2-32

EXERCISE 2-11A

a. Examples of expenses that would be matched directly with revenue:

2-33

EXERCISE 2-12A

a.

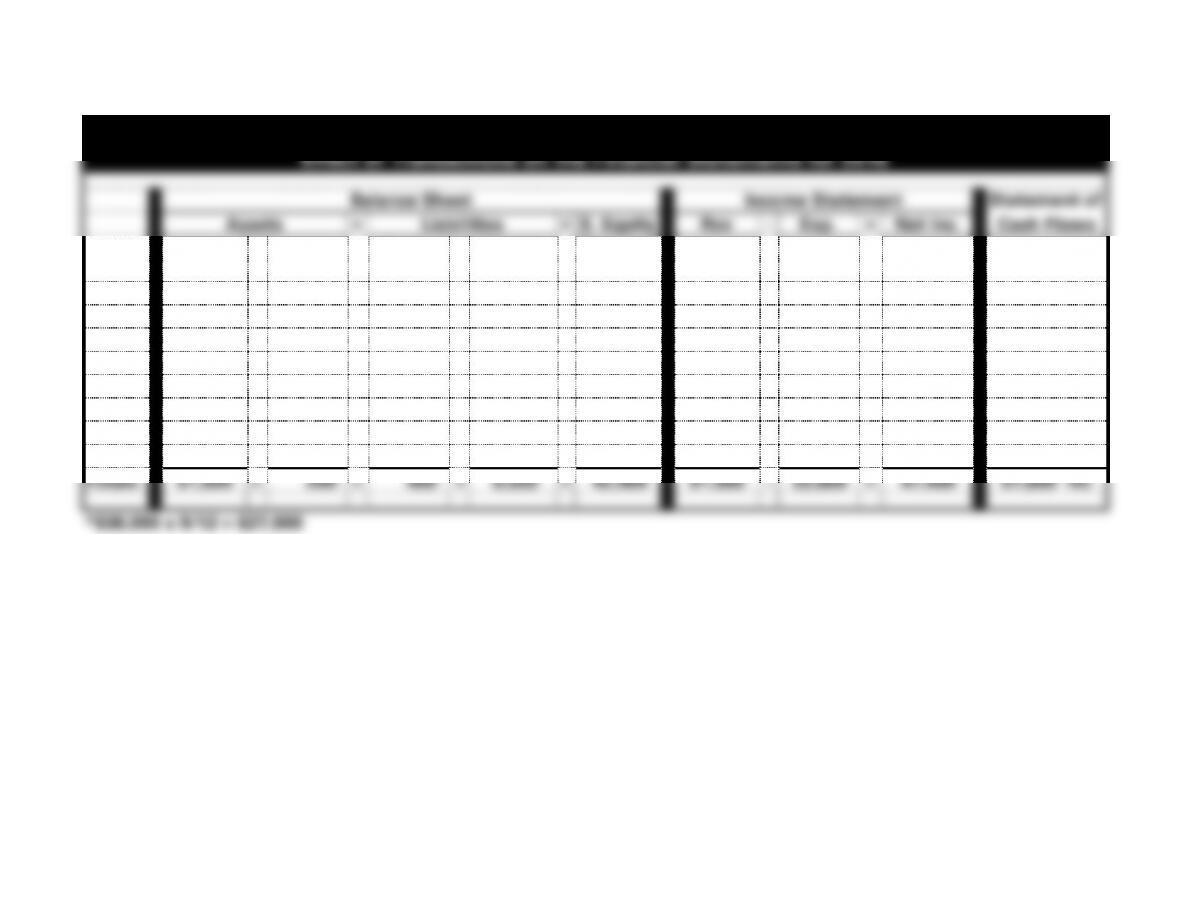

Pizza Express

Effect of Events on Financial Statements for 2016

Assets

=

Liab.

+

Stockholders’

Equity

Income Statement

Statement

of

Event

No.

Cash

+

Supplies

=

Accts.

Pay.

+

Com.

Stock

+

Ret.

Earn.

Rev.

−

Exp.

=

Net

Income

Cash

Flows

Beg. Bal

2,500

+

-0-

=

-0-

+

1,400

+

1,100

-0-

−

-0-

=

-0-

-0-

1.

NA

+

3,600

=

3,600

+

NA

+

NA

NA

−

NA

=

NA

NA

2.

12,300

+

NA

=

NA

+

NA

+

12,300

12,300

−

NA

=

12,300

12,300 OA

3.

(2,700)

+

NA

=

(2,700)

+

NA

+

NA

NA

−

NA

=

NA

(2,700) OA

4.

NA

+

(3,350)

=

NA

+

NA

+

(3,350)

NA

−

3,350

=

(3,350)

NA

Totals

12,100

+

250

=

900

+

1,400

+

10,050

12,300

−

3,350

=

8,950

9,600 NC

2-34

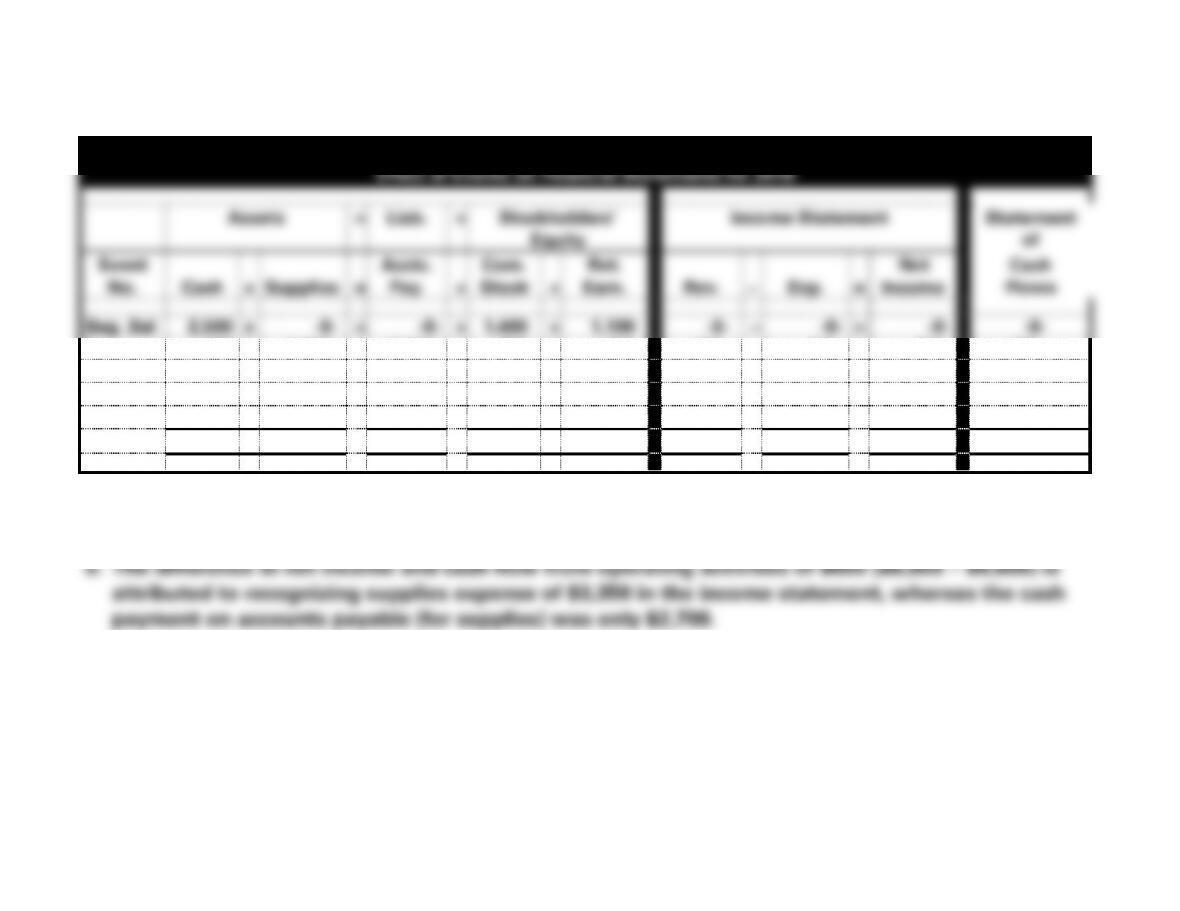

EXERCISE 2-13A a.

Yard Professionals Inc.

Effect of Events on the Accounting Equation

Assets

=

Liab.

+

Stk. Equity

Event

Cash

Supplies

=

Accounts

Payable

Retained

Earnings

1. Provided Service

35,000

35,000

2. Purchased Supplies

6,000

6,000

3. Used Supplies

(4,200)

(4,200)

Totals

35,000

1,800

=

6,000

30,800

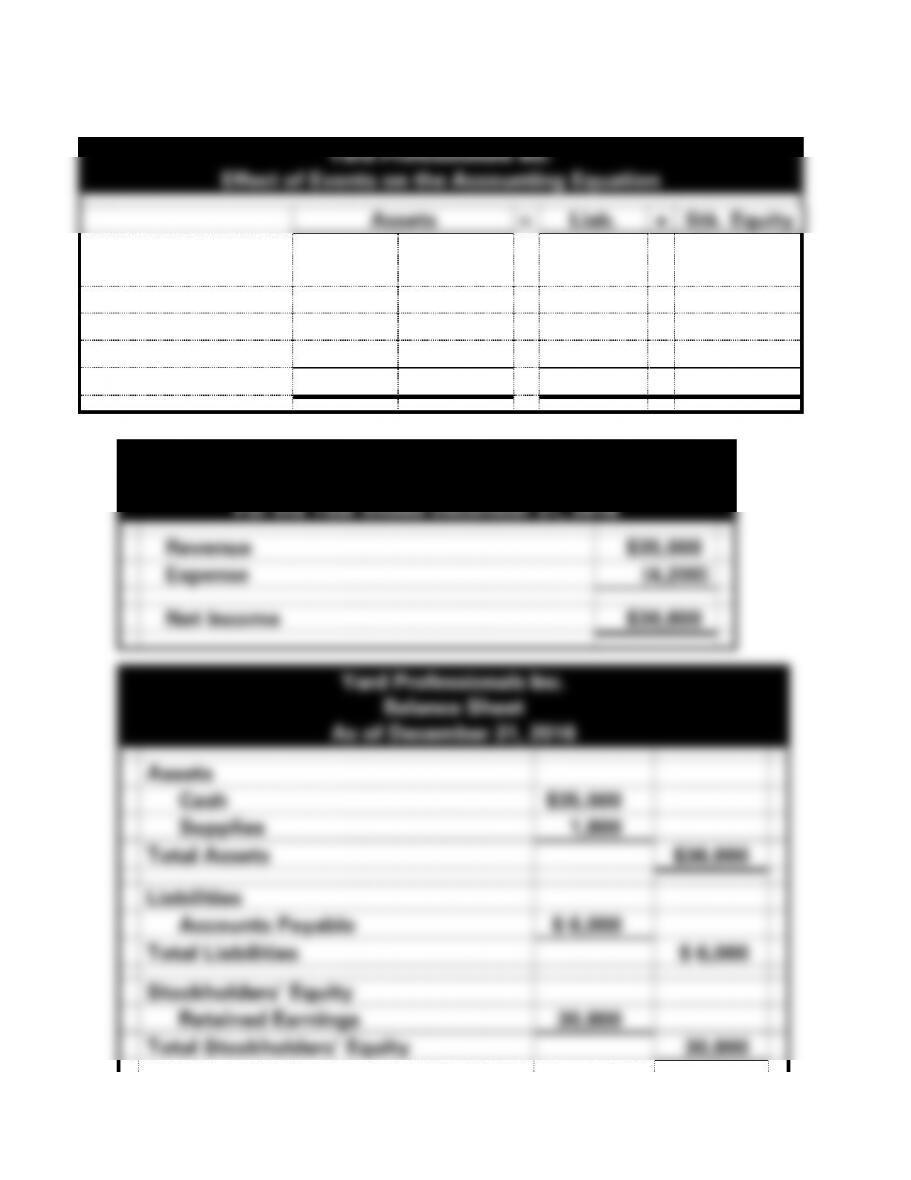

b.

Yard Professionals Inc.

Income Statement

For the Year Ended December 31, 2016

Revenue

$35,000

Expense

(4,200)

Net Income

$30,800

Yard Professionals Inc.

Balance Sheet

As of December 31, 2016

Assets

Cash

$35,000

Supplies

1,800

Total Assets

$36,800

Liabilities

Accounts Payable

$ 6,000

Total Liabilities

$ 6,000

Stockholders’ Equity

Retained Earnings

30,800

Total Stockholders’ Equity

30,800

2-35

Total Liab. and Stockholders’ Equity

$36,800

2-36

EXERCISE 2-13A b. (cont.)

Yard Professionals Inc.

Statement of Cash Flows

For the Year Ended December 31, 2016

Cash Flows From Operating Activities:

Cash Receipt from Revenue

$35,000

Net Cash Flow from Operating Activities

$35,000

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities:

-0-

Net Change in Cash

35,000

Plus: Beginning Cash Balance

-0-

Ending Cash Balance

$35,000

2-37

EXERCISE 2-14A

a. A cost is the value sacrificed for goods and services that are expected

to bring a current or future benefit to the organization. A cost can be

b.

Asset

Expense

(1)

X (Purchased Building)

(2)

X (Purchased Supplies)

(3)

X (Used Supplies)

(4)

X (Paid Insurance in Advance)

(5)

X (Accrued Salaries)

EXERCISE 2-15A

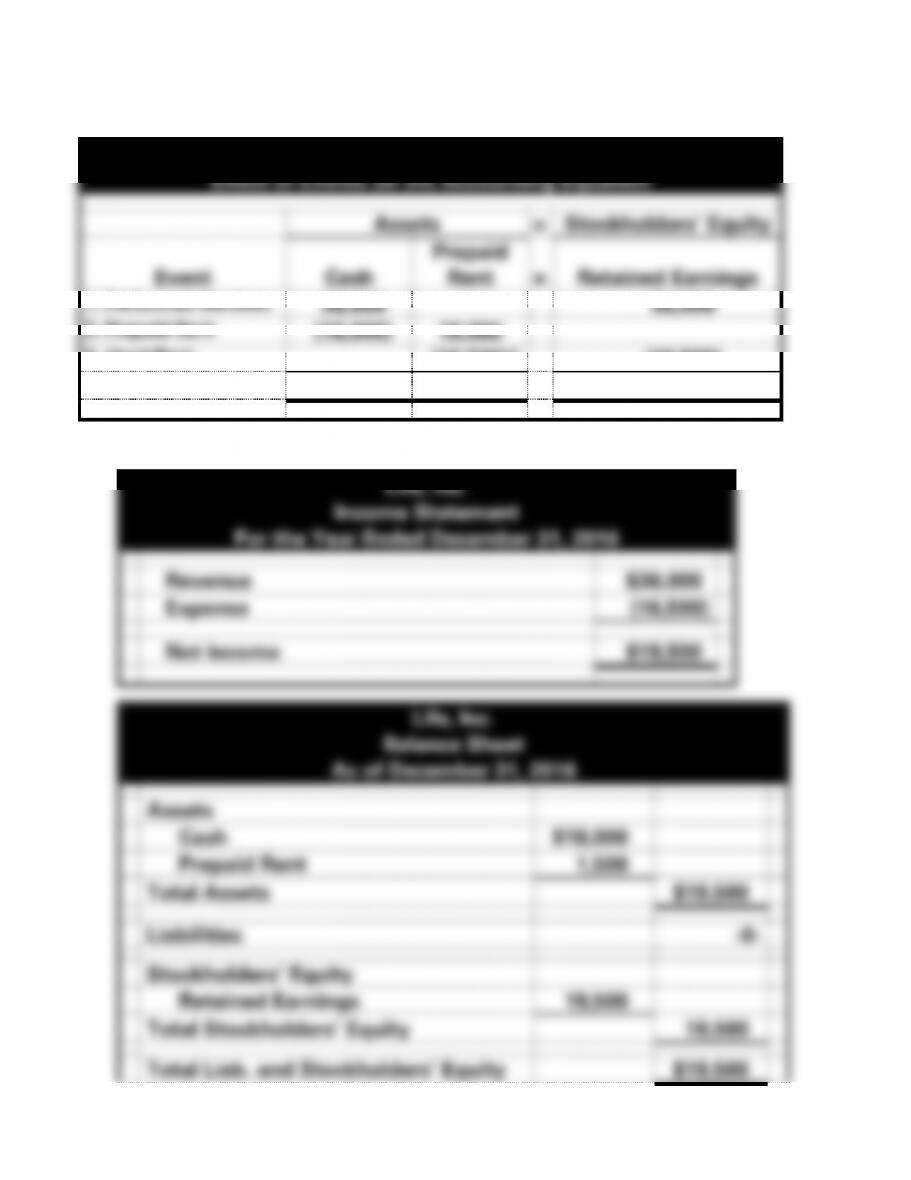

a.

Life, Inc.

Effect of Events on the Accounting Equation

Assets

=

Stockholders’ Equity

Event

Cash

Prepaid

Rent

=

Retained Earnings

1. Performed Services

36,000

36,000

2. Prepaid Rent

(18,000)

18,000

3. Used Rent

(16,500)*

(16,500)

Totals

18,000

1,500

=

19,500

*$18,000 x 11/12 = $16,500

b.

Life, Inc.

Income Statement

For the Year Ended December 31, 2016

Revenue

$36,000

Expense

(16,500)

Net Income

$19,500

Life, Inc.

Balance Sheet

As of December 31, 2016

Assets

Cash

$18,000

Prepaid Rent

1,500

Total Assets

$19,500

Liabilities

-0-

Stockholders’ Equity

Retained Earnings

19,500

Total Stockholders’ Equity

19,500

Total Liab. and Stockholders’ Equity

$19,500

2-39

2-40

EXERCISE 2-15A b. (cont.)

Life, Inc.

Statement of Cash Flows

For the Year Ended December 31, 2016

Cash Flows From Operating Activities:

Cash Receipt from Revenue

$36,000

Cash Payment for Rent

(18,000)

Net Cash Flow from Operating Activities

$18,000

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities:

-0-

Net Change in Cash

18,000

Plus: Beginning Cash Balance

-0-

Ending Cash Balance

$18,000

2-41

EXERCISE 2-16A

a.

Maine Corporation

Accounting Equation 2016

Assets

=

Liab.

+

Stockholders’ Equity

Event

Cash

Prepaid

Rent

=

+

Com.

Stock

+

Retained

Earnings

Paid rent in

advance

(18,000)

18,000

Adj. Rent exp.

(13,500)*

(13,500)

Totals

(18,000)

4,500

=

-0-

+

-0-

+

(13,500)

*$18,000 x 9/12 = $13,500

b. The required entry would decrease assets by $13,500 [($18,000 12)

x 9] and decrease stockholders’ equity by $13,500 (retained

earnings). If this entry is not made, assets and stockholders’ equity

would both be overstated on the balance sheet by $13,500. On the

income statement, expenses would be understated causing net

income to be overstated by $13,500.

2-42

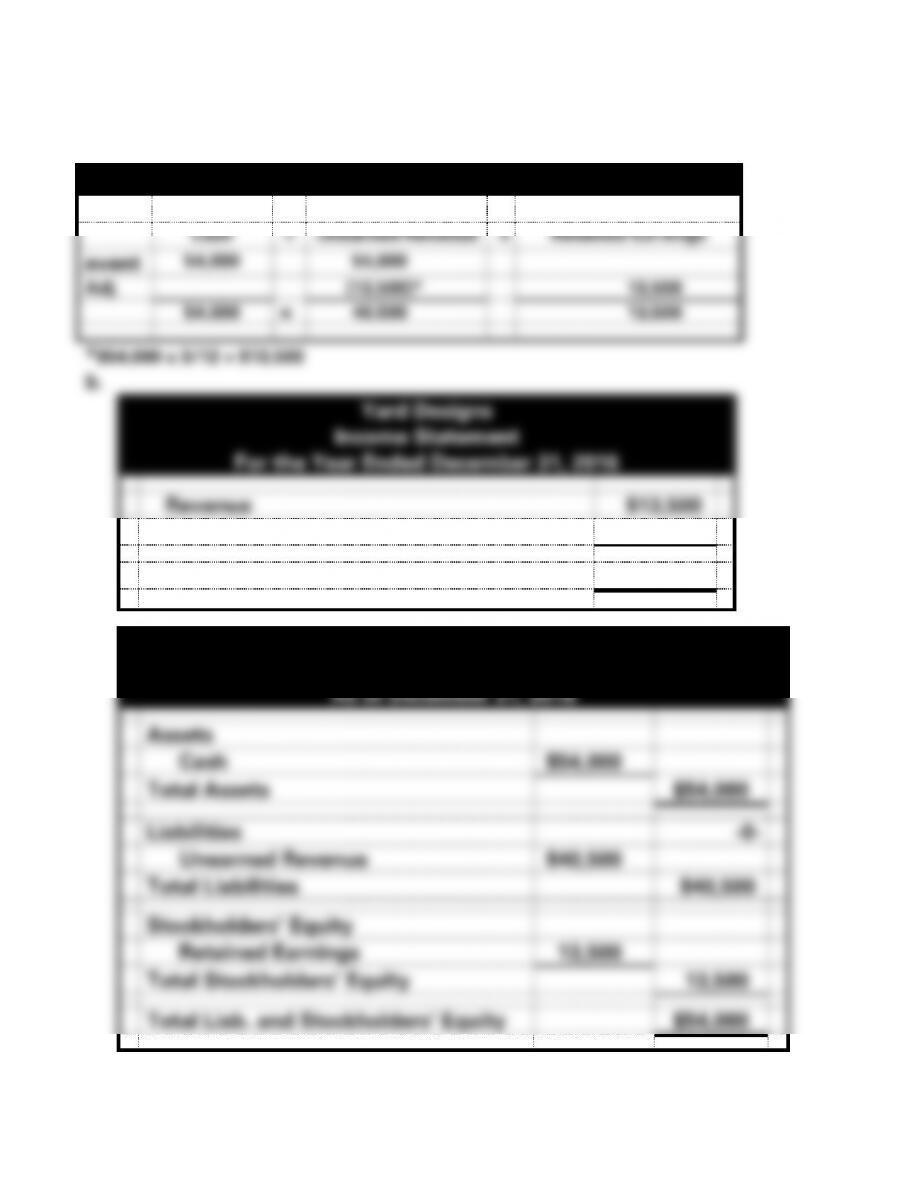

EXERCISE 2-17A

a.

Yard Designs 2016

Event

Assets

=

Liabilities

+

Stockholders’ Equity

Cash

=

Unearned Revenue

+

Retained Earnings

event

54,000

54,000

Adj.

(13,500)*

13,500

54,000

=

40,500

13,500

*$54,000 x 3/12 = $13,500

b.

Yard Designs

Income Statement

For the Year Ended December 31, 2016

Revenue

$13,500

Expense

-0-

Net Income

$13,500

Yard Designs

Balance Sheet

As of December 31, 2016

Assets

Cash

$54,000

Total Assets

$54,000

Liabilities

-0-

Unearned Revenue

$40,500

Total Liabilities

$40,500

Stockholders’ Equity

Retained Earnings

13,500

Total Stockholders’ Equity

13,500

Total Liab. and Stockholders’ Equity

$54,000

2-43

EXERCISE 2-17A b. (cont.)

Yard Designs

Statement of Cash Flows

For the Year Ended December 31, 2016

Cash Flows From Operating Activities:

Cash Receipt from Revenue

$54,000

Net Cash Flow from Operating Activities

$54,000

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities:

-0-

Net Change in Cash

54,000

Plus: Beginning Cash Balance

-0-

Ending Cash Balance

$54,000

2-44

EXERCISE 2-18A

Note: This exercise can be used to assess writing skills.

2–45

EXERCISE 2-19A

Hart Attorney At Law

Effect of Transactions on the Financial Statements for 2016

Balance Sheet

Income Statement

Statement of

Assets

=

Liabilities

+

S. Equity

Rev

−

Exp.

=

Net Inc.

Cash Flows

No.

Cash

+

Supplies

=

Accts.

Payable

+

Unearn.

Rev.

+

Retained

Earnings

1.

36,000

+

NA

=

NA

+

36,000

+

NA

NA

−

NA

=

NA

36,000 OA

2.

54,000

+

NA

=

NA

+

NA

+

54,000

54,000

−

NA

=

54,000

54,000 OA

3.

NA

+

2,800

=

2,800

+

NA

+

NA

NA

−

NA

=

NA

NA

4.

(2,400)

+

NA

=

(2,400)

+

NA

+

NA

NA

−

NA

=

NA

(2,400) OA

5.

(5,000)

+

NA

=

NA

+

NA

+

(5,000)

NA

−

NA

=

NA

(5,000) FA

6.

(31,000)

+

NA

=

NA

+

NA

+

(31,000)

NA

−

31,000

=

(31,000)

(31,000) OA

7.

NA

+

(2,600)

=

NA

+

NA

+

(2,600)

NA

−

2,600

=

(2,600)

NA

8.

NA

+

NA

=

NA

+

(27,000)*

+

27,000

27,000

−

NA

=

27,000

NA

Totals

51,600

+

200

=

400

+

9,000

+

42,400

81,000

−

33,600

=

47,400

51,600 NC

*$36,000 x 9/12 = $27,000

2–46

EXERCISE 2-20A

a.

Bell Personal Financial Planning

Horizontal Statements Model for 2016

Assets

=

Liabilities

+

Stk. Equity

Income Statement

Statement

of

Event

Cash

=

Unearned

Revenue

+

Retained

Earnings

Rev.

−

Exp.

=

Net

Income

Cash

Flows

1. Advance Payment

36,000

36,000

NA

NA

NA

NA

36,000 OA

2. Revenue Earned

NA

(21,000)*

21,000

21,000

NA

21,000

NA

Totals

36,000

=

15,000

+

21,000

21,000

−

-0-

=

21,000

36,000 NC

2–47

EXERCISE 2-21A

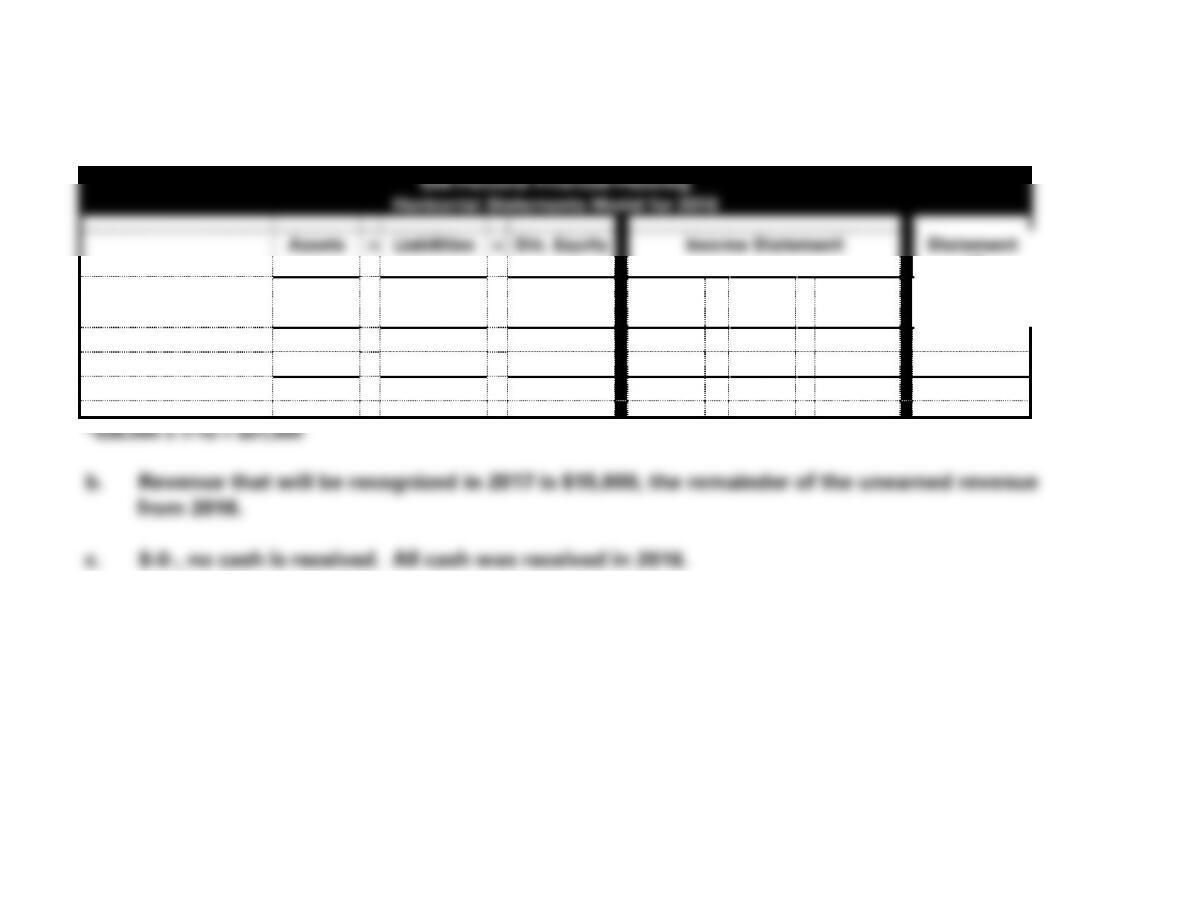

a.

Josh Smith Attorney – 2016

Event

Assets

=

Liabilities

+

Stockholders’ Equity

Cash

=

Unearned

Revenue

+

Common

Stock

+

Retained

Earnings

Cash collected

10,800

10,800

Revenue earned

(5,400)*

5,400

*$10,800 x 3/6 = $5,400

b.

James Company – 2016

Event

Assets

=

Liab.

+

Stockholders’ Equity

Cash

Prepaid

Legal Fees

=

+

Common

Stock

+

Retained

Earnings

Cash paid

(10,800)

10,800

Service used

(5,400)*

(5,400)

*$10,800 x 3/6 = $5,400

2–48

EXERCISE 2-22A

a. deferral

b. neither

c. neither

2–49

EXERCISE 2-23A

Note: There are many examples of events that illustrate the required

2–50

EXERCISE 2-24A

a.

Event

Requires year-end

adjusting entry?

1.

No

2.

No

3.

Yes

4.

Yes

5.

No

6.

Yes

7.

No

8.

No

9.

No

10.

No

b. Adjusting entries are required to update accounting records for income

2–51

EXERCISE 2-25A

a.

Event

Classification

1.

FA

2.

NA

3.

OA

4.

OA

5.

OA

6.

NA

7.

OA

8.

FA

9.

OA

10.

NA

b.

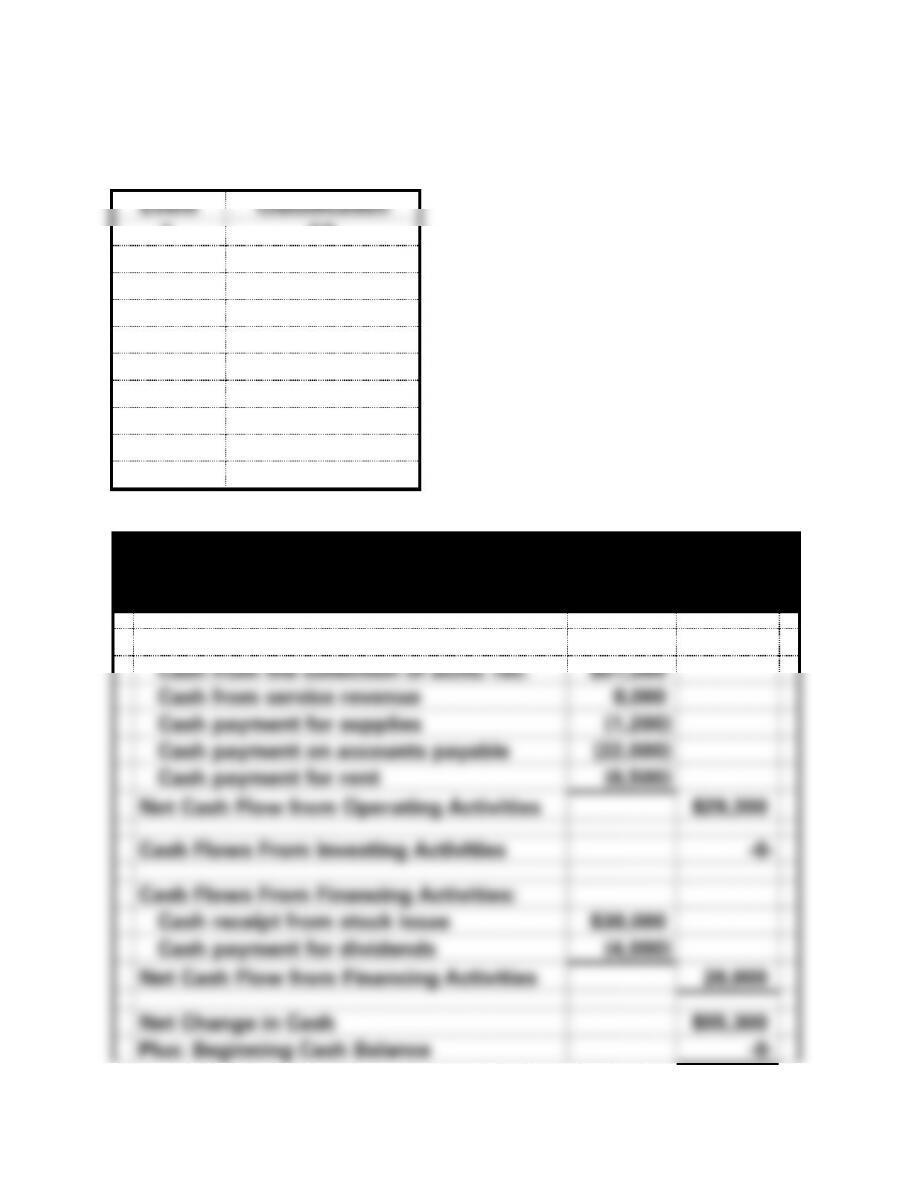

Ewing Company

Statement of Cash Flows

For the Year Ended December 31, 2016

Cash Flows From Operating Activities:

Cash from the collection of accts. rec.

$51,000

Cash from service revenue

8,000

Cash payment for supplies

(1,200)

Cash payment on accounts payable

(22,000)

Cash payment for rent

(6,500)

Net Cash Flow from Operating Activities

$29,300

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities:

Cash receipt from stock issue

$30,000

Cash payment for dividends

(4,000)

Net Cash Flow from Financing Activities

26,000

Net Change in Cash

$55,300

Plus: Beginning Cash Balance

-0-