11–97

11–98

PROBLEM 11-19B (cont.)

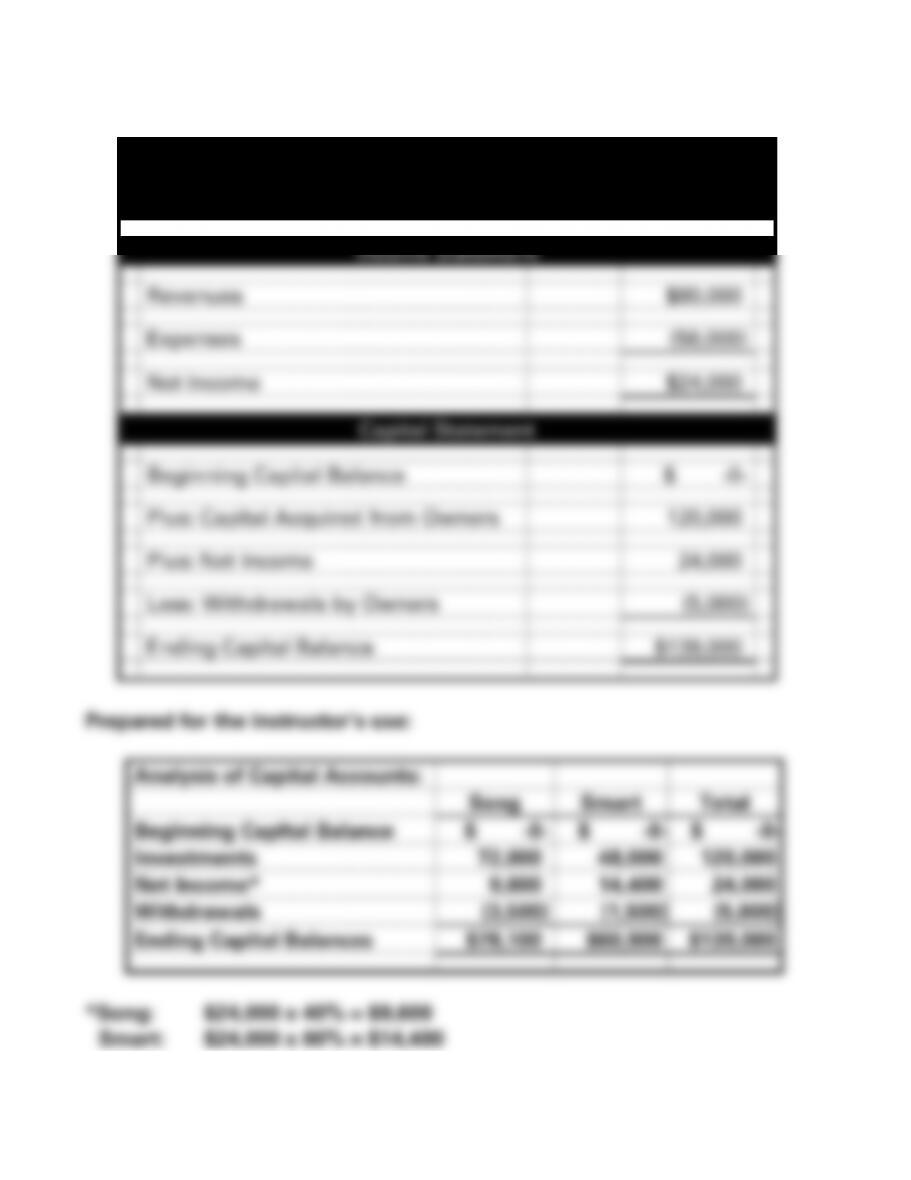

b. Partnership

Best Auto Parts Company

Financial Statements

For the Year Ended December 31, 2016

Income Statement

Revenues

$80,000

Expenses

(56,000)

Net Income

$24,000

Capital Statement

Beginning Capital Balance

$ -0-

Plus: Capital Acquired from Owners

120,000

Plus: Net Income

24,000

Less: Withdrawals by Owners

(5,000)

Ending Capital Balance

$139,000

Prepared for the instructor’s use:

Analysis of Capital Accounts:

Song

Smart

Total

Beginning Capital Balance

$ -0-

$ -0-

$ -0-

Investments

72,000

48,000

120,000

Net Income*

9,600

14,400

24,000

Withdrawals

(3,500)

(1,500)

(5,000)

Ending Capital Balances

$78,100

$60,900

$139,000

*Song: $24,000 x 40% = $9,600

Smart: $24,000 x 60% = $14,400

11–99

PROBLEM 11-19B b. (cont.)

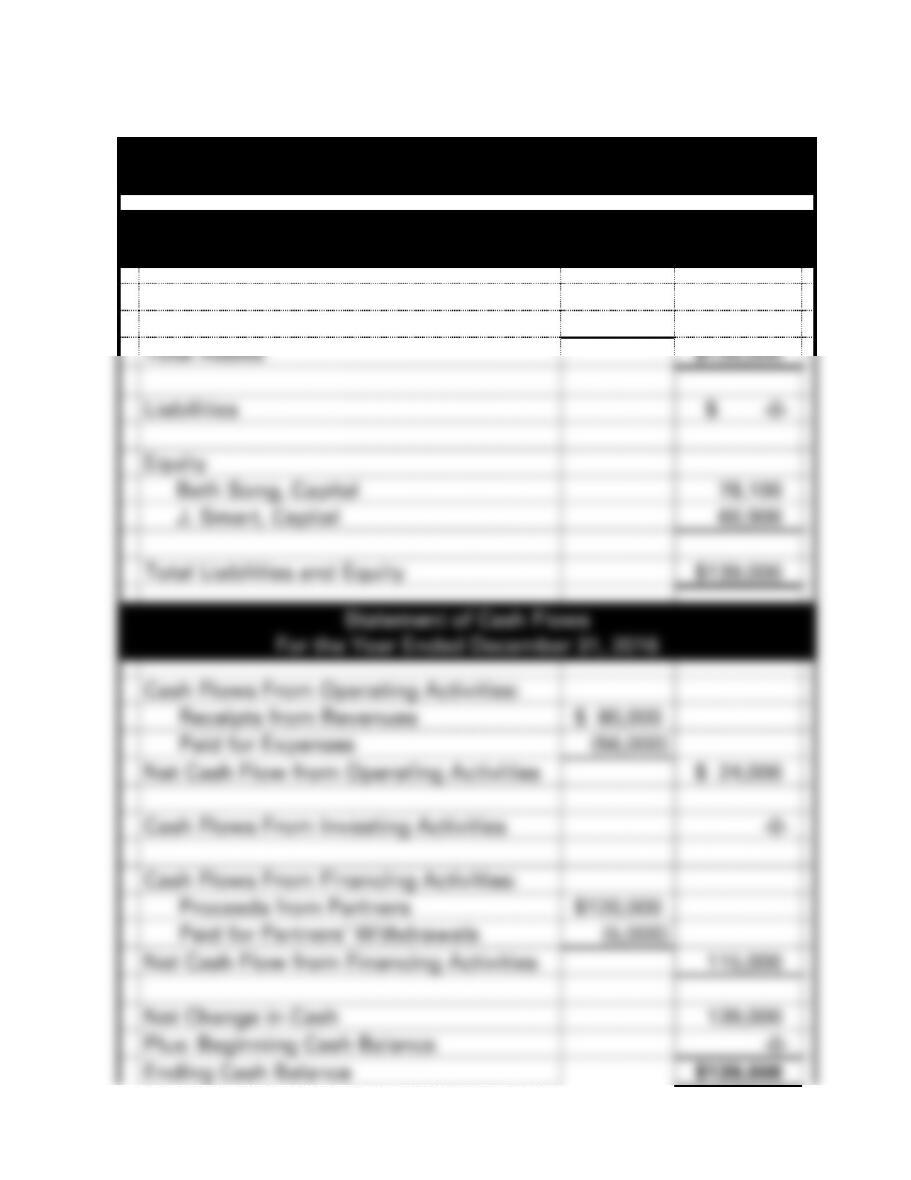

Best Auto Parts Company

Financial Statements

Balance Sheet

As of December 31, 2016

Assets

Cash

$139,000

Total Assets

$139,000

Liabilities

$ -0-

Equity

Beth Song, Capital

78,100

J. Smart, Capital

60,900

Total Liabilities and Equity

$139,000

Statement of Cash Flows

For the Year Ended December 31, 2016

Cash Flows From Operating Activities:

Receipts from Revenues

$ 80,000

Paid for Expenses

(56,000)

Net Cash Flow from Operating Activities

$ 24,000

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities:

Proceeds from Partners

$120,000

Paid for Partners’ Withdrawals

(5,000)

Net Cash Flow from Financing Activities

115,000

Net Change in Cash

139,000

Plus: Beginning Cash Balance

-0-

Ending Cash Balance

$139,000

11-100

11-101

PROBLEM 11-19B (cont.)

c. Corporation

Best Auto Parts Company

Financial Statements

For the Year Ended December 31, 2016

Income Statement

Revenues

$80,000

Expenses

(56,000)

Net Income

$24,000

Statement of Changes in Stockholders’ Equity

Beginning Common Stock

$ -0-

Plus: Issuance of Common Stock

120,000

Ending Common Stock

$120,000

Beginning Retained Earnings

-0-

Plus: Net Income

24,000

Less: Dividends

(5,000)

Ending Retained Earnings

19,000

Total Stockholders’ Equity

$139,000

11-102

PROBLEM 11-19B c. (cont.)

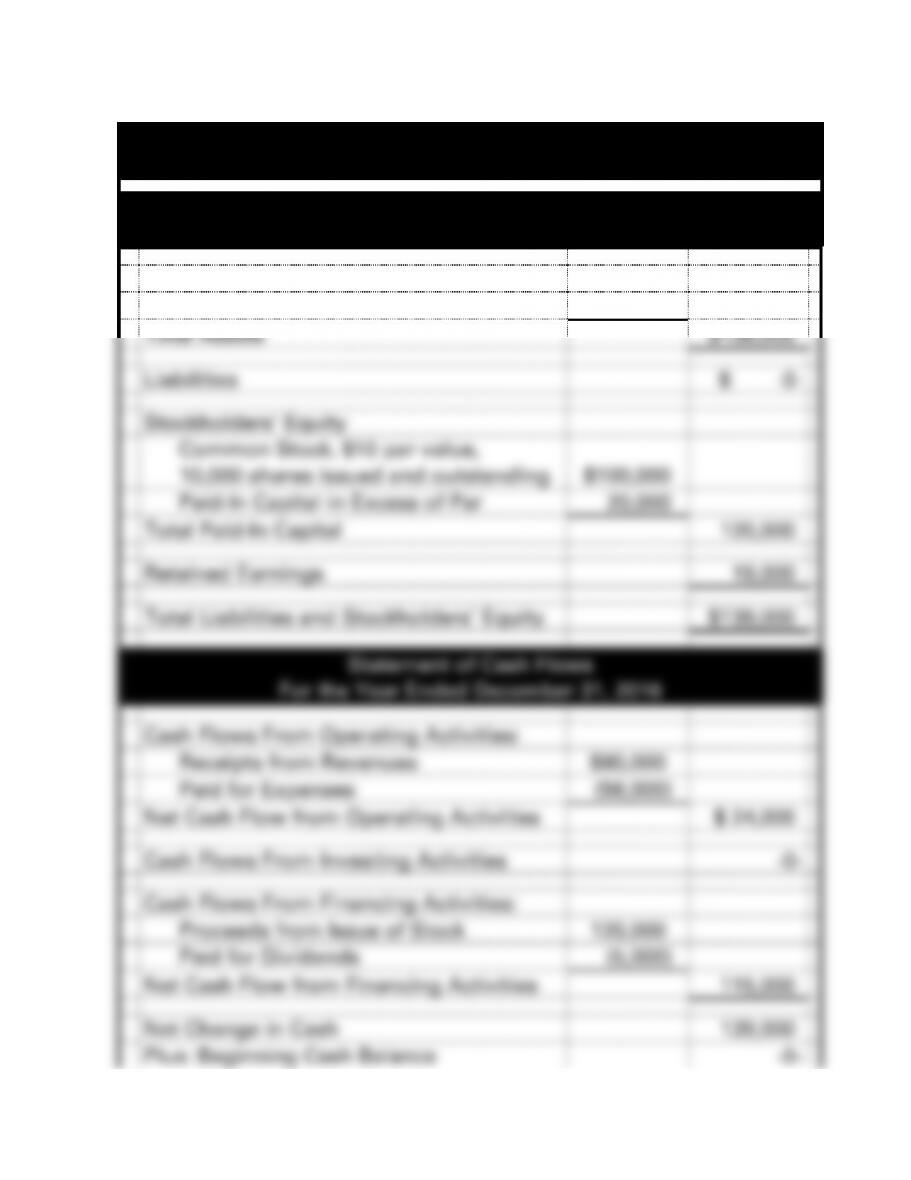

Best Auto Parts Company

Financial Statements

Balance Sheet

As of December 31, 2016

Assets

Cash

$139,000

Total Assets

$139,000

Liabilities

$ -0-

Stockholders’ Equity

Common Stock, $10 par value,

10,000 shares issued and outstanding

$100,000

Paid-In Capital in Excess of Par

20,000

Total Paid-In Capital

120,000

Retained Earnings

19,000

Total Liabilities and Stockholders’ Equity

$139,000

Statement of Cash Flows

For the Year Ended December 31, 2016

Cash Flows From Operating Activities:

Receipts from Revenues

$80,000

Paid for Expenses

(56,000)

Net Cash Flow from Operating Activities

$ 24,000

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities:

Proceeds from Issue of Stock

120,000

Paid for Dividends

(5,000)

Net Cash Flow from Financing Activities

115,000

Net Change in Cash

139,000

Plus: Beginning Cash Balance

-0-

11-103

Ending Cash Balance

$139,000

11-104

PROBLEM 11-20B

Note: This exercise can be used to assess writing skills. If a more

comprehensive answer is desired, this exercise can be assigned as a short

research project.

11-105

PROBLEM 11-21B

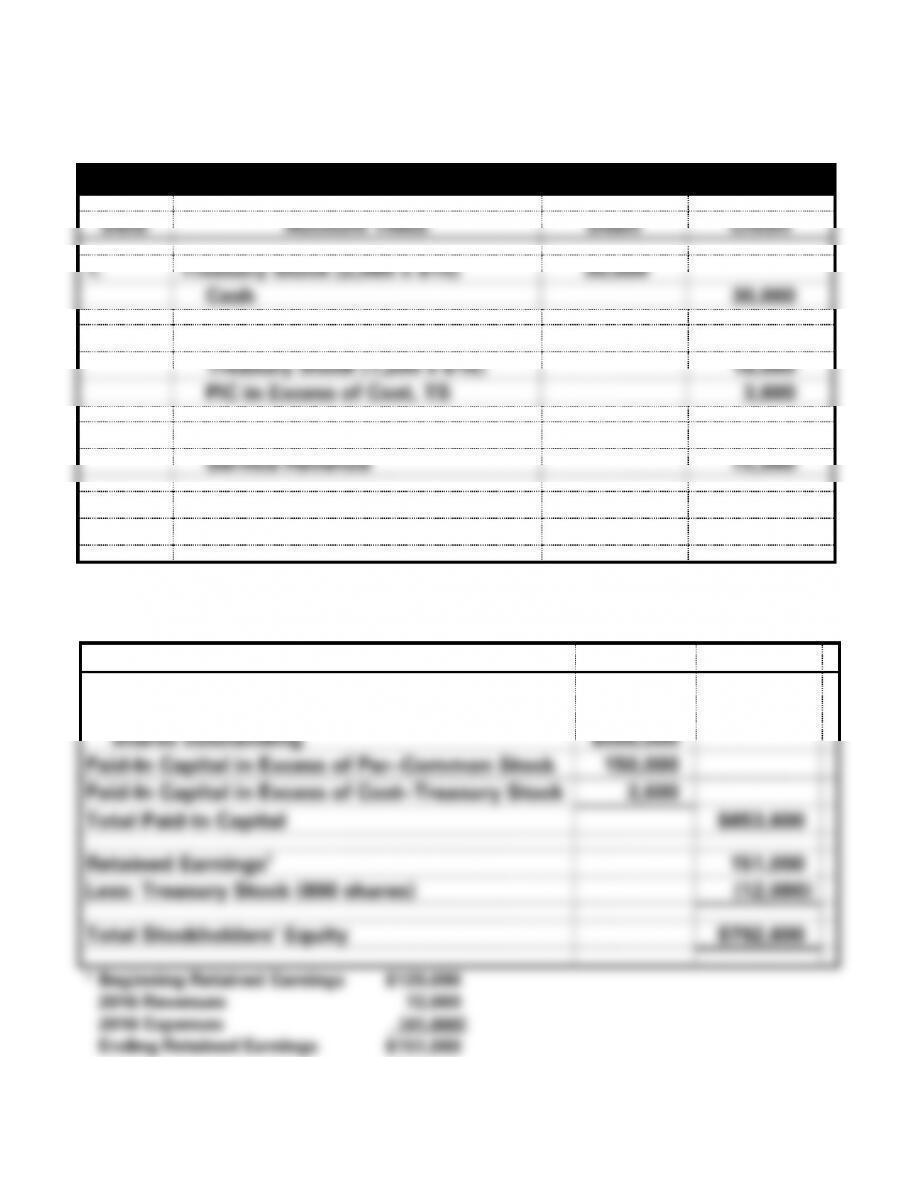

a.

Date

Account Titles

Debit

Credit

1.

Treasury Stock (2,000 x $15)

30,000

Cash

30,000

2.

Cash (1,200 x $18)

21,600

Treasury Stock (1,200 x $15)

18,000

PIC in Excess of Cost, TS

3,600

3.

Cash

72,000

Service Revenue

72,000

4.

Operating Expenses

41,000

Cash

41,000

b.

Stockholders’ Equity

Common Stock, $10 par value, 100,000 shares

authorized, 50,000 shares issued, and 49,200

shares outstanding

$500,000

Paid-In Capital in Excess of Par−Common Stock

150,000

Paid-In Capital in Excess of Cost−Treasury Stock

3,600

Total Paid-In Capital

$653,600

Retained Earnings1

151,000

Less: Treasury Stock (800 shares)

(12,000)

Total Stockholders’ Equity

$792,600

1 Beginning Retained Earnings $120,000

2016 Revenues 72,000

2016 Expenses (41,000)

Ending Retained Earnings $151,000

11-106

PROBLEM 11-22B

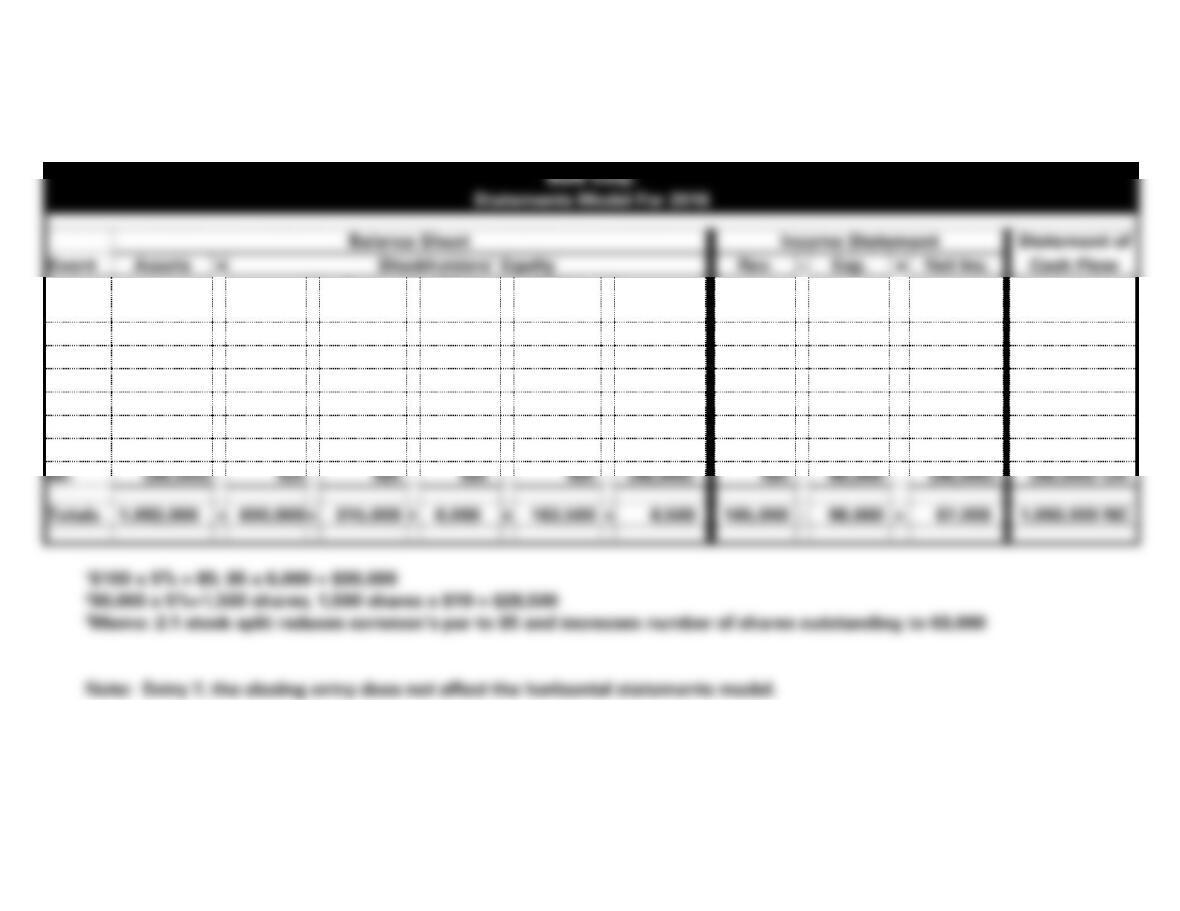

a. NC = Net Change in Cash

Burk Corp.

Statements Model For 2016

Balance Sheet

Income Statement

Statement of

Event

Assets

=

Stockholders’ Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

Pfd. Stk.

+

Com.

Stk.

+

PIC in

Exc. PS

+

PIC in

Exc. CS

+

Ret. Earn

1.

450,000

NA

300,000

NA

150,000

NA

NA

NA

NA

450,000 FA

2.

606,000

600,000

NA

6,000

NA

NA

NA

NA

NA

606,000 FA

3.

(30,000)1

NA

NA

NA

NA

(30,000)

NA

NA

NA

(30,000) FA

4.

NA

NA

15,000

NA

13,500

(28,500)2

NA

NA

NA

NA

5. memo

no entry3

NA

NA

NA

NA

NA

NA

NA

NA

NA

6a.

165,000

NA

NA

NA

NA

165,000

165,000

NA

165,000

165,000 OA

6b.

(98,000)

NA

NA

NA

NA

(98,000)

NA

98,000

(98,000)

(98,000) OA

Totals

1,093,000

=

600,000

+

315,000

+

6,000

+

163,500

+

8,500

165,000

−

98,000

=

67,000

1,093,000 NC

1$100 x 5% = $5; $5 x 6,000 = $30,000

230,000 x 5%=1,500 shares; 1,500 shares x $19 = $28,500

3Memo: 2:1 stock split reduces common’s par to $5 and increases number of shares outstanding to 63,000

Note: Entry 7, the closing entry does not affect the horizontal statements model.

11-107

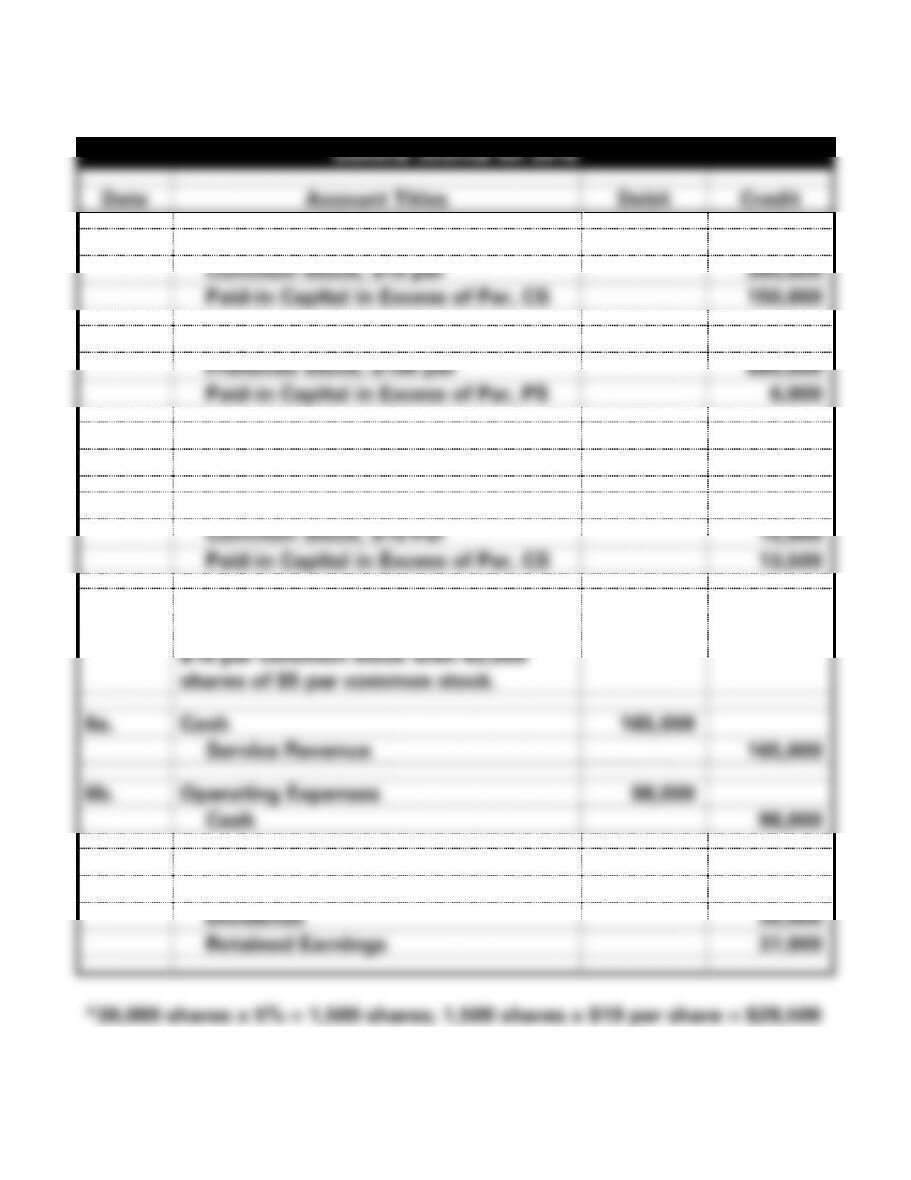

PROBLEM 11-22B (cont.)

b.

General Journal for 2016

Date

Account Titles

Debit

Credit

1.

Cash (30,000 x $15)

450,000

Common Stock, $10 par

300,000

Paid-in Capital in Excess of Par, CS

150,000

2.

Cash (6,000 x $101)

606,000

Preferred Stock, $100 par

600,000

Paid-in Capital in Excess of Par, PS

6,000

3.

Dividends ($100 x 5% x 6,000)

30,000

Cash

30,000

4.

Retained Earnings

28,500*

Common Stock, $10 Par

15,000

Paid-in Capital in Excess of Par, CS

13,500

5.

Concord’s declaration of a 2-for-1 stock

split will replace the 31,500 shares of

$10 par common stock with 63,000

shares of $5 par common stock.

6a.

Cash

165,000

Service Revenue

165,000

6b.

Operating Expenses

98,000

Cash

98,000

7.

Service Revenue

165,000

Operating Expenses

98,000

Dividends

30,000

Retained Earnings

37,000

11-108

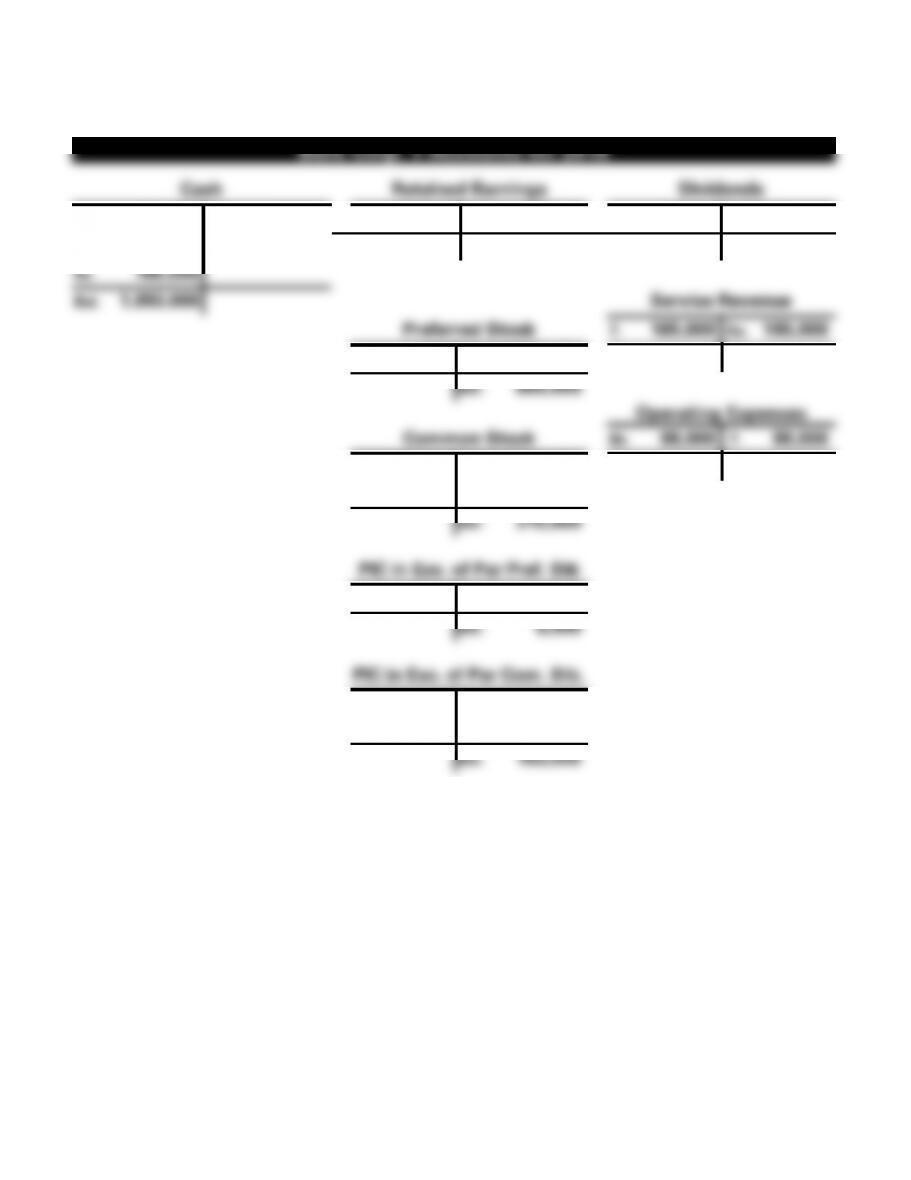

PROBLEM 11-22B b. (cont.)

Burk Corp. T-Accounts for 2016

Cash

Retained Earnings

Dividends

1. 450,000

3. 30,000

4. 28,500

7. 37,000

3. 30,000

7. 30,000

2. 606,000

6b. 98,000

Bal. 8,500

Bal. -0-

6a. 165,000

Bal. 1,093,000

Service Revenue

Preferred Stock

7. 165,000

6a. 165,000

2. 600,000

Bal. -0-

Bal. 600,000

Operating Expenses

Common Stock

6b. 98,000

7. 98,000

1. 300,000

Bal. -0-

4. 15,000

Bal. 315,000

PIC in Exc. of Par Pref. Stk

2. 6,000

Bal. 6,000

PIC in Exc. of Par Com. Stk.

1. 150,000

4. 13,500

Bal. 163,500

11-109

PROBLEM 11-22B (cont.)

c.

Burk Corp.

December 31, 2016

Stockholders’ Equity

Preferred Stock, $100 par value, 5%, 6,000

shares issued and outstanding

$600,000

Common Stock, $5, par, 63,000 shares issued

and outstanding

315,000

Paid-In Capital in Excess of Par, Preferred

Stock

6,000

Paid-In Capital in Excess of Par, Common Stock

163,500

Total Paid-In Capital

$1,084,500

Retained Earnings

8,500

Total Stockholders’ Equity

$1,093,000

11-110

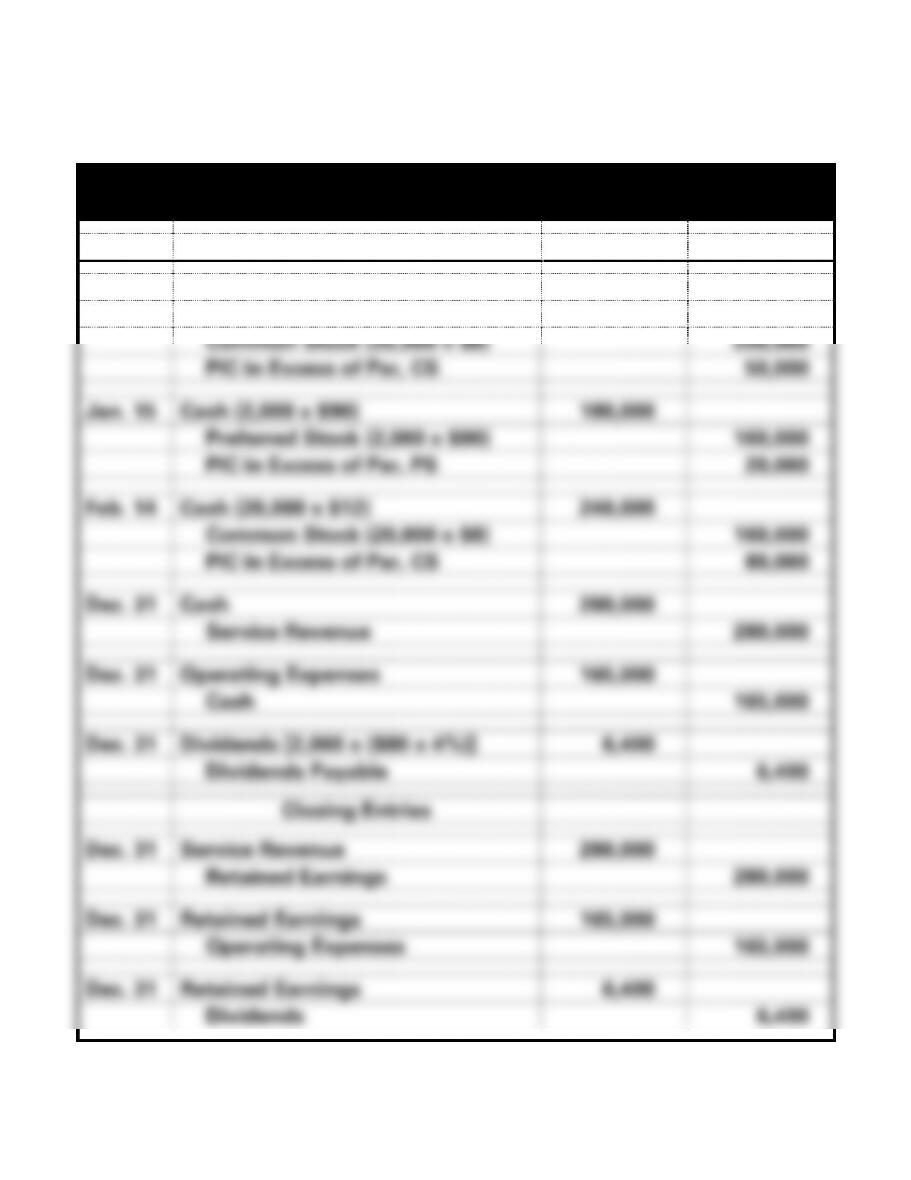

PROBEM 11-23B

a.

Edgar Corporation

General Journal

Date

Account Titles

Debit

Credit

2016

Jan. 2

Cash (25,000 x $10)

250,000

Common Stock (25,000 x $8)

200,000

PIC in Excess of Par, CS

50,000

Jan. 15

Cash (2,000 x $90)

180,000

Preferred Stock (2,000 x $80)

160,000

PIC in Excess of Par, PS

20,000

Feb. 14

Cash (20,000 x $12)

240,000

Common Stock (20,000 x $8)

160,000

PIC in Excess of Par, CS

80,000

Dec. 31

Cash

280,000

Service Revenue

280,000

Dec. 31

Operating Expenses

165,000

Cash

165,000

Dec. 31

Dividends [2,000 x ($80 x 4%)]

6,400

Dividends Payable

6,400

Closing Entries

Dec. 31

Service Revenue

280,000

Retained Earnings

280,000

Dec. 31

Retained Earnings

165,000

Operating Expenses

165,000

Dec. 31

Retained Earnings

6,400

Dividends

6,400

11-111

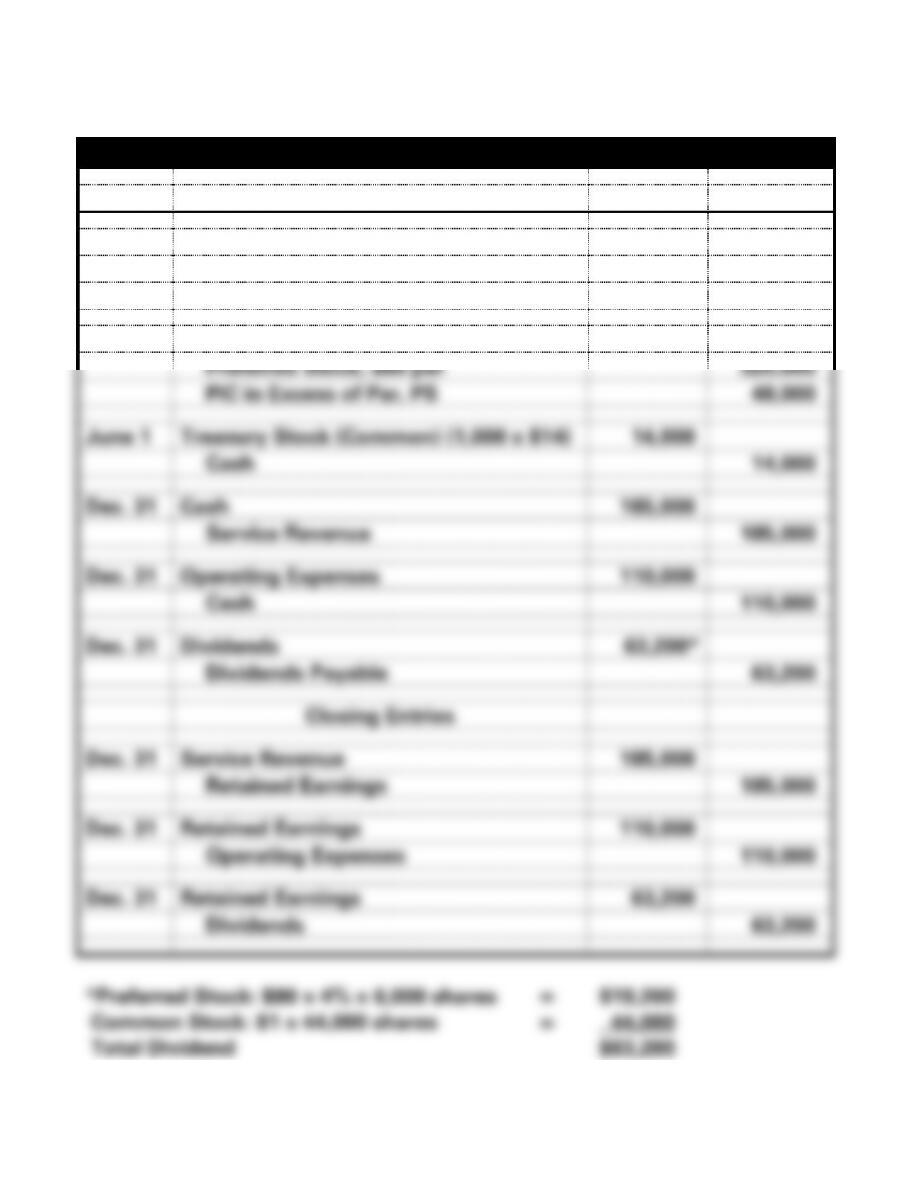

PROBLEM 11-23B a. (cont.)

Edgar Corporation General Journal

Date

Account Titles

Debit

Credit

2017

Jan. 31

Dividends Payable

6,400

Cash

6,400

Mar. 1

Cash (4,000 x $92)

368,000

Preferred Stock, $80 par

320,000

PIC in Excess of Par, PS

48,000

June 1

Treasury Stock (Common) (1,000 x $14)

14,000

Cash

14,000

Dec. 31

Cash

185,000

Service Revenue

185,000

Dec. 31

Operating Expenses

110,000

Cash

110,000

Dec. 31

Dividends

63,200*

Dividends Payable

63,200

Closing Entries

Dec. 31

Service Revenue

185,000

Retained Earnings

185,000

Dec. 31

Retained Earnings

110,000

Operating Expenses

110,000

Dec. 31

Retained Earnings

63,200

Dividends

63,200

11-112

PROBLEM 11-23B a. (cont.)

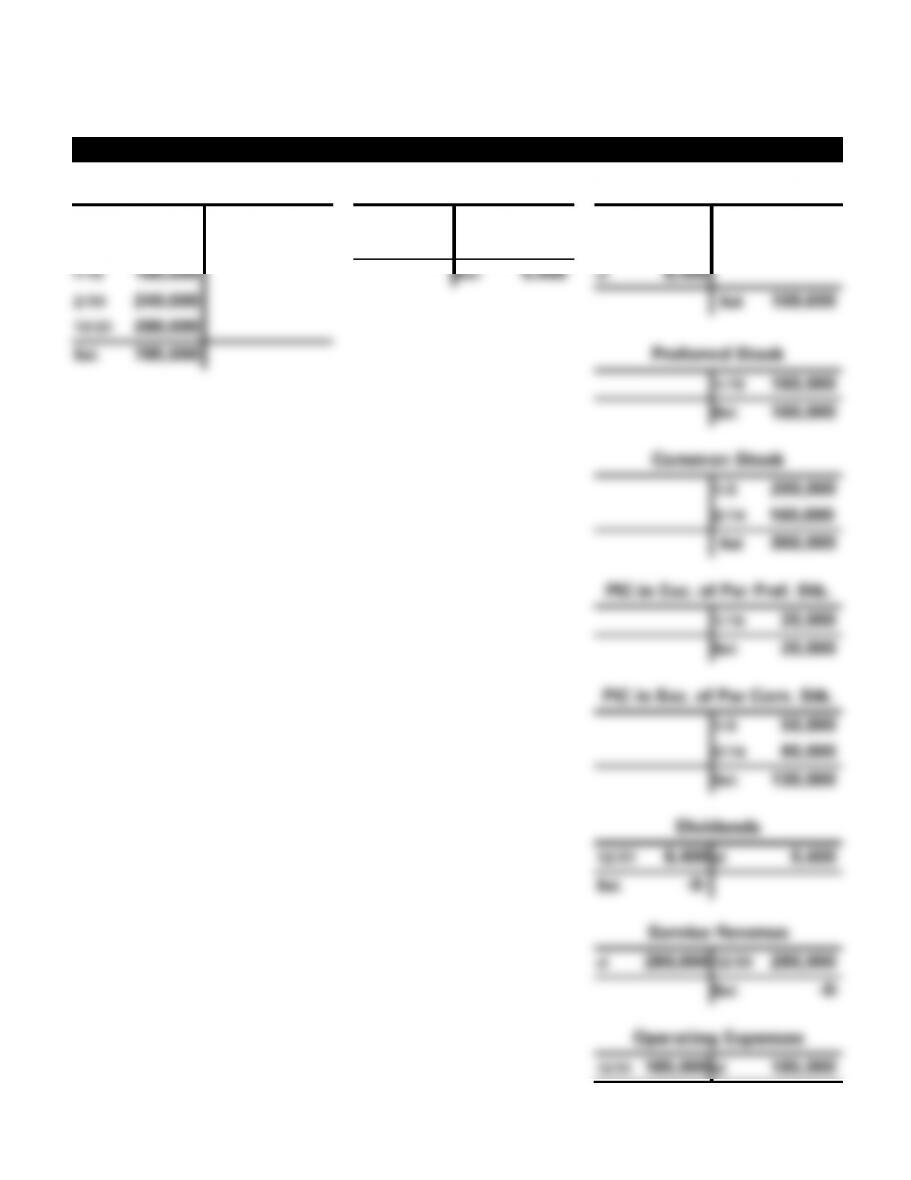

Edgar Corporation T-Accounts for 2016

Cash

Dividends Payable

Retained Earnings

2016

2016

2016

1/2 250,000

12/31 165,000

12/31 6,400

cl 165,000

cl 280,000

1/15 180,000

Bal. 6,400

cl 6,400

2/14 240,000

Bal. 108,600

12/31 280,000

Bal. 785,000

Preferred Stock

1/15 160,000

Bal. 160,000

Common Stock

1/2 200,000

2/14 160,000

Bal. 360,000

PIC in Exc. of Par Pref. Stk.

1/15 20,000

Bal. 20,000

PIC in Exc. of Par Com. Stk.

1/2 50,000

2/14 80,000

Bal. 130,000

Dividends

12/31 6,400

cl 6,400

Bal. -0-

Service Revenue

cl 280,000

12/31 280,000

Bal. -0-

Operating Expenses

12/31 165,000

cl 165,000

11-113

Bal. -0-

11-114

PROBLEM 11-23B a. (cont.)

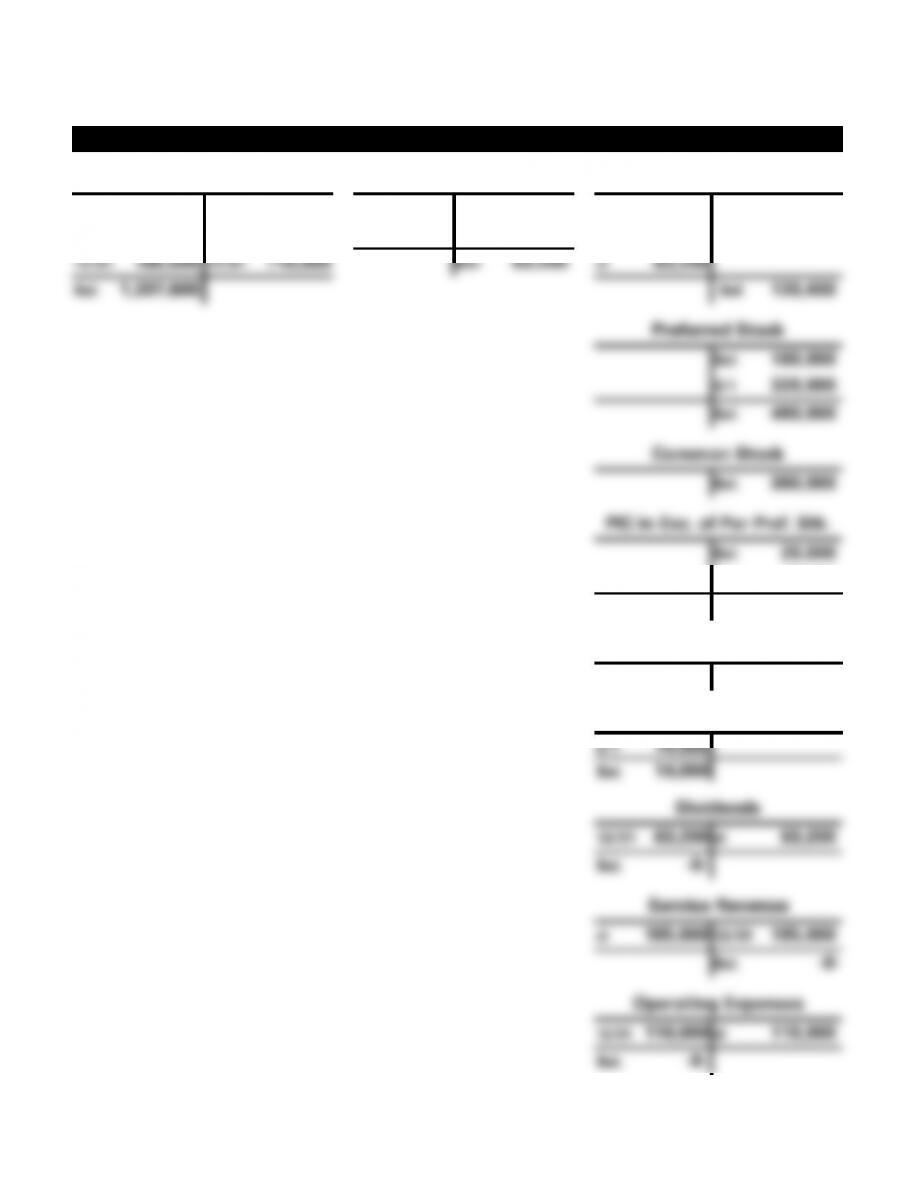

Edgar Corporation T-Accounts for 2017

Cash

Dividends Payable

Retained Earnings

Bal. 785,000

1/31 6,400

Bal. 6,400

Bal. 108,600

3/1 368,000

6/1 14,000

1/31 6,400

12/31 63,200

cl 110,000

cl 185,000

12/31 185,000

12/31 110,000

Bal. 63,200

cl 63,200

Bal. 1,207,600

Bal. 120,400

Preferred Stock

Bal. 160,000

3/1 320,000

Bal. 480,000

Common Stock

Bal. 360,000

PIC in Exc. of Par Pref. Stk.

Bal. 20,000

3/1 48,000

Bal. 68,000

PIC in Exc. of Par Com. Stk.

Bal. 130,000

Treasury Stock

6/1 14,000

Bal. 14,000

Dividends

12/31 63,200

cl 63,200

Bal. -0-

Service Revenue

cl 185,000

12/31 185,000

Bal. -0-

Operating Expenses

12/31 110,000

cl 110,000

Bal. -0-

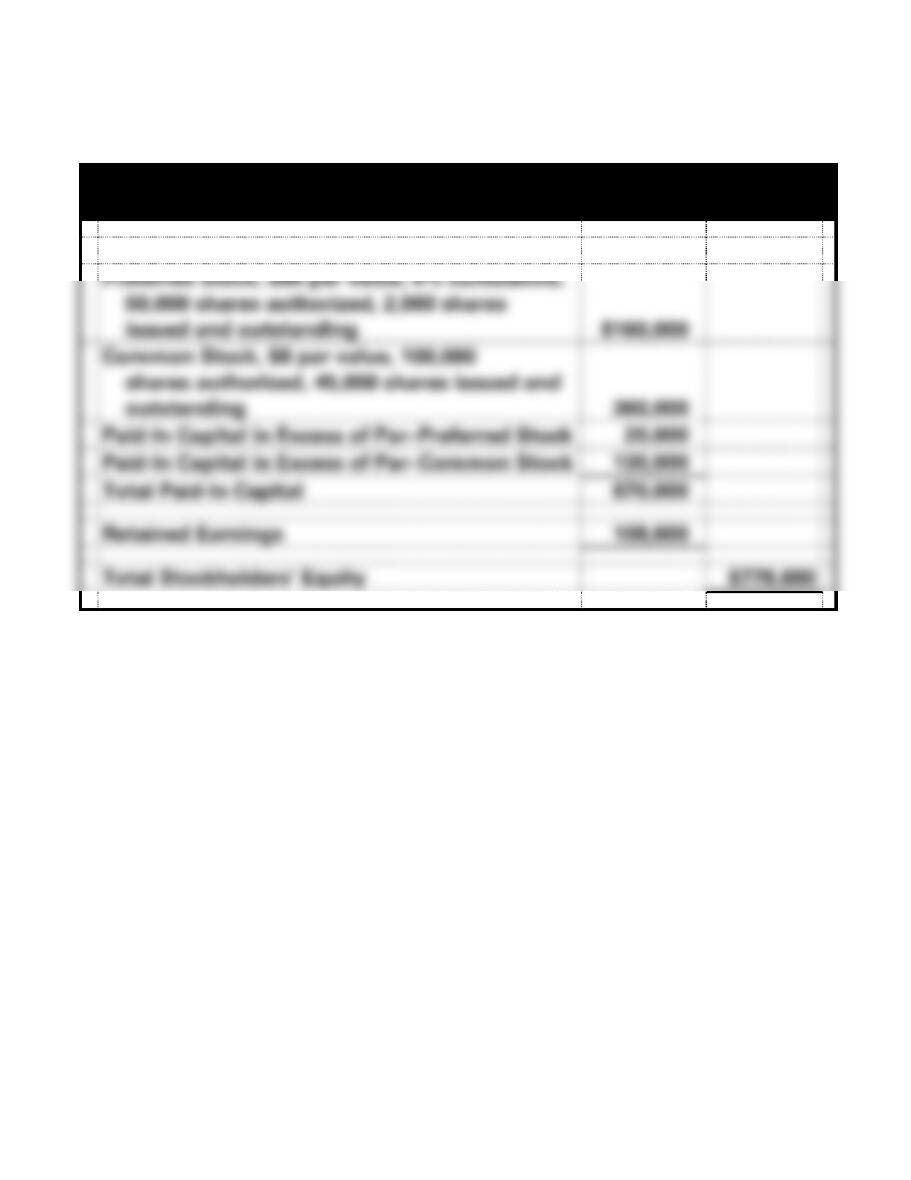

PROBLEM 11-23B (cont.)

b.

2016

Edgar Coproration

December 31, 3016

Stockholders’ Equity

Preferred Stock, $80 par value, 4% cumulative,

50,000 shares authorized, 2,000 shares

issued and outstanding

$160,000

Common Stock, $8 par value, 100,000

shares authorized, 45,000 shares issued and

outstanding

360,000

Paid-In Capital in Excess of Par−Preferred Stock

20,000

Paid-In Capital in Excess of Par−Common Stock

130,000

Total Paid-In Capital

670,000

Retained Earnings

108,600

Total Stockholders’ Equity

$778,600

11-116

PROBLEM 11-23B (cont.)

c.

Schedule provided for use of instructor.

Schedule of Number of

Shares of Common Stock

Shares

Issued

Shares

Outstanding

2016

Jan. 2

25,000

25,000

Feb. 14

20,000

20,000

Totals

45,000

45,000

2017

June 1

(1,000)

Totals

45,000

44,000

Shares issued and outstanding are the same for 2016. However, for 2017,

the 1,000 shares of treasury stock reduce the number of outstanding

shares. In 2017, there are 45,000 shares issued but only 44,000

outstanding.