EXERCISE 5-2B

Harris Co.

First Purchase

$3,600

Second Purchase

4,200

Total

$7,800

(a)

(b)

(c)

FIFO

LIFO

W. AVG.

Cost of Goods Sold

$3,600

$4,200

$3,900*

Ending Inventory

4,200

3,600

3,900*

*Average Cost per Unit: $7,800 2 = $3,900

EXERCISE 5-3B

Marley Company

Inventory Purchases

Beginning Inventory

400

@

$50

=

$20,000

First Purchase

500

@

55

=

27,500

Second Purchase

600

@

58

=

34,800

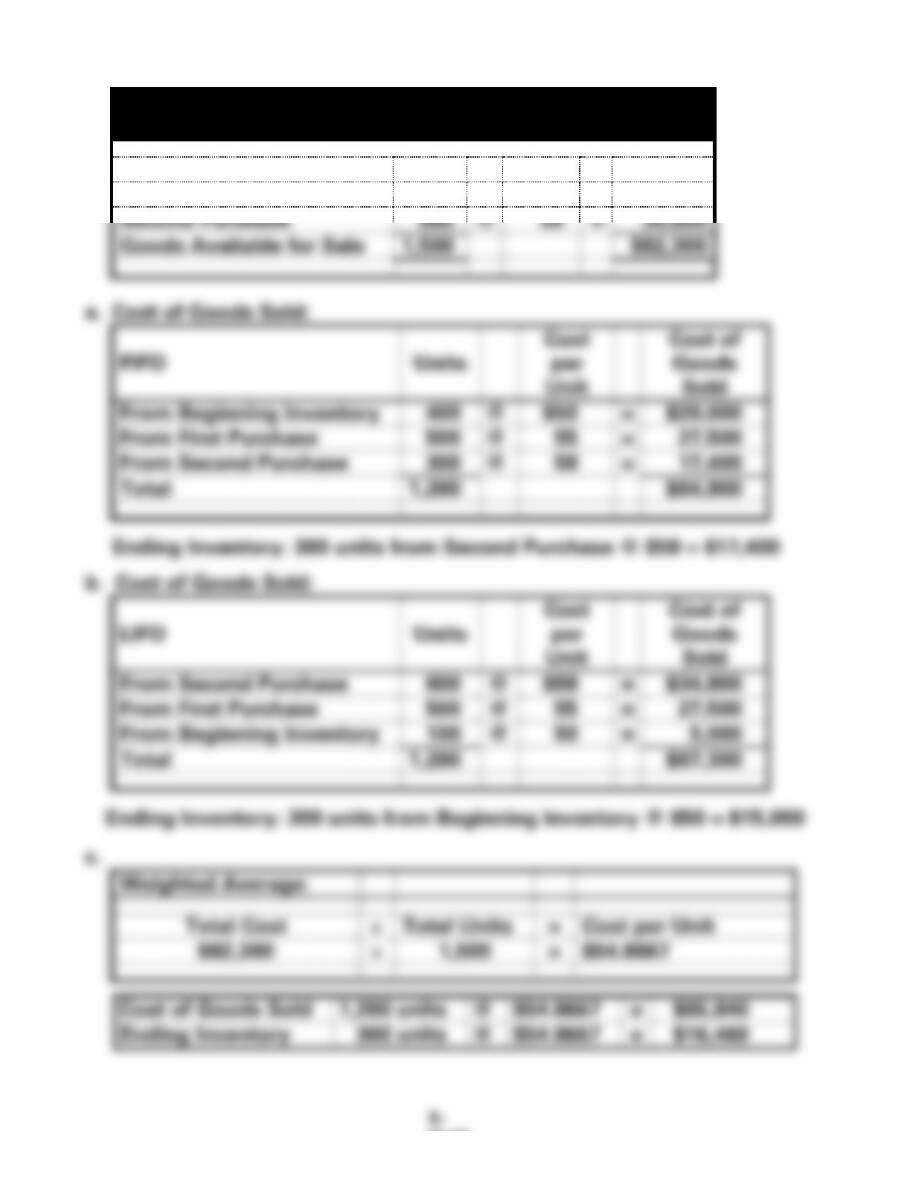

Goods Available for Sale

1,500

$82,300

a. Cost of Goods Sold:

FIFO

Units

Cost

per

Unit

Cost of

Goods

Sold

From Beginning Inventory

400

@

$50

=

$20,000

From First Purchase

500

@

55

=

27,500

From Second Purchase

300

@

58

=

17,400

Total

1,200

$64,900

Ending Inventory: 300 units from Second Purchase @ $58 = $17,400

b. Cost of Goods Sold:

LIFO

Units

Cost

per

Unit

Cost of

Goods

Sold

From Second Purchase

600

@

$58

=

$34,800

From First Purchase

500

@

55

=

27,500

From Beginning Inventory

100

@

50

=

5,000

Total

1,200

$67,300

Ending Inventory: 300 units from Beginning Inventory @ $50 = $15,000

c.

Weighted Average:

Total Cost

Total Units

=

Cost per Unit

$82,300

1,500

=

$54.8667

Cost of Goods Sold

1,200 units

@

$54.8667

Ending Inventory

300 units

EXERCISE 5-4B

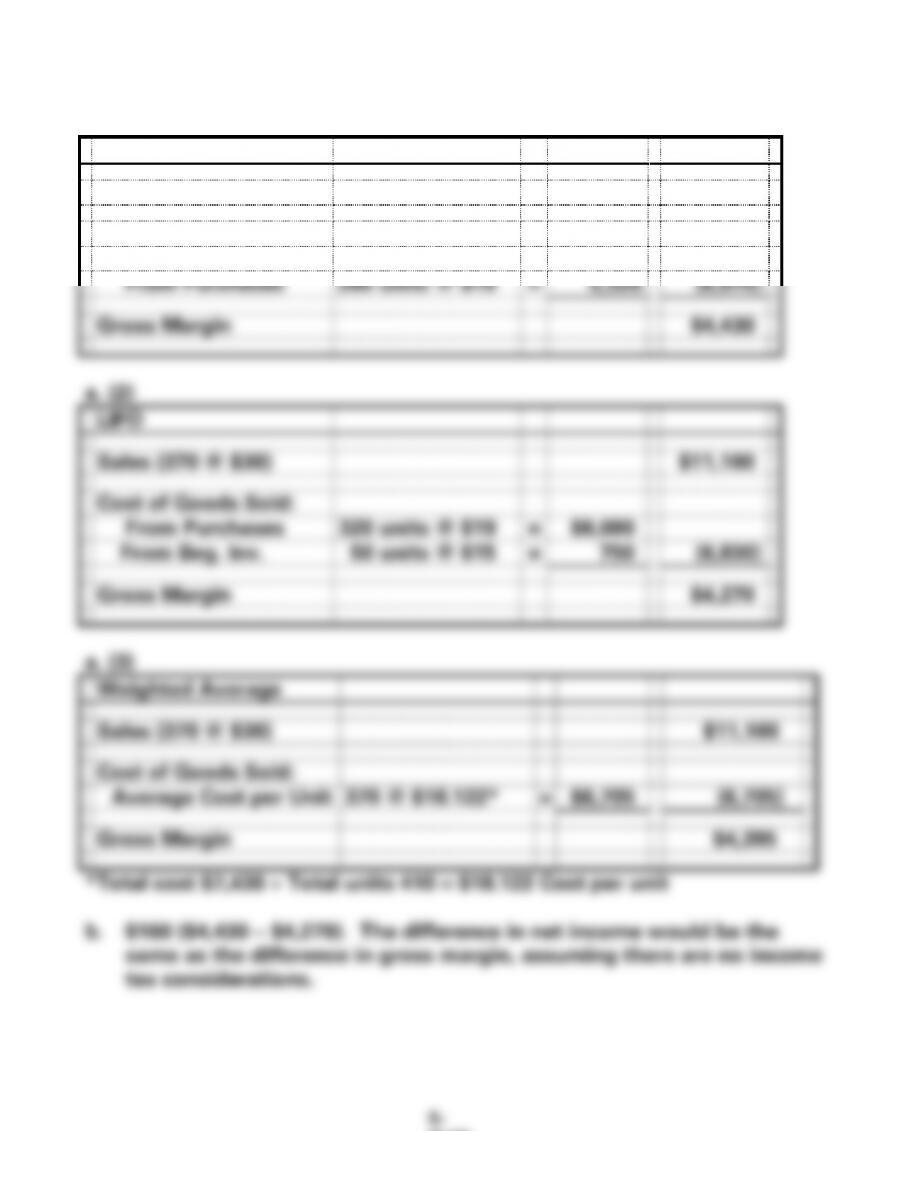

a. (1) Stanley Company

FIFO

Sales (370 @ $30)

$11,100

Cost of Goods Sold:

From Beginning Inv.

90 units @ $15

=

$ 1,350

From Purchases

280 units @ $19

=

5,320

(6,670)

Gross Margin

$4,430

a. (2)

LIFO

Sales (370 @ $30)

$11,100

Cost of Goods Sold:

From Purchases

320 units @ $19

=

$6,080

From Beg. Inv.

50 units @ $15

=

750

(6,830)

Gross Margin

$4,270

Weighted Average

Sales (370 @ $30)

$11,100

Cost of Goods Sold:

Average Cost per Unit

370 @ $18.122*

=

$6,705

(6,705)

Gross Margin

$4,395

*Total cost $7,430 Total units 410 = $18.122 Cost per unit

b. $160 ($4,430 − $4,270). The difference in net income would be the

same as the difference in gross margin, assuming there are no income

tax considerations.

EXERCISE 5-4B (cont.)

c.

FIFO

LIFO

W. Avg.

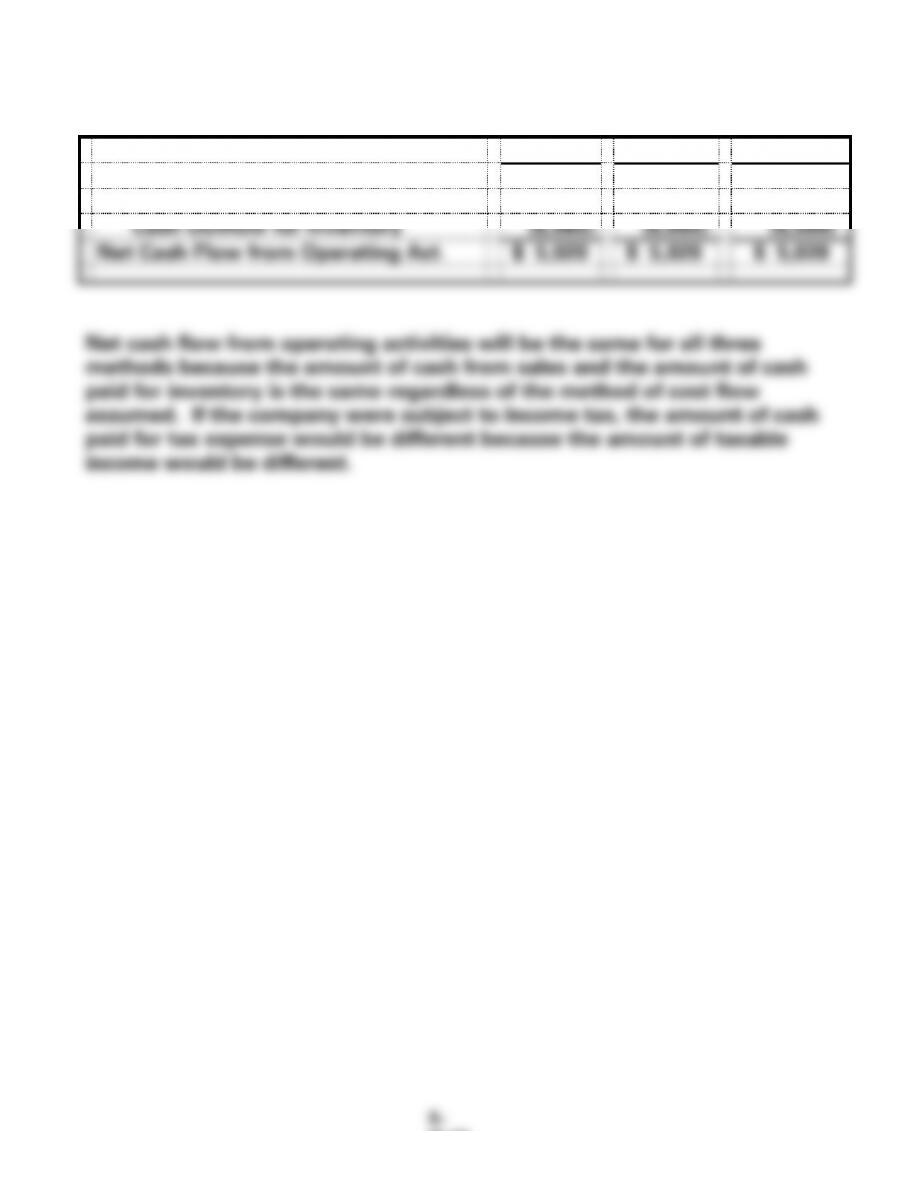

Cash Flows From Operating Activities:

Cash Inflow from Customers

$11,100

$11,100

$11,100

Cash Outflow for Inventory

(6,080)

(6,080)

(6,080)

Net Cash Flow from Operating Act.

$ 5,020

$ 5,020

$ 5,020

Net cash flow from operating activities will be the same for all three

methods because the amount of cash from sales and the amount of cash

paid for inventory is the same regardless of the method of cost flow

assumed. If the company were subject to income tax, the amount of cash

paid for tax expense would be different because the amount of taxable

income would be different.

EXERCISE 5-5B

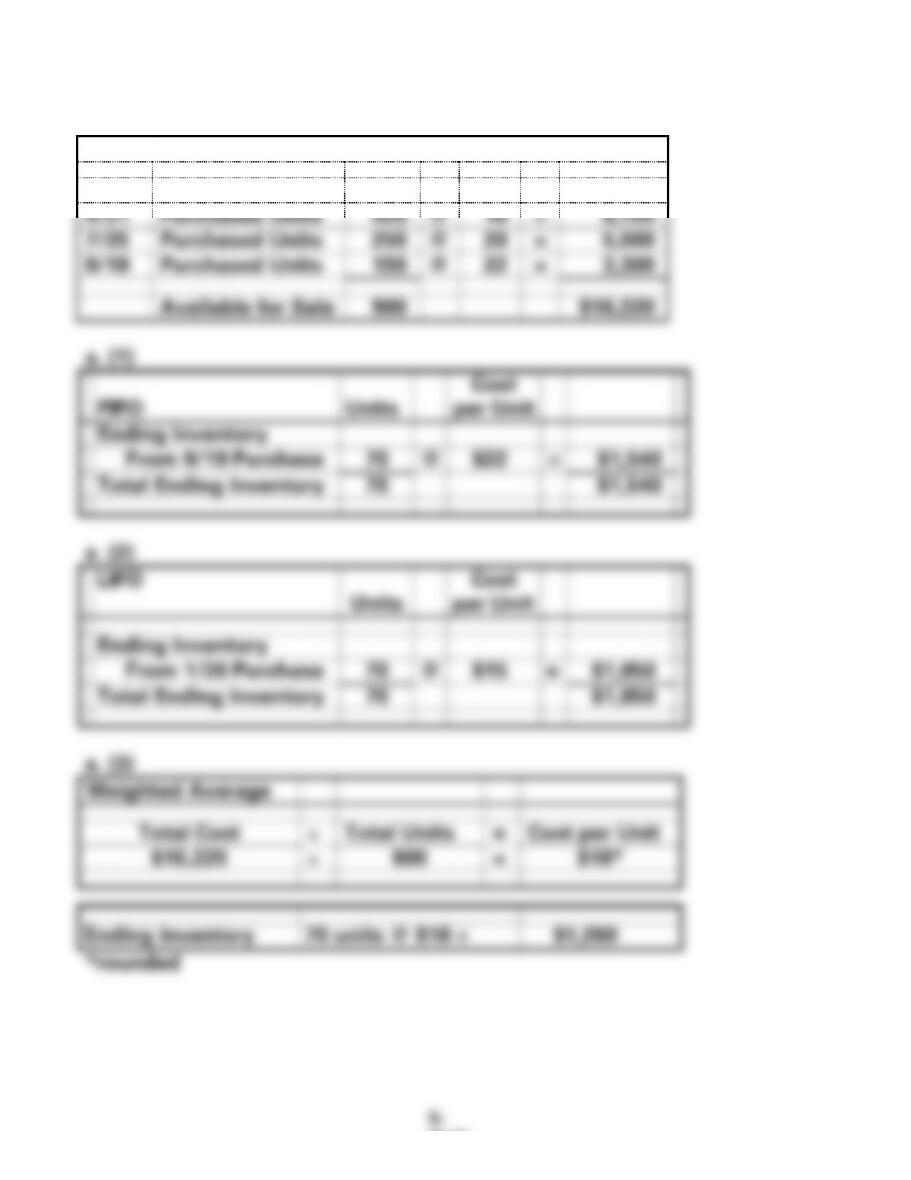

a.

Scott Sales

Summary of Purchase Transactions

1/20

Purchased Units

80

@

$15

=

$ 1,200

4/21

Purchased Units

420

@

16

=

6,720

7/25

Purchased Units

250

@

20

=

5,000

9/19

Purchased Units

150

@

22

=

3,300

Available for Sale

900

$16,220

a. (1)

FIFO

Units

Cost

per Unit

Ending Inventory

From 9/19 Purchase

70

@

$22

=

$1,540

Total Ending Inventory

70

$1,540

a. (2)

LIFO

Units

Cost

per Unit

Ending Inventory

From 1/20 Purchase

70

@

$15

=

$1,050

Total Ending Inventory

70

$1,050

a. (3)

Weighted Average

Total Cost

Total Units

=

Cost per Unit

$16,220

900

=

$18*

Ending Inventory

70 units @ $18 =

$1,260

*rounded

EXERCISE 5-5B (cont.)

b.

Note: The purchase entries are the same for all three methods.

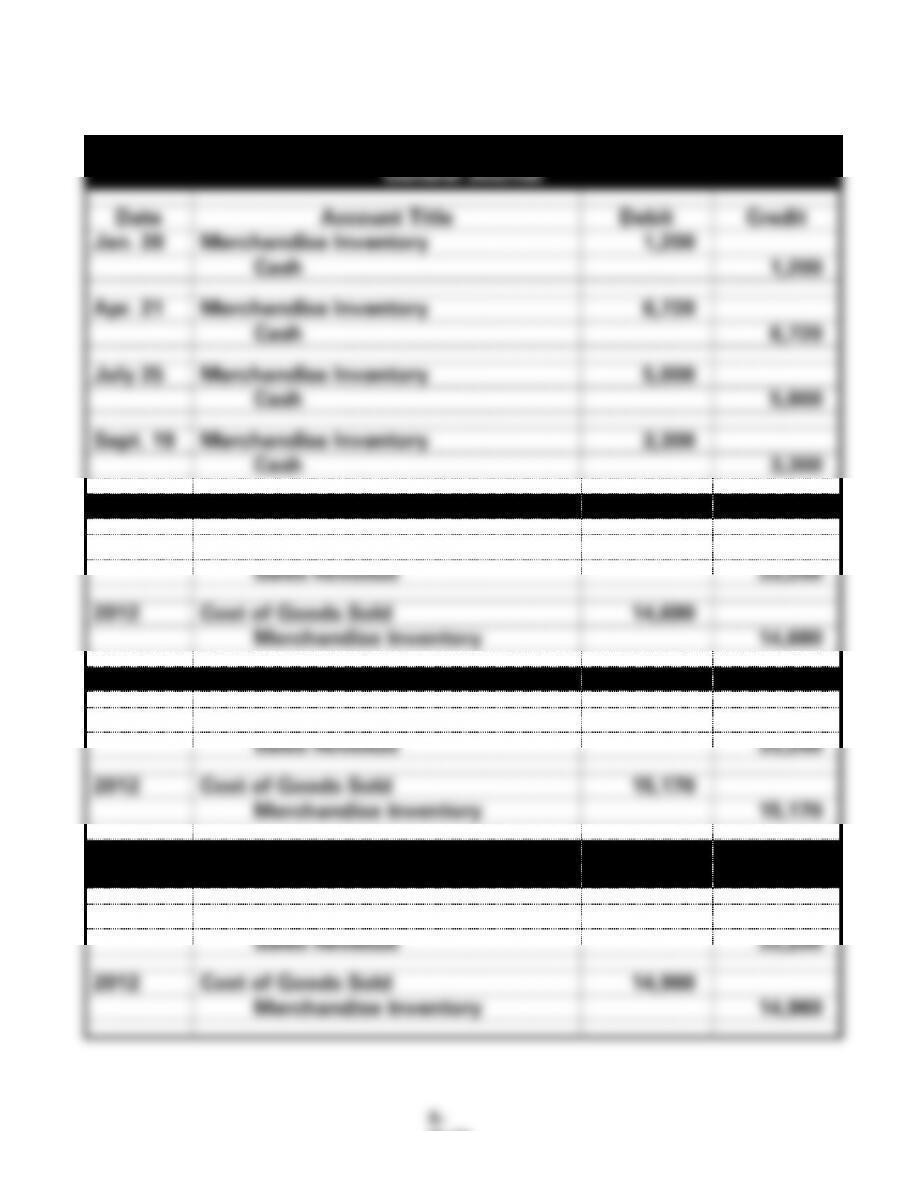

Scott Sales

General Journal

Date

Account Title

Debit

Credit

Jan. 20

Merchandise Inventory

1,200

Cash

1,200

Apr. 21

Merchandise Inventory

6,720

Cash

6,720

July 25

Merchandise Inventory

5,000

Cash

5,000

Sept. 19

Merchandise Inventory

3,300

Cash

3,300

(1) FIFO Sales and Cost of Goods Sold

2012

Cash

33,200

Sales Revenue

33,200

2012

Cost of Goods Sold

14,680

Merchandise Inventory

14,680

(2) LIFO Sales and Cost of Goods Sold

2012

Cash

33,200

Sales Revenue

33,200

2012

Cost of Goods Sold

15,170

Merchandise Inventory

15,170

(3) Weighted Average Sales and Cost of Goods

Sold

2012

Cash

33,200

Sales Revenue

33,200

2012

Cost of Goods Sold

14,960

Merchandise Inventory

14,960

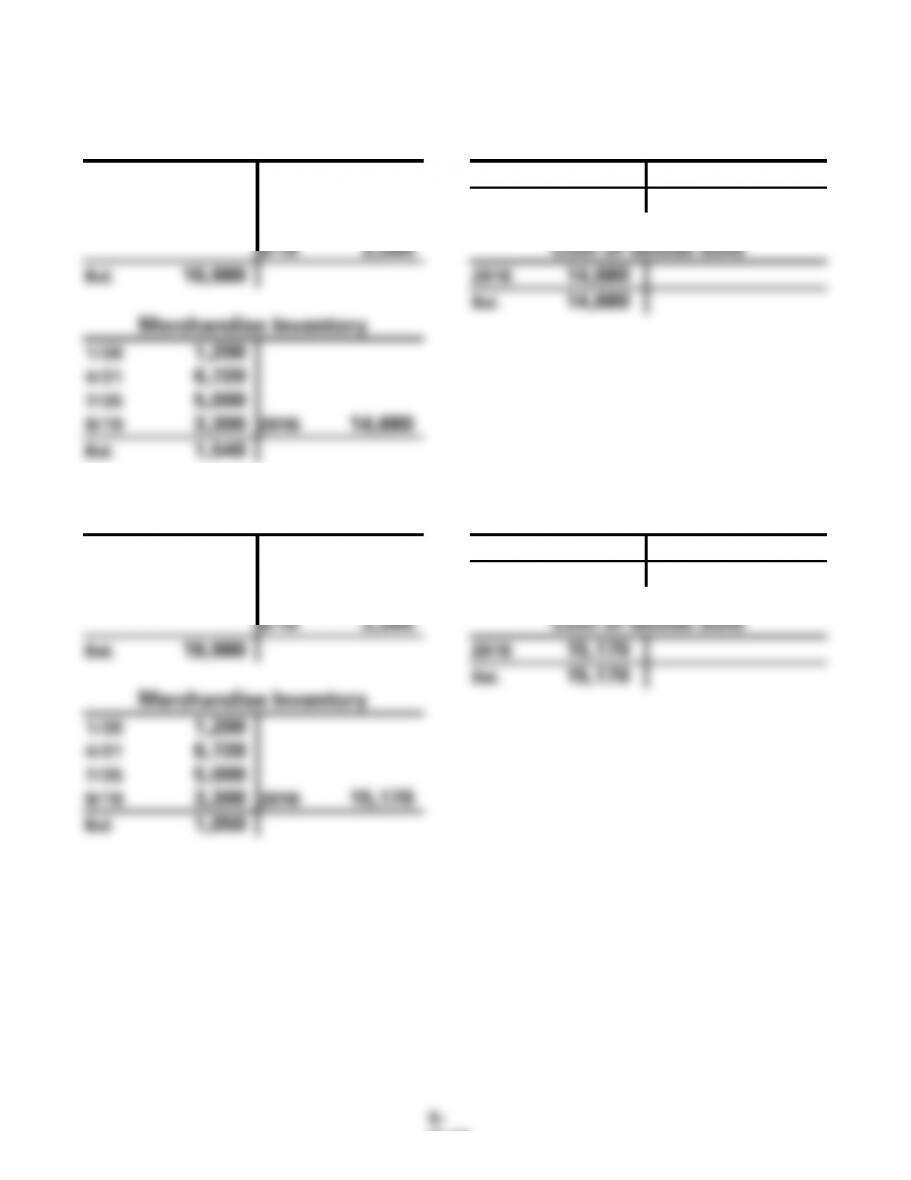

EXERCISE 5-5B b. (cont.)

(1) FIFO

Cash

Sales Revenue

2016 33,200

1/20 1,200

2016 33,200

4/21 6,720

Bal. 33,200

7/25 5,000

9/19 3,300

Cost of Goods Sold

Bal. 16,980

2016 14,680

Bal. 14,680

Merchandise Inventory

1/20 1,200

4/21 6,720

7/25 5,000

9/19 3,300

2016 14,680

Bal. 1,540

(2) LIFO

Cash

Sales Revenue

2016 33,200

1/20 1,200

2016 33,200

4/21 6,720

Bal. 33,200

7/25 5,000

9/19 3,300

Cost of Goods Sold

Bal. 16,980

2016 15,170

Bal. 15,170

Merchandise Inventory

1/20 1,200

4/21 6,720

7/25 5,000

9/19 3,300

2016 15,170

Bal. 1,050

EXERCISE 5-5B b. (cont.)

(3) Weighted Average

Cash

Sales Revenue

2016 33,200

1/20 1,200

2013 33,200

4/21 6,720

Bal. 33,200

7/25 5,000

9/19 3,300

Cost of Goods Sold

Bal. 16,980

2016 14,960

Bal. 14,960

Merchandise Inventory

1/20 1,200

4/21 6,720

7/25 5,000

9/19 3,300

2016 14,960

Bal. 1,260

EXERCISE 5-5B (cont.)

c.

FIFO

Sales (830 units @ $40)

$33,200

Cost of Goods Sold

Cost of Goods Avail. for Sale*

$16,220

Less: Ending Inventory

(1,540)

Cost of Goods Sold

(14,680)

Gross Margin

$18,520

LIFO

Sales (830 units @ $40)

$33,200

Cost of Goods Sold

Cost of Goods Avail. for Sale*

$16,220

Less: Ending Inventory

(1,050)

Cost of Goods Sold

(15,170)

Gross Margin

$18,030

*This amount is computed in the Summary of Purchase Transactions at

the beginning of the problem.

Difference in Gross Margin: $18,520 − $18,030 = $490

Note to Instructor: Cost of goods sold can be computed on a units-sold

basis rather than subtracting ending inventory from goods available for

sale.

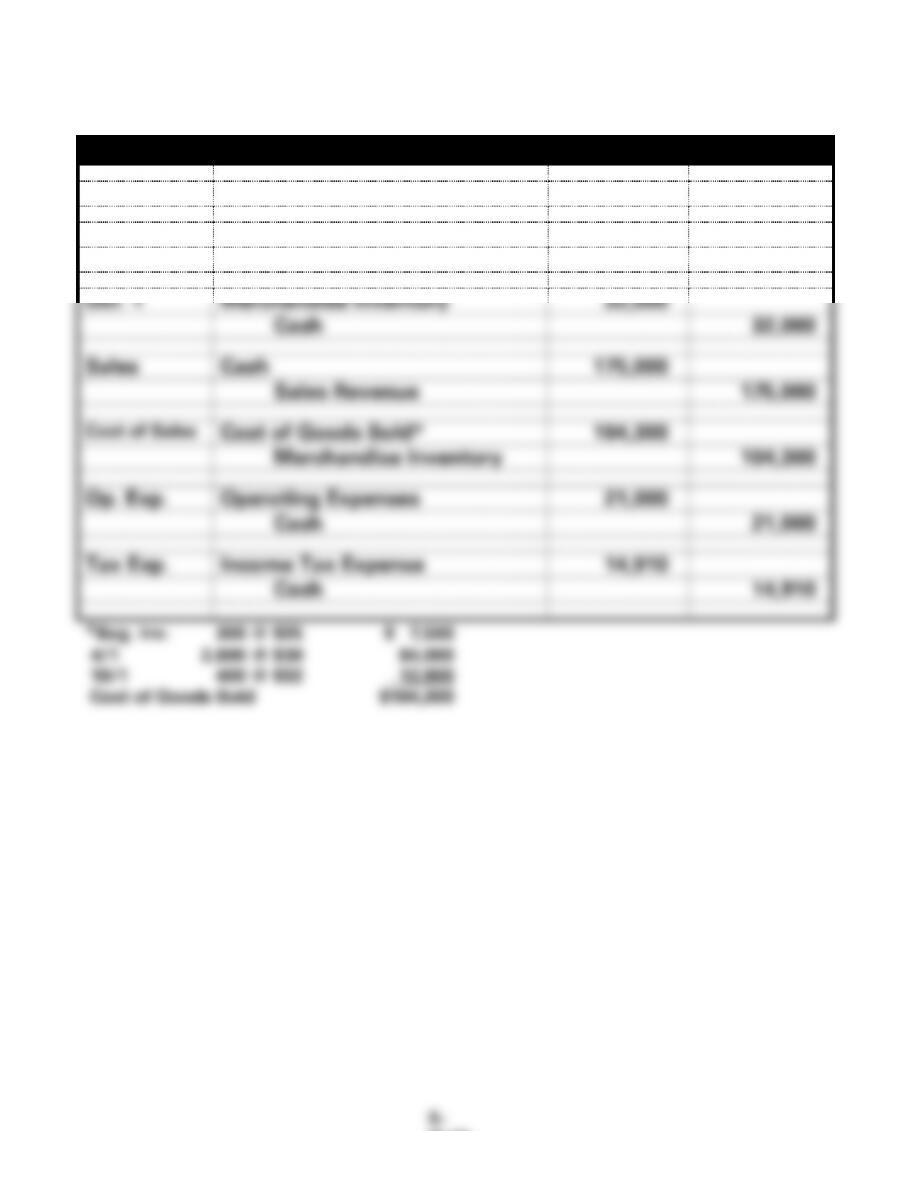

EXERCISE 5-6B

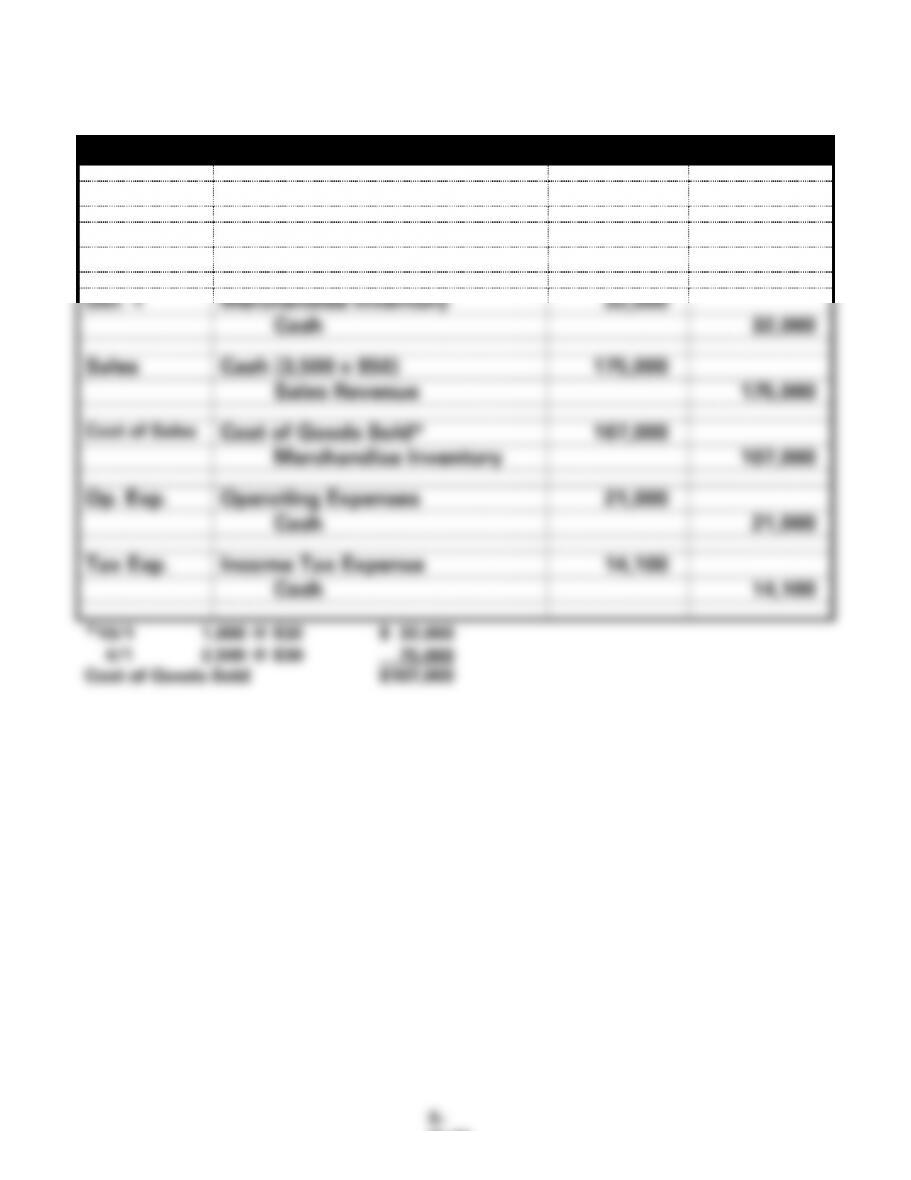

a. (1) FIFO

Date

Account Title

Debit

Credit

Apr. 1

Merchandise Inventory

84,000

Cash

84,000

Oct. 1

Merchandise Inventory

32,000

Cash

32,000

Sales

Cash

175,000

Sales Revenue

175,000

Cost of Sales

Cost of Goods Sold*

104,300

Merchandise Inventory

104,300

Op. Exp.

Operating Expenses

21,000

Cash

21,000

Tax Exp.

Income Tax Expense

14,910

Cash

14,910

*Beg. Inv. 300 @ $25 $ 7,500

4/1 2,800 @ $30 84,000

10/1 400 @ $32 12,800

Cost of Goods Sold $104,300

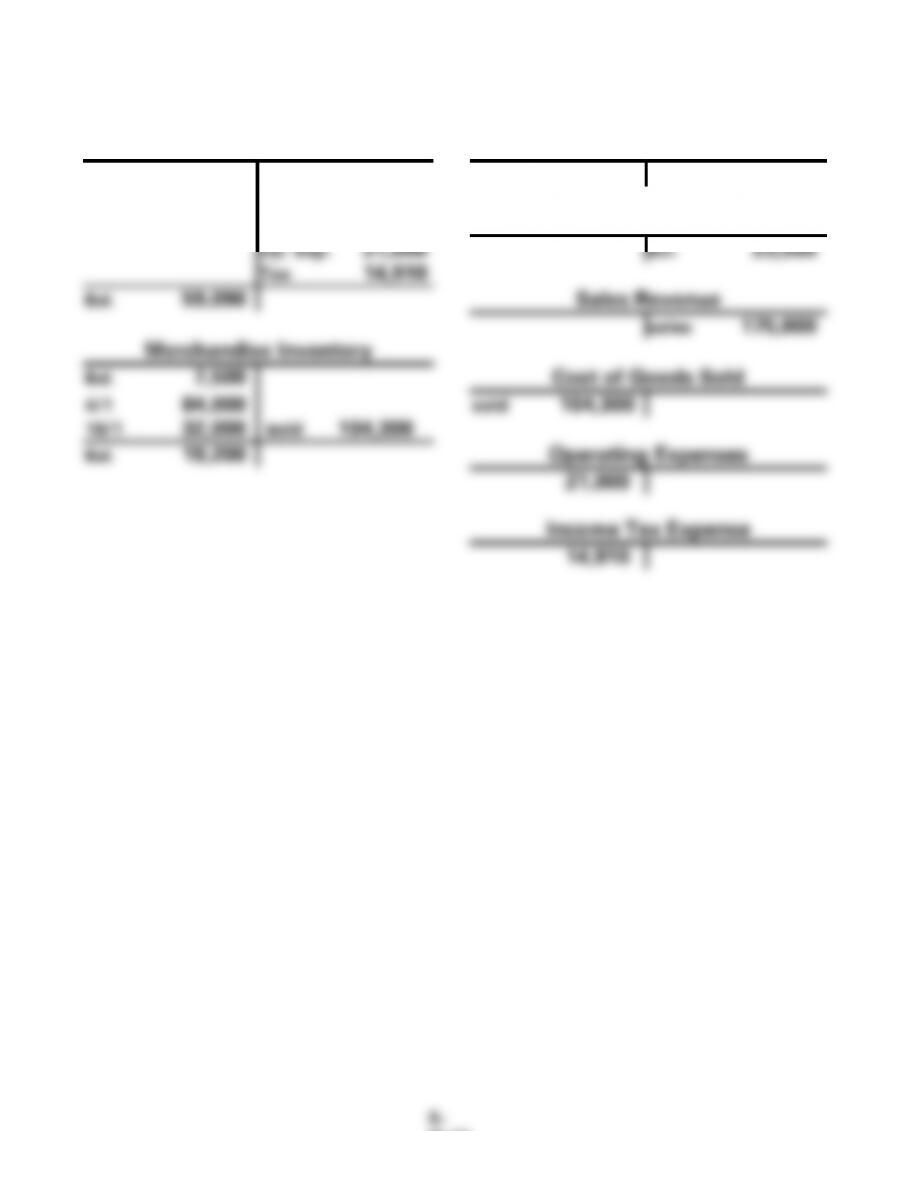

EXERCISE 5-6B a. (cont.)

(1) FIFO

Cash

Common Stock

Bal. 36,000

Bal. 20,000

sales 175,000

4/1 84,000

10/1 32,000

Retained Earnings

Op. Exp. 21,000

Bal. 23,500

Tax 14,910

Bal. 59,090

Sales Revenue

sales 175,000

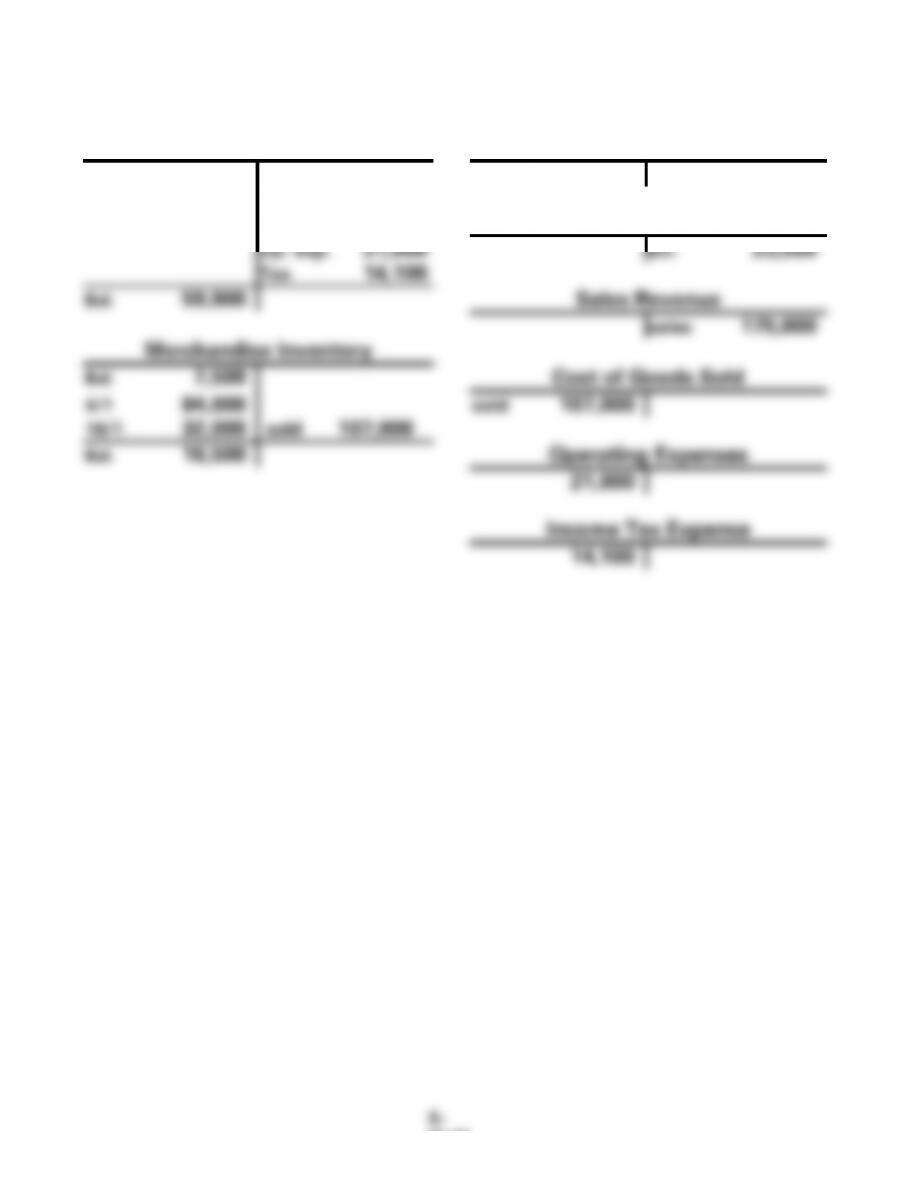

Merchandise Inventory

Bal. 7,500

Cost of Goods Sold

4/1 84,000

sold 104,300

10/1 32,000

sold 104,300

Bal. 19,200

Operating Expenses

21,000

Income Tax Expense

14,910

EXERCISE 5-6B a. (cont.)

a. (2) LIFO

Date

Account Title

Debit

Credit

Apr. 1

Merchandise Inventory

84,000

Cash

84,000

Oct. 1

Merchandise Inventory

32,000

Cash

32,000

Sales

Cash (3,500 x $50)

175,000

Sales Revenue

175,000

Cost of Sales

Cost of Goods Sold*

107,000

Merchandise Inventory

107,000

Op. Exp.

Operating Expenses

21,000

Cash

21,000

Tax Exp.

Income Tax Expense

14,100

Cash

14,100

*10/1 1,000 @ $32 $ 32,000

4/1 2,500 @ $30 75,000

Cost of Goods Sold $107,000

EXERCISE 5-6B a. (cont.)

(2) LIFO

Cash

Common Stock

Bal. 36,000

Bal. 20,000

sales 175,000

4/1 84,000

10/1 32,000

Retained Earnings

Op. Exp. 21,000

Bal. 23,500

Tax 14,100

Bal. 59,900

Sales Revenue

sales 175,000

Merchandise Inventory

Bal. 7,500

Cost of Goods Sold

4/1 84,000

sold 107,000

10/1 32,000

sold 107,000

Bal. 16,500

Operating Expenses

21,000

Income Tax Expense

14,100

EXERCISE 5-6B (cont.)

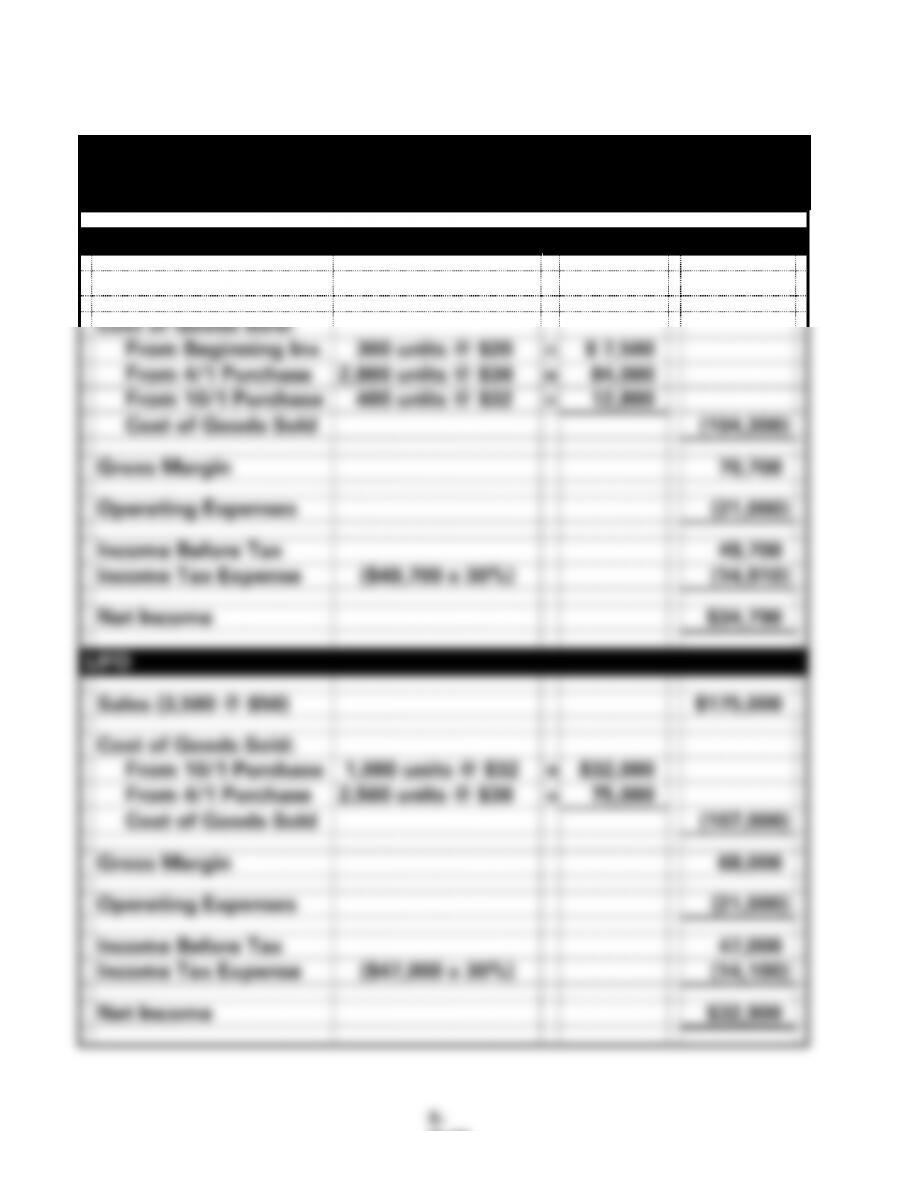

b.

Bryant Company

Income Statements

For the Year Ended December 31, 20XX

FIFO

Sales (3,500 @ $50)

$175,000

Cost of Goods Sold:

From Beginning Inv.

300 units @ $20

=

$ 7,500

From 4/1 Purchase

2,800 units @ $30

=

84,000

From 10/1 Purchase

400 units @ $32

=

12,800

Cost of Goods Sold

(104,300)

Gross Margin

70,700

Operating Expenses

(21,000)

Income Before Tax

49,700

Income Tax Expense

($49,700 x 30%)

(14,910)

Net Income

$34,790

LIFO

Sales (3,500 @ $50)

$175,000

Cost of Goods Sold:

From 10/1 Purchase

1,000 units @ $32

=

$32,000

From 4/1 Purchase

2,500 units @ $30

=

75,000

Cost of Goods Sold

(107,000)

Gross Margin

68,000

Operating Expenses

(21,000)

Income Before Tax

47,000

Income Tax Expense

($47,000 x 30%)

(14,100)

Net Income

$32,900

EXERCISE 5-6B (cont.)

c. Income tax savings would be the difference between the tax using

FIFO and the tax using LIFO, or $14,910 − $14,100 = $810.

d.

Bryant Company

Cash Flows from Operating Activities

FIFO

LIFO

Cash Flows From Operating Activities:

Cash Inflow from Customers

$175,000

$175,000

Cash Outflow for Inventory*

(116,000)

(116,000)

Cash Outflow for Operating Expenses

(21,000)

(21,000)

Cash Outflow for Income Tax Expense

(14,910)

(14,100)

Net Cash Flow from Operating Activities

$ 23,090

$ 23,900

*Computation of cash paid for inventory:

4/1 Purchase 2,800 units @ $30 = $ 84,000

10/1 Purchase 1,000 units @ 32 = 32,000

$116,000

e. More income tax must be paid on the higher amount of income

before tax reported under FIFO. Therefore, more cash used for

operating activities leaves less net cash flow from operating

activities.

5-82

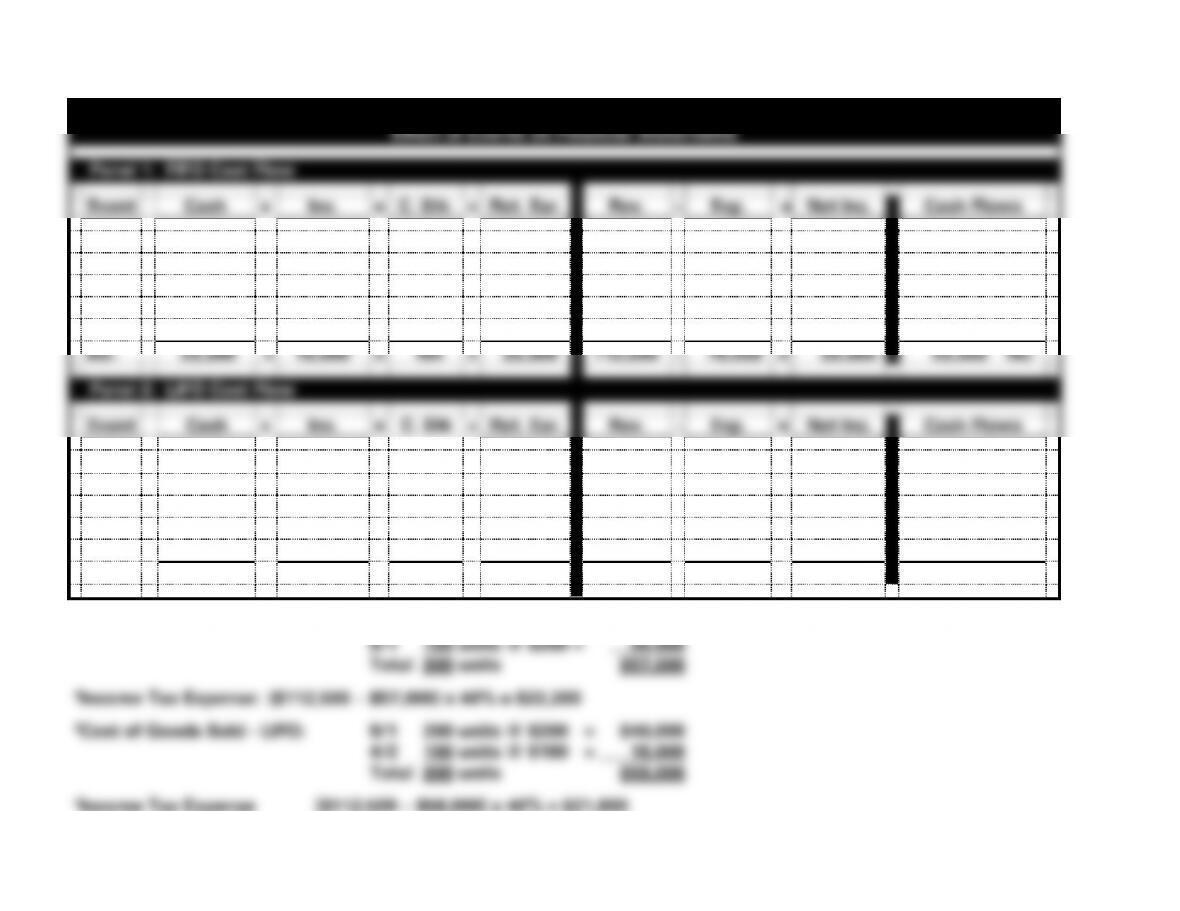

EXERCISE 5-7B a. NC = Net Change in Cash

Home Gifts, Inc.

Effect of Events on Financial Statements

Panel 1: FIFO Cost Flow

Event

Cash

+

Inv.

=

C. Stk.

+

Ret. Ear.

Rev.

−

Exp.

=

Net Inc.

Cash Flows

1.

112,500

+

NA

=

NA

+

112,500

112,500

−

NA

=

112,500

112,500 OA

2.

(27,000)

+

27,000

=

NA

+

NA

NA

−

NA

=

NA

(27,000) OA

3.

(40,000)

+

40,000

=

NA

+

NA

NA

−

NA

=

NA

(40,000) OA

4.

NA

+

(57,000)1

=

NA

+

(57,000)

NA

−

57,000

=

(57,000)

NA

5.

(22,200)2

+

NA

=

NA

+

(22,200)

NA

−

22,200

=

(22,200)

(22,200) OA

Bal.

23,300

+

10,000

=

NA

+

33,300

112,500

−

79,200

=

33,300

23,300 NC

Panel 2: LIFO Cost Flow

Event

Cash

+

Inv.

=

C. Stk

+

Ret. Ear.

Rev.

−

Exp.

=

Net Inc.

Cash Flows

1.

112,500

+

NA

=

NA

+

112,500

112,500

−

NA

=

112,500

112,500 OA

2.

(27,000)

+

27,000

=

NA

+

NA

NA

−

NA

=

NA

(27,000) OA

3.

(40,000)

+

40,000

=

NA

+

NA

NA

−

NA

=

NA

(40,000) OA

4.

NA

+

(58,000)3

=

NA

+

(58,000)

NA

−

58,000

=

(58,000)

NA

5.

(21,800)4

+

NA

=

NA

+

(21,800)

NA

−

21,800

=

(21,800)

(21,800) OA

Bal.

23,700

+

9,000

=

NA

+

32,700

112,500

−

79,800

=

32,700

23,700 NC

1Cost of Goods Sold – FIFO: 4/2 150 units @ $180 = $27,000

5-83

EXERCISE 5-7B (cont.)

b. Net Income assuming FIFO cost flow: $33,300 (see statements model

above).

c. Net Income assuming LIFO cost flow: $32,700 (see statements model

above).

EXERCISE 5-8B

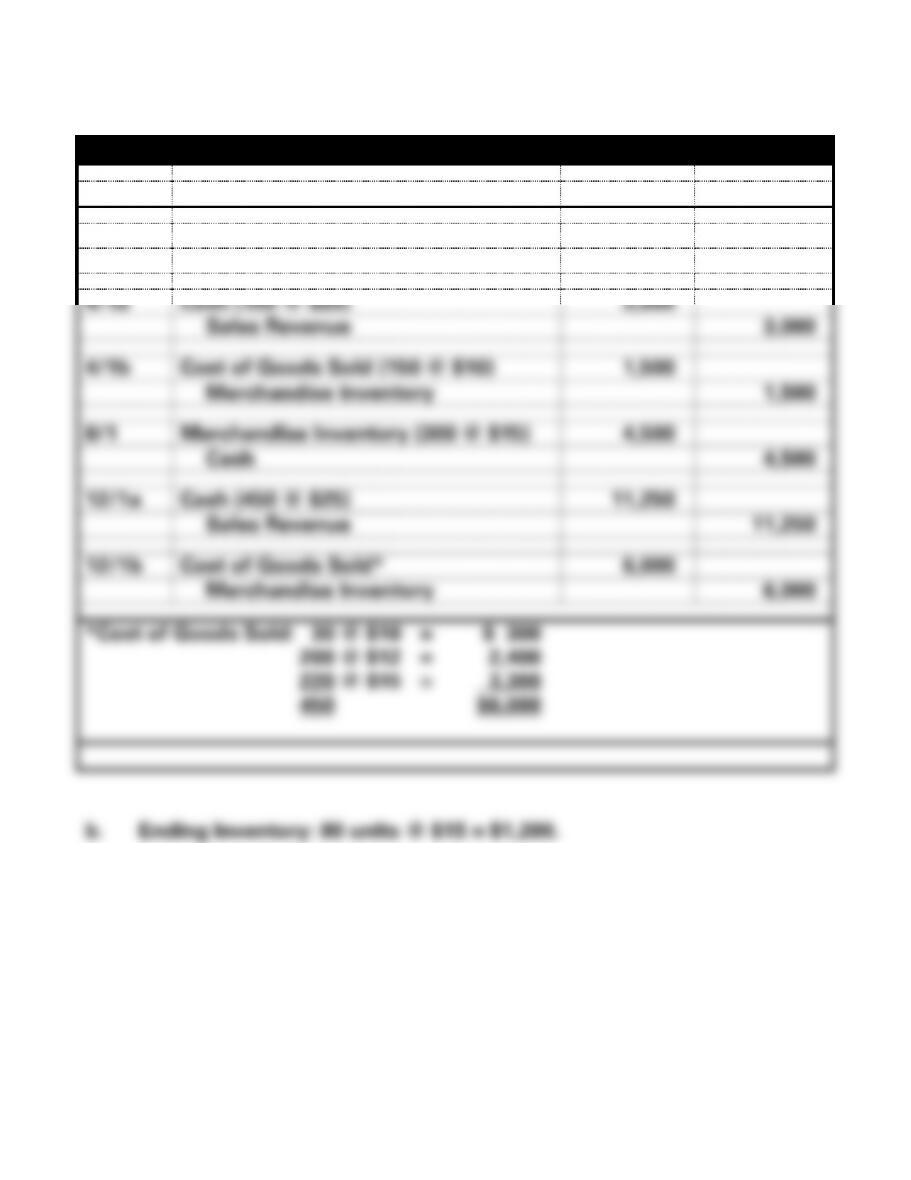

a.

Duncan Steel Company General Journal

Date

Account Titles

Debit

Credit

1/1/11

Merchandise Inventory (200 @ $12)

2,400

Cash

2,400

4/1a

Cash (150 @ $20)

3,000

Sales Revenue

3,000

4/1b

Cost of Goods Sold (150 @ $10)

1,500

Merchandise Inventory

1,500

8/1

Merchandise Inventory (300 @ $15)

4,500

Cash

4,500

12/1a

Cash (450 @ $25)

11,250

Sales Revenue

11,250

12/1b

Cost of Goods Sold*

6,000

Merchandise Inventory

6,000

*Cost of Goods Sold: 30 @ $10 = $ 300

200 @ $12 = 2,400

220 @ $15 = 3,300

450 $6,000

5-85

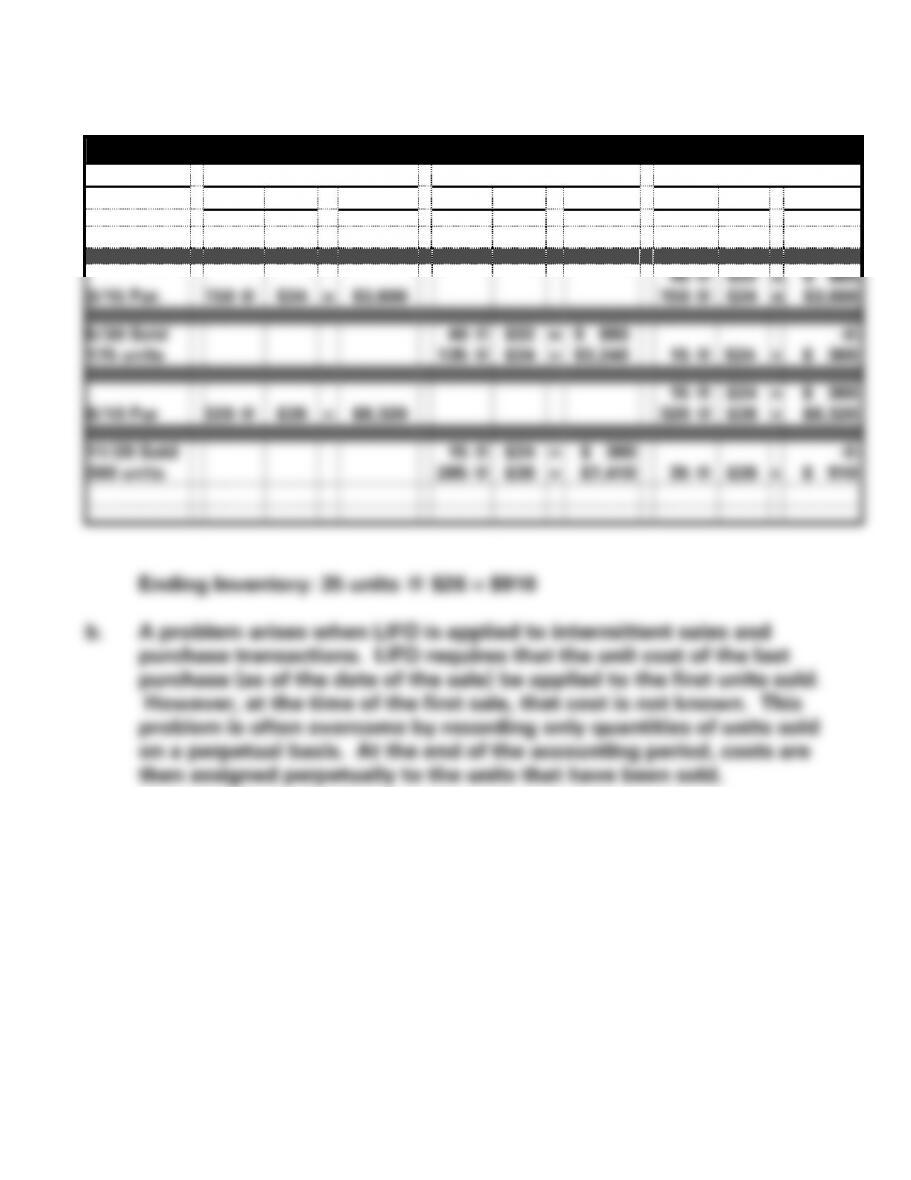

EXERCISE 5-9A

a.

Nash Auto Parts, Inc.

Date

Purchased

Sold

Inventory Balance

Units

Cost

Total

Units

Cost

Total

Units

Cost

Total

1/1 Beg. Inv.

40 @

$22

=

$ 880

3/15 Pur.

150 @

$24

=

$3,600

40 @

150 @

$22

$24

=

=

$ 880

$3,600

5/30 Sold

175 units

40 @

135 @

$22

$24

=

=

$ 880

$3,240

15 @

$24

=

-0-

$ 360

8/10 Pur

320 @

$26

=

$8,320

15 @

320 @

$24

$26

=

=

$ 360

$8,320

11/20 Sold

300 units

15 @

285 @

$24

$26

=

=

$ 360

$7,410

35 @

$26

=

-0-

$ 910

Ending Inventory: 35 units @ $26 = $910

b. A problem arises when LIFO is applied to intermittent sales and

purchase transactions. LIFO requires that the unit cost of the last

purchase (as of the date of the sale) be applied to the first units sold.

However, at the time of the first sale, that cost is not known. This

problem is often overcome by recording only quantities of units sold

on a perpetual basis. At the end of the accounting period, costs are

then assigned perpetually to the units that have been sold.

5-86

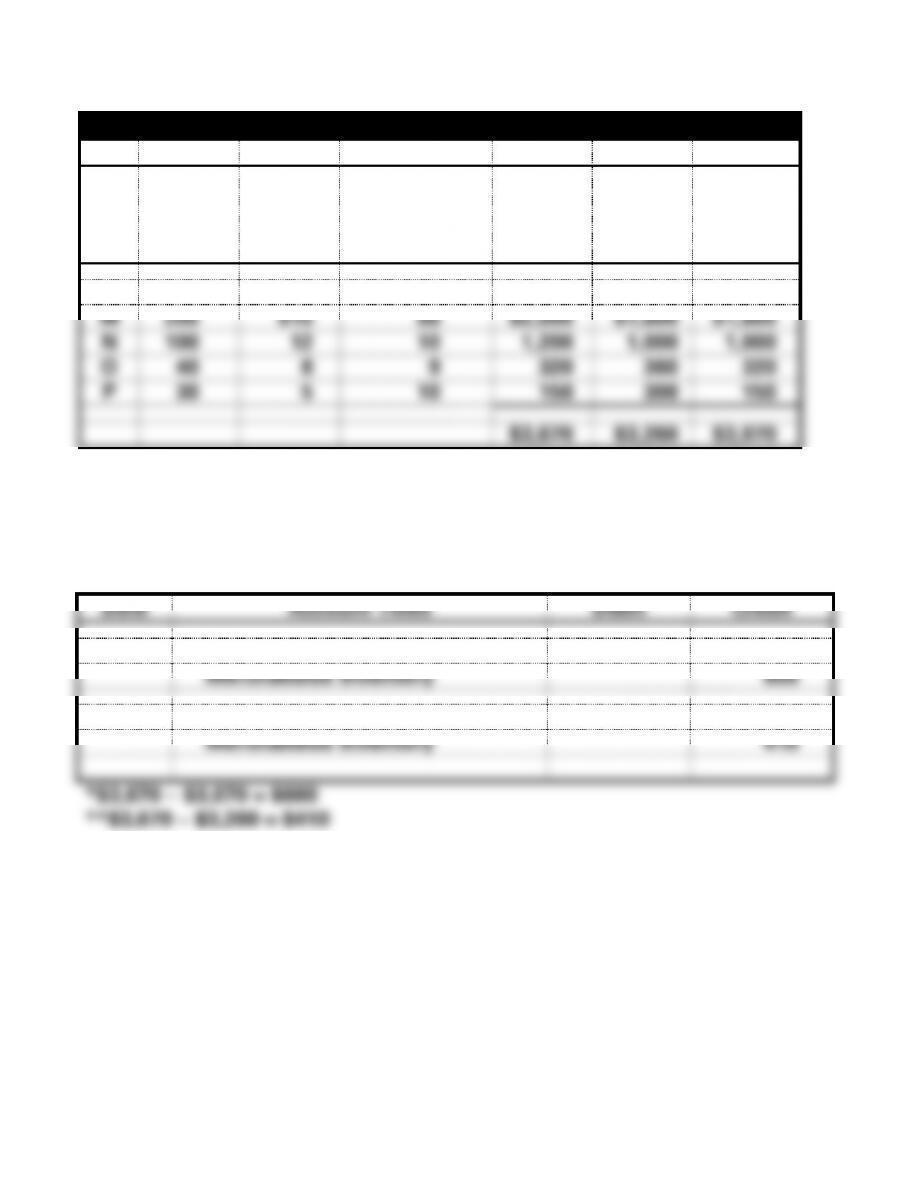

EXERCISE 5-10B

a.

James Hardware

a.

b.

c.

d.

e.

f.

g.

Item

Quantity

Cost Per

Unit

Mkt. Val.

per Unit

Total

Cost

Total

Market

Ind. Item

Lower

Cost/Mkt

.

(b x c)

(b x d)

(e or f)

M

200

$10

$8

$2,000

$1,600

$1,600

N

100

12

10

1,200

1,000

1,000

O

40

8

9

320

360

320

P

30

5

10

150

300

150

$3,670

$3,260

$3,070

(1) Ending inventory using the individual item method: $3,070

(2) Ending inventory using the aggregate method: $3,260

b.

Date

Account Titles

Debit

Credit

(1)

Cost of Goods Sold*

600

Merchandise Inventory

600

(2)

Cost of Goods Sold**

410

Merchandise Inventory

410