Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 12 Statement of Cash Flows

12-81

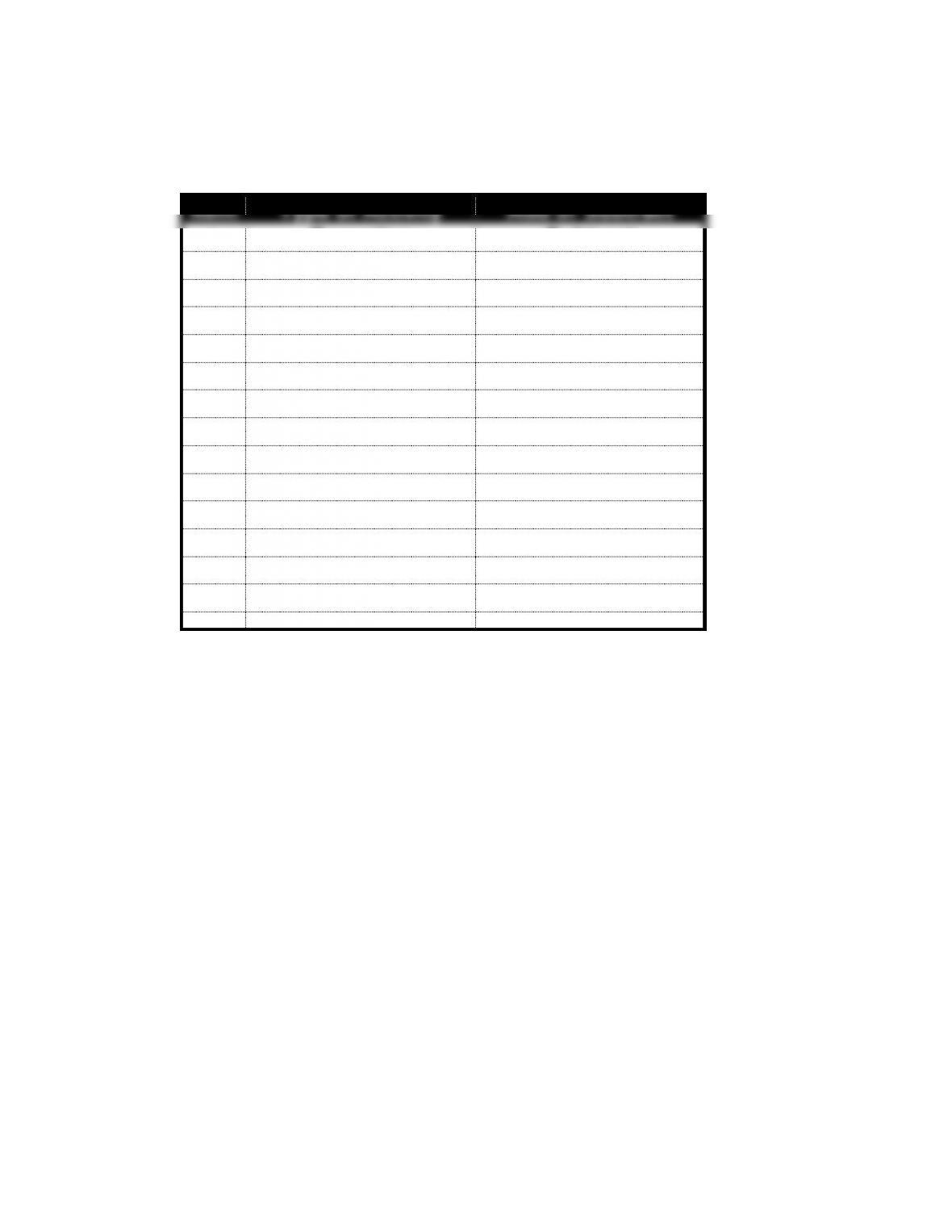

PROBLEM 12-17B

Item

Type of Activity

Add or Subtract

a.

Operating

Subtract

b.

Investing

Subtract

c.

Operating

Subtract

d.

Operating

Add

e.

Financing

Subtract

f.

Operating

Subtract

g.

Financing

Subtract

h.

Financing

Add

i.

Investing

Add

j.

Operating

Add

k.

Financing

Add

l.

Operating

Add

m.

Operating

Add

n.

Financing

Subtract

12-82

Chapter 12 Statement of Cash Flows

12-83

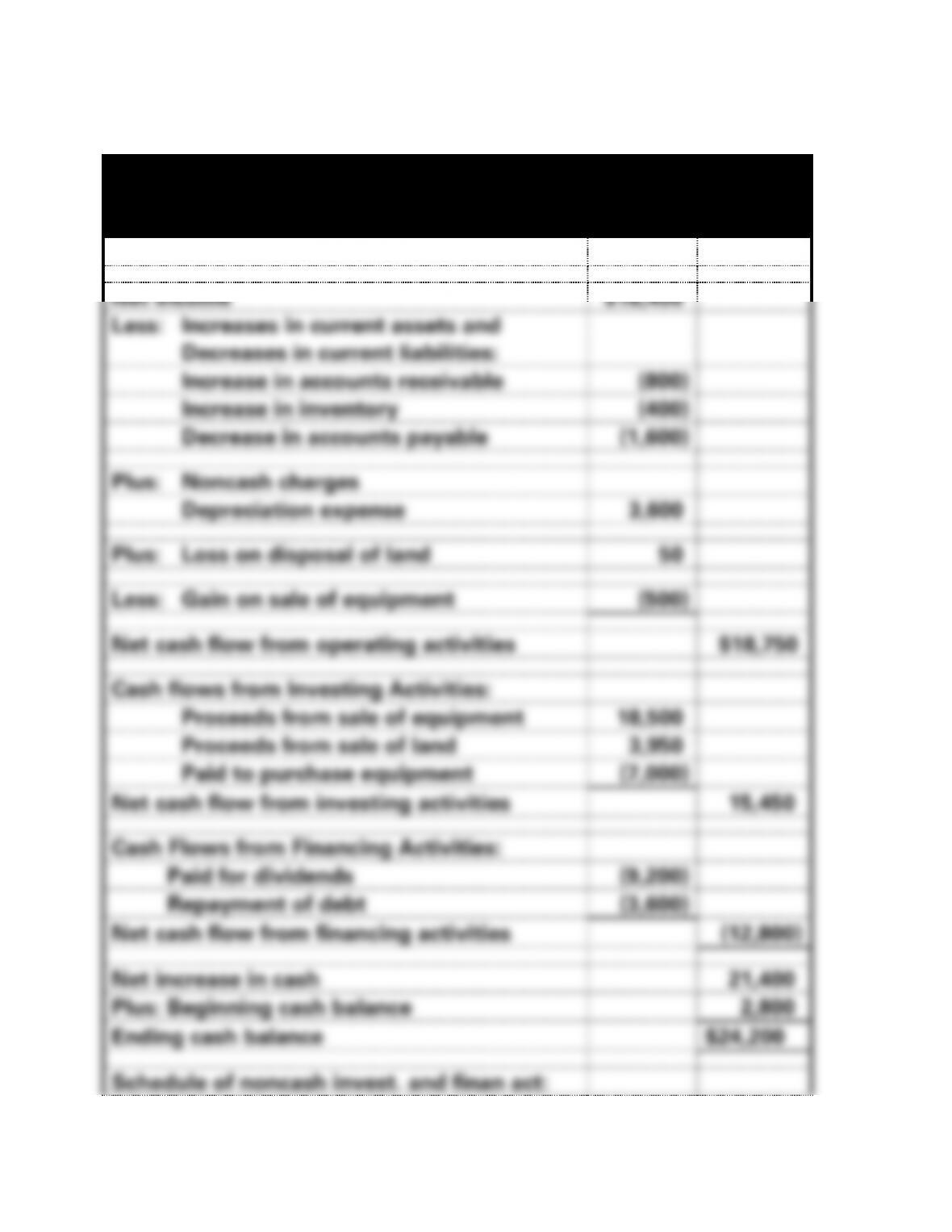

PROBLEM 12-18B

Culinary Products Company

Statement of Cash Flows

For the Year Ended December 31, 2017

Cash Flows from Operating Activities:

Net income

$18,400

Less: Increases in current assets and

Decreases in current liabilities:

Increase in accounts receivable

(800)

Increase in inventory

(400)

Decrease in accounts payable

(1,600)

Plus: Noncash charges

Depreciation expense

3,600

Plus: Loss on disposal of land

50

Less: Gain on sale of equipment

(500)

Net cash flow from operating activities

$18,750

Cash flows from Investing Activities:

Proceeds from sale of equipment

18,500

Proceeds from sale of land

3,950

Paid to purchase equipment

(7,000)

Net cash flow from investing activities

15,450

Cash Flows from Financing Activities:

Paid for dividends

(9,200)

Repayment of debt

(3,600)

Net cash flow from financing activities

(12,800)

Net increase in cash

21,400

Plus: Beginning cash balance

2,800

Ending cash balance

$24,200

Schedule of noncash invest. and finan act:

Chapter 12 Statement of Cash Flows

12-84

Issued common stock for land

$ 12,000

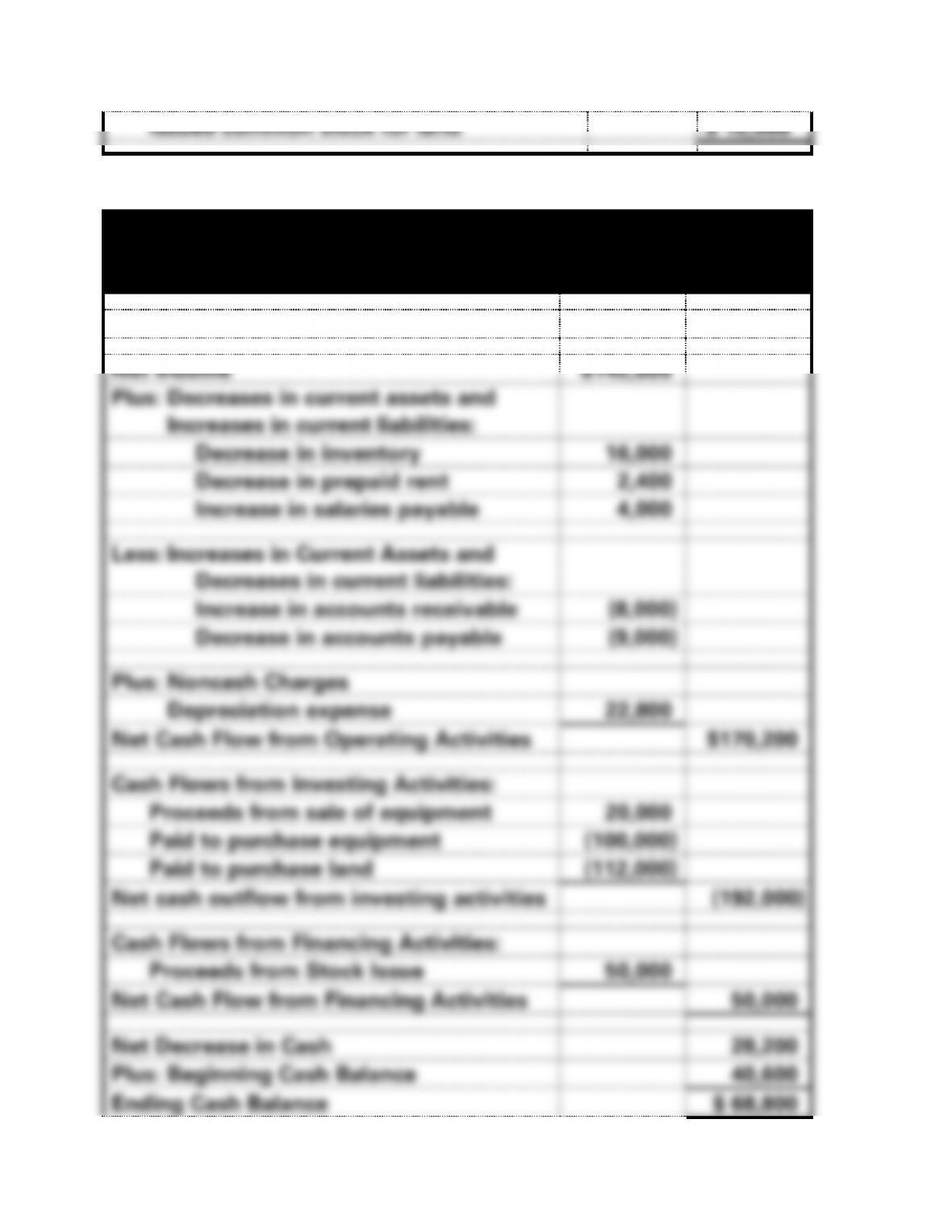

PROBLEM 12-19B

Wang Beauty Products, Inc.

Statement of Cash Flows

For the Year Ended December 31, 2017

Cash Flows from Operating Activities:

Net income

$142,000

Plus: Decreases in current assets and

Increases in current liabilities:

Decrease in inventory

16,000

Decrease in prepaid rent

2,400

Increase in salaries payable

4,000

Less: Increases in Current Assets and

Decreases in current liabilities:

Increase in accounts receivable

(8,000)

Decrease in accounts payable

(9,000)

Plus: Noncash Charges

Depreciation expense

22,800

Net Cash Flow from Operating Activities

$170,200

Cash Flows from Investing Activities:

Proceeds from sale of equipment

20,000

Paid to purchase equipment

(100,000)

Paid to purchase land

(112,000)

Net cash outflow from investing activities

(192,000)

Cash Flows from Financing Activities:

Proceeds from Stock Issue

50,000

Net Cash Flow from Financing Activities

50,000

Net Decrease in Cash

28,200

Plus: Beginning Cash Balance

40,600

Ending Cash Balance

$ 68,800

12-85

Chapter 12 Statement of Cash Flows

12-86

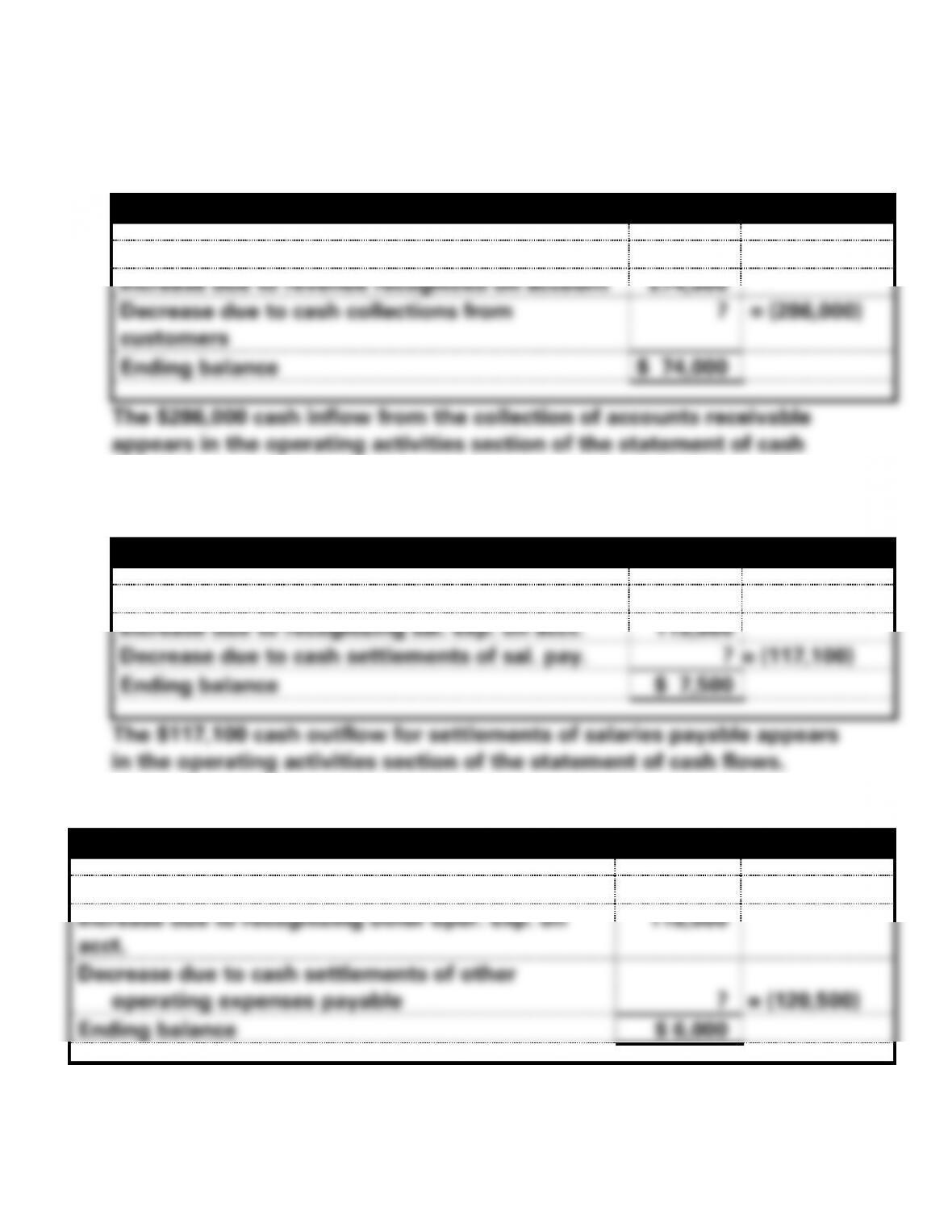

PROBLEM 12-20B

a.

(1)

Reconciliation of Accounts Receivable Account

Beginning balance

$86,000

Increase due to revenue recognized on account

274,000

Decrease due to cash collections from

customers

?

= (286,000)

Ending balance

$ 74,000

flows.

(2)

Reconciliation of Salaries Payable Account

Beginning balance

$ 9,600

Increase due to recognizing sal. exp. on acct.

115,000

Decrease due to cash settlements of sal. pay.

?

= (117,100)

Ending balance

$ 7,500

(3)

Reconciliation of Other Operating Expenses Payable Account

Beginning balance

$ 8,500

Increase due to recognizing other oper. exp. on

acct.

118,000

Decrease due to cash settlements of other

operating expenses payable

?

= (120,500)

Ending balance

$ 6,000

Chapter 12 Statement of Cash Flows

12-87

12-88

PROBLEM 12-20B (continued)

(4) Depreciation expense does not affect cash flow and is not

(5)

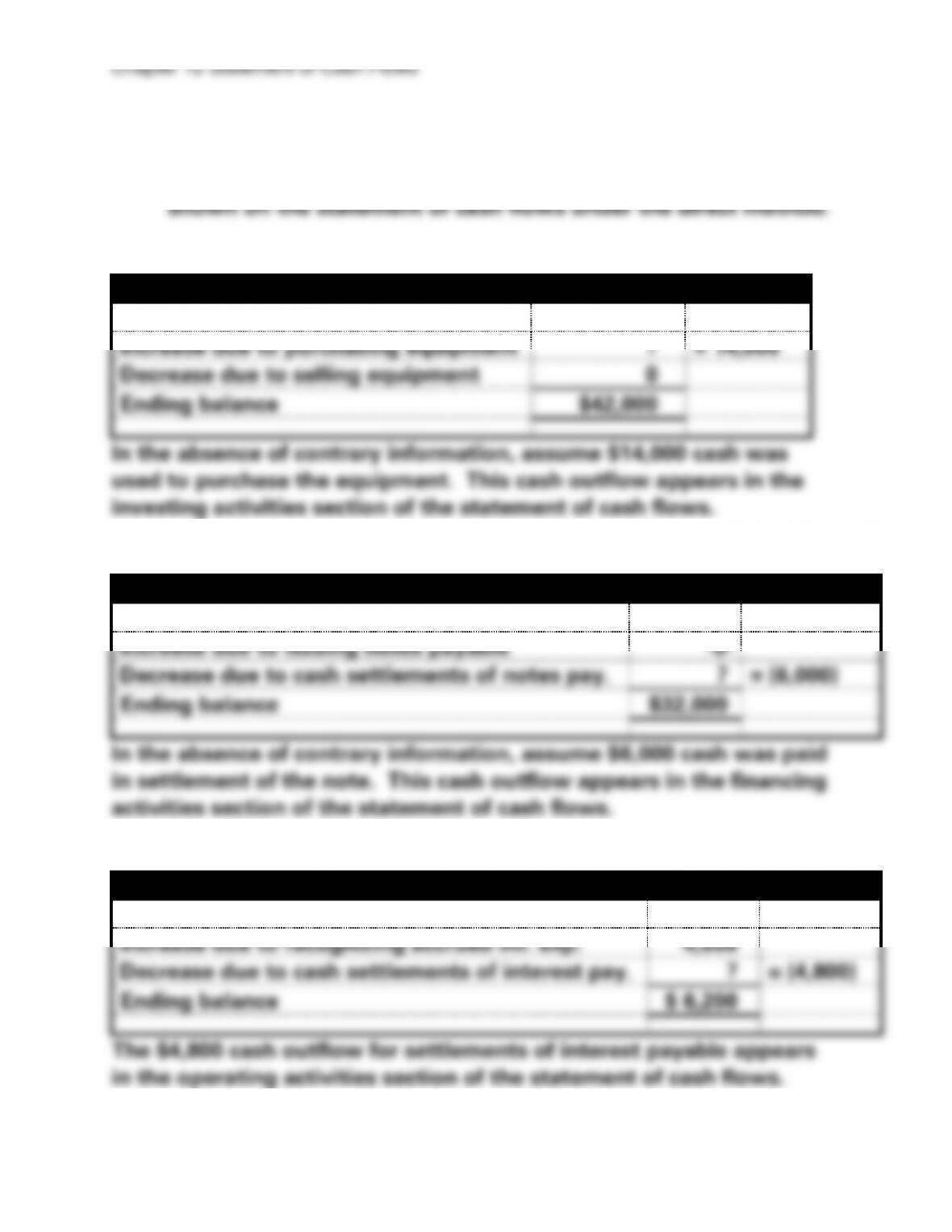

Reconciliation of Equipment Account

Beginning balance

$28,000

Increase due to purchasing equipment

?

= 14,000

Decrease due to selling equipment

0

Ending balance

$42,000

In the absence of contrary information, assume $14,000 cash was

used to purchase the equipment. This cash outflow appears in the

investing activities section of the statement of cash flows.

(6)

Reconciliation of Notes Payable Account

Beginning balance

$38,000

Increase due to issuing notes payable

-0-

Decrease due to cash settlements of notes pay.

?

= (6,000)

Ending balance

$32,000

In the absence of contrary information, assume $6,000 cash was paid

in settlement of the note. This cash outflow appears in the financing

activities section of the statement of cash flows.

(7)

Reconciliation of Interest Payable Account

Beginning balance

$ 6,400

Increase due to recognizing accrued int. exp.

4,600

Decrease due to cash settlements of interest pay.

?

= (4,800)

Ending balance

$ 6,200

The $4,800 cash outflow for settlements of interest payable appears

in the operating activities section of the statement of cash flows.

Chapter 12 Statement of Cash Flows

12-89

12-90

PROBLEM 12-20B (continued)

(8)

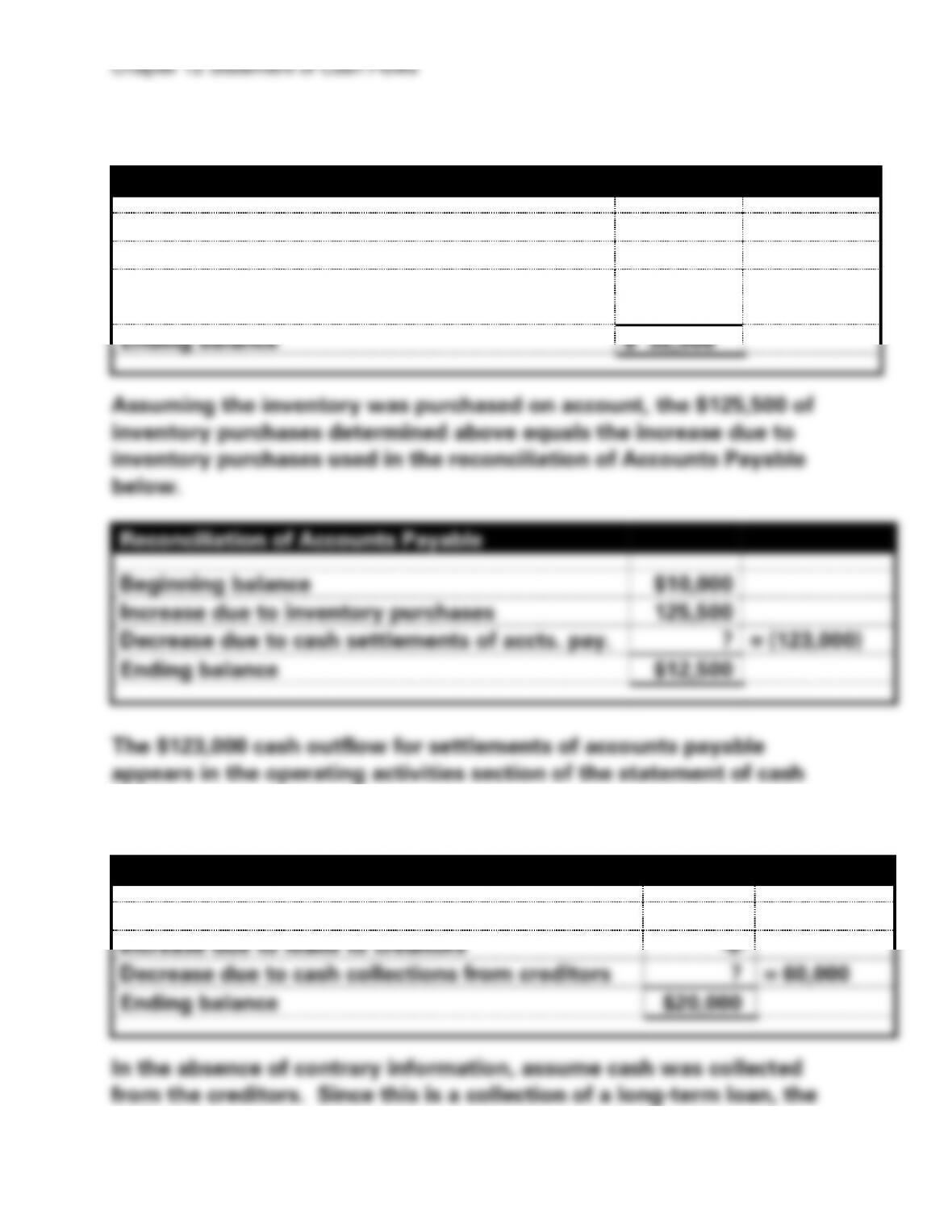

Reconciliation of Inventory

Beginning balance

$ 26,000

Increase due to inventory purchases

?

= 125,500

Decrease due to recognizing cost of goods

sold

(119,000)

Ending balance

$ 32,500

Reconciliation of Accounts Payable

Beginning balance

$10,000

Increase due to inventory purchases

125,500

Decrease due to cash settlements of accts. pay.

?

= (123,000)

Ending balance

$12,500

flows.

(9)

Reconciliation of Notes Receivable

Beginning balance

$80,000

Increase due to loans to creditors

-0-

Decrease due to cash collections from creditors

?

= 60,000

Ending balance

$20,000

Chapter 12 Statement of Cash Flows

12-91

Chapter 12 Statement of Cash Flows

12-92

PROBLEM 12-20B (cont.)

(10)

Reconciliation of Common Stock Account

Beginning balance

$140,000

Increase due to issuing common stock

?

= 50,000

Ending balance

$190,000

In the absence of contrary information, assume cash was obtained

when the stock was issued. This cash inflow appears in the financing

activities section of the statement of cash flows.

(11)

Reconciliation of Land Account

Beginning Balance

$48,000

Increase due to purchasing land

?

= 0

Decrease due to selling land

(20,000)

Ending Balance

$28,000

The reconciliation suggests that no land was purchased during the

period. The full sales price of $16,000 as reported in the transaction

data results in a cash inflow that appears in the investing activities

section of the statement of cash flows. The loss is not shown in the

operating activities section of the statement of cash flows under the

direct method.

12-93

PROBLEM 12-20B (cont.)

(12)

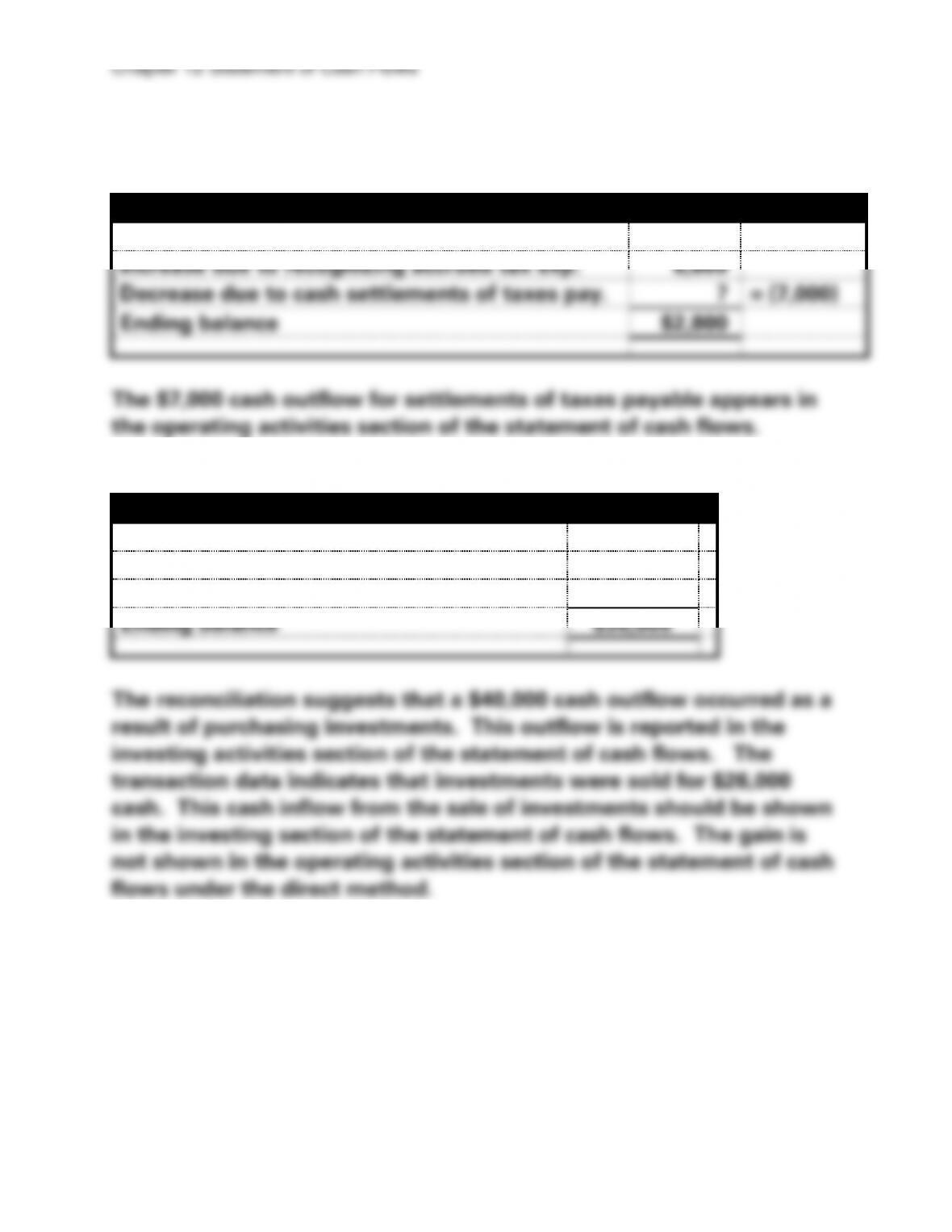

Reconciliation of Taxes Payable Account

Beginning balance

$3,200

Increase due to recognizing accrued tax exp.

6,600

Decrease due to cash settlements of taxes pay.

?

= (7,000)

Ending balance

$2,800

The $7,000 cash outflow for settlements of taxes payable appears in

the operating activities section of the statement of cash flows.

(13)

Reconciliation of Investments Account

Beginning balance

$10,000

Increase due to purchasing investments

40,000

Decrease due to selling investments

(20,000)

Ending balance

$30,000

The reconciliation suggests that a $40,000 cash outflow occurred as a

result of purchasing investments. This outflow is reported in the

investing activities section of the statement of cash flows. The

transaction data indicates that investments were sold for $26,000

cash. This cash inflow from the sale of investments should be shown

in the investing section of the statement of cash flows. The gain is

not shown in the operating activities section of the statement of cash

flows under the direct method.

Chapter 12 Statement of Cash Flows

12-94

PROBLEM 12-20B (cont.)

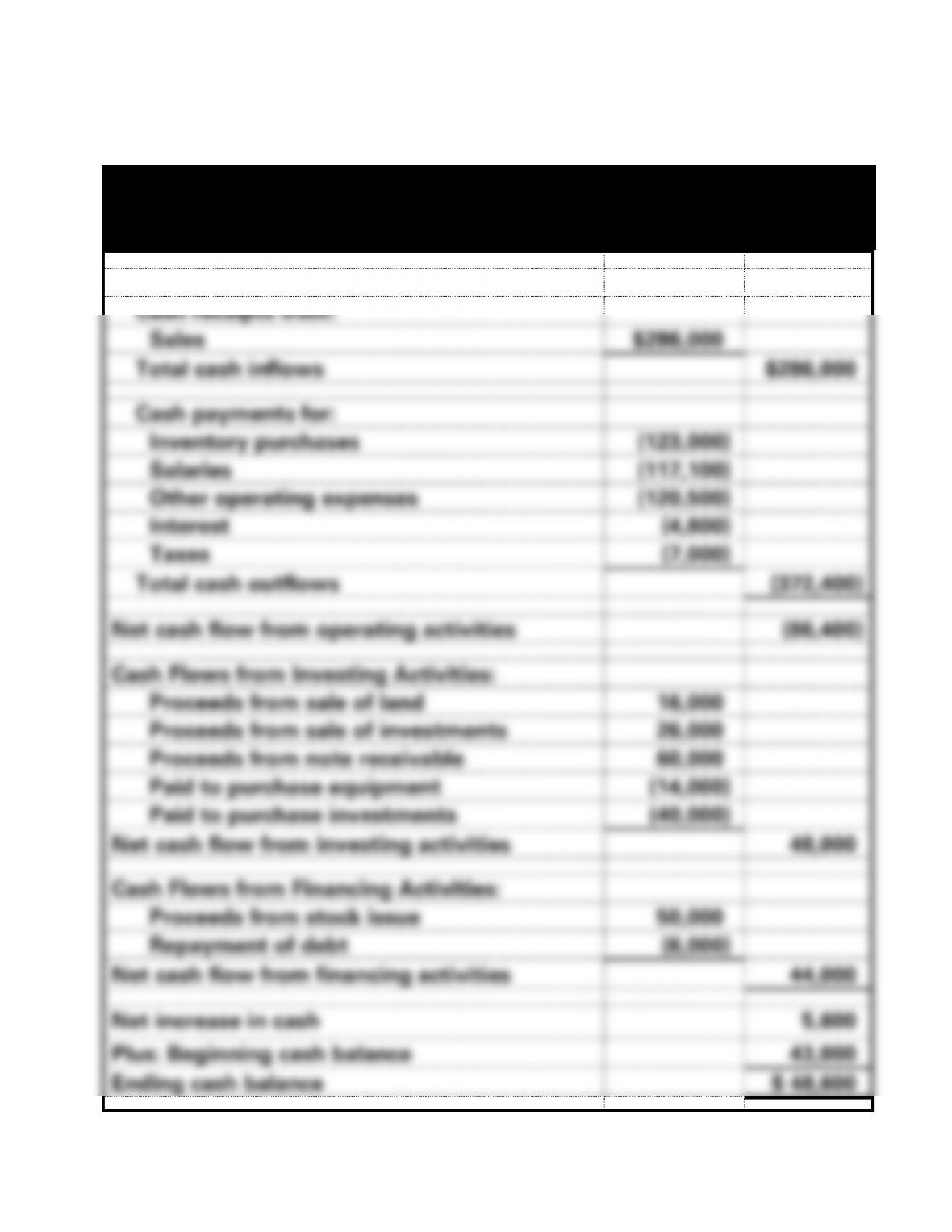

Electric Company

Statement of Cash Flows

For the Year Ended December 31, 2017

Cash Flows from Operating Activities:

Cash receipts from:

Sales

$286,000

Total cash inflows

$286,000

Cash payments for:

Inventory purchases

(123,000)

Salaries

(117,100)

Other operating expenses

(120,500)

Interest

(4,800)

Taxes

(7,000)

Total cash outflows

(372,400)

Net cash flow from operating activities

(86,400)

Cash Flows from Investing Activities:

Proceeds from sale of land

16,000

Proceeds from sale of investments

26,000

Proceeds from note receivable

60,000

Paid to purchase equipment

(14,000)

Paid to purchase investments

(40,000)

Net cash flow from investing activities

48,000

Cash Flows from Financing Activities:

Proceeds from stock issue

50,000

Repayment of debt

(6,000)

Net cash flow from financing activities

44,000

Net increase in cash

5,600

Plus: Beginning cash balance

43,000

Ending cash balance

$ 48,600