Chapter 12 Statement of Cash Flows

12–21

EXERCISE 12–12A

a.

Reconciliation of Common Stock Account

Beginning balance

$150,000

Increase due to issuing common stock

?

= 25,000

Ending balance

$175,000

Cash Flows from Financing Activities

Proceeds from issue of common stock

$ 25,000

Paid for purchase of treasury stock

(20,000)

Net cash inflow from financing activities

$ 5,000

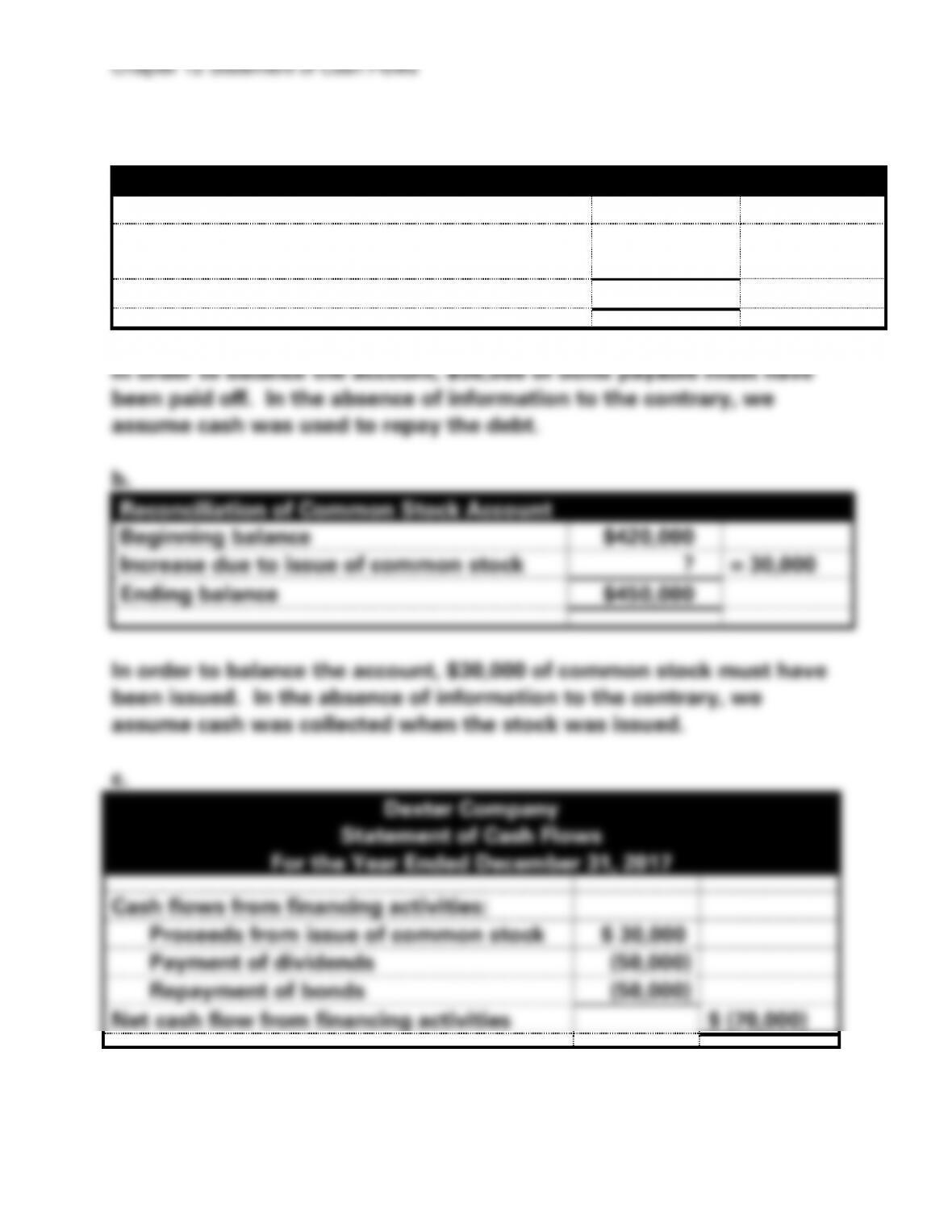

Cash flows from financing activities:

Proceeds from issue of common stock

Payment of dividends

(50,000)

Repayment of bonds

(50,000)

Net cash flow from financing activities

$ (70,000)

EXERCISE 12-13A

a.

Reconciliation of Bonds Payable Account

Beginning balance

$400,000

Decrease due to repayment of bonds

payable

?

= (50,000)

Ending balance

$350,000

Reconciliation of Common Stock Account

Beginning balance

$420,000

Increase due to issue of common stock

?

= 30,000

Ending balance

$450,000

Chapter 12 Statement of Cash Flows

12–23

PROBLEM 12-14A

a. Direct Method

Reconciliation of Accounts Receivable

Beginning balance

$ 52,000

Increase due to revenue recognized on account

720,000

Decrease due to cash collections from

customers

?

= (724,000)

Ending balance

$ 48,000

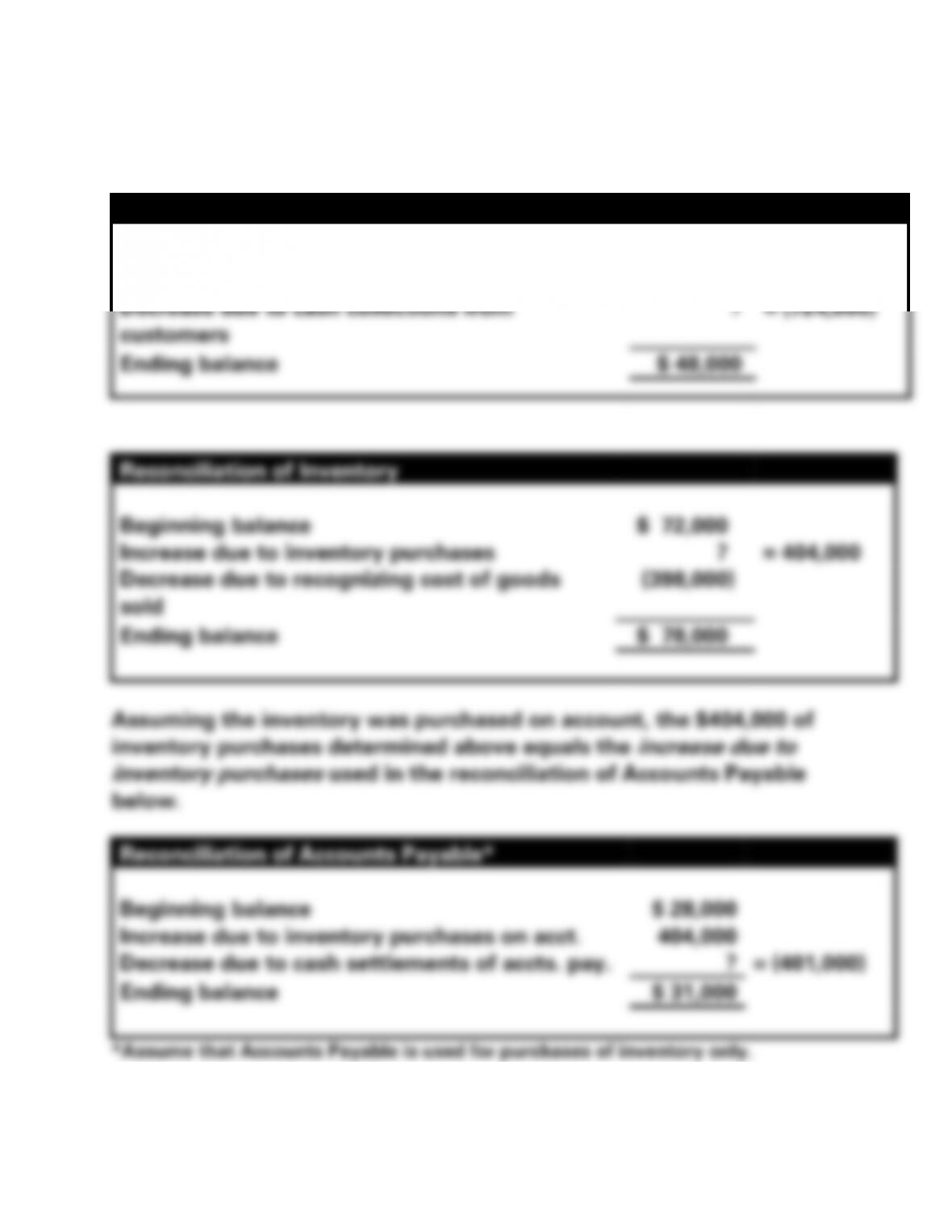

Reconciliation of Inventory

Beginning balance

$ 72,000

Increase due to inventory purchases

?

= 404,000

Decrease due to recognizing cost of goods

sold

(398,000)

Ending balance

$ 78,000

Reconciliation of Accounts Payable*

Beginning balance

$ 28,000

Increase due to inventory purchases on acct.

404,000

Decrease due to cash settlements of accts. pay.

?

= (401,000)

Ending balance

$ 31,000

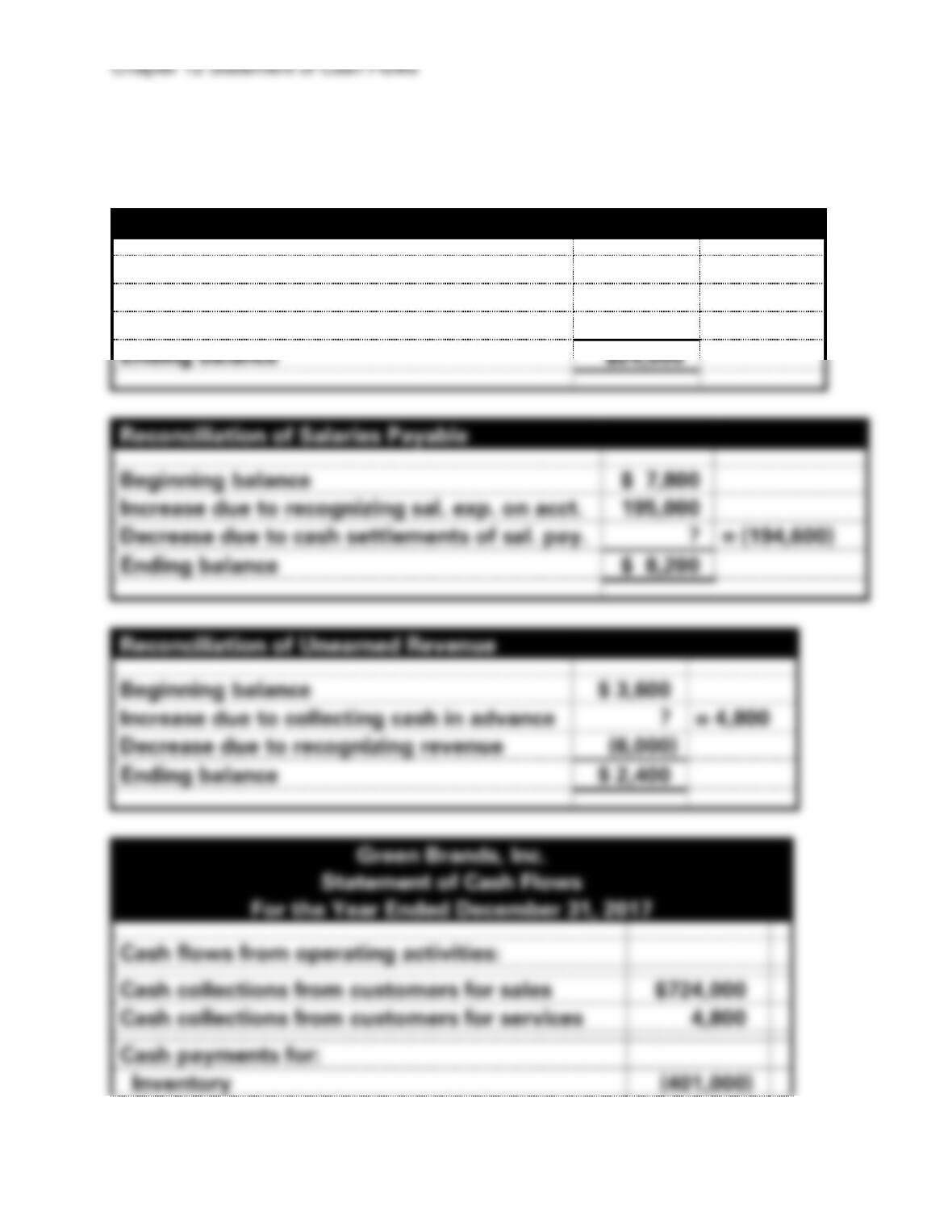

Cash flows from operating activities:

Cash collections from customers for sales

Cash collections from customers for services

Cash payments for:

PROBLEM 12-14A (cont.)

Reconciliation of Prepaid Insurance

Beginning balance

$ 32,000

Increase due to the cash outflow for ins.

?

= 28,000

Decrease due to recognizing ins. expense

(36,000)

Ending balance

$24,000

Reconciliation of Salaries Payable

Beginning balance

$ 7,800

Increase due to recognizing sal. exp. on acct.

195,000

Decrease due to cash settlements of sal. pay.

?

= (194,600)

Ending balance

$ 8,200

Reconciliation of Unearned Revenue

Beginning balance

$ 3,600

Increase due to collecting cash in advance

?

= 4,800

Decrease due to recognizing revenue

(6,000)

Ending balance

$ 2,400

Chapter 12 Statement of Cash Flows

12–25

Insurance

(28,000)

Salaries

(194,600)

Net cash inflow from operating activities

$105,200

Chapter 12 Statement of Cash Flows

12–26

PROBLEM 12-14A (cont.)

b. Begin by determining the amount of change in the balances in the

current asset, other than cash, and current liability accounts.

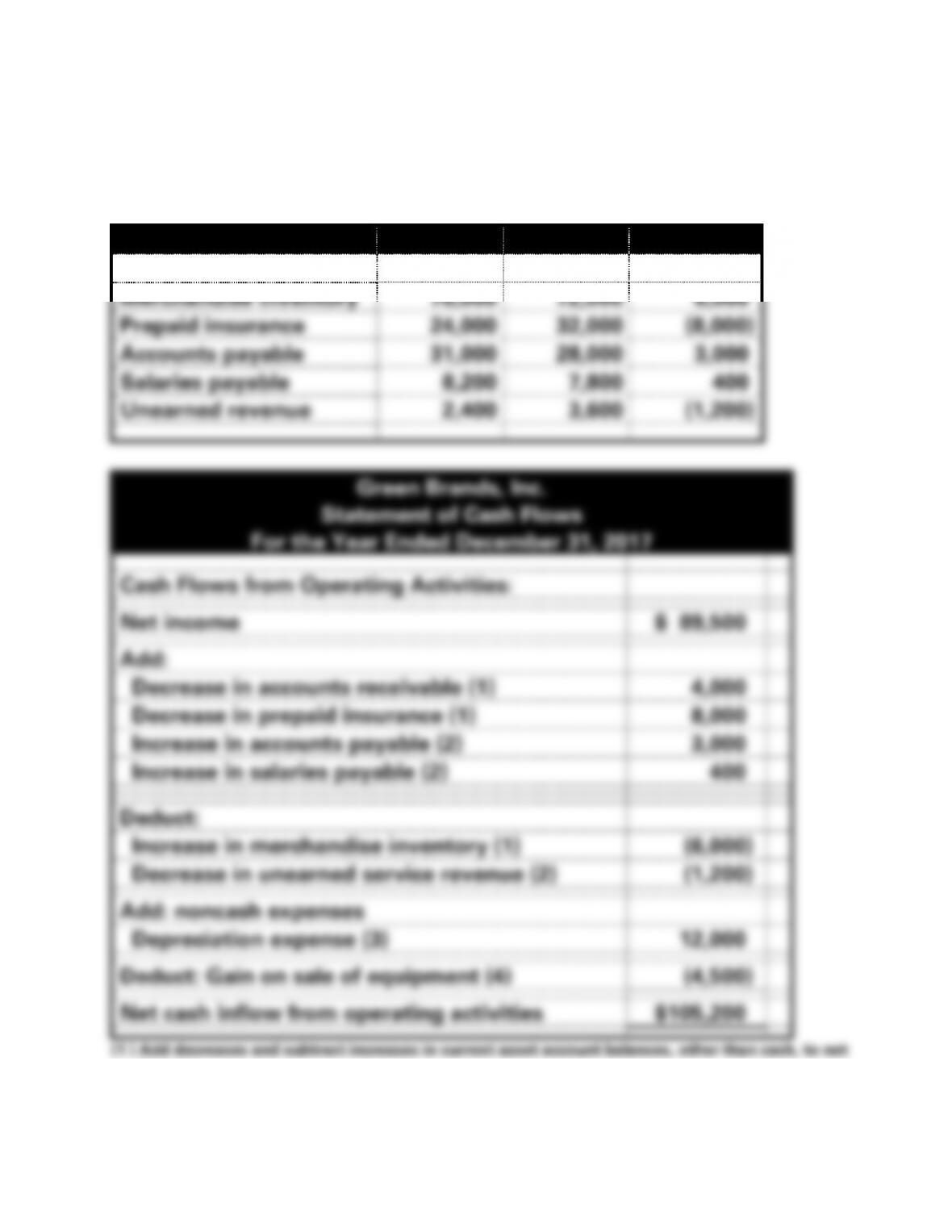

Account Title

2017

2016

Change

Accounts receivable

$48,000

$52,000

(4,000)

Merchandise inventory

78,000

72,000

6,000

Prepaid insurance

24,000

32,000

(8,000)

Accounts payable

31,000

28,000

3,000

Salaries payable

8,200

7,800

400

Unearned revenue

2,400

3,600

(1,200)

Green Brands, Inc.

Statement of Cash Flows

For the Year Ended December 31, 2017

Cash Flows from Operating Activities:

Net income

$ 89,500

Add:

Decrease in accounts receivable (1)

4,000

Decrease in prepaid insurance (1)

8,000

Increase in accounts payable (2)

3,000

Increase in salaries payable (2)

400

Deduct:

Increase in merchandise inventory (1)

(6,000)

Decrease in unearned service revenue (2)

(1,200)

Add: noncash expenses

Depreciation expense (3)

12,000

Deduct: Gain on sale of equipment (4)

(4,500)

Net cash inflow from operating activities

$105,200

(1 ) Add decreases and subtract increases in current asset account balances, other than cash, to net

income.

(2) Add increases and subtract decreases in current liability account balances to net income.

(3) Add noncash expenses (e.g., depreciation) to net income.

12–27

(4) Add losses and subtract gains from the sale of noncurrent assets to net income.

Chapter 12 Statement of Cash Flows

12–28

PROBLEM 12-15A

a.

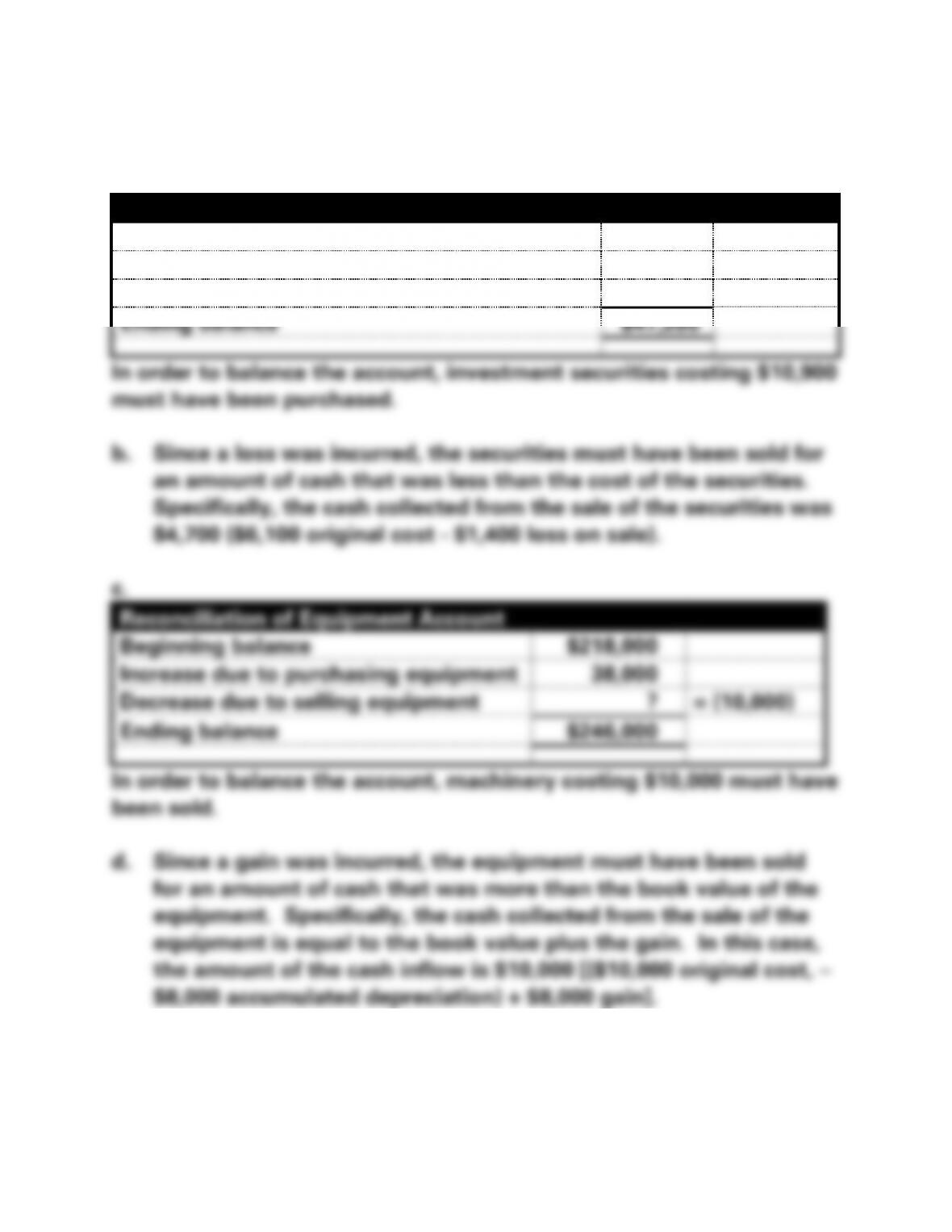

Reconciliation of Investment securities Account

Beginning balance

$42,400

Increase due to purchase of investment sec.

?

= 10,900

Decrease due to sale of investment sec.

(6,100)

Ending balance

$47,200

In order to balance the account, investment securities costing $10,900

must have been purchased.

b. Since a loss was incurred, the securities must have been sold for

an amount of cash that was less than the cost of the securities.

Specifically, the cash collected from the sale of the securities was

$4,700 ($6,100 original cost – $1,400 loss on sale).

c.

Reconciliation of Equipment Account

Beginning balance

$218,000

Increase due to purchasing equipment

38,000

Decrease due to selling equipment

?

= (10,000)

Ending balance

$246,000

In order to balance the account, machinery costing $10,000 must have

been sold.

d. Since a gain was incurred, the equipment must have been sold

for an amount of cash that was more than the book value of the

equipment. Specifically, the cash collected from the sale of the

equipment is equal to the book value plus the gain. In this case,

the amount of the cash inflow is $10,000 [($10,000 original cost, −

$8,000 accumulated depreciation) + $8,000 gain].

12–29

PROBLEM 12-15A (cont.)

e.

Reconciliation of Buildings Account

Beginning balance

$720,000

Increase due to purchasing buildings

?

= 136,000

Decrease due to cost of building demolished

(210,000)

Ending balance

$646,000

In order to balance the account, buildings costing $136,000 must have

been purchased. In the absence of information to the contrary, we

assume cash was paid to purchase the buildings.

f.

Reconciliation of Land Account

Beginning balance

$72,000

Increase due to purchasing land

?

= 53,000

Decrease due to selling land

(30,000)

Ending balance

$95,000

In order to balance the account, land costing $53,000 must have been

purchased. In the absence of information to the contrary, we assume

cash was paid to purchase the land.

g.

Mass Company

Statement of Cash Flows

For the Year Ended December 31, 2017

Cash Flows from Investing Activities:

Proceeds from sale of investment securities

$ 4,700

Proceeds from sale of equipment

10,000

Proceeds from sale of land

27,000

Paid to purchase investment securities

(10,900)

Paid to purchase equipment

(38,000)

Paid to purchase buildings

(136,000)

Paid to purchase land

(53,000)

Chapter 12 Statement of Cash Flows

12–30

Net cash outflow from investing activities

$(196,200)

PROBLEM 12-16A

a.

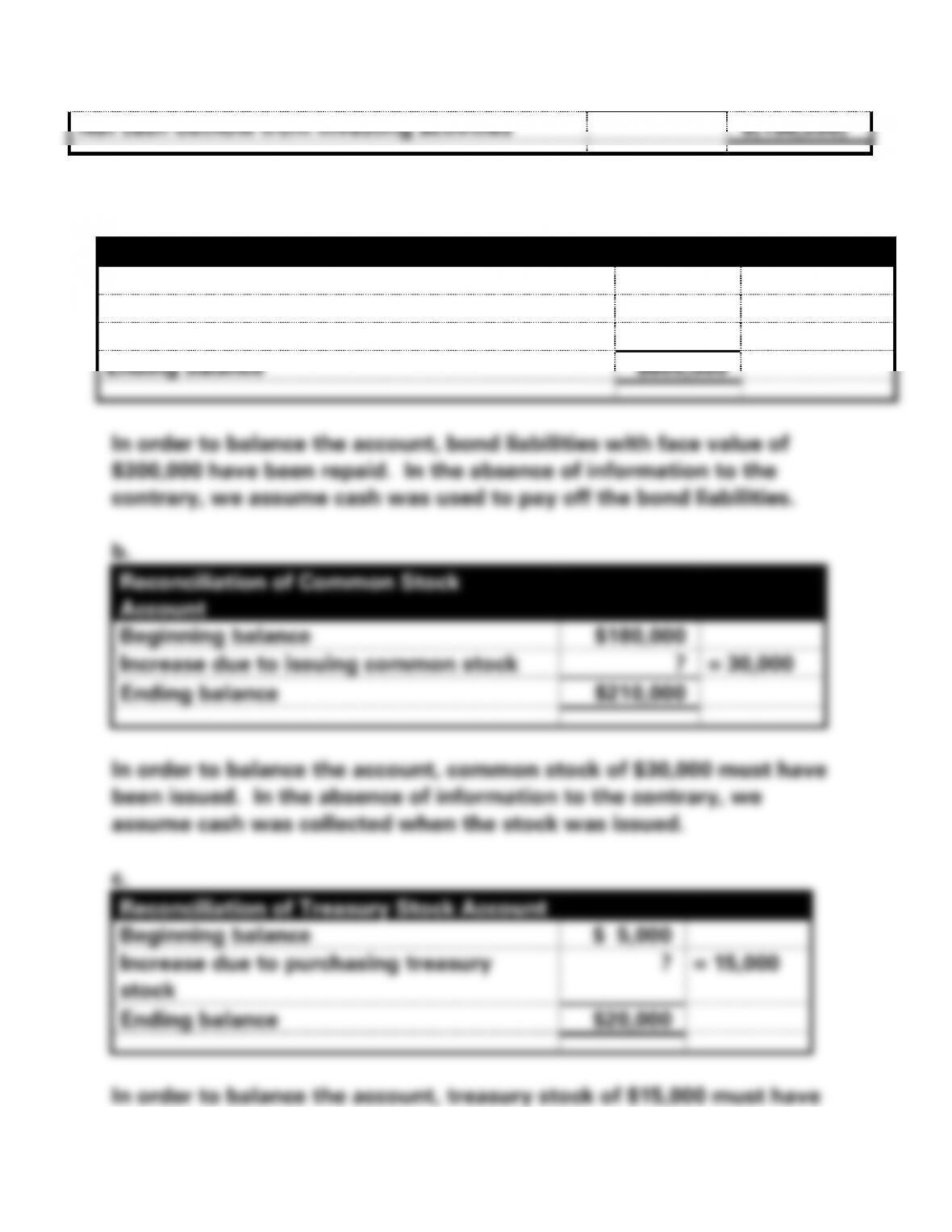

Reconciliation of Bonds Payable Account

Beginning balance

$800,000

Increase due to issuing bonds payable

100,000

Decrease due to cash settlements of bonds pay.

?

= (300,000)

Ending balance

$600,000

In order to balance the account, bond liabilities with face value of

$300,000 have been repaid. In the absence of information to the

contrary, we assume cash was used to pay off the bond liabilities.

b.

Reconciliation of Common Stock

Account

Beginning balance

$180,000

Increase due to issuing common stock

?

= 30,000

Ending balance

$210,000

In order to balance the account, common stock of $30,000 must have

been issued. In the absence of information to the contrary, we

assume cash was collected when the stock was issued.

c.

Reconciliation of Treasury Stock Account

Beginning balance

$ 5,000

Increase due to purchasing treasury

stock

?

= 15,000

Ending balance

$20,000

In order to balance the account, treasury stock of $15,000 must have

Chapter 12 Statement of Cash Flows

12–31

PROBLEM 12-16A (cont.)

d.

Reconciliation of Retained Earnings Account

Beginning balance

$75,000

Increase due to recognizing net income

32,000

Decrease due to paying dividends

?

= (21,000)

Ending balance

$86,000

Cash Flows from Financing Activities

Proceeds from issue of bond liabilities

$100,000

Proceeds from issue of common stock

30,000

Repayment of bond liabilities

(300,000)

Paid for purchase of treasury stock

(15,000)

Payment of dividends

(21,000)

Net cash outflow from financing activities

$(206,000)

Chapter 12 Statement of Cash Flows

12–32

PROBLEM 12-17A

Item

Type of Activity

Add or Subtract

a.

Operating

Subtract

b.

Operating

Add

c.

Investing

Subtract

d.

Operating

Subtract

e.

Financing

Subtract

f.

Operating

Subtract

g.

Operating

Add

h.

Financing

Subtract

i.

Operating

Add

j.

Investing

Add

k.

Financing

Add

l.

Financing

Subtract

m.

Operating

Add

n.

Financing

Add

12–33

PROBLEM 12-18A

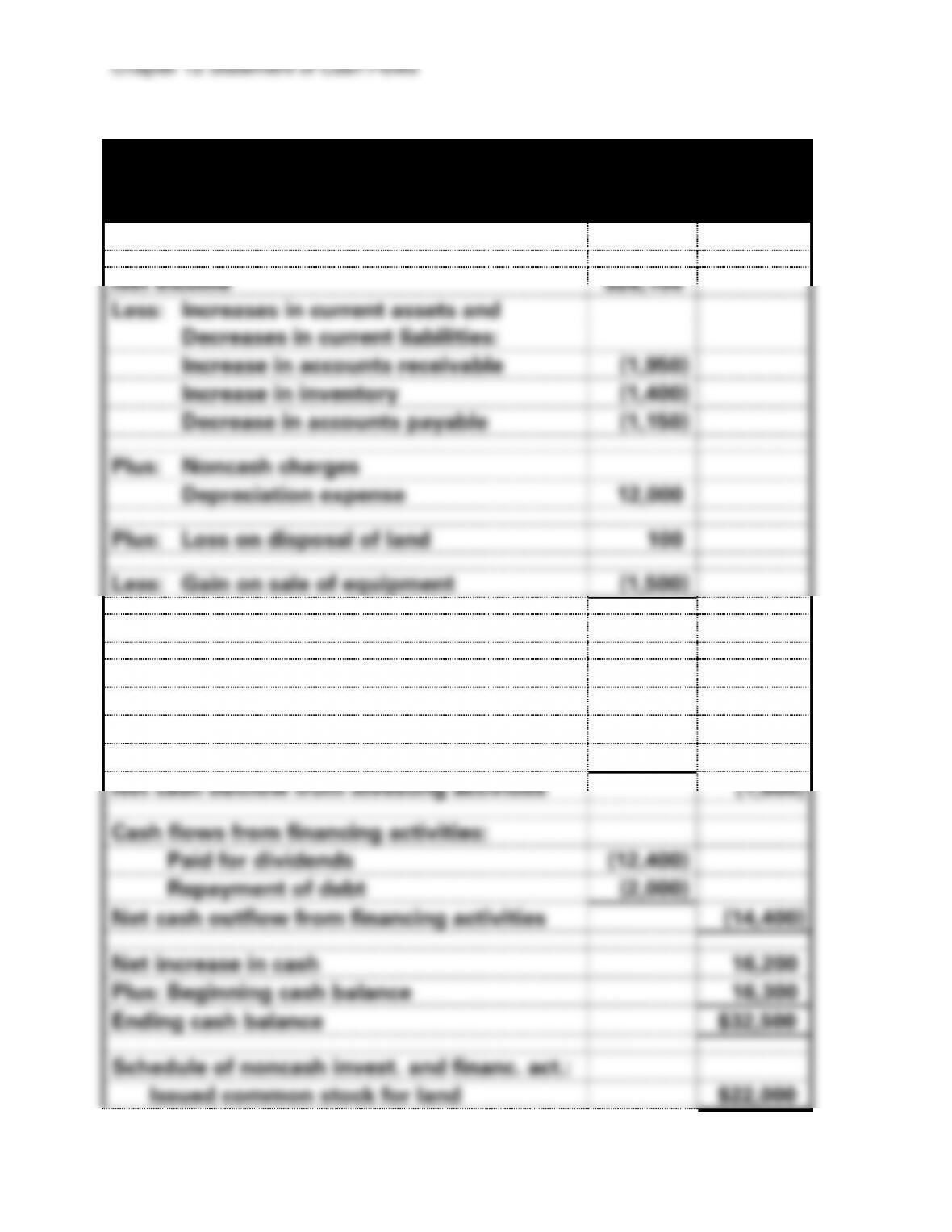

Gypsy Company

Statement of Cash Flows

For the Year Ended December 31, 2017

Cash flows from operating activities:

Net income

$26,100

Less: Increases in current assets and

Decreases in current liabilities:

Increase in accounts receivable

(1,950)

Increase in inventory

(1,400)

Decrease in accounts payable

(1,150)

Plus: Noncash charges

Depreciation expense

12,000

Plus: Loss on disposal of land

100

Less: Gain on sale of equipment

(1,500)

Net cash inflow from operating activities

$32,200

Cash flows from investing activities:

Proceeds from sale of equipment

21,500

Proceeds from sale of land

5,900

Paid to purchase equipment

(29,000)

Net cash outflow from investing activities

(1,600)

Cash flows from financing activities:

Paid for dividends

(12,400)

Repayment of debt

(2,000)

Net cash outflow from financing activities

(14,400)

Net increase in cash

16,200

Plus: Beginning cash balance

16,300

Ending cash balance

$32,500

Schedule of noncash invest. and financ. act.:

Issued common stock for land

$22,000

Chapter 12 Statement of Cash Flows

12–34

12–35

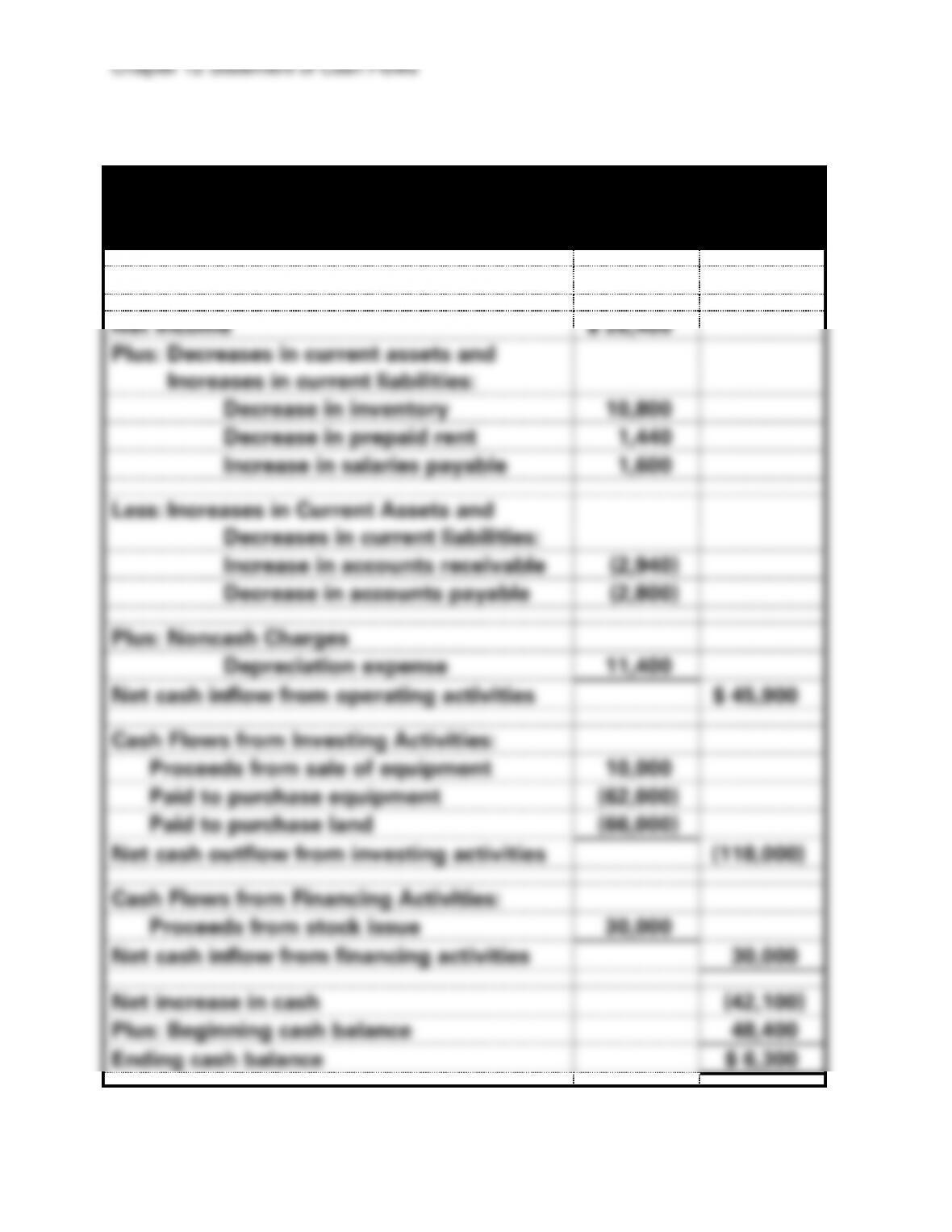

PROBLEM 12-19A

Raceway Corporation

Statement of Cash Flows

For the Year Ended December 31, 2017

Cash Flows From Operating Activities:

Net Income

$ 26,400

Plus: Decreases in current assets and

Increases in current liabilities:

Decrease in inventory

10,800

Decrease in prepaid rent

1,440

Increase in salaries payable

1,600

Less: Increases in Current Assets and

Decreases in current liabilities:

Increase in accounts receivable

(2,940)

Decrease in accounts payable

(2,800)

Plus: Noncash Charges

Depreciation expense

11,400

Net cash inflow from operating activities

$ 45,900

Cash Flows from Investing Activities:

Proceeds from sale of equipment

10,000

Paid to purchase equipment

(62,000)

Paid to purchase land

(66,000)

Net cash outflow from investing activities

(118,000)

Cash Flows from Financing Activities:

Proceeds from stock issue

30,000

Net cash inflow from financing activities

30,000

Net increase in cash

(42,100)

Plus: Beginning cash balance

48,400

Ending cash balance

$ 6,300

Chapter 12 Statement of Cash Flows

12–36

PROBLEM 12-20A

a.

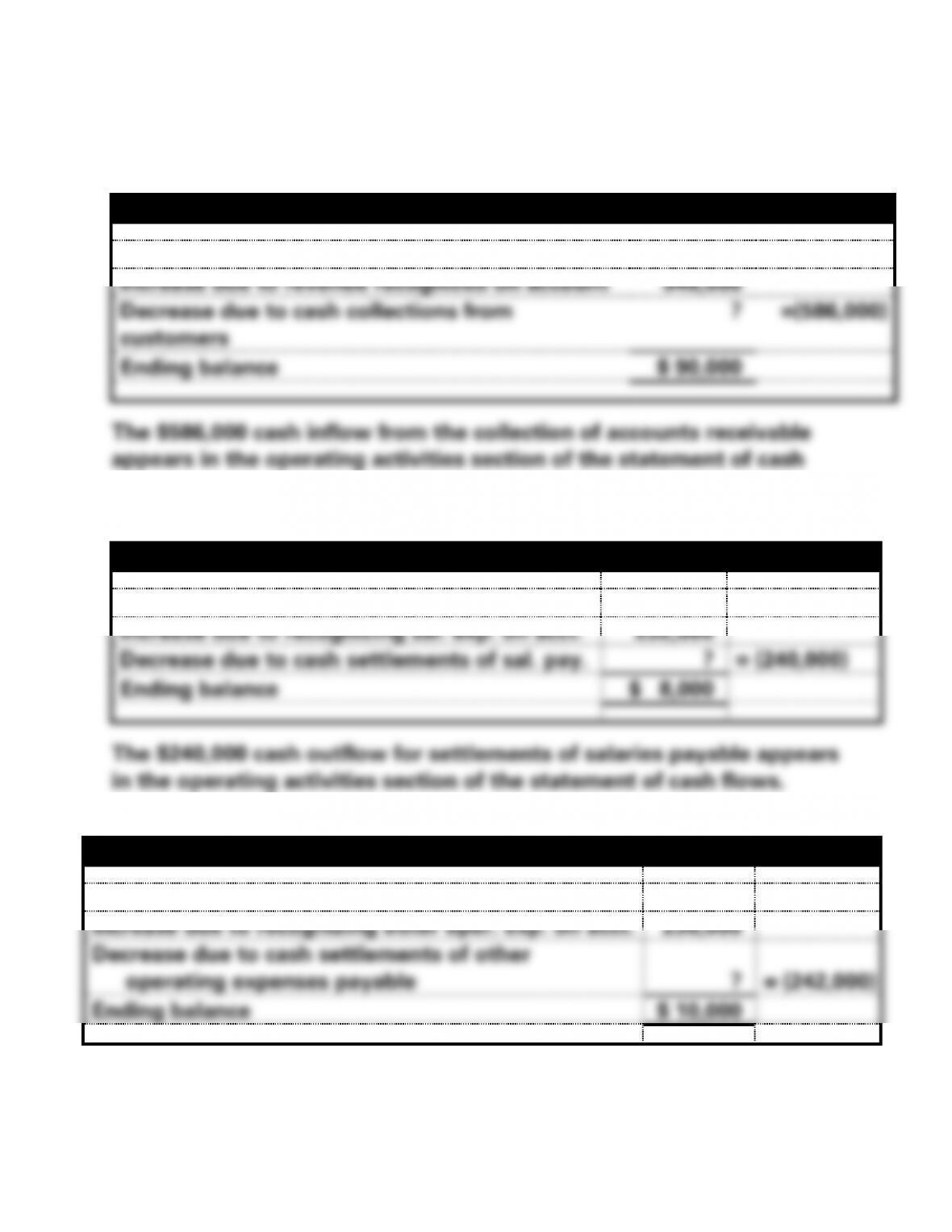

(1)

Reconciliation of Accounts Receivable Account

Beginning balance

$128,000

Increase due to revenue recognized on account

548,000

Decrease due to cash collections from

customers

?

=(586,000)

Ending balance

$ 90,000

flows.

(2)

Reconciliation of Salaries Payable Account

Beginning balance

$ 16,000

Increase due to recognizing sal. exp. on acct.

232,000

Decrease due to cash settlements of sal. pay.

?

= (240,000)

Ending balance

$ 8,000

(3)

Reconciliation of Other Operating Expenses Payable

Beginning balance

$ 16,000

Increase due to recognizing other oper. exp. on acct.

236,000

Decrease due to cash settlements of other

operating expenses payable

?

= (242,000)

Ending balance

$ 10,000

Chapter 12 Statement of Cash Flows

12–37

12–38

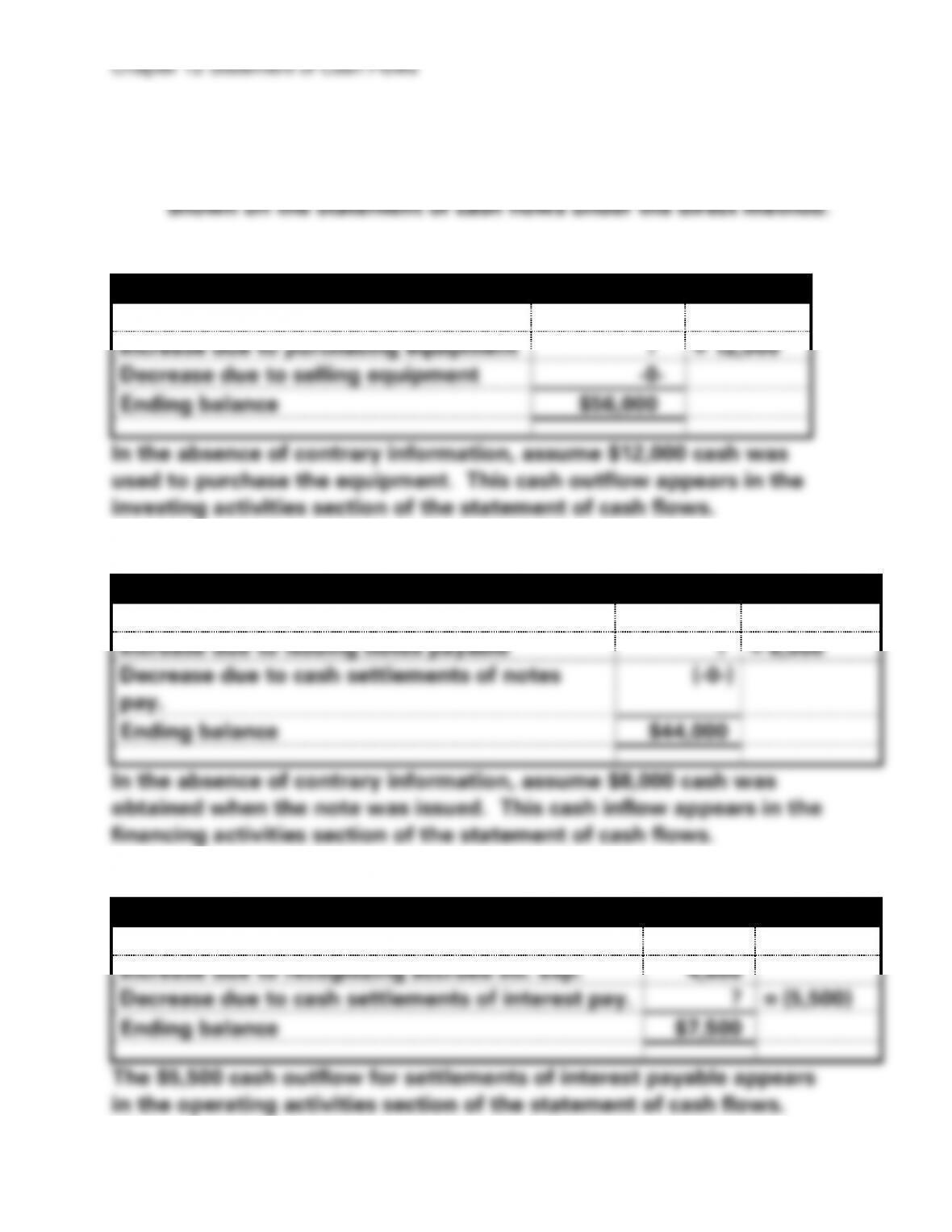

PROBLEM 12-20A (cont.)

(4) Depreciation expense does not affect cash flow and is not

(5)

Reconciliation of Equipment Account

Beginning balance

$44,000

Increase due to purchasing equipment

?

= 12,000

Decrease due to selling equipment

-0-

Ending balance

$56,000

In the absence of contrary information, assume $12,000 cash was

used to purchase the equipment. This cash outflow appears in the

investing activities section of the statement of cash flows.

(6)

Reconciliation of Notes Payable Account

Beginning balance

$36,000

Increase due to issuing notes payable

?

= 8,000

Decrease due to cash settlements of notes

pay.

(-0-)

Ending balance

$44,000

In the absence of contrary information, assume $8,000 cash was

obtained when the note was issued. This cash inflow appears in the

financing activities section of the statement of cash flows.

(7)

Reconciliation of Interest Payable Account

Beginning balance

$8,400

Increase due to recognizing accrued int. exp.

4,600

Decrease due to cash settlements of interest pay.

?

= (5,500)

Ending balance

$7,500

The $5,500 cash outflow for settlements of interest payable appears

in the operating activities section of the statement of cash flows.

Chapter 12 Statement of Cash Flows

12–39

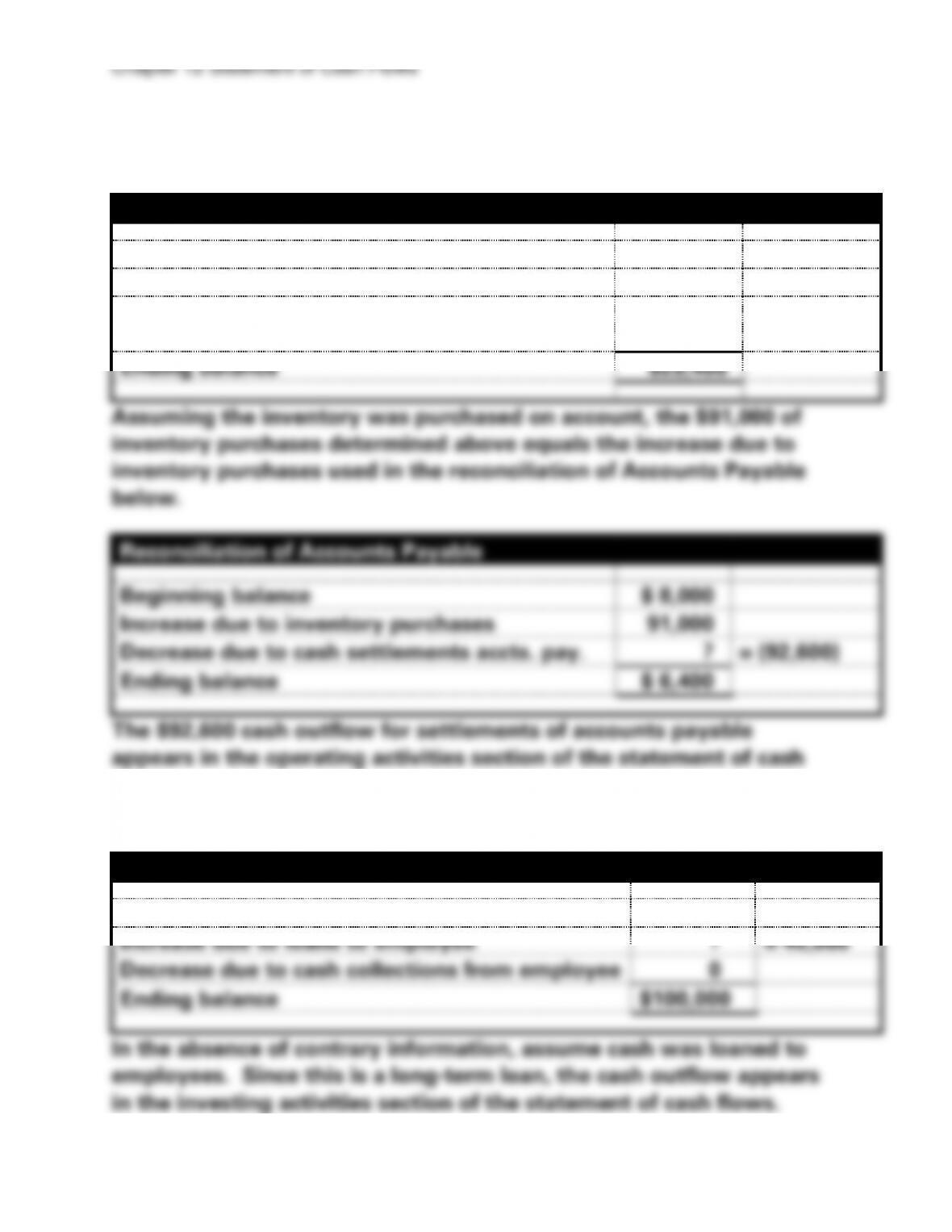

Beginning balance

Increase due to inventory purchases

Decrease due to cash settlements accts. pay.

= (92,600)

Ending balance

Reconciliation of Notes Receivable

Beginning balance

Increase due to loans to employee

Decrease due to cash collections from employee

Ending balance

PROBLEM 12-20A (cont.)

(8)

Reconciliation of Inventory

Beginning balance

$ 22,000

Increase due to inventory purchases

?

= 91,000

Decrease due to recognizing cost of goods

sold

(83,600)

Ending balance

$29,400