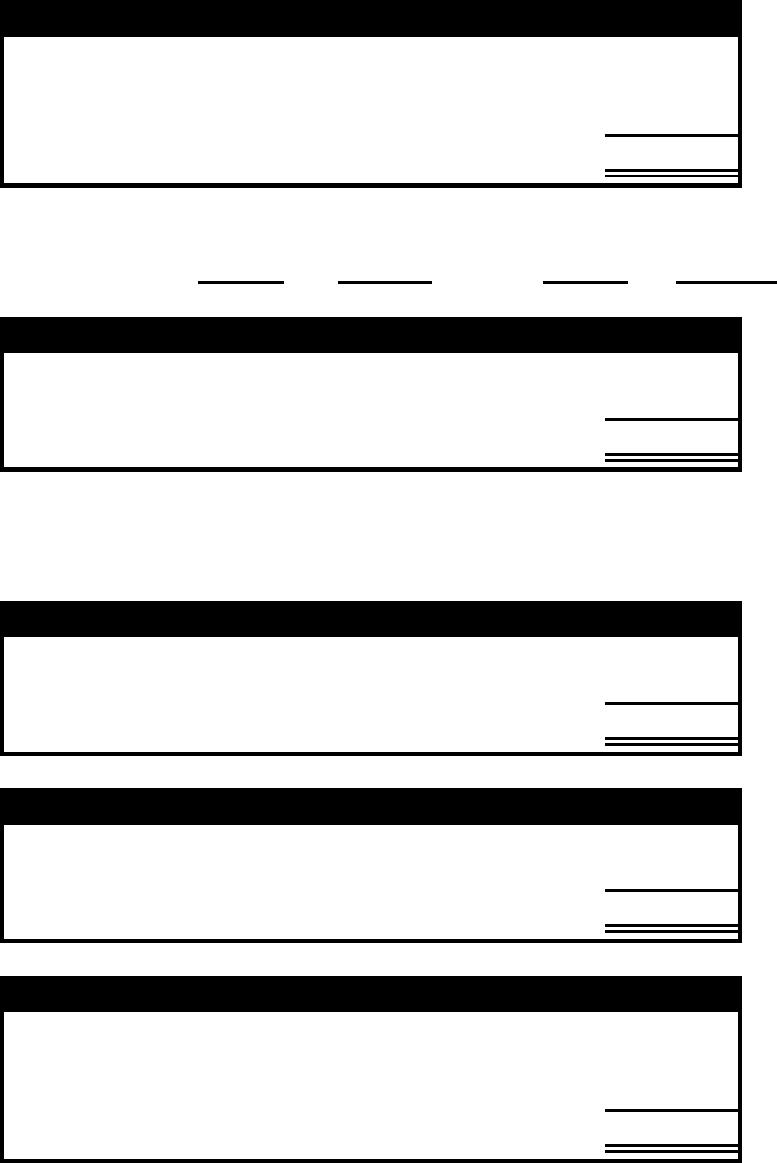

12–16

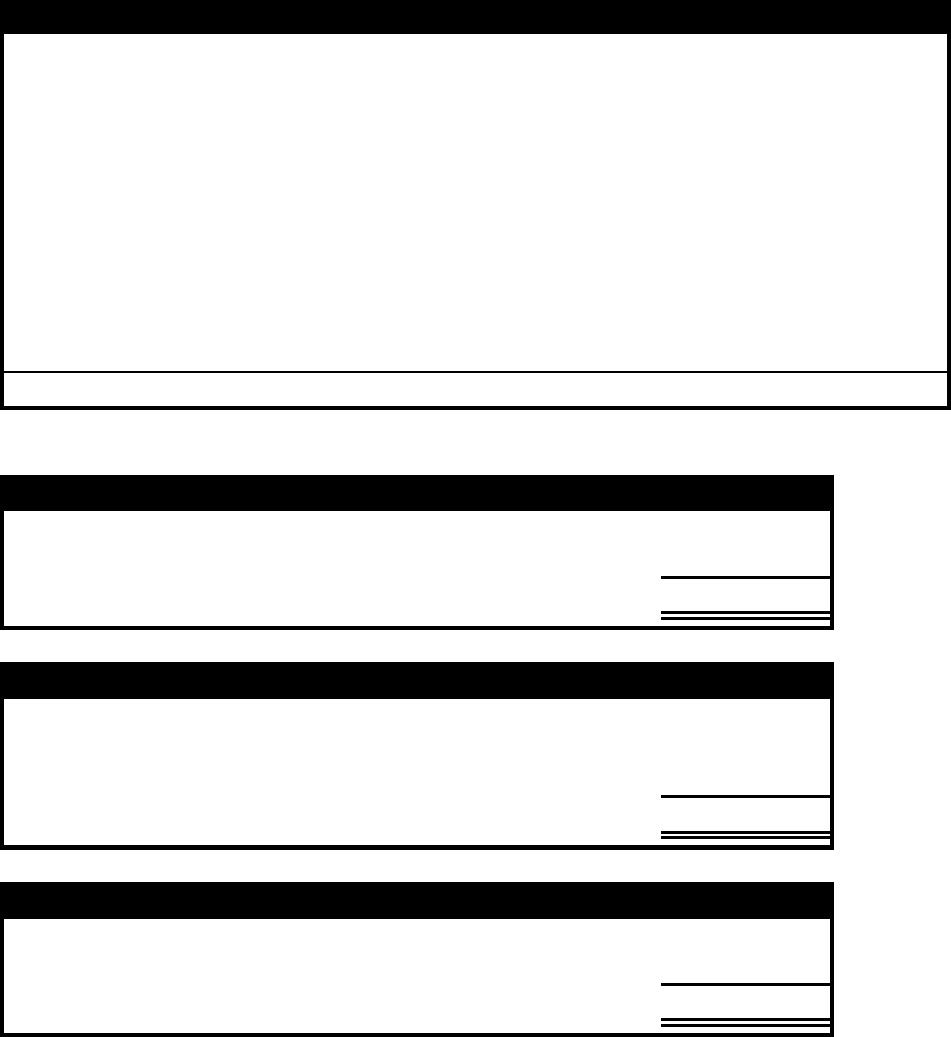

Demonstration Problem 12-1 Solution, part b., Direct Method

Cash Flows from Operating Activities

Rules provided for reference:

Rules for Computing Cash Flow from Operating Activities, Direct Method

Rule 1

Revenue, plus decreases, minus increases in related current

assets (accrued revenues)

Rule 2

Revenue, plus increases, minus decreases in related current

liabilities (unearned revenues)

Rule 3

Expense items, plus increases, minus decreases in related

current assets (prepaid expenses)

Rule 4

Expense items, minus increases, plus decreases in related

current liabilities (accrued expenses)

Rule 5

Ignore gains, losses, and noncash revenue and expense

items reported on the income statement

Equals

Net cash flow from operating activities

Cash Inflow from Revenue

Sales revenue

$98,000

Rule 1

Minus increase in accounts receivable

(1,000)

Cash inflow from revenue

$97,000

Cash Outflow for Inventory

Cost of goods sold

$62,000

Rule 3

Minus decrease in inventory

(4,000)

Rule 4

Minus increase in accounts payable

(2,000)

Cash outflow for inventory

$56,000

Cash Outflow for Salaries

Salaries expense

$14,000

Rule 4

Plus decrease in salaries payable

5,000

Cash outflow for salaries

$19,000

Cash flows from investing and financing activities are presented

the same way under both the indirect and direct methods.

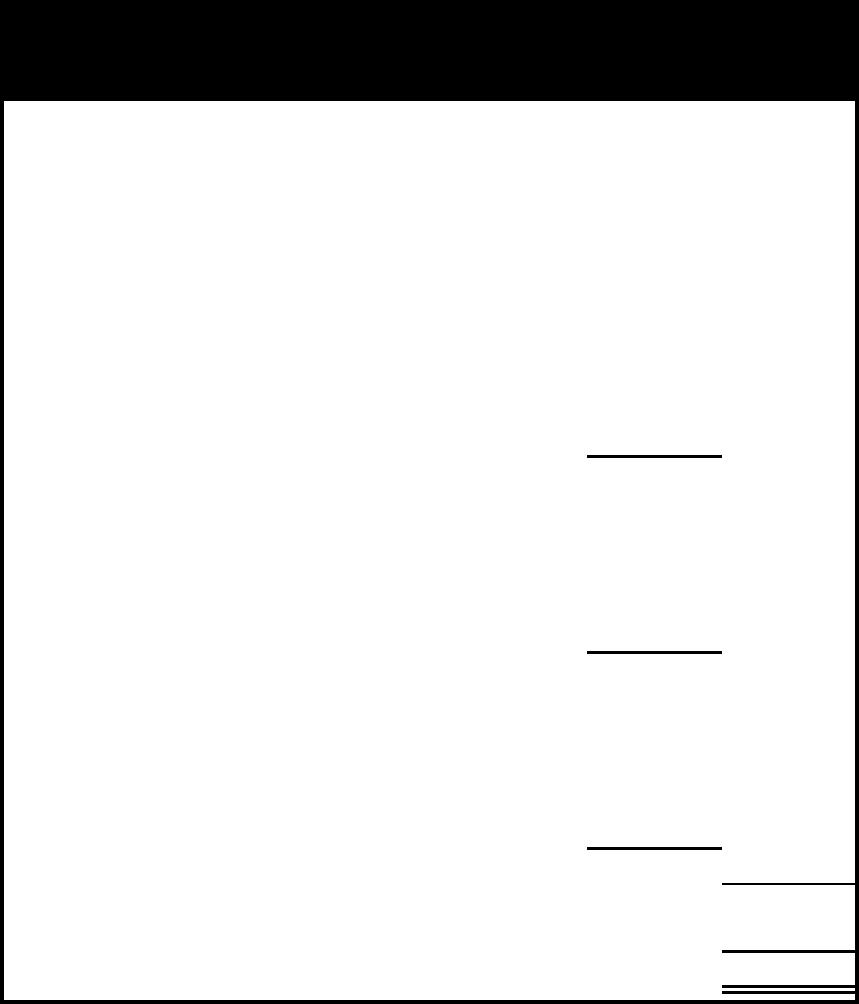

12–17

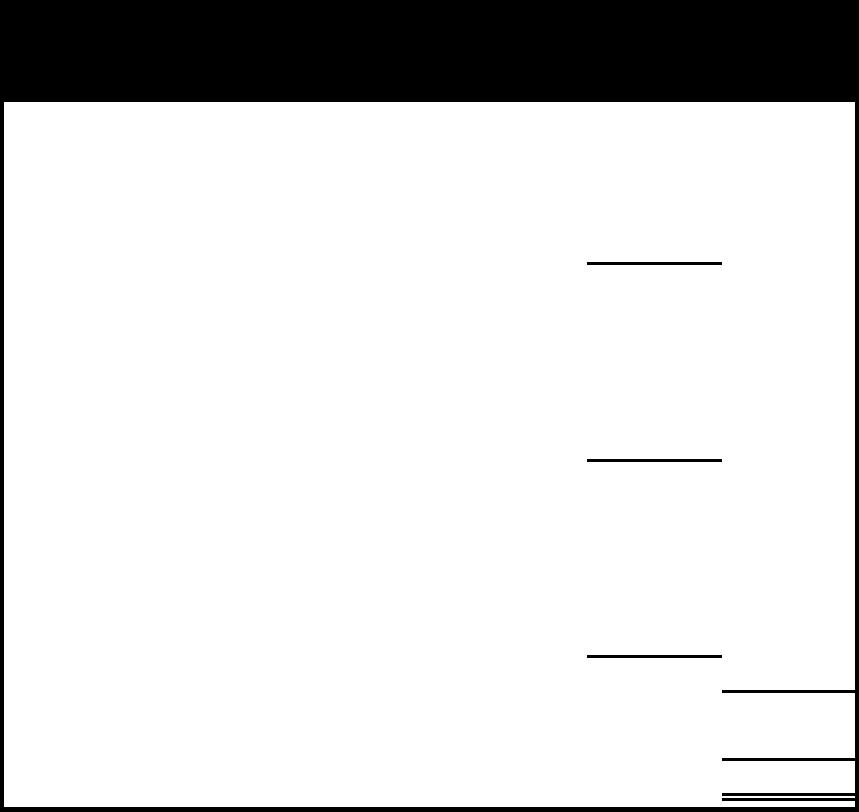

Demonstration Problem 12-1 Solution, part b. Direct Method

Hatch Company

Statement of Cash Flows

For the Year Ended December 31, 2016

Cash flows from operating activities

Cash inflow from revenue

$97,000

Cash outflow for inventory

(56,000)

Cash outflow for salaries expense

(19,000)

Net cash inflow from operating activities

$ 22,000

Cash flows from investing activities

Cash inflow from equipment sale

4,000

Cash outflow for equipment purchase

(9,000)

Cash outflow for land purchase

(14,000)

Net cash outflow for investing activities

(19,000)

Cash flows from financing activities

Cash inflow from stock issue

7,000

Cash outflow for debt payment

(6,000)

Cash payments for dividends

(5,000)

Net cash outflow for financing activities

(4,000)

Net decrease in cash

(1,000)

Beginning cash balance

2,000

Ending cash balance

$ 1,000

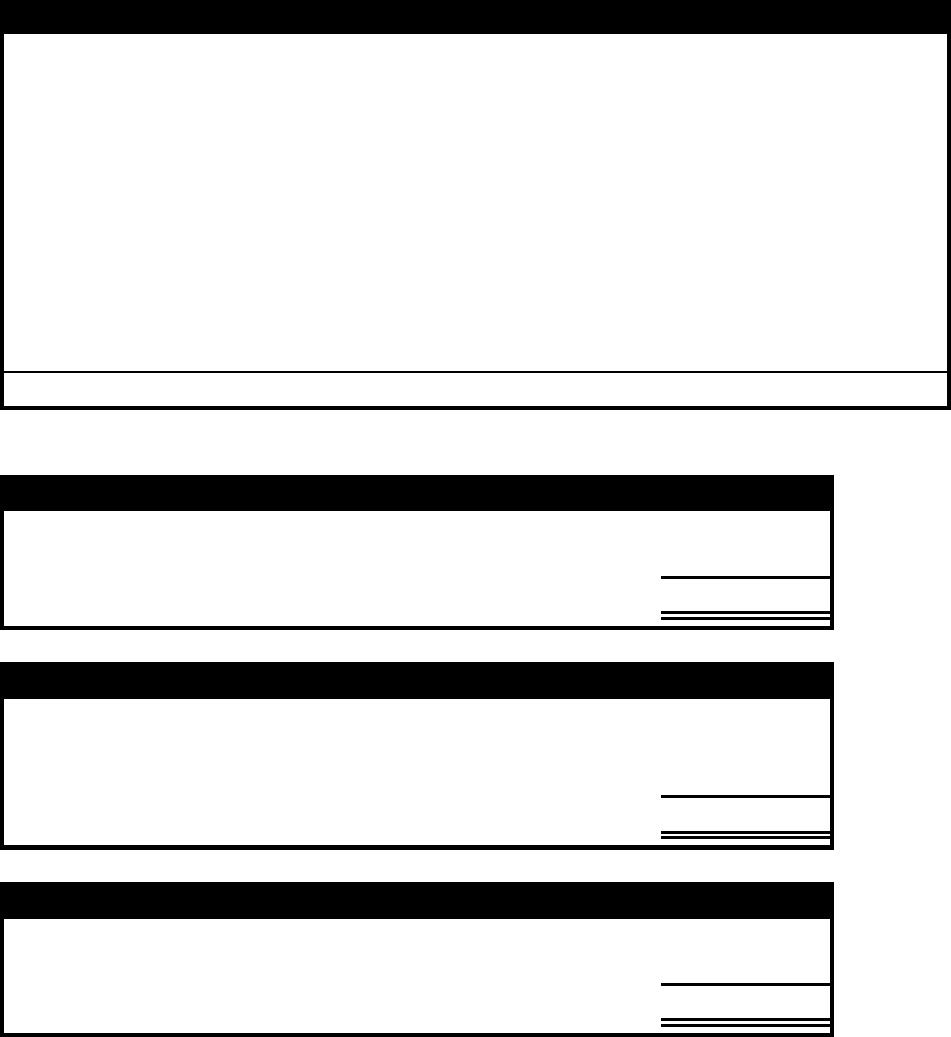

12–18

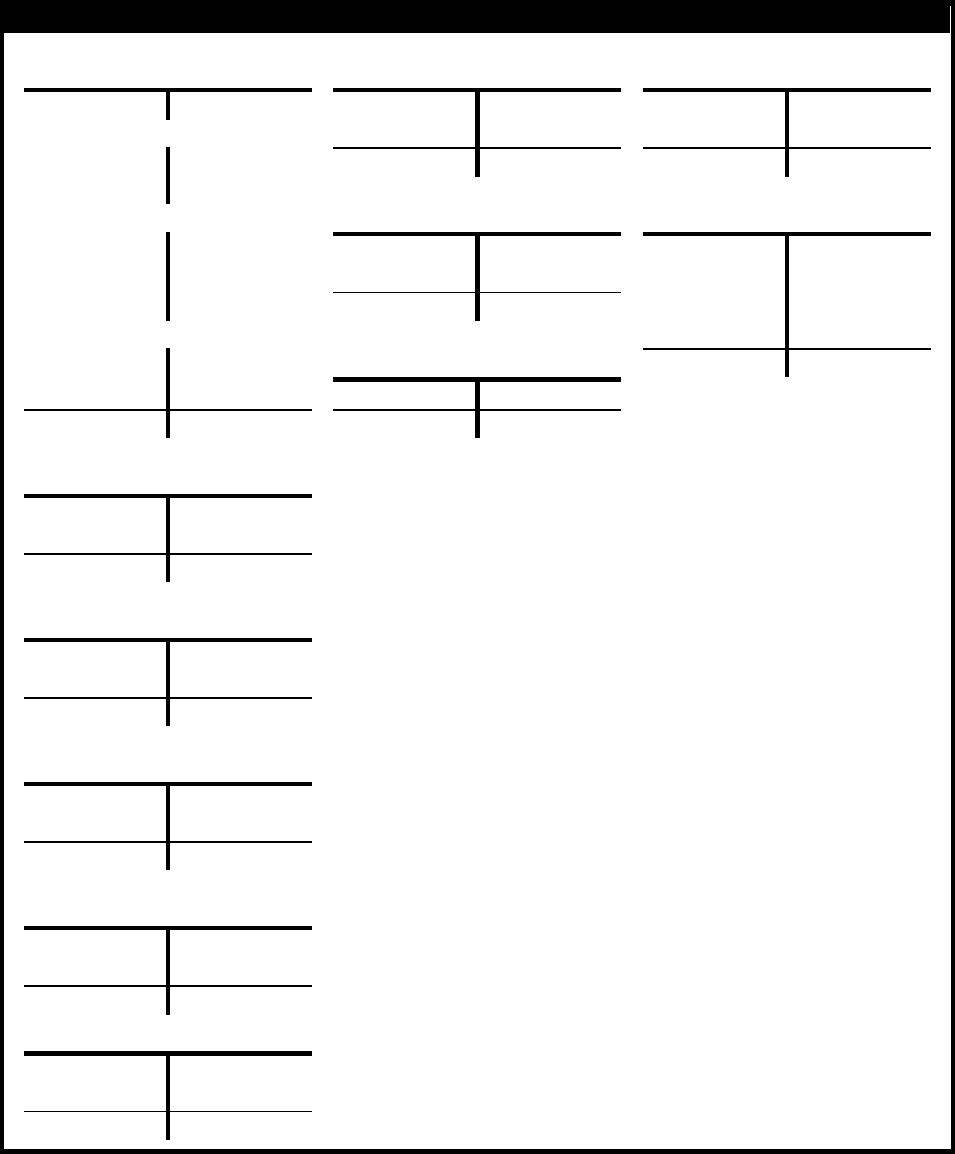

Demonstration Problem 12-1 Solution, part b. T-Account Approach,

Direct Method (Provided for Instructor Convenience)

T-Accounts

Cash

Accounts Payable

Common Stock

Bal. 2,000

(b3) 56,000

6,000 Bal.

18,000 Bal.

Operating Activities

58,000 (b2)

7,000 (g1)

(a2) 97,000

56,000 (b3)

8,000 Bal.

25,000 Bal.

19,000 (c2)

Investing Activities

Salaries Payable

Retained Earnings

(d2) 4,000

9,000 (d3)

(c2) 19,000

9,000 Bal.

(b1) 62,000

7,000 Bal.

14,000 (e1)

14,000 (c1)

(c1) 14,000

98,000 (a1)

4,000 Bal.

(d1) 10,000

3,000 (d2)

Financing Activities

(h1) 5,000

(g1) 7,000

6,000 (f1)

Notes Payable

17,000 Bal.

5,000 (h1)

(f1) 6,000

20,000 Bal.

Bal. 1,000

14,000 Bal.

Accounts Receivable

Bal. 8,000

97,000 (a2)

(a1) 98,000

Bal. 9,000

Merchandise Inventory

Bal. 20,000

62,000 (b1)

(b2) 58,000

Bal. 16,000

Equipment

Bal. 27,000

6,000 (d2)

(d3) 9,000

Bal. 30,000

Accumulated Dep.

(d2) 5,000

12,000 Bal.

10,000 (d1)

17,000 Bal.

Land

Bal. 15,000

(e1) 14,000

Bal. 29,000

12–19

Demonstration Problem 12-1 Workpaper, part a.1. Indirect Method,

Cash Flows from Operating Activities

Rules provided for reference:

Rules for Converting Net Income to Cash Flow from Operating Activities

Net Income ±

Rule 1

Add decreases and subtract increases in current assets

Rule 2

Add increases and subtract decreases in current liabilities

Rule 3

Add noncash expenses

Rule 4

Add losses, subtract gains

Equals

Net cash flow from operating activities

Noncash Current Asset and Current Liability Account Balances

Account Title

2016

2015

Change

Cash flows from Operating Activities

Net income

$

RULE

Add:

Rule 1

Rule 2

Rule 3

Subtract:

Rule 1

Rule 2

Rule 4

Net cash inflow from operating activities

$ 22,000

12–20

Demonstration Problem 12-1 Workpaper, part a.2. Indirect Method,

Cash Flows from Investing Activities

Equipment Account Information

Beginning balance in equipment

Add: Purchase of equipment (cash outflow)

Deduct: Sale of equipment (cash inflow)*

Ending balance in equipment

*Cash inflow for equipment sale:

Book value of equipment sold + gain

($ – $ ) + $ = $

Land Account Information

Beginning balance in land

Add: Purchases of land (cash outflow)

Ending balance in land

Demonstration Problem 12-1 Workpaper, part a.3. Indirect Method,

Cash Flows from Financing Activities

Notes Payable Account Information

Beginning balance in notes payable

Deduct: debt repayment (cash outflow)

Ending balance in notes payable

Common Stock Account Information

Beginning balance in common stock

Add: common stock issued (cash inflow)

Ending balance in common stock

Retained Earnings Account Information

Beginning balance in retained earnings

Add: Net income

Deduct: Dividends (cash outflow)

Ending balance in retained earnings

12–21

Demonstration Problem 12-1 Workpaper, part a.4. Indirect Method,

Statement of Cash Flows

Hatch Company

Statement of Cash Flows

For the Year Ended December 31, 2016

Cash flows from operating activities

Net income

$

Add:

Decrease in inventory

Increase in accounts payable

Depreciation expense (noncash)

Subtract:

Increase in accounts receivable

Decrease in salaries payable

Gain on sale of equipment (noncash)

Net cash inflow from operating activities

$

Cash flows from investing activities

Cash inflow from equipment sale

Cash outflow for equipment purchase

Cash outflow for land purchase

Net cash outflow for investing activities

Cash flows from financing activities

Cash inflow from stock issue

Cash outflow for debt payment

Cash payments for dividends

Net cash outflow for financing activities

Net decrease in cash

(1,000)

Beginning cash balance

Ending cash balance

$ 1,000

12–22

Demonstration Problem 12-1 Workpaper, part b., Direct Method

Cash Flows from Operating Activities

Rules provided for reference:

Rules for Computing Cash Flow from Operating Activities, Direct Method

Rule 1

Revenue, plus decreases, minus increases in related current

assets (accrued revenues)

Rule 2

Revenue, plus increases, minus decreases in related current

liabilities (unearned revenues)

Rule 3

Expense items, plus increases, minus decreases in related

current assets (prepaid expenses)

Rule 4

Expense items, minus increases, plus decreases in related

current liabilities (accrued expenses)

Rule 5

Ignore gains, losses, and noncash revenue and expense

items reported on the income statement

Equals

Net cash flow from operating activities

Cash Inflow from Revenue

Sales revenue

Rule 1

Cash inflow from revenue

Cash Outflow for Inventory

Cost of goods sold

Rule 3

Rule 4

Cash outflow for inventory

Cash Outflow for Salaries

Salaries expense

Rule 4

Cash outflow for salaries

Cash flows from investing and financing activities are presented

the same way under both the indirect and direct methods.

12–23

Demonstration Problem 12-1 Workpaper, part b. Direct Method

Hatch Company

Statement of Cash Flows

For the Year Ended December 31, 2016

Cash flows from operating activities

Cash inflow from revenue

$

Cash outflow for inventory

Cash outflow for salaries expense

Net cash inflow from operating activities

$

Cash flows from investing activities

Cash inflow from equipment sale

Cash outflow for equipment purchase

Cash outflow for land purchase

Net cash outflow for investing activities

Cash flows from financing activities

Cash inflow from stock issue

Cash outflow for debt payment

Cash payments for dividends

Net cash outflow for financing activities

Net decrease in cash

(1,000)

Beginning cash balance

Ending cash balance

$ 1,000

12–24

Demonstration Problem 12-1 Workpaper, part b. T-Account Approach,

Direct Method (Provided for Instructor Convenience)

T-Accounts

Cash

Accounts Payable

Common Stock

Bal. 2,000

Operating Activities

Investing Activities

Salaries Payable

Retained Earnings

Financing Activities

Notes Payable

Bal. 1,000

Accounts Receivable

Merchandise Inventory

Equipment

Accumulated Dep.

Land

12–25

Quiz Questions for Chapter 12

Use the following information to answer the next three questions.

Comparative Balance Sheets, December 31

2016

2015

Cash

$ 200

$ 500

Accounts receivable

2,200

4,000

Prepaid rent

3,000

1,000

Inventory

8,000

5,000

Land

19,000

13,000

Total assets

$32,400

$23,500

Accounts payable

$12,000

$ 6,500

Note payable

7,000

10,000

Common stock

6,400

1,500

Retained earnings

7,000

5,500

Total equity

$32,400

$23,500

Income Statement for 2016

Sales revenue

$ 20,000

Cost of goods sold

(15,200)

Gross margin

4,800

Rent expense

(1,000)

Net income

$ 3,800

1. The amount of net cash flow from operating activities for 2016 was

a. $6,100.

b. $9,100.

c. $ 600.

d. $18,800.

2. The amount of net cash flow from investing activities for 2016 was

a. $(9,000).

b. $(1,000).

c. $(4,000).

d. $(6,000).

3. The amount of net cash flow from financing activities for 2016 was

a. $(5,300).

b. $(400).

c. $(4,900).

d. $2,300.

12–26

4. Which of the following statements is true regarding preparing the statement of cash flows?

a. The information needed to prepare the statement of cash flows can be obtained from last year’s bal-

ance sheet and comparative income statements.

b. Revenue and expense accounts are most important in determining cash flows from financing activi-

ties.

c. Long-term asset accounts are used to determine cash flows from investing activities.

d. Cash paid for inventory is classified as an investing activities cash outflow.

5. Which of the following cash transactions is classified as an investing activity on the statement of cash

flows?

a. Cash borrowed.

b. Cash received from issuing stock.

c. Cash collected on a loan.

d. Cash received from revenue.

6. Jackson Hole, Inc. owns equipment that cost $25,000. The equipment has a four-year useful life and a

$5,000 salvage value. Assuming the company uses straight-line depreciation, the amount of deprecia-

tion expense that would appear each year on the statement of cash flows presented using the direct meth-

od would be

a. zero.

b. a $6,250 cash outflow under operating activities.

c. a $5,000 cash outflow under investing activities.

d. a $5,000 cash outflow under operating activities.

7. A building costing $55,000 with $16,500 of accumulated depreciation was sold for $40,000. How would

the cash flow from the sale appear on the statement of cash flows?

a. $1,500 in operating activities and $38,500 in investing activities.

b. $40,000 in investing activities.

c. $38,500 noncash financing and investing activities and $1,500 in operating activities.

d. $40,000 in financing activities.

8. The owners of X Company invested $2,000 in the company. X Company used the cash to invest in Y

Company. On X’s statement of cash flows these transactions would be classified, respectively, as

a. an investing activity and an investing activity.

b. a financing activity and a financing activity.

c. a financing activity and an investing activity.

d. an investing activity and a financing activity.

9. Issuing a note for the purchase of land is an example of

a. an investing activity.

b. a financing activity.

c. a noncash investing and financing activity.

d. a transaction that would not appear on the statement of cash flows.

10. The sum of the three major components (operating activities, investing activities, and financing activi-

ties) on a statement of cash flows will add up to

a. the change in the Cash account balance between the beginning and ending of the period.

b. the ending cash balance.

c. the amount of cash inflow for the period.

d. net income for the period.

12–27

Quiz Answers

Question

Answer

1

A

2

D

3

B

4

C

5

C

6

A

7

B

8

C

9

C

10

A

12–28

Summary Outline of a Lesson Plan for Chapter 12

I. Explain accrual to cash conversions. First teach students to identify the relation-

ships between cash flows and changes in balance sheet accounts.

A. Purchase of land.

B. Convert a simple direct method example of cash flows from operating activities to

the indirect method.

C. Explain the general rules for converting net income to cash flows from operating

activities.

II. Use financial statements as the source of data for preparing the statement of

cash flowsÄindirect method. Use Demonstration Problem 12-1 to illustrate using

comparative balance sheets and an income statement as the source of data. Have stu-

dents begin by identifying changes in current asset and current liability accounts, then

using the rules to obtain cash flows from operating activities. Explain changes in the

remaining balance sheet items and prepare a formal statement of cash flows.

III. Reconstruct the statement of cash flows using the direct method (appendix).

Again use Demonstration Problem 12-1. Illustrate presenting cash flows from op-

erating activities using the indirect method. Apply the rules for converting net in-

come to cash flow from operating activities:

Rule 1

Revenue plus decreases, minus increases in related current

assets (accrued revenues)

Rule 2

Revenue plus increases, minus decreases in related current

liabilities (unearned revenues)

Rule 3

Expense items plus increases, minus decreases in related

current assets (prepaid expenses)

Rule 4

Expense items minus increases, plus decreases in related

current liabilities (accrued expenses)

Rule 5

Ignore gains, losses, and noncash revenue and expense

items reported on the income statement

Equals

Net cash flow from operating activities

IV. Time considerations and homework assignments. Spend one hour introducing ac-

crual to cash conversions and the rules for converting net income to cash flows from

operating activities under the indirect method. It takes another hour to prepare the

complete statement of cash flows under the indirect method. Explaining the direct

method of presenting cash flows from operating activities takes thirty minutes. Prob-

lems 12-19A or 12-19B and 12-21A or 12-21B are similar to the demonstration prob-

lem. Although these problems specifically require either the direct or indirect method

of determining cash flow from operating activities, we suggest you instruct students

to work the operating activities sections of the problems you’ve assigned using both

the direct and indirect methods.

12–29

Summary Outline of an Alternate Lesson Plan for Chapter 12

(T-account Approach, Direct Method)

I. Use T-accounts to explain accrual to cash conversions. First teach students to

identify the relationships between cash flows and changes in balance sheet accounts.

Introduce relationships that are progressively more difficult.

A. Purchase of land.

B. Conversion of accrual-based revenue to cash received.

C. Determining cash paid for inventory.

II. Use financial statements as the source of data for preparing the statement of

cash flowsÄdirect method. Use Demonstration Problem 12-1 to illustrate using

comparative balance sheets and an income statement as the source of data for deriv-

ing the statement of cash flows. Have students begin the problem by opening T–

accounts for all the balance sheet items. Reconstruct the journal entries that recorded

income statement transactions. Explain changes in the remaining balance sheet items

and prepare a formal statement of cash flows.

III. Reconstruct the statement of cash flows using the indirect method. Reuse the da-

ta in Demonstration Problem 12-1 to illustrate presenting cash flows from operating

activities using the indirect method. Apply the rules for converting net income to

cash flow from operating activities:

Rule 1. Add decreases and subtract increases in current asset account balances.

Rule 2. Add increases and subtract decreases in current liability account balances.

Rule 3. Add noncash expenses to net income.

Rule 4. Add losses to net income and subtract gains from net income.

IV. Time considerations and homework assignments. Spend one hour of class time

introducing accrual to cash conversions. It takes another hour and a half to explain

the T-account analysis. Explaining the indirect method of presenting cash flows from

operating activities takes thirty minutes. Problems 12-19A or 12-19B and 12-21A or

12-21B are similar to the demonstration problem. Although these problems specifi-

cally require either the direct or indirect method of determining cash flow from oper-

ating activities, we suggest you instruct students to work the operating activities sec-

tions of the problems you’ve assigned using both the direct and indirect methods.