8-65

EXERCISE 8-7B a. (cont.)

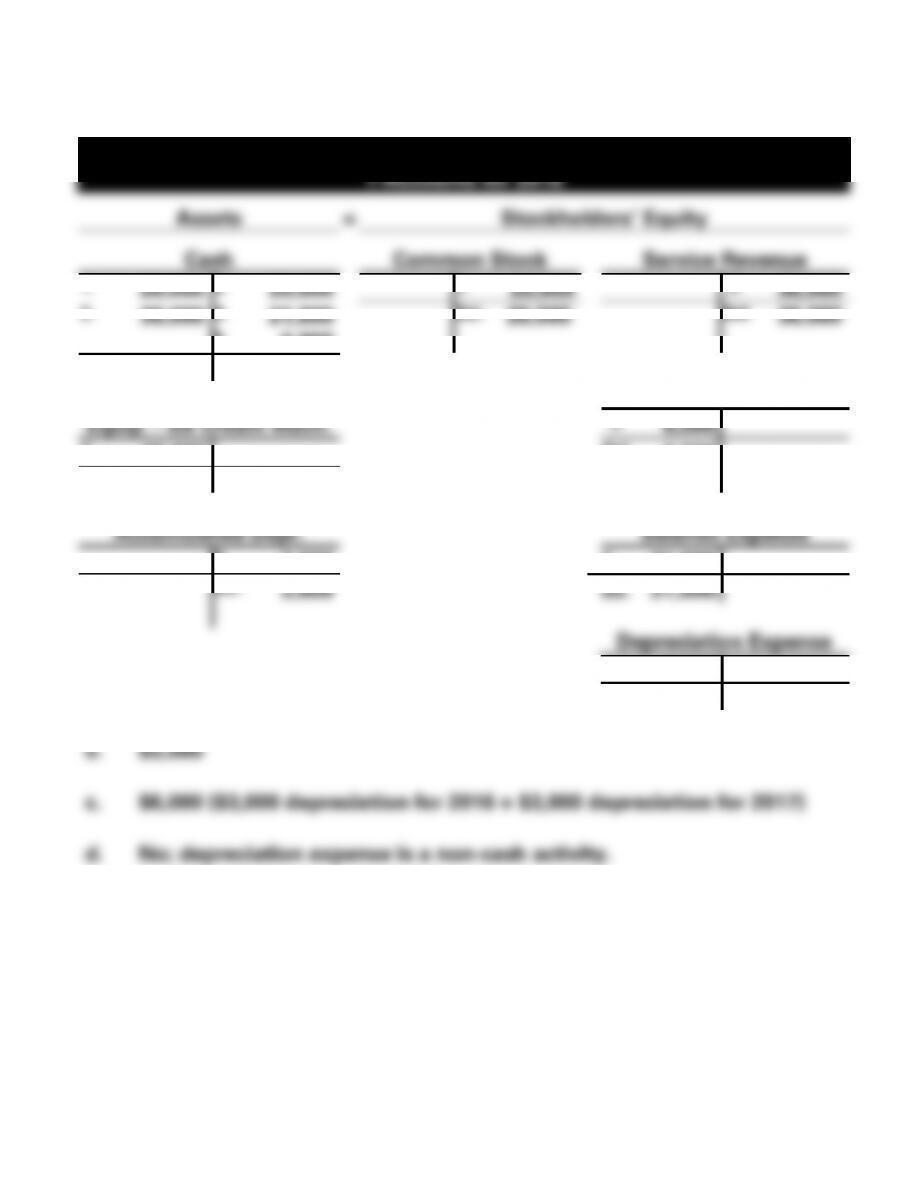

The Soda Shop

T-Accounts for 2016

Assets

=

Stockholders’ Equity

Cash

Common Stock

Service Revenue

1.

20,000

2.

20,000

1.

20,000

3.

36,000

3.

36,000

4.

21,000

Bal.

20,000

Bal.

36,000

5.

6,000

Bal.

9,000

Operating Expense

Equip. – Ice Cream Mach.

5.

6,000

2.

20,000

Bal.

6,000

Bal.

20,000

Accumulated Depr.

Salaries Expense

6.

3,000

4.

21,000

Bal.

3,000

Bal. 21,000

Depreciation Expense

6. 3,000

Bal.

3,000

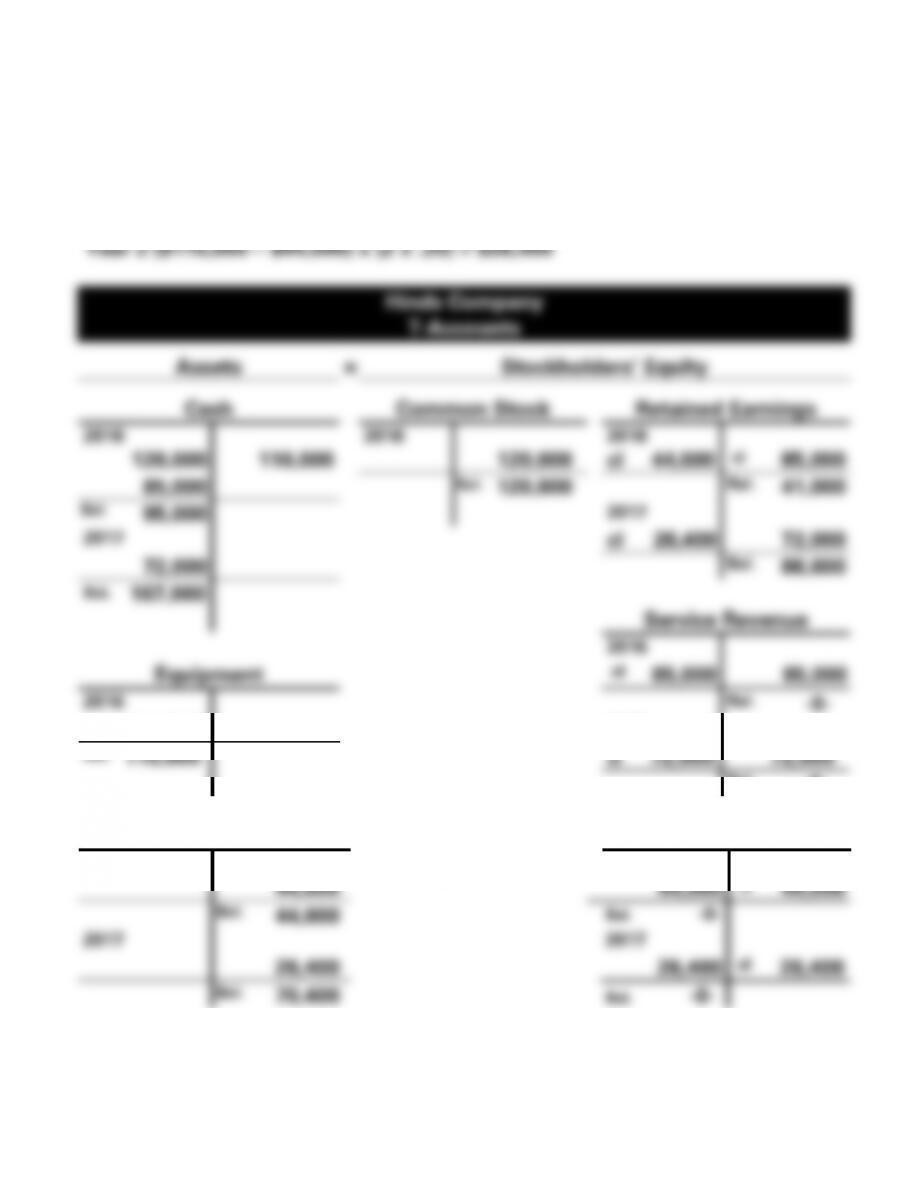

EXERCISE 8-8B

*Depreciation Calculation: (Cost − Accumulated Depr.) x (2 x SL Rate)

SL Rate = 1 5 = 20%

Year 1 ($110,000 − $ -0-) x (2 x .20) = $44,000

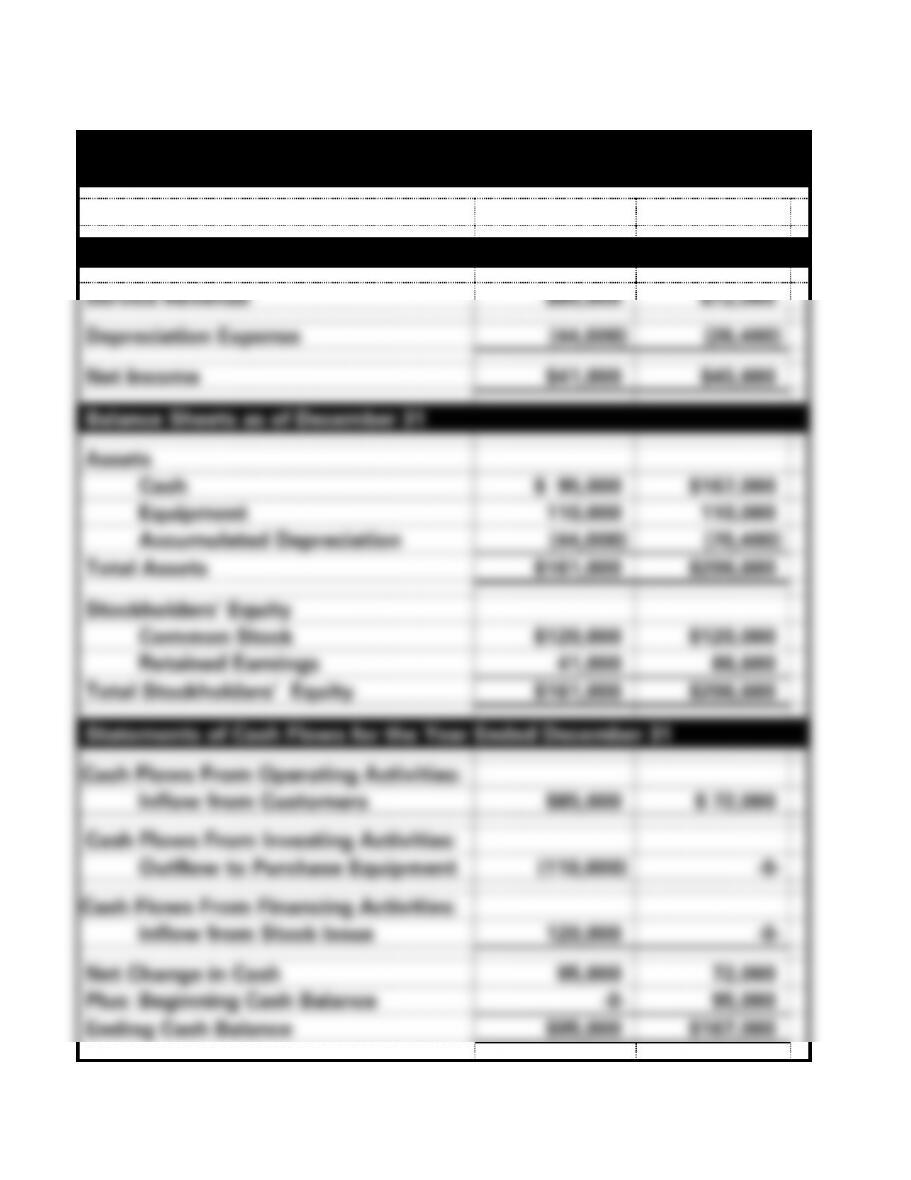

8-67

EXERCISE 8-8B (cont.)

Hinds Company

Financial Statements

2016

2017

Income Statements for the Year Ended December 31

Service Revenue

$85,000

$72,000

Depreciation Expense

(44,000)

(26,400)

Net Income

$41,000

$45,600

Balance Sheets as of December 31

Assets

Cash

$ 95,000

$167,000

Equipment

110,000

110,000

Accumulated Depreciation

(44,000)

(70,400)

Total Assets

$161,000

$206,600

Stockholders’ Equity

Common Stock

$120,000

$120,000

Retained Earnings

41,000

86,600

Total Stockholders’ Equity

$161,000

$206,600

Statements of Cash Flows for the Year Ended December 31

Cash Flows From Operating Activities:

Inflow from Customers

$85,000

$ 72,000

Cash Flows From Investing Activities:

Outflow to Purchase Equipment

(110,000)

-0-

Cash Flows From Financing Activities:

Inflow from Stock Issue

120,000

-0-

Net Change in Cash

95,000

72,000

Plus: Beginning Cash Balance

-0-

95,000

Ending Cash Balance

$95,000

$167,000

EXERCISE 8-9B

a. Calculation of Depreciation:

Van Cost $35,000

Sales Tax & Title Fees 1,500

Total Cost $36,500

EXERCISE 8–10B

a.

1. Straight-Line Calculation:

2. Double-Declining Balance Calculation:

(Cost − Accumulated Depreciation) x (2 x Straight-Line Rate)

Straight-Line Rate = 1 5 = .20

Year 1 ($75,000 − $0) x (2 x .20) = $30,000

Year 2 ($75,000 − $30,000) x (2 x .20) = 18,000

8-70

8-71

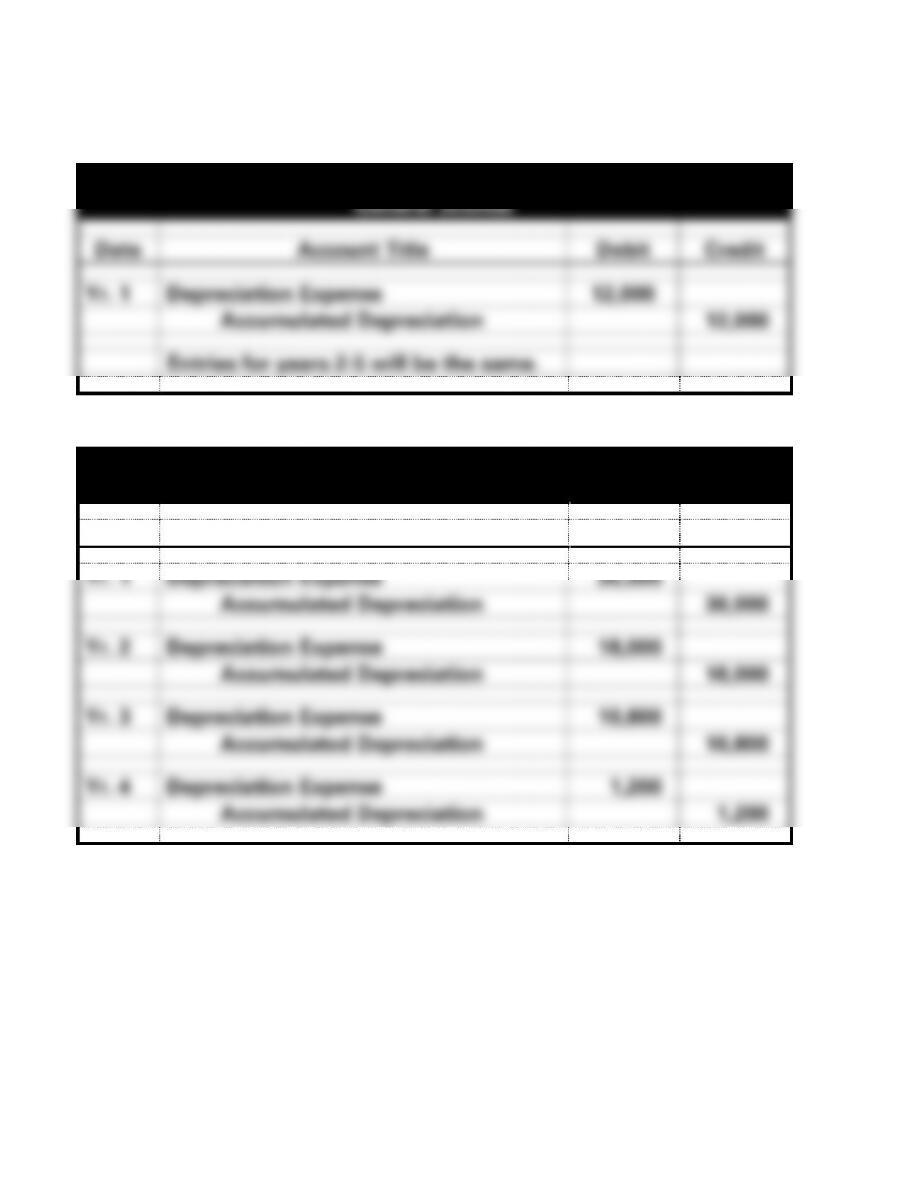

EXERCISE 8-10B (cont.)

c. 1.

Hill Manufacturing

General Journal

Date

Account Title

Debit

Credit

Yr. 1

Depreciation Expense

12,000

Accumulated Depreciation

12,000

Entries for years 2-5 will be the same.

c. 2.

Hill Manufacturing

General Journal

Date

Account Title

Debit

Credit

Yr. 1

Depreciation Expense

30,000

Accumulated Depreciation

30,000

Yr. 2

Depreciation Expense

18,000

Accumulated Depreciation

18,000

Yr. 3

Depreciation Expense

10,800

Accumulated Depreciation

10,800

Yr. 4

Depreciation Expense

1,200

Accumulated Depreciation

1,200

8-72

EXERCISE 8-11B

a. Historical Cost $50,000

Less: Accumulated Depreciation (41,000)

Book Value $ 9,000

8-73

EXERCISE 8-12B

Heflin Enterprises

2017 Accounting Equation

Assets

=

Stockholders’ Equity

Event

Cash

Land

=

Common

Stock

+

Retained

Earnings

a.1

+22,500

(20,000)

=

2,500

b.1

+18,500

(20,000)

=

(1,500)

a. 1) See above.

(2) Gain of $2,500 ($22,500 sales price − $20,000 cost).

(3) Cash inflow from investing activities, $22,500.

(2) Loss of $1,500 ($18,500 sales price − $20,000 cost).

(3) Cash inflow from investing activities, $18,500.

8-74

EXERCISE 8-13B

a. Double-Declining Balance

(Cost − Accum. Depr.) x (2 x SL Rate) = Depr. Exp. Per Year

SL Rate = 1 5 = .20

2016: ($47,000 − $0) x (2 x .20) = $18,800

8-75

EXERCISE 8-13B (cont.)

c. Calculation of Book Value

Double-Declining Balance

Cost $47,000

8-76

EXERCISE 8–14B

a. MACRS depreciation = Cost x MACRS Table %

8-77

EXERCISE 8-15B

Depreciation

Expense

2016: $72,500 − $12,500 = $60,000; $60,000 3 = $20,000

8-78

EXERCISE 8-16B

Shredding Machine:

Book value would still be $6,000; the $1,900 repair cost will be

expensed.

8-79

EXERCISE 8–17B

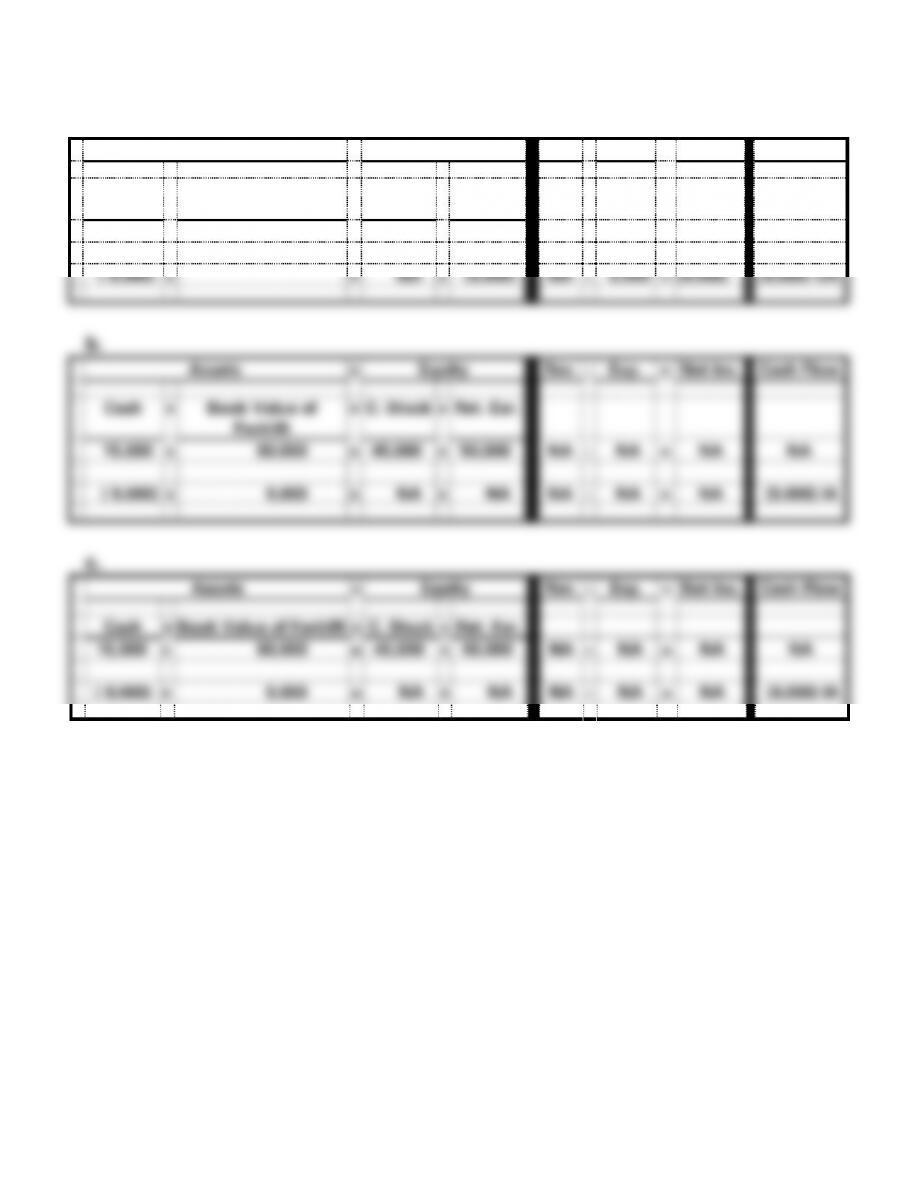

a.

Assets

=

Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

Cash

+

Book Value of

Forklift

=

C. Stock

+

Ret. Ear.

15,000

+

80,000

=

45,000

+

50,000

NA

−

NA

=

NA

NA

( 9,000)

+

=

NA

+

(9,000)

NA

−

9,000

=

(9,000)

(9,000) OA

Assets

=

Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

Cash

+

Book Value of

Forklift

=

C. Stock

+

Ret. Ear.

15,000

+

80,000

=

45,000

+

50,000

NA

−

NA

=

NA

NA

( 9,000)

+

9,000

=

NA

+

NA

NA

−

NA

=

NA

(9,000) IA

Assets

=

Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

Cash

+

Book Value of Forklift

=

C. Stock

+

Ret. Ear.

15,000

+

80,000

=

45,000

+

50,000

NA

−

NA

=

NA

NA

( 9,000)

+

9,000

=

NA

+

NA

NA

−

NA

=

NA

(9,000) IA

8-80

EXERCISE 8-18B

2017.

b. $22,000 of expense would be recognized in 2016 and $-0- in 2017.

c. $-0- cash outflow from operating activities in 2016, $-0- cash outflow

2017.

EXERCISE 8-19B

a. Depletion charge per unit: $800,000 1,200,000 cubic yds = $.67* per

cubic yd.

*rounded

b.

Depletion Calculation:

Year 1 $.67 x 650,000 = $435,500

8-82

EXERCISE 8-20B

a. Patent $48,000 5 = $9,600 per year

The goodwill is not amortized.

b.

Garth Manufacturing

Statements Model

Assets

=

Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

Cash

+

Patent

+

Goodwill

=

94,000

+

NA

+

NA

=

94,000

NA

−

NA

=

NA

NA

Acq.

(83,000)

+

48,000

+

35,000

=

NA

NA

−

NA

=

NA

(83,000) IA

Pat.

NA

+

(9,600)

+

NA

=

(9,600)

NA

−

9,600

=

(9,600)

NA

c.

Account Titles

Debit

Credit

Patents

48,000

Goodwill

35,000

Cash

83,000

Account Titles

Debit

Credit

Amortization Expense – Patents

9,600

Patents

9,600

EXERCISE 8-21B

a. Acquisition Price:

Cash Paid $275,000

Liabilities Assumed 10,000

8-84