8-38

EXERCISE 8-14A

a. MACRS depreciation = Cost x MACRS Table %

EXERCISE 8-15A

Depreciation

Expense

2016: $42,000 − $3,000 = $39,000; $39,000 3 = $13,000

8-39

EXERCISE 8-16A

Tow Truck:

Book value would still be $6,500; the $1,550 repair cost will be

expensed.

8-40

EXERCISE 8-17A

a.

Assets

=

Stockholders’ Equity

Rev.

–

Exp.

=

Net Inc.

Cash Flow

Cash

+

Book Value of Comp

=

C. Stock

+

Ret. Ear.

45,000

+

16,000

=

40,000

+

21,000

NA

−

NA

=

NA

NA

(6,000)

+

NA

=

NA

+

(6,000)

NA

−

6,000

=

(6,000)

(6,000) OA

Assets

=

Stockholders’ Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

Cash

+

Book Value of Comp

=

C. Stock

+

Ret. Ear.

45,000

+

16,000

=

40,000

+

21,000

NA

−

NA

=

NA

NA

(6,000)

+

6,000

=

NA

+

NA

NA

−

NA

=

NA

(6,000) IA

Assets

=

Stockholders’ Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

Cash

+

Book Value of Comp

=

C. Stock

+

Ret. Ear.

45,000

+

16,000

=

40,000

+

21,000

NA

−

NA

=

NA

NA

(6,000)

+

6,000

=

NA

+

NA

NA

−

NA

=

NA

(6,000) IA

8-41

EXERCISE 8-18A

2017.

b. $22,000 of expense would be recognized in 2016 and $-0- in 2017.

c. $-0- cash outflow from operating activities in 2016, $-0- cash outflow

2017.

8-42

EXERCISE 8-19A

a. Depletion charge per unit: $600,000 40,000 tons = $15 per ton

b.

Depletion Calculation:

Year 1 $15 x 15,000 = $225,000

Year 2 $15 x 18,000 = $270,000

Colorado Mining Co.

Statements Model

Assets

=

Stockholders’ Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

Cash

+

Coal Res.

=

C. Stock

+

Ret. Ear.

800,000

+

NA

=

800,000

+

NA

NA

−

NA

=

NA

NA

(600,000)

+

600,000

=

NA

+

NA

NA

−

NA

=

NA

(600,000) IA

Depletion for Year 1

NA

+

(225,000)

=

NA

+

(225,000)

NA

−

225,000

=

(225,000)

NA

Depletion for Year 2

NA

+

(270,000)

=

NA

+

(270,000)

NA

−

270,000

=

(270,000)

NA

c.

Date

Account Titles

Debit

Credit

Year 1

Depletion Expense

225,000

Coal Reserves

225,000

Date

Account Titles

Debit

Credit

Year 2

Depletion Expense

270,000

Coal Reserves

270,000

EXERCISE 8-20A

a. Patent $40,000 4 = $10,000 per year

The goodwill is not amortized under GAAP.

b.

Dynamo Manufacturing

Statements Model

Assets

Liab.

+

Equity

Rev.

–

Exp.

=

Net Inc.

Cash Flow

Cash

+

Patent

+

Goodwill

=

90,000

NA

NA

NA

90,000

NA

NA

NA

NA

Acq.

(75,000)

40,000

35,000

NA

NA

NA

NA

NA

(75,000) IA

Amort

.

NA

(10,000)

NA

NA

(10,000)

10,000

(10,000)

NA

c.

Account Titles

Debit

Credit

Patents

40,000

Goodwill

35,000

Cash

75,000

Account Titles

Debit

Credit

Amortization Expense – Patents

10,000

Patents

10,000

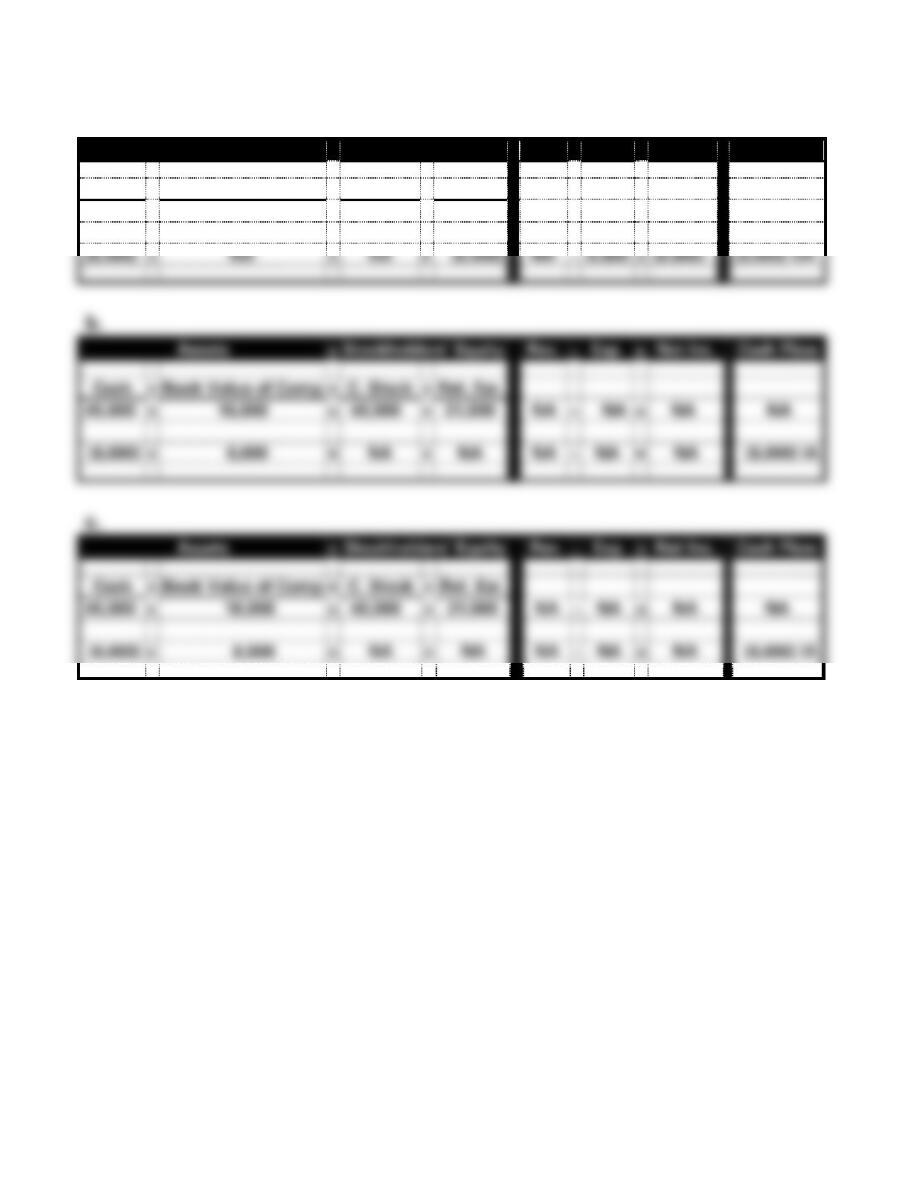

EXERCISE 8-21A

a. Acquisition Price:

Cash Paid $320,000

Liabilities Assumed 40,000

8-10

Cash

320,000

8-11

EXERCISE 8-22A

a. U.S. GAAP requires research and development cost to be expensed in

8-12

EXERCISE 8-23A

a. Under U.S. GAAP, the land would be reported at its original cost of

$600,000. The building would be reported at its book value,

determined as follows:

8-13

EXERCISE 8-23A (cont.)

c. Under IFRS, the land would be reported on the 2017 balance sheet at

$600,000, and on the 2018 balance sheet at $650,000.

The building would be reported at its book value of $2,850,000 in

2017; (see the computations for U.S. GAAP above). For 2018 the

2018. See computations above.

8-14

SOLUTIONS TO PROBLEMS – SERIES A – CHAPTER 8

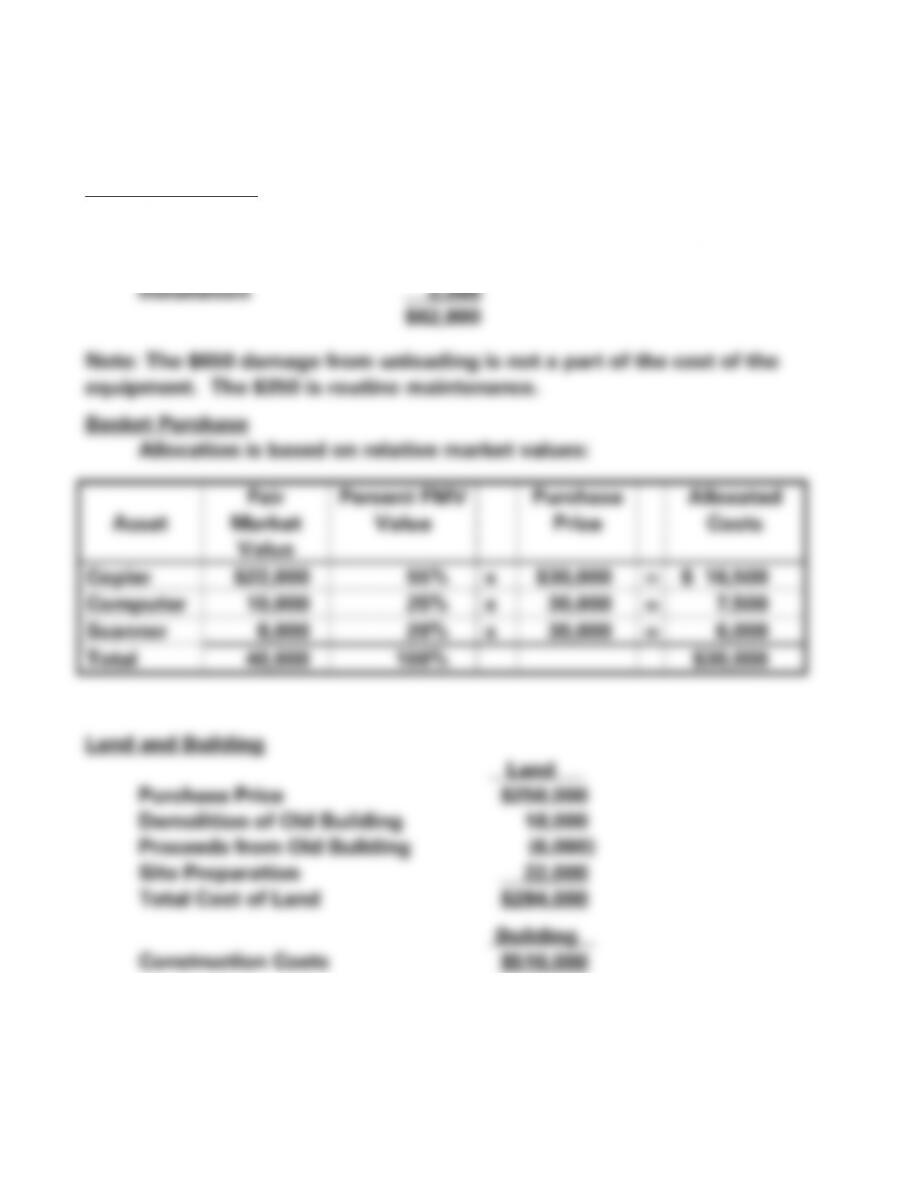

PROBLEM 8-24A

Office Equipment

List Price $60,000

Discount ($60,000 x 2%) (1,200)

Transportation-In 1,500

8-15

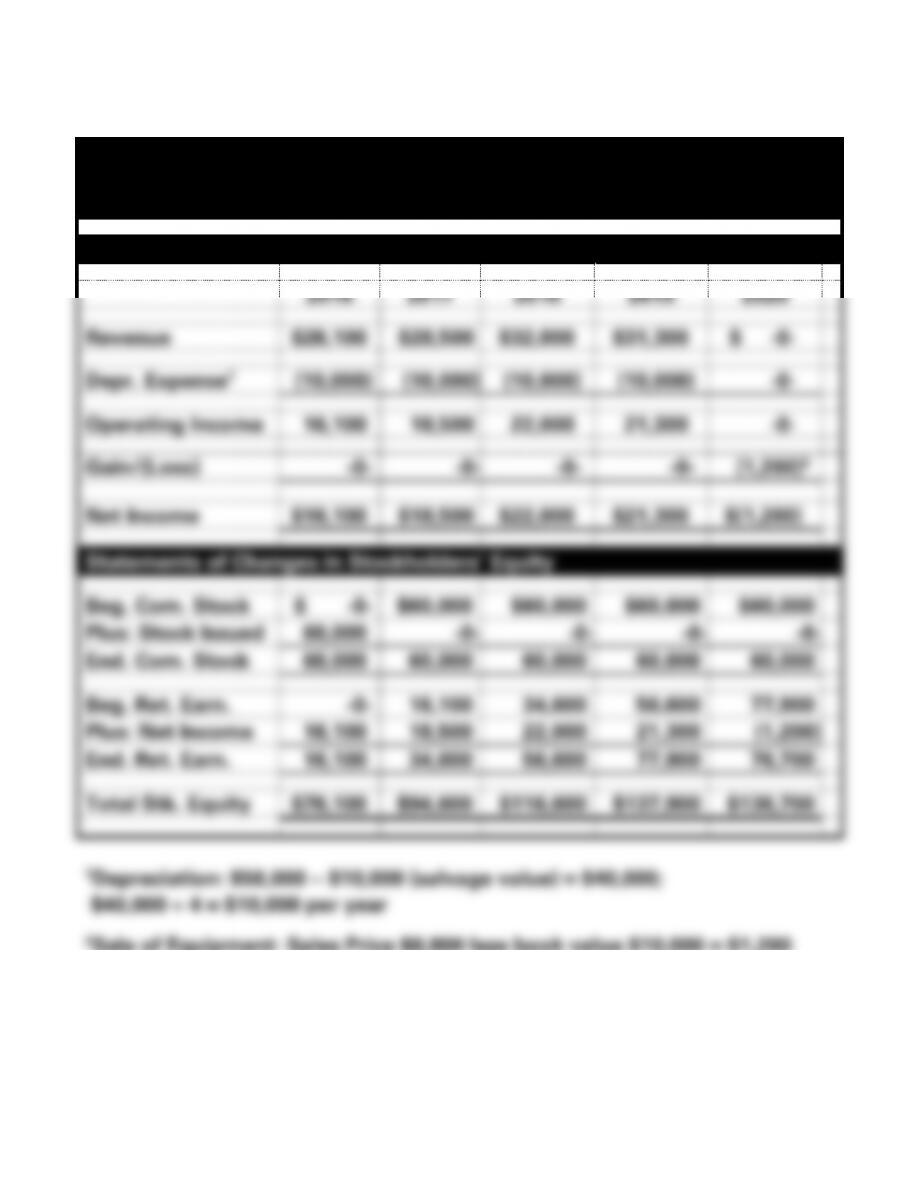

PROBLEM 8-25A

Bensen Company

Financial Statements

For the Year Ended December 31

Income Statements

2016

2017

2018

2019

2020

Revenue

$26,100

$28,500

$32,000

$31,300

$ -0-

Depr. Expense1

(10,000)

(10,000)

(10,000)

(10,000)

-0-

Operating Income

16,100

18,500

22,000

21,300

-0-

Gain/(Loss)

-0-

-0-

-0-

-0-

(1,200)2

Net Income

$16,100

$18,500

$22,000

$21,300

$(1,200)

Statements of Changes in Stockholders’ Equity

Beg. Com. Stock

$ -0-

$60,000

$60,000

$60,000

$60,000

Plus: Stock Issued

60,000

-0-

-0-

-0-

-0-

End. Com. Stock

60,000

60,000

60,000

60,000

60,000

Beg. Ret. Earn.

-0-

16,100

34,600

56,600

77,900

Plus: Net Income

16,100

18,500

22,000

21,300

(1,200)

End. Ret. Earn.

16,100

34,600

56,600

77,900

76,700

Total Stk. Equity

$76,100

$94,600

$116,600

$137,900

$136,700

loss

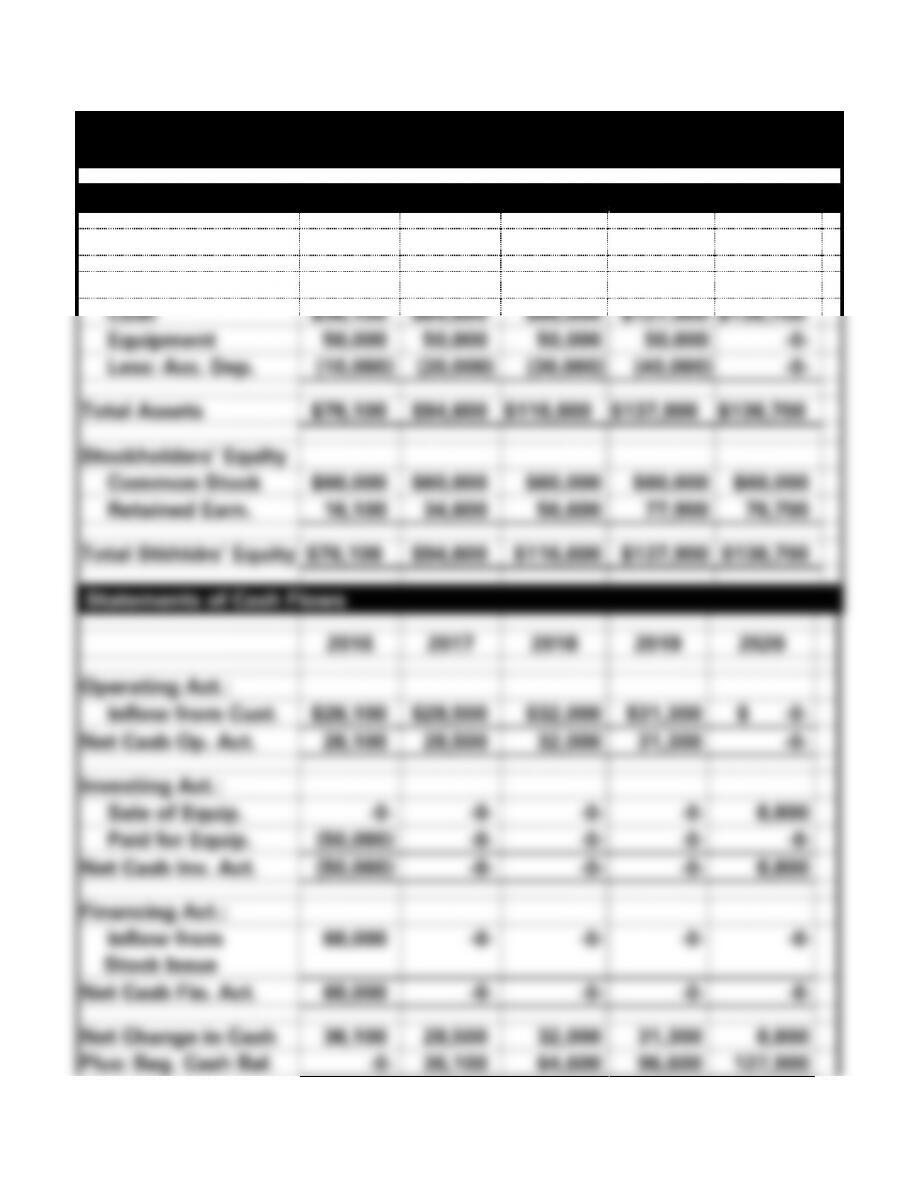

PROBLEM 8-25A (cont.)

Bensen Company

Financial Statements

Balance Sheets

2016

2017

2018

2019

2020

Assets

Cash

$36,100

$64,600

$96,600

$127,900

$136,700

Equipment

50,000

50,000

50,000

50,000

-0-

Less: Acc. Dep.

(10,000)

(20,000)

(30,000)

(40,000)

-0-

Total Assets

$76,100

$94,600

$116,600

$137,900

$136,700

Stockholders’ Equity

Common Stock

$60,000

$60,000

$60,000

$60,000

$60,000

Retained Earn.

16,100

34,600

56,600

77,900

76,700

Total Stkhldrs’ Equity

$76,100

$94,600

$116,600

$137,900

$136,700

Statements of Cash Flows

2016

2017

2018

2019

2020

Operating Act.:

Inflow from Cust.

$26,100

$28,500

$32,000

$31,300

$ -0-

Net Cash Op. Act.

26,100

28,500

32,000

31,300

-0-

Investing Act.:

Sale of Equip.

-0-

-0-

-0-

-0-

8,800

Paid for Equip.

(50,000)

-0-

-0-

-0-

-0-

Net Cash Inv. Act.

(50,000)

-0-

-0-

-0-

8,800

Financing Act.:

Inflow from

Stock Issue

60,000

-0-

-0-

-0-

-0-

Net Cash Fin. Act.

60,000

-0-

-0-

-0-

-0-

Net Change in Cash

36,100

28,500

32,000

31,300

8,800

Plus: Beg. Cash Bal.

-0-

36,100

64,600

96,600

127,900

8-17

Ending Cash Bal.

$36,100

$64,600

$96,600

$127,900

$136,700

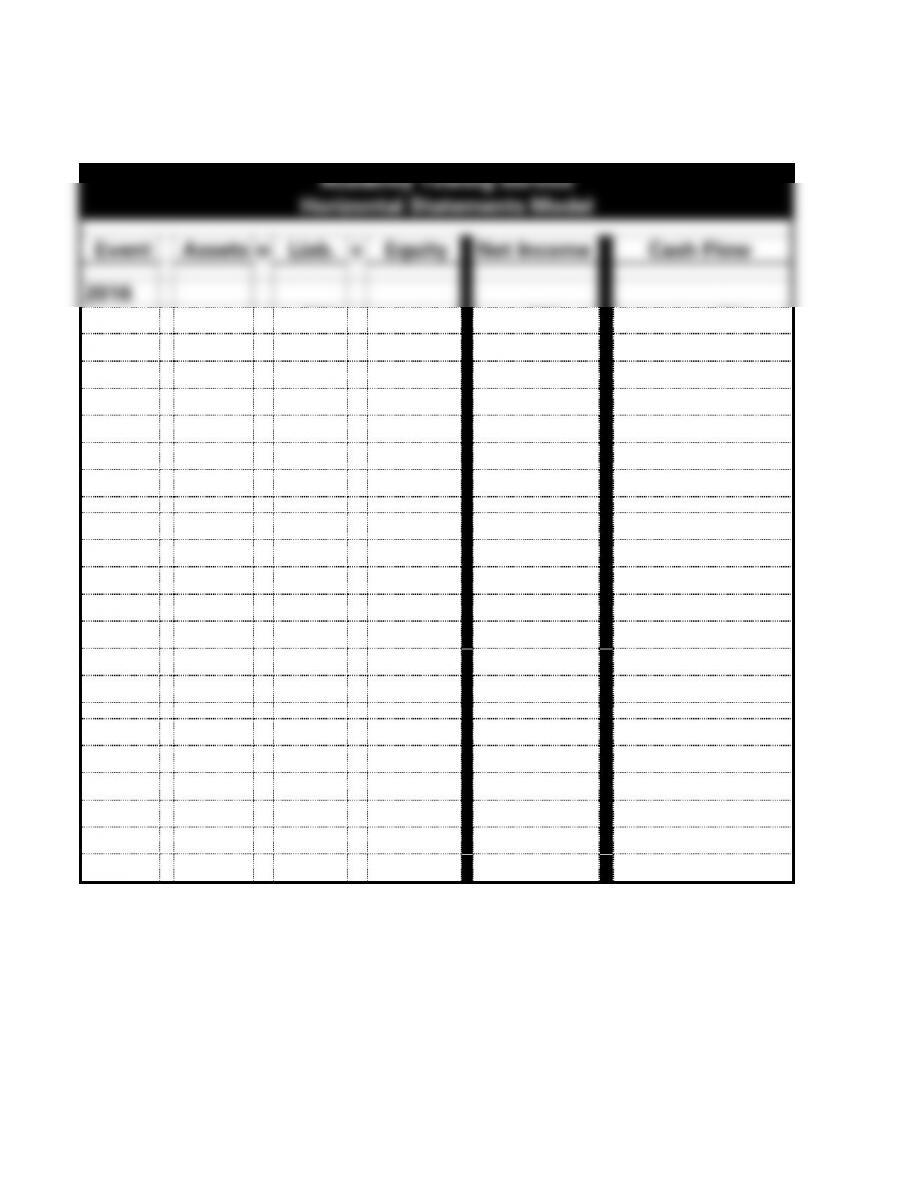

PROBLEM 8-26A

a.

Academy Towing Service

Horizontal Statements Model

Event

Assets

=

Liab.

+

Equity

Net Income

Cash Flow

2016

1.

+

NA

+

NA

+ FA

2.

+−

NA

NA

NA

− IA

3.

+−

NA

NA

NA

− IA

4.

+

NA

+

+

+ OA

5.

−

NA

−

−

− OA

6.

−

NA

−

−

NA

7.

NA

NA

+−

NA

NA

2017

1.

−

NA

−

−

− OA

2.

−

NA

−

−

− OA

3.

+

NA

+

+

+ OA

4.

−

NA

−

−

− OA

5.

−

NA

−

−

NA

6.

NA

NA

+−

NA

NA

2018

1.

+−

NA

NA

NA

− IA

2.

−

NA

−

−

− OA

3.

+

NA

+

+

+ OA

4.

−

NA

−

−

NA

5.

NA

NA

+−

NA

NA

8-19

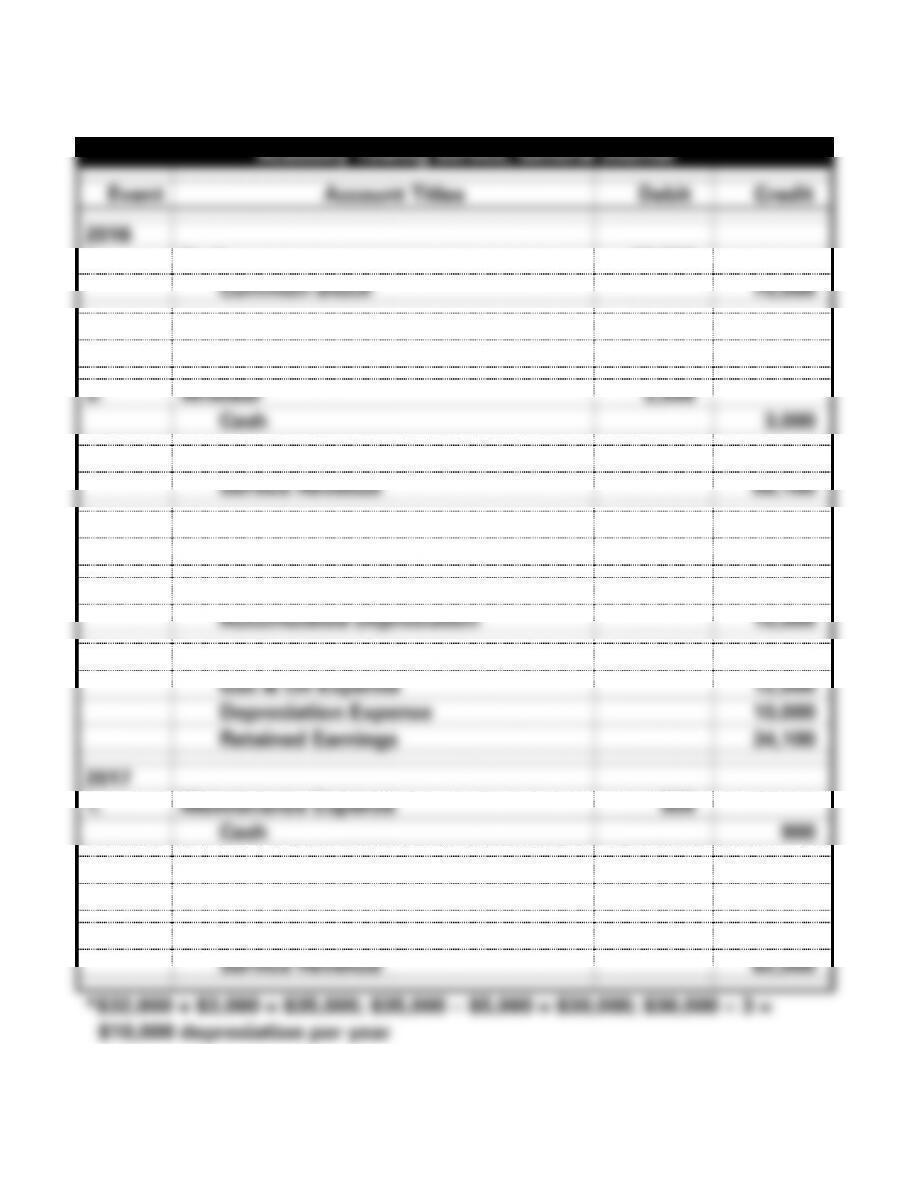

PROBLEM 8-26A (cont.)

b.

Academy Towing Service, General Journal

Event

Account Titles

Debit

Credit

2016

1.

Cash

70,000

Common Stock

70,000

2.

Wrecker

32,000

Cash

32,000

3.

Wrecker

3,000

Cash

3,000

4.

Cash

56,100

Service Revenue

56,100

5.

Gas & Oil Expense

12,000

Cash

12,000

6.

Depreciation Expense*

10,000

Accumulated Depreciation

10,000

7. cl

Service Revenue

56,100

Gas & Oil Expense

12,000

Depreciation Expense

10,000

Retained Earnings

34,100

2017

1.

Maintenance Expense

900

Cash

900

2.

Maintenance Expense

1,250

Cash

1,250

3.

Cash

62,000

Service Revenue

62,000

PROBLEM 8-26A b. (cont.)

Academy Towing Service

General Journal

Event

Account Titles

Debit

Credit

2017

4.

Gas & Oil Expense

18,000

Cash

18,000

5.

Depreciation Expense

10,000

Accumulated Depreciation

10,000

6. cl

Service Revenue

62,000

Maintenance Expense

2,150

Gas & Oil Expense

18,000

Depreciation Expense

10,000

Retained Earnings

31,850

2018

1.

Accumulated Depreciation

4,800

Cash

4,800

2.

Gas & Oil Expense

19,100

Cash

19,100

3.

Cash

65,000

Service Revenue

65,000

4.

Depreciation Expense*

7,400

Accumulated Depreciation

7,400

5. cl

Service Revenue

65,000

Gas & Oil Expense

19,100

Depreciation Expense

7,400

Retained Earnings

38,500

8-21

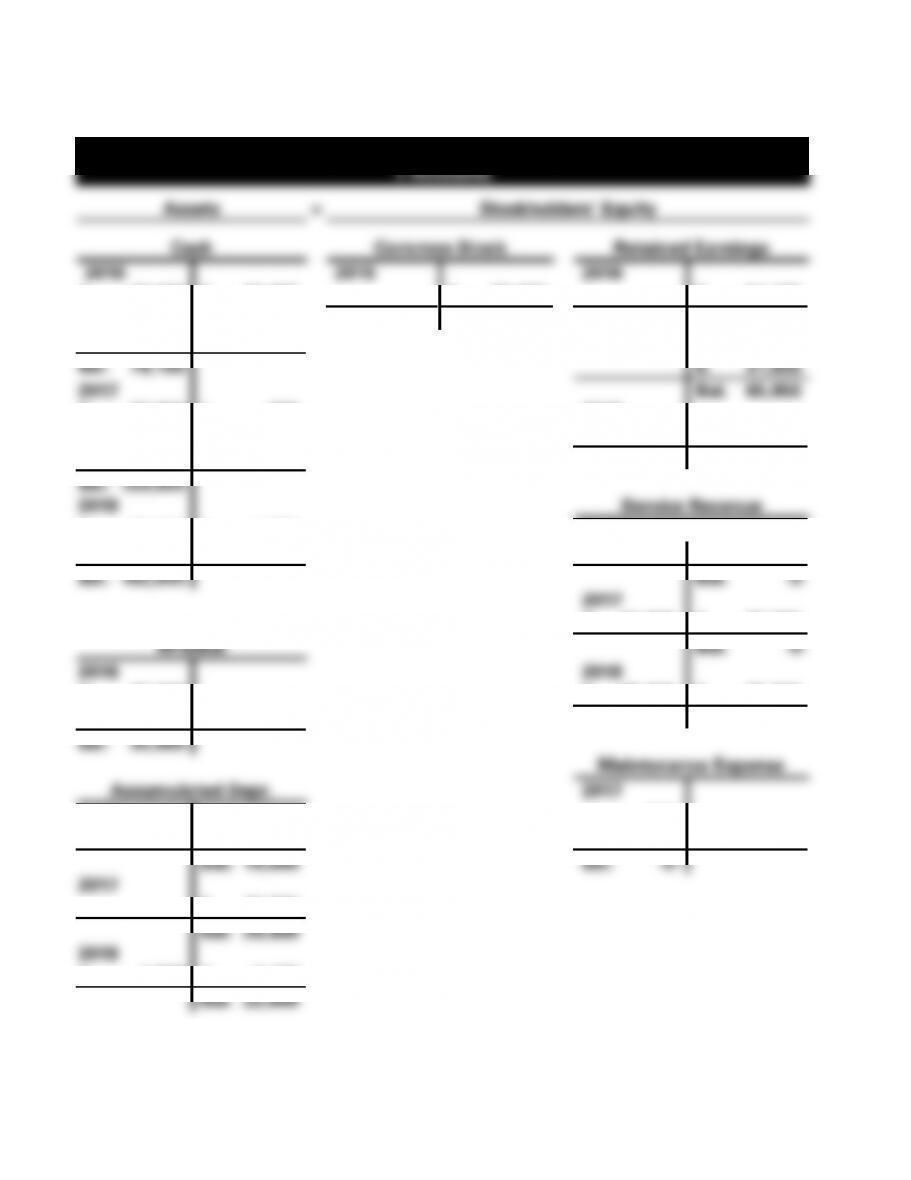

PROBLEM 8-26A b. (cont.)

Academy Towing Service

T-Accounts

Assets

=

Stockholders’ Equity

Cash

Common Stock

Retained Earnings

2016

2016

2016

1. 70,000

2. 32,000

1. 70,000

7. 34,100

4. 56,100

3. 3,000

Bal. 70,000

Bal. 34,100

5. 12,000

2017

Bal. 79,100

6. 31,850

2017

Bal. 65,950

3. 62,000

1. 900

2018

2. 1,250

5. 38,500

4. 18,000

Bal. 104,450

Bal. 120,950

2018

Service Revenue

3. 65,000

1. 4,800

2016

2. 19,100

7. 56,100

4. 56,100

Bal. 162,050

Bal. -0-

2017

6. 62,000

3. 62,000

Wrecker

Bal. -0-

2016

2018

2. 32,000

5. 65,000

3. 65,000

3. 3,000

Bal. -0-

Bal. 35,000

Maintenance Expense

Accumulated Depr.

2017

2016

1. 900

6. 10,000

2. 1,250

6. 2,150

Bal. 10,000

Bal. -0–

2017

5. 10,000

Bal. 20,000

2018

1. 4,800

4. 7,400

Bal. 22,600

8-22

PROBLEM 8-26A b. (cont.)

Academy Towing Service

T-Accounts

Assets

=

Stockholders’ Equity

Gas & Oil Expense

2016

5. 12,000

7. 12,000

Bal. -0–

2017

4. 18,000

6. 18,000

Bal. -0–

2018

2. 19,100

5. 19,100

Bal. -0–

Depreciation Expense

2016

6. 10,000

7. 10,000

Bal. -0–

2017

5. 10,000

6. 10,000

Bal. -0–

2018

4. 7,400

5. 7,400

Bal. -0–