1-1

ANSWERS TO QUESTIONS – CHAPTER 1

1. Stakeholders are the parties that use accounting information.

Stakeholders with a direct interest include owners, managers,

creditors, suppliers, and employees. These individuals are directly

2. Accounting provides information that is useful in making decisions

5. The market for business resources involves three distinct

6. Financial Resource: money

1-2

Physical Resource: natural resources (i.e. land, forests, mine ore,

7. Investors expect a distribution of the business’s profits as a return

8. Financial accounting provides information that is useful to external

9. Not-for-profit or nonprofit entities provide goods or services to

consumers for humanitarian or special reasons rather than to earn a

10. The U.S. rules of accounting information measurement are called

11. Careers in public accounting consist of providing services to the

general public from a public accounting firm. These services include

12. Items reported on the financial statements are organized into

1-3

1. Assets

2. Liabilities

13. Assets, the economic resources of a business, are used to produce

14. The assets of a business belong to that business entity and there

15. Creditors are individuals and/or institutions that have provided

goods or services to the business which are not yet paid for, or

17. The accounting equation is:

ASSETS – LIABILITIES = STOCKHOLDERS’ EQUITY

1-4

of the assets remaining after the creditors’ claims have been

18. The owners ultimately bear the risk and collect the rewards

19. A double-entry bookkeeping system is one in which every

transaction affects at least two accounts. A transaction can affect

20. The right side of the accounting equation can be viewed as either

sources of assets or as obligations and commitment of the business.

21. The business could make a distribution of $1,000, but only $800 of it

22. Capital is acquired from owners by issuing stock to them. When

23. Assets that are acquired by issuing common stock are the result of

24. Revenue increases the asset side of the accounting equation and

1-5

25. The three primary sources of assets are (1) investments by owners

26. Retained earnings are a result of a business retaining its earned

27. Distributions to owners, called dividends, decrease the asset side of

28. Dividends and expenses are similar in that they both decrease assets

and affect the accounting equation in the same way (i.e. reduction of

29. (1) Income Statement – measures the difference between the asset

(2) Statement of Changes in Stockholders’ Equity – explains the

(3) Balance Sheet – lists the assets and the corresponding claims

(4) Statement of Cash Flows – explains how a company obtained

1-6

32. A business liquidation is when a business ceases to operate, its

33. The going concern doctrine assumes that a business is able to

34. The matching concept is the practice of pairing revenues and

35. (1) Operating activities – explain the cash generated from revenue

(2) Investing activities – include cash received or spent by the

(3) Financing activities – include cash inflows and outflows from

36. Asset accounts are arranged on the balance sheet in accordance

37. Articulation refers to the interrelationships among the various

38. Temporary accounts are used to capture information for a single

accounting period. The balances in temporary accounts are

39. The information in the temporary accounts is transferred to Retained

1-7

accounts have a zero balance at the beginning of the next

accounting period. This allows the income statement and statement

40. The historical cost concept requires that most assets be reported at

the amount paid for them regardless of their increase or decrease in

41. An asset source transaction results in an increase in an asset

account and an increase in one of the claims accounts; i.e.,

investments by owners (equity), borrowing funds from creditors

42. While the contents of annual reports vary from company to

company, all annual reports contain:

43. U.S. GAAP, generally accepted accounting principles in the United

States, are the measurement rules established by the (FASB)

1-8

Reporting Standards (IFRS) are issued by the International

Accounting Standards Board and are an attempt to set a common

1-9

SOLUTIONS TO EXERCISES – SERIES A – CHAPTER 1

EXERCISE 1-1A

The three participants in the free business market are:

Note to instructor:

The memo should discuss the fact that the resource owners are those

who own resources that are desired by others, either in the original form

1-10

EXERCISE 1-2A

a. The most common designation held by a public accountant is the

CPA license. CPA stands for certified public accountant. CPAs are

licensed by the state government (or other jurisdiction). Although

EXERCISE 1-3A

Entities mentioned:

Effect on cash:

Vicky Hill Recovery Fund

Increase for cash contributions, $21,000

Decrease for payment of advertising, $1,000

Decrease payment for hospital bills, $12,000

Decrease for donation to National Cyclist

Fund, $8,000

Karen White

Decrease by contribution, $1,000

WKUX

Increase for advertising revenue, $1,000

Public

Decrease for contributions, $20,000

Mercy Hospital

Increase for medical care, $12,000

National Cyclist Fund

Increase for donation, $8,000

1-12

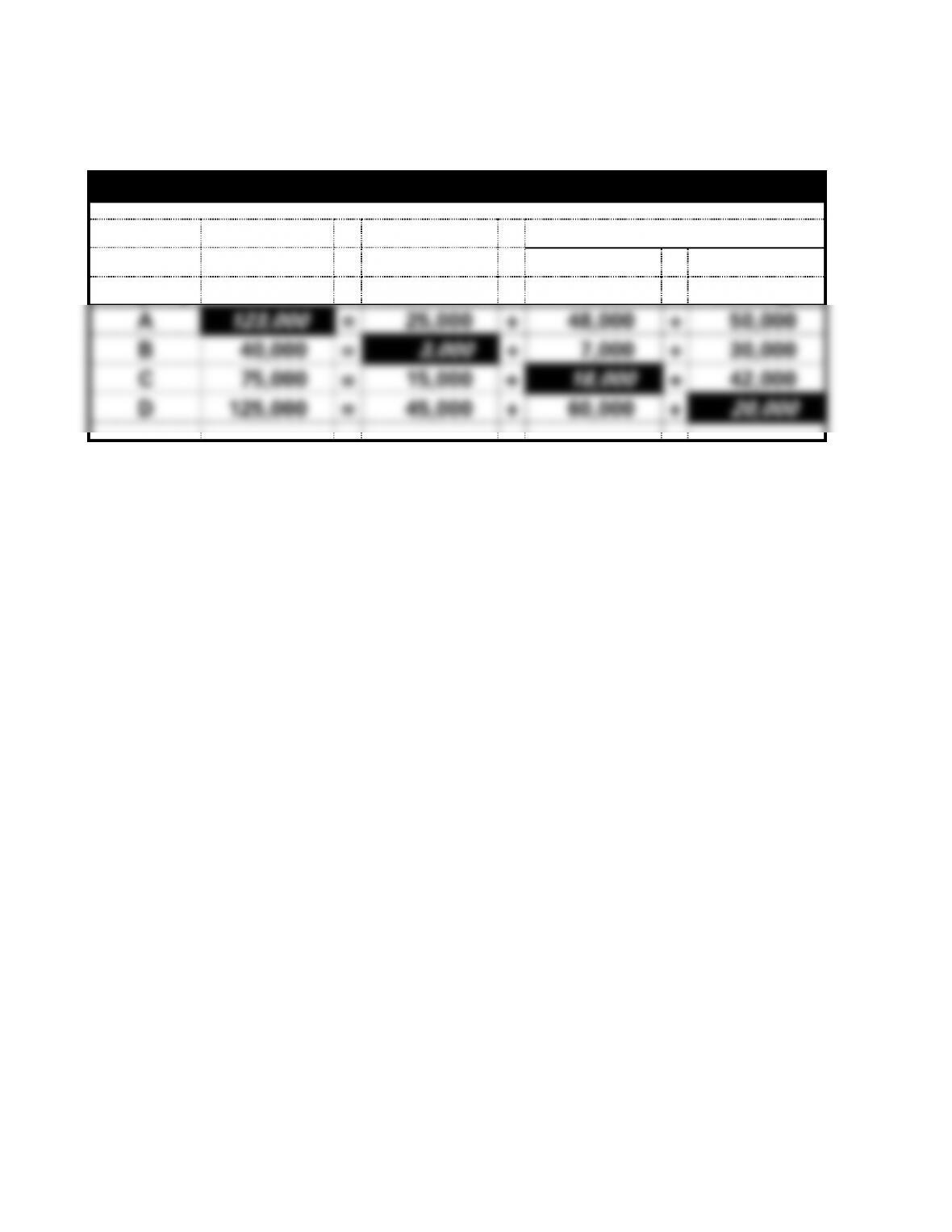

EXERCISE 1-4A

Accounting Equation

Stockholders’ Equity

Common

Retained

Company

Assets

=

Liabilities

+

Stock

+

Earnings

A

123,000

=

25,000

+

48,000

+

50,000

B

40,000

=

3,000

+

7,000

+

30,000

C

75,000

=

15,000

+

18,000

+

42,000

D

125,000

=

45,000

+

60,000

+

20,000

1-13

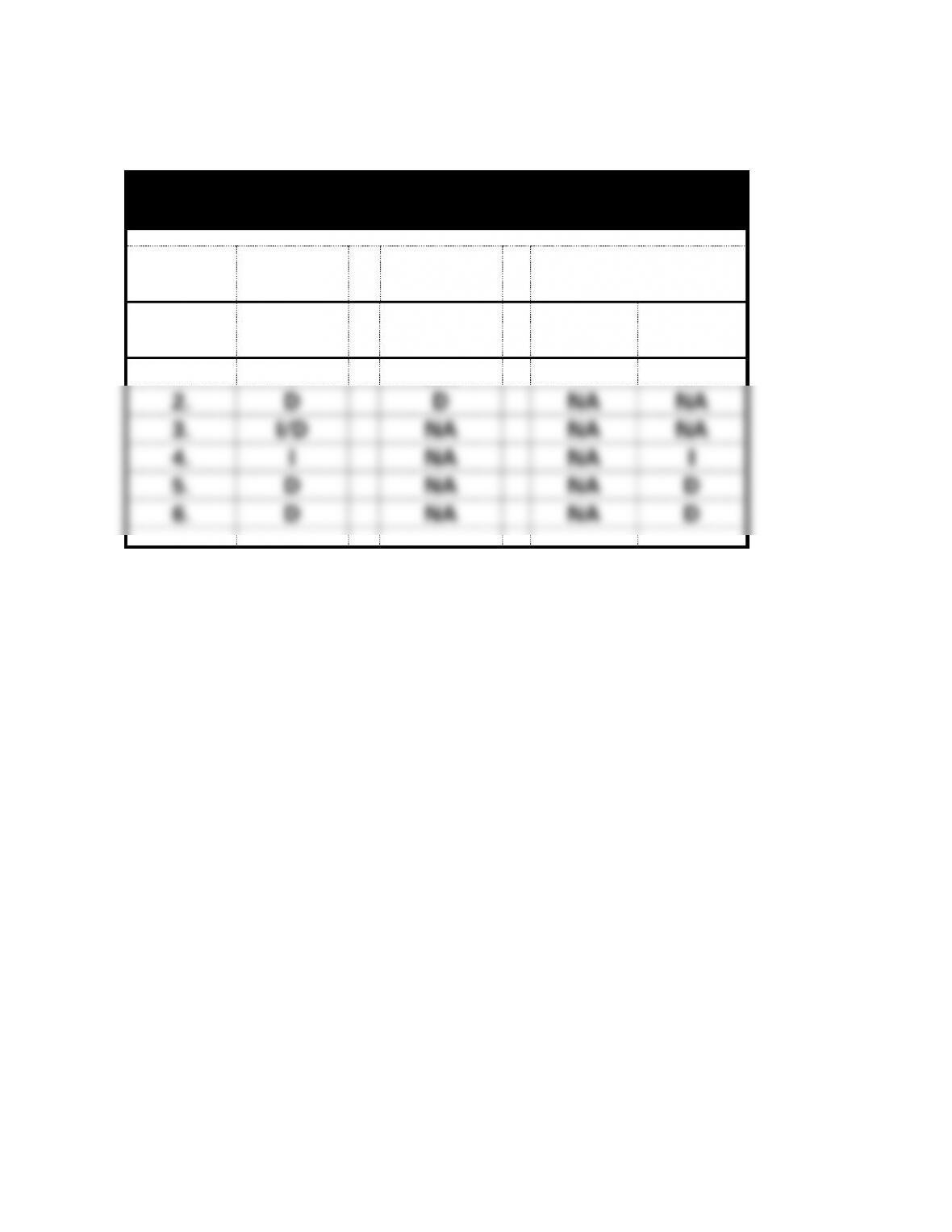

EXERCISE 1-5A

Olive Enterprises

Accounting Equation

Stockholders’

Equity

Event

Number

Assets

=

Liabilities

+

Common

Stock

Retained

Earnings

1.

I

NA

I

NA

2.

D

D

NA

NA

3.

I/D

NA

NA

NA

4.

I

NA

NA

I

5.

D

NA

NA

D

6.

D

NA

NA

D

1-14

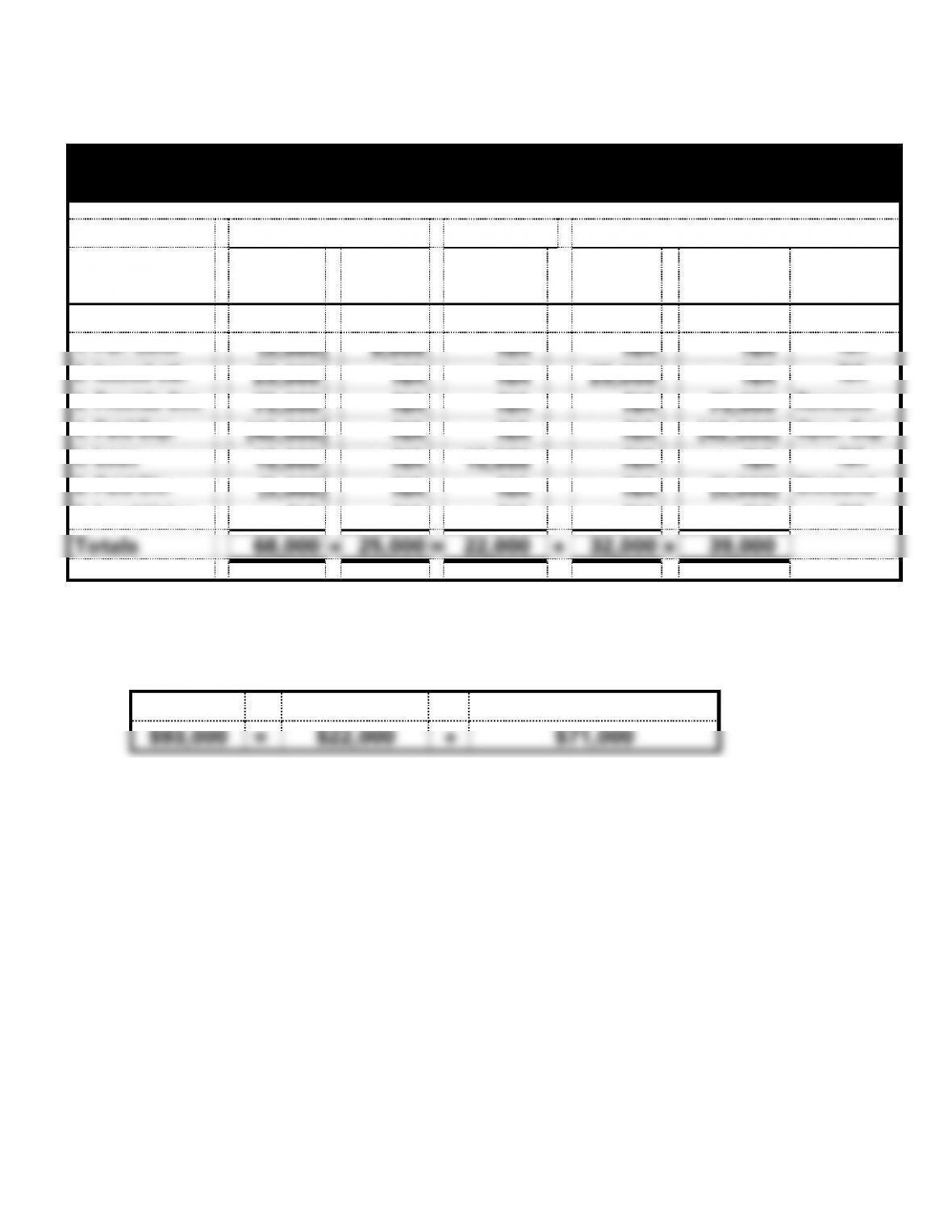

EXERCISE 1-6A

a.

Better Corporation

Accounting Equation for 2016

Assets

=

Liabilities

+

Stockholders’ Equity

Event

Cash

+

Land

=

Notes

Payable

+

Com.

Stock

+

Retained

Earnings

Acct.

Title/RE

Bal. 1/1/16

10,000

20,000

12,000

7,000

11,000

1. Pur. Land

(5,000)

5,000

NA

NA

NA

NA

2. Issued stk.

25,000

NA

NA

25,000

NA

NA

3. Provide Svc.

75,000

NA

NA

NA

75,000

Revenue

4. Paid Exp.

(42,000)

NA

NA

NA

(42,000)

Oper. Exp.

5. Loan

10,000

NA

10,000

NA

NA

NA

6. Paid Div.

(5,000)

NA

NA

NA

(5,000)

Dividend

7. Land Value

NA

NA

NA

NA

NA

NA

Totals

68,000

+

25,000

=

22,000

+

32,000

+

39,000

b.

Assets

=

Liabilities

+

Stockholders’ Equity

$93,000

=

$22,000

+

$71,000

c. The balances of total assets, liabilities and stockholders’ equity will

be the same on January 1, 2017 as the balances on December 31,

2016. (See b. above)

1-15

EXERCISE 1-7A

a.

Assets

=

Liabilities

+

Stockholders’ Equity

Cash

=

Note Payable

+

Common Stock

+

Retained Earnings

195,000

=

90,500

+

84,500

+

?

Retained Earnings = $195,000 – $90,500 – $84,500 = $20,000

b. & c.

Moss Company

Effect of 2017 Transactions on the Accounting Equation

Assets

=

Liabilities

+

Stockholders’ Equity

Notes

Common

Retained

Event

Cash

=

Payable

+

Stock

+

Earnings

Beginning Balances

195,000

90,500

84,500

20,000

1. Earned Revenue

42,000

NA

NA

42,000

2. Paid expenses

(24,000)

NA

NA

(24,000)

3. Paid dividend

(3,000)

NA

NA

(3,000)

Ending Balance

210,000

=

90,500

+

84,500

+

35,000

d.

Cash

=

Note Payable

+

Common Stock

+

Retained Earnings

210,000

=

90,500

+

84,500

+

35,000

1-16

EXERCISE 1-8A

a.

Assets

=

Liabilities

+

Stockholders’ Equity

Computers

Notes Payable

Operating Expenses

Building

Utilities Payable

Utilities Expense

Cash

Accounts Payable

Gasoline Expense

Land

Rent Revenue

Trucks

Retained Earnings

Supplies

Salaries Expense

Office Furniture

Common Stock

Service Revenue

Interest Expense

Dividends

Supplies Expense

b. No. The type of accounts will vary depending on the type of business.

Some businesses will have only one revenue account; other businesses

may have more than one type of revenue account. For instance, a

business may have both service revenue and interest revenue. Also,

the expense accounts that a business has are somewhat dependent on

the type and complexity of the business. For instance, if a business

owns its own building, it will not have rent expense. If a business does

not have employees, it will not have salaries expense. The level of

detail desired by the business will also affect the type of revenue and

expense accounts that a business will have.

EXERCISE 1-9A

a.

Cash

+

Land

=

Creditors

+

Stockholders’

Equity

$16,000

$ 0

$6,000

$10,000

(12,000)

12,000

NA

NA

Bal.

$ 4,000

+

$12,000

=

$6,000

+

$10,000

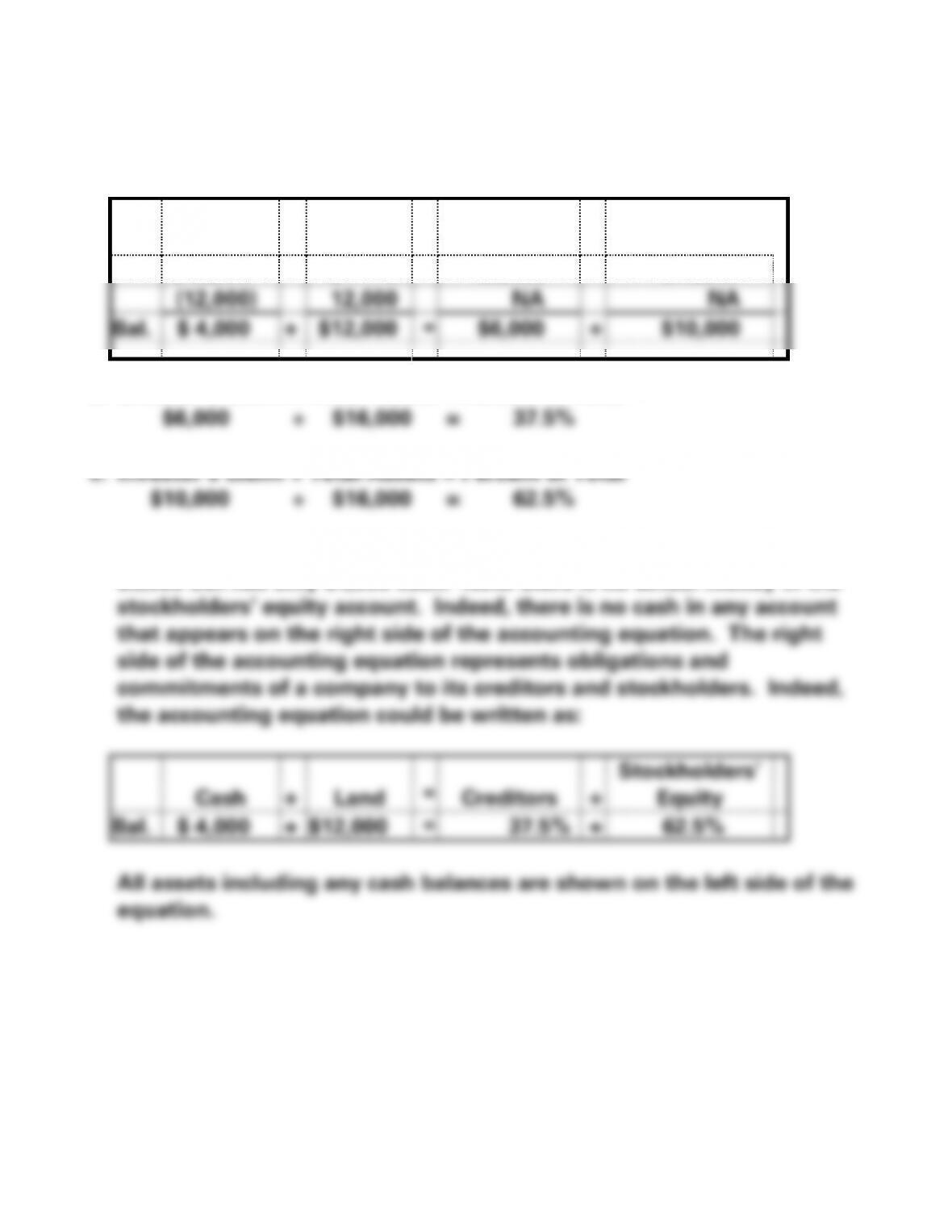

b. Creditor’s Claim ÷ Total Assets = Percent of Total

d. The company cannot repay the debt. The company owes the creditors

$6,000 but has only $4,000 cash. Note there is no actual money in the

Cash

+

Land

Creditors

+

Stockholders’

Equity

Bal.

$ 4,000

+

$12,000

=

+

62.5%

1-18

EXERCISE 1-10A

a. While the exact amount of any available dividend cannot be

determined, the maximum dividend that could be paid based on the

information would be $1,800, the amount of retained earnings. In

order to determine the amount that could be paid, the balance of the

1-19

EXERCISE 1-11A

a. Creditors receive their $400 interest payment, leaving $1,200 ($1,600 –

$400) to be paid as dividends to the investors.

c. Creditors receive their $400 interest payment. No dividend is paid to

above.

1-20

EXERCISE 1-12A

a. Investors put assets into the company with the expectation of sharing

profits. Creditors lend assets to the company with the expectation of

repayment of the principal plus interest on the loan.

b.

Harris Company

Accounting Equation

Event

Assets

=

Liabilities

+

Stockholders’ Equity

Acquired assets

$7,800

$3,600

$4,200

Earned income

2,000

2,000

Balance

$9,800

$3,600

$6,200

Since creditors are owed $3,600 and there are sufficient funds to pay

them; the creditors will receive the $3,600 that they are owed. Since

the investors own the business, they are entitled to the profits earned

by the business. The investors will receive $6,200 (their original $4,200

investment plus the $2,000 of profit).

c.

Harris Company

Accounting Equation

Event

Assets

=

Liabilities

+

Stockholders’ Equity

Acquired assets

$7,800

$3,600

$4,200

Incurred loss

(2,000)

(2,000)

Balance

$5,800

$3,600

$2,200

Since creditors are owed $3,600 and there are sufficient funds to pay

them; the creditors will receive the $3,600 that they are owed. Since

the investors own the business, they suffer the losses earned by the

business. The investors will receive $2,200 (their original $4,200

investment minus the $2,000 loss).