Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

4-61

EXERCISE 4-22A (cont.) (Appendix)

b.

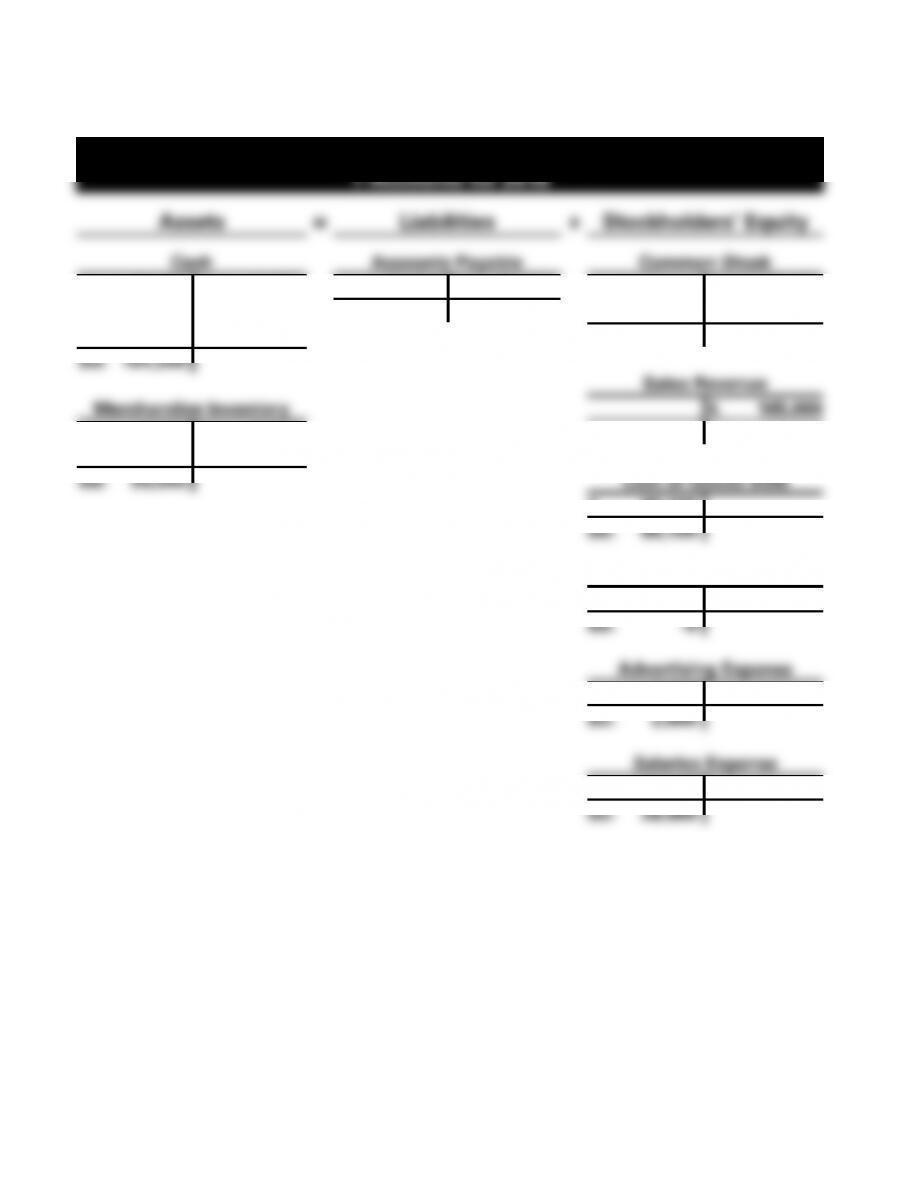

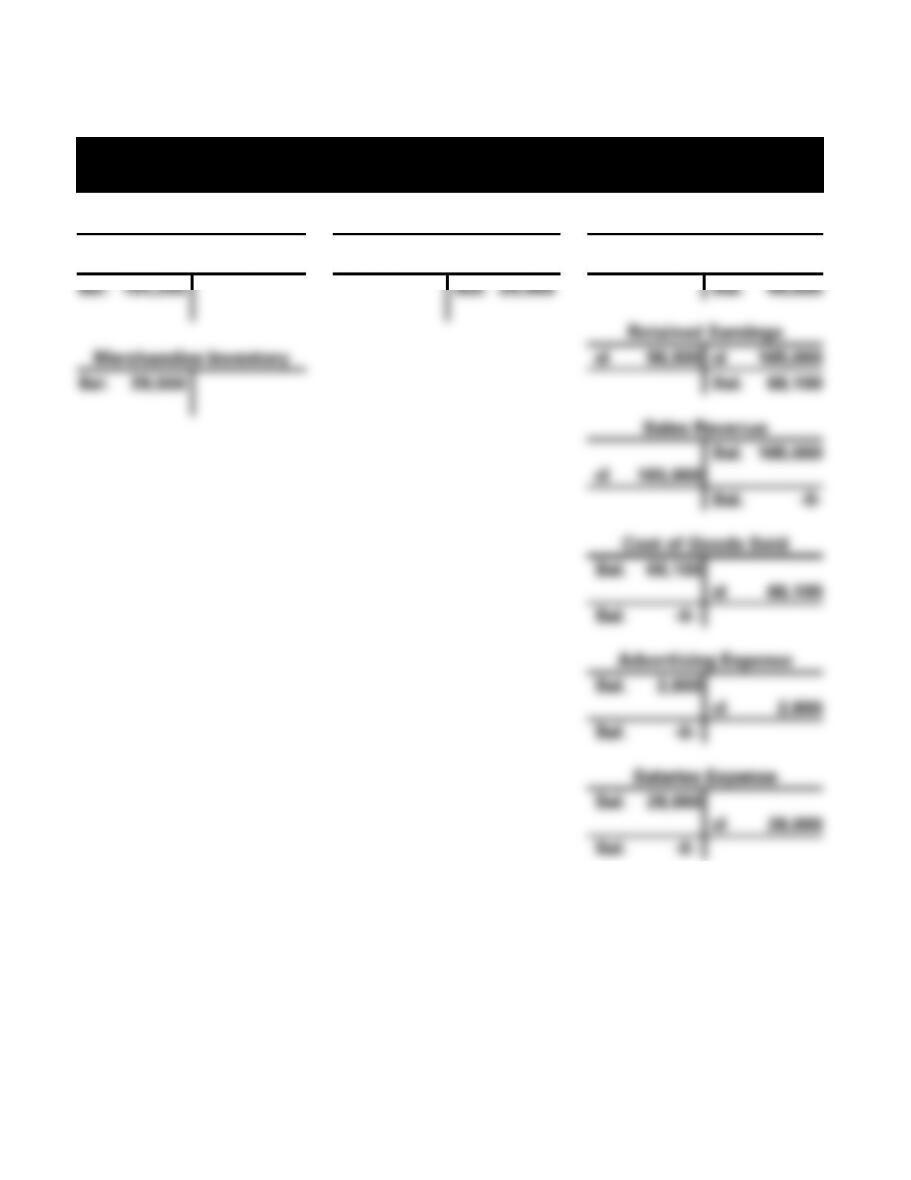

Bob’s Bike Shop

T-Accounts for 2016

Assets

=

Liabilities

+

Stockholders’ Equity

Cash

Accounts Payable

Common Stock

1. 35,000

4. 2,800

7. 65,000

3. 85,000

1. 35,000

5. 165,000

6. 28,000

Bal. 20,000

2. 9,600

7. 65,000

Bal. 44,600

Bal. 104,200

Sales Revenue

Merchandise Inventory

5. 165,000

2. 9,600

8. 9,600

Bal. 165,000

8. 28,500

Bal. 28,500

Cost of Goods Sold

8. 66,100

Bal. 66,100

Purchases

3. 85,000

8. 85,000

Bal. -0-

Advertising Expense

4. 2,800

Bal. 2,800

Salaries Expense

6. 28,000

Bal. 28,000

4-62

EXERCISE 4-22A (cont.) (Appendix)

c.

Bob’s Bike Shop

Financial Statements

For the Year Ended December 31, 2016

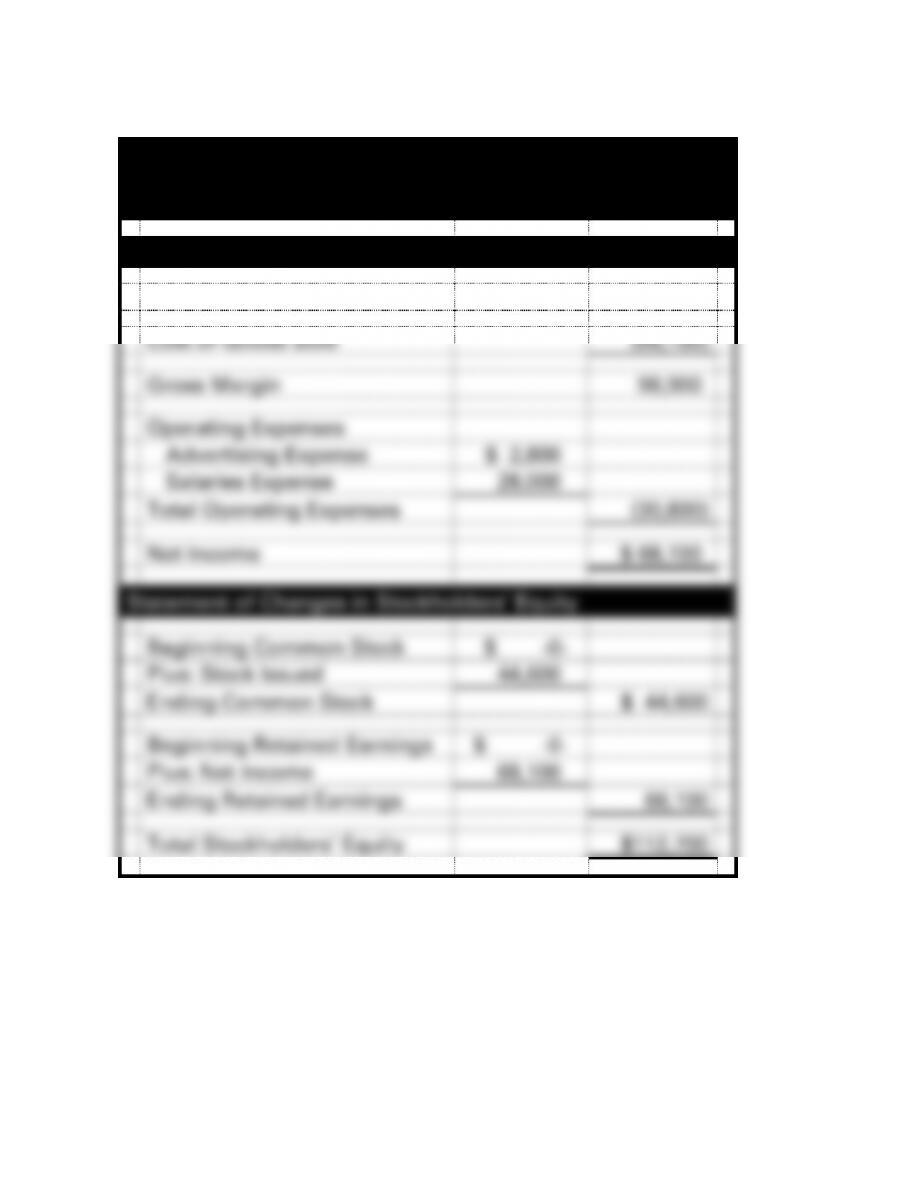

Income Statement

Net Sales

$165,000

Cost of Goods Sold

(66,100)

Gross Margin

98,900

Operating Expenses

Advertising Expense

$ 2,800

Salaries Expense

28,000

Total Operating Expenses

(30,800)

Net Income

$ 68,100

Statement of Changes in Stockholders’ Equity

Beginning Common Stock

$ -0-

Plus: Stock Issued

44,600

Ending Common Stock

$ 44,600

Beginning Retained Earnings

$ -0-

Plus: Net Income

68,100

Ending Retained Earnings

68,100

Total Stockholders’ Equity

$112,700

4-63

EXERCISE 4-22A c. (cont.) (Appendix)

Bob’s Bike Shop

Financial Statements

Balance Sheet

As of December 31, 2016

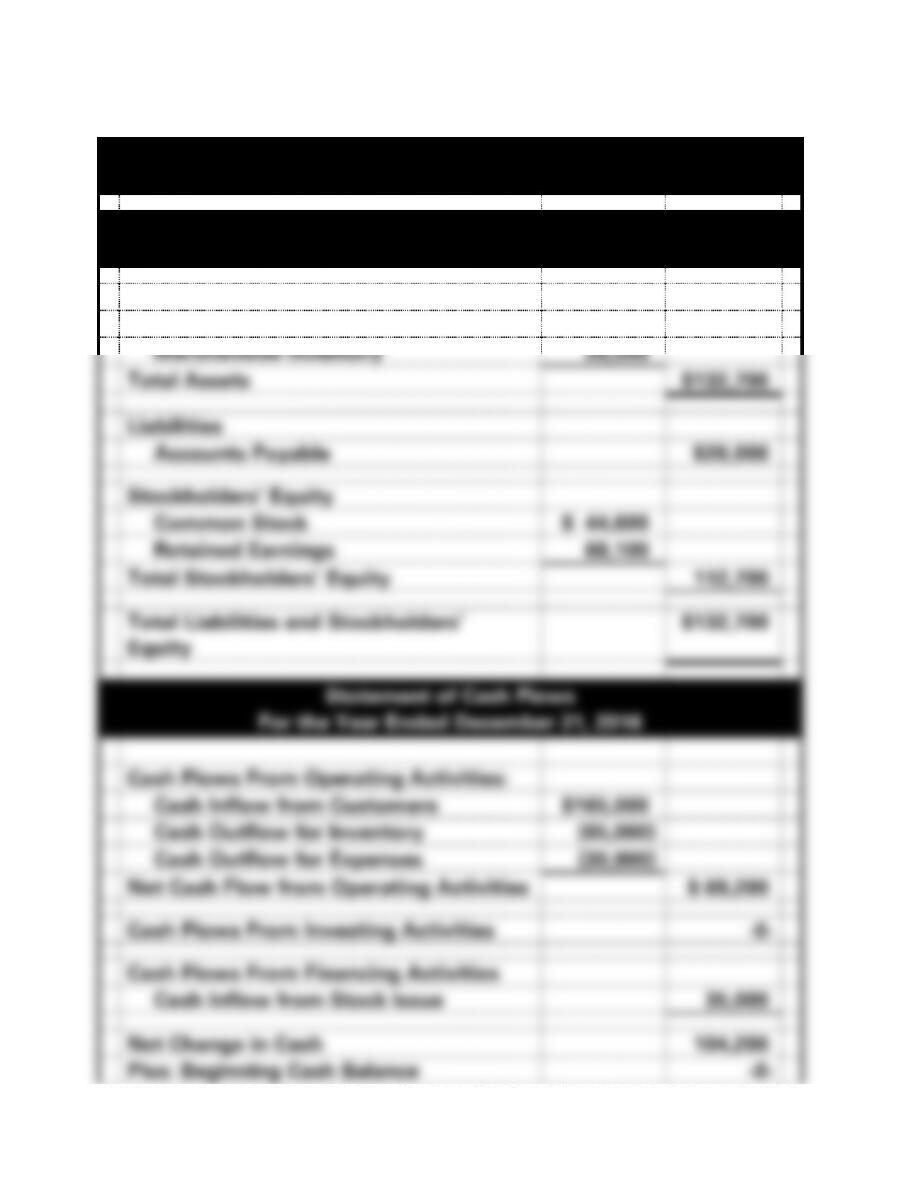

Assets

Cash

$104,200

Merchandise Inventory

28,500

Total Assets

$132,700

Liabilities

Accounts Payable

$20,000

Stockholders’ Equity

Common Stock

$ 44,600

Retained Earnings

68,100

Total Stockholders’ Equity

112,700

Total Liabilities and Stockholders’

Equity

$132,700

Statement of Cash Flows

For the Year Ended December 31, 2016

Cash Flows From Operating Activities:

Cash Inflow from Customers

$165,000

Cash Outflow for Inventory

(65,000)

Cash Outflow for Expenses

(30,800)

Net Cash Flow from Operating Activities

$ 69,200

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities

Cash Inflow from Stock Issue

35,000

Net Change in Cash

104,200

Plus: Beginning Cash Balance

-0-

4-64

Ending Cash Balance

$104,200

4-65

EXERCISE 4-22A (cont.) (Appendix)

d.

Bob’s Bike Shop

General Journal

Date

Account Titles

Debit

Credit

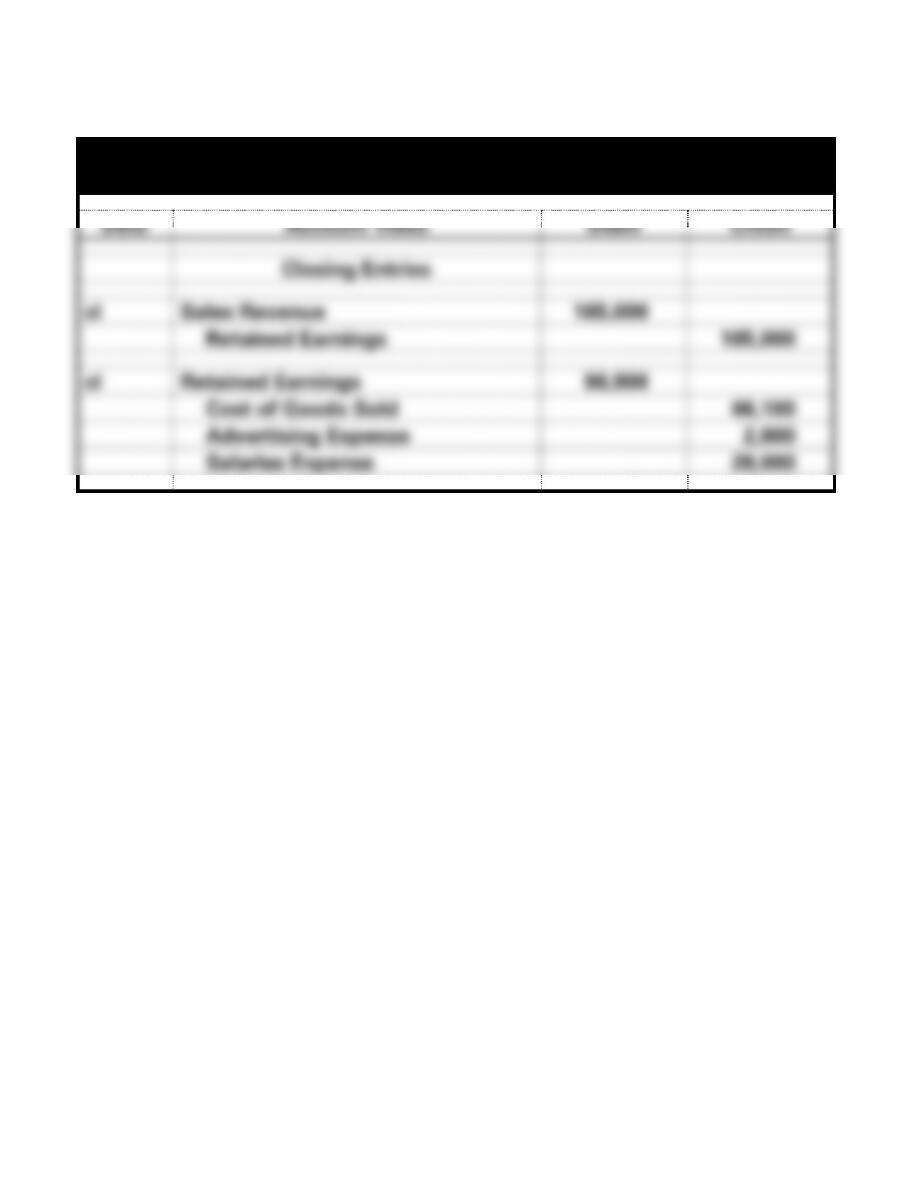

Closing Entries

cl

Sales Revenue

165,000

Retained Earnings

165,000

cl

Retained Earnings

96,900

Cost of Goods Sold

66,100

Advertising Expense

2,800

Salaries Expense

28,000

4-66

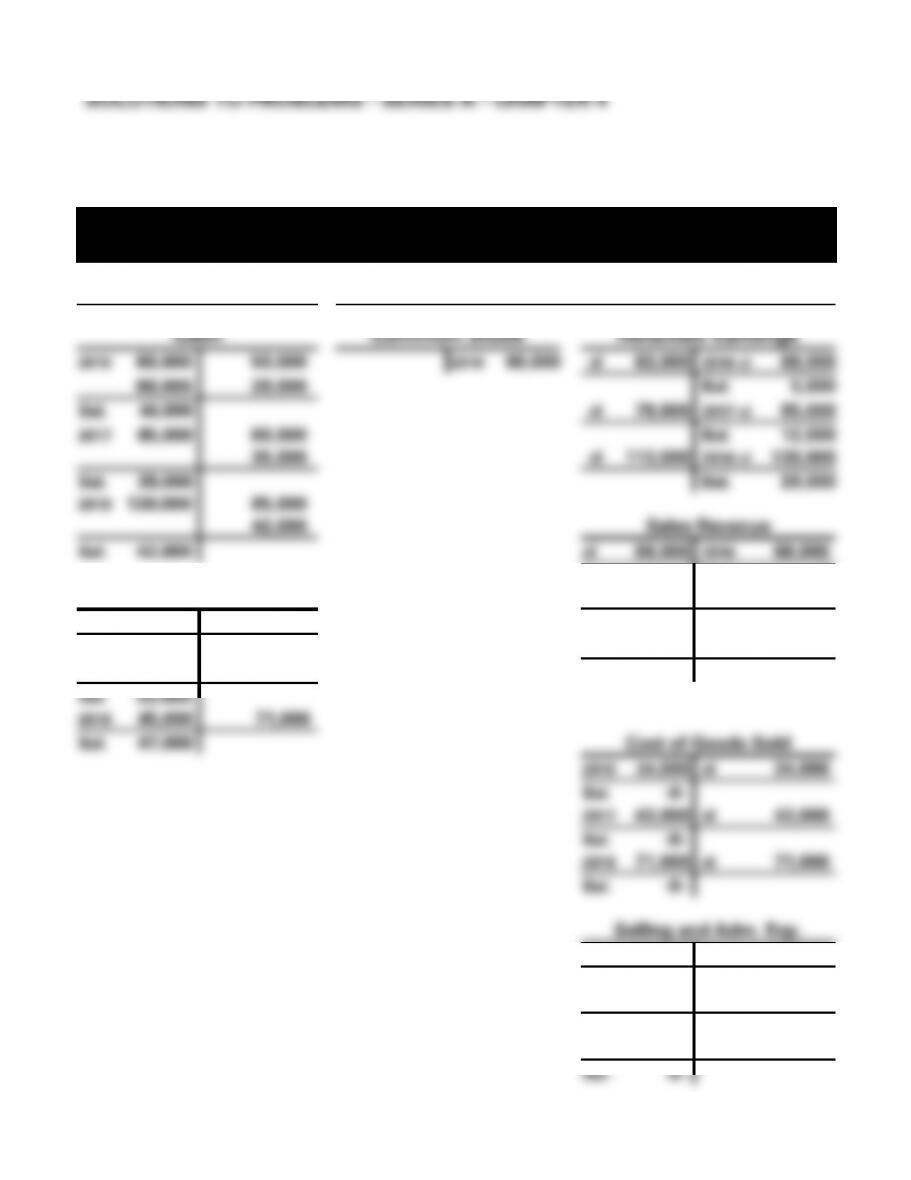

EXERCISE 4-22A d. (cont.) (Appendix)

Bob’s Bike Shop

T-Accounts

Assets

=

Liabilities

+

Stockholders’ Equity

Cash

Accounts Payable

Common Stock

Bal. 104,200

Bal. 20,000

Bal. 44,600

Retained Earnings

Merchandise Inventory

cl 96,900

cl 165,000

Bal. 28,500

Bal. 68,100

Sales Revenue

Bal. 165,000

cl 165,000

Bal. -0-

Cost of Goods Sold

Bal. 66,100

cl 66,100

Bal. -0-

Advertising Expense

Bal. 2,800

cl 2,800

Bal. -0-

Salaries Expense

Bal. 28,000

cl 28,000

Bal. -0-

4-67

EXERCISE 4-22A (cont.) (Appendix)

e.

Bob’s Bike Shop

Post-Closing Trial Balance

As of December 31, 2016

Account Titles

Debit

Credit

Cash

$104,200

Merchandise Inventory

28,500

Accounts Payable

$ 20,000

Common Stock

44,600

Retained Earnings

68,100

Totals

$132,700

$132,700

f. A business that may use the periodic method would be a small retailer

that does not have the necessary computer equipment to be able to

record the cost of goods as they are sold. Also, it may be more cost

effective for a business with small amounts of inventory to use the

periodic method. Most large retailers now use the perpetual inventory

system. The use of computer systems that track inventory make the

use of the perpetual method possible. Inventory items are scanned

into inventory when received and scanned out of inventory when sold.

For example, most large grocery stores use the perpetual system of

recording inventory.

g. Owners may contribute many types of assets to a business in exchange

for stock in the business. For instance, an owner may contribute

automobiles, office equipment, land, building, or other similar assets

that are personally owned in exchange for stock in a corporation.

4-68

PROBLEM 4-23A

T-accounts are provided for the instructor’s use:

Blooming Flower Company

T-Accounts 2016, 2017, and 2018

Assets

=

Stockholders’ Equity

Cash

Common Stock

Retained Earnings

2016 60,000

50,000

2016 60,000

cl 63,000

2016 cl 68,000

68,000

29,000

Bal. 5,000

Bal. 49,000

cl 78,000

2017 cl 85,000

2017 85,000

60,000

Bal. 12,000

35,000

cl 113,000

2018 cl 130,000

Bal. 39,000

Bal. 29,000

2018 130,000

85,000

42,000

Sales Revenue

Bal. 42,000

cl 68,000

2016 68,000

Bal. -0-

Merchandise Inv.

cl 85,000

2017 85,000

2016 50,000

34,000

Bal. -0-

Bal. 16,000

cl 130,000

2018 130,000

2017 60,000

43,000

Bal. -0-

Bal. 33,000

2018 85,000

71,000

Bal. 47,000

Cost of Goods Sold

2016 34,000

cl 34,000

Bal. -0-

2017 43,000

cl 43,000

Bal. -0-

2018 71,000

cl 71,000

Bal. -0-

Selling and Adm. Exp.

2016 29,000

cl 29,000

Bal. -0-

2017 35,000

cl 35,000

Bal. -0-

2018 42,000

cl 42,000

Bal. -0-

4-69

4-70

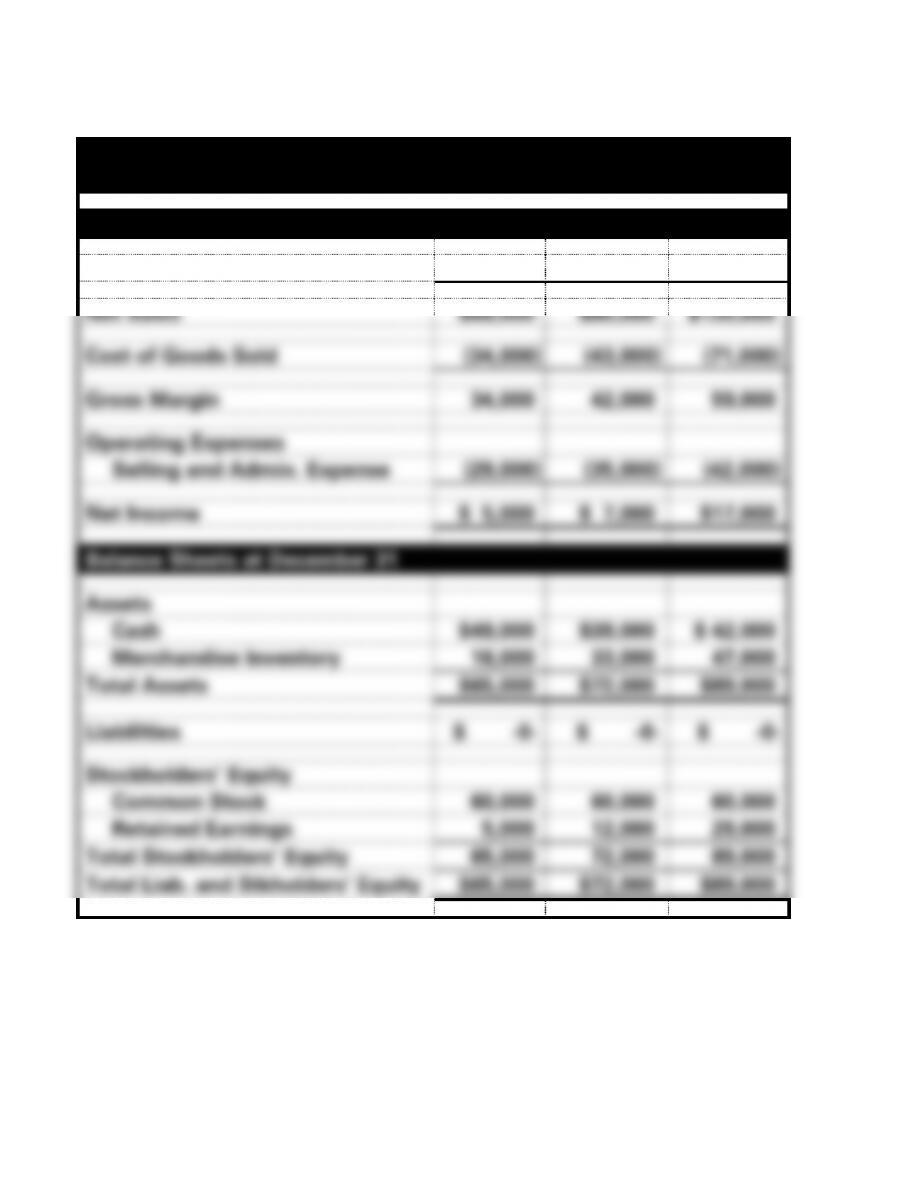

PROBLEM 4-23A (cont.)

Blooming Flower Company

Financial Statements

Income Statements for the Year Ended December 31

2016

2017

2018

Net Sales

$68,000

$85,000

$130,000

Cost of Goods Sold

(34,000)

(43,000)

(71,000)

Gross Margin

34,000

42,000

59,000

Operating Expenses

Selling and Admin. Expense

(29,000)

(35,000)

(42,000)

Net Income

$ 5,000

$ 7,000

$17,000

Balance Sheets at December 31

Assets

Cash

$49,000

$39,000

$ 42,000

Merchandise Inventory

16,000

33,000

47,000

Total Assets

$65,000

$72,000

$89,000

Liabilities

$ -0-

$ -0-

$ -0-

Stockholders’ Equity

Common Stock

60,000

60,000

60,000

Retained Earnings

5,000

12,000

29,000

Total Stockholders’ Equity

65,000

72,000

89,000

Total Liab. and Stkholders’ Equity

$65,000

$72,000

$89,000

4-71

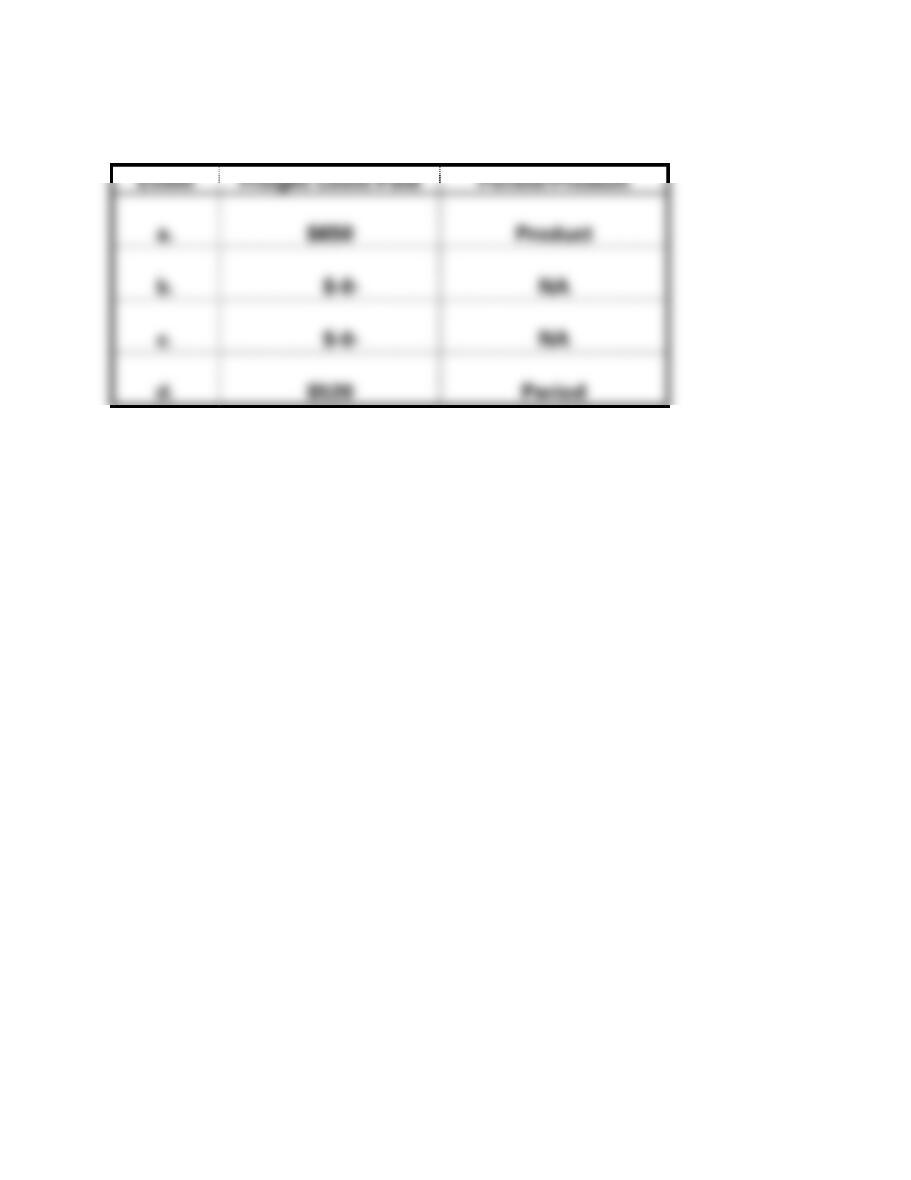

PROBLEM 4-24A

Event

Freight Costs Paid

Period/Product

a.

$650

Product

b.

$-0-

NA

c.

$-0-

NA

d.

$520

Period

4-72

PROBLEM 4-25A

Event

Product Costs

Period Costs

a.

b.

c.

d.

e.

f.

g.

h.

i.

j.

4-73

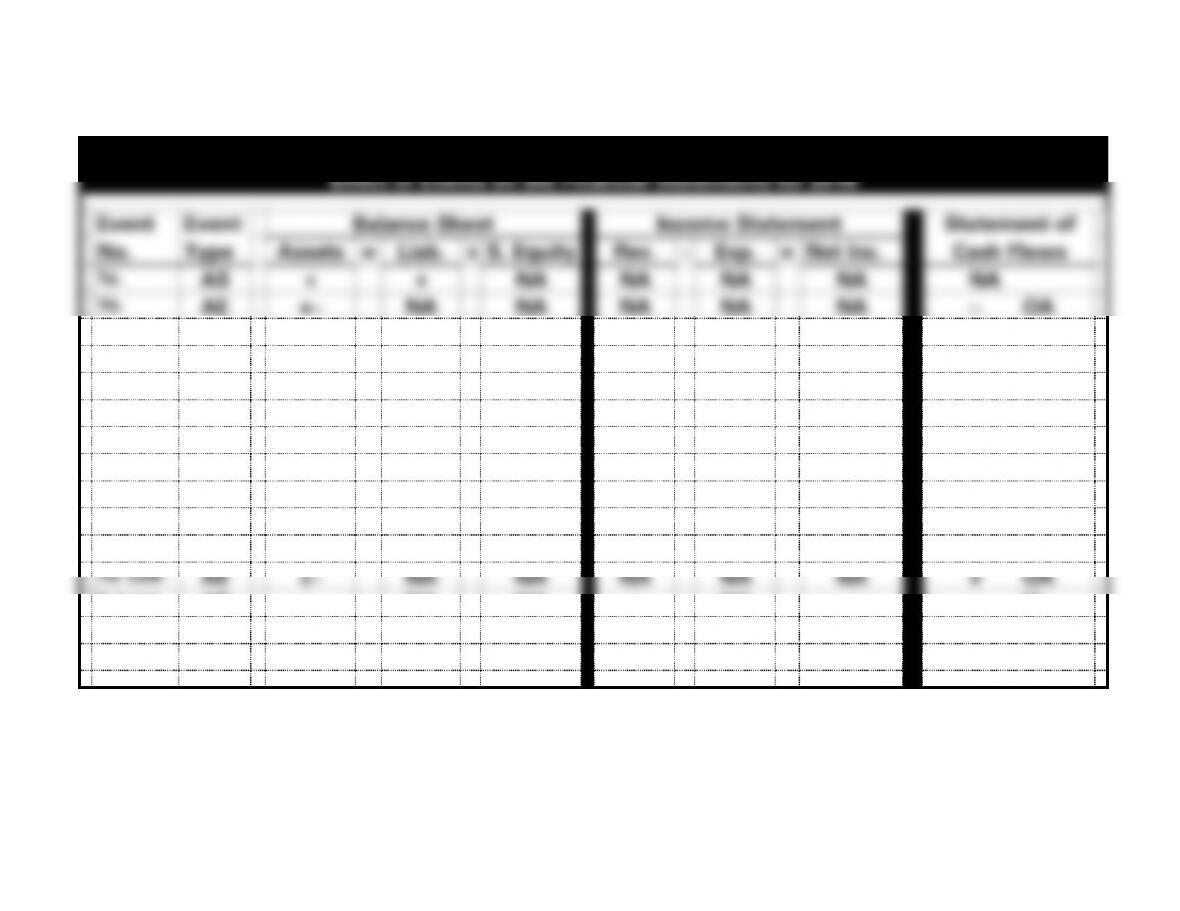

PROBLEM 4-26A

a.

Redd Company

Effect of Events on the Financial Statements for 2016

Event

Event

Balance Sheet

Income Statement

Statement of

No.

Type

Assets

=

Liab.

+

S. Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flows

1a.

AS

+

+

NA

NA

NA

NA

NA

1b.

AE

+−

NA

NA

NA

NA

NA

− OA

2.

AU

−

−

NA

NA

NA

NA

NA

3a. Disc.

AU

−

−

NA

NA

NA

NA

NA

3b. Pay.

AU

−

−

NA

NA

NA

NA

− OA

4a. Sale

AS

+

NA

+

+

NA

+

NA

4b. Cost

AU

−

NA

−

NA

+

−

NA

5a. Ret

AU

−

NA

−

−

NA

−

− OA

5b. Ret.

AS

+

NA

+

NA

−

+

NA

6. Frt.

AU

−

NA

−

NA

+

−

− OA

7a. Disc.

AU

−

NA

−

−

NA

−

NA

7b. Coll.

AE

+−

NA

NA

NA

NA

NA

+ OA

8. Land

AE

+−

NA

NA

+

NA

+

+ IA

9. Int.

AS

+

NA

+

+

NA

+

NA

10. Adj.

AU

−

NA

−

NA

+

−

NA

4-74

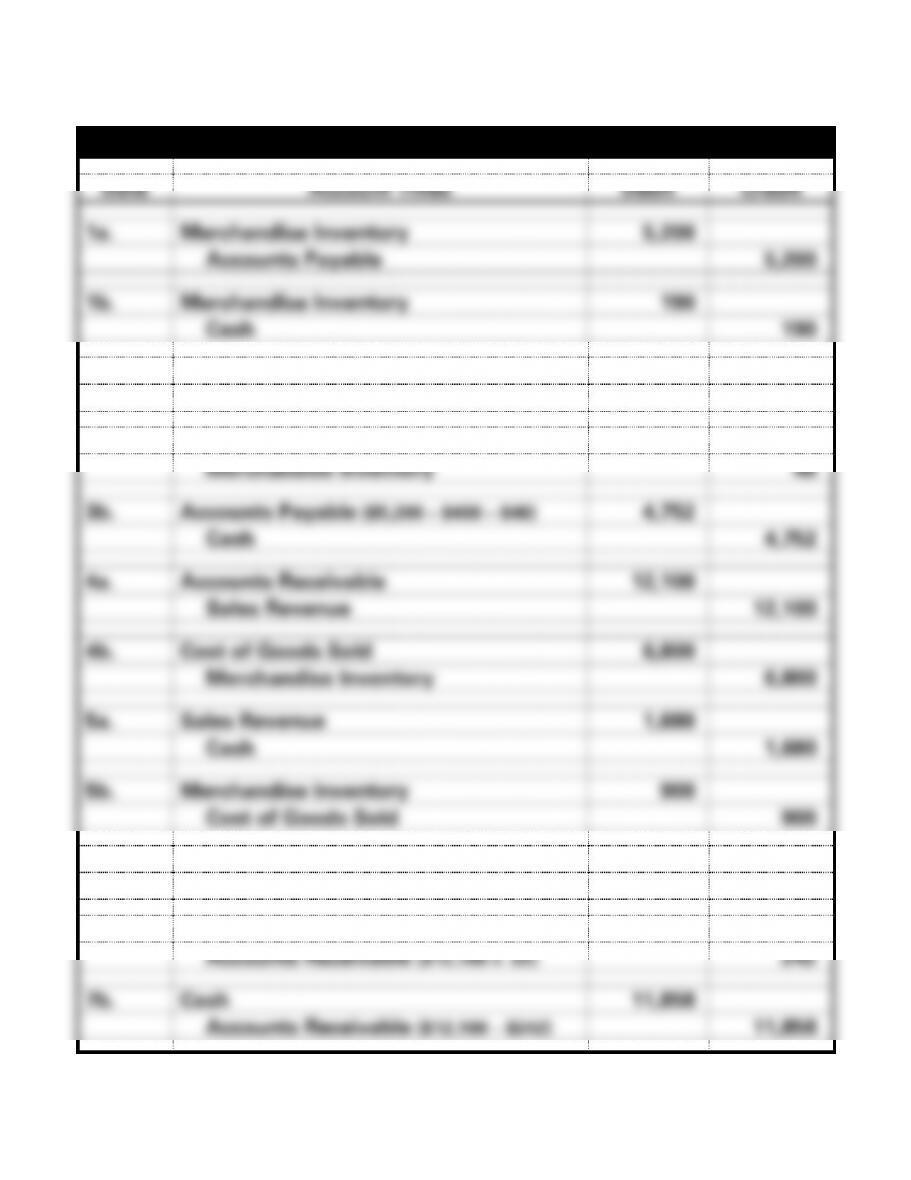

PROBLEM 4-26A (cont.)

b.

Redd Company General Journal

Date

Account Titles

Debit

Credit

1a.

Merchandise Inventory

5,200

Accounts Payable

5,200

1b.

Merchandise Inventory

190

Cash

190

2.

Accounts Payable

400

Merchandise Inventory

400

3a.

Accounts Payable [($5,200 – $400) x .01]

48

Merchandise Inventory

48

3b.

Accounts Payable ($5,200 – $400 – $48)

4,752

Cash

4,752

4a.

Accounts Receivable

12,100

Sales Revenue

12,100

4b.

Cost of Goods Sold

6,800

Merchandise Inventory

6,800

5a.

Sales Revenue

1,680

Cash

1,680

5b.

Merchandise Inventory

900

Cost of Goods Sold

900

6.

Transportation-out

140

Cash

140

7a.

Sales Revenue

242

Accounts Receivable ($12,100 x .02)

242

7b.

Cash

11,858

Accounts Receivable ($12,100 – $242)

11,858

4-75

PROBLEM 4-26A b. (cont.)

Redd Company General Journal

Date

Account Titles

Debit

Credit

8.

Cash

8,500

Land

7,000

Gain on the Sale of Land

1,500

9.

Interest Receivable

600

Interest Revenue

600

10.

Cost of Goods Sold (Inventory Loss)

642

Merchandise Inventory

642

4-76

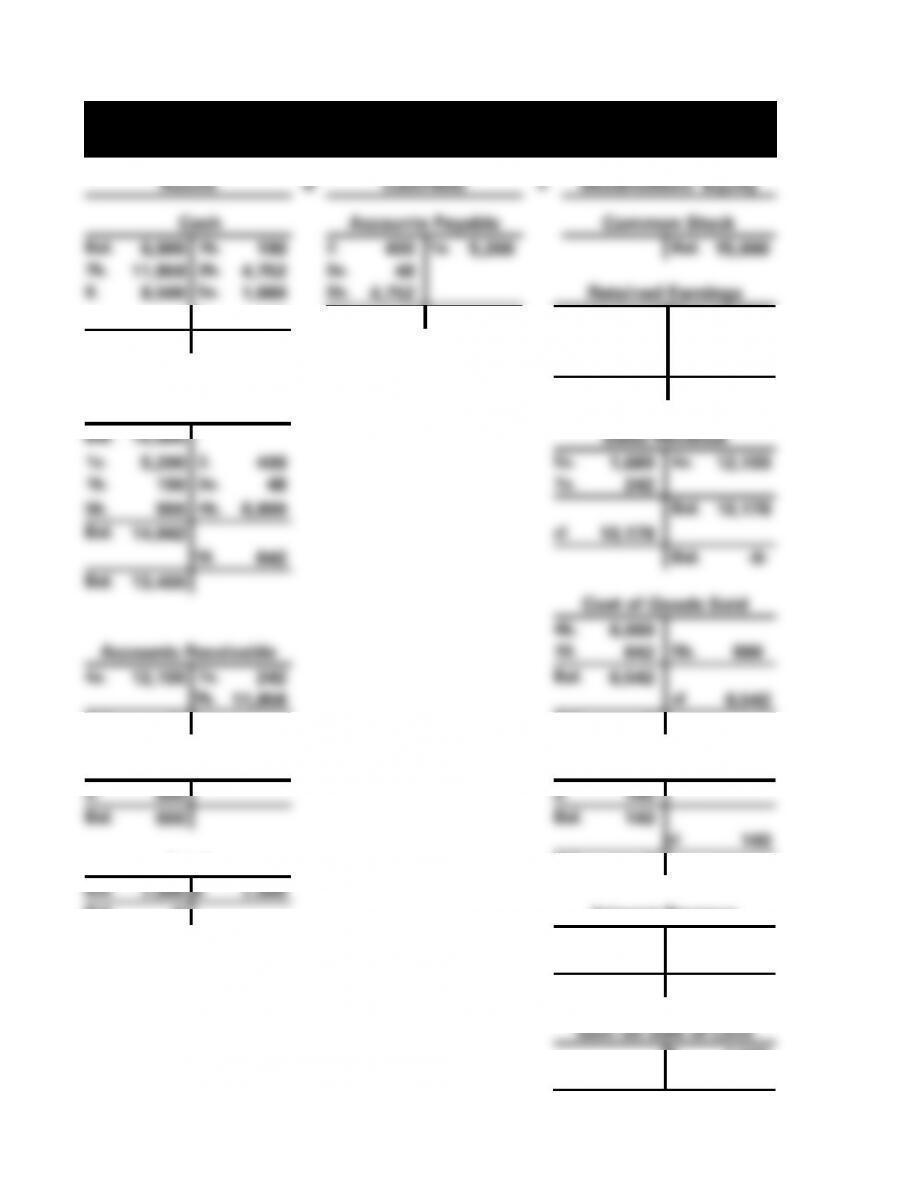

PROBLEM 4-26A (cont.) c.

Redd Company

T-Accounts for 2016

Assets

=

Liabilities

+

Stockholders’ Equity

Cash

Accounts Payable

Common Stock

Bal.

6,900

1b.

190

2.

400

1a.

5,200

Bal.

15,000

7b.

11,858

3b.

4,752

3a.

48

8.

8,500

5a.

1,680

3b.

4,752

Retained Earnings

6.

140

Bal.

-0-

Bal.

13,900

Bal.

20,496

cl.

2,100

cl

6,682

cl

10,178

Bal.

19,496

Mdse. Inventory

Bal.

15,000

Sales Revenue

1a.

5,200

2.

400

5a.

1,680

4a.

12,100

1b.

190

3a.

48

7a.

242

5b.

900

4b.

6,800

Bal.

10,178

Bal.

14,042

cl

10,178

10.

642

Bal.

-0-

Bal.

13,400

Cost of Goods Sold

4b.

6,800

Accounts Receivable

10.

642

5b.

900

4a.

12,100

7a.

242

Bal.

6,542

7b.

11,858

cl

6,542

Bal.

-0-

Bal.

-0-

Interest Receivable

Transportation-out

9.

600

6.

140

Bal.

600

Bal.

140

cl

140

Land

Bal.

-0-

Bal.

7,000

8.

7,000

Bal.

-0-

Interest Revenue

9.

600

cl.

600

Bal.

-0-

Gain on Sale of Land

8.

1,500

cl.

1,500