4-95

Net Cash Flow from Operating Activities $ 4,500

4-96

EXERCISE 4-3B (cont.)

f. Net income is $11,000 and net cash flow from operating activities is

4-97

EXERCISE 4-4B

a.

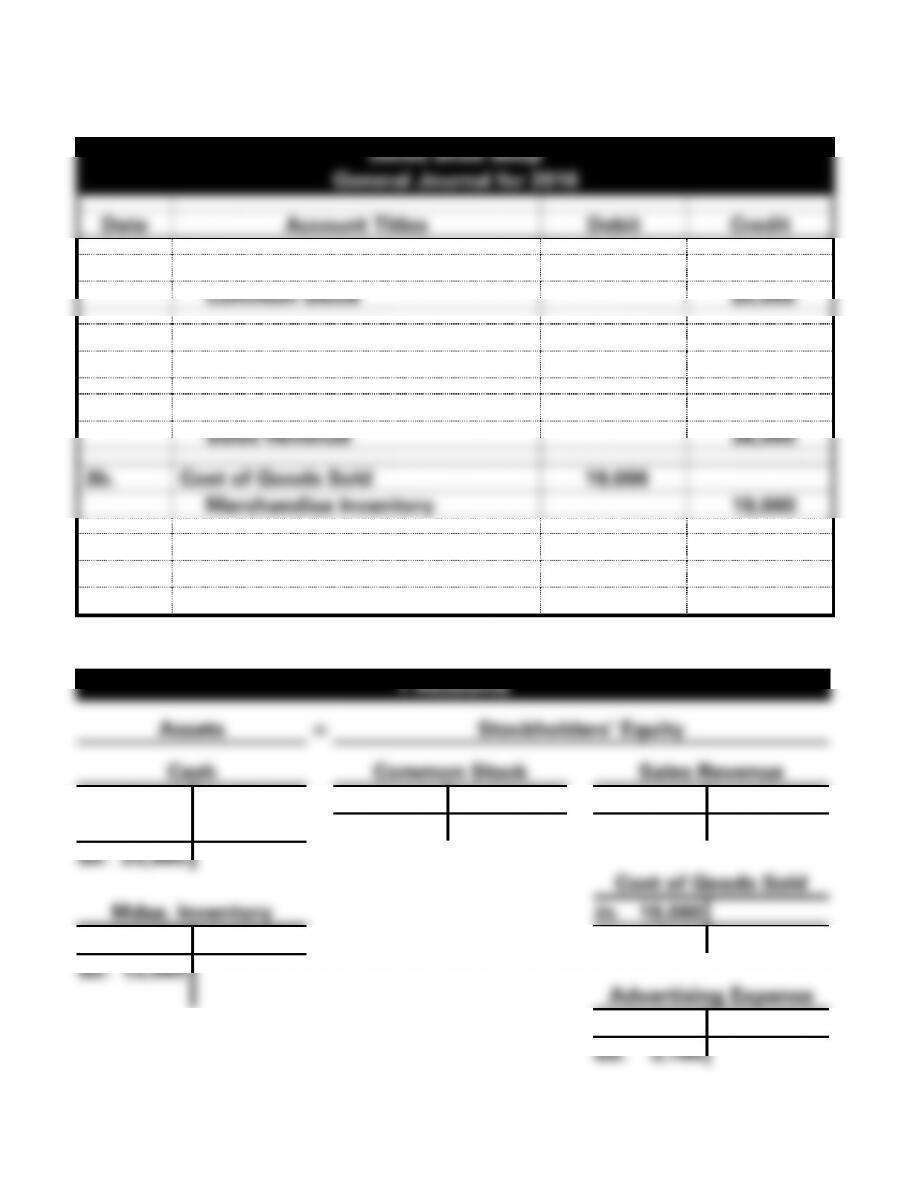

Jones Shoe Shop

General Journal for 2016

Date

Account Titles

Debit

Credit

1.

Cash

25,000

Common Stock

25,000

2.

Merchandise Inventory

32,000

Cash

32,000

3a.

Cash

36,000

Sales Revenue

36,000

3b.

Cost of Goods Sold

19,000

Merchandise Inventory

19,000

4.

Advertising Expense

3,100

Cash

3,100

b.

T-Accounts

Assets

=

Stockholders’ Equity

Cash

Common Stock

Sales Revenue

1. 25,000

2. 32,000

1. 25,000

3a. 36,000

3a. 36,000

4. 3,100

Bal. 25,000

Bal. 36,000

Bal. 25,900

Cost of Goods Sold

Mdse. Inventory

3b. 19,000

2. 32,000

3b. 19,000

Bal. 19,000

Bal. 13,000

Advertising Expense

4. 3,100

Bal. 3,100

4-98

EXERCISE 4-4B (cont.)

c.

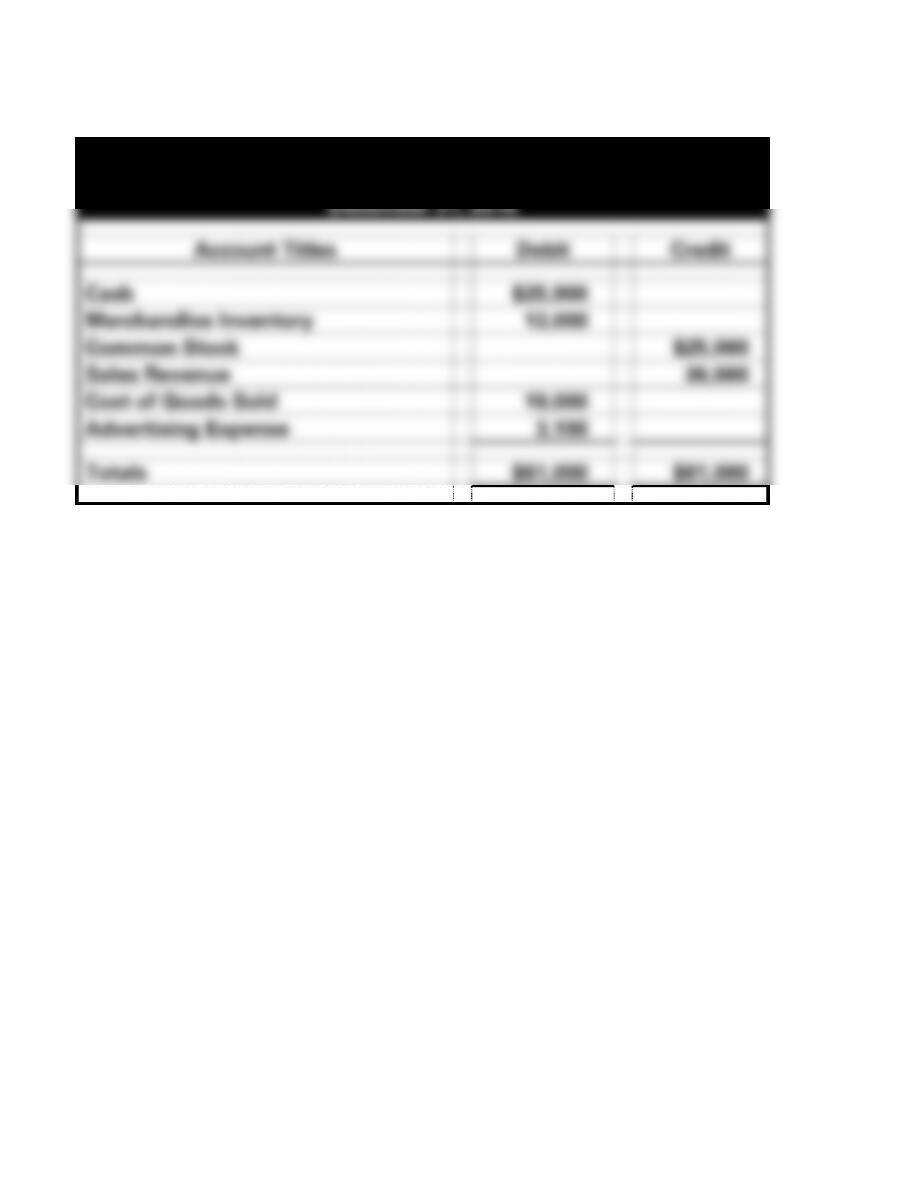

Jones Shoe shop

Trial Balance

December 31, 2016

Account Titles

Debit

Credit

Cash

$25,900

Merchandise Inventory

13,000

Common Stock

$25,000

Sales Revenue

36,000

Cost of Goods Sold

19,000

Advertising Expense

3,100

Totals

$61,000

$61,000

4-99

EXERCISE 4-5B

d. buyer

4-100

EXERCISE 4-6B

a.

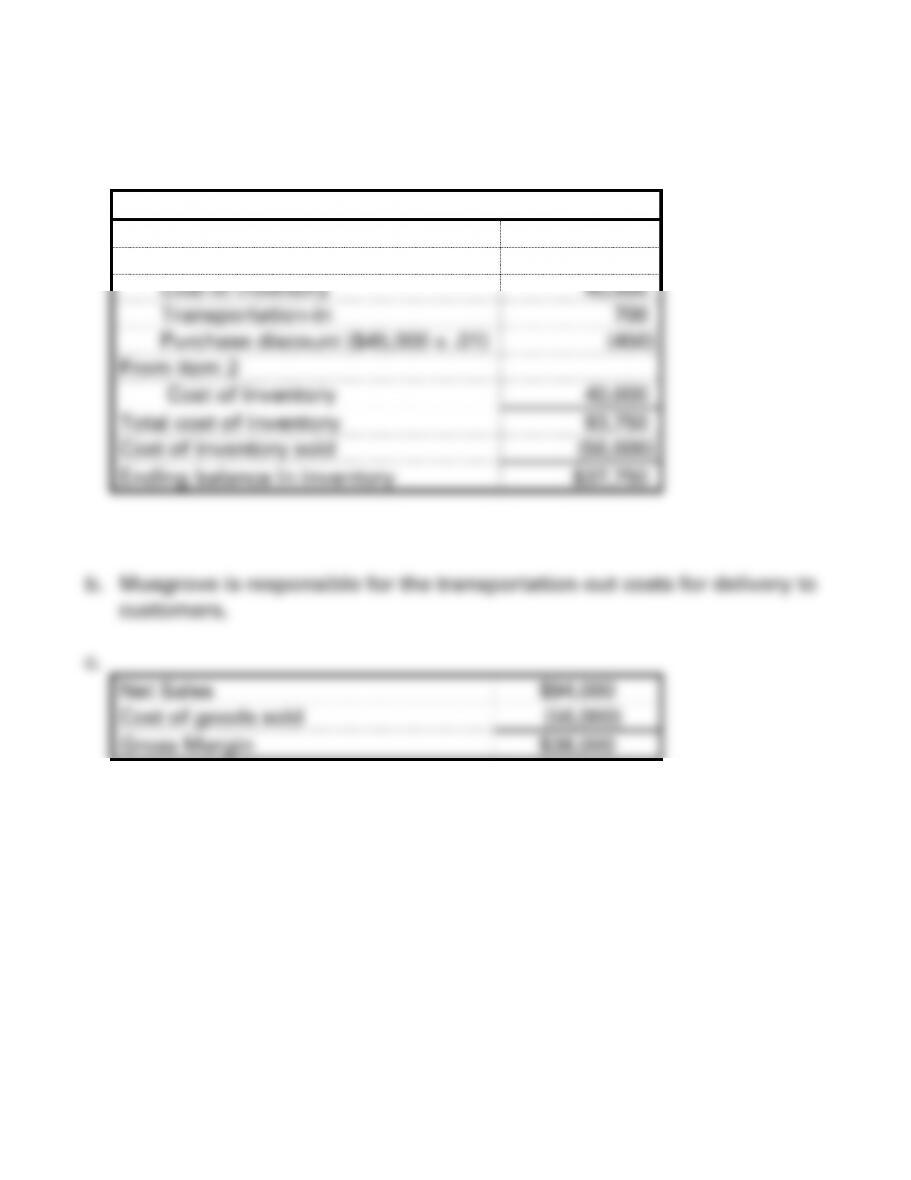

Calculation of Ending Inventory

Beginning balance in inventory

$ 8,500

From item 1:

Cost of inventory

45,000

Transportation-in

700

Purchase discount ($45,000 x .01)

(450)

From item 2

Cost of inventory

40,000

Total cost of inventory

93,750

Cost of inventory sold

(56,000)

Ending balance in inventory

$37,750

Net Sales

$94,000

Cost of goods sold

(56,000)

Gross Margin

$38,000

4-101

EXERCISE 4-7B

a.

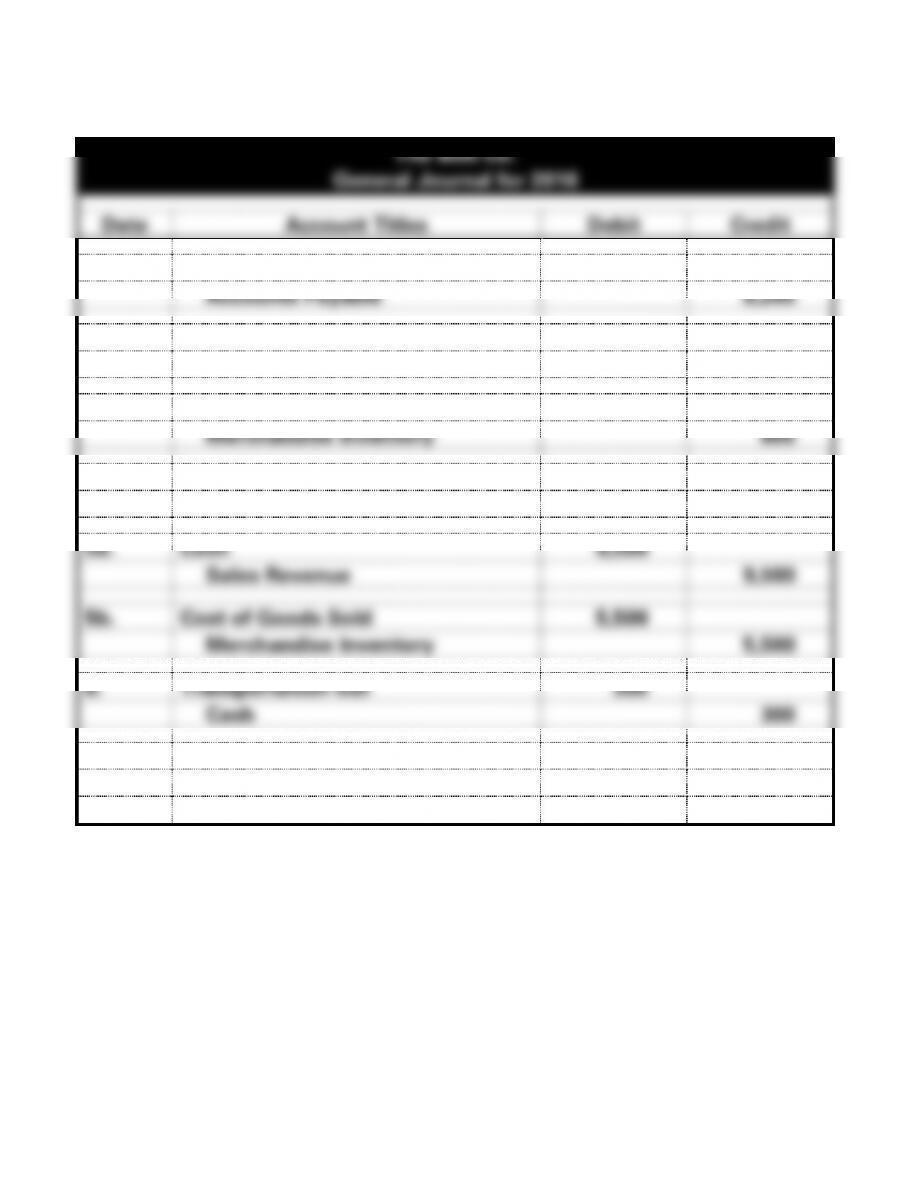

The Bolt Co.

General Journal for 2016

Date

Account Titles

Debit

Credit

1.

Merchandise Inventory

8,200

Accounts Payable

8,200

2.

Merchandise Inventory

600

Cash

600

3.

Accounts Payable

800

Merchandise Inventory

800

4.

Accounts Payable

400

Merchandise Inventory

400

5a.

Cash

9,500

Sales Revenue

9,500

5b.

Cost of Goods Sold

5,500

Merchandise Inventory

5,500

6.

Transportation-out

300

Cash

300

7.

Accounts Payable

5,000

Cash

5,000

4-102

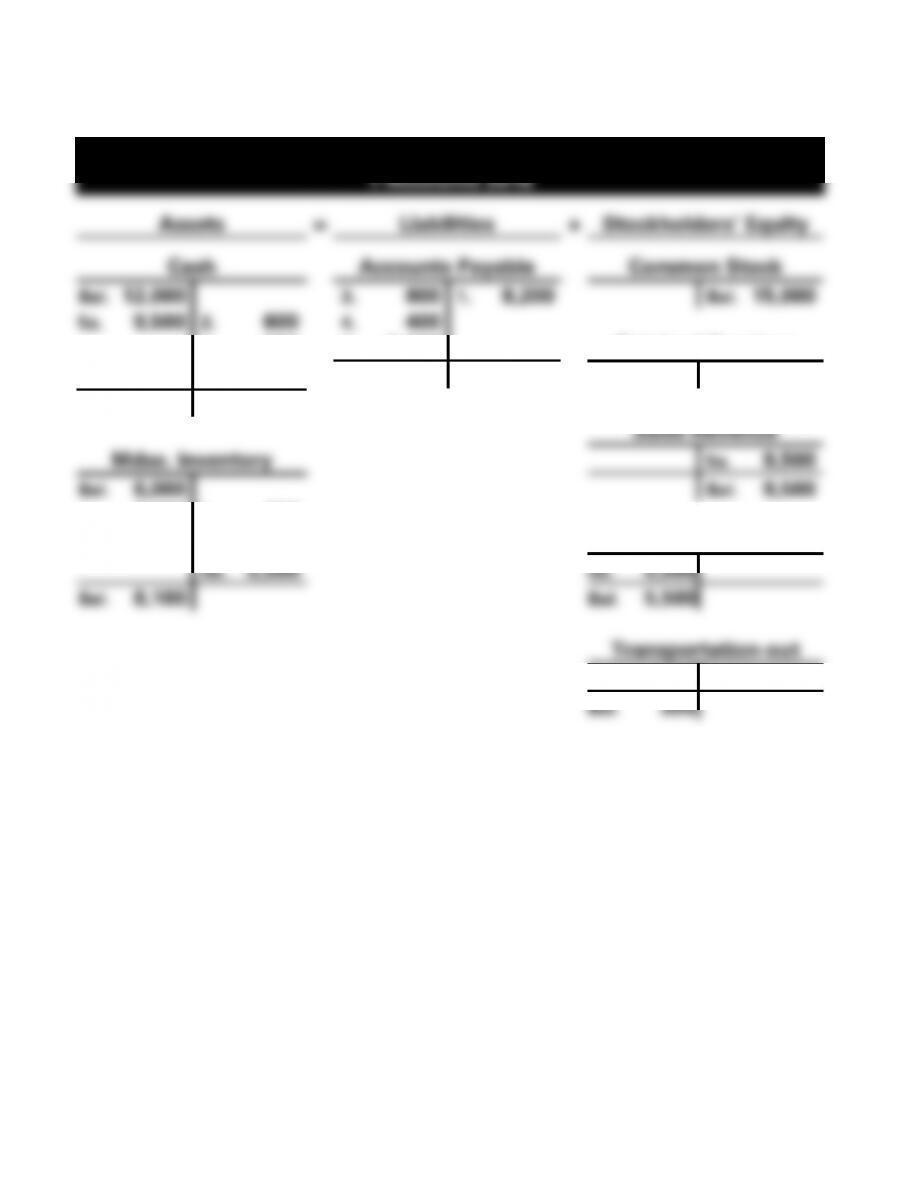

EXERCISE 4-7B (cont.)

b.

The Bolt Co.

T-Accounts 2016

Assets

=

Liabilities

+

Stockholders’ Equity

Cash

Accounts Payable

Common Stock

Bal. 12,000

3. 800

1. 8,200

Bal. 15,000

5a. 9,500

2. 600

4. 400

6. 300

7. 5,000

Retained Earnings

7. 5,000

Bal. 2,000

Bal. 3,000

Bal. 15,600

Sales Revenue

Mdse. Inventory

5a. 9,500

Bal. 6,000

Bal. 9,500

1. 8,200

3. 800

2. 600

4. 400

Cost of Goods Sold

5b. 5,500

5b. 5,500

Bal. 8,100

Bal. 5,500

Transportation-out

6. 300

Bal. 300

4-103

EXERCISE 4-7B (cont.)

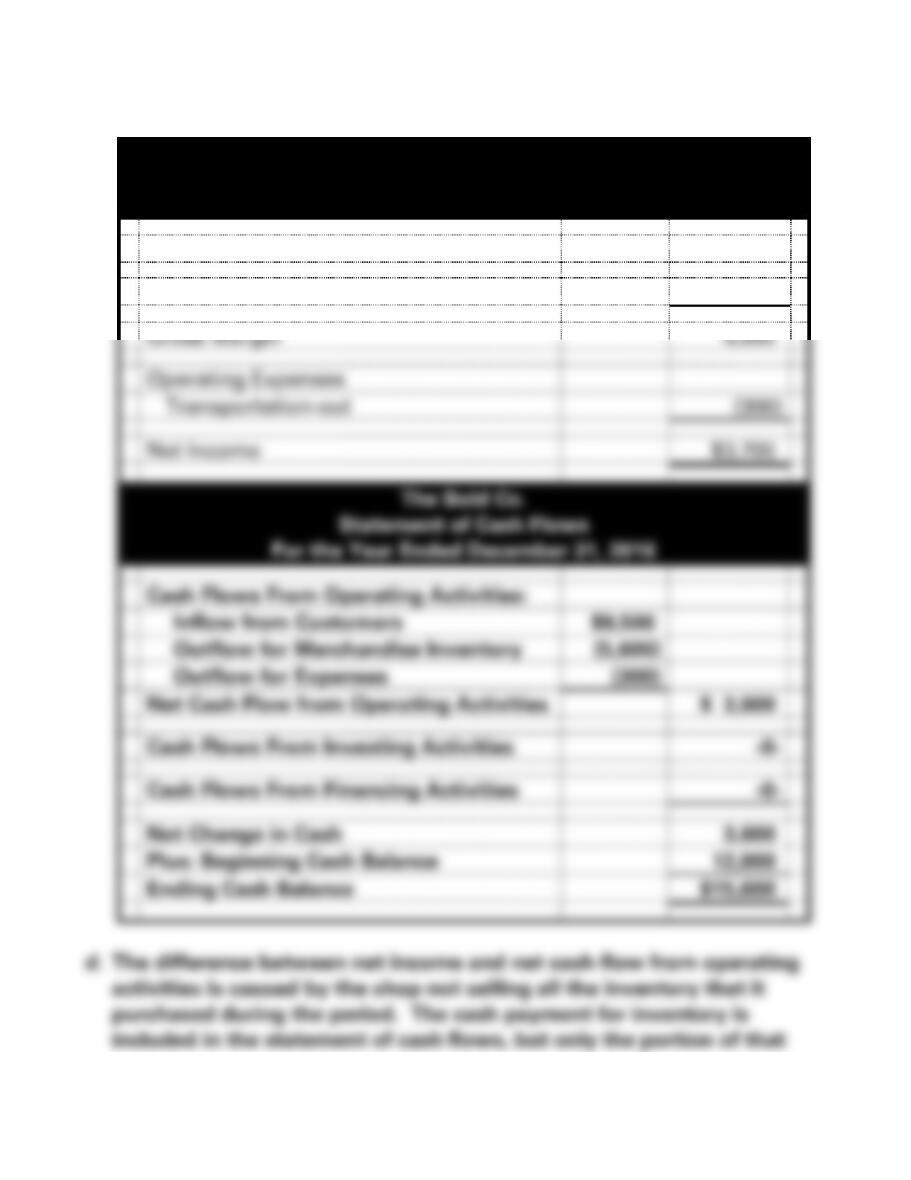

c.

The Bolt Co.

Income Statement

For the Year Ended December 31, 2016

Net Sales

$9,500

Cost of Goods Sold

(5,500)

Gross Margin

4,000

Operating Expenses

Transportation-out

(300)

Net Income

$3,700

The Bold Co.

Statement of Cash Flows

For the Year Ended December 31, 2016

Cash Flows From Operating Activities:

Inflow from Customers

$9,500

Outflow for Merchandise Inventory

(5,600)

Outflow for Expenses

(300)

Net Cash Flow from Operating Activities

$ 3,600

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities

-0-

Net Change in Cash

3,600

Plus: Beginning Cash Balance

12,000

Ending Cash Balance

$15,600

d. The difference between net income and net cash flow from operating

activities is caused by the shop not selling all the inventory that it

purchased during the period. The cash payment for inventory is

included in the statement of cash flows, but only the portion of that

4-104

payment allocated to goods actually sold is included on the income

4-105

EXERCISE 4-8B

Transaction

Debited to Inventory

a. Transportation-in

Yes

b. Allowance for damaged inventory

No

c. Purchase of inventory

Yes

d. Purchase of office supplies

No

e. Transportation-out

No

f. Cash discount on goods sold

No

4-106

EXERCISE 4-9B

a.

Transaction

Period Costs

Product Costs

Not

Applicable

1.

2.

3.

4.

5.

6.

7.

8.

9.

10.

4-107

EXERCISE 4-9B (cont.)

b.

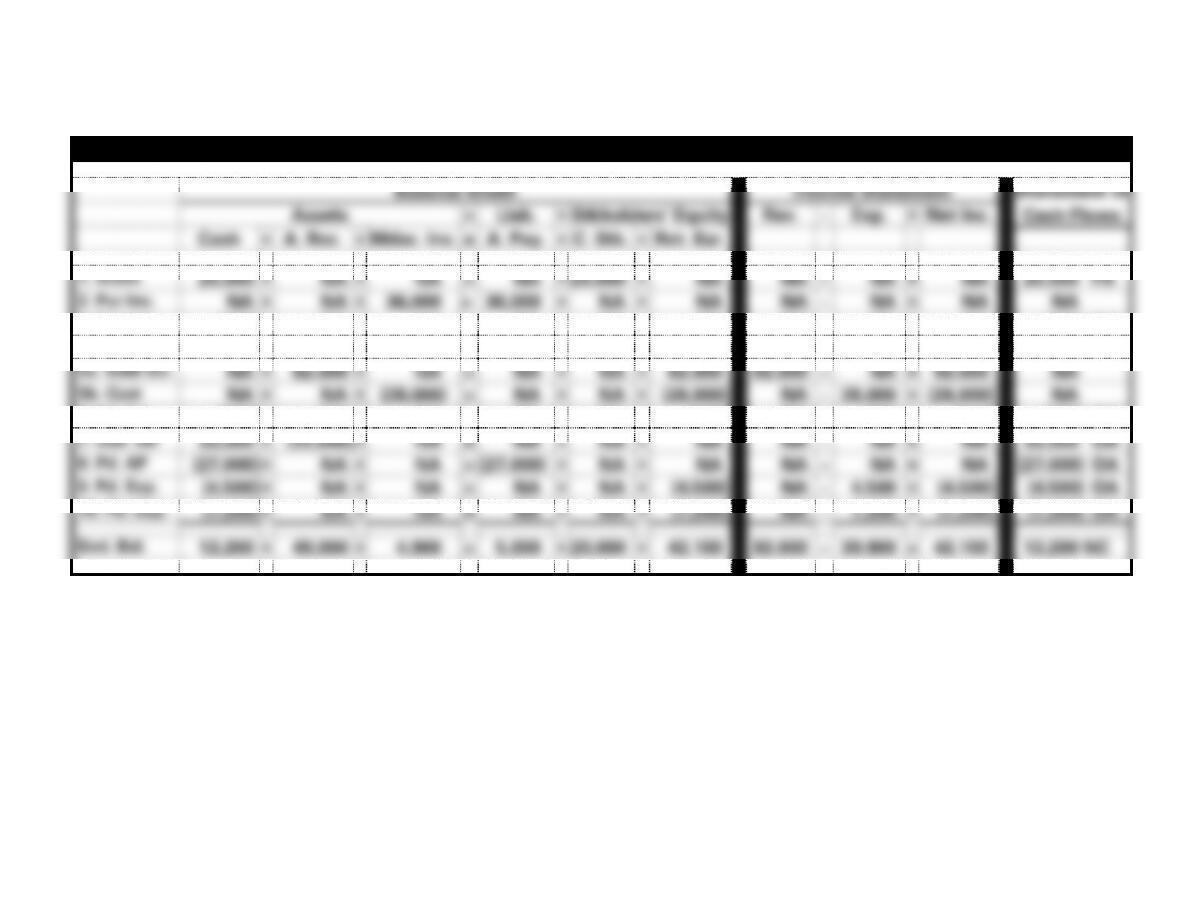

Wild Rose Co. Horizontal Statements Model for 2016

Balance Sheet

Income Statement

Statement of

Assets

=

Liab.

+

Stkholders’ Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flows

Cash

+

A. Rec.

+

Mdse. Inv.

=

A. Pay.

+

C. Stk.

+

Ret. Ear.

1. Stock

20,000

+

NA

+

NA

=

NA

+

20,000

+

NA

NA

−

NA

=

NA

20,000 FA

2. Pur Inv.

NA

+

NA

+

36,000

=

36,000

+

NA

+

NA

NA

−

NA

=

NA

NA

3. Freight

(900)

+

NA

+

900

=

NA

+

NA

+

NA

NA

−

NA

=

NA

(900) OA

4. Ret. Inv.

NA

+

NA

+

(4,000)

=

(4,000)

+

NA

+

NA

NA

−

NA

=

NA

NA

5a. Sold Inv.

NA

+

82,000

+

NA

=

NA

+

NA

+

82,000

82,000

−

NA

=

82,000

NA

5b. Cost

NA

+

NA

+

(28,000)

=

NA

+

NA

+

(28,000)

NA

−

28,000

=

(28,000)

NA

6. Pd. Frt.

(200)

+

NA

+

NA

=

NA

+

NA

+

(200)

NA

−

200

=

(200)

(200) OA

7. Coll. AR

33,000

+

(33,000)

+

NA

=

NA

+

NA

+

NA

NA

−

NA

=

NA

33,000 OA

8. Pd. AP

(27,000)

+

NA

+

NA

=

(27,000)

+

NA

+

NA

NA

−

NA

=

NA

(27,000) OA

9. Pd. Exp.

(4,500)

+

NA

+

NA

=

NA

+

NA

+

(4,500)

NA

−

4,500

=

(4,500)

(4,500) OA

10. Pd. Exp.

(7,200)

+

NA

+

NA

=

NA

+

NA

+

(7,200)

NA

−

7,200

=

(7,200)

(7,200) OA

End. Bal.

13,200

+

49,000

+

4,900

=

5,000

+

20,000

+

42,100

82,000

−

39,900

=

42,100

13,200 NC

EXERCISE 4-10B

a. Purchase $19,000

Less: return (8,500)

Gross due (subject to discount) 10,500

4-109

EXERCISE 4-10B (cont.)

c. $10,500; he would not be eligible for the discount.

d.

Salon Imports Effect of Events on the Financial Statements

Events

Balance Sheet

Income Statement

Stmt. Of Cash Flows

Assets

=

Liab.

+

Stkholders’

Equity

Rev.

−

Exp.

=

Net Inc.

Cash

+

Mdse. Inv.

=

A. Pay.

+

C. Stk.

+

Ret. Ear.

3. Pd. AP

(10,500)

+

NA

=

(10,500)

+

NA

+

NA

−

NA

=

NA

(10,500) OA

4-110

EXERCISE 4-11B

Event

No.

Event

Type

Assets

=

Liab.

+

S.

Equity

Rev.

−

Exp.

=

Net Inc.

Statement

of

Cash Flows

1.

AE

+−

NA

NA

NA

NA

NA

− OA

2a.

AS

+

NA

+

+

NA

+

NA

2b.

AU

−

NA

−

NA

+

−

NA

3.

AU

−

−

NA

NA

NA

NA

NA

4.

AS

+

+

NA

NA

NA

NA

NA

5.

AU

−

−

NA

NA

NA

NA

− OA

6.

AU

−

NA

−

NA

+

−

− OA

7a.

AS

+

NA

+

+

NA

+

+ OA

7b.

AU

−

NA

−

NA

+

−

NA

8.

AU

−

NA

−

NA

+

−

− OA

9.

AE

+−

NA

NA

NA

NA

NA

− OA

10.

AE

+/−

NA

NA

NA

NA

NA

+ OA

4-111

EXERCISE 4-12B

a.

Rabbe Sales

T-Accounts for 2016

Assets

=

Stockholders’ Equity

Cash

Common Stock

Sales Revenue

1. 80,000

2. 35,000

1. 80,000

3a. 40,500

3a. 40,500

Bal. 80,000

Bal. 40,500

Bal. 85,500

Cost of Goods Sold

Mdse. Inventory

3b. 21,000

2. 35,000

3b. 21,000

4. 500

Bal. 14,000

Bal. 21,500

4. 500

(14,000 − 13,500)

Bal. 13,500

b.

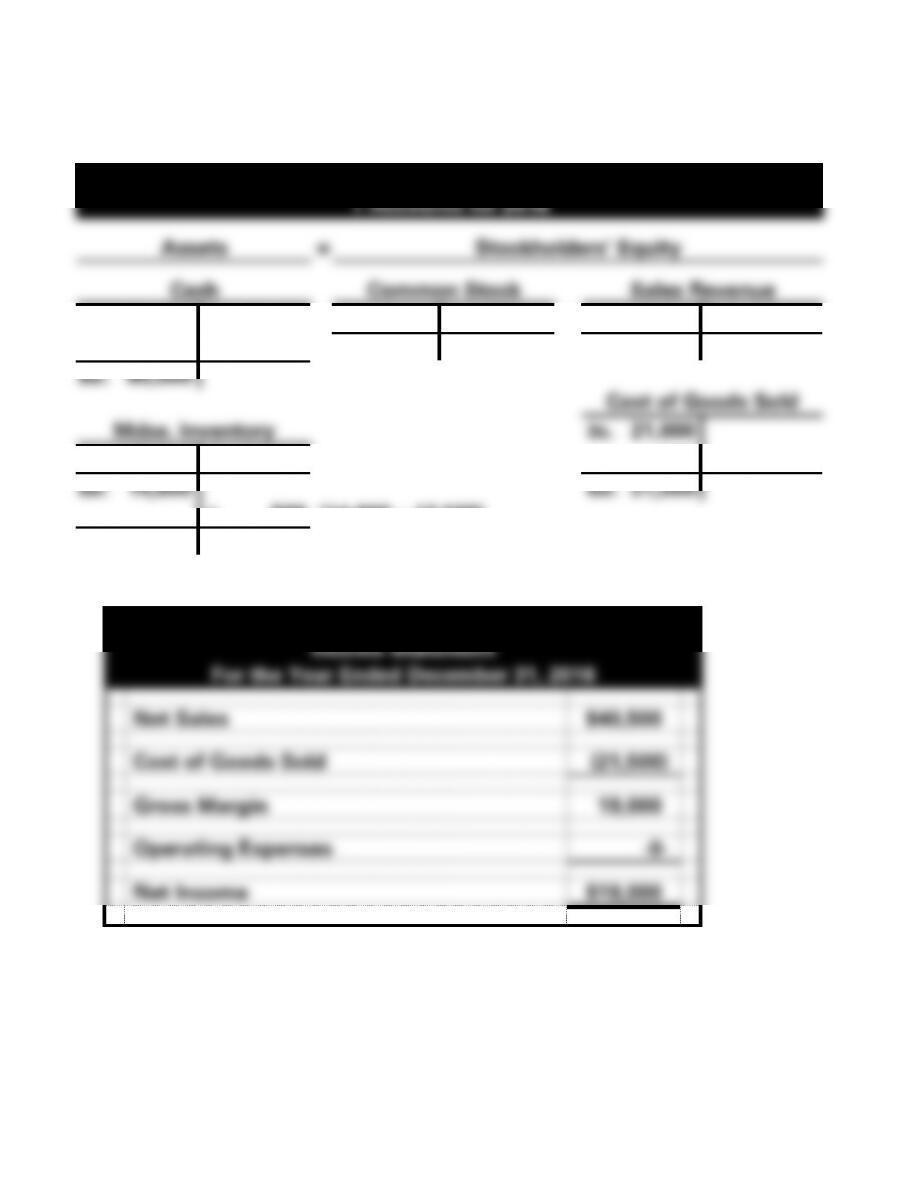

Rabbe Sales

Income Statement

For the Year Ended December 31, 2016

Net Sales

$40,500

Cost of Goods Sold

(21,500)

Gross Margin

19,000

Operating Expenses

-0-

Net Income

$19,000

4-112

EXERCISE 4-12B b. (cont.)

Rabbe Sales

Balance Sheet

As of December 31, 2016

Assets

Cash

$85,500

Merchandise Inventory

13,500

Total Assets

$99,000

Liabilities

$ -0-

Stockholders’ Equity

Common Stock

$80,000

Retained Earnings

19,000

Total Stockholders’ Equity

99,000

Total Liab. And Stockholders’ Equity

$99,000

4-113

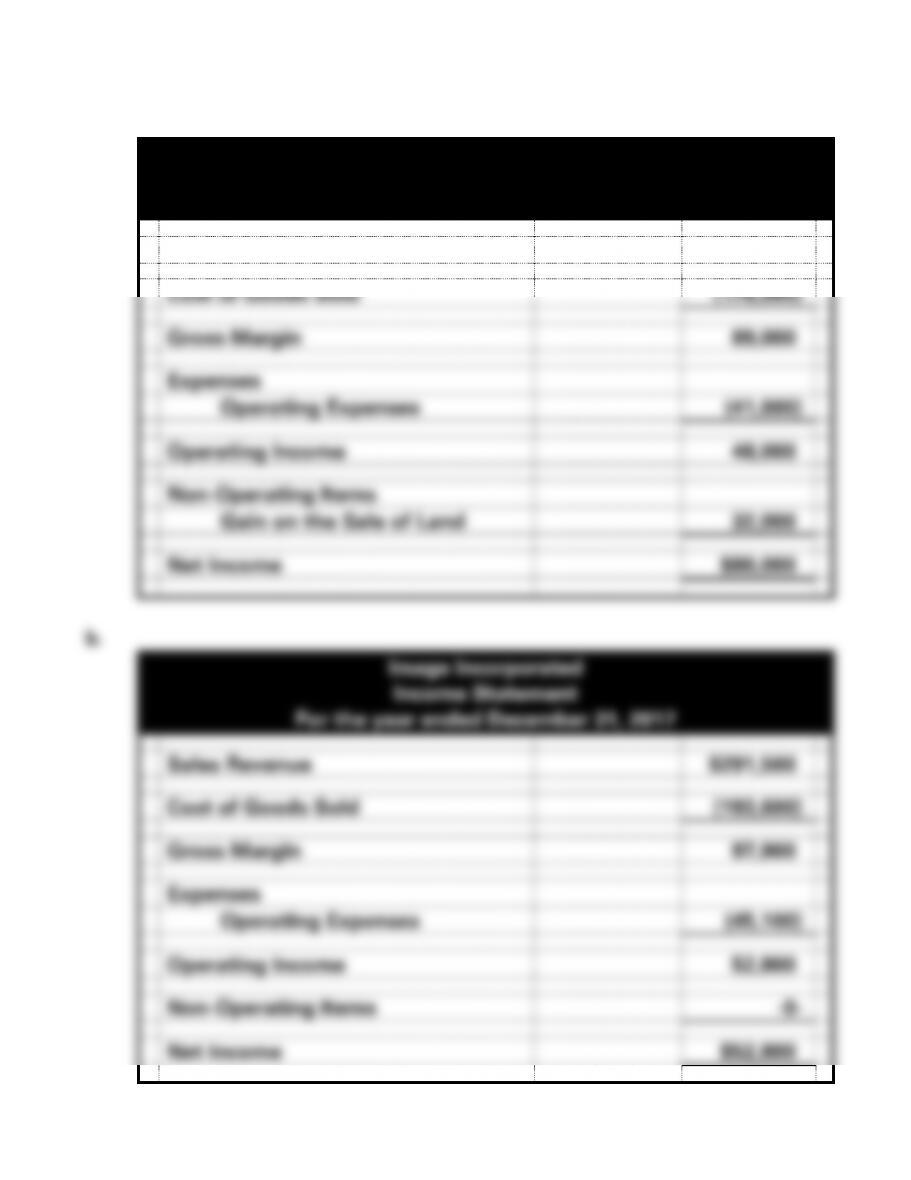

EXERCISE 4-13B

a.

Image Incorporated

Income Statement

For the year ended December 31, 2016

Sales Revenue

$265,000

Cost of Goods Sold

(176,000)

Gross Margin

89,000

Expenses

Operating Expenses

(41,000)

Operating Income

48,000

Non-Operating Items

Gain on the Sale of Land

32,000

Net Income

$80,000

Image Incorporated

Income Statement

For the year ended December 31, 2017

Sales Revenue

$291,500

Cost of Goods Sold

(193,600)

Gross Margin

97,900

Expenses

Operating Expenses

(45,100)

Operating Income

52,800

Non-Operating Items

-0-

Net Income

$52,800

4-114