2–69

m. Beg. RE $47,500 + NI $20,850 − Div. $2,000 = Ending retained earnings $66,350

2–70

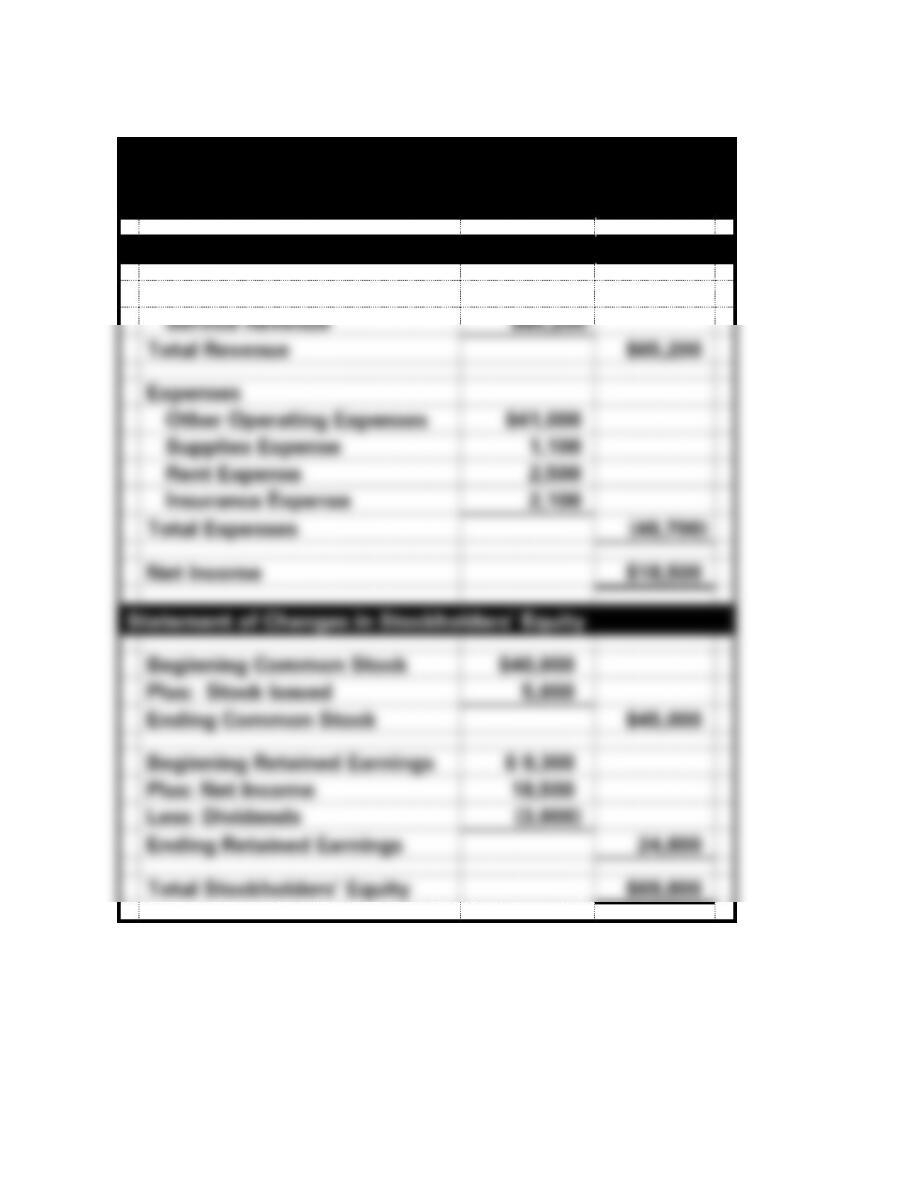

PROBLEM 2-41A

Barker Company

Financial Statements

For the Year Ended December 31, 2016

Income Statement

Revenue

Service Revenue

$65,200

Total Revenue

$65,200

Expenses

Other Operating Expenses

$41,000

Supplies Expense

1,100

Rent Expense

2,500

Insurance Expense

2,100

Total Expenses

(46,700)

Net Income

$18,500

Statement of Changes in Stockholders’ Equity

Beginning Common Stock

$40,000

Plus: Stock Issued

5,000

Ending Common Stock

$45,000

Beginning Retained Earnings

$ 9,300

Plus: Net Income

18,500

Less: Dividends

(3,000)

Ending Retained Earnings

24,800

Total Stockholders’ Equity

$69,800

2–71

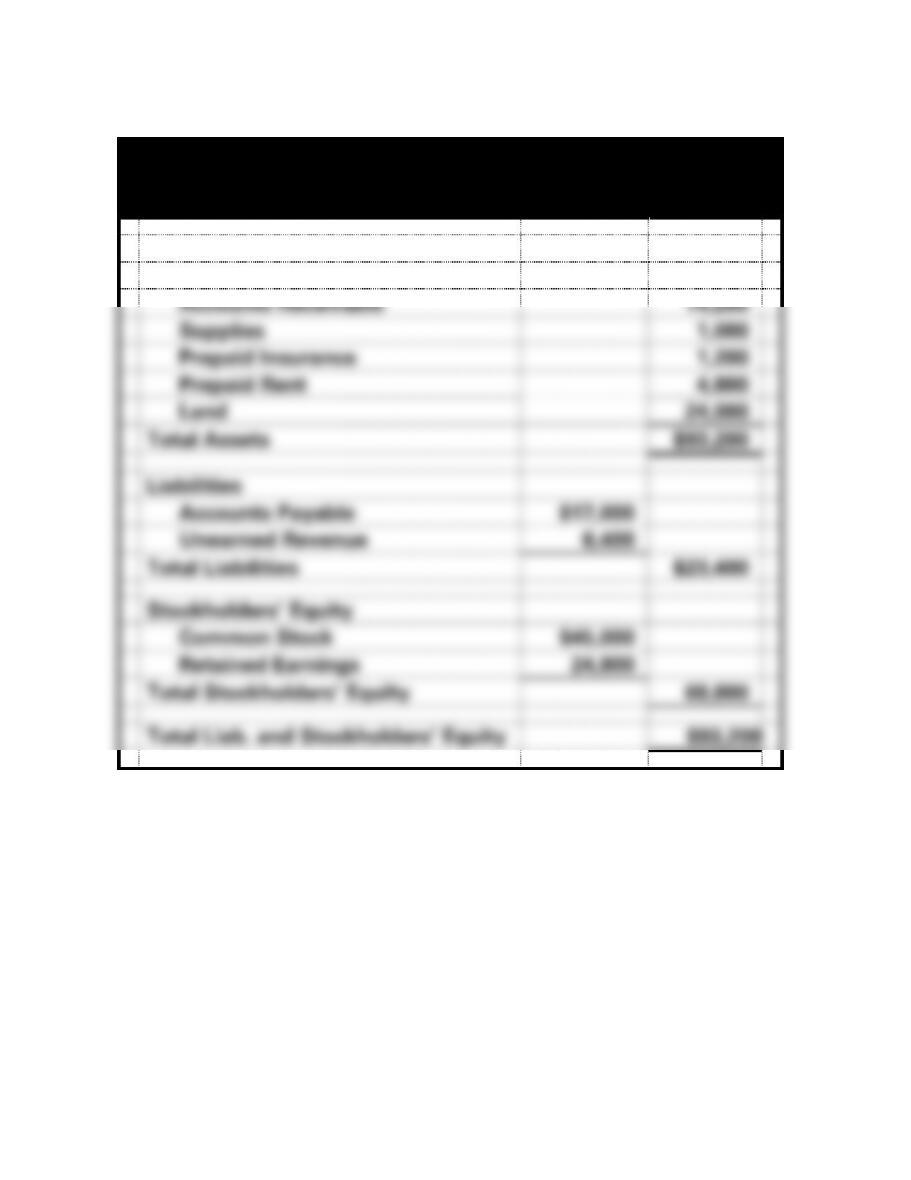

PROBLEM 2-41A (cont.)

Barker Company

Balance Sheet

As of December 31, 2016

Assets

Cash

$ 48,000

Accounts Receivable

14,200

Supplies

1,000

Prepaid Insurance

1,200

Prepaid Rent

4,800

Land

24,000

Total Assets

$93,200

Liabilities

Accounts Payable

$17,000

Unearned Revenue

6,400

Total Liabilities

$23,400

Stockholders’ Equity

Common Stock

$45,000

Retained Earnings

24,800

Total Stockholders’ Equity

69,800

Total Liab. and Stockholders’ Equity

$93,200

2–72

PROBLEM 2-41A (cont.)

Barker Company

Statement of Cash Flows

For the Year Ended December 31, 2016

Cash Flow From Operating Activities

$15,600

Cash Flow From Investing Activities

(5,200)

Cash Flow From Financing Activities

(5,000)

Net Change in Cash

5,400

Plus: Beginning Cash Balance

42,600*

Ending Cash Balance

$48,000

2–73

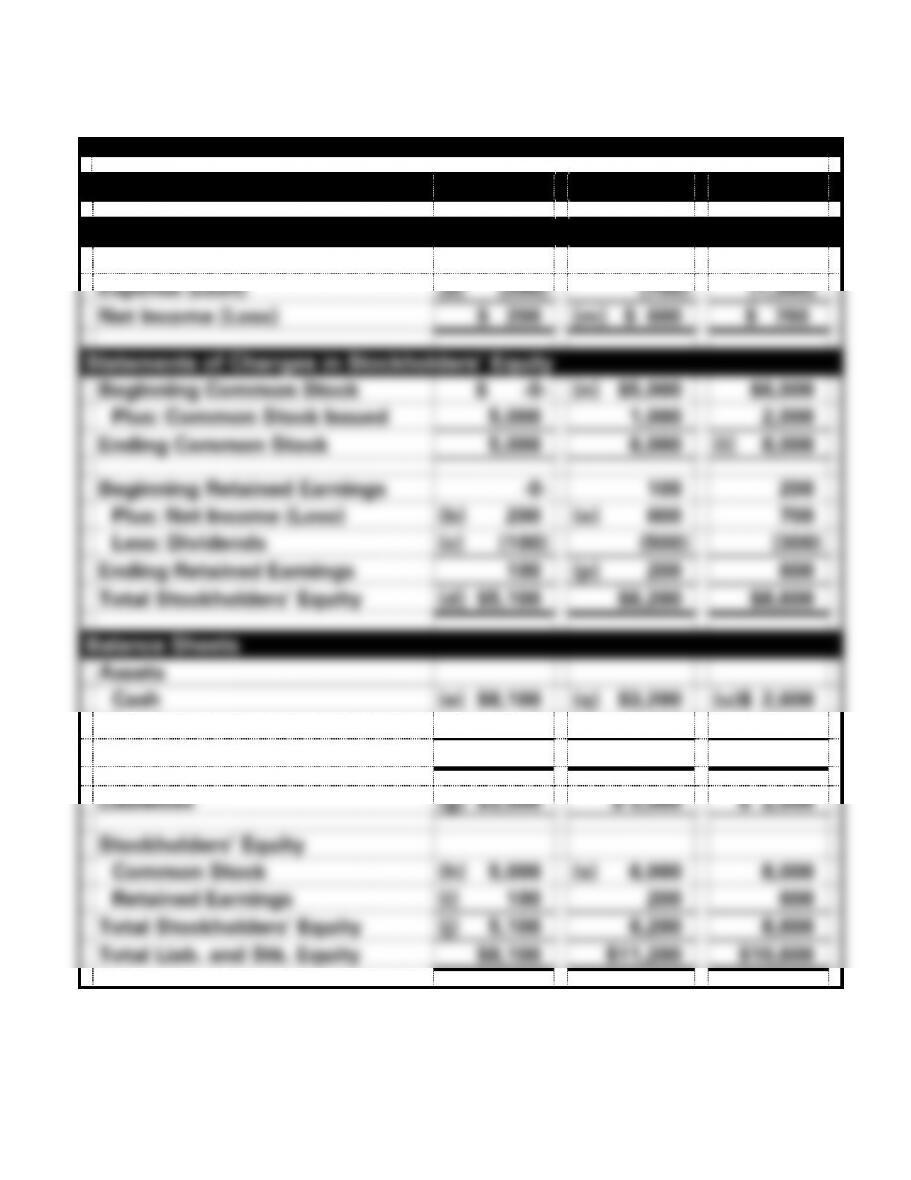

PROBLEM 2-42A

FOR THE YEARS

2016

2017

2018

Income Statements

Revenue (cash)

$ 700

$1,300

$ 2,000

Expense (cash)

(a) (500)

(700)

(1,300)

Net Income (Loss)

$ 200

(m) $ 600

$ 700

Statements of Changes in Stockholders’ Equity

Beginning Common Stock

$ -0-

(n) $5,000

$6,000

Plus: Common Stock Issued

5,000

1,000

2,000

Ending Common Stock

5,000

6,000

(t) 8,000

Beginning Retained Earnings

-0-

100

200

Plus: Net Income (Loss)

(b) 200

(o) 600

700

Less: Dividends

(c) (100)

(500)

(300)

Ending Retained Earnings

100

(p) 200

600

Total Stockholders’ Equity

(d) $5,100

$6,200

$8,600

Balance Sheets

Assets

Cash

(e) $8,100

(q) $3,200

(u)$ 2,600

Land

-0-

(r) 8,000

8,000

Total Assets

(f) $8,100

$11,200

$10,600

Liabilities

(g) $3,000

$ 5,000

$ 2,000

Stockholders’ Equity

Common Stock

(h) 5,000

(s) 6,000

8,000

Retained Earnings

(i) 100

200

600

Total Stockholders’ Equity

(j) 5,100

6,200

8,600

Total Liab. and Stk. Equity

$8,100

$11,200

$10,600

2–74

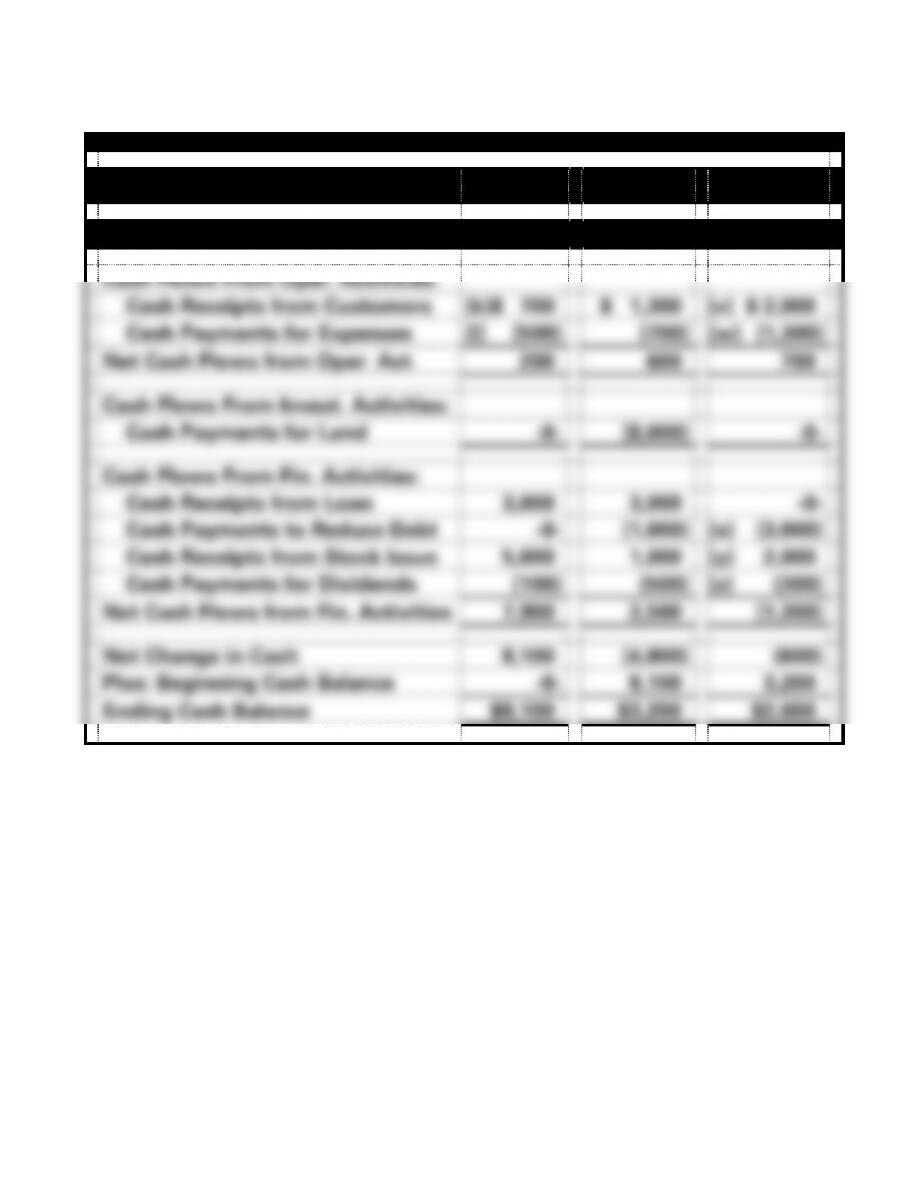

PROBLEM 2-42A (cont.)

FOR THE YEARS

2016

2017

2018

Statements of Cash Flows

Cash Flows From Oper. Activities:

Cash Receipts from Customers

(k)$ 700

$ 1,300

(v) $ 2,000

Cash Payments for Expenses

(l) (500)

(700)

(w) (1,300)

Net Cash Flows from Oper. Act.

200

600

700

Cash Flows From Invest. Activities:

Cash Payments for Land

-0-

(8,000)

-0-

Cash Flows From Fin. Activities:

Cash Receipts from Loan

3,000

3,000

-0-

Cash Payments to Reduce Debt

-0-

(1,000)

(x) (3,000)

Cash Receipts from Stock Issue

5,000

1,000

(y) 2,000

Cash Payments for Dividends

(100)

(500)

(z) (300)

Net Cash Flows from Fin. Activities

7,900

2,500

(1,300)

Net Change in Cash

8,100

(4,900)

(600)

Plus: Beginning Cash Balance

-0-

8,100

3,200

Ending Cash Balance

$8,100

$3,200

$2,600

2–75

PROBLEM 2-42A (cont.)

Computations of amounts:

a. $500 Expense = $700 Revenue − $200 Net Income.

b. $200 Net Income = $200 Net Income from Income Statement.

c. $100 Dividends = $200 Net Income − $100 Ending Ret. Earnings.

k. $700 Cash Receipts from Revenue = $700 Revenue from Income Statement.

l. $500 Cash Payment for Expenses = $500 Expense from Income Statement.

m. $600 Net Income = $1,300 Revenue − $700 Expense.

n. $5,000 Beginning Common Stock = $5,000 Ending Common Stock 2016.

o. $600 Net Income = $600 Net Income from Income Statement.

w. $1,300 Cash Payments for Expenses = $1,300 Expense from Income Statement.

x. $3,000 Cash Payment to Reduce Debt = $5,000 Balance of Liabilities, 2017− $2,000

Balance of Liabilities, 2018.

y. $2,000 Cash Receipts from Stock Issue = $2,000 Stock Issued from Statement of

Changes in Stockholders’ Equity.

2–76

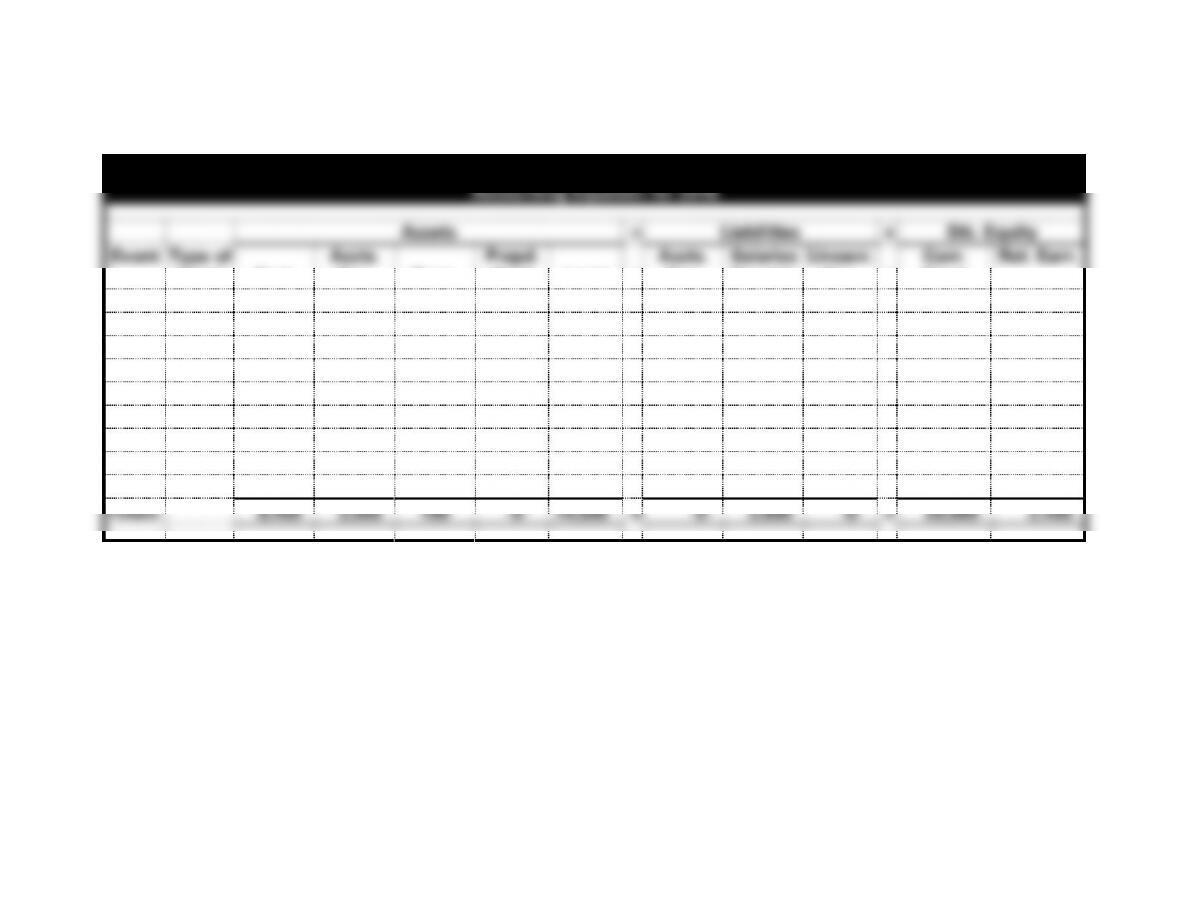

PROBLEM 2-43a

a.

Alcorn Service Company

Accounting Equation for 2016

Assets

=

Liabilities

+

Stk. Equity

Event

Type of

Event

Cash

Accts.

Rec.

Supp.

Prepd.

Rent

Land

=

Accts.

Pay.

Salaries

Payable

Unearn.

Rev.

+

Com.

Stock

Ret. Earn.

1.

AS

20,000

20,000

2.

AS

800

800

3.

AE

(14,000)

14,000

4.

AU

(800)

(800)

5.

AS

10,500

10,500

6.

AU

(3,800)

(3,800)

7.

AE

7,000

(7,000)

8.

CE

3,600

(3,600)

9.

AU

(700)

(700)

Totals

8,400

3,500

100

-0-

14,000

=

-0-

3,600

-0-

+

20,000

2,400

2–77

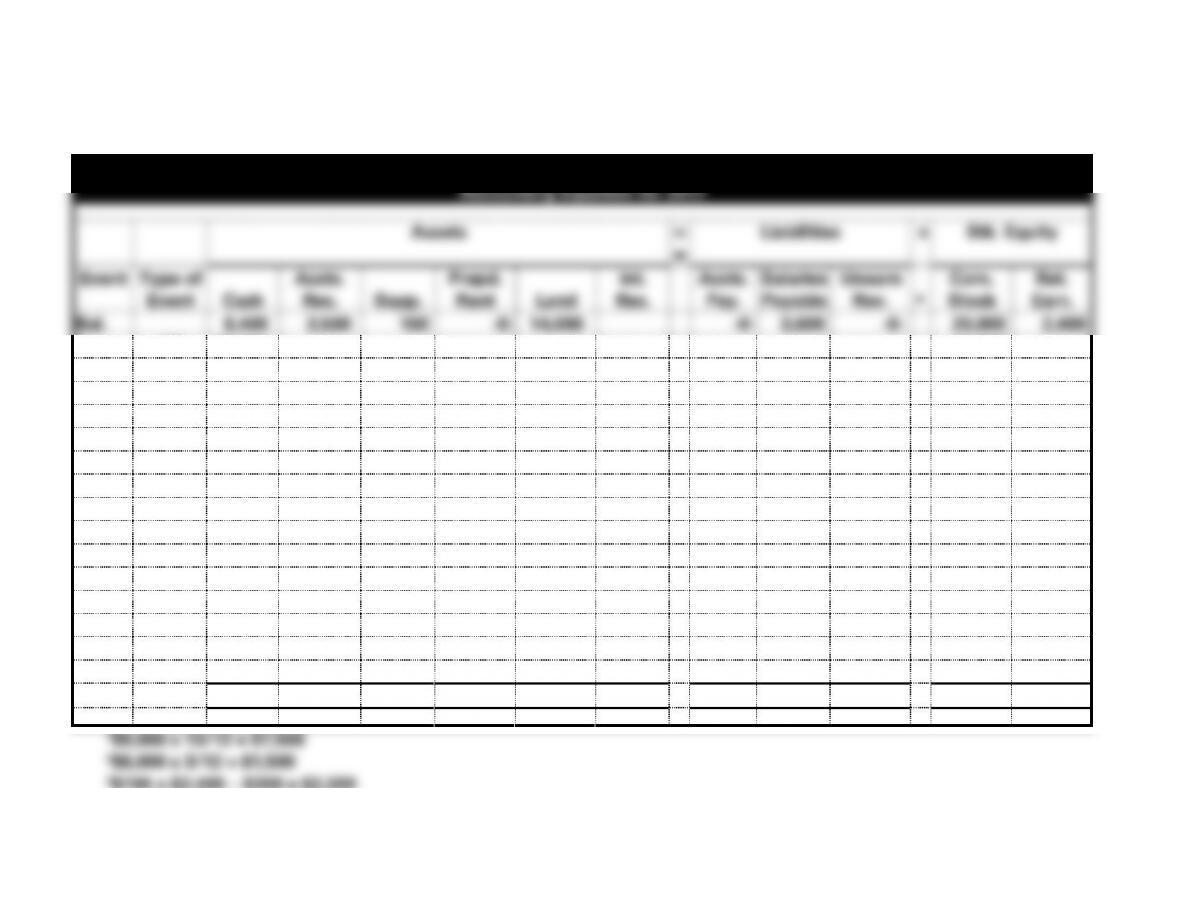

PROBLEM 2-43A a. (cont.)

Alcorn Service Company

Accounting Equation for 2017

Assets

=

=

Liabilities

+

Stk. Equity

Event

Type of

Event

Cash

Accts.

Rec.

Supp.

Prepd.

Rent

Land

Int.

Rec.

Accts.

Pay.

Salaries

Payable

Unearn

Rev.

+

Com.

Stock

Ret.

Earn.

Bal.

8,400

3,500

100

-0-

14,000

-0–

3,600

-0-

20,000

2,400

1.

AS

15,000

15,000

2.

AU

(3,600)

(3,600)

3.

AE

(9,000)

9,000

4.

AE

14,000

(14,000)

5.

AS

6,000

6,000

6.

AS

2,400

2,400

7.

AS

24,500

24,500

8.

AE

12,600

(12,600)

9.

AU

(2,000)

(2,000)

10.

AU

(2,850)

(2,850)

11.

AU

(7,500)1

(7,500)

12.

CE

(1,500)2

1,500

13.

AU

(2,200)3

(2,200)

14.

CE

4,800

(4,800)

15.

AS

500

500

Totals

38,550

15,400

300

1,500

-0–

500

2,400

4,800

4,500

+

35,000

9,550

2–78

2–79

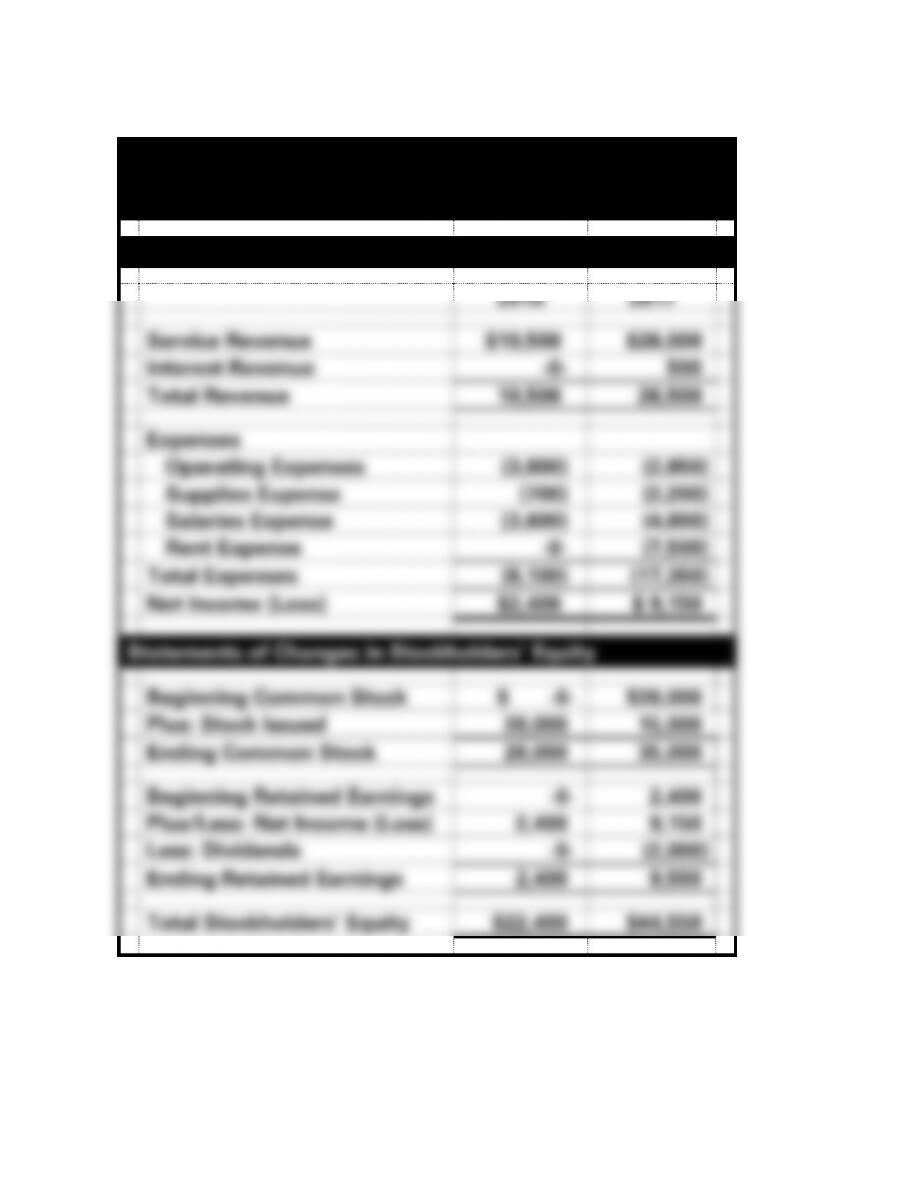

PROBLEM 2-43A (cont.)

b.

Alcorn Service Company

Financial Statements

For the Years Ended December 31, 2016 and 2017

Income Statements

2016

2017

Service Revenue

$10,500

$26,000

Interest Revenue

-0-

500

Total Revenue

10,500

26,500

Expenses

Operating Expenses

(3,800)

(2,850)

Supplies Expense

(700)

(2,200)

Salaries Expense

(3,600)

(4,800)

Rent Expense

-0-

(7,500)

Total Expenses

(8,100)

(17,350)

Net Income (Loss)

$2,400

$ 9,150

Statements of Changes in Stockholders’ Equity

Beginning Common Stock

$ -0-

$20,000

Plus: Stock Issued

20,000

15,000

Ending Common Stock

20,000

35,000

Beginning Retained Earnings

-0-

2,400

Plus/Less: Net Income (Loss)

2,400

9,150

Less: Dividends

-0-

(2,000)

Ending Retained Earnings

2,400

9,550

Total Stockholders’ Equity

$22,400

$44,550

2–80

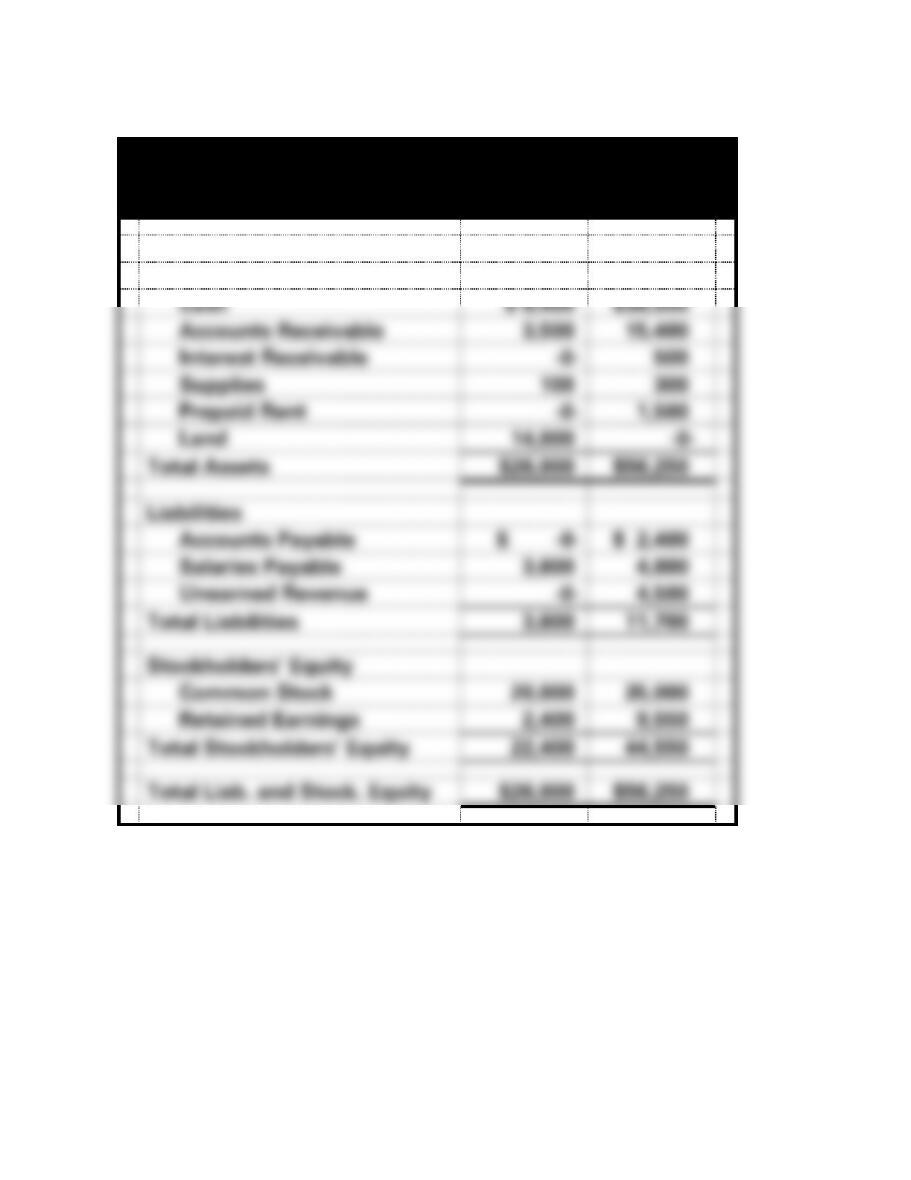

PROBLEM 2-43A b. (cont.)

Alcorn Service Company

Balance Sheets

As of December 31, 2016 and 2017

2016

2017

Assets

Cash

$ 8,400

$38,550

Accounts Receivable

3,500

15,400

Interest Receivable

-0-

500

Supplies

100

300

Prepaid Rent

-0-

1,500

Land

14,000

-0-

Total Assets

$26,000

$56,250

Liabilities

Accounts Payable

$ -0-

$ 2,400

Salaries Payable

3,600

4,800

Unearned Revenue

-0-

4,500

Total Liabilities

3,600

11,700

Stockholders’ Equity

Common Stock

20,000

35,000

Retained Earnings

2,400

9,550

Total Stockholders’ Equity

22,400

44,550

Total Liab. and Stock. Equity

$26,000

$56,250

2–81

PROBLEM 2-43A b. (cont.)

Alcorn Service Company

Statements of Cash Flows

For the Years Ended December 31, 2016 and 2017

2016

2017

Cash Flows From Operating Activities:

Cash Receipts from Customers1

$7,000

$18,600

Cash Payments for Expense2

(4,600)

(15,450)

Net Cash Flow from Operating Activities

2,400

3,150

Cash Flows From Investing Activities:

Cash Payment for Land

(14,000)

-0-

Cash Proceeds from Sale of Land

-0-

14,000

Net Cash Flow From Investing Activities

(14,000)

14,000

Cash Flows From Financing Activities:

Cash Receipts from Stock Issue

20,000

15,000

Cash Payment for Dividends

-0-

(2,000)

Net Cash Flow From Financing Activities

20,000

13,000

Net Change in Cash

8,400

30,150

Plus: Beginning Cash Balance

-0-

8,400

Ending Cash Balance

$8,400

$38,550

2–82

PROBLEM 2-44A

1. The availability of an opportunity

2. The existence of some sort of pressure

3. The capacity for rationalization

1. Even though Pete has exceeded his authority, no one has

2. Pete is in a financial bind and does not want to discuss his

3. He rationalizes that his actions do not hurt anyone because the

fee.

2–83

PROBLEM 2-45A (Appendix)

Accounting Equation (Prepared for Instructor’s Use)

Accounting Equation

Assets

Liabilities

Stk. Equity

Date

Cash

Acc Rec.

Pp.

Rent

Supp.

CD

Int.

Rec.

Truck

Acc

Depr.

Land

Acc.

Pay.

Sal.

Pay.

Note

Pay.

Int

Pay.

Unear.

Rev.

Com.

Stock

Ret.

Earn

Bal.

26,000

9,000

42,000

5,000

28,000

44,000

1/1

15,000

15,000

1/1

(22,000)

22,000

2/1

12,000

12,000

2/1

(3,000)

3,000

3/1

(2,000)

(2,000)

4/1

(28,000)

28,000

5/1

(4,000)

(4,000)

7/1

5,400

5,400

9/1

42,000

(42,000)

10/1

5,000

5,000

11/1

(50,000)

50,000

12/31

42,000

42,000

12/31

40,000

(40,000)

12/31

6,000

(6,000)

12/31

5,200

(5,200)

12/31

(4,800)

(4,800)

12/31a

(5,000)1

(5,000)

12/31a

9902

(990)

12/31a

(2,750)3

(2,750)

12/31a

(2,700)4

2,700

12/31a

5005

500

Bal.

31,400

11,000

250

200

50,000

500

22,000

(5,000)

28,000

12,000

5,200

12,000

990

2,700

43,000

62,460

(1) 12/31a Depreciation Expense $22,000 − $2,000 = $20,000; $20,000 4 = $5,000

(2) 12/31a Interest Expense $12,000 x 9% = $1,080; $1,080 x 11/12 = $990

(3) 12/31a Expired Rent $3,000 x 11/12 = $2,750

(4) 12/31a Unearned Revenue earned $5,400 x 6/12 = $2,700

(5) 12/31a Interest Earned $50,000 x 6% = $3,000; $3,000 x 2/12 = $500

2-84

PROBLEM 2-45A (cont.)

1. Jan. 1, purchase of truck; depreciation expense.

2. Feb. 1, note payable issued; interest expense.

3. Feb. 1, prepaid rent; rent expense.

4. July 1, unearned revenue; cash was received in advance; earned

revenue.

5. Nov. 1, purchase of CD; interest revenue.

b. $12,000 X 9% X 11/12 = $990

c. $40,000 + $5,400 − $3,000 − $4,000 = $38,400

d. $3,000 X 11/12 = $2,750

2-85