SOLUTIONS TO EXERCISES – SERIES A – CHAPTER 10

EXERCISE 10-1A

a. Year 1

Option 1 – annual interest only:

$150,000 x 8% = $12,000

Option 2 – annual interest and $15,000 on principal:

EXERCISE 10-2A

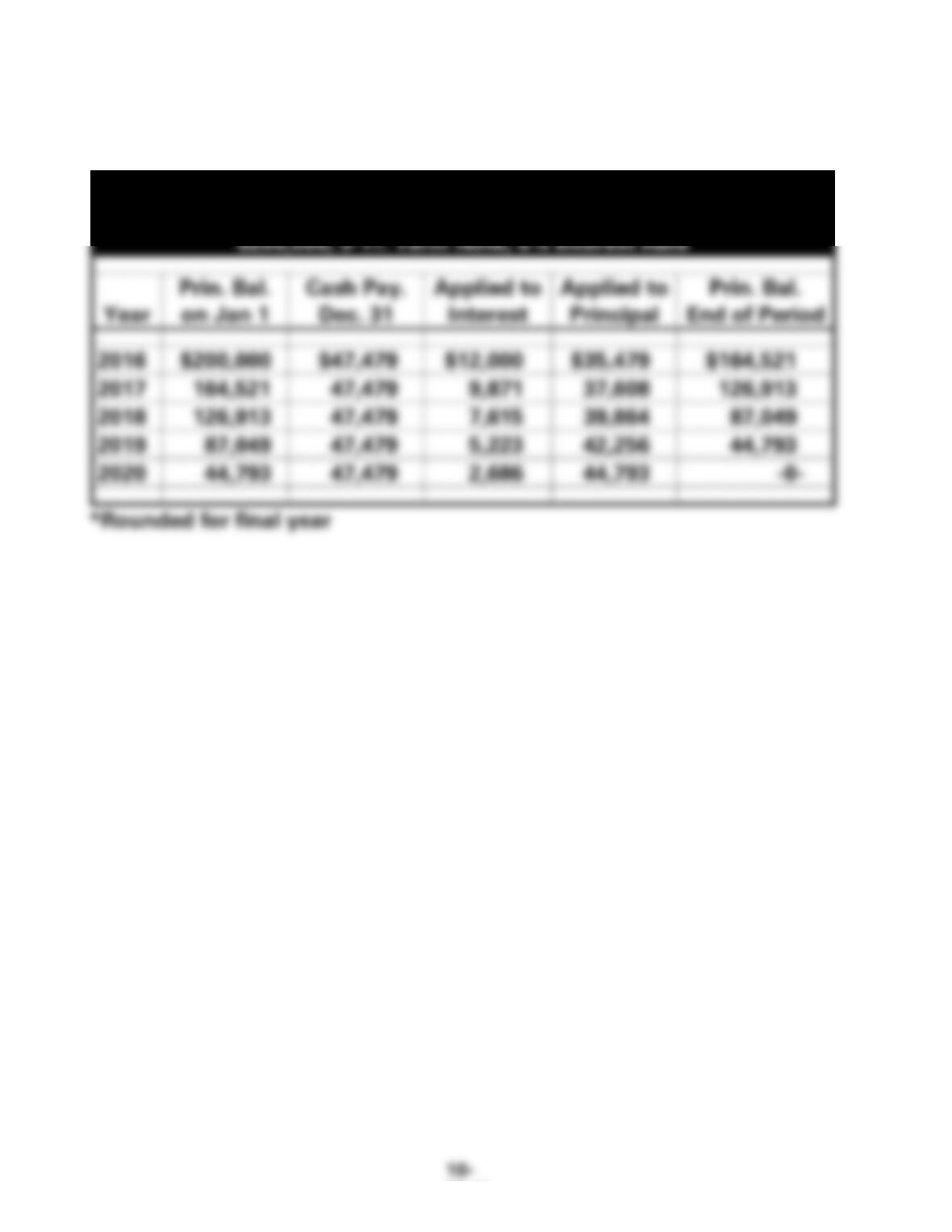

Beatie Co.

Amortization Schedule

$200,000, 5-Yr. Term Note, 6% Interest Rate

Year

Prin. Bal.

on Jan 1

Cash Pay.

Dec. 31

Applied to

Interest

Applied to

Principal

Prin. Bal.

End of Period

2016

$200,000

$47,479

$12,000

$35,479

$164,521

2017

164,521

47,479

9,871

37,608

126,913

2018

126,913

47,479

7,615

39,864

87,049

2019

87,049

47,479

5,223

42,256

44,793

2020

44,793

47,479

2,686

44,793

-0-

*Rounded for final year

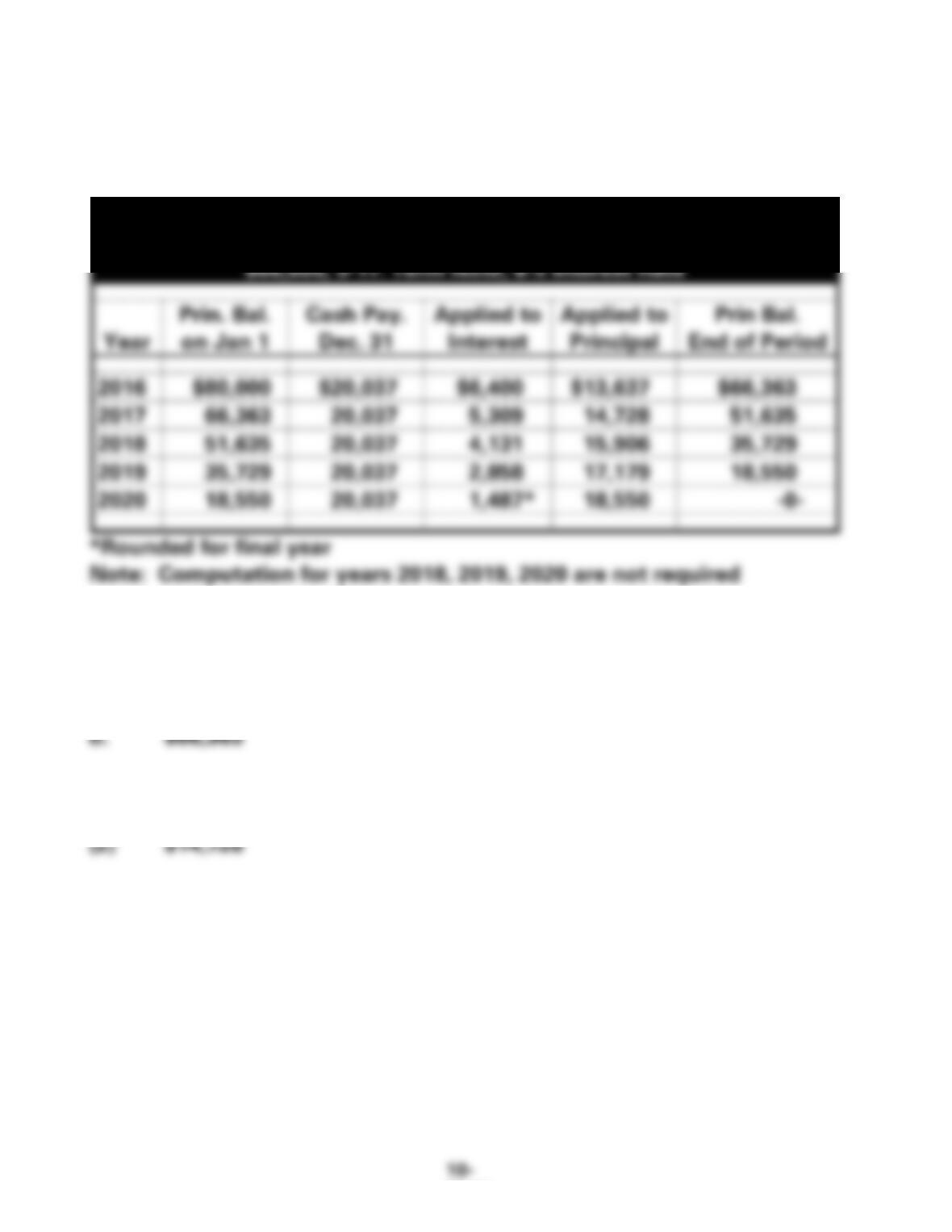

EXERCISE 10-3A

Provided for the use of the Instructor:

Dayle Company

Amortization Schedule

$80,000, 5-Yr. Term Note, 8% Interest Rate

Year

Prin. Bal.

on Jan 1

Cash Pay.

Dec. 31

Applied to

Interest

Applied to

Principal

Prin Bal.

End of Period

2016

$80,000

$20,037

$6,400

$13,637

$66,363

2017

66,363

20,037

5,309

14,728

51,635

2018

51,635

20,037

4,131

15,906

35,729

2019

35,729

20,037

2,858

17,179

18,550

2020

18,550

20,037

1,487*

18,550

-0-

*Rounded for final year

Note: Computation for years 2018, 2019, 2020 are not required

a.

(1) $6,400

(2) $13,637

c.

(1) $5,309

EXERCISE 10-4A

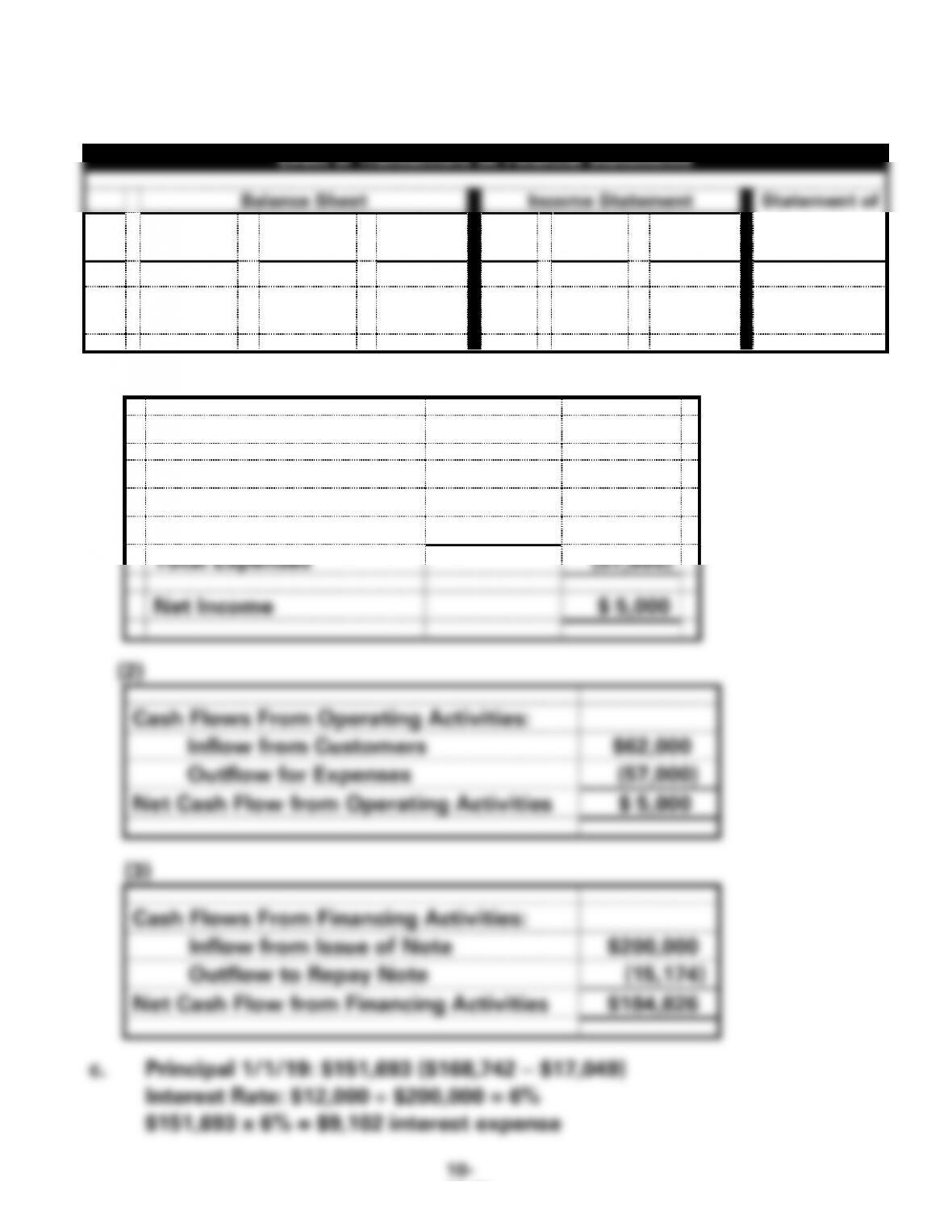

a.

Effect of Transactions on Financial Statements

Balance Sheet

Income Statement

Statement of

No

.

Assets

=

Liab.

+

S.

Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

1.

200,000

=

200,000

+

NA

NA

−

NA

=

NA

200,000FA

2.

(27,174)

=

(15,174)

+

(12,000)

NA

−

12,000

=

(12,000)

(15,174)FA

(12,000)OA

b. (1)

Revenue

$62,000

Expenses

Operating Expenses

$45,000

Interest Expense

12,000

Total Expenses

(57,000)

Net Income

$ 5,000

Cash Flows From Operating Activities:

Inflow from Customers

$62,000

Outflow for Expenses

(57,000)

Net Cash Flow from Operating Activities

$ 5,000

Cash Flows From Financing Activities:

Inflow from Issue of Note

$200,000

Outflow to Repay Note

(15,174)

Net Cash Flow from Financing Activities

$184,826

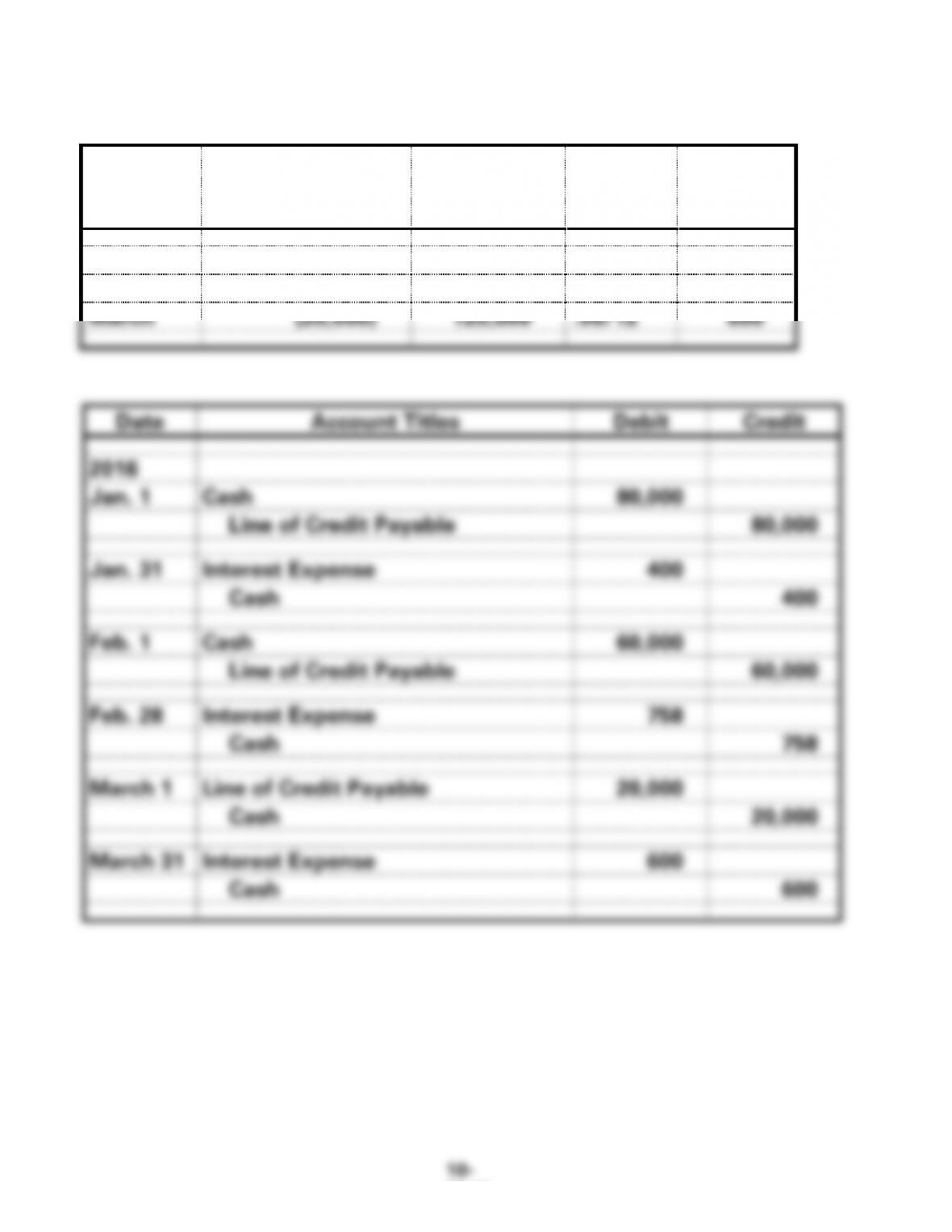

EXERCISE 10–5A

Month

Amount

Borrowed

(Repaid)

Balance End

of Month

Interest

Rate

Interest

Expense

January

$80,000

$80,000

.06/12

$400

February

60,000

140,000

.065/12

758

March

(20,000)

120,000

.06/12

600

EXERCISE 10-6A

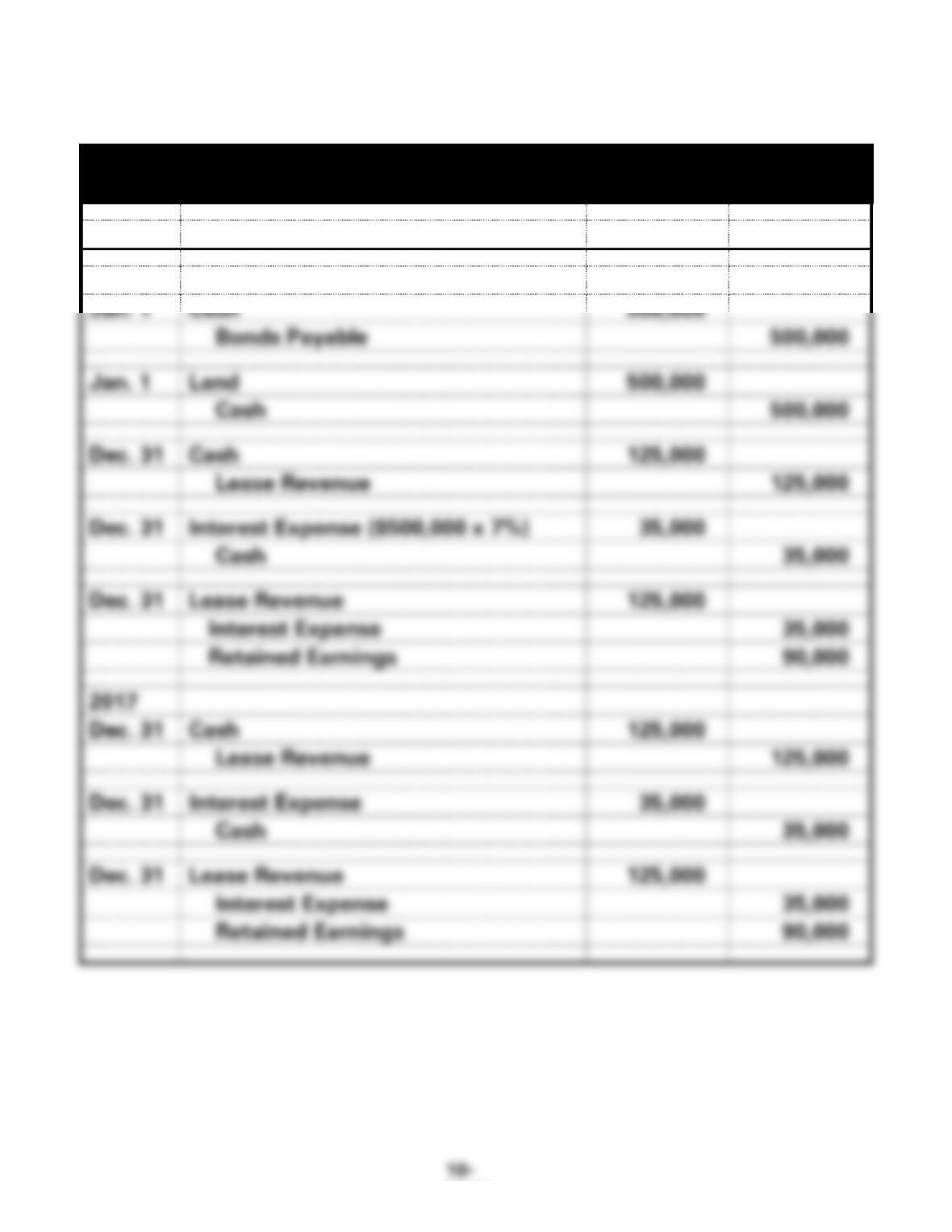

a.

Doyle Company

General Journal

Date

Account Titles

Debit

Credit

2016

Jan. 1

Cash

500,000

Bonds Payable

500,000

Jan. 1

Land

500,000

Cash

500,000

Dec. 31

Cash

125,000

Lease Revenue

125,000

Dec. 31

Interest Expense ($500,000 x 7%)

35,000

Cash

35,000

Dec. 31

Lease Revenue

125,000

Interest Expense

35,000

Retained Earnings

90,000

2017

Dec. 31

Cash

125,000

Lease Revenue

125,000

Dec. 31

Interest Expense

35,000

Cash

35,000

Dec. 31

Lease Revenue

125,000

Interest Expense

35,000

Retained Earnings

90,000

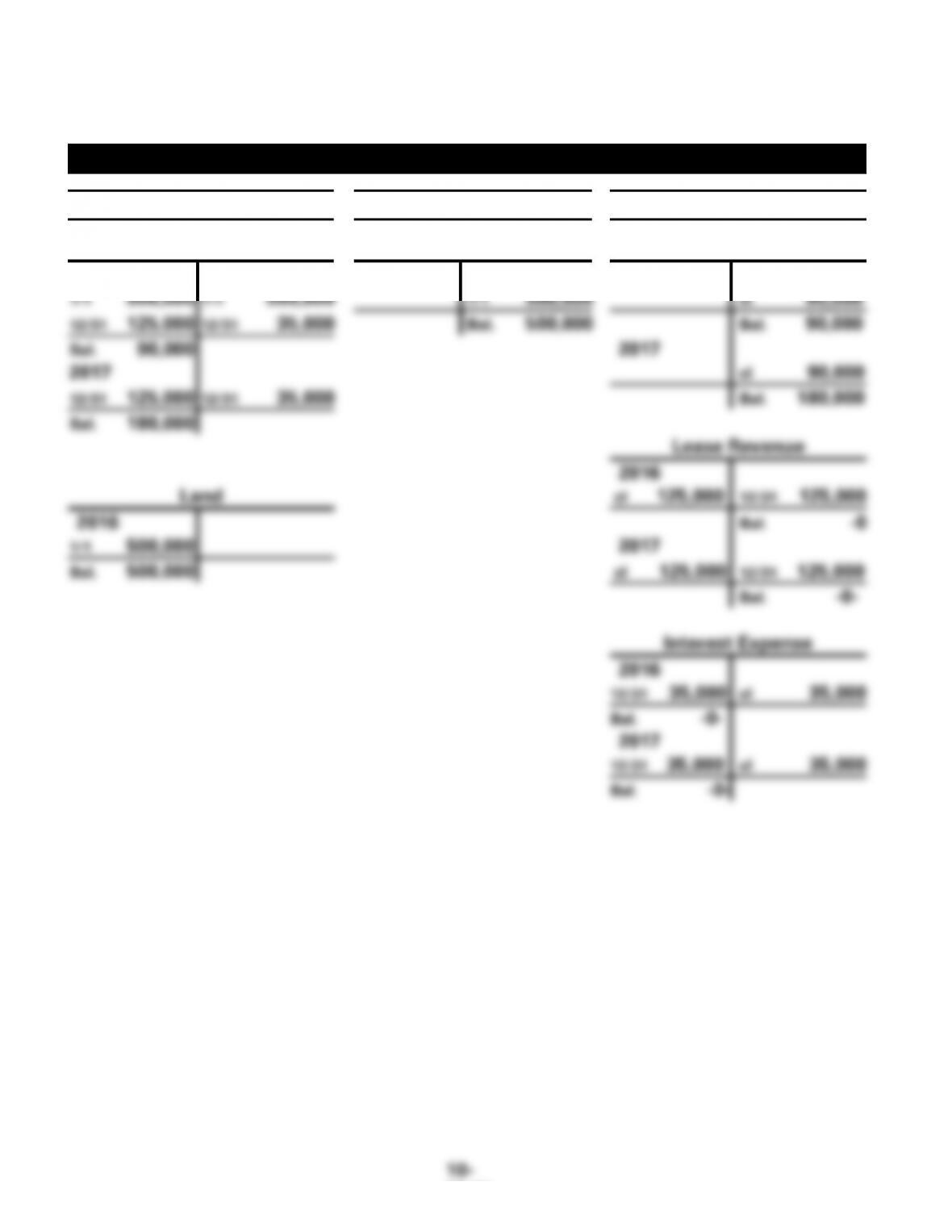

EXERCISE 10-6A a. (cont.)

Doyle Company

Assets

=

Liabilities

+

Stockholders’ Equity

Cash

Bonds Payable

Retained Earnings

2016

2016

2016

1/1 500,000

1/1 500,000

1/1 500,000

cl 90,000

12/31 125,000

12/31 35,000

Bal. 500,000

Bal. 90,000

Bal. 90,000

2017

2017

cl 90,000

12/31 125,000

12/31 35,000

Bal. 180,000

Bal. 180,000

Lease Revenue

2016

Land

cl 125,000

12/31 125,000

2016

Bal. -0

1/1 500,000

2017

Bal. 500,000

cl 125,000

12/31 125,000

Bal. -0-

Interest Expense

2016

12/31 35,000

cl 35,000

Bal. -0-

2017

12/31 35,000

cl 35,000

Bal. -0-

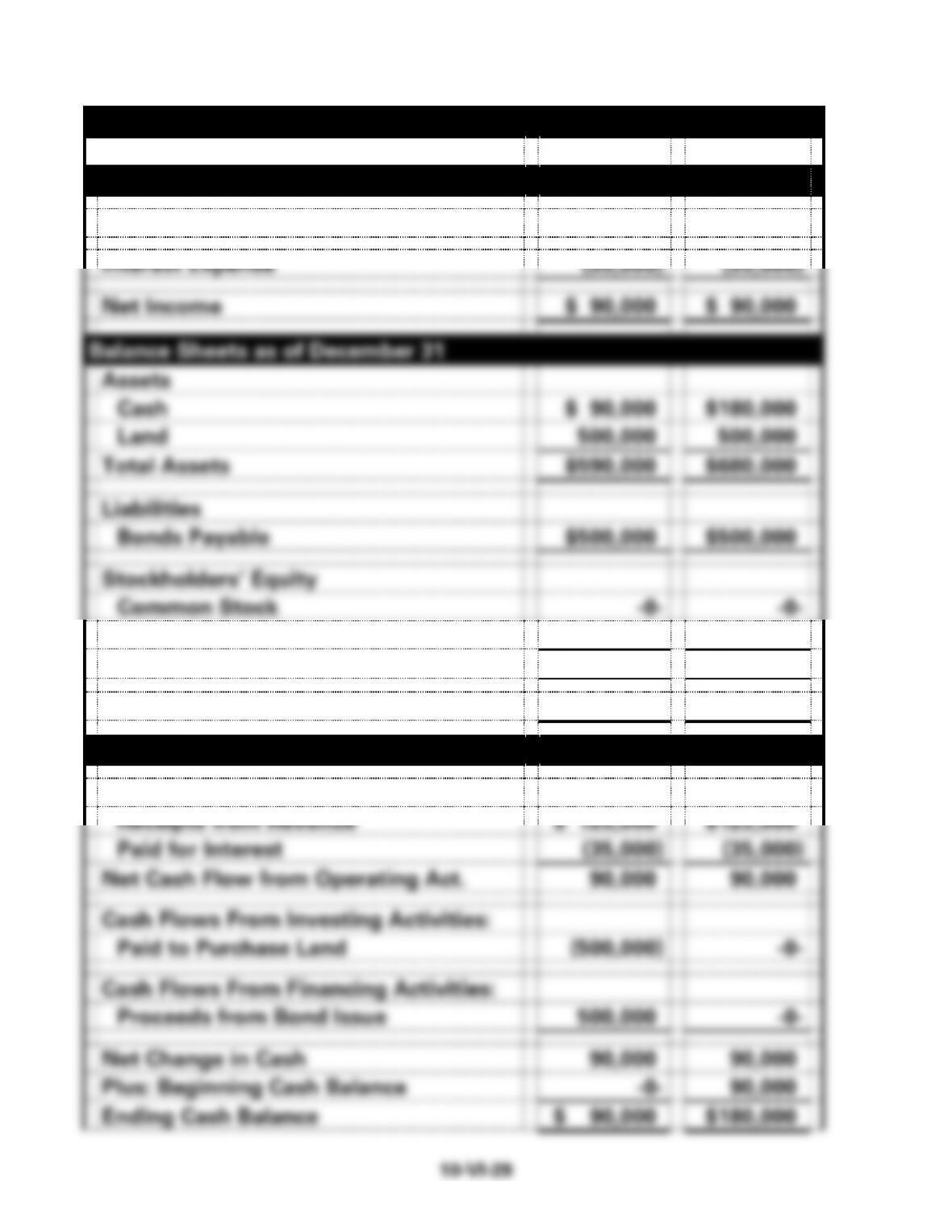

EXERCISE 10-6A b. (cont.)

Doyle Company

Financial Statements

2016

2017

Income Statements for the Year Ended Decebmer 31

Lease Revenue

$125,000

$125,000

Interest Expense

(35,000)

(35,000)

Net Income

$ 90,000

$ 90,000

Balance Sheets as of December 31

Assets

Cash

$ 90,000

$180,000

Land

500,000

500,000

Total Assets

$590,000

$680,000

Liabilities

Bonds Payable

$500,000

$500,000

Stockholders’ Equity

Common Stock

-0-

-0-

Retained Earnings

90,000

180,000

Total Stockholders’ Equity

90,000

180,000

Total Liab. and Stockholders’ Equity

$590,000

$680,000

Statements of Cash Flows for the Year Ended December 31

Cash Flows From Operating Activities:

Receipts from Revenue

$ 125,000

$125,000

Paid for Interest

(35,000)

(35,000)

Net Cash Flow from Operating Act.

90,000

90,000

Cash Flows From Investing Activities:

Paid to Purchase Land

(500,000)

-0-

Cash Flows From Financing Activities:

Proceeds from Bond Issue

500,000

-0-

Net Change in Cash

90,000

90,000

Plus: Beginning Cash Balance

-0-

90,000

Ending Cash Balance

$ 90,000

$180,000

10–VI–30

EXERCISE 10-7A

Bell Corp.

General Journal

Date

Account Titles

Debit

Credit

2016

Jan.1

Cash

180,000

Bonds Payable

180,000

Dec. 31

Interest Expense*

10,800

Cash

10,800

2017

Dec. 31

Interest Expense

10,800

Cash

10,800

*$180,000 x 6% = $10,800 interest expense per year

EXERCISE 10-8A

Nivan Co.

Date

Account Titles

Debit

Credit

2016

Jan. 1

Cash

500,000

Bonds Payable

500,000

2020

Dec. 31

Loss on Bond Redemption*

15,000

Bonds Payable

500,000

Cash

515,000

EXERCISE 10–9A

The total amount of interest paid each year will be the same regardless of

whether it is paid annually or semiannually. If the interest is paid

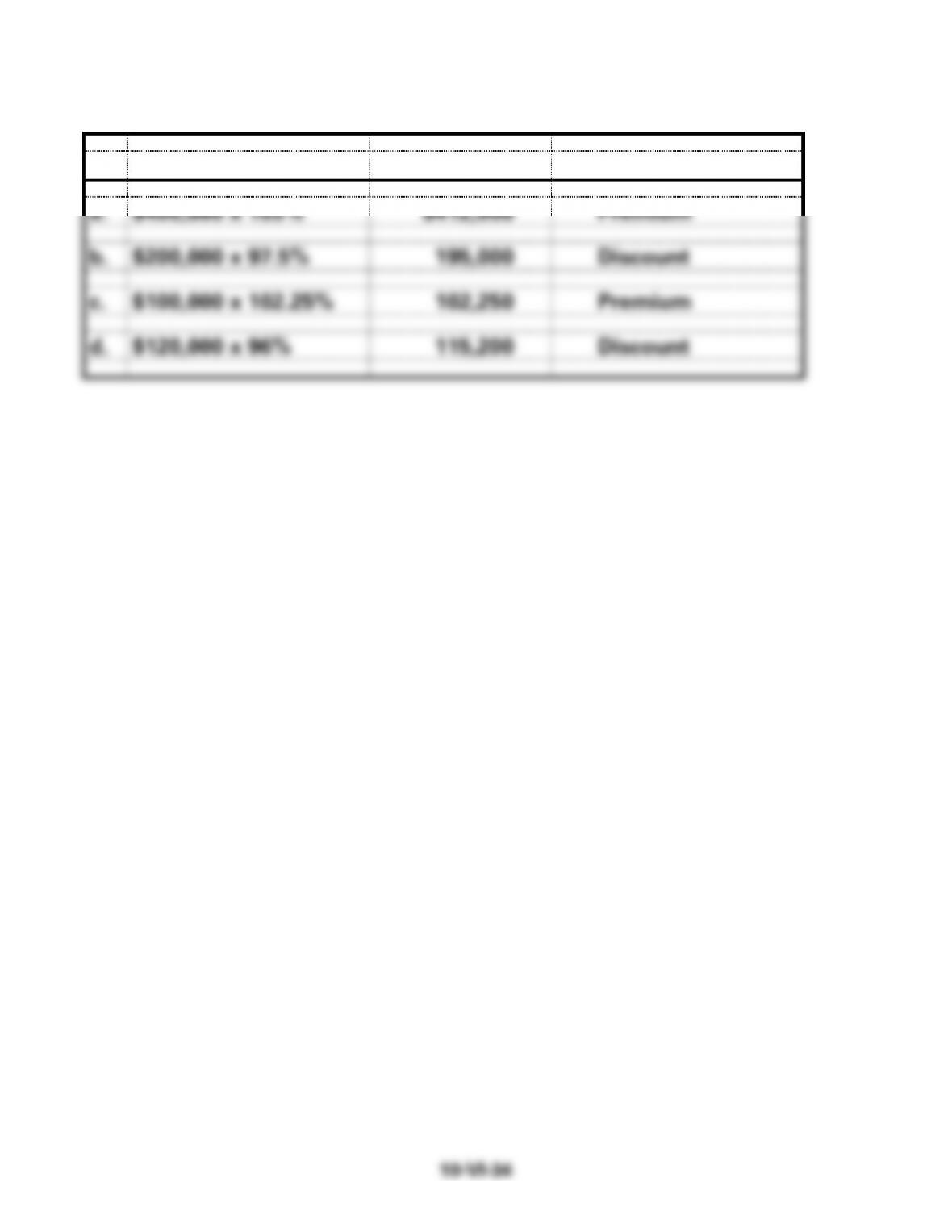

EXERCISE 10-10A

Face x Selling Price

Cash Proceeds

Discount or Premium

a.

$400,000 x 103%

$412,000

Premium

b.

$200,000 x 97.5%

195,000

Discount

c.

$100,000 x 102.25%

102,250

Premium

d.

$120,000 x 96%

115,200

Discount

EXERCISE 10-11A

a. Premium

b. Face

EXERCISE 10-12A

EXERCISE 10-13A

a. $80,000 x 1.25% = $1,000; Premium

EXERCISE 10-14A

a.

Effect of Transactions on Financial Statements

Balance Sheet

Income Statement

No

.

Assets

=

Liab.

+

S. Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

1.

+

+

NA

NA

NA

NA

+ FA

2.

−

+

−

NA

+

−

− OA

b. Discount: $180,000 x 2% = $3,600

Amortization of bond discount: $3,600 5 = $720 per year

Carrying Value, December 31, 2016:

Bonds Payable $180,000

Less: Discount on Bonds Payable (2,880)*

EXERCISE 10-15A

a.

Square Foot Grill, Inc.

General Journal

Date

Account Titles

Debit

Credit

2016

July 1

Cash1

204,000

Premium on Bonds Payable

4,000

Bonds Payable

200,000

Dec. 31

Interest Expense

5,800

Premium on Bonds Payable2

200

Cash3

6,000

Dec. 31

Retained Earnings

5,800

Interest Expense

5,800

2017

June 30

Interest Expense

5,800

Premium on Bonds Payable

200

Cash

6,000

Dec. 31

Interest Expense

5,800

Premium on Bonds Payable

200

Cash

6,000

Dec. 31

Retained Earnings

11,600

Interest Expense

11,600

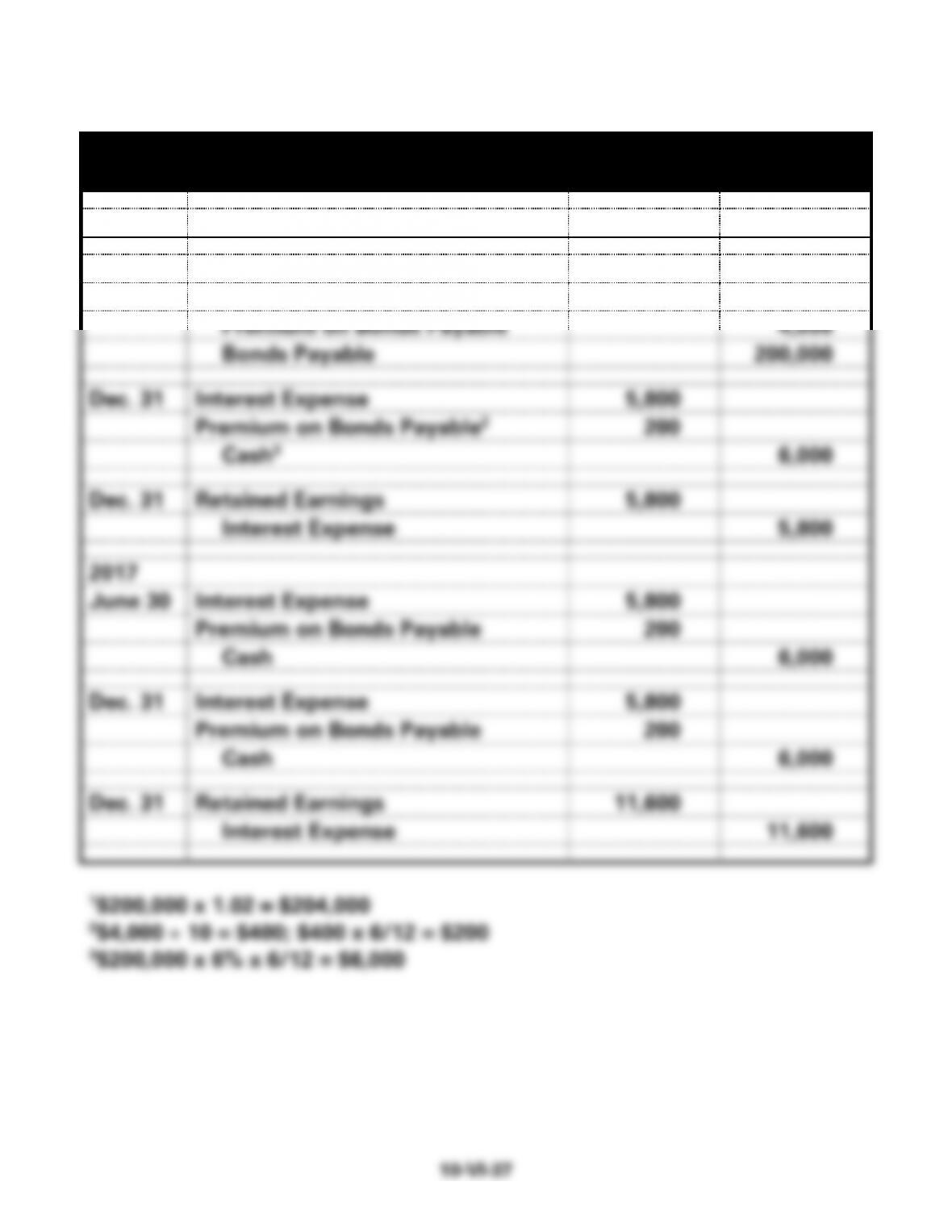

EXERCISE 10-15A a.(cont.)

Square Foot Grill, Inc.

T-accounts

Assets

=

Liabilities

+

Stockholders’ Equity

Cash

Bonds Payable

Retained Earnings

2016

2016

2016

7/1 204,000

12/31 6,000

7/1 200,000

cl 5,800

Bal. 198,000

Bal. 200,000

Bal. 5,800

2017

2017

6/30 6,000

cl 11,600

12/31 6,000

Premium on Bonds Pay.

Bal. 17,400

Bal. 186,000

2016

12/31 200

7/1 4,000

Interest Expense

Bal. 3,800

2016

2017

12/31 5,800

cl 5,800

6/30 200

Bal. -0-

12/31 200

2017

Bal. 3,400

6/30 5,800

12/31 5,800

cl 11,600

Bal. -0-

10–VI–38

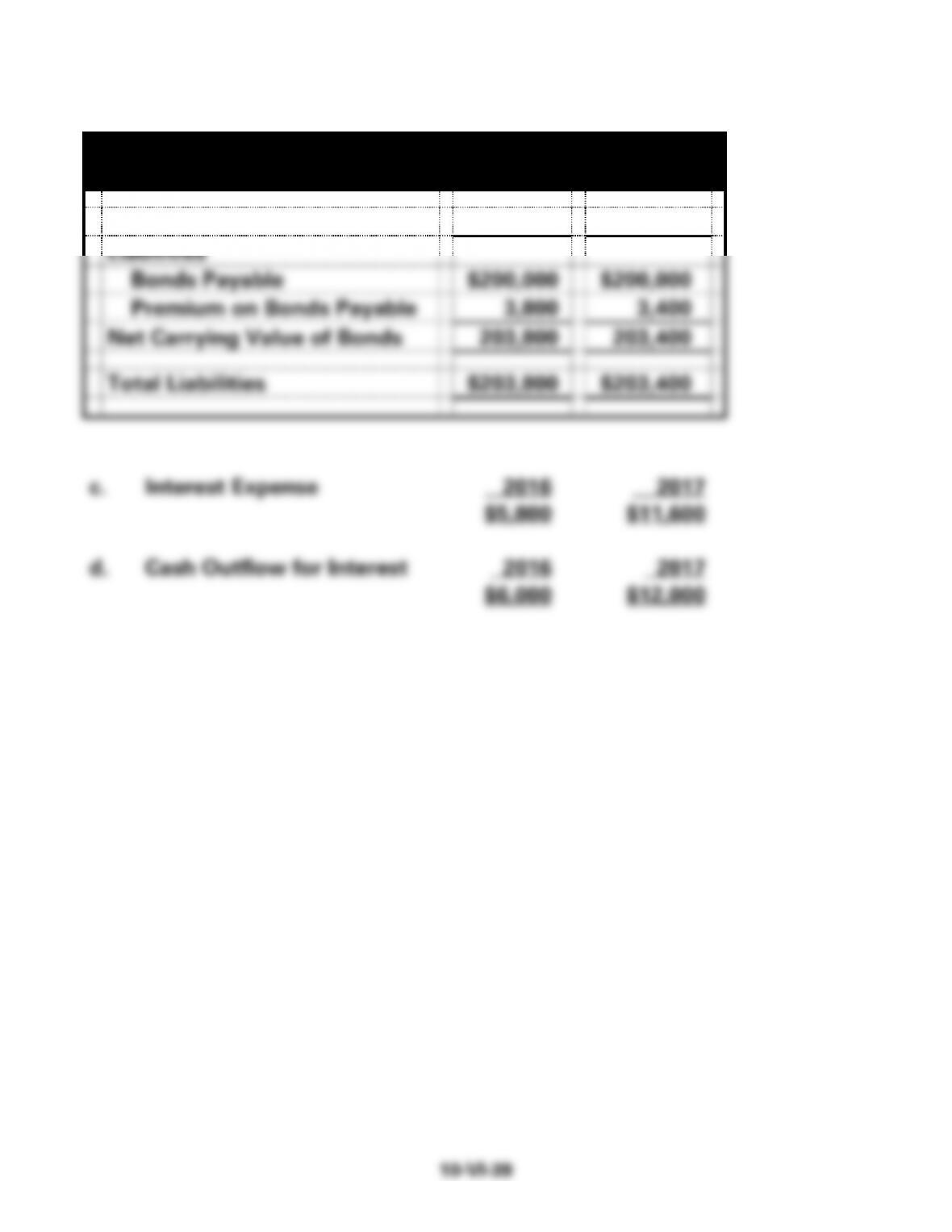

EXERCISE 10-15A (cont.)

b.

Square Foot Grill, Inc.

Balance Sheet As of December 31

2016

2017

Liabilities

Bonds Payable

$200,000

$200,000

Premium on Bonds Payable

3,800

3,400

Net Carrying Value of Bonds

203,800

203,400

Total Liabilities

$203,800

$203,400

EXERCISE 10-16A

Price Co.

General Journal

Date

Account Titles

Debit

Credit

2016

Jan. 1

Cash1

183,350

Discount on Bonds Payable

6,650

Bonds Payable

190,000

Dec. 31

Interest Expense

12,370

Discount on Bonds Payable2

1,330

Cash3

11,400

2017

Dec. 31

Interest Expense

12,730

Discount on Bonds Payable

1,330

Cash

11,400

EXERCISE 10-17A

a.

Effect of Transactions on Financial Statements

Balance Sheet

Income Statement

Statement of

No

.

Assets

=

Liab.

+

S. Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

1.

+

+

NA

NA

NA

NA

+ FA

2a.

NA

−

+

NA

−

+

NA

2b.

−

NA

−

NA

+

−

− OA

b. Premium: $150,000 x 3% = $4,500

Amortization of bond premium: $4,500 5 = $900 per year

Carrying Value, December 31, 2016:

Bonds Payable $150,000