9-1

Chapter 9

Accounting for Liabilities and Payroll

General Comments for Chapter 9

Students were initially introduced to the concept of accounts payable in Chapter 2. Chapter 9

looks at liabilities in more depth by exploring sales tax and payroll tax payables. Contingent

liabilities, accounting for warranty obligations, the going concern concept, and the classified

balance sheet are also introduced in this chapter. Since most students have had some type of

job experience, they will be able to relate to the discussions around wages and payroll taxes

payable. Chapter 2 introduced the concept of interest payable but students were provided

with the amount of interest expense and interest payable. In Chapter 9, students learn how to

compute interest expense and interest payable when a partial year of interest is payable at the

end of the accounting cycle.

If you would like to begin the chapter with a problem-based learning exercise, see the notes

below.

Problem-Based Learning Case:

Warranty Expenses

Instructions: The case appears on the following page in a format you can copy or display.

Distribute copies of the case to the class before providing any explanation of bad debt or war-

ranty expenses. Ask students to read the case and individually develop answers. After al-

lowing students time to develop their individual answers, put them into groups to reach con-

sensus on an answer. Also, ask each group to select a spokesperson. Allow groups time to

develop answers, then call on some of the spokespersons to share their solutions. As you re-

spond to the student solutions, explain the basic concepts of accounting for warranty expens-

es.

The correct answer is:

Fees revenue

$ 180,000

Warranty expense

(1,200)

Other operating expenses

(120,000)

Net income

$ 58,800

9-2

Chapter 9 Problem-Based Learning Case:

Bad Debts and Warranty Expenses

Wilson Eye Care earned $180,000 of revenue on account during

2016. Wilson offers its customers a one–year “satisfaction or your

money back” guarantee. Very few customers return their eye-

glasses. Although by year-end no one had returned eyeglasses

sold in 2016, Wilson estimated that its guarantee would cost the

company $1,200 in warranty expense during 2017. Wilson incurred

$120,000 of other operating expenses during 2016. Using this in-

formation alone, what amount of net income should Wilson report

on its 2016 income statement?

9-3

Detailed Outline of a Lesson Plan for Chapter 9

Note to users of the previous edition: The previous edition of this text did not cover contin-

gent liabilities nor did it include any discussions around payroll taxes payable. These topics

have been added in this chapter of the text.

I. Use Demonstration Problem 9-1 to introduce accounting for warranty obligations

(or to continue the discussion around warranty obligations if you started the

chapter with the Problem-Based Learning case).

II. Use Demonstration Problem 9-2 to discuss interest payable. Students sometimes

struggle with this concept when the interest payment is not due in the current account-

ing period. It helps to reinforce the fact that accounting is based on the matching

principle and that interest payable is matching revenues in a given account period

with expenses incurred to earn those revenues. Explain that interest is really the ex-

pense for the use of someone else’s money. Since the company had the had the full

use of the money for some period of time during the current accounting period, the

expense (interest) related to the use of that money must be recorded. The concept of

interest payable was introduced in chapter 2, so students have already had some expo-

sure to the topic in your earlier class sessions. Part 1 of this problem helps students

see how to compute accrued interest – and lets them see that accrued interest payable

in one setting is accrued interest receivable in another setting. Part 2 of this problem

then allows students to apply their knowledge from Part 1.

III. Use Demonstration Problem 9-3 to introduce payroll taxes payable. Most students

have had some type of work experience by this point in their lives so they will under-

stand the concepts of gross wages and net wages. You can begin this discussion by

writing ‘Gross Pay’ on the board and then asking students to share those items that

would be deducted from a paycheck to arrive at net pay. Then you can relate these

items to the payroll taxes payable example in the Demonstration Problem. Explain

that employers also must pay certain taxes that are on top of the taxes deducted from

the employee paycheck.

IV. Use Demonstration Problem 9-4 to introduce sales tax payable. Since you have al-

ready discussed payroll taxes payable, students should be able to grasp the concept of

sales tax payable fairly quickly.

V. Discuss what’s meant by ‘going concern’ and ‘classified balance sheet’. These terms

will be new to most students. Since the going concern concept assumes that a com-

pany will operate indefinitely, it ties in well with the discussion around balance sheets

where ending account balances from the prior year carry forward to become begin-

ning account balances in the current year. If a company weren’t going to continue in-

9-4

definitely, presenting cumulative account balances in a financial statement would not

make sense. You can reinforce the discussion by naming some accounts and asking

students to identify if they are assets, liability, or equity. If assets or liability ac-

counts, ask students to determine if they are current or long-term. If long-term asset

accounts, ask students to determine if the accounts are tangible or intangible. This

will help students understand how accounts would be classified on the balance sheet.

VI. If you assign the chapter appendix, use Demonstration Problem 9-5 to introduce

accounting for a discount note. The problem covers two cycles. The note has a

one-year term. Date of issue, accrual of interest, and repayment of principal at ma-

turity are covered. Before demonstrating how to record the transactions, explain that

discounting is another way of charging interest. In contrast to an interest-bearing

note, the issuer does not receive cash in the amount of the face value of a discount

note.

Use the rate of return formula (annual interest ÷ cash borrowed) to demonstrate

that the effective rate of interest is higher on a discount note than an interest-bearing

note. Use a $5,000 face value note with a 12% rate of interest. The amount of cash

borrowed with an interest-bearing note is $5,000 and the amount of interest is $600.

The effective interest rate is 12% ($600 ÷ $5,000). In contrast, the amount of cash

borrowed with a discount note is $4,400 ($5,000 – $600). The effective interest rate

is 13.64% ($600 ÷ $4,400). Caution students to always look for the effective rate of

interest when borrowing money.

Now begin Demonstration Problem 9-5. Record the first event in T-accounts.

Emphasize that the amount of cash received is less than the face value of the note.

Explain how the carrying value of the note payable is reduced through a contra–

liability account (discount on note payable). Since all other contra accounts discussed

so far have been associated with asset accounts, explain that contra accounts can also

be associated with liability accounts. Just as was the case with asset accounts, com-

bining the balances in the liability account and the associated contra account will pro-

vide information regarding the net value of the liability. Emphasize that on the issue

date the company’s liability to the bank is only the amount of the cash received (face

value Ä discount). The liability increases the longer the note is held because interest

accrues on the note. In Event No. 4 students should see how accrued interest expense

reduces the discount and concurrently increases the carrying value of the liability.

Stress that the carrying value (the liability) on the December 31 balance sheet is high-

er because the customer not only owes the principal borrowed but also the interest

that has accrued. Close the revenue and expense accounts for 2016. After recording

the 2016 transactions in T-accounts, use the horizontal financial statements model to

show how each event will affect the financial statements.

Finally, record the 2017 transactions in T-accounts. Emphasize that the discount

balance is zero after accrued interest is recorded on the maturity date. The cash paid

at maturity (the face value of the note) is greater than the amount that was borrowed

because the payment at maturity includes interest as well as repayment of principal.

9-5

VII. Time considerations and homework assignments. Plan to spend approximately

two hours of class time on this chapter. Use the Demonstration Problems to introduce

students to the various concepts covered in this chapter. Then consider assigning the

following Exercises or Problems as homework to reinforce what you covered in class:

Problem 9-19 A or B reinforce interest payable, Exercise 9-4 A or B reinforce sales

tax payable, Exercise 9-6 A or B reinforce warranty concepts and Problem 9-23 A or

B reinforce recording payroll transactions. Exercise 9-13 A or B is a great compre-

hensive assignment.

Demonstration Problem 9-1 – Warranty Expense

Versa Training Services provides instruction on how to pass the CPA examination. Versa

has attained phenomenal growth by offering its customers a money-back guarantee. Any

student who attends all classes and completes all homework assignments is entitled to a com-

plete refund if he or she fails to pass the exam. The following events pertain to a new course

that was recently established by Versa.

1. During 2016, Versa charged a total of 40 students $400 each for the training. Versa only

accepts cash payment for training.

2. Versa estimates that 10 percent of the students will attend all the classes, complete all the

homework assignments, and yet fail the exam and demand a cash refund.

3. During 2016, only 1 customer presented his exam results to Versa and requested a cash

refund. Versa paid a $400 cash refund to a customer after he received his exam results.

This refund was the first of several Versa expected to grant to unsuccessful candidates.

Required

a. Record the events in T-accounts, including closing the revenue and expense accounts to

retained earnings

b. Record the events using the horizontal financial statements model under the titles of the

affected accounts. Record a zero under each heading not affected by the event. Compare

the final balances in the T-accounts from part a. with the ending balances in the horizon-

tal financial statements model.

Demonstration Problem 9-2 – Interest Payable and Interest Ex-

pense

Part 1.

Johnson Company borrowed $1,000 cash by issuing a one-year note payable to McCoy

Company. McCoy charged Johnson interest on the note at a 12% annual rate. Both compa-

nies close their books on December 31, 2016.

Required

a. Determine the amount of accrued interest expense Johnson would report and the amount

of accrued interest revenue McCoy would report at December 31, 2016 under each of the

9-6

three following independent assumptions of the note issue date. The note was issued

(money was borrowed) on (1) April 1, 2016; (2) June 1, 2016; and (3) October 1, 2016.

b. Recompute the amount of interest for 2016 assuming the same facts as above except the

note has an 8-month term instead of a one-year term.

Part 2.

Frank’s Hot Dogs borrowed $10,000 from City Bank on July 1, 2016. The loan was at 5%

annual interest and was to be repaid on July 1, 2018. During both 2016 and 2017, Frank’s

earned $5,000 cash revenue and paid $2,000 cash for expenses. On December 31 of 2016

and 2017, the accountants for Frank’s Hot Dogs prepared year-end adjusting and closing en-

tries.

Required

a. Record the transactions and required year-end adjusting and closing entries for 2016 and

2017 in T-accounts.

b. Record the transactions and required year-end adjusting and closing entries for 2016 and

2017 using the horizontal financial statements model.

c. Using the horizontal financial statements model, record the required entries when Frank’s

Hot Dogs repaid the loan on July 1, 2018.

Demonstration Problem 9-3 – Employment Taxes Payable

Colby Company had one salaried employee, Carl Colby, who was paid $2,000 per month.

According to the employment tax laws, Colby Company had to remit Federal and State em-

ployment taxes on a quarterly basis. Colby Company also agreed to pay for benefits on a

quarterly basis. During each month, Carl had the following deductions withheld from his

paycheck:

Federal income tax $400

State income tax $200

Social Security 6% of gross

Medicare 1.5% of gross

Medical Insurance $100

United Way contribution $50

Additionally, Colby Company provided Carl with the following company-paid benefits:

Vacation 1 day earned per month, valued at $67

Medical Insurance $100

Finally, Colby Company had the following employment tax responsibilities:

Social Security match that withheld from employee

Medicare match that withheld from employee

Federal Unemployment 0.8% of gross payroll

State Unemployment 5.4% of gross payroll

9-7

Required:

a. Record Carl Colby’s monthly payroll entry using T-accounts.

b. Record Colby Company’s monthly employer payroll entry using T-accounts.

c. Using the horizontal financial statements model, record Carl’s deductions for Janu-

ary, February, and March as well as Colby Company’s employment tax liabilities.

Then record Colby Company’s quarterly payments associated with Carl Colby’s em-

ployment (remember that 3 monthly payroll entries will have been made by the time

these payments are due).

Demonstration Problem 9-4 – Sales Tax Payable

Dance Costumes Inc. had total sales (including sales tax) of $10,450.

Required:

a. Assuming a sales tax rate of 4.5%, record the sales entry and related tax payment

using T-accounts and then record the transactions using the horizontal financial

statements model.

Demonstration Problem 9-5 – Discount Note

Computer Consultants experienced the following accounting events in its first year of opera-

tion.

1. The company was started on April 1, 2016 when it issued a $5,000 face value discount

note to State Bank. The note had a 12% discount rate and a one-year term.

2. Paid $4,200 cash for operating expenses.

3. Recognized $7,300 of cash service revenue.

4. Recognized accrued interest expense at December 31, 2016.

Accounting events affecting 2017 were as follows:

1. On April 1, 2017 Computer Consultants recognized the final three months of accrued in-

terest expense on the discount note.

2. Paid State Bank the face value of the note.

3. Recognized $9,500 of cash service revenue.

4. Paid $6,400 cash for operating expenses.

Required

a. Record the events for 2016 and 2017 in T-accounts.

b. Record the events for 2016 and 2017 using the horizontal financial statements model.

9-8

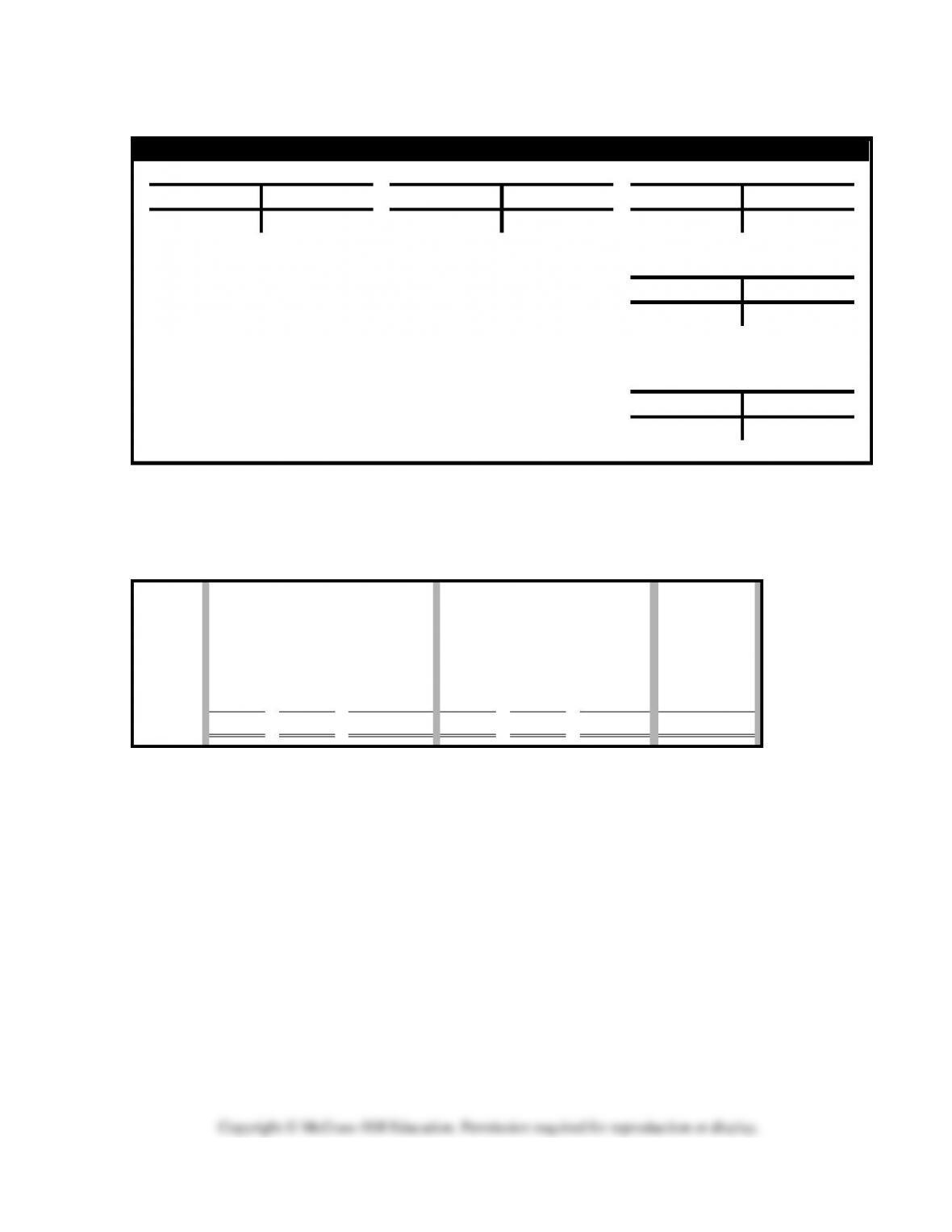

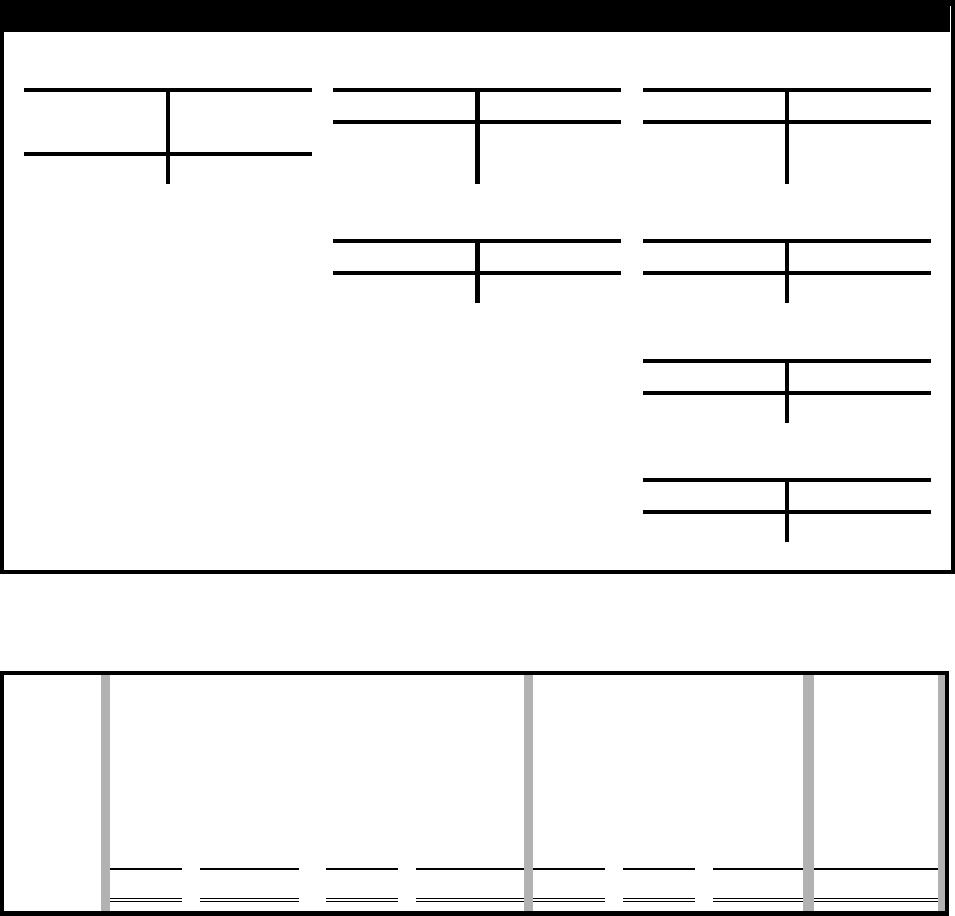

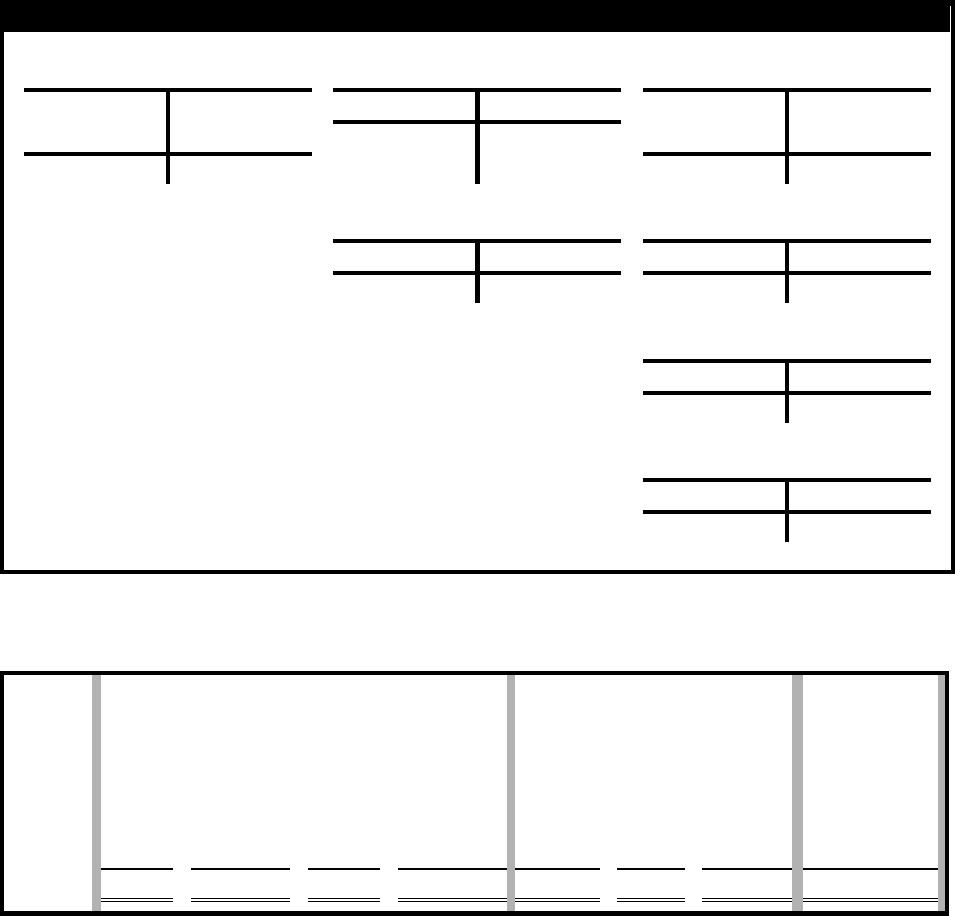

Demonstration Problem 9-1 Solution, part a. T-accounts

Ledger T-Accounts

Cash

Warranty Payable

Retained Earnings

(1) 16,000

400 (3)

(3) 400

1,600 (2)

cl. 1,600

16,000 cl.

Bal. 15,600

1,200 Bal.

14,400 Bal.

Services Revenue

cl. 16,000

16,000 (1)

Warranty Expense

(2) 1,600

1,600 cl.

Demonstration Problem 9-1 Solution, part b. Horizontal Financial

Statements Model

Event

Assets

=

Liab.

+

Equity

Rev.

–

Exp.

=

Net Inc.

Cash Flow

No.

Cash

=

W. Pay

Ret. Earn.

Beg. bal.

0

=

0

+

0

0

–

0

=

0

0

1.

16,000

=

0

+

16,000

16,000

–

0

=

16,000

16,000 OA

2.

0

=

1,600

+

(1,600)

0

–

1,600

=

(1,600)

0

3.

(400)

(400)

+

0

0

–

0

=

0

(400) OA

Totals

15,600

=

1,200

+

14,400

16,000

–

1,600

=

14,400

15,600 NC

2-1

Demonstration Problem 9-2 Solution

Part 1.

Johnson’s 2016 interest expense equals McCoy’s 2016 interest revenue, as follows:

a.

Date Note Issued

Principal

x

Rate

x

Time

=

Accrued Interest

April 1, 2016

$1,000

x

.12

x

(9 ÷ 12)

=

$90

June 1, 2016

$1,000

x

.12

x

(7 ÷ 12)

=

$70

October 1, 2016

$1,000

x

.12

x

(3 ÷ 12)

=

$30

b.

Date Note Issued

Principal

x

Rate

x

Time

=

Accrued Interest

April 1, 2016

$1,000

x

.12

x

(8 ÷ 12)

=

$80

June 1, 2016

$1,000

x

.12

x

(7 ÷ 12)

=

$70

October 1, 2016

$1,000

x

.12

x

(3 ÷ 12)

=

$30

Part 2.

Demonstration Problem 9-2 Solution, part 2.a. T-Accounts

Demonstration Problem 9-2 Solution, part 2,b. Horizontal Financial

Statements Model

Demonstration Problem 9-2 Solution, part 2.c. Horizontal Financial

Statements Model

Worksheet Edmonds

FFAC9e Ch 9 IM sol.xls

Demonstration Problem 9-3 Solution, part a. T-Accounts

Demonstration Problem 9-3 Solution, part b. Horizontal Financial

Statements Model

Demonstration Problem 9-4 Solution, part a. T-Accounts

Demonstration Problem 9-4 Solution, part b. Horizontal Financial

Statements Model

2-2

Demonstration Problem 9-5 Solution, part a. 2016 T-accounts

2016 Ledger T-Accounts

Cash

Notes Payable

Retained Earnings

(1) 4,400

4,200 (2)

5,000 (1)

2,650 cl.

(3) 7,300

5,000 Bal.

2,650 Bal.

Bal. 7,500

Discount on Note Pay.

Service Revenue

(1) 600

450 (4)

cl. 7,300

7,300 (3)

Bal. 150

Operating Expenses

(2) 4,200

4,200 cl.

Interest Expense

(4) 450

450 cl.

Demonstration Problem 9-5 Solution, part b. Statements Model, 2016

Event

Assets

=

Liabilities

+

Equity

Rev.

–

Exp.

=

Net Inc.

Cash Flow

No.

Cash

=

Note Pay.

+

(Disc.)

+

Ret. Earn.

Beg. bal.

0

=

0

+

0

+

0

0

–

0

=

0

0

1.

4,400

=

5,000

+

(600)

+

0

0

–

0

=

0

4,400 FA

2.

(4,200)

=

0

+

0

+

(4,200)

0

–

4,200

=

(4,200)

(4,200) OA

3.

7,300

=

0

+

0

+

7,300

7,300

–

0

=

7,300

7,300 OA

4.

0

=

0

+

450

+

(450)

0

–

450

=

(450)

0

Totals

7,500

=

5,000

+

(150)

+

2,650

7,300

–

4,650

=

2,650

7,500 NC

2-3

Demonstration Problem 9-5 Solution, part a. 2017 T-accounts

2017 Ledger T-Accounts

Cash

Notes Payable

Retained Earnings

Bal. 7,500

5,000 (2)

(2) 5,000

5,000 Bal.

2,650 Bal.

(3) 9,500

6,400 (4)

2,950 cl.

Bal. 5,600

5,600 Bal.

Discount on Note Pay.

Service Revenue

Bal. 150

150 (1)

cl. 9,500

9,500 (3)

Operating Expenses

(4) 6,400

6,400 cl.

Interest Expense

(1) 150

150 cl.

Demonstration Problem 9-5 Solution, part b. Statements Model, 2017

Event

Assets

=

Liabilities

+

Equity

Rev.

–

Exp.

=

Net Inc.

Cash Flow

No.

Cash

=

Note Pay.

+

(Disc.)

+

Ret. Earn.

Beg. bal.

7,500

=

5,000

+

(150)

+

2,650

0

–

0

=

0

0

1.

0

=

0

+

150

+

(150)

0

–

150

=

(150)

0

2.

(5,000)

=

(5,000)

+

0

+

0

0

–

0

=

0

(5,000) FA

3.

9,500

=

0

+

0

+

9,500

9,500

–

0

=

9,500

9,500 OA

4.

(6,400)

=

0

+

0

+

(6,400)

0

–

6,400

=

(6,400)

(6,400) OA

Totals

5,600

=

0

+

0

+

5,600

9,500

–

6,550

=

2,950

(1,900) NC

2-4

Demonstration Problem 9-1 Workpaper, part a. T-accounts, 2016

Ledger T-Accounts

Cash

Warranty Payable

Retained Earnings

Bal. 15,600

1,200 Bal.

14,400 Bal.

Services Revenue

Warranty Expense

Demonstration Problem 9-1 Workpaper, part b. Horizontal Finan-

cial Statements Model

Event

Assets

=

Liab.

+

Equity

Rev.

–

Exp.

=

Net Inc.

Cash Flow

No.

Cash

=

W. Pay

Ret. Earn.

Beg. bal.

=

+

=

1.

=

+

=

2.

=

+

=

3.

+

=

Totals

15,600

=

1,200

+

14,400

16,000

–

1,600

=

14,400

15,600 NC

9-1

Demonstration Problem 9-2 Workpaper, part a. T Accounts

Demonstration Problem 9-2 Workpaper, part b. Horizontal Finan-

cial Statements Model

Demonstration Problem 9-2 Workpaper, part c. Horizontal Finan-

cial Statements Model

Worksheet Edmonds

FFAC9e Ch 9 wkp 9-2 9-3.xlsx

Demonstration Problem 9-3 Workpaper, part a. T Accounts

Demonstration Problem 9-3 Workpaper, part b. Horizontal Finan-

cial Statements Model

Demonstration Problem 9-4 Workpaper

Due to the simplicity of this demonstration problem, there is no workpaper provided. You

should be able to easily illustrate this problem on the board without the need for additional

supporting tools.

9-2

Demonstration Problem 9-5 Workpaper, part a. 2016 T-accounts

2016 Ledger T-Accounts

Cash

Notes Payable

Retained Earnings

5,000 Bal.

2,650 Bal.

Bal. 7,500

Discount on Note Pay.

Service Revenue

Bal. 150

Operating Expenses

Interest Expense

Demonstration Problem 9-5 Workpaper, part b. Statements Model, 2016

Event

Assets

=

Liabilities

+

Equity

Rev.

–

Exp.

=

Net Inc.

Cash Flow

No.

Cash

=

Note Pay.

+

(Disc.)

+

Ret. Earn.

Beg. bal.

0

=

0

+

0

+

0

0

–

0

=

0

0

1.

=

+

+

–

=

2.

=

+

+

–

=

3.

=

+

+

–

=

4.

=

+

+

–

=

Totals

7,500

=

5,000

+

(150)

+

2,650

7,300

–

4,650

=

2,650

7,500 NC

9-3

Demonstration Problem 9-5 Workpaper, part a. 2017 T-accounts

2017 Ledger T-Accounts

Cash

Notes Payable

Retained Earnings

Bal. 7,500

5,000 Bal.

2,650 Bal.

Bal. 5,600

5,600 Bal.

Discount on Note Pay.

Service Revenue

Bal. 150

Operating Expenses

Interest Expense

Demonstration Problem 9-5 Workpaper, part b. Statements Model, 2017

Event

Assets

=

Liabilities

+

Equity

Rev.

–

Exp.

=

Net Inc.

Cash Flow

No.

Cash

=

Note Pay.

+

(Disc.)

+

Ret. Earn.

Beg. bal.

7,500

=

5,000

+

(150)

+

2,650

0

–

0

=

0

0

1.

=

+

+

–

=

2.

=

+

+

–

=

3.

=

+

+

–

=

4.

=

+

+

–

=

Totals

5,600

=

0

+

0

+

5,600

9,500

–

6,550

=

2,950

(1,900) NC

9-4

Quiz Questions for Chapter 9

1. Which statement best expresses the ‘going concern’ concept?

a. A company is assumed to continue operations indefinitely, benefitting from assets and paying liabili-

ties.

b. A company has a concern about its future.

c. The auditors have issued an opinion that expresses ongoing concerns about the financial stability of a

company.

d. There is a concern about the financial health of an industry overall and the abilities of the companies

that are part of that industry to generate profits.

2. What is unique about a classified balance sheet?

a. It contains highly confidential information that is classified as secure and should only be made availa-

ble to individuals with top-level security clearance.

b. It contains information that is classified as unique to a particular industry.

c. It contains information that the company has classified as most important to present to financial state-

ment readers.

d. It distinguishes current assets and liabilities from those that are considered non-current or long-term.

3. On April 1, Broke Company borrowed $10,000 from Central Bank. The note was for 1 year and carried an

8% annual interest rate. Broke Company’s year-end is December 31. What kind of adjusting entry, if any,

needs to be recorded at year-end by Broke Company to properly record events associated with the loan

from Central Bank?

a. $600 to record interest expense and interest payable

b. $800 to record interest expense and interest payable

c. $400 to record interest expense and interest payable

d. no adjusting entry is necessary

4. Suzie’s Fashions sold $2,000 of merchandise on a given day, plus 5% sales tax. All sales were on account.

How should Suzie’s Fashions record the sales transactions?

a. Accounts Receivable $2,100

Sales Revenue $2,100

b. Accounts Receivable $2,100

Sales Tax Payable $100

Sales Revenue $2,000

c. Accounts Receivable $2,100

Sales Tax Expense $100

Sales Revenue $2,000

d. Accounts Receivable $2,000

Sales Revenue $2,000

Use this information to answer the next 2 questions.

Jones Company employees are paid at the end of every week. There are 2 employees and each are paid $500

per week. Jones withholds $50 in Federal tax and $25 in state tax per employee. Jones then remits these taxes

withheld at the end of every quarter.

5. At the end of every week, Jones Company would record a payroll transaction that would:

a. Decrease Cash by $850 and increase Salary Expense by $1,000

b. Decrease Cash by $500 and increase Salary Expense by $500

c. Decrease Cash by $450 and increase Salary Expense by $450

d. Decrease Cash by $425 and increase Salary Expense by $425

6. When Jones Company records the weekly salary payments, what accounts would be impacted?

a. Cash, Salaries Payable, Federal tax expense and state tax expense

b. Cash, Salaries Expense, Federal taxes payable and state taxes payable

9-5

c. Cash, Salaries Expense, Federal tax expense, and state tax expense

d. Cash and Salaries Expense only. Any Federal or state tax accounts would be impacted at quarter-end

when Jones Company pays those taxes.

7. Training Services, Inc. (TSI) guarantees the quality of its instructional services. TSI earned $40,000 of

cash revenue from instructional services in 2016. The company estimates that future warranty claims will

be 6 percent of revenue. During 2016, TSI paid $700 cash on warranty claims. Based on this information,

the amount of net income and the net change in cash for 2016 would be

a. $37,600 / $39,300.

b. $37,600 / $37,600.

c. $39,300 / 39,300.

d. $38,300 / $39,300.

The following information pertains to the next three questions. On April 1, 2016, Hope Co. issued a $5,000

face value discount note to the Capital Bank. The note had a 12 percent discount rate and a one-year term.

8. The amount of cash Hope received on April 1, 2016, was

a. $5,000.

b. $4,250.

c. $4,400.

d. $5,500.

9. The total carrying value of Hope’s liabilities on December 31, 2016, would be

a. $5,600.

b. $5,000.

c. $5,450.

d. $4,850.

10. If Hope Co. earned $2,000 of revenue in 2016, the amount of net income would be

a. $2,000.

b. $1,550.

c. $1,400.

d. $1,850.

11. Smith Company experienced an accounting event that was recorded in its general journal as indicated be-

low:

Warranties Payable

xxx

Cash

xxx

Which of the following reflects how this event affects the company’s financial statements?

Assets

=

Liab.

+

Equity

Rev.

–

Exp.

=

Net Inc.

Cash Flow

a.

–

NA

–

NA

+

–

– OA

b.

+ –

NA

NA

+

NA

+

+ OA

c.

–

–

NA

NA

+

–

– OA

d.

–

–

NA

NA

NA

NA

– OA

9-6

Quiz Answers

Question

Answer

1

A

2

D

3

A

4

B

5

A

6

B

7

A

8

C

9

D

10

B

11

D

9-7

Summary Outline of a Lesson Plan for Chapter 9

I. Use Demonstration Problem 9-1 to introduce accounting for warranty obligations

(or to continue the discussion around warranty obligations if you started the chap–

ter with the Problem-Based Learning case).

II. Use Demonstration Problem 9-2 to discuss interest payable

III. Use Demonstration Problem 9-3 to introduce payroll taxes payable.

IV. Use Demonstration Problem 9-4 to introduce sales tax payable.

V. Discuss what’s meant by ‘going concern’ and ‘classified balance sheet’. Consider

naming some accounts and asking students to tell if they are current assets, current lia-

bilities, intangible assets, long-term tangible assets, or long-term liabilities.

VI. If you assign the chapter appendix, use Demonstration Problem 9-5 to introduce

accounting for a discount note.

VII. Time considerations and homework assignments. Plan to spend approximately two

hours of class time on this chapter. Use the Demonstration Problems to introduce stu-

dents to the various concepts covered in this chapter. Then consider assigning the fol-

lowing Exercises or Problems as homework to reinforce what you covered in class:

Problem 9-19 A or B (interest payable), Exercise 9-4 A or B (sales tax payable), Exer-

cise 9-6 A or B (warranty) and Problem 9-23 A or B (payroll). Exercise 9-13 A or B is a

great comprehensive assignment.