3-6–45

COMPREHENSIVE PROBLEM – CHAPTER 3 (cont.)

e.

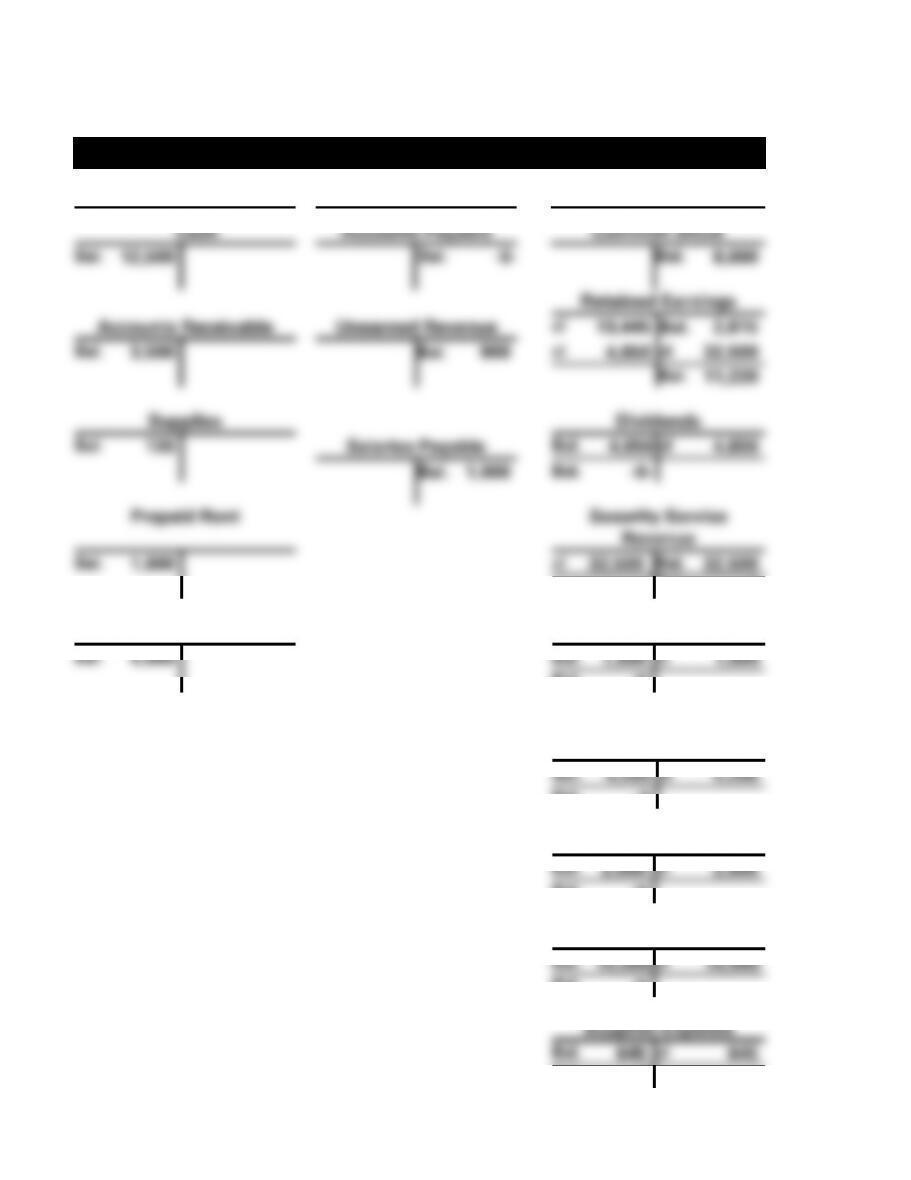

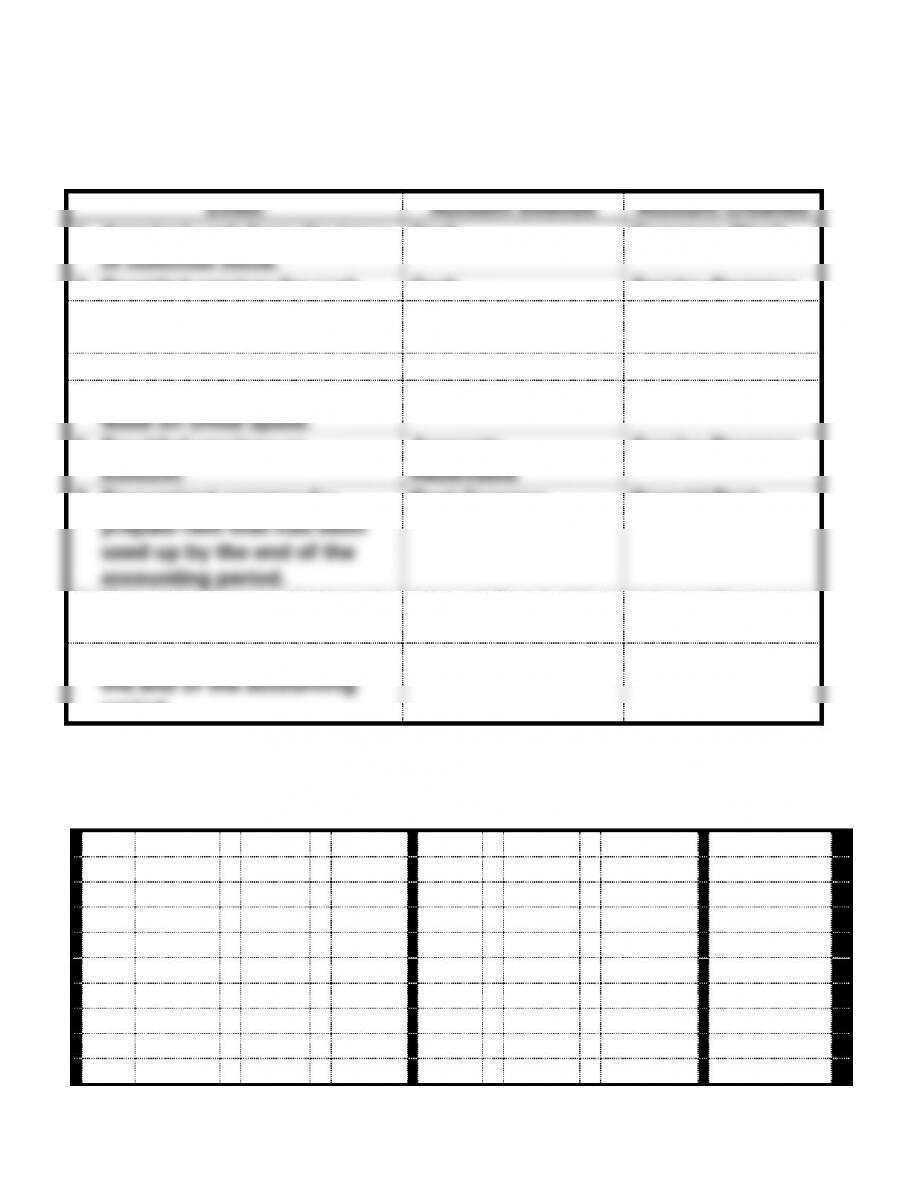

Pacilio Security Services, Inc. T-Accounts for 2013

Assets

=

Liabilities

+

Stockholders’ Equity

Cash

Accounts Payable

Common Stock

Bal.

12,500

Bal.

-0-

Bal.

8,000

Retained Earnings

Accounts Receivable

Unearned Revenue

cl

19,445

Bal.

2,815

Bal.

3,500

Bal.

900

cl

4,650

cl

32,500

Bal.

11,220

Supplies

Dividends

Bal.

120

Salaries Payable

Bal.

4,650

cl

4,650

Bal.

1,000

Bal.

-0-

Prepaid Rent

Security Service

Revenue

Bal.

1,000

cl

32,500

Bal.

32,500

Bal.

-0-

Land

Advertising Expense

Bal.

4,000

Bal.

1,800

cl

1,800

Bal.

-0-

Other Operating

Expense

Bal.

4,200

cl

4,200

Bal.

-0-

Rent Expense

Bal.

2,800

cl

2,800

Bal.

-0-

Salaries Expense

Bal.

10,000

cl

10,000

Bal.

-0-

Supplies Expense

Bal.

645

cl

645

Bal.

-0-

3-6–46

3-6–47

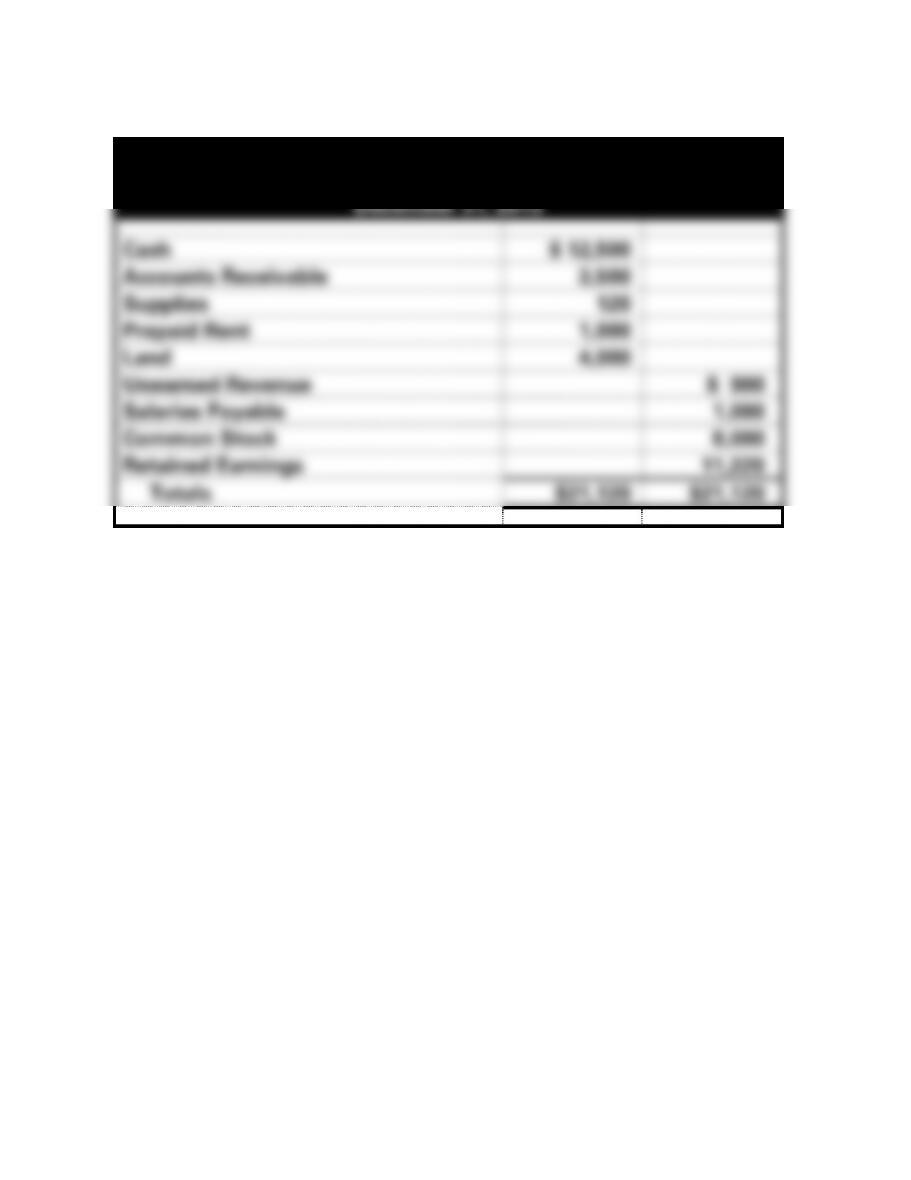

COMPREHENSIVE PROBLEM- CHAPTER 3 (cont.)

f.

Pacilio Security Services, Inc.

Post-Closing Trial Balance

December 31, 2013

Cash

$ 12,500

Accounts Receivable

3,500

Supplies

120

Prepaid Rent

1,000

Land

4,000

Unearned Revenue

$ 900

Salaries Payable

1,000

Common Stock

8,000

Retained Earnings

11,220

Totals

$21,120

$21,120

3-6–48

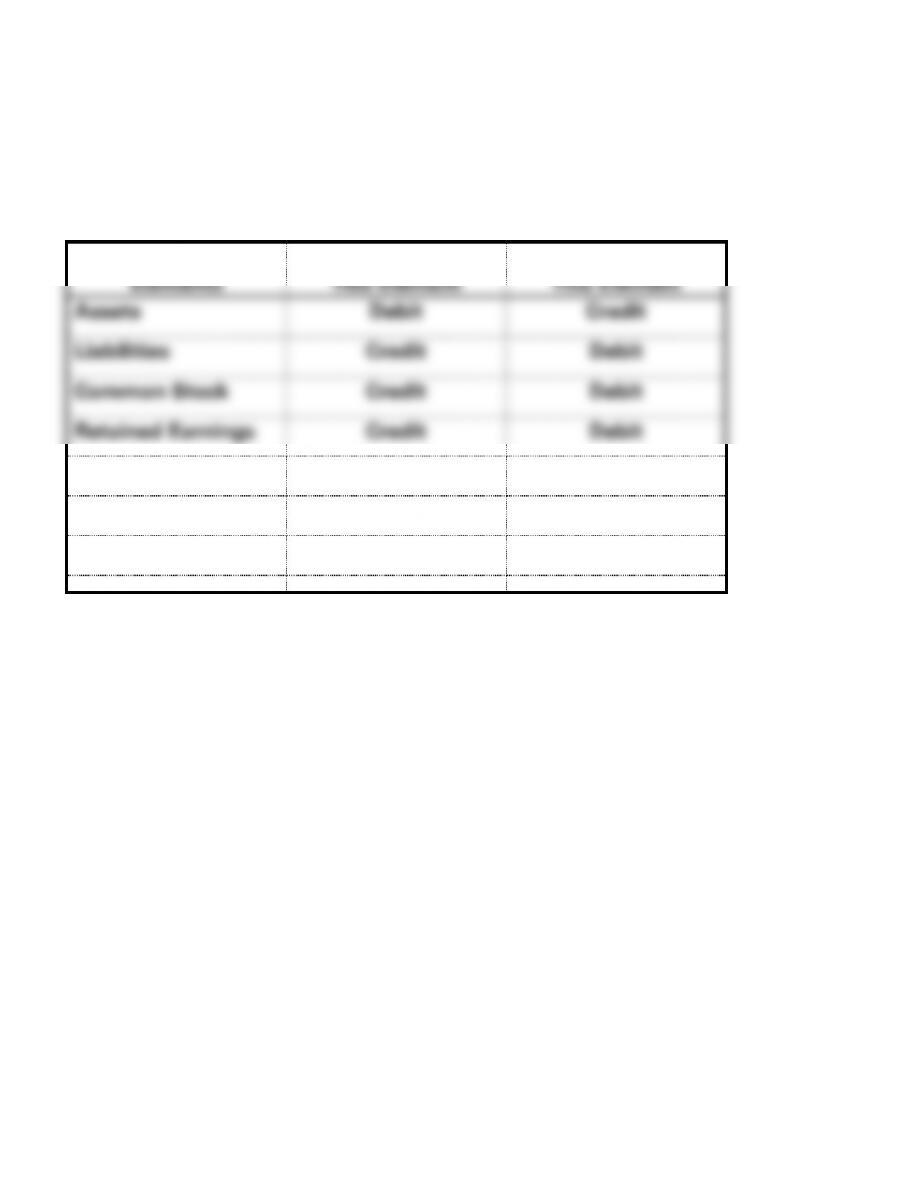

SOLUTIONS TO EXERCISES – SERIES A – CHAPTER 3

EXERCISE 3-1A

Accounting

Elements

Used to Increase

This Element

Used to Decrease

This Element

Assets

Debit

Credit

Liabilities

Credit

Debit

Common Stock

Credit

Debit

Retained Earnings

Credit

Debit

Revenue

Credit

Debit

Expense

Debit

Credit

Dividends

Debit

Credit

3-6–49

EXERCISE 3-2A

3-6–50

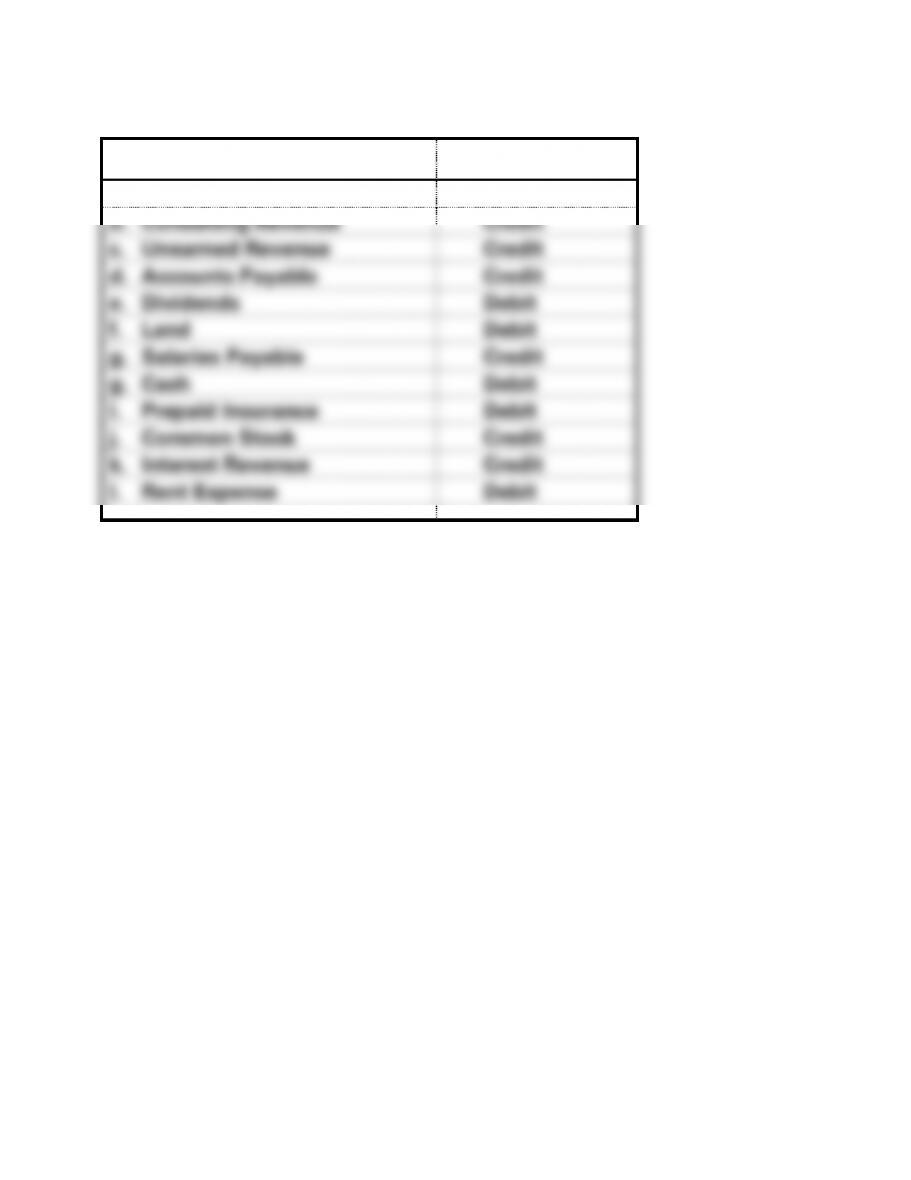

EXERCISE 3-3A

Account

Normal Balance

a. Salaries Expense

Debit

b. Consulting Revenue

Credit

c. Unearned Revenue

Credit

d. Accounts Payable

Credit

e. Dividends

Debit

f. Land

Debit

g. Salaries Payable

Credit

g. Cash

Debit

i. Prepaid Insurance

Debit

j. Common Stock

Credit

k. Interest Revenue

Credit

l. Rent Expense

Debit

EXERCISE 3-4A

a.

Event

Account Debited

Account Credited

1. Acquired cash from the issue

of common stock.

Cash

Common Stock

2. Provided services for cash.

Cash

Service Revenue

3. Paid cash for salaries

expense.

Salaries Expense

Cash

4. Purchased supplies for cash.

Supplies

Cash

5. Paid in advance for two-year

lease on office space.

Prepaid Rent

Cash

6. Provided services on

account.

Accounts

Receivable

Service Revenue

7. Recognized expense for

prepaid rent that had been

used up by the end of the

accounting period.

Rent Expense

Prepaid Rent

8. Recognized accrued interest

revenue

Interest Receivable

Interest Revenue

9. Recorded accrued salaries at

the end of the accounting

period.

Salaries Expense

Salaries Payable

b.

No.

Assets

=

Liab.

+

Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

1.

+

NA

+

NA

NA

NA

+ FA

2.

+

NA

+

+

NA

+

+ OA

3.

−

NA

−

NA

+

−

− OA

4.

+/−

NA

NA

NA

NA

NA

− OA

5.

+/−

NA

NA

NA

NA

NA

− OA

6.

+

NA

+

+

NA

+

+ OA

7.

−

NA

−

NA

+

−

NA

8.

+

NA

+

+

NA

+

NA

9.

NA

+

−

NA

+

−

NA

3-6–52

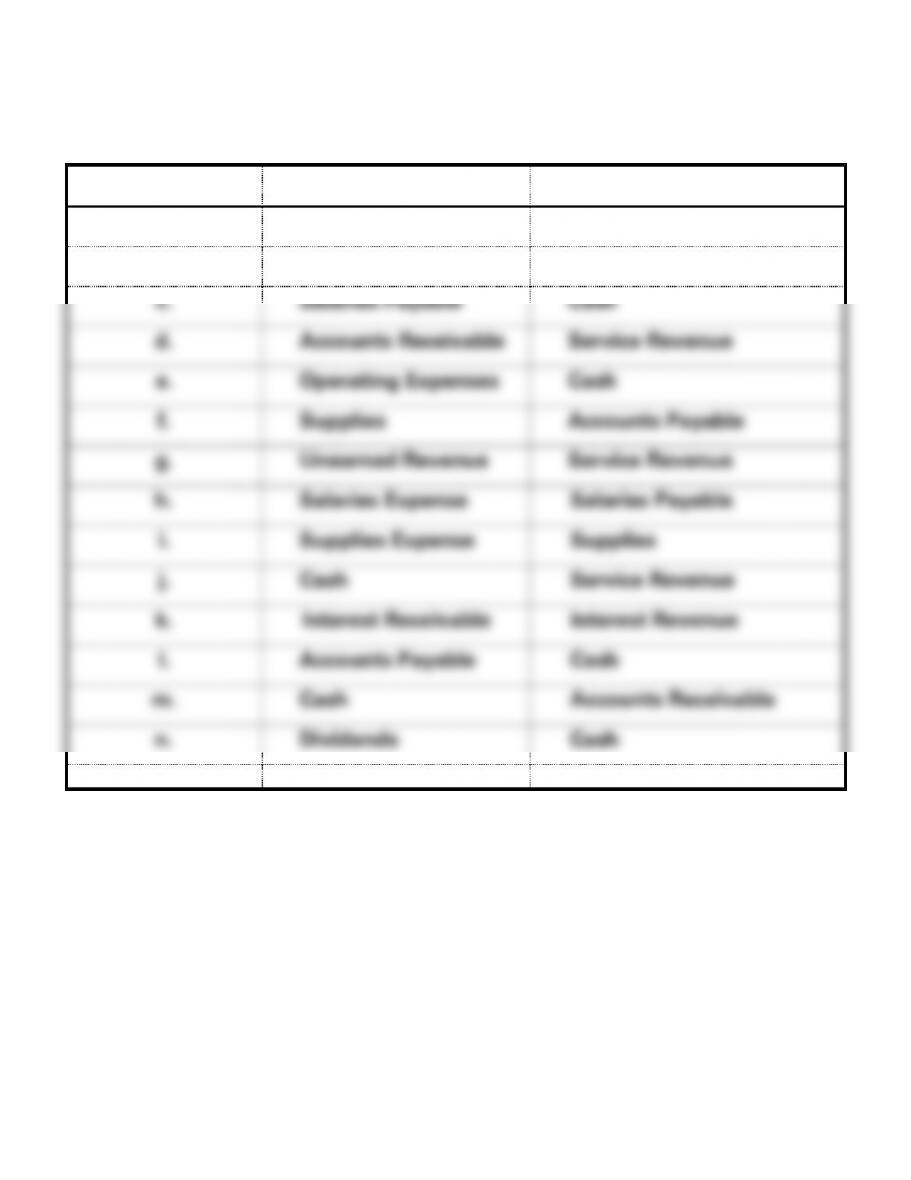

EXERCISE 3-5A

Event

Account Debited

Account Credited

a.

Cash

Common Stock

b.

Cash

Unearned Revenue

c.

Salaries Payable

Cash

d.

Accounts Receivable

Service Revenue

e.

Operating Expenses

Cash

f.

Supplies

Accounts Payable

g.

Unearned Revenue

Service Revenue

h.

Salaries Expense

Salaries Payable

i.

Supplies Expense

Supplies

j.

Cash

Service Revenue

k.

Interest Receivable

Interest Revenue

l.

Accounts Payable

Cash

m.

Cash

Accounts Receivable

n.

Dividends

Cash

3-6–53

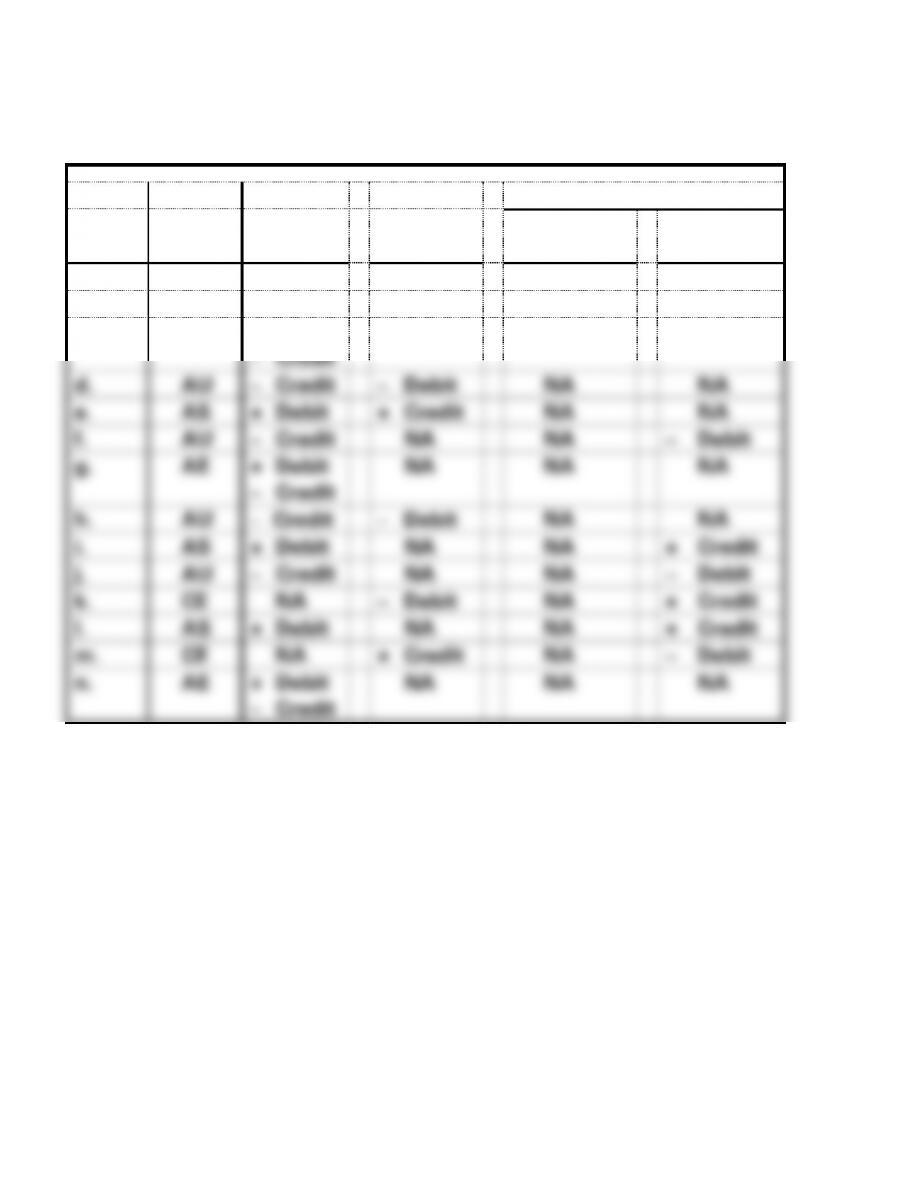

EXERCISE 3-6A

Stockholders’ Equity

Event

Type of

Event

Assets

=

Liabilities

+

Common

Stock

+

Retained

Earnings

a.

AS

+ Debit

+ Credit

NA

NA

b.

AS

+ Debit

NA

+ Credit

NA

c.

AE

+ Debit

− Credit

NA

NA

NA

d.

AU

− Credit

− Debit

NA

NA

e.

AS

+ Debit

+ Credit

NA

NA

f.

AU

− Credit

NA

NA

− Debit

g.

AE

+ Debit

− Credit

NA

NA

NA

h.

AU

− Credit

− Debit

NA

NA

i.

AS

+ Debit

NA

NA

+ Credit

j.

AU

− Credit

NA

NA

− Debit

k.

CE

NA

− Debit

NA

+ Credit

l.

AS

+ Debit

NA

NA

+ Credit

m.

CE

NA

+ Credit

NA

− Debit

n.

AE

+ Debit

− Credit

NA

NA

NA

3-6–54

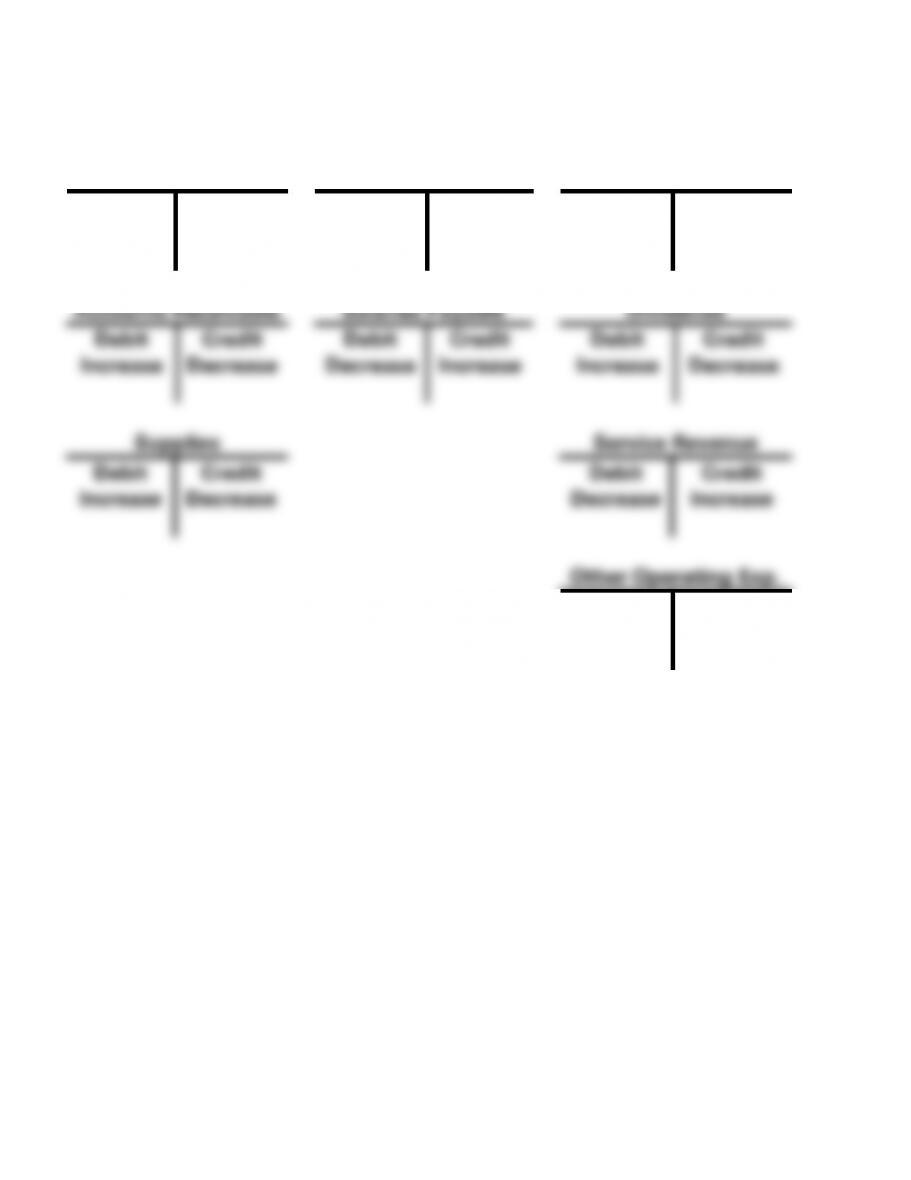

EXERCISE 3-7A

Cash

Accounts Payable

Common Stock

Debit

Credit

Debit

Credit

Debit

Credit

Increase

Decrease

Decrease

Increase

Decrease

Increase

Accounts Receivable

Salaries Payable

Dividends

Debit

Credit

Debit

Credit

Debit

Credit

Increase

Decrease

Decrease

Increase

Increase

Decrease

Supplies

Service Revenue

Debit

Credit

Debit

Credit

Increase

Decrease

Decrease

Increase

Other Operating Exp.

Debit

Credit

Increase

Decrease

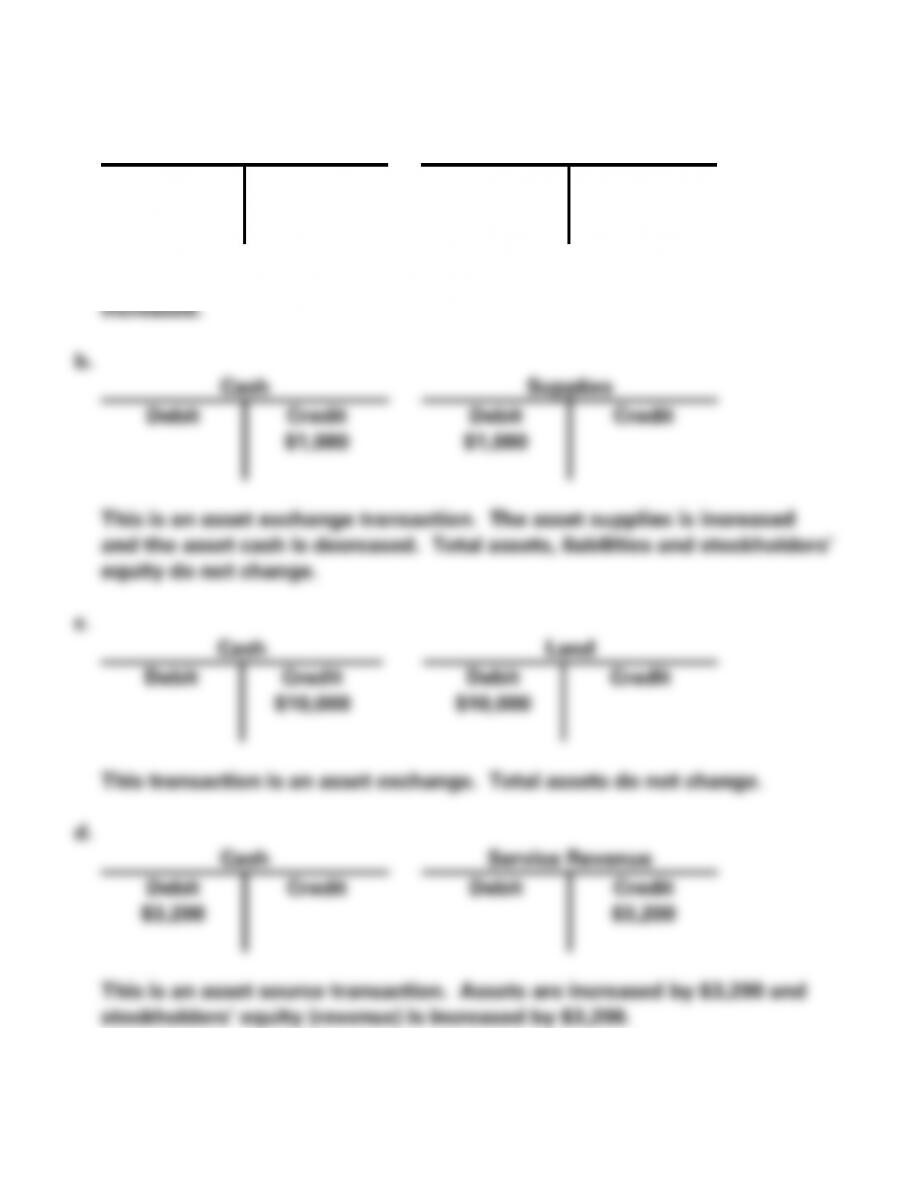

EXERCISE 3-8A

a.

Cash

Common Stock

Debit

Credit

Debit

Credit

$20,000

$20,000

This is an asset source transaction. Assets are increased; equity is

Cash

Supplies

Debit

Credit

Debit

Credit

$1,000

$1,000

Credit

Credit

Cash

Debit

Credit

Credit

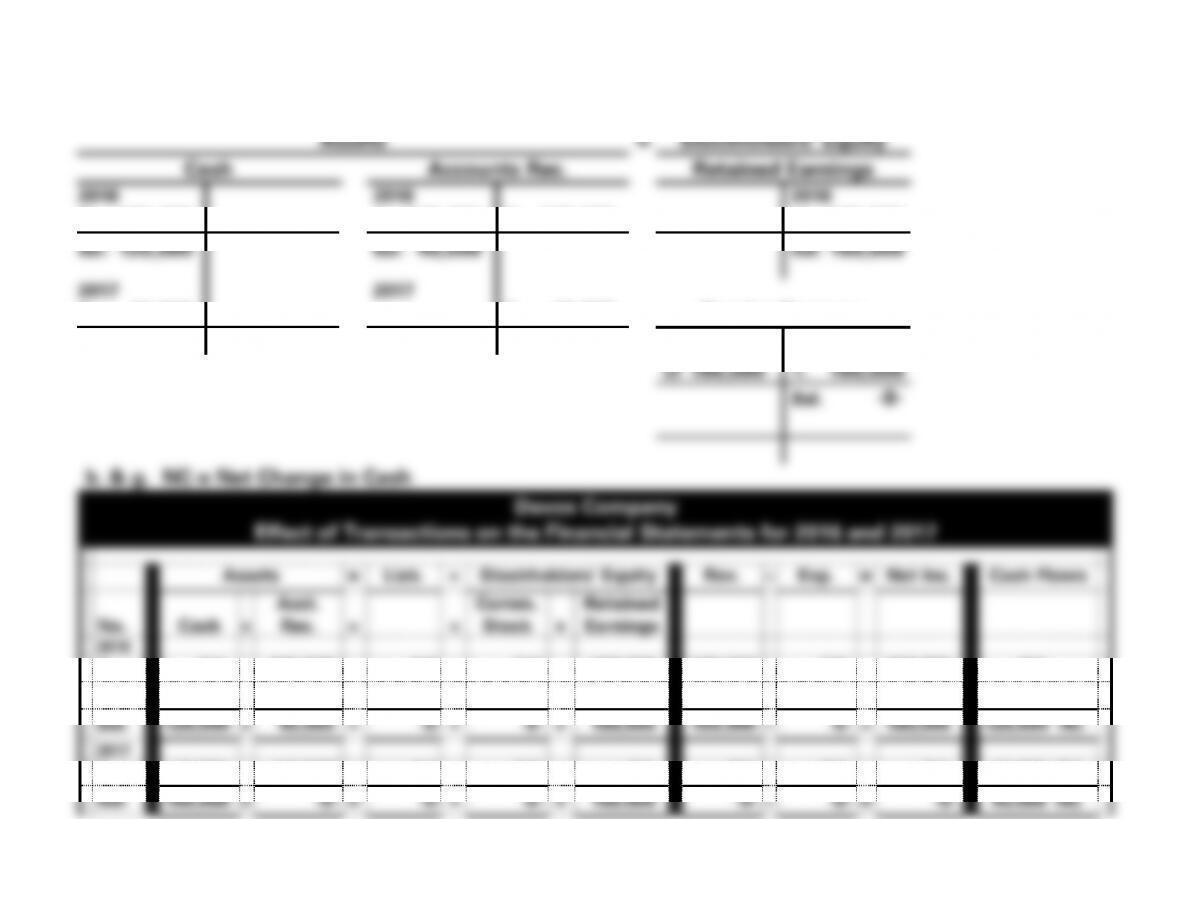

EXERCISE 3-9A

a., e. & f.

Assets

=

Stockholders’ Equity

Cash

Accounts Rec.

Retained Earnings

2016

2016

2016

2. 120,000

1. 160,000

2. 120,000

cl 160,000

Bal. 120,000

Bal. 40,000

Bal. 160,000

2017

2017

3. 40,000

3. 40,000

Service Revenue

Bal. 160,000

Bal. -0-

2016

cl 160,000

1. 160,000

Bal. -0-

+

3-57

3-58

EXERCISE 3-9A (cont.)

c. 2016 Revenue = $160,000

3-59

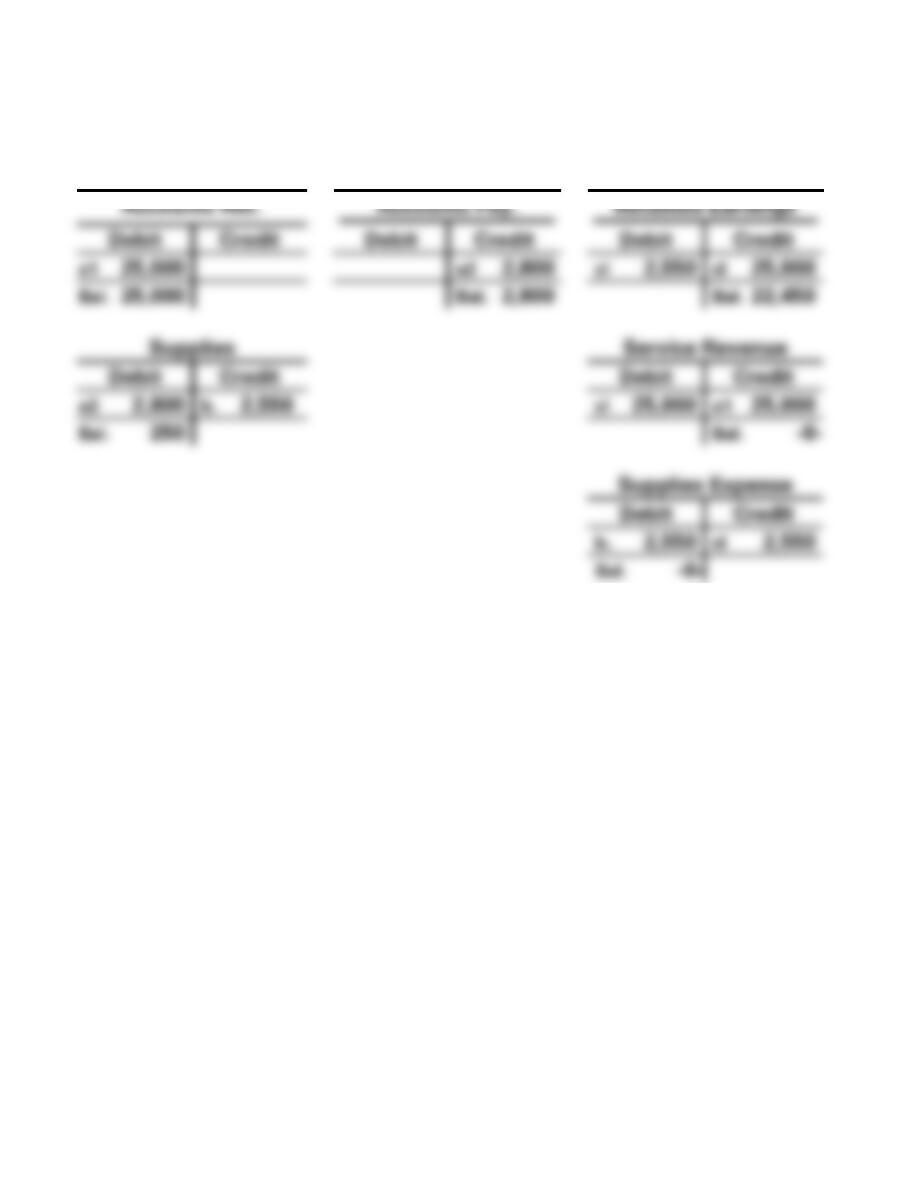

EXERCISE 3-10A

a. b. & e.

Assets

=

Liabilities

+

Stockholders’ Equity

Accounts Rec.

Accounts Pay.

Retained Earnings

Debit

Credit

Debit

Credit

Debit

Credit

a1 25,000

a2 2,800

cl 2,550

cl 25,000

Bal. 25,000

Bal. 2,800

Bal. 22,450

Supplies

Service Revenue

Debit

Credit

Debit

Credit

a2 2,800

b. 2,550

cl 25,000

a1 25,000

Bal. 250

Bal. -0-

Supplies Expense

Debit

Credit

b. 2,550

cl 2,550

Bal. -0-

3-60

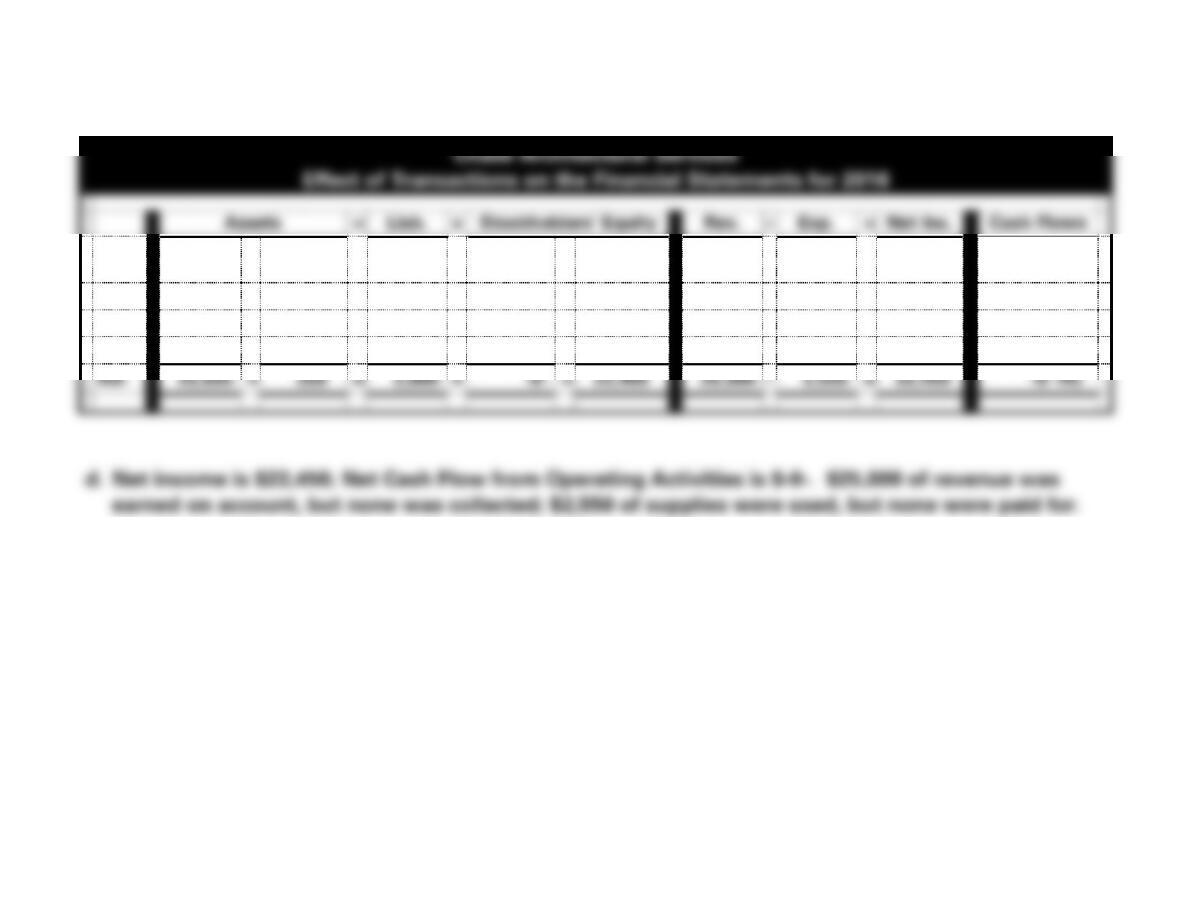

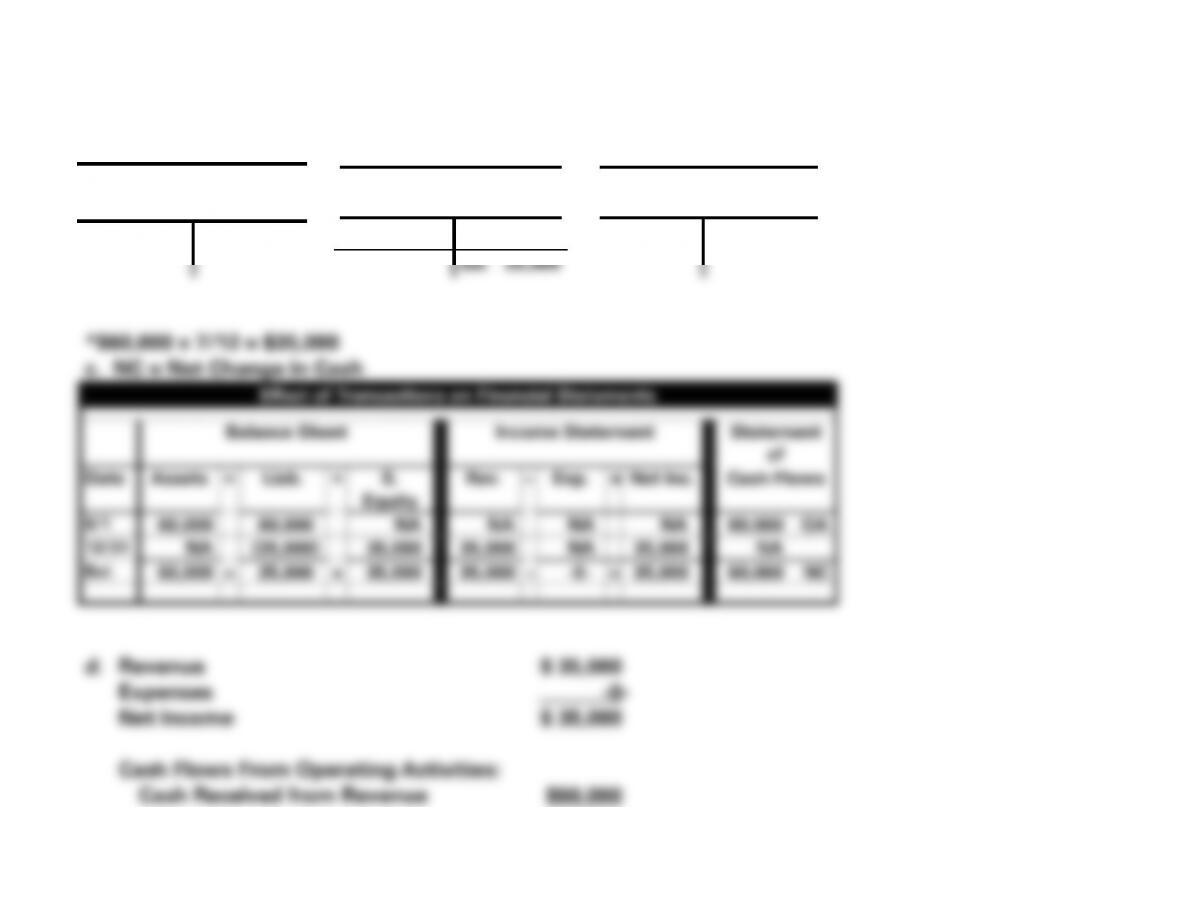

EXERCISE 3-10A (cont.)

c. NC = Net Change in Cash

Chase Architectural Services

Effect of Transactions on the Financial Statements for 2016

Assets

=

Liab.

+

Stockholders’ Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flows

No.

Accts.

Rec.

+

Supplies

=

Accts.

Pay.

+

Commo

n Stock

+

Retained

Earnings

a1.

25,000

NA

NA

NA

25,000

25,000

NA

25,000

NA

a2.

NA

2,800

2,800

NA

NA

NA

NA

NA

NA

b.

NA

(2,550)

NA

NA

(2,550)

NA

2,550

(2,550)

NA

Bal.

25,000

+

250

=

2,800

+

-0-

+

22,450

25,000

−

2,550

=

22,450

-0- NC

d. Net income is $22,450; Net Cash Flow from Operating Activities is $-0-. $25,000 of revenue was

earned on account, but none was collected; $2,550 of supplies were used, but none were paid for.

3-61

EXERCISE 3-10A (cont.)

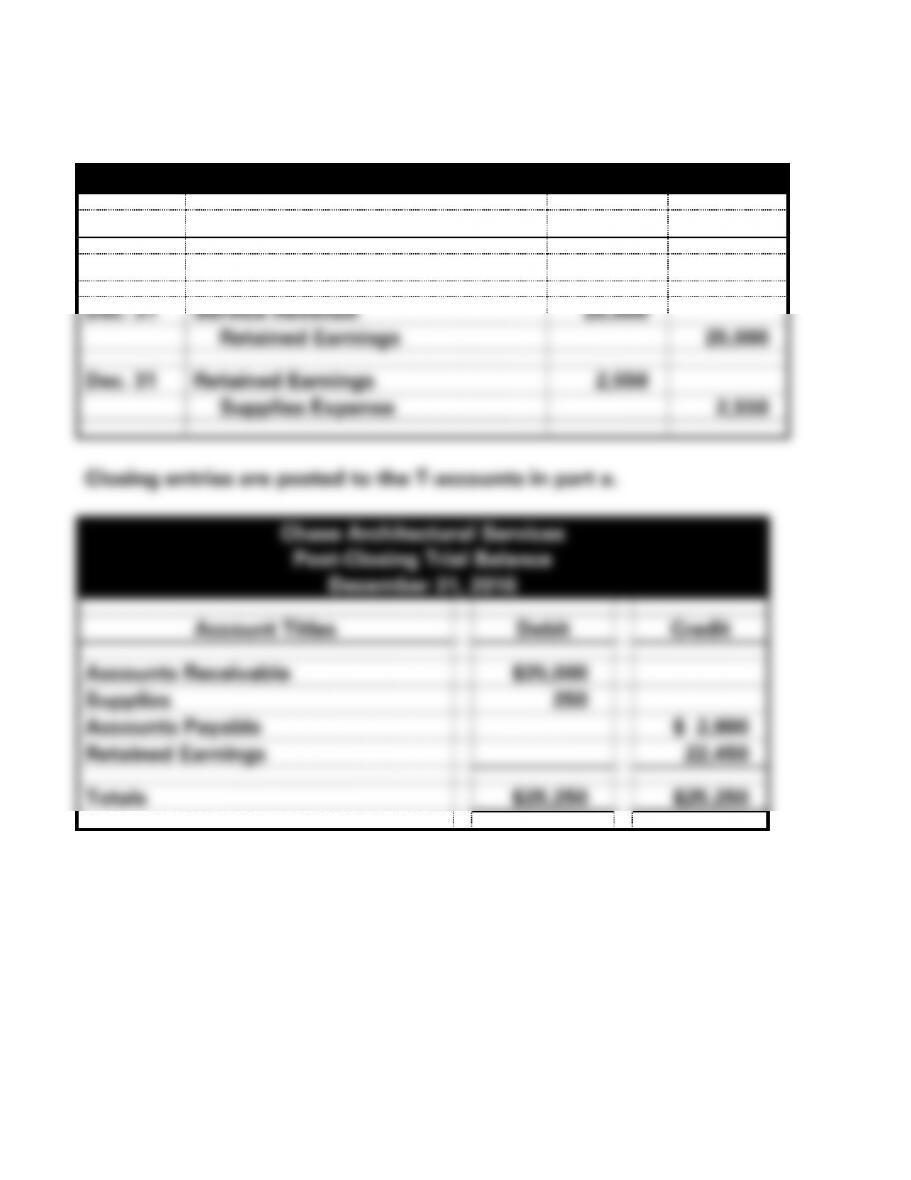

e.

General Journal

Date

Account Titles

Debit

Credit

Closing Entries

Dec. 31

Service Revenue

25,000

Retained Earnings

25,000

Dec. 31

Retained Earnings

2,550

Supplies Expense

2,550

Closing entries are posted to the T-accounts in part a.

Chase Architectural Services

Post-Closing Trial Balance

December 31, 2016

Account Titles

Debit

Credit

Accounts Receivable

$25,000

Supplies

250

Accounts Payable

$ 2,800

Retained Earnings

22,450

Totals

$25,250

$25,250

3-62

EXERCISE 3-11A

a. & b.

Assets

=

Liabilities

+

Stockholders’ Equity

Cash

Unearned Revenue

Service Revenue

6/1 60,000

12/31 35,000

6/1 60,000

12/31 35,000*

Bal. 25,000

3-63

Net Cash Flow from Operating Activities $60,000

3-64

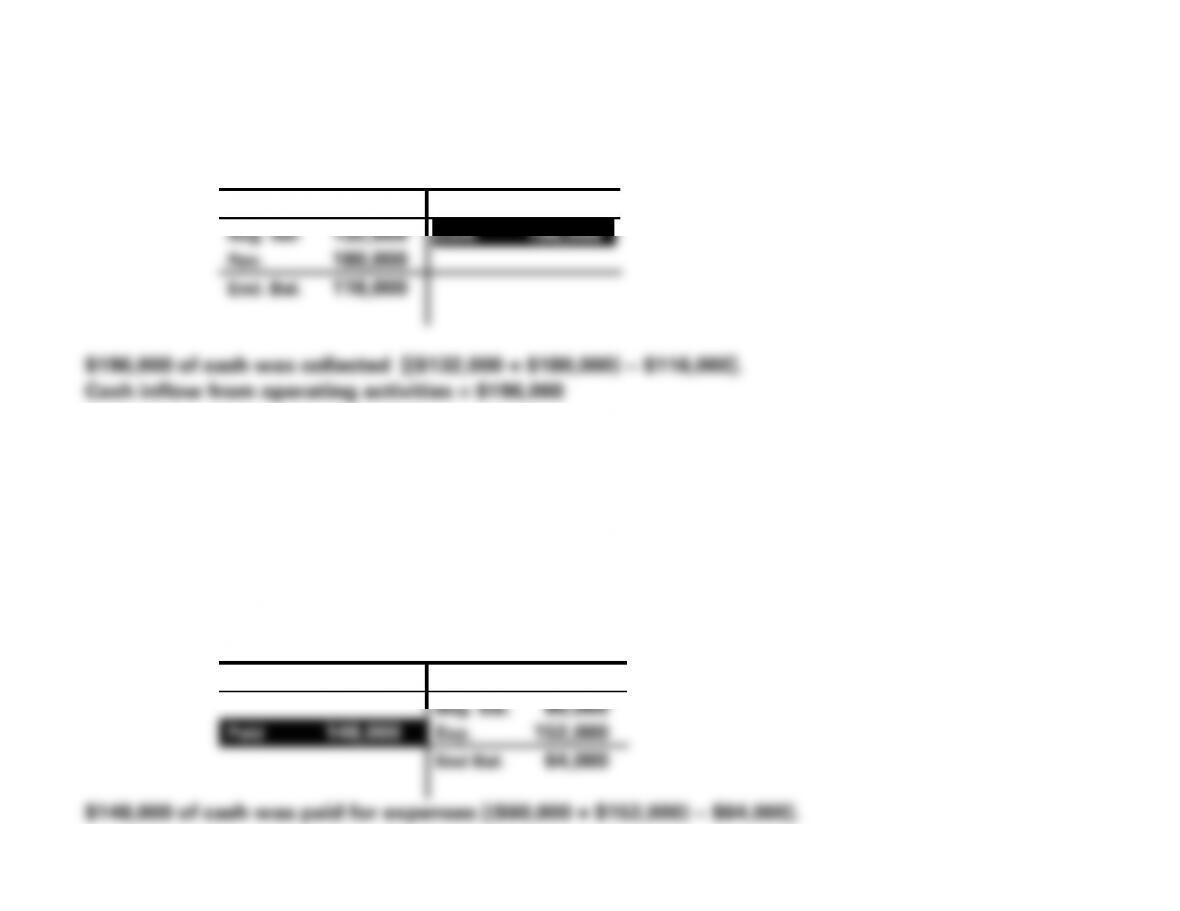

EXERCISE 3-12A

Accounts Receivable

Debit

Credit

Beg. Bal. 132,000

Coll. 196,000

Rev. 180,000

End. Bal. 116,000

$196,000 of cash was collected [($132,000 + $180,000) − $116,000].

Cash inflow from operating activities = $196,000

EXERCISE 3-13A

Accounts Payable

Debit

Credit

Beg. Bal. 60,000

Paid 148,000

Exp. 152,000

End Bal. 64,000

$148,000 of cash was paid for expenses [($60,000 + $152,000) − $64,000].