Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

9-150

PROBLEM 9-25B (cont.)

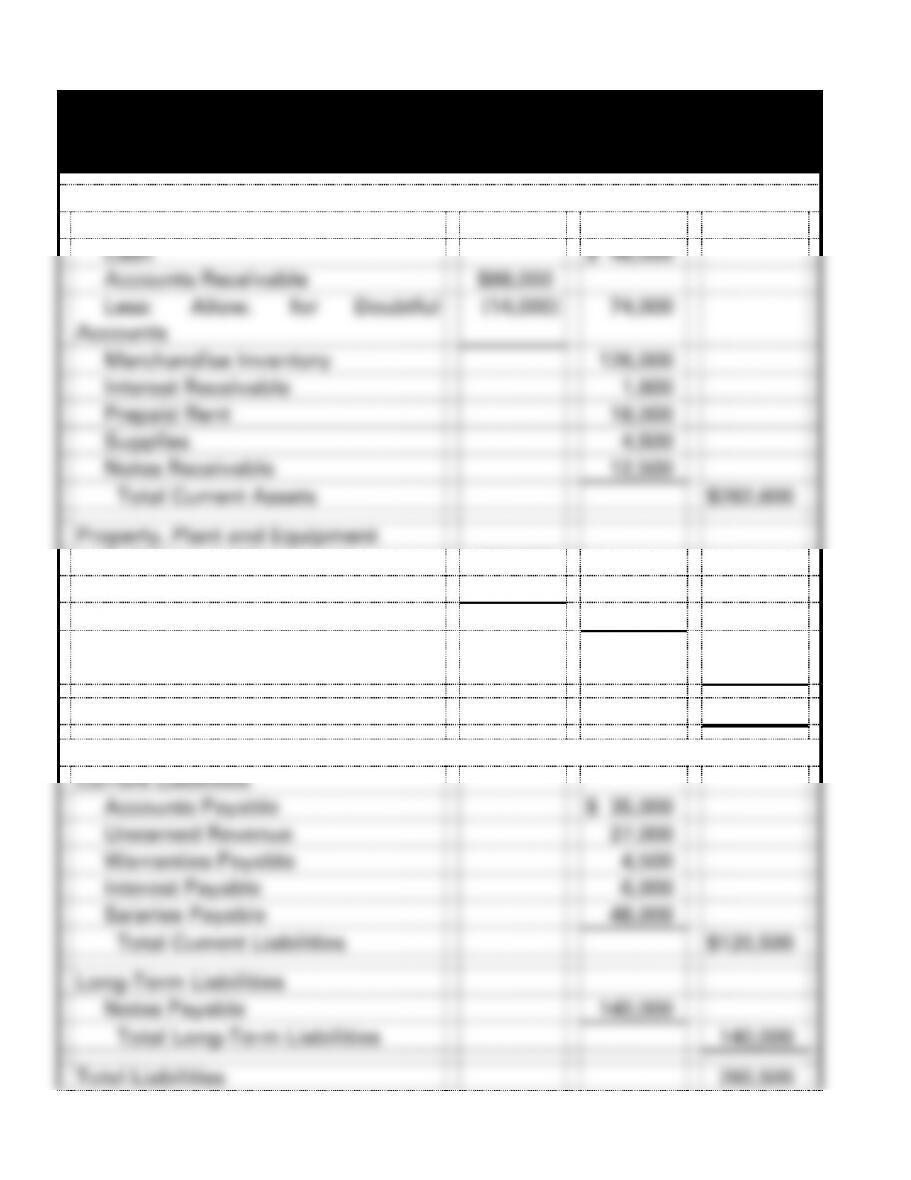

Brown Company

Balance Sheet

As of December 31, 2016

Assets

Current Assets

Cash

$ 46,000

Accounts Receivable

$88,000

Less: Allow. for Doubtful

Accounts

(14,000)

74,000

Merchandise Inventory

126,000

Interest Receivable

1,600

Prepaid Rent

18,000

Supplies

4,500

Notes Receivable

12,500

Total Current Assets

$282,600

Property, Plant and Equipment

Buildings and Equipment

206,000

Less: Accumulated Depreciation

(46,000)

160,000

Land

75,000

Total Property, Plant and

Equipment

235,000

Total Assets

$517,600

Liabilities and Stockholders’ Equity

Current Liabilities

Accounts Payable

$ 35,000

Unearned Revenue

27,000

Warranties Payable

4,500

Interest Payable

6,000

Salaries Payable

48,000

Total Current Liabilities

$120,500

Long-Term Liabilities

Notes Payable

140,000

Total Long-Term Liabilities

140,000

Total Liabilities

260,500

9-151

Stockholders’ Equity

Common Stock

90,000

Retained Earnings*

167,100

Total Stockholders’ Equity

257,100

Total Liabilities and Stockholders’

Equity

$517,600

9-152

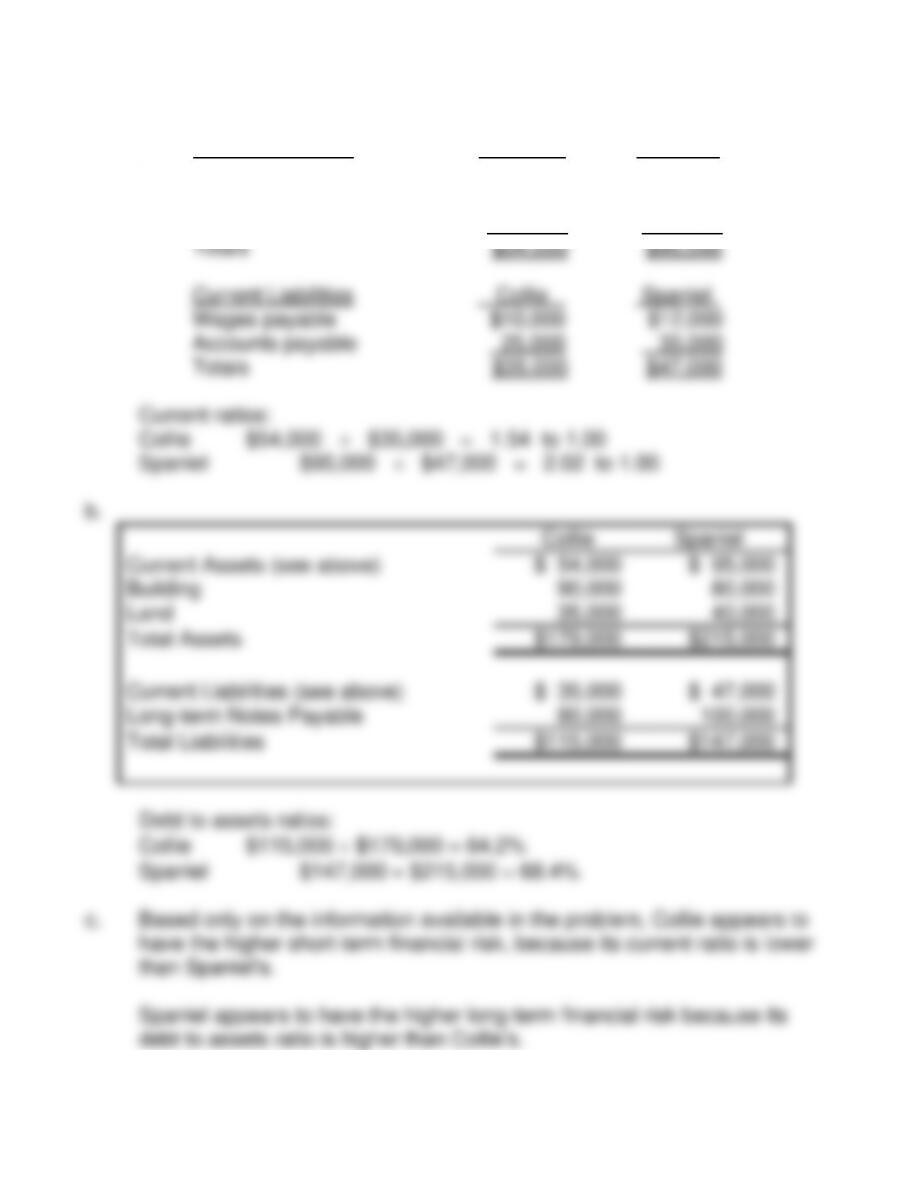

PROBLEM 9-26B

a. Current Assets Collie Spaniel

Cash $12,000 $15,000

Merchandise inventory 20,000 55,000

Accounts receivable 22,000 25,000

9-153

PROBLEM 9-27B

a.

Ball Company

Effect of Transactions on Financial Statements

No.

Assets

=

Liab.

+

Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

2016

1.

+

+

NA

NA

NA

NA

+ FA

2.

+

NA

+

+

NA

+

+ OA

3.

−

NA

−

NA

+

−

− OA

4.

NA

+

−

NA

+

−

NA

2017

1.

+

NA

+

+

NA

+

+ OA

2.

−

NA

−

NA

+

−

− OA

3a.

NA

+

−

NA

+

−

NA

3b.

−

−

NA

NA

NA

NA

−

OA,FA

9-154

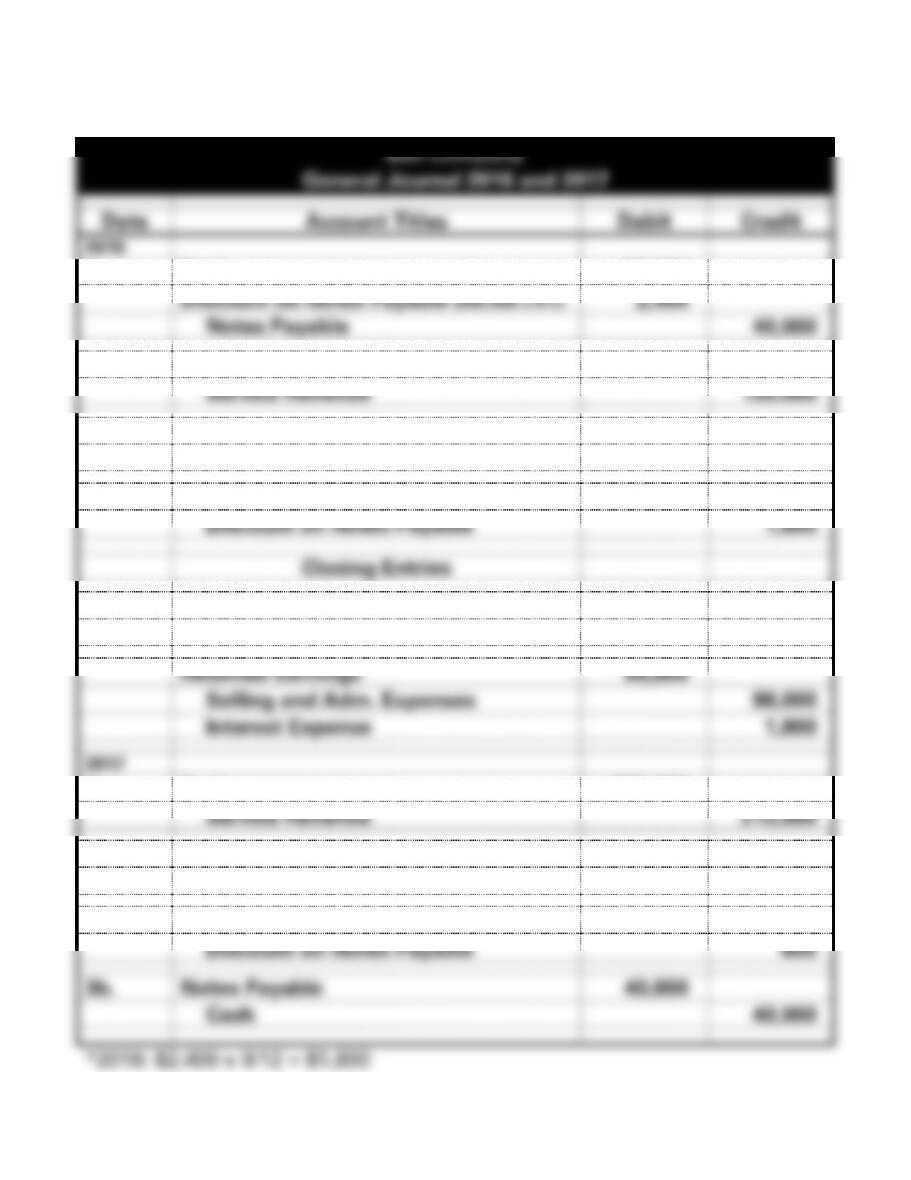

PROBLEM 9-27B (cont.) (Appendix)

b.

Ball Company

General Journal 2016 and 2017

Date

Account Titles

Debit

Credit

2016

1.

Cash

37,600

Discount on Notes Payable ($40,000 x 6%)

2,400

Notes Payable

40,000

2.

Cash

130,000

Service Revenue

130,000

3.

Selling and Adm. Expenses

98,000

Cash

98,000

4.

Interest Expense*

1,800

Discount on Notes Payable

1,800

Closing Entries

5. cl

Service Revenue

130,000

Retained Earnings

130,000

Retained Earnings

99,800

Selling and Adm. Expenses

98,000

Interest Expense

1,800

2017

1.

Cash

215,000

Service Revenue

215,000

2.

Selling and Adm. Expenses

151,000

Cash

151,000

3a.

Interest Expense*

600

Discount on Notes Payable

600

3b.

Notes Payable

40,000

Cash

40,000

*2016: $2,400 x 9/12 = $1,800

9-155

9-156

PROBLEM 9-27B b. (cont.) (Appendix)

Ball Company

General Journal, 2016 and 2017

2017

Closing Entries

4. cl

Service Revenue

215,000

Retained Earnings

215,000

Retained Earnings

151,600

Selling and Adm. Expenses

151,000

Interest Expense

600

9-157

PROBLEM 9-27B b. (cont.) (Appendix)

Ball Company

T-Accounts

Assets

=

Liabilities

+

Stockholders’ Equity

Cash

Notes Payable

Retained Earnings

2016

2016

2016

1. 37,600

3. 98,000

1. 40,000

cl 99,800

cl 130,000

2. 130,000

Bal. 40,000

Bal. 30,200

Bal. 69,600

2017

2017

2017

3b. 40,000

cl. 151,600

cl 215,000

1. 215,000

2. 151,000

Bal. -0-

Bal. 93,600

3b. 40,000

Bal. 93,600

Discount on Notes Pay.

Service Revenue

2016

2016

1. 2,400

4. 1,800

cl 130,000

2. 130,000

Bal. 600

Bal. -0-

2017

2017

3a. 600

cl 215,000

1. 215,000

Bal. -0-

Bal. -0-

Selling and Adm. Exp.

2016

3. 98,000

cl 98,000

Bal. -0-

2017

2. 151,000

cl 151,000

Bal. -0-

Interest Expense

2016

4. 1,800

cl 1,800

Bal. -0-

2017

3a. 600

cl 600

Bal. -0-

9-158

PROBLEM 9-27B (cont.) (Appendix)

c.

Ball Company

Financial Statements

For the Year Ended December 31

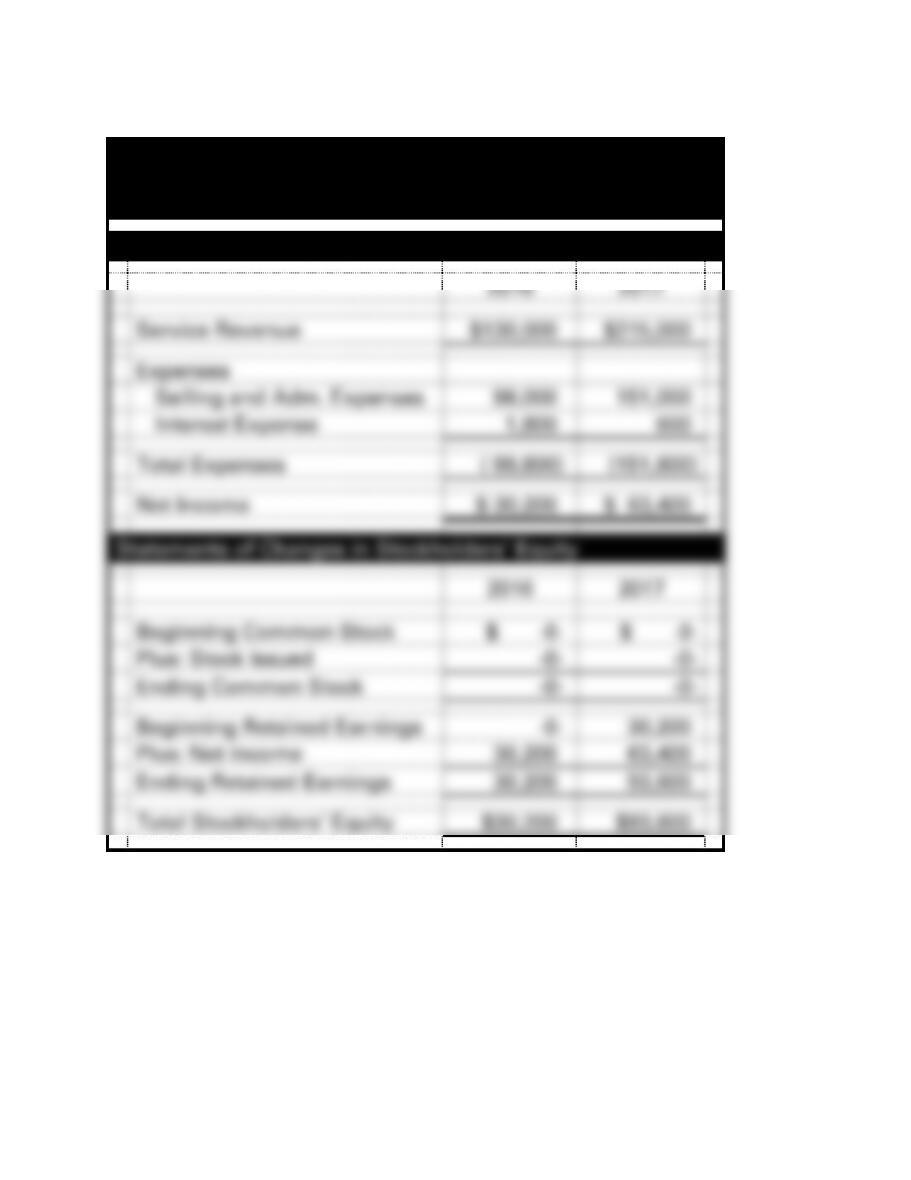

Income Statements

2016

2017

Service Revenue

$130,000

$215,000

Expenses

Selling and Adm. Expenses

98,000

151,000

Interest Expense

1,800

600

Total Expenses

( 99,800)

(151,600)

Net Income

$ 30,200

$ 63,400

Statements of Changes in Stockholders’ Equity

2016

2017

Beginning Common Stock

$ -0-

$ -0-

Plus: Stock Issued

-0-

-0-

Ending Common Stock

-0-

-0-

Beginning Retained Earnings

-0-

30,200

Plus: Net Income

30,200

63,400

Ending Retained Earnings

30,200

93,600

Total Stockholders’ Equity

$30,200

$93,600

9-159

PROBLEM 9-27B c. (cont.) (Appendix)

Ball Company

Financial Statements

Balance Sheets

As of December 31

2016

2017

Assets

Cash

$69,600

$93,600

Total Assets

$69,600

$93,600

Liabilities

Notes Payable

$40,000

$ -0-

Less: Discount on Notes Payable

(600)

-0-

Total Liabilities

39,400

-0-

Stockholders’ Equity

Common Stock

-0-

-0-

Retained Earnings

30,200

93,600

Total Stockholders’ Equity

30,200

93,600

Total Liabilities and Stockholders’ Equity

$69,600

$93,600

9-6

PROBLEM 9-27B c. (cont.) (Appendix)

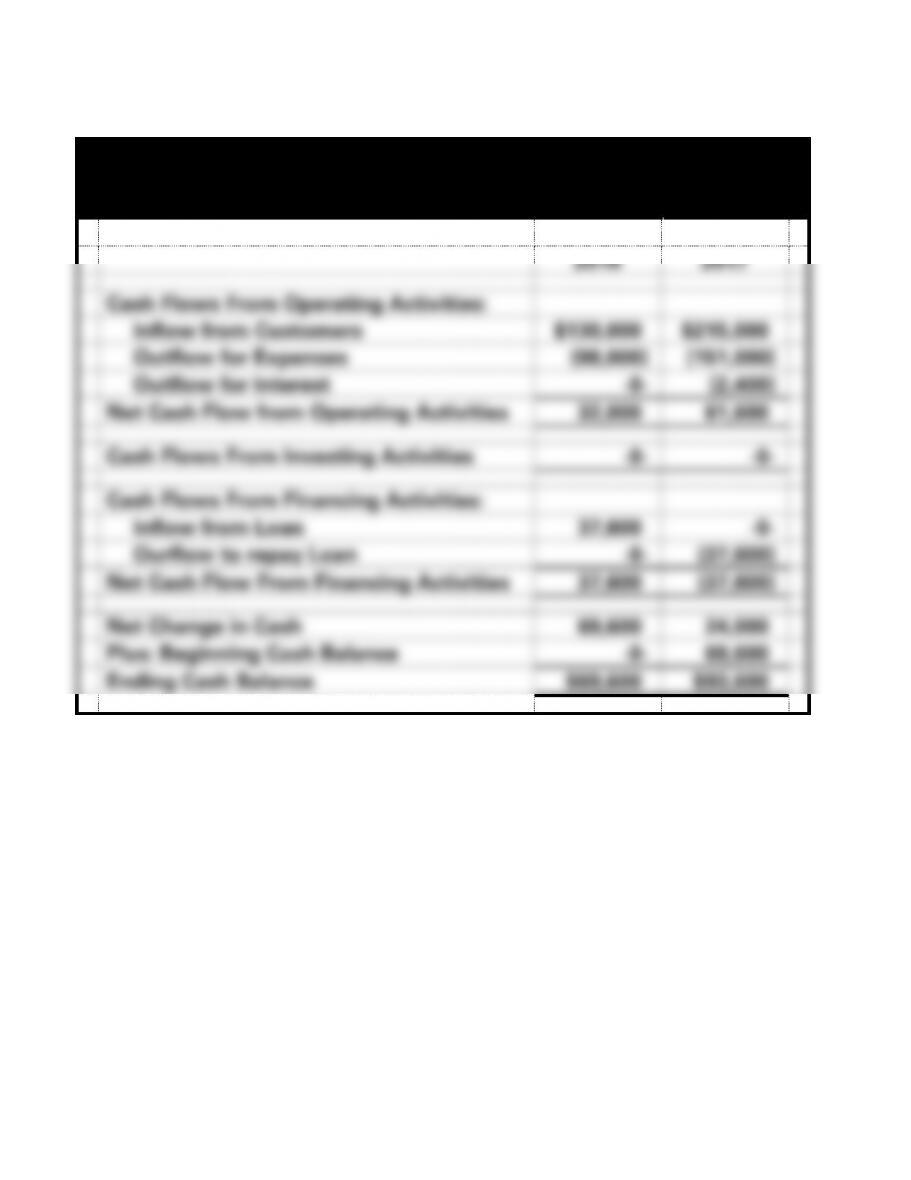

Ball Company

Statements of Cash Flows

For the Year Ended December 31

2016

2017

Cash Flows From Operating Activities:

Inflow from Customers

$130,000

$215,000

Outflow for Expenses

(98,000)

(151,000)

Outflow for Interest

-0-

(2,400)

Net Cash Flow from Operating Activities

32,000

61,600

Cash Flows From Investing Activities

-0-

-0-

Cash Flows From Financing Activities:

Inflow from Loan

37,600

-0-

Ourflow to repay Loan

-0-

(37,600)

Net Cash Flow From Financing Activities

37,600

(37,600)

Net Change in Cash

69,600

24,000

Plus: Beginning Cash Balance

-0-

69,600

Ending Cash Balance

$69,600

$93,600

9-7

ANSWERS TO QUESTIONS – CHAPTER 9

1. A cash payment to creditors is an asset use transaction. This type of

2. Current liabilities are liabilities that are payable within one operating

cycle. A long-term debt is due in more than one year from the date

3. The entry to record accrued interest consists of a debit to Interest

4. The maker of a note is sometimes called the issuer. It is the party

5. The going concern assumption is based upon the premise that since

6. An adjusting entry for accrued but unpaid interest is necessary for

7. Big does not pay any interest in 2016. All interest is paid at the

8. Collection of sales tax is not revenue. The retailer is merely acting

9. A contingent liability is a potential liability arising from a past event.

9-8

10. The three categories of contingent liabilities are:

1. Probable and reasonably estimated

2. Reasonably possible

3. Remote

11. Only contingent liabilities that are probable and reasonably

12. Contingent liabilities that are probable and reasonably estimated are

recognized in the financial statements, but contingent liabilities that

13. Contingent liabilities that are probable but not reasonably estimable

and those that are reasonably possible but not reasonably estimated

14. A warranty is a guarantee of a product or service.

15. Recognizing future warranty obligations will increase liabilities and

16. Warranty cost is not shown on the statement of cash flows until the

17. A business supervises, directs, and controls the work of an

18. Wages generally refers to compensation earned based on the

9-9

19. The W-2 form provides the employee and the federal and state

government the amount of gross earnings and amounts withheld by

20. The two components of the FICA tax are the Social Security tax and

the Medicare tax. The Social Security tax funds the social security

21. The FICA tax is paid one half by the employee and one half by the

employer. Social Security tax is only paid on approximately the first

22. Gross pay is the total amount of salaries or wages earned before any

23. Amounts withheld from an employee’s pay are a liability because

these withholdings must be paid to the appropriate parties, e.g.

24. Proceeds from the Federal Unemployment Tax are used to finance

25. Total compensation cost includes salaries and wages, the

9-10

26. Example of fringe benefits include vacation pay, sick pay, medical,

27. A classified balance sheet is one that separates assets and liabilities

28. Liquidity refers to a business’s ability to generate short-term cash

29. This is generally true. A high current ratio indicates the ability of a

company to meet its short-term debt obligations. However, if the

30. With an interest-bearing note, accrued interest is added to the face

made.

31. The carrying value of a discount note is computed by subtracting the

account.

32. The effective rate of interest is higher on the discounted note because

the actual amount of interest paid is more than the amount of the

9-11

Discounted Interest

Bearing

Face Value $10,000 $10,000

33. Amortization of discount reduces net income on the income

34. Event Effect on Accounting Equation

Issuing Discount Note Increase in Cash (asset); Increase in

Notes Payable (liability); Increase in

35. Discount on Notes Payable is a contra-liability account that is

9-12

SOLUTIONS TO EXERCISES - SERIES A - CHAPTER 9

EXERCISE 9-1A

a. $-0-; No interest was paid in 2016. (Interest will be paid in 2017 when

9-13

PROBLEM 9-2A

a. $12,000 x 8% = $960; $960 x 4/12 = $320

b. $320

c. $-0-; No interest was paid in 2016. (Interest will be paid in 2017 when the note matures.)

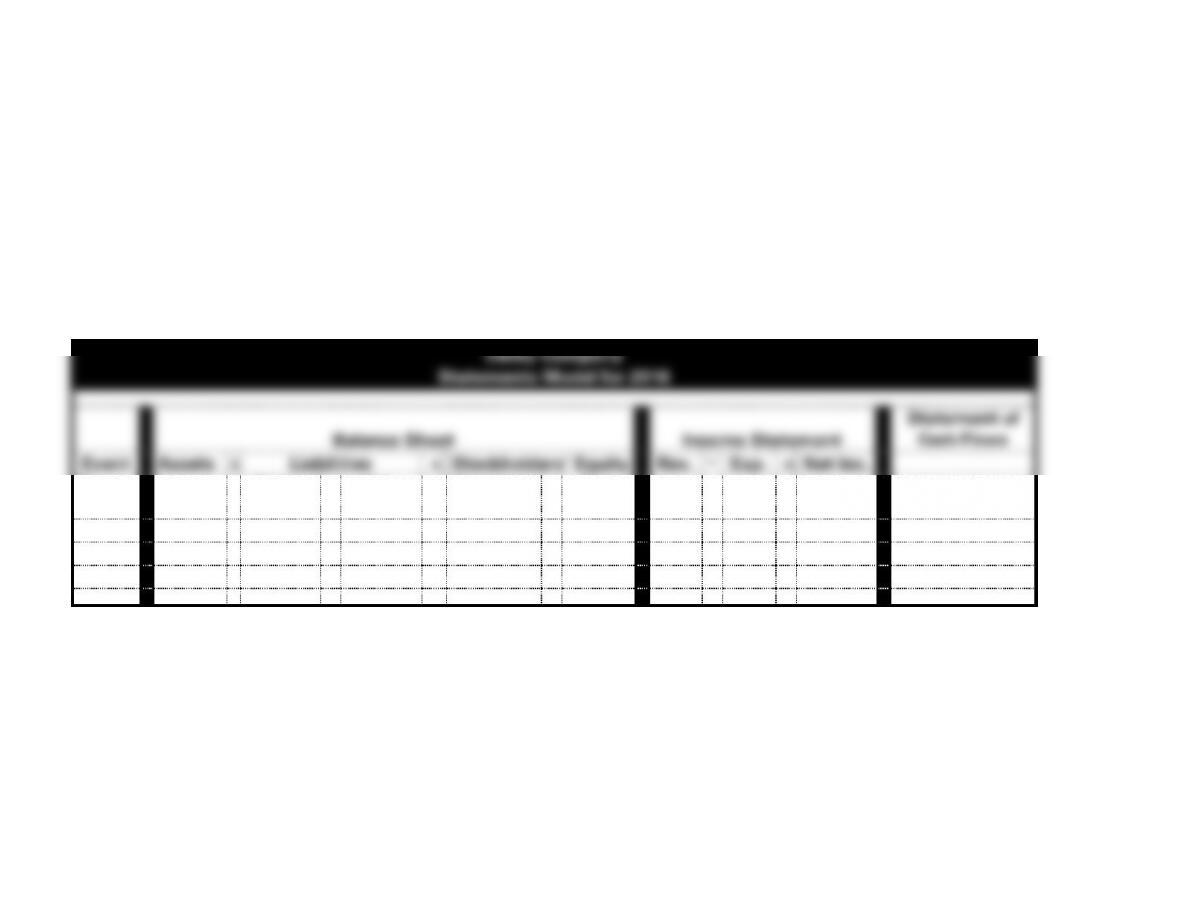

d.

Darby Company

Statements Model for 2016

Balance Sheet

Income Statement

Statement of

Cash Flows

Event

Assets

=

Liabilities

+

Stockholders’ Equity

Rev.

-

Exp.

=

Net Inc.

No.

Cash

=

Notes

Payable

+

Int.

Payable

+

Common

Stock

+

Ret.

Earn.

1.

I

NA

NA

NA

I

I

NA

I

I OA

2.

I

I

NA

NA

NA

NA

NA

NA

I FA

3.

NA

NA

I

NA

D

NA

I

D

NA

EXERCISE 9-3A

a. Book Sales $250,000

Miscellaneous Items Sales 85,000

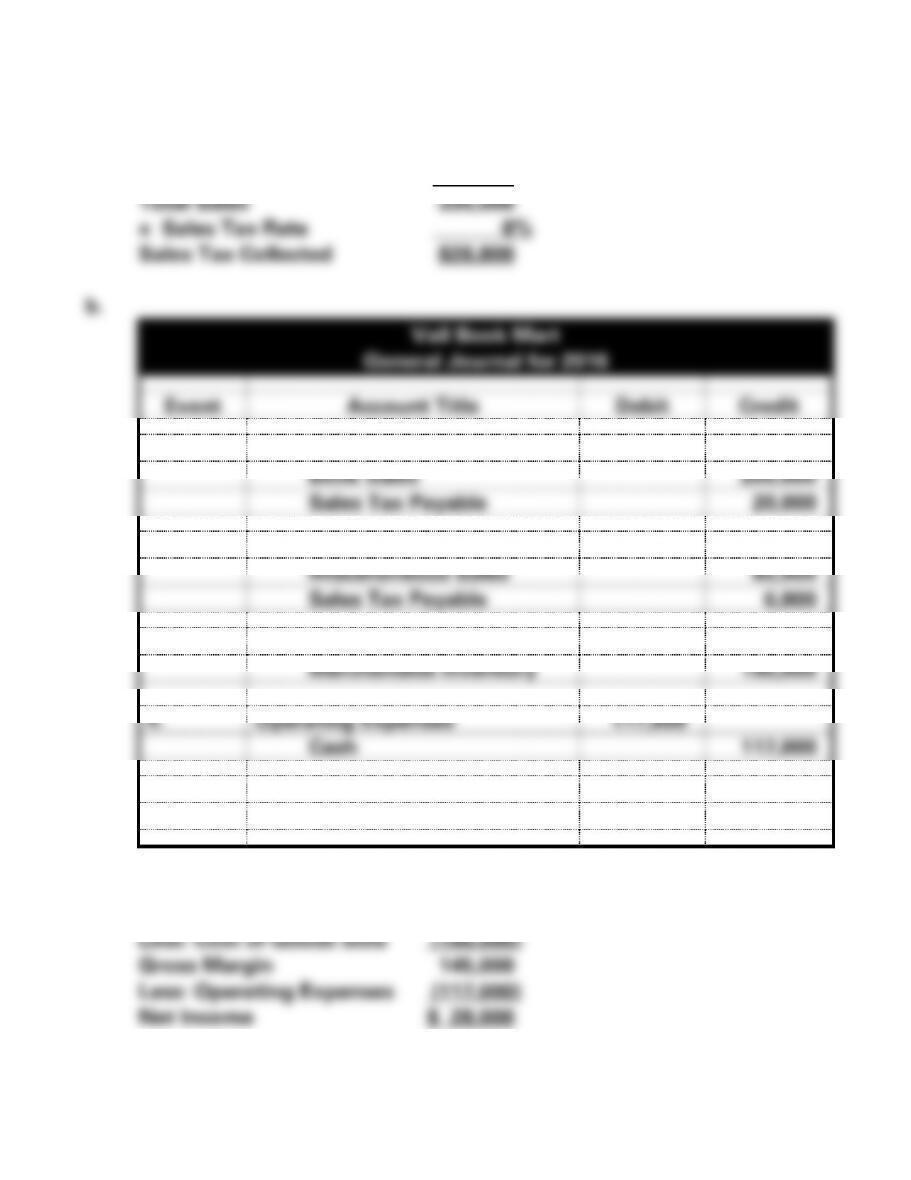

EXERCISE 9-4A a.

Topeca Supply

General Journal for 2016

Event

Account Titles

Debit

Credit

1. Nov.

Cash ($165,000 x 1.07)

176,550

Sales Revenue

165,000

Sales Tax Payable

11,550

2. Dec. 10

Sales Tax Payable

11,550

Cash

11,550

3. Dec.

Cash ($180,000 x 1.07)

192,600

Sales Revenue

180,000

Sales Tax Payable

12,600