4-75

ATC 4-1 (All dollar amounts are in millions.)

a. Gross margin was not given, so it must be computed.

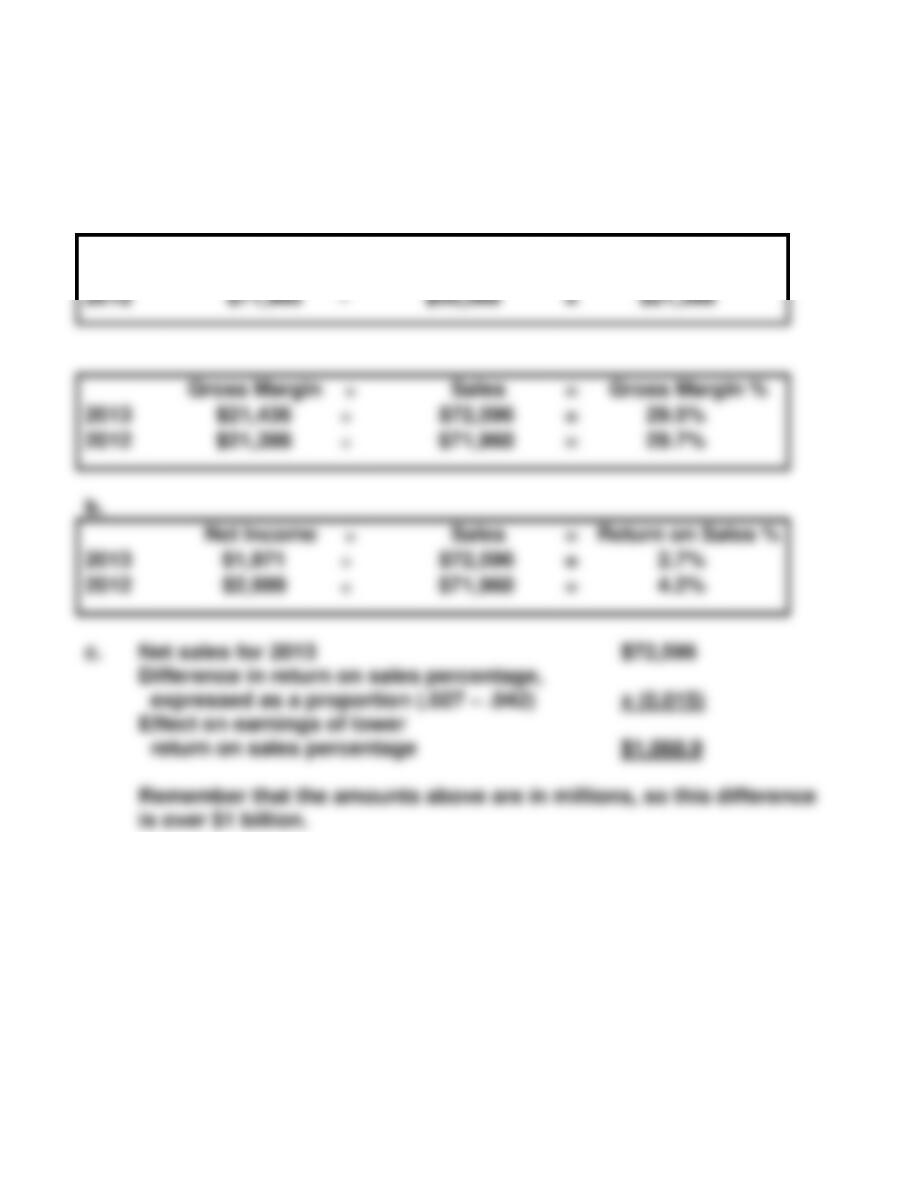

Sales

–

Cost of Sales

=

Gross Margin

2013

$72,596

–

$51,160

=

$21,436

2012

$71,960

–

$50,568

=

$21,398

Gross Margin

Sales

=

Gross Margin %

2013

$21,436

$72,596

=

29.5%

2012

$21,398

$71,960

=

29.7%

b.

Net Income

Sales

=

Return on Sales %

2013

$1,971

$72,596

=

2.7%

2012

$2,999

$71,960

=

4.2%

c. Net sales for 2013 $72,596

Difference in return on sales percentage,

expressed as a proportion (.027 – .042) x (0.015)

Effect on earnings of lower

return on sales percentage $1,088.9

Remember that the amounts above are in millions, so this difference

is over $1 billion.

ATC 4-2

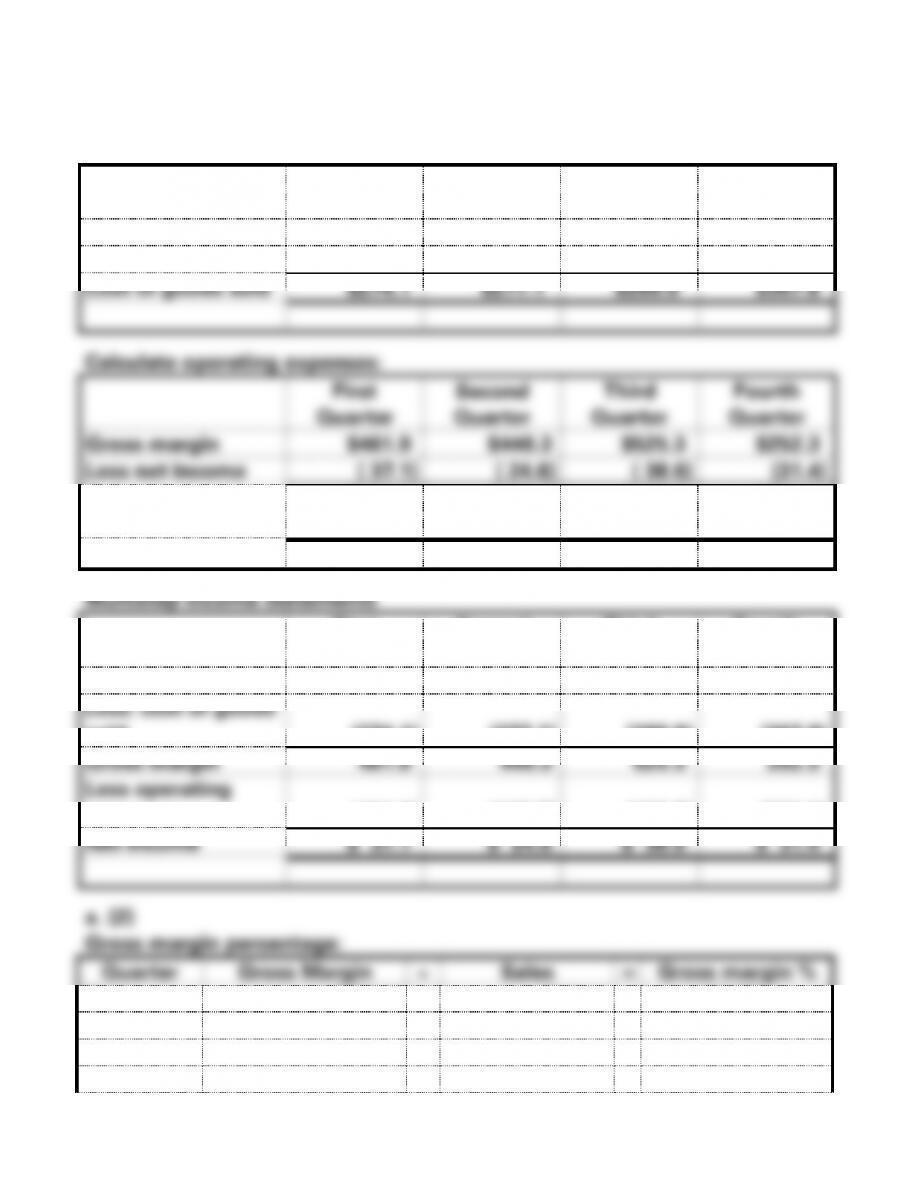

a. (1)

Calculate cost of goods sold:

First

Quarter

Second

Quarter

Third

Quarter

Fourth

Quarter

Sales

$736.0

$717.4

$815.2

$620.1

Less gross margin

(461.9)

(440.3)

(525.3)

(252.3)

Cost of goods sold

$274.1

$277.1

$289.9

$367.8

First

Quarter

Second

Quarter

Third

Quarter

Fourth

Quarter

Gross margin

$461.9

$440.3

$525.3

$252.3

Less net income

( 37.1)

( 24.6)

( 38.6)

(31.4)

Operating

expenses

$424.8

$415.7

$486.7

$220.9

First

Quarter

Second

Quarter

Third

Quarter

Fourth

Quarter

Sales

$736.0

$717.4

$815.2

$620.1

Less: cost of goods

sold

(274.1)

(277.1)

(289.9)

(367.8)

Gross margin

461.9

440.3

525.3

252.3

Less operating

expenses

(424.8)

(415.7)

(486.7)

(220.9)

Net income

$ 37.1

$ 24.6

$ 38.6

$ 31.4

Sales

62.8%

4-77

4-78

ATC 4-2 a. (cont.)

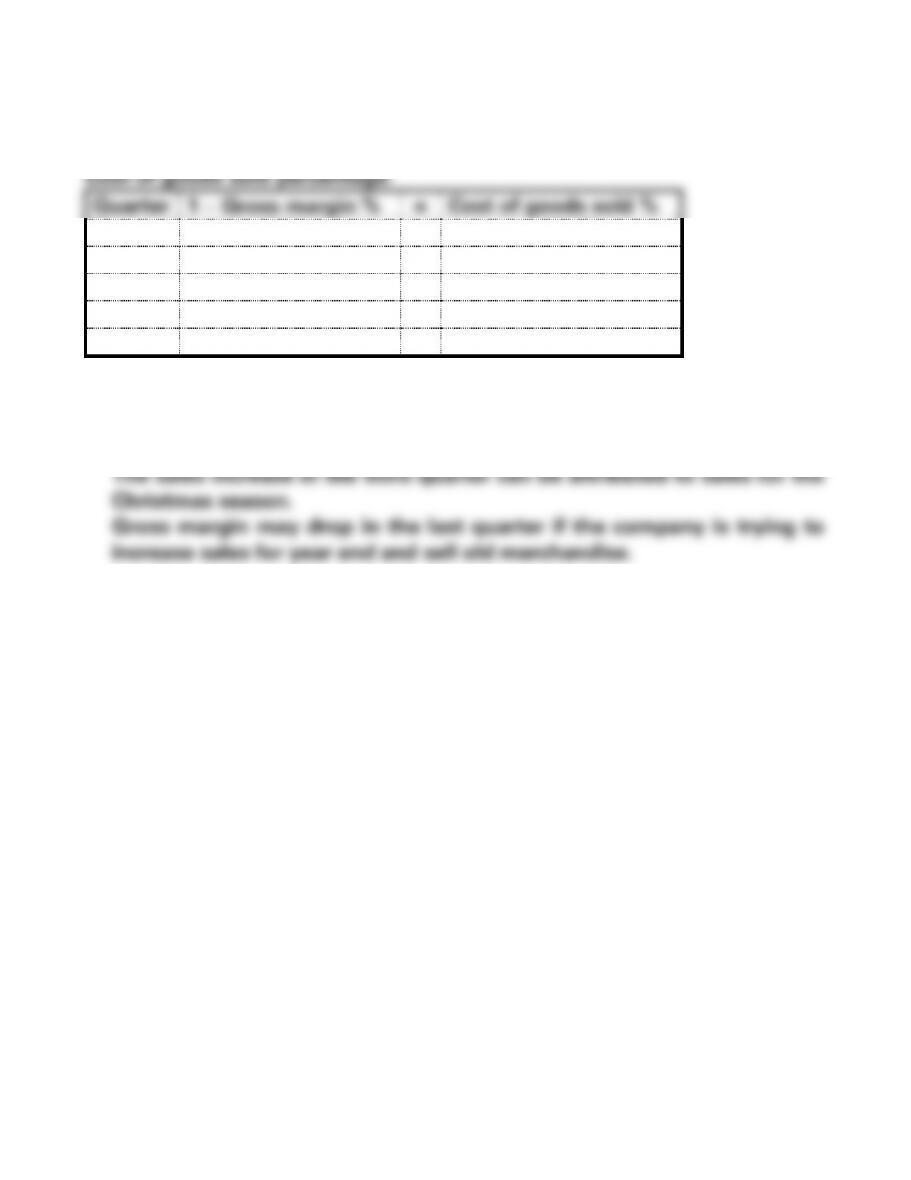

a. (2)

Quarter

1 − Gross margin %

=

Cost of goods sold %

First

1.00 − .628

=

37.2%

Second

1.00 − .614

=

38.6%

Third

1.00 − .644

=

35.6%

Fourth

1.00 − .407

=

59.3%

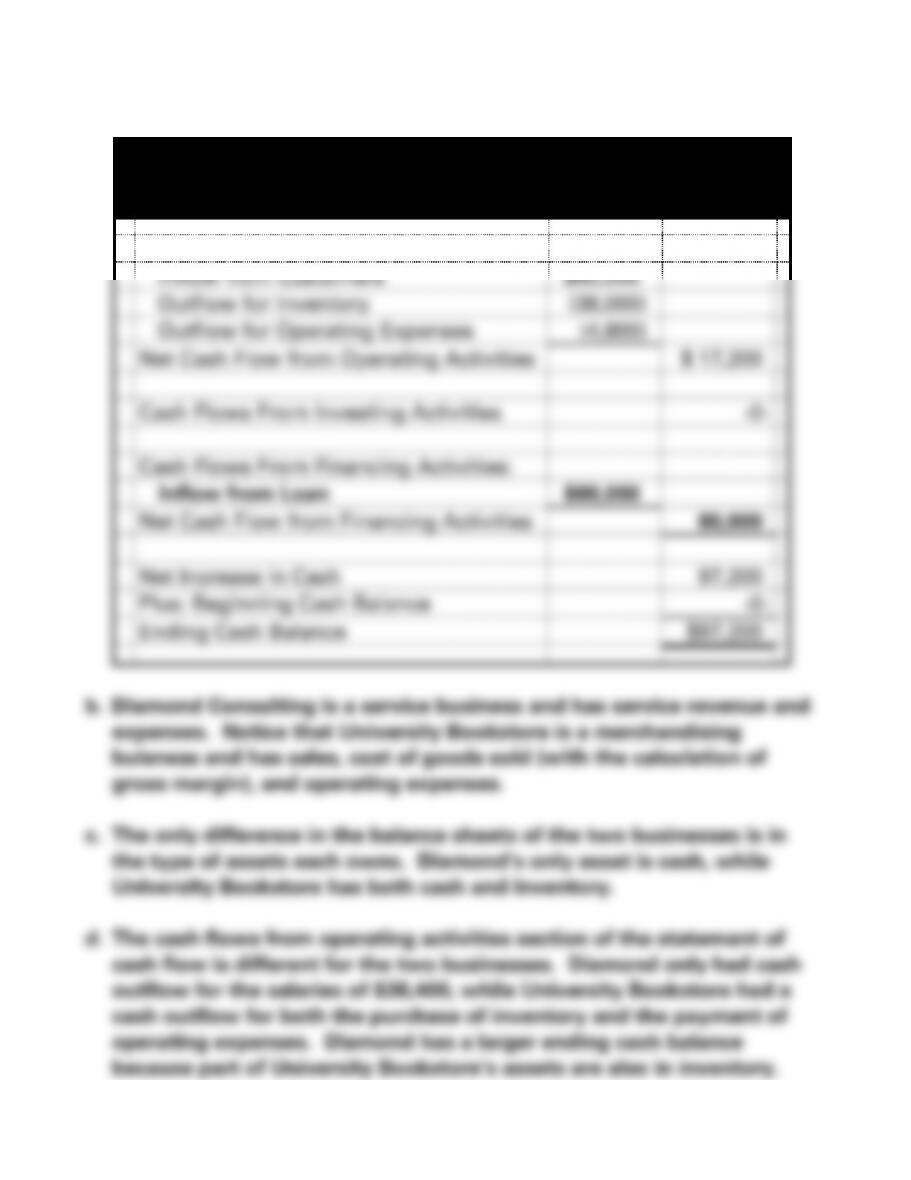

b. Some points the students may mention include:

4-79

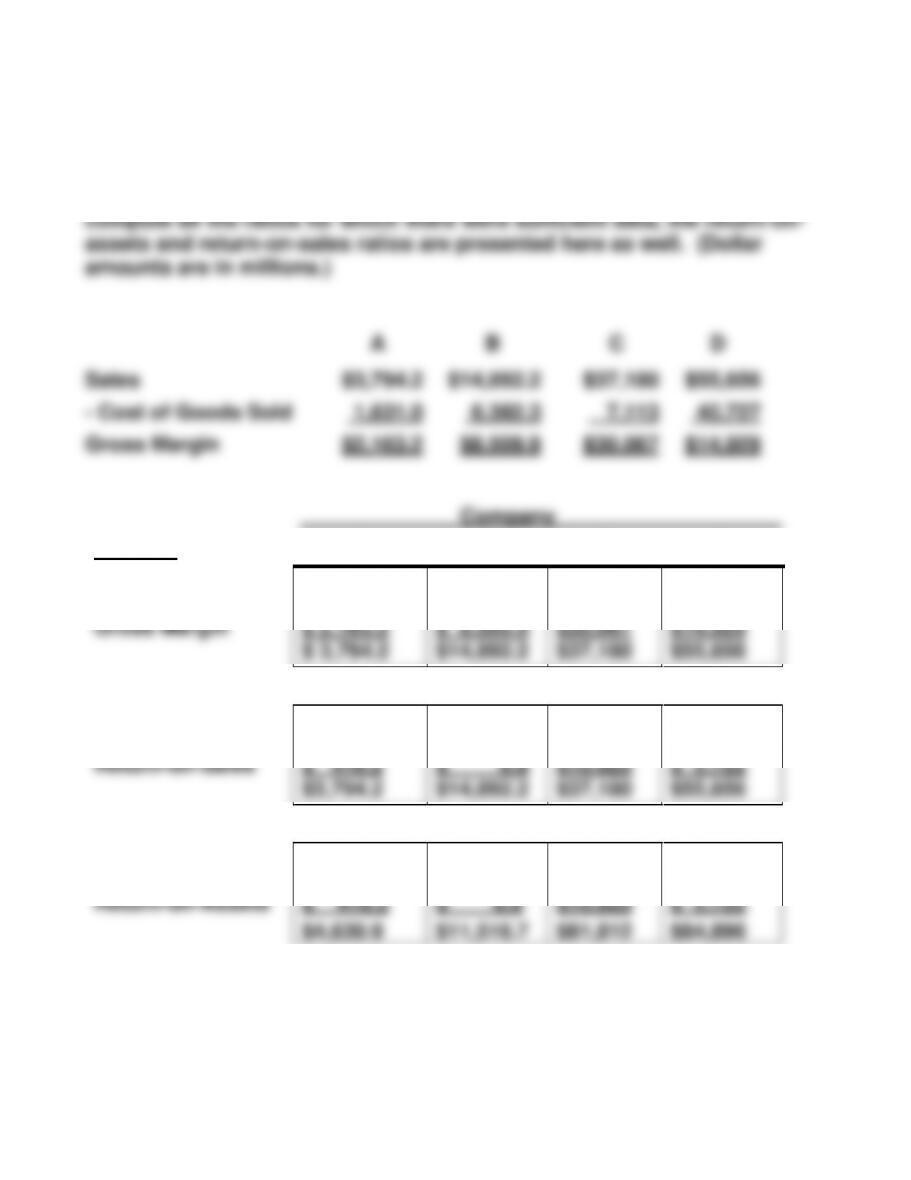

ATC 4-3

The correct matching of the four companies with their related financial

data can be achieved primarily with the gross margin percentage ratio,

plus other factors. However, on the assumption that many students will

RATIO:

A

B

C

D

57.0% =

57.1% =

80.9% =

26.8% =

Gross Margin

$ 2,163.2

$ 8,509.9

$30,067

$14,929

$ 3,794.2

$14,892.2

$37,180

$55,656

11.0% =

0.1% =

29.3% =

10.3% =

Return-on-Sales

$ 416.2

$ 8,8

$10,925

$ 5,722

$3,794.2

$14,892.2

$37,180

$55,656

9.0% =

0.1% =

13.4% =

6.7% =

Return-on-Assets

$ 416.2

$ 8.8

$10,925

$ 5,722

$4,630.9

$11,516.7

$81,812

$84,896

Sales

– Cost of Goods Sold

Gross Margin

4-80

ATC 4-3 (cont.)

The four companies relate to the financial information as follows:

Tiffany is company “A”

Starbucks is company “B”

Oracle is company “C”

4-81

ATC 4-4

a. Gross Margin Percentages:

First, the gross margins must be calculated:

2013: $4,089,128 – $1,333,842 = $2,755,286

2012: $3,946,116 – $1,281,002 = $2,665,114

4-82

ATC 4-5

a. Since Whole Foods is a high-end retailer of groceries, one would

expect its gross margin percentage to be higher than Kroger’s. The

fact that Kroger charges less for its groceries than Whole Foods

does not necessarily mean that its return on sales percentage will be

lower. Kroger probably pays less per square foot of space for its

4-83

ATC 4-6

a.

This writing assignment tests both analytical and writing skills.

Some of the analytical amounts that should be included are:

For 2016:

Sales are overstated by $146,800.

Cost of goods sold is overstated by $94,623.

4-84

A member should maintain objectivity and be free of conflicts of

interest in discharging professional responsibilities. A member in

public practice should be independent in fact and appearance when

violated.

4-85

ATC 4-7

a. An immediate write-off would result in a $600,000 inventory loss

reported under unusual items on the company’s income

statement. This loss would be subtracted from income from

continuing operations. Accordingly, net income would decline.

The write-off would decrease assets (i.e., inventory) and equity

bonus would suffer from an event that happened in the prior

period.

d. Given that the damaged inventory is worthless, it would be

unethical for Ms. Fontanez to refuse to recognize it in the period

the loss was incurred. Fairness would dictate that Ms. Fontanez

accept the loss because it occurred in a period under her

4-86

the law.

4-87

ATC 4-8

This solution is based on Alcoa’s 2013 Form 10-K. Dollar amounts are in

millions.

a.& b.

2013 2012

Sales $23,032 $23,700

Cost of goods sold 19,286 20,401

4-88

EXERCISE 4-1B

a.

Diamond Consulting

Income Statement

For the Year Ended 2016

Revenue

Consulting Revenue

$60,000

Expenses

Salaries Expense

(38,400)

Net Income

$21,600

Diamond Consulting

Balance Sheet

As of the End of the Year 2016

Assets

Cash*

$101,600

Total Assets

$101,600

Liabilities

Notes Payable

$ 80,000

Total Liabilities

$ 80,000

Stockholders’ Equity

Retained Earnings

$21,600

Total Stockholders’ Equity

21,600

Total Liab. and Stockholders’ Equity

$101,600

4-89

EXERCISE 4-1B a. (cont.)

Diamond Consulting

Statement of Cash Flows

For the Year Ended 2016

Cash Flows From Operating Activities:

Inflow from Clients

$60,000

Outflow for Salaries

(38,400)

Net Cash Flow from Operating Activ.

$ 21,600

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities:

Inflow from Loan

$80,000

Net Cash Flow from Financing Activ.

80,000

Net Increase in Cash

101,600

Plus: Beginning Cash Balance

-0-

Ending Cash Balance

$101,600

4-90

EXERCISE 4-1B a. (cont.)

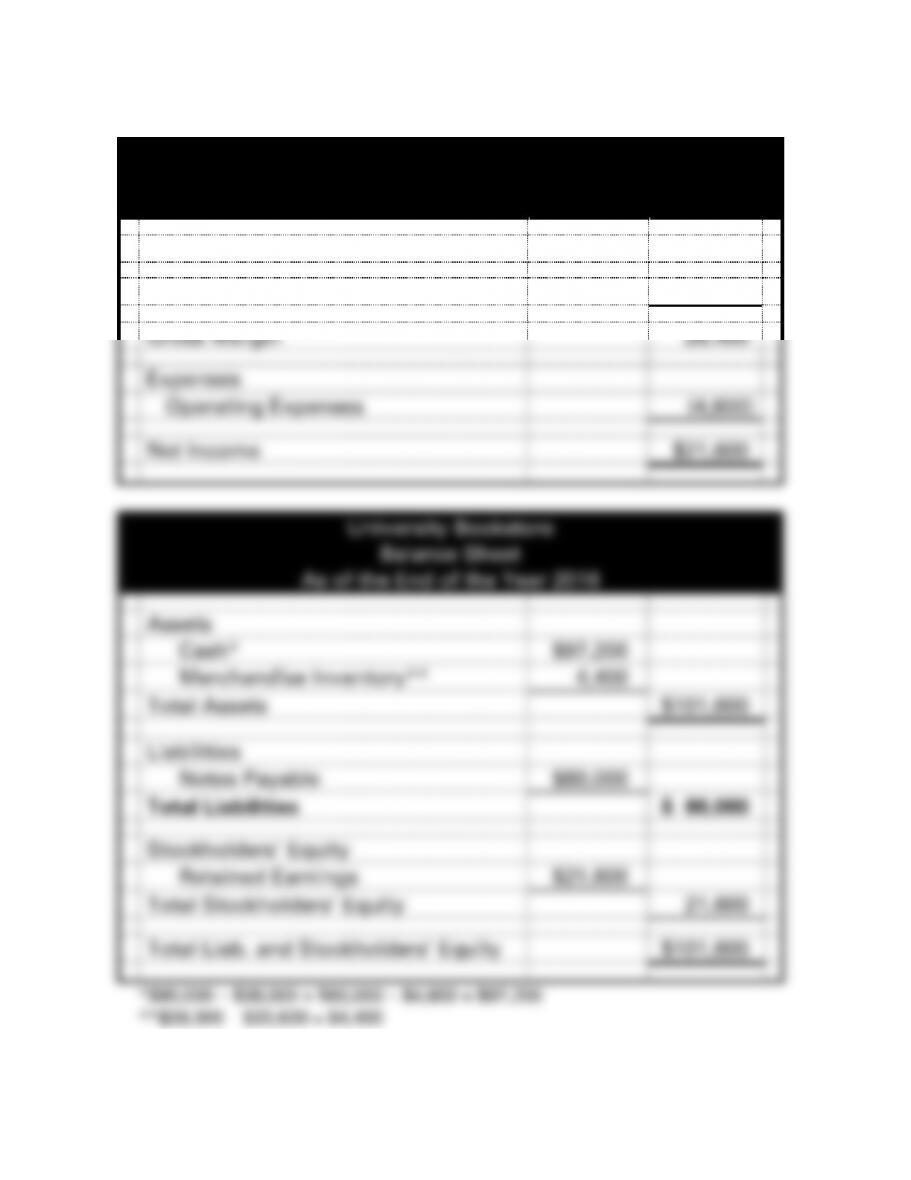

University Bookstore

Income Statement

For the Year Ended 2016

Net Sales

$60,000

Cost of Goods Sold

(33,600)

Gross Margin

26,400

Expenses

Operating Expenses

(4,800)

Net Income

$21,600

University Bookstore

Balance Sheet

As of the End of the Year 2016

Assets

Cash*

$97,200

Merchandise Inventory**

4,400

Total Assets

$101,600

Liabilities

Notes Payable

$80,000

Total Liabilities

$ 80,000

Stockholders’ Equity

Retained Earnings

$21,600

Total Stockholders’ Equity

21,600

Total Liab. and Stockholders’ Equity

$101,600

4-91

EXERCISE 4-1B a. (cont.)

University Bookstore

Statement of Cash Flows

For the Year Ended 2016

Cash Flows From Operating Activities:

Inflow from Customers

$60,000

Outflow for Inventory

(38,000)

Outflow for Operating Expenses

(4,800)

Net Cash Flow from Operating Activities

$ 17,200

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities:

Inflow from Loan

$80,000

Net Cash Flow from Financing Activities

80,000

Net Increase in Cash

97,200

Plus: Beginning Cash Balance

-0-

Ending Cash Balance

$97,200

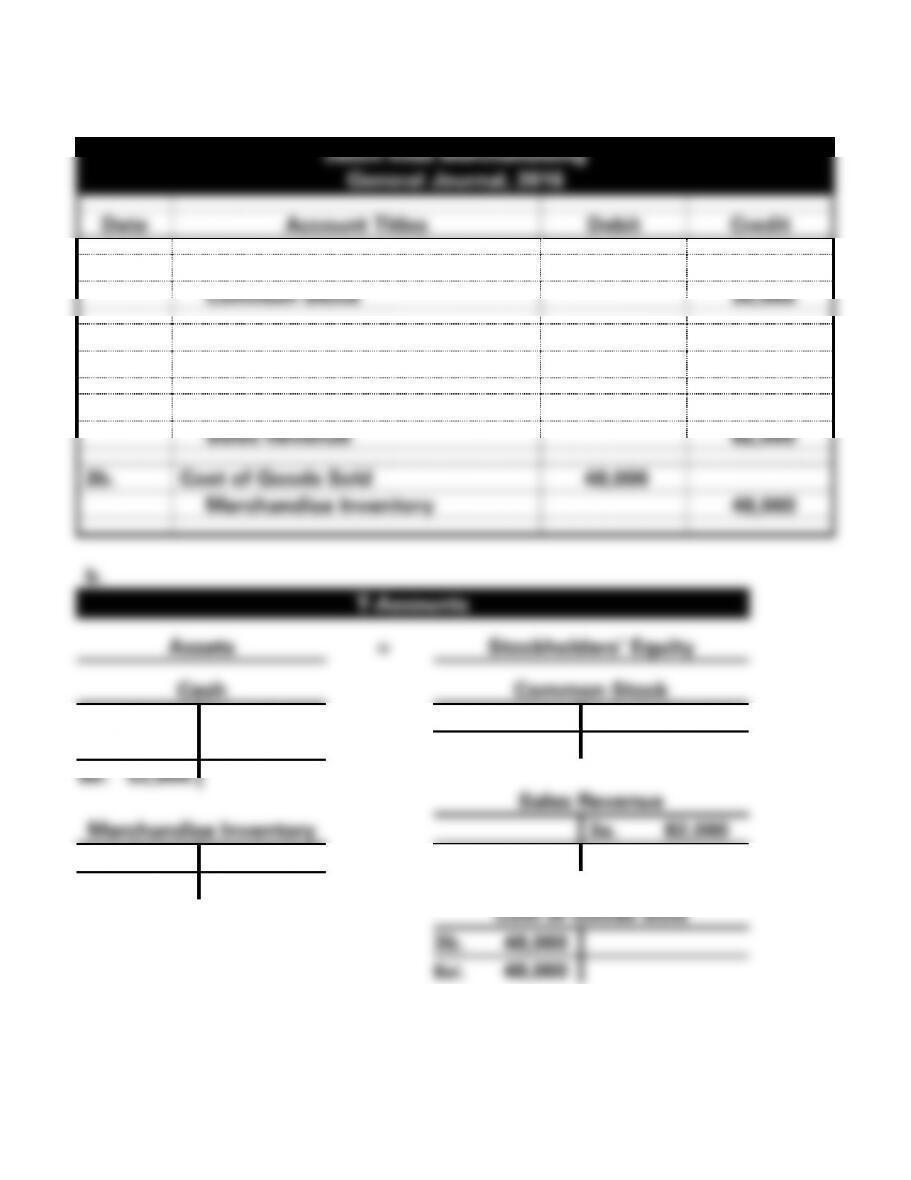

EXERCISE 4-2B

a.

Jason Kidd Merchandising

General Journal, 2016

Date

Account Titles

Debit

Credit

1.

Cash

30,000

Common Stock

30,000

2.

Merchandise Inventory

60,000

Cash

60,000

3a.

Cash

82,000

Sales Revenue

82,000

3b.

Cost of Goods Sold

48,000

Merchandise Inventory

48,000

2. 60,000

3a. 82,000

3b. 48,000

4-93

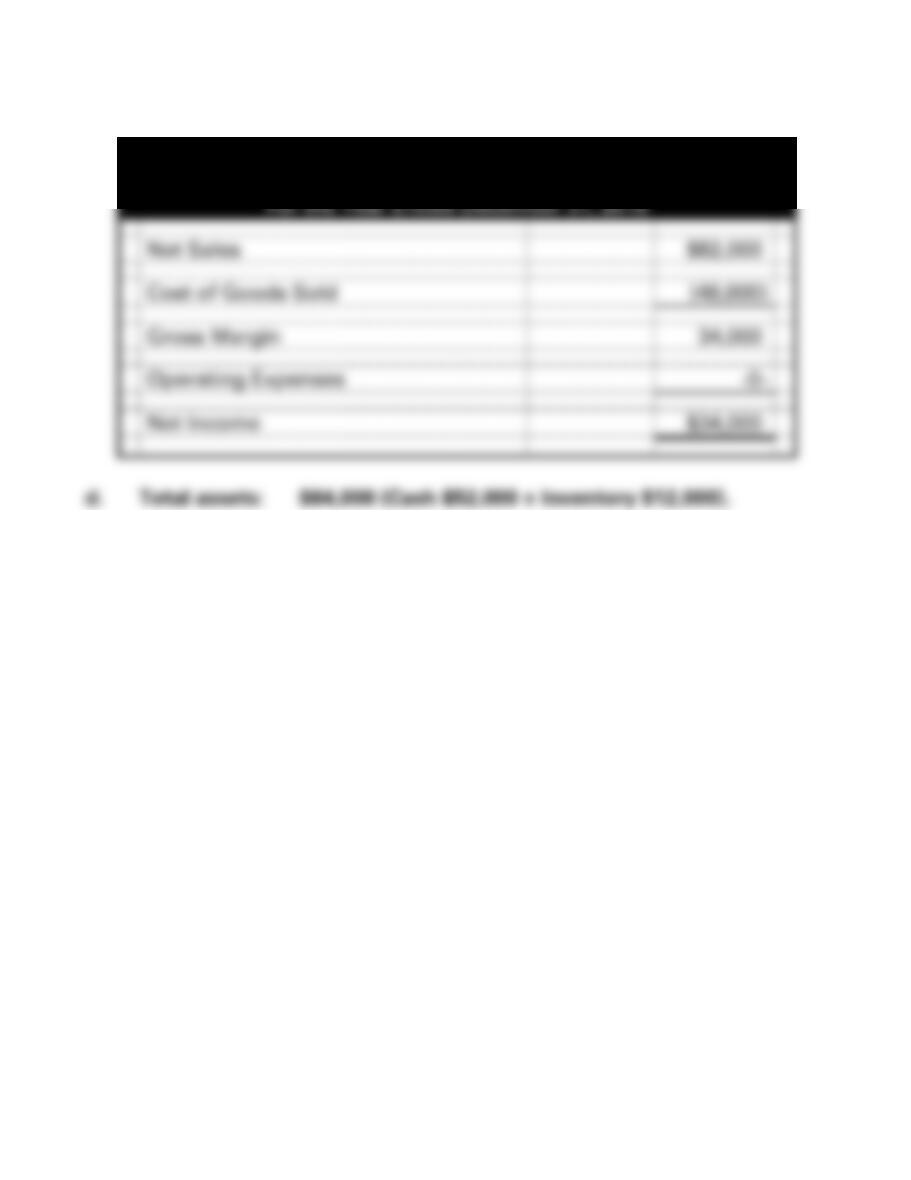

EXERCISE 4-2B (cont.)

c.

Jason Kidd Merchandising

Income Statement

For the Year Ended December 31, 2016

Net Sales

$82,000

Cost of Goods Sold

(48,000)

Gross Margin

34,000

Operating Expenses

-0-

Net Income

$34,000

d. Total assets: $64,000 (Cash $52,000 + Inventory $12,000).

4-94

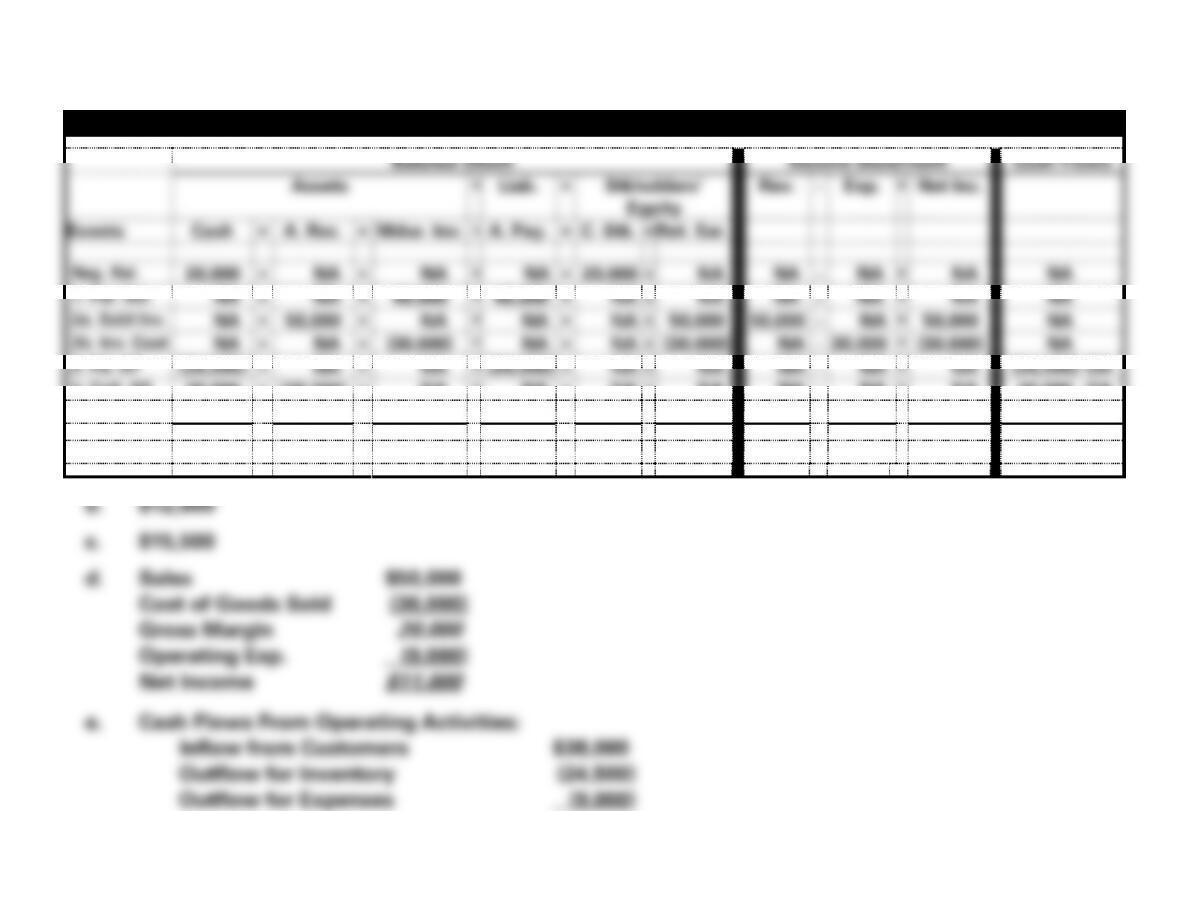

EXERCISE 4-3B a.

Rondor Merchandising Company Effect of Events on the Financial Statements

Balance Sheet

Income Statement

Cash Flows

Assets

=

Liab.

+

Stkholders’

Equity

Rev.

−

Exp.

=

Net Inc.

Events

Cash

+

A. Rec.

+

Mdse. Inv.

=

A. Pay.

+

C. Stk.

+

Ret. Ear.

Beg. Bal.

20,000

+

NA

+

NA

=

NA

+

20,000

+

NA

NA

−

NA

=

NA

NA

1. Pur. Inv.

NA

+

NA

+

40,000

=

40,000

+

NA

+

NA

NA

−

NA

=

NA

NA

2a. Sold Inv.

NA

+

50,000

+

NA

=

NA

+

NA

+

50,000

50,000

−

NA

=

50,000

NA

2b. Inv. Cost

NA

+

NA

+

(30,000)

=

NA

+

NA

+

(30,000)

NA

−

30,000

=

(30,000)

NA

3. Pd. AP

(24,500)

+

NA

+

NA

=

(24,500)

+

NA

+

NA

NA

−

NA

=

NA

(24,500) OA

4. Coll. AR

38,000

+

(38,000)

+

NA

=

NA

+

NA

+

NA

NA

−

NA

=

NA

38,000 OA

5. Pd. Exp.

(9,000)

+

NA

+

NA

=

NA

+

NA

+

(9,000)

NA

−

9,000

=

(9,000)

(9,000) OA

End. Bal.

24,500

+

12,000

+

10,000

=

15,500

+

20,000

+

11,000

50,000

−

39,000

=

11,000

4,500 NC