10–73

ATC 10-2

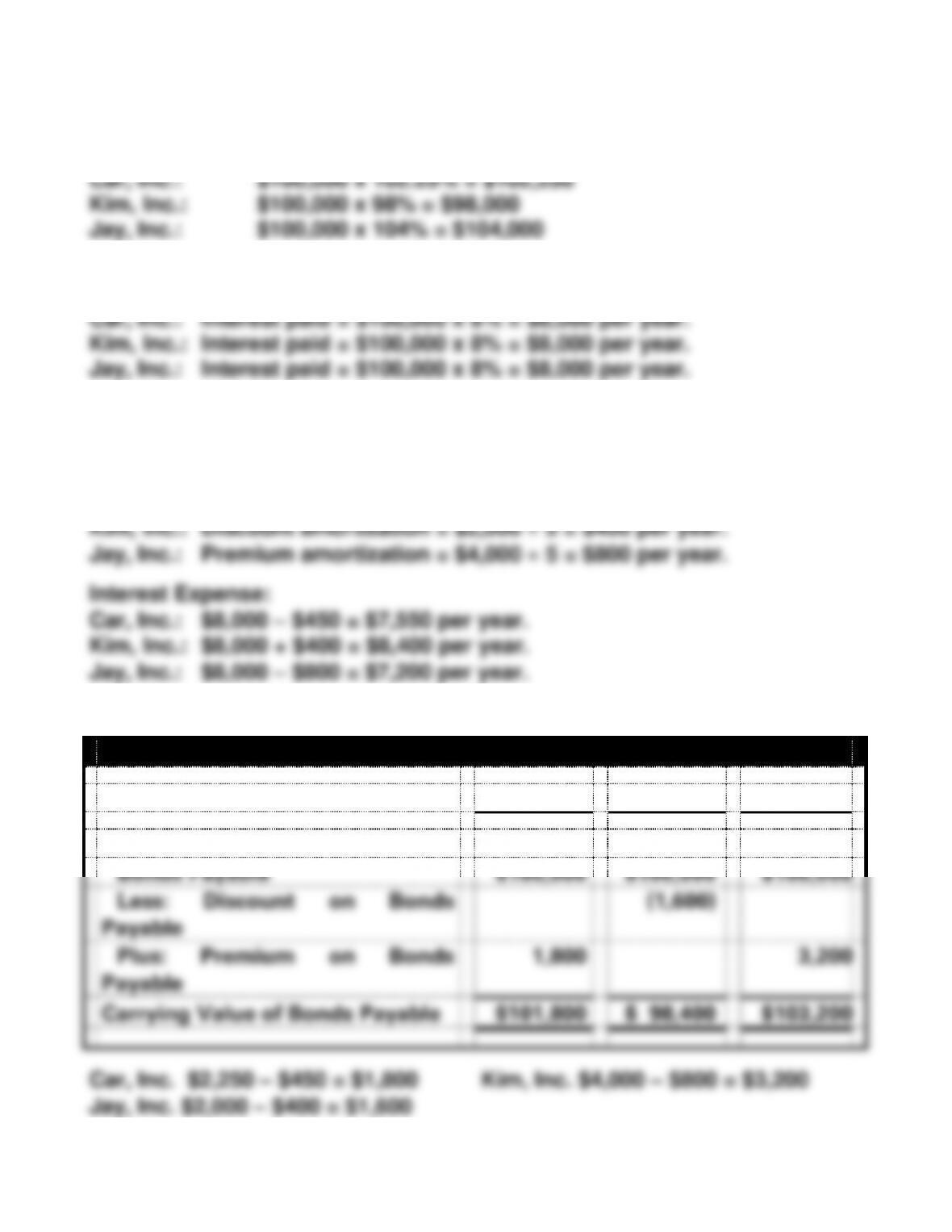

a.

(1)(a) Cash Proceeds

(1)(b)

Interest Paid:

(1)(c)

Interest Expense = Interest paid +/− amortized discount/premium.

Amortization of premium or discount:

Car, Inc.: Premium amortization = $2,250 5 = $450 per year.

(2)

December 31, 2016

Car

Kim

Jay

Liabilities

Bonds Payable

$100,000

$100,000

$100,000

Less: Discount on Bonds

Payable

(1,600)

Plus: Premium on Bonds

Payable

1,800

3,200

Carrying Value of Bonds Payable

$101,800

$ 98,400

$103,200

10–74

ATC 10-2 (cont.)

c. The amount of interest expense is different for each of the three

companies because the issue price was different; consequently the

10–75

ATC 10-3

Students should be reminded that the analysts at Standard & Poor’s have had a lot

more information upon which to base their ratings than is presented in the

textbook. The credit ratings and the company to which each relates are as follow:

AAA = Automatic Data Processing (ADP)

A = Boeing

much about future expectations (will JCP’s losses continue?) as it is

about the current condition of a company’s balance sheet.

The data presented show that the ADP probably is in the best financial

contrition. Its times interest earned is 16 times higher than the next best

company, Boeing, and its return on assets ratio and debt to assets ratios

10–76

ATC 10-4

a. Sonic Corporation, dollar amounts in thousands.

2013

2012

Net Income

$36,701

$36,085

Interest Expense

29,098

31,608

Income Tax Expense

19,598

21,877

EBIT

$85,397

$89,570

10–77

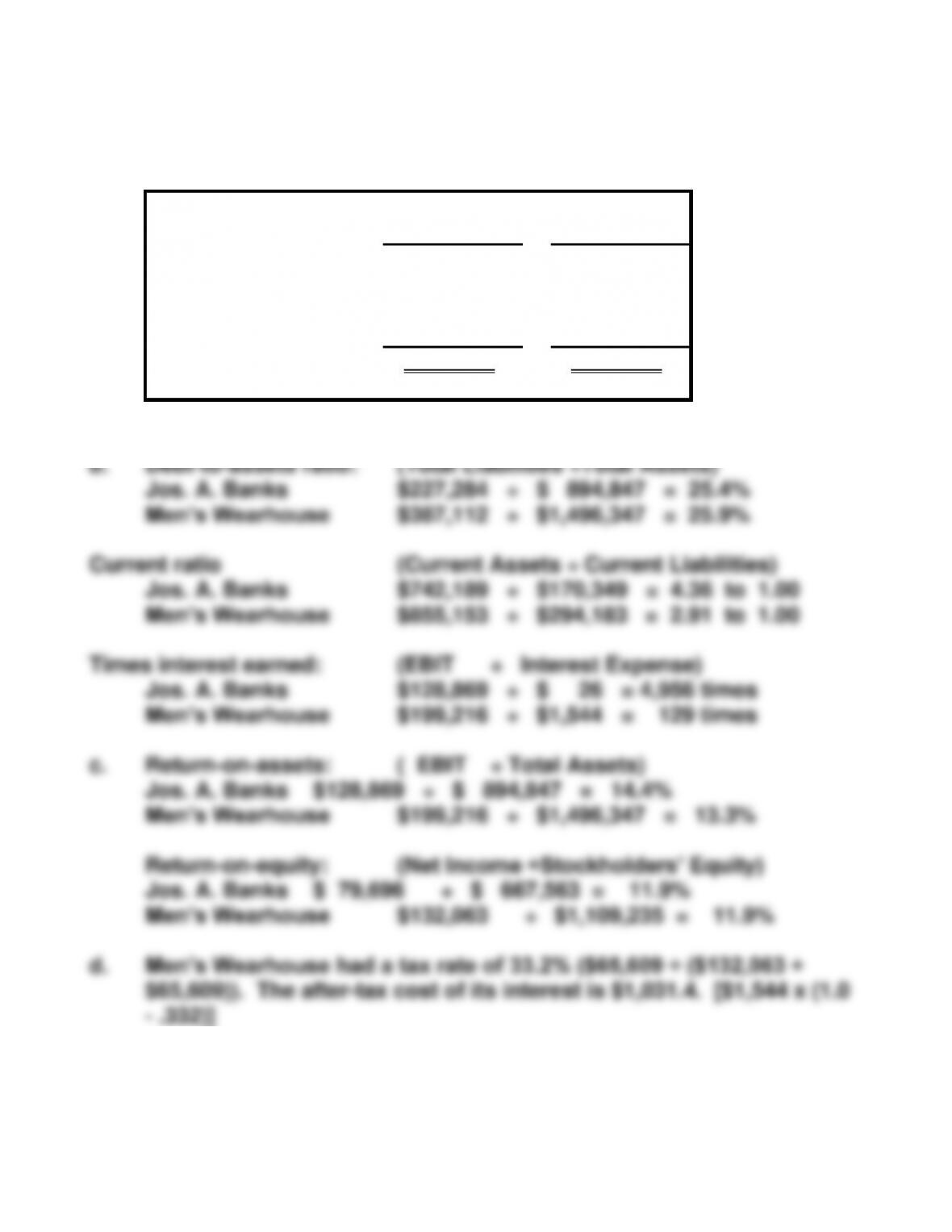

ATC 10-5

a. Dollar amounts in thousands.

Jos. A.

Banks

Men’s

Wearhouse

Net Income

$ 79,696

$132,063

Interest Expense

26

1,544

Income Tax Expense

49,147

65,609

EBIT

$128,869

$199,216

10–78

ATC 10-6

a.

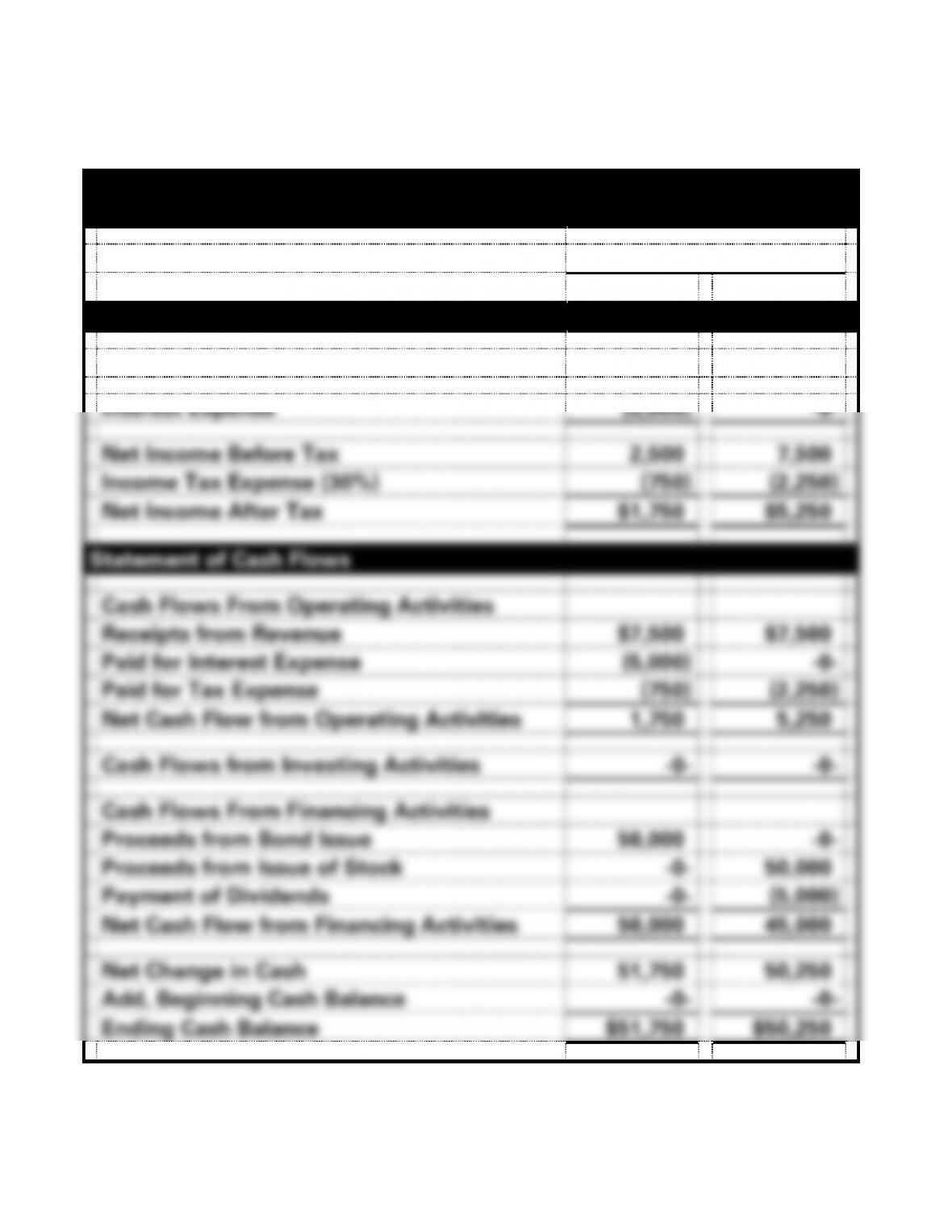

Mack Company

Selected Financial Statements for 2016

Type of Financing

Debt

Equity

Income Statement

Rental Revenue ($50,000 x .15)

$7,500

$7,500

Interest Expense

(5,000)

-0-

Net Income Before Tax

2,500

7,500

Income Tax Expense (30%)

(750)

(2,250)

Net Income After Tax

$1,750

$5,250

Statement of Cash Flows

Cash Flows From Operating Activities

Receipts from Revenue

$7,500

$7,500

Paid for Interest Expense

(5,000)

-0-

Paid for Tax Expense

(750)

(2,250)

Net Cash Flow from Operating Activities

1,750

5,250

Cash Flows from Investing Activities

-0-

-0-

Cash Flows From Financing Activities

Proceeds from Bond Issue

50,000

-0-

Proceeds from Issue of Stock

-0-

50,000

Payment of Dividends

-0-

(5,000)

Net Cash Flow from Financing Activities

50,000

45,000

Net Change in Cash

51,750

50,250

Add, Beginning Cash Balance

-0-

-0-

Ending Cash Balance

$51,750

$50,250

10–79

ATC 10-6 (cont.)

b. The students should explain that the net income will be higher under

10–80

ATC 10-7

a. Forecast Statements

Financial Statements

Forecast

1

Forecast

2

Forecast

3

Income Statements

Revenue

$120,000

$160,000

$160,000

Operating Expenses

(70,000)

(77,000)

(77,000)

Income Before Interest and Taxes

50,000

83,000

83,000

Interest Expense

-0-

-0-

(11,620)

Income Tax Expense (30%)

(15,000)

(24,900)

(21,414)

Net Income

$ 35,000

$ 58,100

$ 49,966

Statements of Changes in Stockholders’ Equity

Beginning Retained Earnings

$15,000

$15,000

$15,000

Plus: Net Income

35,000

58,100

49,966

Less: Dividend to Watson

-0-

(11,620)

-0-

Ending Retained Earnings

$50,000

$61,480

$64,966

Balance Sheets

Assets (see Note 1 below)

$400,000

$511,480

$514,966

Liabilities

$ -0-

$ -0-

$100,000

Stockholders’ Equity

Common Stock

350,000

450,000

350,000

Retained Earnings

50,000

61,480

64,966

Total Liab. And Stockholders’ Equity

$400,000

$511,480

$514,966

10–81

ATC 10-7 (cont.)

b. The difference in retained earning between forecast 2 and 3 is:

Forecast 3

−

Forecast 2

=

Difference

Ret. Earnings

$64,966

−

$61,480

=

$3,486

10–82

ATC 10-8

This solution is based on the Union Pacific’s Form10-K for the fiscal year

ended December 31, 2013, and dollar amounts are in millions.

a. Total liabilities $28,506

were 2.4 times greater than those for capital leases ($4,066 ÷ $1,702).

If the operating lease payments had to be included in liabilities, this