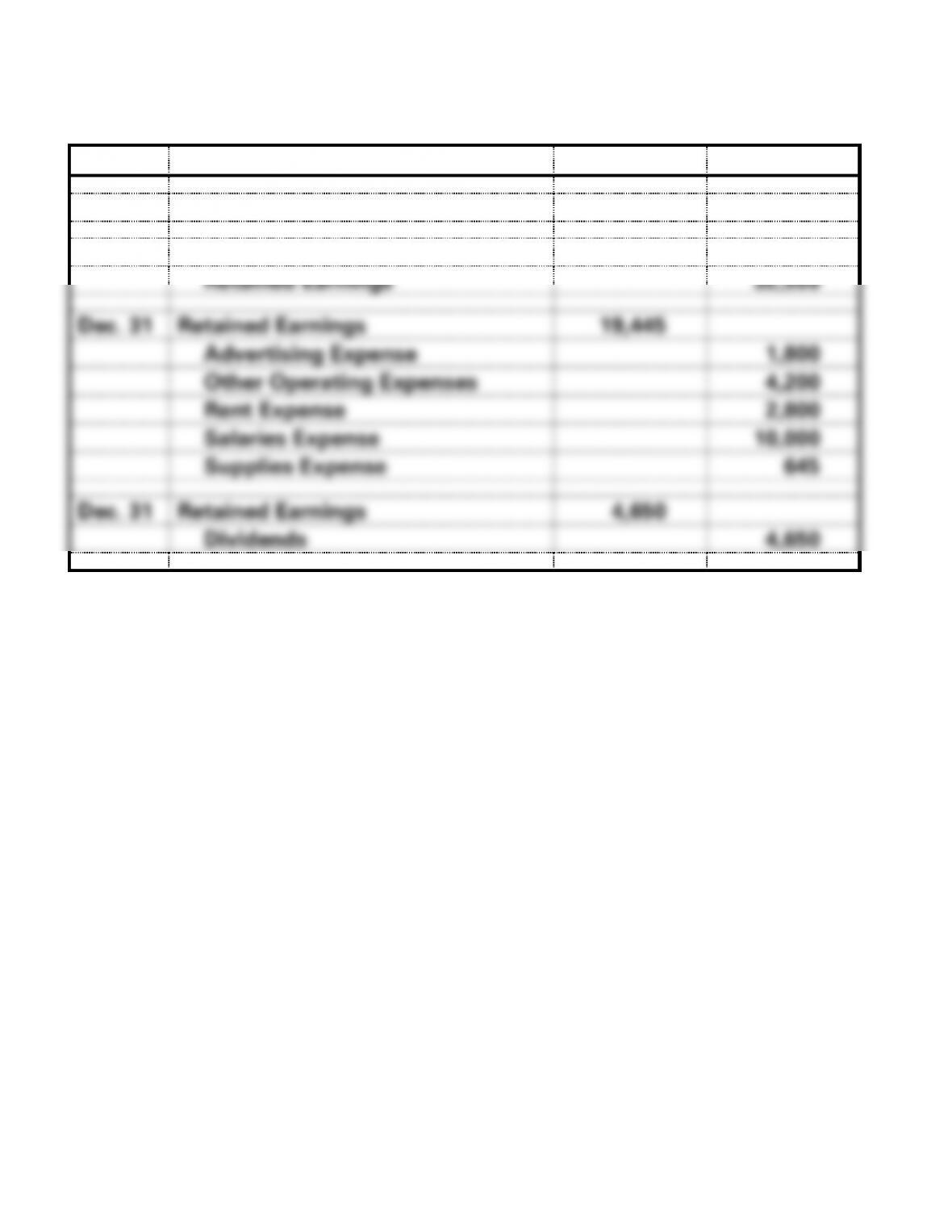

Closing Entries

Dec. 31

Security Service Revenue

32,500

Retained Earnings

32,500

Dec. 31

Retained Earnings

19,445

Advertising Expense

1,800

Other Operating Expenses

4,200

Rent Expense

2,800

Salaries Expense

10,000

Supplies Expense

645

Dec. 31

Retained Earnings

4,650

Dividends

4,650