11–24

EXERCISE 11-2A (cont.)

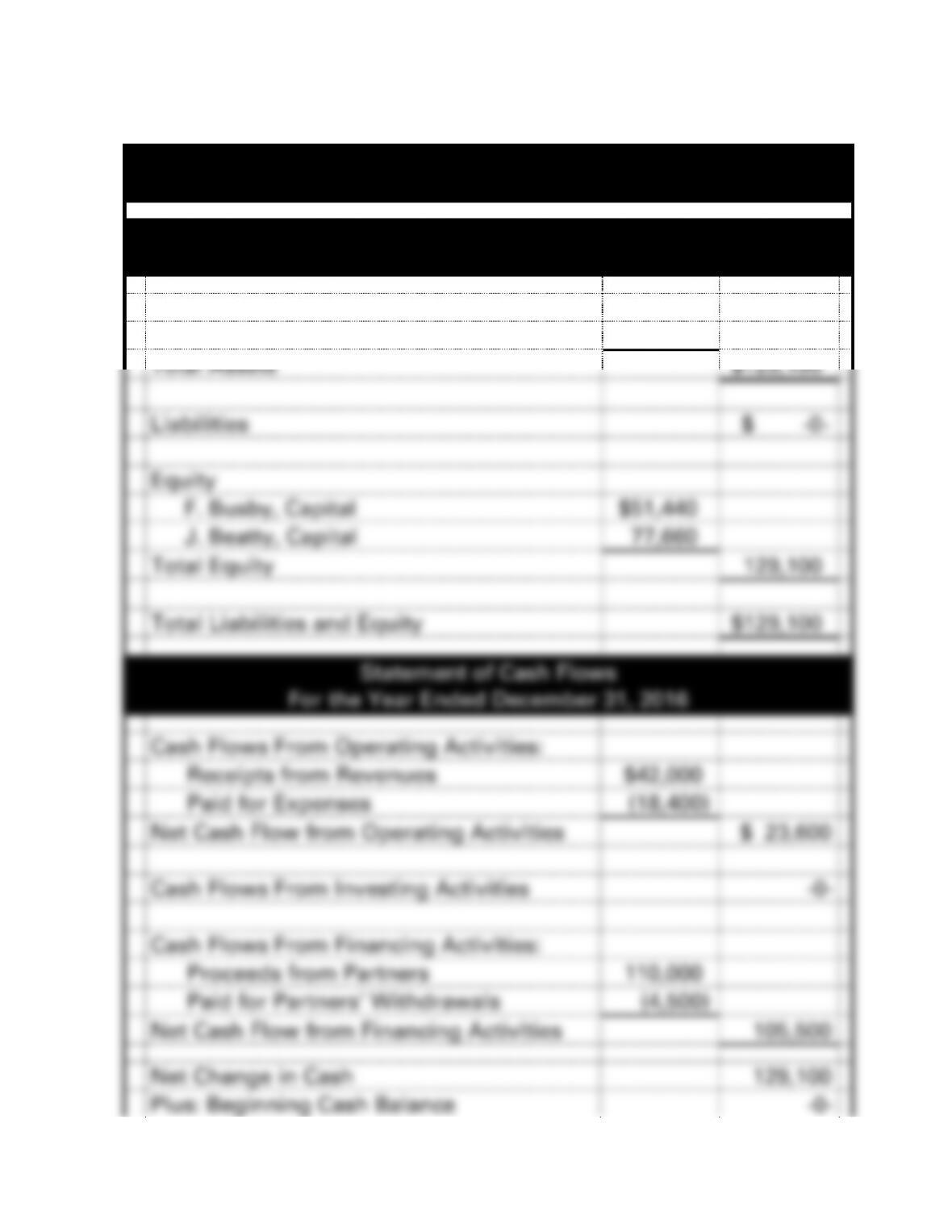

B&B Partnership

Financial Statements

Balance Sheet

As of December 31, 2016

Assets

Cash

$129,100

Total Assets

$129,100

Liabilities

$ -0-

Equity

F. Busby, Capital

$51,440

J. Beatty, Capital

77,660

Total Equity

129,100

Total Liabilities and Equity

$129,100

Statement of Cash Flows

For the Year Ended December 31, 2016

Cash Flows From Operating Activities:

Receipts from Revenues

$42,000

Paid for Expenses

(18,400)

Net Cash Flow from Operating Activities

$ 23,600

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities:

Proceeds from Partners

110,000

Paid for Partners’ Withdrawals

(4,500)

Net Cash Flow from Financing Activities

105,500

Net Change in Cash

129,100

Plus: Beginning Cash Balance

-0-

11–25

Ending Cash Balance

$129,100

11–26

EXERCISE 11-3A

Transactions:

Issued 2,000 shares of $5 par stock @ $12

$24,000

Revenues

31,000

Expenses

17,100

Dividends Paid

2,000

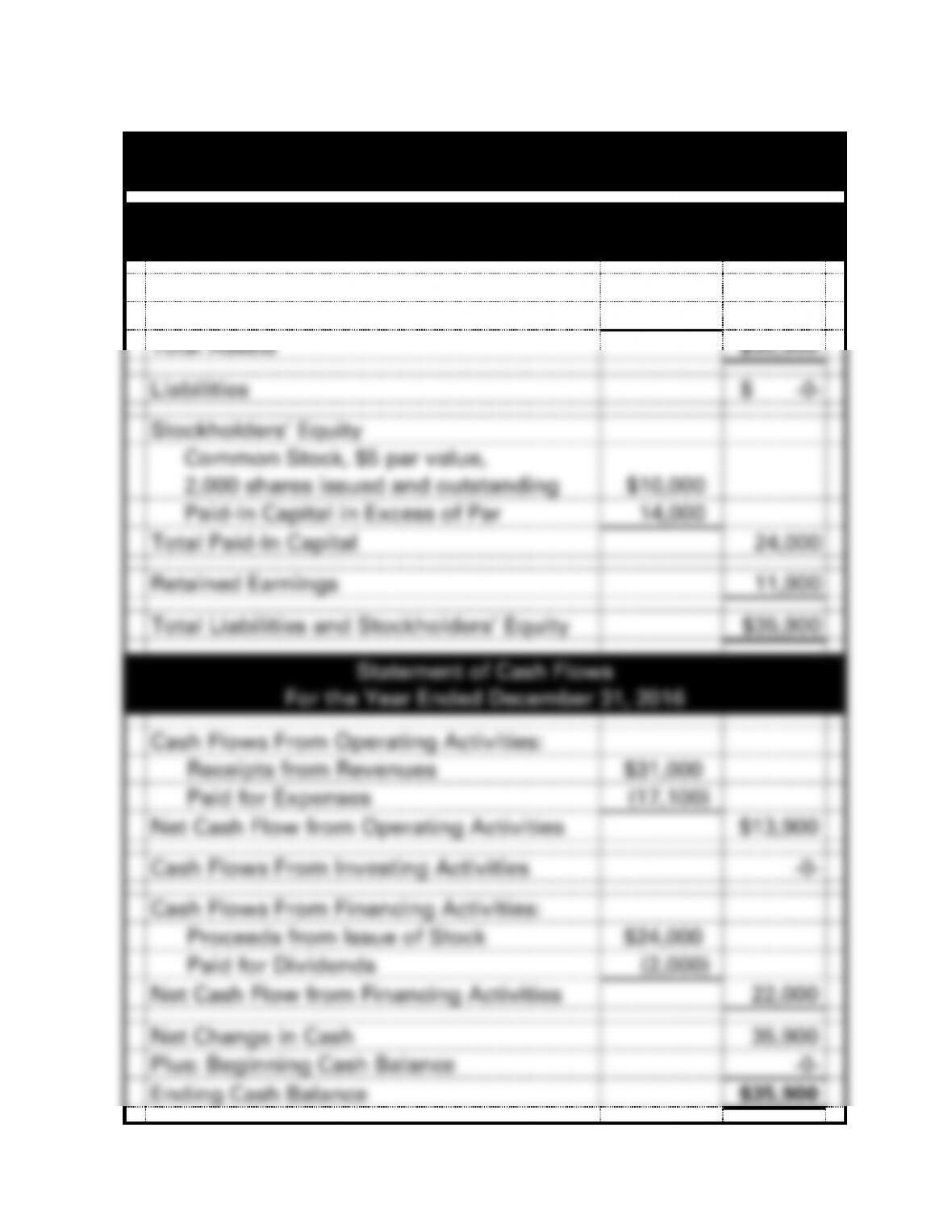

Astro Corporation

Financial Statements

For the Year Ended December 31, 2016

Income Statement

Revenues

$31,000

Expenses

(17,100)

Net Income

$13,900

Statement of Changes in Stockholders’ Equity

Beginning Common Stock

$ -0-

Plus: Issuance of Common Stock

24,000

Ending Common Stock

$24,000

Beginning Retained Earnings

-0-

Plus: Net Income

13,900

Less: Dividend

(2,000)

Ending Retained Earnings

11,900

Total Stockholders’ Equity

$35,900

11–27

EXERCISE 11-3A (cont.)

Astro Corporation

Financial Statements

Balance Sheet

As of December 31, 2016

Assets

Cash

$35,900

Total Assets

$35,900

Liabilities

$ -0-

Stockholders’ Equity

Common Stock, $5 par value,

2,000 shares issued and outstanding

$10,000

Paid-In Capital in Excess of Par

14,000

Total Paid-In Capital

24,000

Retained Earnings

11,900

Total Liabilities and Stockholders’ Equity

$35,900

Statement of Cash Flows

For the Year Ended December 31, 2016

Cash Flows From Operating Activities:

Receipts from Revenues

$31,000

Paid for Expenses

(17,100)

Net Cash Flow from Operating Activities

$13,900

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities:

Proceeds from Issue of Stock

$24,000

Paid for Dividends

(2,000)

Net Cash Flow from Financing Activities

22,000

Net Change in Cash

35,900

Plus: Beginning Cash Balance

-0-

Ending Cash Balance

$35,900

11–28

EXERCISE 11-4A

a.

Balance Sheet

Income Statement

Event

Assets

=

Liab

+

Stockholders’ Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

Cash

=

+

Com.

Stk.

+

PIC in

Excess

3/1

96,000

=

NA

+

60,000

+

36,000

NA

−

NA

=

NA

96,000 FA

5/2

180,000

=

NA

+

100,000

+

80,000

NA

−

NA

=

NA

180,000 FA

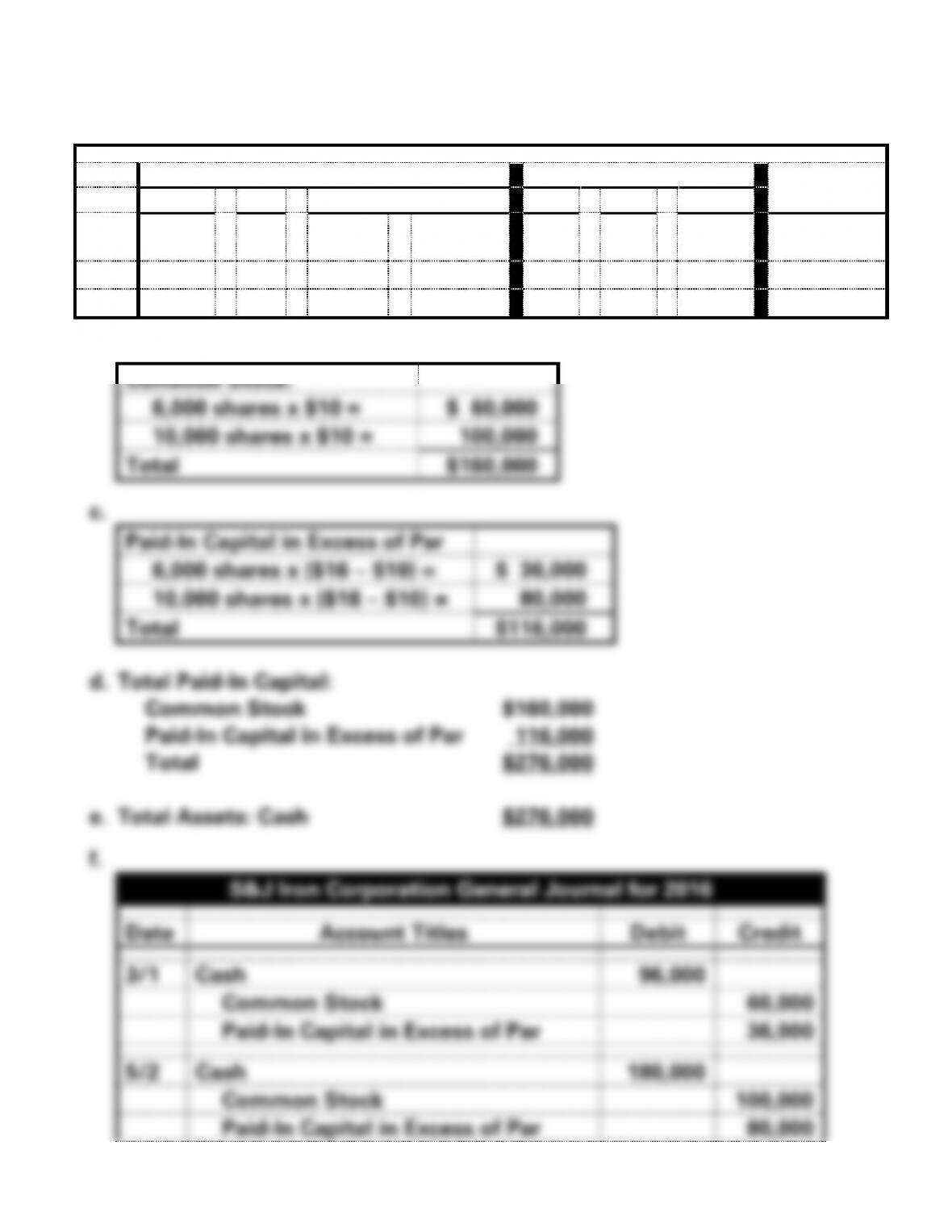

b.

Common Stock:

6,000 shares x $10 =

$ 60,000

10,000 shares x $10 =

100,000

Total

$160,000

c.

Paid-In Capital in Excess of Par

6,000 shares x ($16 − $10) =

$ 36,000

10,000 shares x ($18 − $10) =

80,000

Total

$116,000

d. Total Paid-In Capital:

Common Stock $160,000

Paid-In Capital in Excess of Par 116,000

Total $276,000

e. Total Assets: Cash $276,000

f.

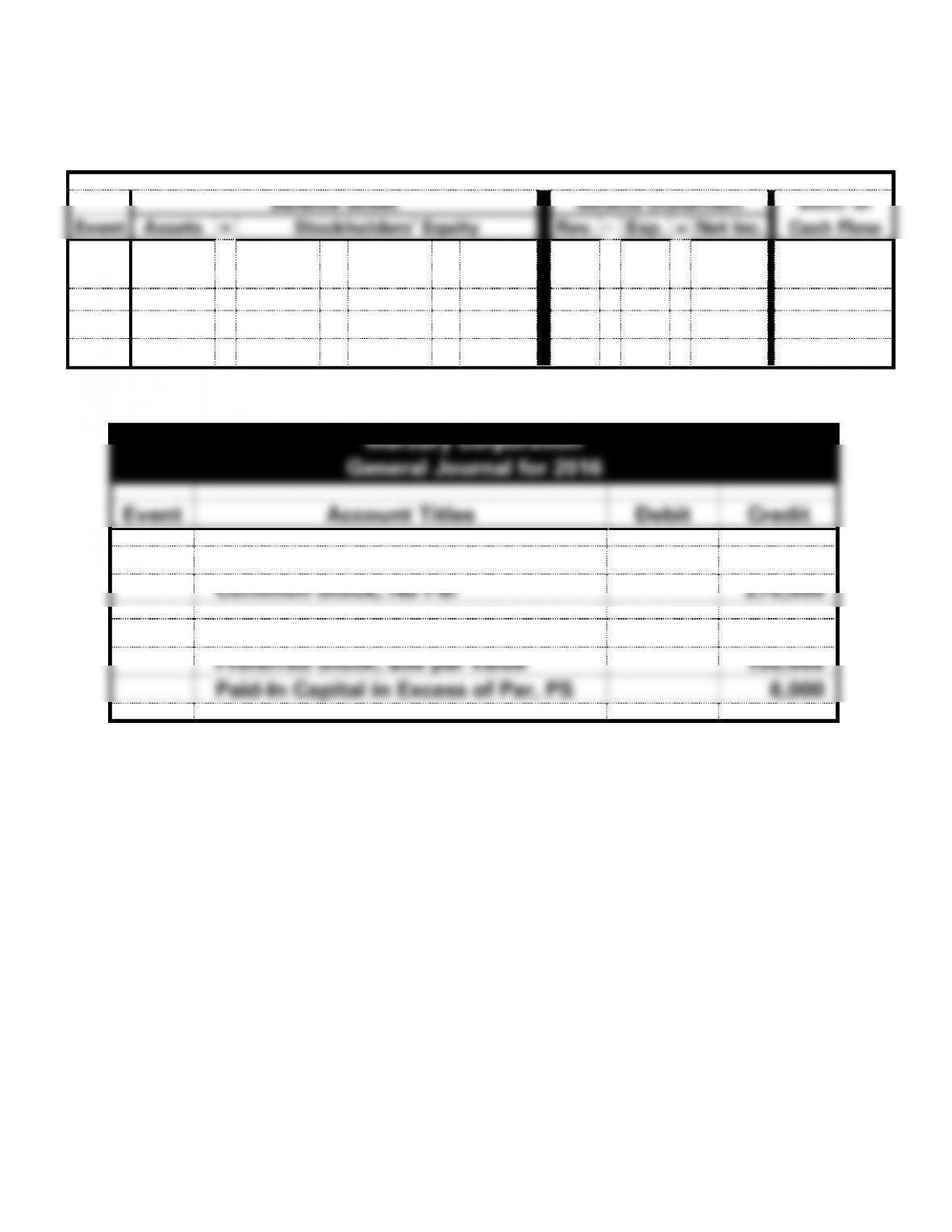

S&J Iron Corporation General Journal for 2016

Date

Account Titles

Debit

Credit

3/1

Cash

96,000

Common Stock

60,000

Paid-In Capital in Excess of Par

36,000

5/2

Cash

180,000

Common Stock

100,000

Paid-In Capital in Excess of Par

80,000

11–29

11–30

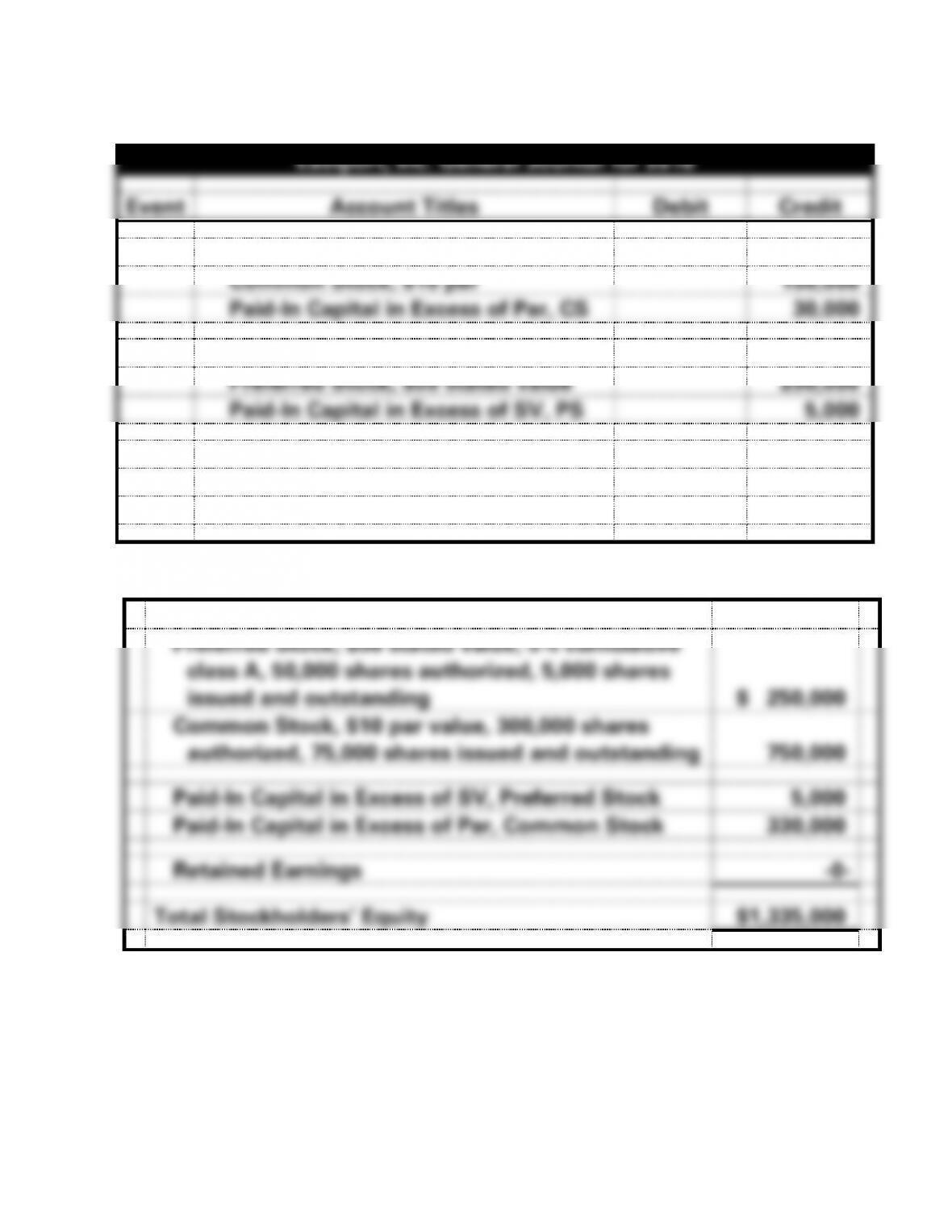

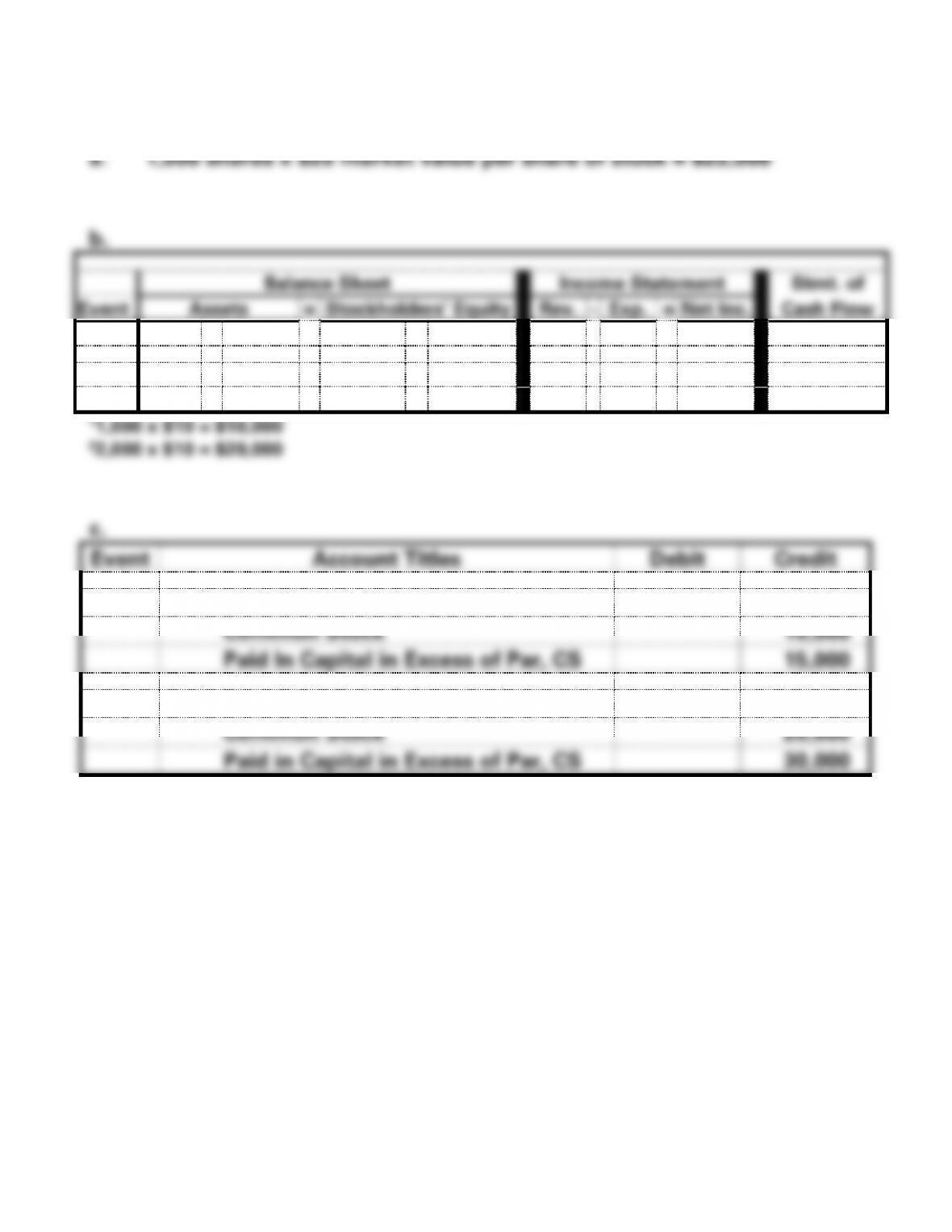

EXERCISE 11-5A

a.

Eastport, Inc. General Journal for 2016

Event

Account Titles

Debit

Credit

1.

Cash (15,000 x $12)

180,000

Common Stock, $10 par

150,000

Paid-In Capital in Excess of Par, CS

30,000

2.

Cash (5,000 x $51)

255,000

Preferred Stock, $50 stated value

250,000

Paid-In Capital in Excess of SV, PS

5,000

3.

Cash (60,000 x $15)

900,000

Common Stock, $10 par

600,000

Paid-In Capital in Excess of Par, CS

300,000

b.

Stockholders’ Equity:

Preferred Stock, $50 stated value, 5% cumulative

class A, 50,000 shares authorized, 5,000 shares

issued and outstanding

$ 250,000

Common Stock, $10 par value, 300,000 shares

authorized, 75,000 shares issued and outstanding

750,000

Paid-In Capital in Excess of SV, Preferred Stock

5,000

Paid-In Capital in Excess of Par, Common Stock

330,000

Retained Earnings

-0-

Total Stockholders’ Equity

$1,335,000

11–31

EXERCISE 11-6A

a.

Balance Sheet

Income Statement

Stmt. of

Event

Assets

=

Stockholders’ Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

Cash

=

Pref.

Stock

+

No-Par

C. Stock

+

PIC in

Excess

1.

270,000

=

NA

+

270,000

+

NA

NA

−

NA

=

NA

270,000 FA

2.

156,000

=

150,000

+

NA

+

6,000

NA

−

NA

=

NA

156,000 FA

b.

Mercury Corporation

General Journal for 2016

Event

Account Titles

Debit

Credit

1.

Cash (6,000 x $45)

270,000

Common Stock, No Par

270,000

2.

Cash (3,000 x $52)

156,000

Preferred Stock, $50 par value

150,000

Paid-In Capital in Excess of Par, PS

6,000

EXERCISE 11-7A

11–33

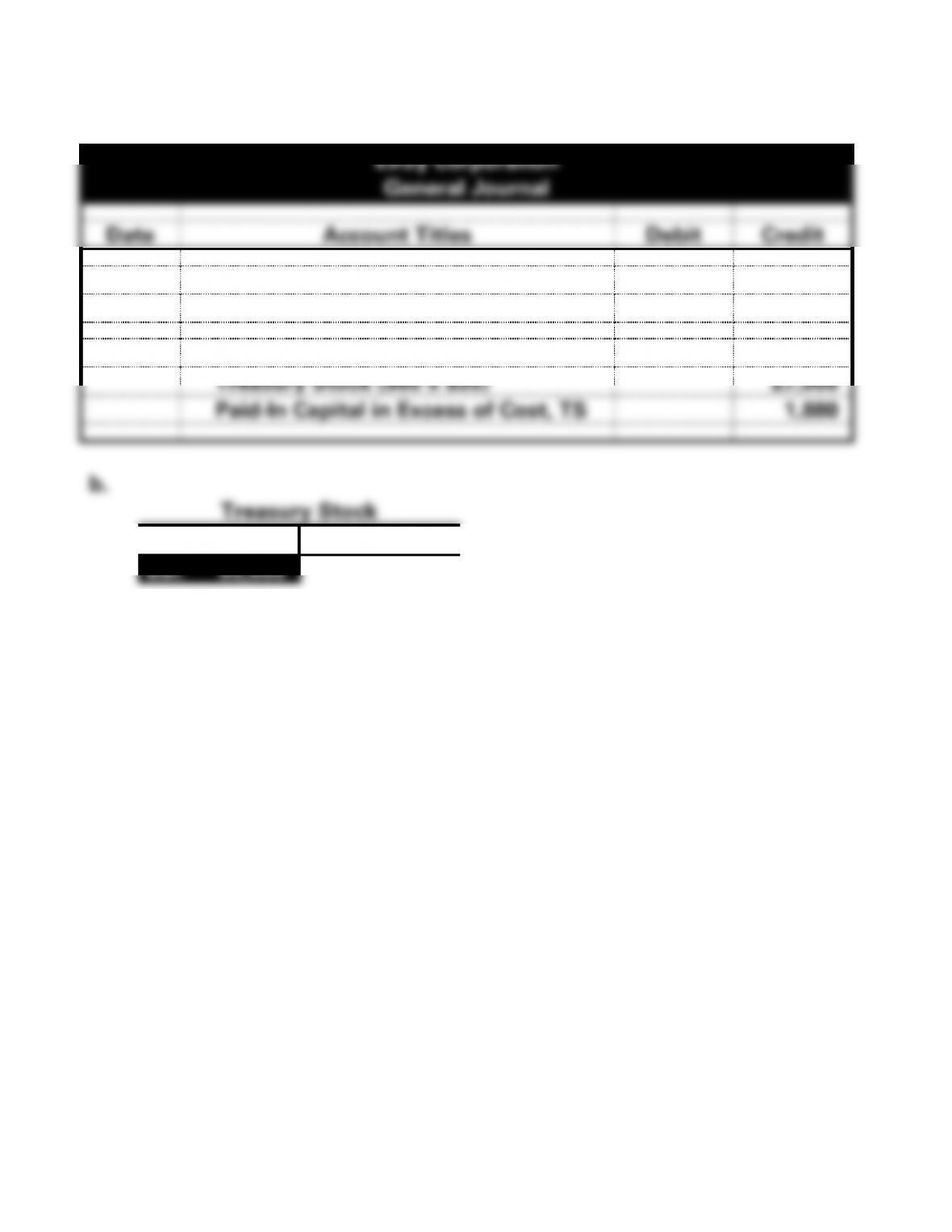

EXERCISE 11-8A

a.

Elroy Corporation

General Journal

Date

Account Titles

Debit

Credit

1.

Treasury Stock (4,000 x $30)

120,000

Cash

120,000

2.

Cash (900 x $32)

28,800

Treasury Stock (900 x $30)

27,000

Paid-In Capital in Excess of Cost, TS

1,880

b.

Treasury Stock

1. 120,000

2. 27,000

Bal. 93,000

11–34

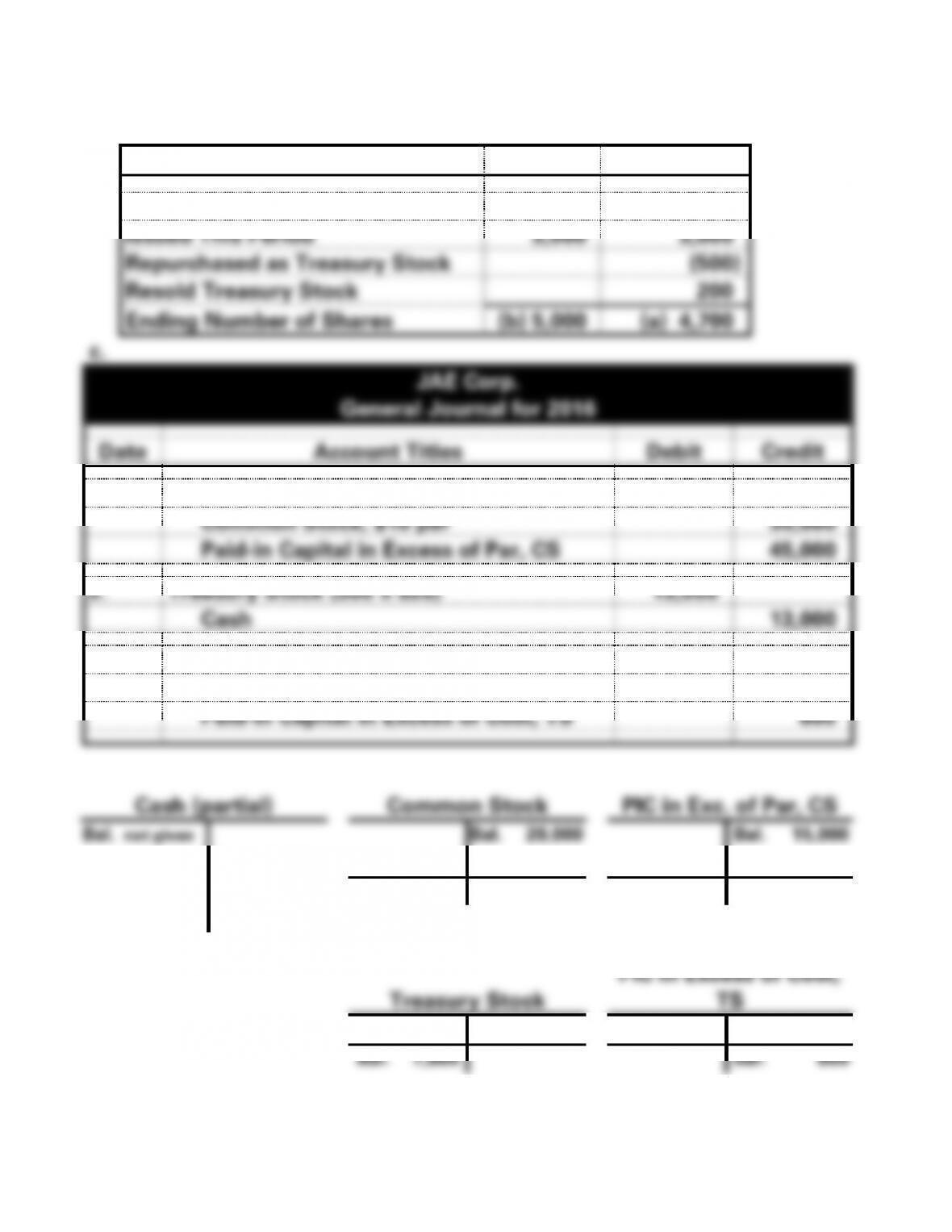

EXERCISE 11-9A

a. & b.

Common Stock

Issued

Outstanding

Beginning Number of Shares

2,000

2,000

Issued This Period

3,000

3,000

Repurchased as Treasury Stock

(500)

Resold Treasury Stock

200

Ending Number of Shares

(b) 5,000

(a) 4,700

c.

JAE Corp.

General Journal for 2016

Date

Account Titles

Debit

Credit

1.

Cash (3,000 x $25)

75,000

Common Stock, $10 par

30,000

Paid-in Capital in Excess of Par, CS

45,000

2.

Treasury Stock (500 x $26)

13,000

Cash

13,000

3.

Cash (200 x $30)

6,000

Treasury Stock (200 x $26)

5,200

Paid-In Capital in Excess of Cost, TS

800

Cash (partial)

Common Stock

PIC in Exc. of Par, CS

Bal. not given

Bal. 20,000

Bal. 15,000

1. 75,000

2. 13,000

1. 30,000

1. 45,000

3. 6,000

Bal. 50,000

Bal. 60,000

Treasury Stock

PIC in Excess of Cost,

TS

2. 13,000

3. 5,200

3. 800

Bal. 7,800

Bal. 800

11–35

EXERCISE 11-9A (cont.)

d.

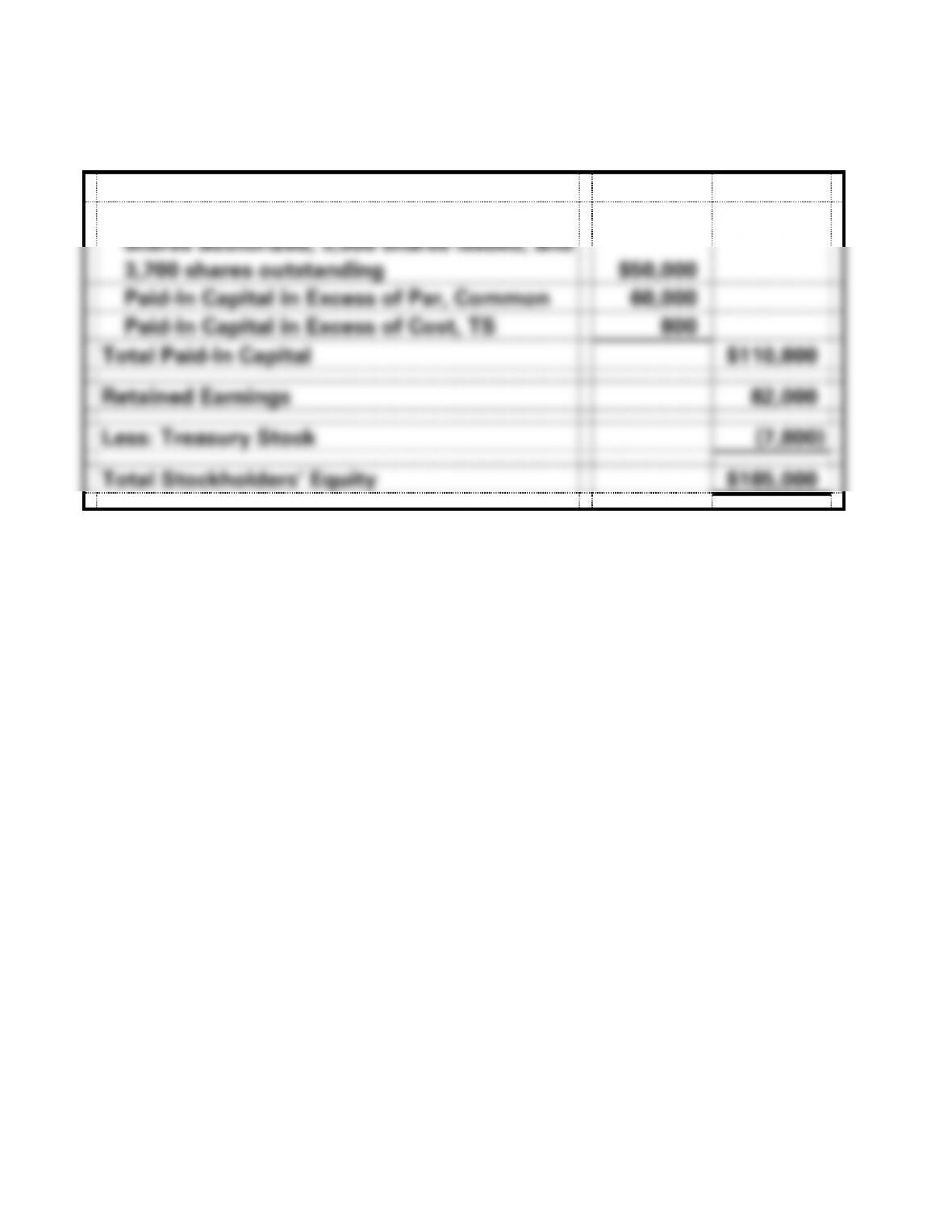

Stockholders’ Equity

Common Stock, $10 par value, 20,000

shares authorized, 5,000 shares issued, and

3,700 shares outstanding

$50,000

Paid-In Capital in Excess of Par, Common

60,000

Paid-In Capital in Excess of Cost, TS

800

Total Paid-In Capital

$110,800

Retained Earnings

82,000

Less: Treasury Stock

(7,800)

Total Stockholders’ Equity

$185,000

11–36

EXERCISE 11-10A

a.

Balance Sheet

Income Statement

Stmt. of

Date

Assets

=

Liab.

+

C. Stk.

+

Ret. Ear.

Rev

−

Exp.

=

Net Inc.

Cash Flow

5/1

NA

=

50,000

+

NA

+

(50,000)

NA

−

NA

=

NA

NA

5/15

NA

=

NA

+

NA

+

NA

NA

−

NA

=

NA

NA

5/31

(50,000)

=

(50,000)

+

NA

+

NA

NA

−

NA

=

NA

(50,000)FA

b.

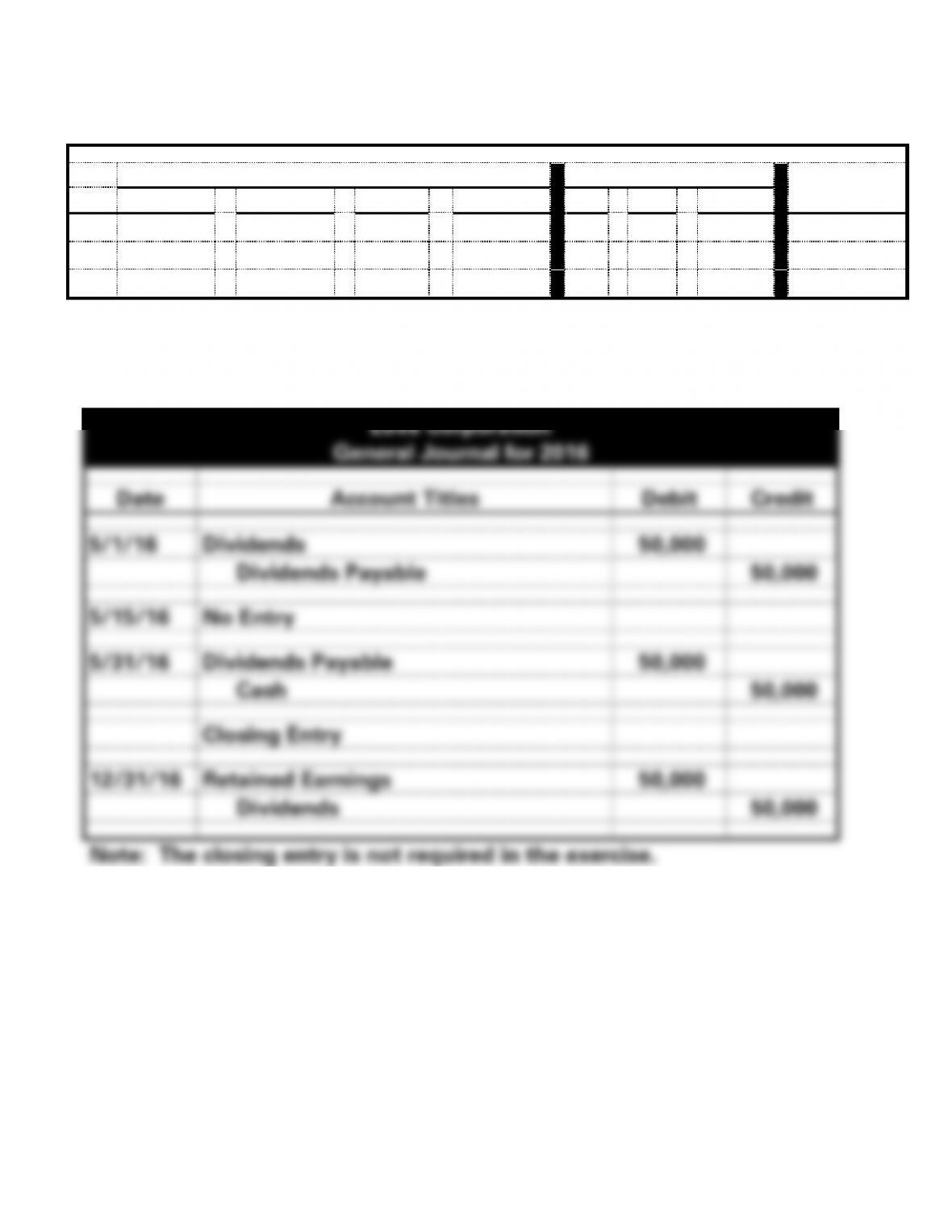

Love Corporation

General Journal for 2016

Date

Account Titles

Debit

Credit

5/1/16

Dividends

50,000

Dividends Payable

50,000

5/15/16

No Entry

5/31/16

Dividends Payable

50,000

Cash

50,000

Closing Entry

12/31/16

Retained Earnings

50,000

Dividends

50,000

Note: The closing entry is not required in the exercise.

11–37

EXERCISE 11-11A

Computation of Preferred Dividends

Par Value

of Stock

x

Dividend %

=

Dividend

per Share

x

Preferred

Shares

Outstanding

=

Total

Dividends

per Year

$50

x

6%

=

$3.00

x

4,000

=

$12,000

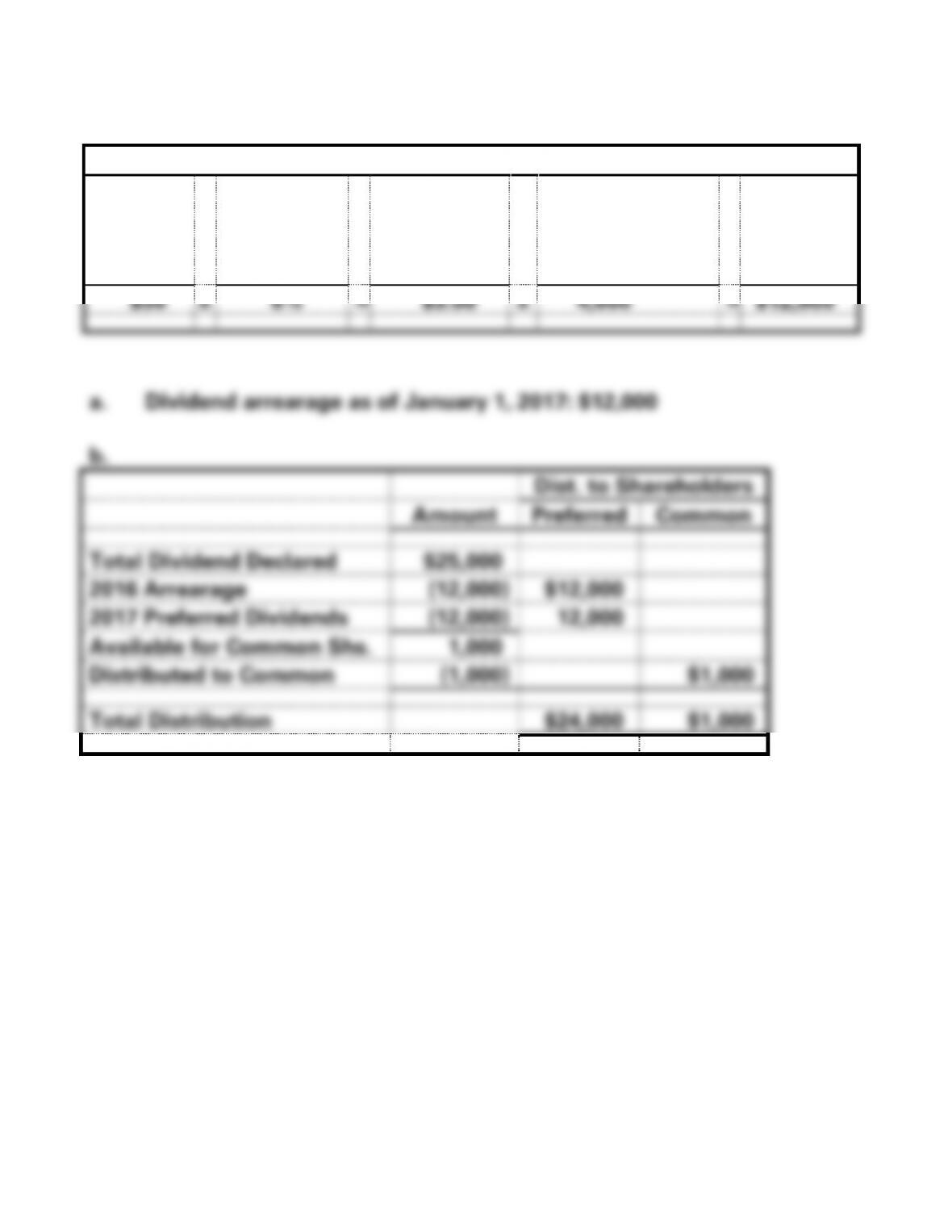

a. Dividend arrearage as of January 1, 2017: $12,000

b.

Dist. to Shareholders

Amount

Preferred

Common

Total Dividend Declared

$25,000

2016 Arrearage

(12,000)

$12,000

2017 Preferred Dividends

(12,000)

12,000

Available for Common Shs.

1,000

Distributed to Common

(1,000)

$1,000

Total Distribution

$24,000

$1,000

EXERCISE 11-12A

a.

Computation of Dividends to Be Paid:

Preferred Stock

$100 par value x 6% x 15,000 shares =

$ 90,000

Common Stock

$.5 x 150,000 shares =

75,000

Total Dividend

$165,000

Debit

11–39

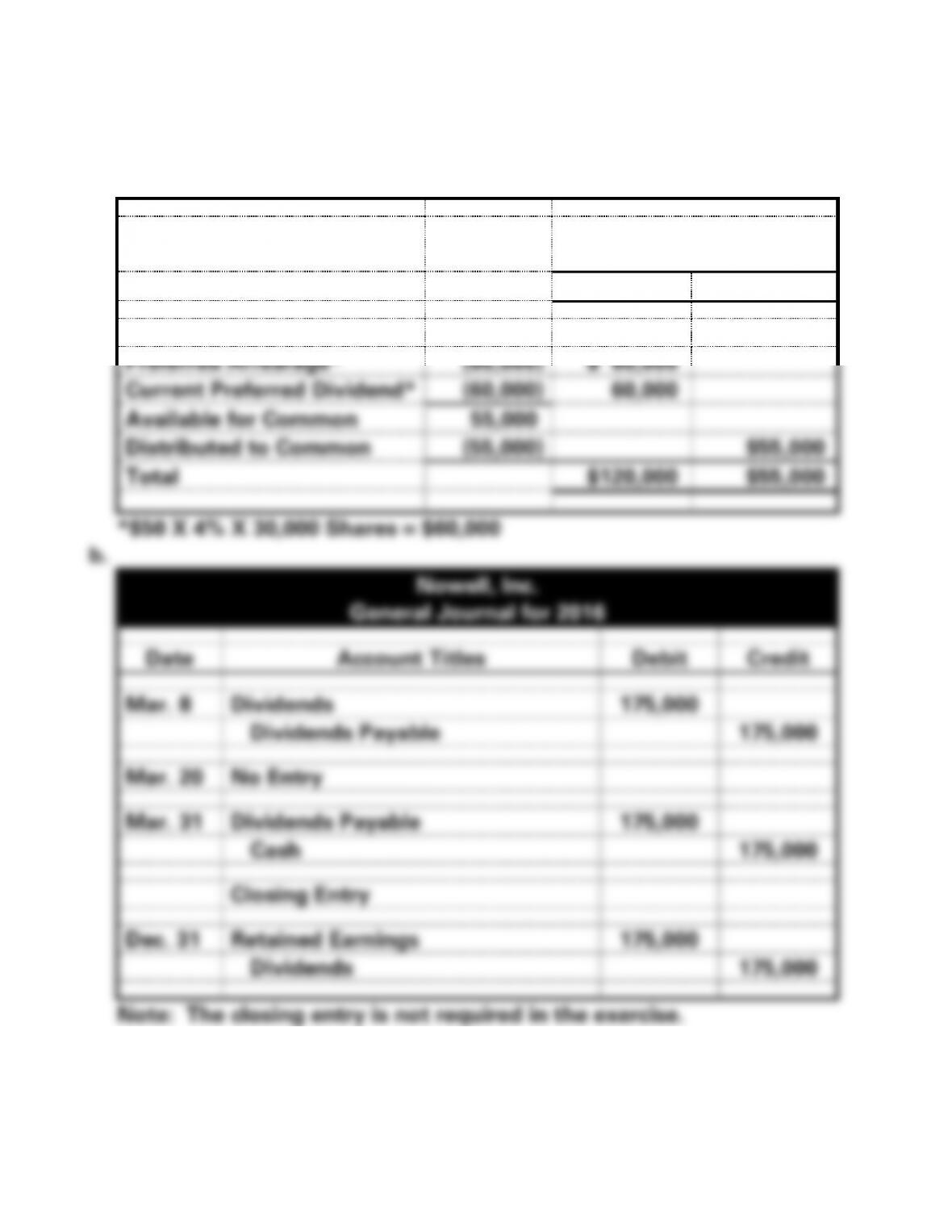

EXERCISE 11-13A

a. Distribution of Dividend:

Distributed to

Shareholders

Preferred

Common

Total Dividend Declared

$175,000

Preferred Arrearage*

(60,000)

$ 60,000

Current Preferred Dividend*

(60,000)

60,000

Available for Common

55,000

Distributed to Common

(55,000)

$55,000

Total

$120,000

$55,000

*$50 X 4% X 30,000 Shares = $60,000

b.

Nowell, Inc.

General Journal for 2016

Date

Account Titles

Debit

Credit

Mar. 8

Dividends

175,000

Dividends Payable

175,000

Mar. 20

No Entry

Mar. 31

Dividends Payable

175,000

Cash

175,000

Closing Entry

Dec. 31

Retained Earnings

175,000

Dividends

175,000

Note: The closing entry is not required in the exercise.

11–40

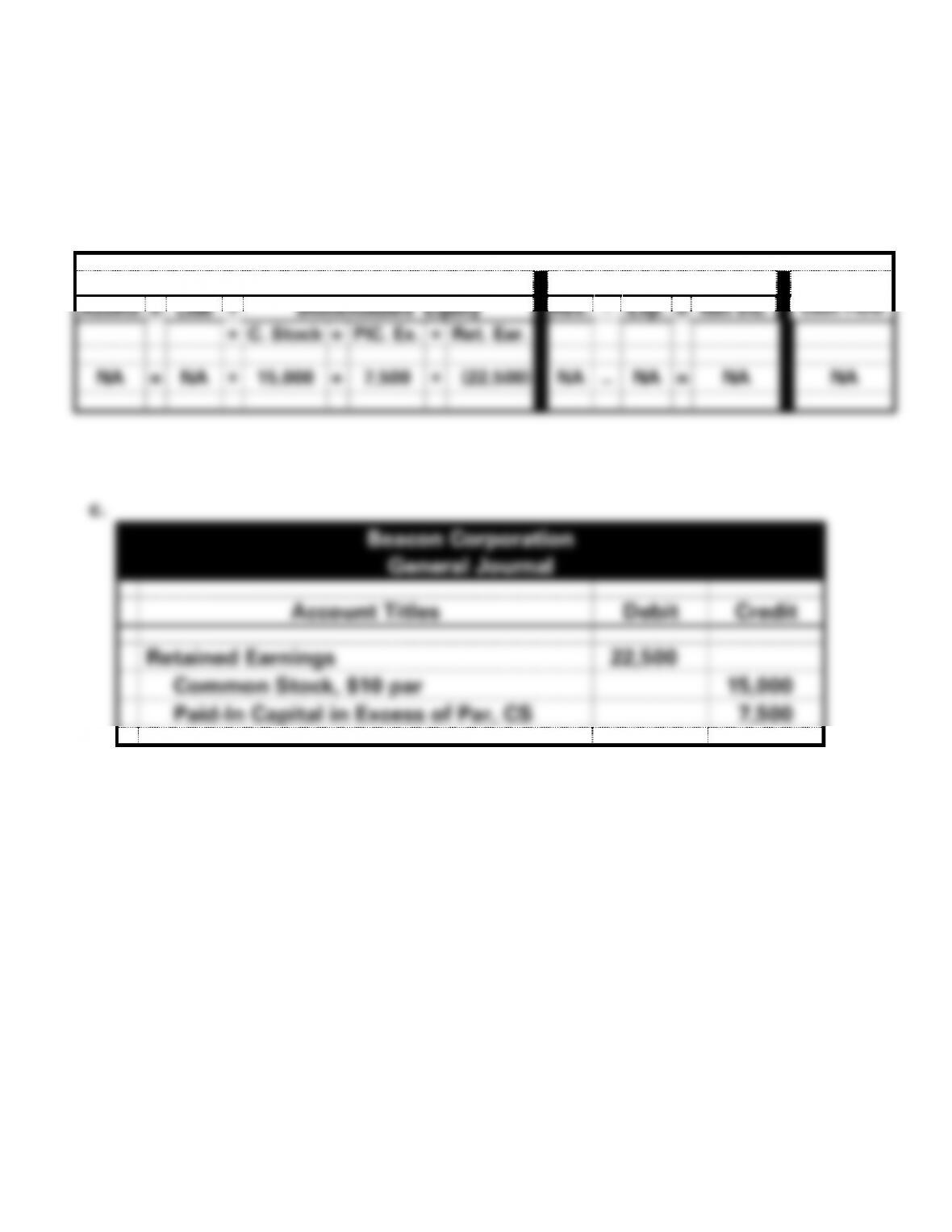

EXERCISE 11-14A

a. (30,000 shares x .05) x $15 = $22,500

b.

Balance Sheet

Income Statement

Stmt. of

Assets

=

Liab

+

Stockholders’ Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

+

C. Stock

+

PIC. Ex.

+

Ret. Ear.

NA

=

NA

+

15,000

+

7,500

+

(22,500)

NA

−

NA

=

NA

NA

c.

Beacon Corporation

General Journal

Account Titles

Debit

Credit

Retained Earnings

22,500

Common Stock, $10 par

15,000

Paid-In Capital in Excess of Par, CS

7,500

11–41

EXERCISE 11–15A

a. No formal entry would be made in the accounting records. A memo

entry would indicate the number of shares had tripled and the par

11–42

EXERCISE 11-16A

a. The price per share of Discount Drugs should increase substantially.

This increase is a result of the expectation of future profits. The

11–43

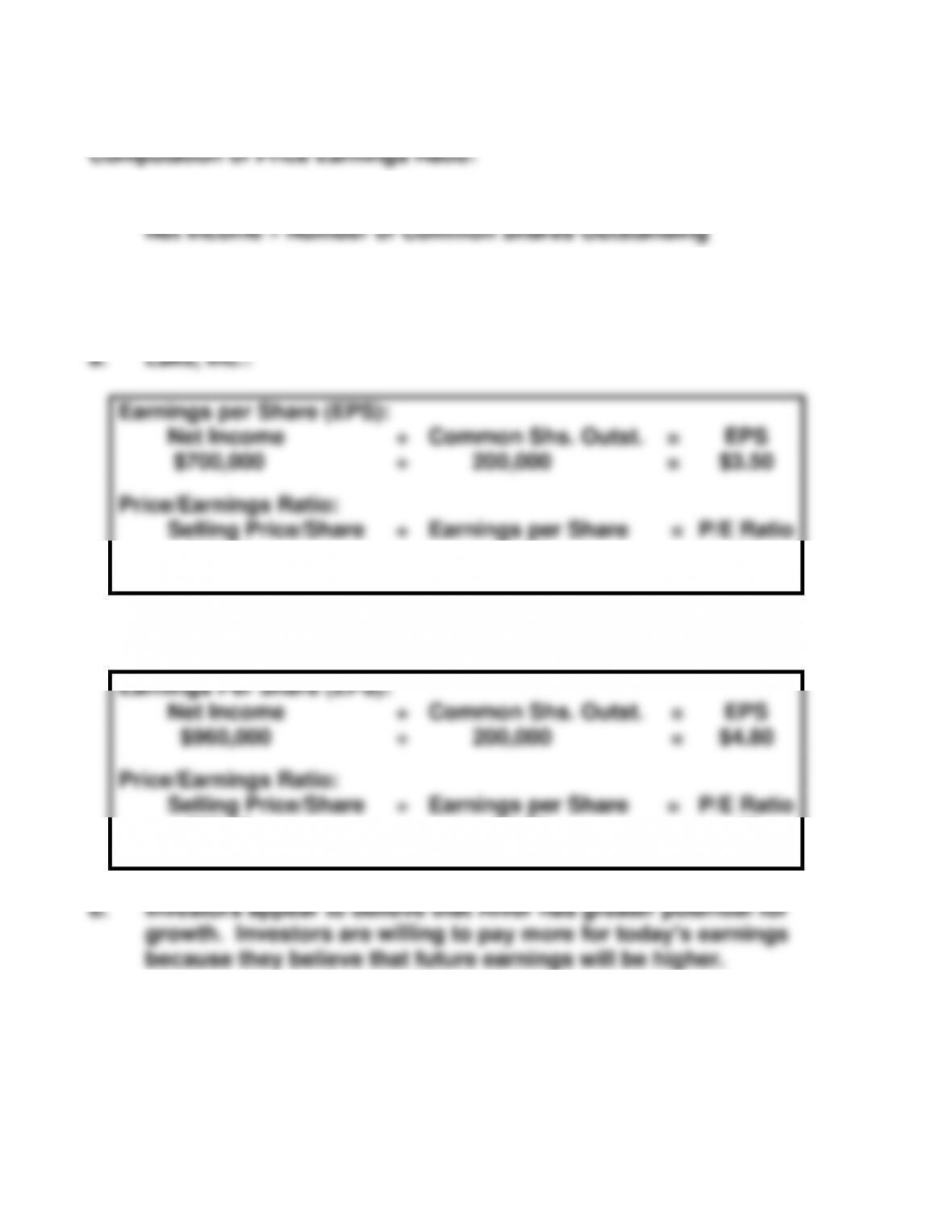

EXERCISE 11-17A

1. Compute Earnings per Share:

2. Compute Price Earnings Ratio:

Selling Price per Share Earnings per Share

Earnings per Share (EPS):

Net Income

÷

Common Shs. Outst.

=

EPS

$700,000

÷

200,000

=

$3.50

Price/Earnings Ratio:

Selling Price/Share

÷

Earnings per Share

=

P/E Ratio

$50.00

÷

$3.50

=

14

River, Inc.:

Earnings Per Share (EPS):

Net Income

÷

Common Shs. Outst.

=

EPS

$960,000

÷

200,000

=

$4.80

Price/Earnings Ratio:

Selling Price/Share

÷

Earnings per Share

=

P/E Ratio

$85.00

÷

$4.80

=

18