4-1

Chapter 4

Accounting for Merchandising Businesses

General Comments for Chapter 4

Chapter 4 introduces accounting for inventory transactions using the perpetual method. In

today’s high-technology environment, the perpetual system has become the predominant

method of accounting for inventories. Because the periodic method is still used in many cir-

cumstances, it is included in the chapter appendix, though in less depth.

With the perpetual method, purchases and related transactions (purchase returns and allow-

ances, purchase discounts, and transportation-in) are recorded in the Inventory account.

Sales returns and allowances and sales discounts are recorded directly in the Sales account.

The balance in the Sales account is therefore the amount of net sales, which is the first item

reported on the income statement. This presentation is consistent with the way sales are re-

ported in real-world financial statements. We challenge you to find a published annual report

that displays the amount of sales discounts or sales returns and allowances in the income

statement. You may want to tell your students that companies can maintain separate ac-

counts for these items if management desires to capture this information for decision-making

purposes. Regardless, these accounts are netted against gross sales before the information is

reported in financial statements.

Recall that the primary objective of the textbook is to teach students how accounting events

affect financial statements. Students do not need to learn both the gross and net methods of

accounting for cash discounts to understand how those discounts affect financial statements.

A disadvantage of traditional textbooks is information overload. The textbook addresses this

problem by reducing the number of alternative recording procedures it presents to students.

In this chapter, the text explanation of cash discounts is limited to the gross method. If stu-

dents learn in accounting principles how discounts affect financial statements, they can easily

learn the net method when they take intermediate accounting.

This chapter introduces the multistep income statement. Direct special attention toward the

reporting of interest. Interest is classified as a nonoperating item on a multistep income

statement and as an operating activities item on the statement of cash flows. This incon-

sistency provides an opportunity to discuss how accounting standards are developed. If you

have not explained the role of the Financial Accounting Standards Board, this is a good time

to do so. Students should learn that accounting standards evolve through a democratic pro-

cess influenced by changes in society. Effective accounting requires adaptation and judg-

ment. It is governed not by natural laws, but by the needs of information users.

4-2

Using Horizontal Financial Statements Models

By now your students should understand a direct approach to explaining how accounting

events affect financial statements. You should use the horizontal financial statements model

whenever it serves your purposes. You may want to use a condensed version of the model.

For example, students should be familiar enough with financial statements to no longer need

statement labels in the model. Also, you may prefer to show net income effects in a single

column. An abbreviated statements model is shown below.

Assets

=

Liabilities

+

Equity

Net Income

Cash Flow

Alter the model as needed to make the points you are teaching. The model’s explanatory

power comes from recording individual events directly into financial statements that are vis-

ually adjacent to one another. So long as these features are retained, the model can be ex-

pressed in various levels of detail. It is a teaching tool. It is not a formal financial statement

presentation. You therefore have considerable latitude with the format of statements models.

You can use the horizontal financial statements model in conjunction with T-accounts.

Show the effects of events on statements before you show how the entries are recorded in T–

accounts or vice versa. Again, you should select the approach that best meets your teaching

objectives. Some instructors use the model extensively. Others use it sparingly. The text

supports whatever approach you find the most effective.

Detailed Outline of a Lesson Plan for Chapter 4

I. Define merchandise inventory as goods purchased for resale to customers, then

distinguish product costs from selling and administrative costs. Explain that

product costs are first accumulated in inventory accounts and then expensed when the

products are sold regardless of when the costs were initially incurred. In contrast,

selling and administrative costs are usually, though not always, expensed in the peri-

od in which they are incurred. Since selling and administrative costs are usually

matched with the period in which they are incurred, they are frequently called period

costs.

II. Sketch adjacent income statements on the board to contrast service businesses

and merchandising businesses. Explain that merchandising companies have the

same types of expenses as service companies (salaries, utilities, advertising), but un-

like service companies, merchandising companies also have cost of goods sold. In-

troduce the multistep income statement by showing the subtotal for gross margin (net

sales minus cost of goods sold) before subtracting period expenses. Initially, avoid

more advanced topics such as accounting for returns, allowances, discounts, and

freight. Introduce these topics after the students understand the basic events illustrat-

ed in Demonstration Problem 4-1.

4-3

III. Work Demonstration Problem 4-1. This problem is so simple; you can write each

transaction on the board one step at a time. Allow students time to record each event

in the horizontal financial statements model. Show them the answer before moving

on to the next transaction. The problem, solution, and workpapers are available if

you desire to duplicate them for your students. Depending on how much you wish to

emphasize recording procedures, you may have your students record the transactions

in general journal format and then post the information into T-accounts.

The requirements call only for preparing an income statement and a balance sheet.

The statement of changes in stockholders’ equity and the statement of cash flows are

not required. By this point, students should be familiar enough with statement prepa-

ration that continual reinforcement is no longer necessary. The effects of events on

statements are easily reinforced through the horizontal financial statements model.

Instead of requiring a full set of formal statements each time you or students work a

problem, require only the relevant ones. In this problem the income statement is re-

quired because it appears in a new format (multistep). Students should also see how

inventory is reported on the balance sheet.

Use the horizontal financial statements model to demonstrate the cash flow effects.

Emphasize that although the company paid $4,500 cash for inventory, only $3,500 of

that cost was charged to cost of goods sold. The remaining amount of product cost

($1,000) is reported as inventory on the balance sheet. This illustration demonstrates

that product costs are expensed in the period in which inventory is sold regardless of

when cash for it is paid.

IV. Demonstration Problem 4-2 provides a platform for explaining such advanced

topics as returns, allowances, cash discounts, and freight costs. Work the problem

in steps, explaining each topic as it arises in the problem. Event No. 2 introduces

cash discount terms. Explain the meaning of 2/10, n/30. Event No. 3 involves freight

costs. At this point you should explain FOB shipping point and FOB destination.

The event invites you to introduce the general topic of freight costs, going beyond the

specific freight transaction described in the problem. Draw pictures! Put rectangles

horizontally across the board representing a supplier, the merchandising company,

and a customer. Draw trucks traveling between the companies. Explain to your stu-

dents that we are viewing all inventory transactions from the merchandising compa-

ny’s point of view. Help students see that transactions between the merchandising

company and its suppliers are purchases, though from the supplier’s point of view

they are sales. In this way your explanation flows from the problem. Use Event No.

4 to introduce purchase returns and allowances. With this approach, you will explain

sales and purchase returns and allowances, cash discounts, and freight costs by the

time you have finished Demonstration Problem 4-2.

V. Explain that failing to pay for purchases within the discount period increases the

actual cost of the inventory. Refer to the payment LDS made in Event No. 5 of

Demonstration Problem 4-2. If LDS had paid after the discount period expired, it

4-4

would have owed the supplier $50,000 (list price of $54,000 purchase – list price of

$4,000 purchase return), not $49,000. The payment would have been recorded as fol-

lows:

Cash

+

Accts.

Receiv.

+

Inventory

=

Accts.

Payable

+

Com.

Stock

+

Ret. Earn.

(5) Pay Acct. Payable

(50,000)

(50,000)

VI. If you plan to include the appendix material, use Demonstration Problem 4-3 to

introduce the periodic inventory method. This problem uses the same transactions

as Demonstration Problem 4-2, illustrating that either of two different accounting

methods can be used to record the same data. Prepare a schedule of cost of goods

sold. Compare the amount of cost of goods sold in the schedule with the amount of

cost of goods sold determined using the perpetual method. You may limit your dis-

cussion to this comparison, or you may go further by requiring your students to pre-

pare journal entries using the periodic method. Ask your students to prepare a set of

financial statements using the periodic method. Chances are few of them will realize

that the statements resulting from the periodic method are identical to the statements

resulting from the perpetual method. We usually let them finish the income statement

before stopping them. Preparing at least one comparative statement demonstrates that

the two methods are alternative approaches to the same end.

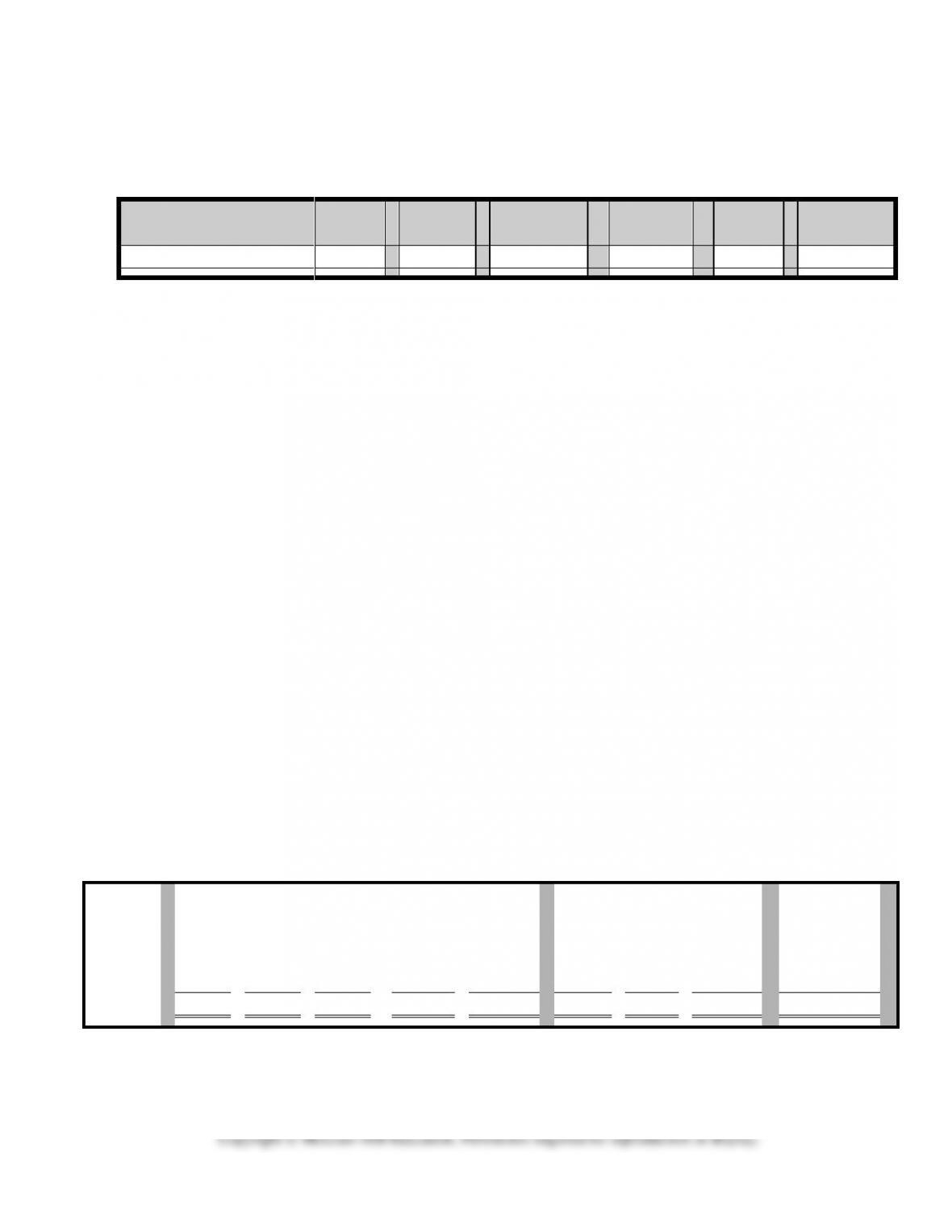

VII. Discuss accounting for lost, damaged, or stolen merchandise. Illustrate by asking

your students to return to Demonstration Problem 4-2. Suppose a physical count

establishes that only $9,000 of inventory is actually on hand at the end of the account-

ing period. Recall that the balance in the inventory account at the end of the period

was $10,800. Have students explain how the $1,800 loss would affect the financial

statements by recording the event in a statements model like shown below. The

“Balances” row displays the amounts in various columns after recording all of the

Demonstration Problem 4-2 transactions. Expenses are shown as one single total

($39,200 + $1,200 + $9,600 = $50,000). These balances agree with the financial

statements solution for Demonstration Problem 4-2. The row labeled “Inv. Loss”

demonstrates the effects of the inventory loss on the financial statements. The “To-

tals” row displays the balances after recognizing the inventory loss.

Assets

=

Claims

Rev.

–

Exp.

=

Net Inc.

Cash Flow

Cash

+

Accts.

Rec.

+

Inv.

=

Com.

Stk.

+

Ret.

Earn.

Balances

48,700

+

14,000

+

10,800

=

60,000

+

13,500

63,500

–

50,000

=

13,500

48,700 NC

Inv. Loss

0

+

0

+

(1,800)

=

0

+

(1,800)

0

–

1,800

=

(1,800)

0

Totals

48,700

+

14,000

+

9,000

=

60,000

+

11,700

63,500

–

51,800

=

11,700

48,700 NC

4-5

VIII. Time considerations and homework assignments. Allot approximately two hours

of class time for Chapter 4. Exercises 4-1A or B and 4-2A or B reinforce the con-

cepts in Demonstration Problem 4-1. Exercises 4-10A and B show the effects of pur-

chase returns and cash discounts. Exercises 4-15A and B contrast single and multi-

step income statements. Problems 4-27A and B provide comprehensive follow-up of

Demonstration Problem 4-2, including a write-down for lost inventory. Problems 4-

28A and B focus on preparing financial statements using the periodic method.

IX. Enrichment. By now you are familiar with the types of cases included at the end of

each chapter. You probably have a preference consistent with your personal objec-

tives. We leave to your judgment the most appropriate form of enrichment. You may

also choose to use the study guide, computer tutorials, or other supplements that ac-

company the text.

4-6

Demonstration Problem 4-1 – Inventory Purchase/Sale, Perpetual

Method

The following events pertain to Jefferson Hardware Store. Jefferson uses the perpetual in-

ventory method.

1. Jefferson Hardware was started on January 1, 2015 when it acquired $5,000 cash by is-

suing common stock.

2. The store paid $4,500 cash to purchase inventory.

3. Jefferson sold for $6,000 cash inventory that cost $3,500.

4. During 2015, the store paid $2,000 cash for operating expenses.

Required

Record the events using the horizontal financial statements model. Prepare a formal income

statement and a balance sheet.

4-7

Demonstration Problem 4-2 – Perpetual Inventory Transactions

Lisa’s Dress Supply (LDS), a garment wholesaler, experienced the following events in 2015,

its first year of operations. LDS uses the perpetual inventory method.

1. LDS was started when it issued common stock for $60,000 cash.

2. LDS purchased on account inventory with a list price of $54,000. Payment terms were

2/10, n/30. LDS records inventory transactions at the gross amount.

3. The freight terms for the merchandise delivered in Event No. 2 were FOB shipping

point. LDS paid the freight cost of $1,000 in cash.

4. An inspection revealed that merchandise with a list price of $4,000 purchased in Event

No. 2 was defective. LDS returned this merchandise to its supplier for credit.

5. LDS paid within the discount period for the inventory purchased in Event No. 2.

6. LDS sold inventory to various retail store customers on account. LDS offers customers

payment terms of 1/15, n/30. The list price for the sales was $68,000. The cost of the

inventory sold was $42,140.

7. Customers returned some goods LDS had sold in Event No. 6. The goods had been sold

for a list price of $4,000 and had a cost of $2,940.

8. LDS paid in cash freight cost of $1,200 for goods delivered to customers FOB destina-

tion.

9. LDS collected cash from customers who paid their balances of LDS accounts receivable

having a list price of $50,000, within the 15-day discount period.

10. LDS paid $9,600 in cash for other operating expenses.

Required

Record the events under an accounting equation, and prepare an income statement, a balance

sheet, and a statement of cash flows.

Demonstration Problem 4-3 – Periodic Inventory Transactions

(Appendix)

Assume Lisa’s Dress Supply uses the periodic rather than the perpetual inventory method.

LDS determined by physical count there was $10,800 of inventory on hand at the end of

2015.

Required

Record the events in Demonstration Problem 4-2 in general journal form. Include an adjust-

ing entry to summarize cost of goods sold, and then prepare closing entries. Prepare a sched-

ule of cost of goods sold. Prepare an income statement, a balance sheet, and a statement of

cash flows assuming that LDS uses the periodic inventory method.

4-8

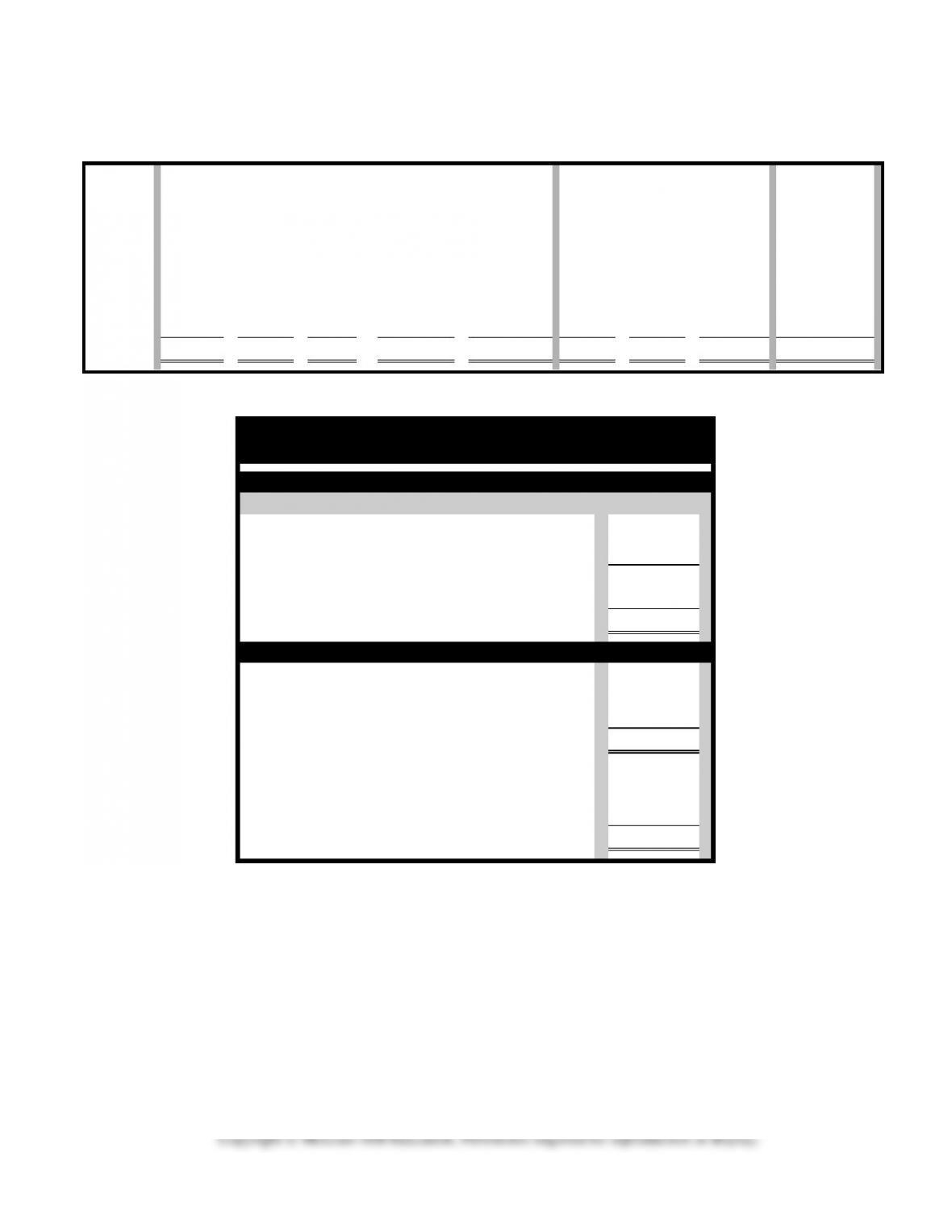

Demonstration Problem 4-1 Solution

Assets

=

Liab.

+

Equity

Rev.

–

Exp.

=

Net Inc.

Cash Flow

No.

Cash

+

Inven.

=

Liab.

+

Com. Stk.

+

Ret. Earn.

Beg. bal.

-0-

+

0

=

0

+

0

+

0

0

–

0

=

0

0

1

5,000

+

0

=

0

+

5,000

+

0

0

–

0

=

0

5,000 FA

2

(4,500)

+

4,500

=

0

+

0

+

0

0

–

0

=

0

(4,500) OA

3(a)

6,000

+

0

=

0

+

0

+

6,000

6,000

–

0

=

6,000

6,000 OA

3(b)

0

+

(3,500)

=

0

+

0

+

(3,500)

0

–

3,500

=

(3,500)

0

4

(2,000)

+

0

=

0

+

0

+

(2,000)

0

–

2,000

=

(2,000)

(2,000) OA

Totals

4,500

+

1,000

=

0

+

5,000

+

500

6,000

–

5,500

=

500

4,500 NC

Jefferson Hardware Store

Financial Statements

Income Statement

For the Year Ended December 31,

2015

Sales

$6,000

Cost of goods sold (product cost)

(3,500)

Gross margin

2,500

Operating expenses (period cost)

(2,000)

Net income

$ 500

Balance Sheet as of December 31

Assets

Cash

$4,500

Inventory

1,000

Total assets

$5,500

Stockholders’ equity

Common stock

$5,000

Retained earnings

500

Total stockholders’ equity

$5,500

4-9

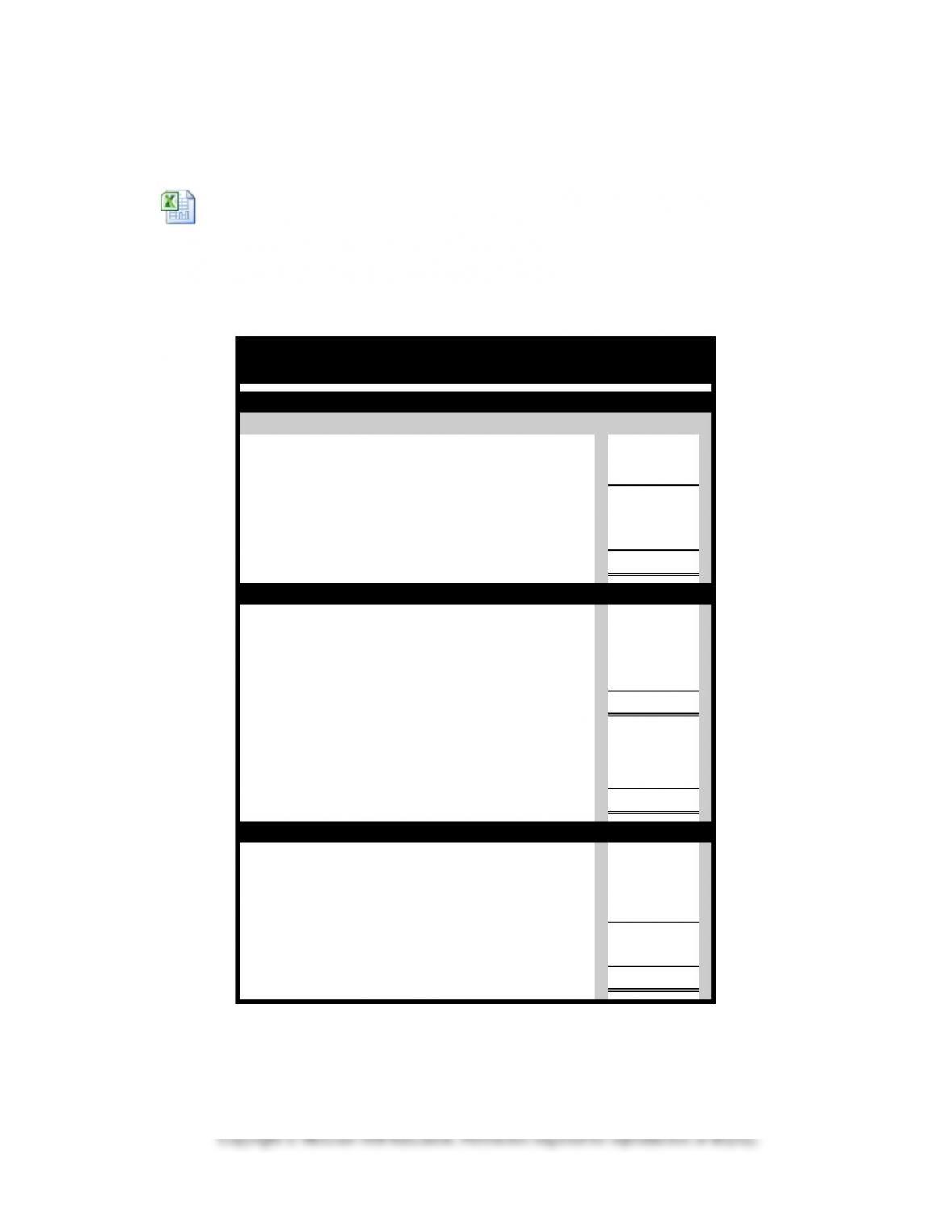

Demonstration Problem 4-2 Solution

Worksheet Edmonds

FFAC9e Ch 4 IM.xlsx

Demonstration Problem 4-2 Solution Financial Statements

Lisa’s Dress Supply

Financial Statements

Income Statement

For the Year Ended December 31,

2015

Net sales

$63,500

Cost of goods sold (product cost)

(39,200)

Gross margin

24,300

Transportation-out (period cost)

(1,200)

Other operating expenses (period cost)

(9,600)

Net income

$13,500

Balance Sheet at December 31

Assets

Cash

$48,700

Accounts receivable

14,000

Inventory

10,800

Total assets

$73,500

Stockholders’ equity

Common stock

$60,000

Retained earnings

13,500

Total stockholders’ equity

$73,500

Statement of Cash Flows

Net cash flow from operating activities1

$(11,300)

Net cash flow from investing activities

0

Net cash flow from financing activities

60,000

Net change in cash

48,700

Beginning cash balance

0

Ending cash balance

$48,700

1Net cash flow from operating activities: $49,500 inflow from revenue less outflows of

$1,000 for transportation-in, $49,000 for payments of accounts payable, $1,200 for trans-

4-10

portation-out, and $9,600 for other operating expenses [$49,500 Ä $1,000 – $49,000 –

$1,200 – $9,600 = ($11,300)].

Copyright © McGraw-Hill Education. Permission required for reproduction or display.

4-11

Demonstration Problem 4-3 Solution

Date

Account Titles

Debit

Credit

Event No.

1

Cash

60,000

Common Stock

60,000

Event No.

2

Purchases

54,000

Accounts Payable

54,000

Event No.

3

Transportation-in

1,000

Cash

1,000

Event No.

4

Accounts Payable

4,000

Purchase Returns and Allowances

4,000

Event No.

5a

Accounts Payable

1,000

Purchase Discounts

1,000

Event No.

5b

Accounts Payable

49,000

Cash

49,000

Event No.

6

Accounts Receivable

68,000

Sales

68,000

Event No.

7

Sales Returns and Allowances

4,000

Accounts Receivable

4,000

Event No.

8

Transportation-out

1,200

Cash

1,200

Event No.

9a

Sales Discounts

500

Accounts Receivable

500

Event No.

9b

Cash

49,500

Accounts Receivable

49,500

Event No.

10

Other Operating Expenses

9,600

Cash

9,600

Adjusting

Cost of Goods Sold

39,200

Inventory

10,800

Purchase Returns and Allowances

4,000

Purchase Discounts

1,000

Purchases

54,000

Transportation-in

1,000

Closing

Sales

68,000

Sales Returns and Allowances

4,000

Sales Discounts

500

Cost of Goods Sold

39,200

Transportation-out

1,200

Other Operating Expenses

9,600

Retained Earnings

13,500