2-127

PROBLEM 2-42B (cont.)

FOR THE YEARS

2016

2017

2018

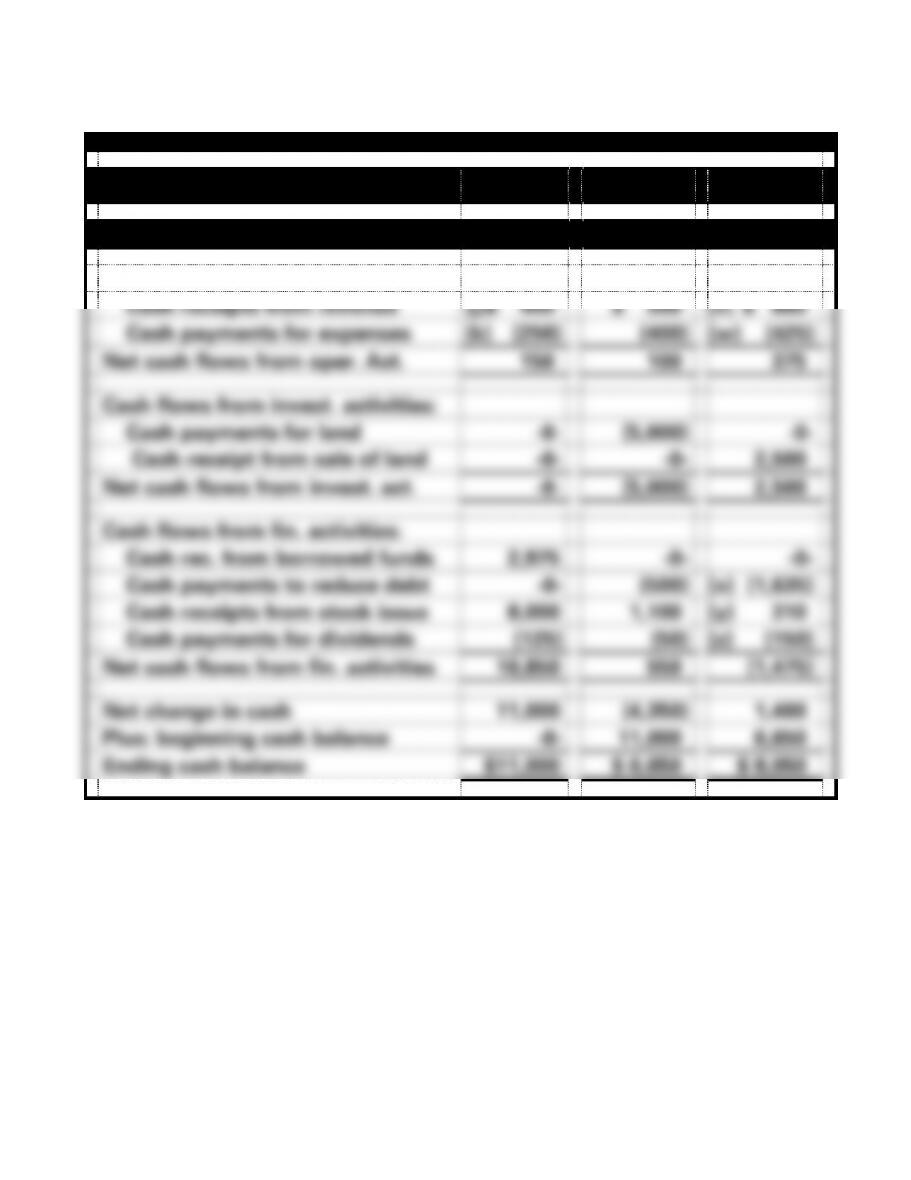

Statements of Cash Flows

Cash flows from oper. activities:

Cash receipts from revenue

(j)$ 400

$ 500

(v) $ 800

Cash payments for expenses

(k) (250)

(400)

(w) (425)

Net cash flows from oper. Act.

150

100

375

Cash flows from invest. activities:

Cash payments for land

-0-

(5,000)

-0-

Cash receipt from sale of land

-0-

-0-

2,500

Net cash flows from invest. act.

-0-

(5,000)

2,500

Cash flows from fin. activities:

Cash rec. from borrowed funds

2,975

-0-

-0-

Cash payments to reduce debt

-0-

(500)

(x) (1,635)

Cash receipts from stock issue

8,000

1,100

(y) 310

Cash payments for dividends

(125)

(50)

(z) (150)

Net cash flows from fin. activities

10,850

550

(1,475)

Net change in cash

11,000

(4,350)

1,400

Plus: beginning cash balance

-0-

11,000

6,650

Ending cash balance

$11,000

$ 6,650

$ 8,050

2-128

PROBLEM 2–42B (cont.)

Computations of amounts:

a. $150 Net Income = $400 Revenue − $250 Expenses.

b. $8,000 Common Stock Issued = $8,000 Ending Common Stock − $-0- Beginning

Common Stock.

i. $25 Retained Earnings = $25 Ending Retained Earnings from Statement of Changes

in Stockholders’ Equity.

j. $400 Cash Receipts from Revenue = $400 Revenue from Income Statement.

k. $250 Cash Payments for Expenses = $250 Expenses from Income Statement.

l. $400 Expenses = $500 Revenue − $100 Net Income.

issued.

t. $9,710 Total Stockholders’ Equity = $9,410 Ending Common Stock + $300 Ending

Retained Earnings.

u. $8,050 Cash = $10,550 Total Assets − $2,500 Land.

v. $800 Cash Receipts from Revenue = $800 Revenue from Income Statement.

w. $425 Cash Payments for Expenses = $425 Expenses from Income Statement.

2-129

PROBLEM 2-43B

a.

Iowa Service Company

Accounting Equation for 2016

Assets

=

Liabilities

+

Stk. Equity

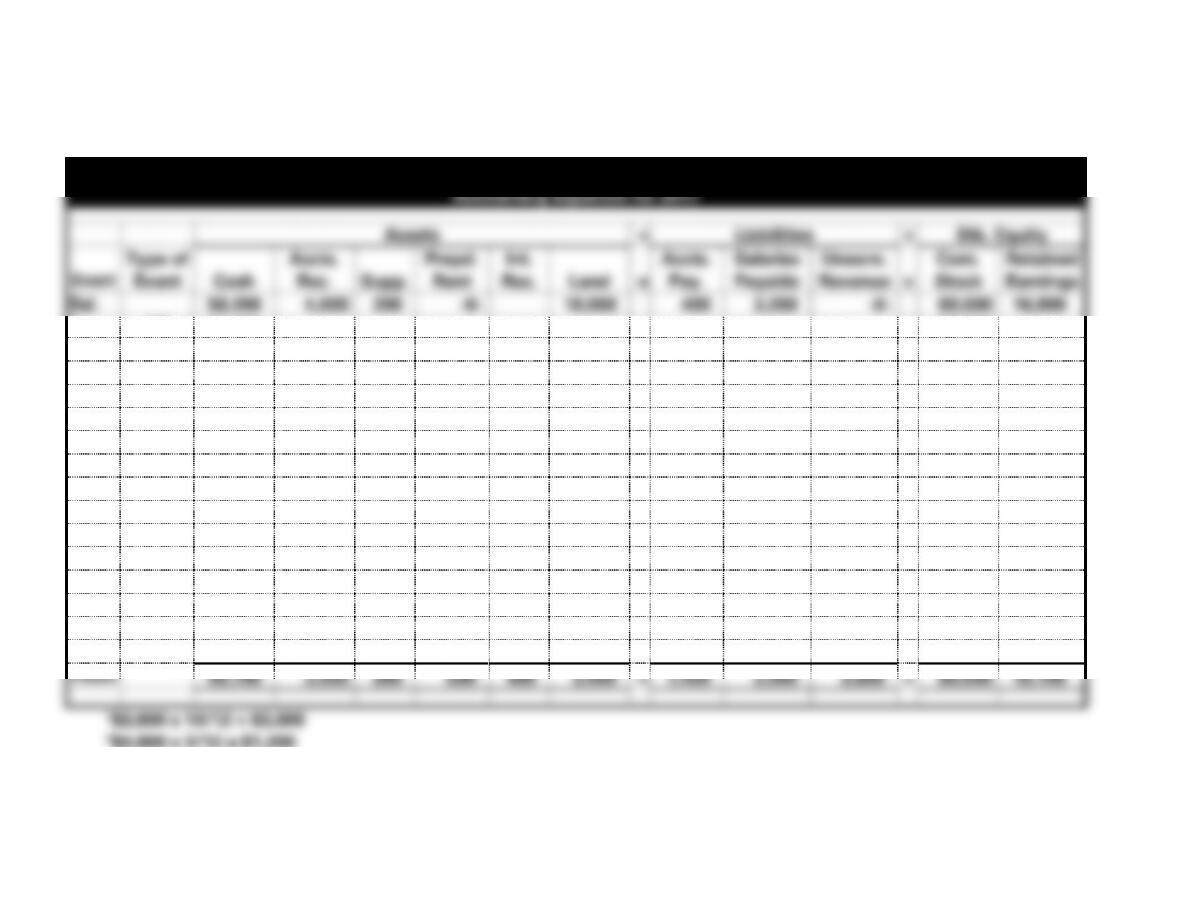

Event

Type of

Event

Cash

Accts.

Rec.

Supp.

Prepd.

Rent

Land

=

Accts.

Pay.

Salaries

Payable

Unearn.

Rev.

+

Com.

Stock

Retained

Earnings

1.

AS

60,000

60,000

2.

AS

1,200

1,200

3.

AE

(18,000)

18,000

4.

AU

(800)

(800)

5.

AS

42,000

42,000

6.

AU

(21,000)

(21,000)

7.

AE

38,000

(38,000)

8.

CE

3,200

(3,200)

9.

AU

(1,000)

(1,000)

Totals

58,200

4,000

200

-0-

18,000

=

400

3,200

-0-

+

60,000

16,800

2-130

PROBLEM 2-43B. (cont.)

Iowa Service Company

Accounting Equation for 2017

Assets

=

Liabilities

+

Stk. Equity

Event

Type of

Event

Cash

Accts.

Rec.

Supp.

Prepd.

Rent

Int.

Rec.

Land

=

Accts.

Pay.

Salaries

Payable

Unearn.

Revenue

+

Com.

Stock

Retained

Earnings

Bal.

58,200

4,000

200

-0-

18,000

400

3,200

-0-

60,000

16,800

1.

AS

20,000

20,000

2.

AU

(3,200)

(3,200)

3.

AE

(3,600)

3,600

4.

AE

15,000

(15,000)

5.

AS

4,800

4,800

6.

AS

1,000

1,000

7.

AS

32,000

32,000

8.

AE

33,000

(33,000)

9.

AU

(5,000)

(5,000)

10.

AU

(19,500)

(19,500)

11.

AU

(3,000)1

(3,000)

12.

CE

(1,200)2

1,200

13.

AU

(900)

(900)

14.

CE

3,900

(3,900)

15.

AS

400

400

Totals

99,700

3,000

300

600

400

3,000

=

1,400

3,900

3,600

+

80,000

18,100

1$3,600 x 10/12 = $3,000

2$4,800 x 3/12 = $1,200

2-131

PROBLEM 2-43B (cont.)

b.

Iowa Service Company

Financial Statements

For the Years Ended December 31, 2016 and 2017

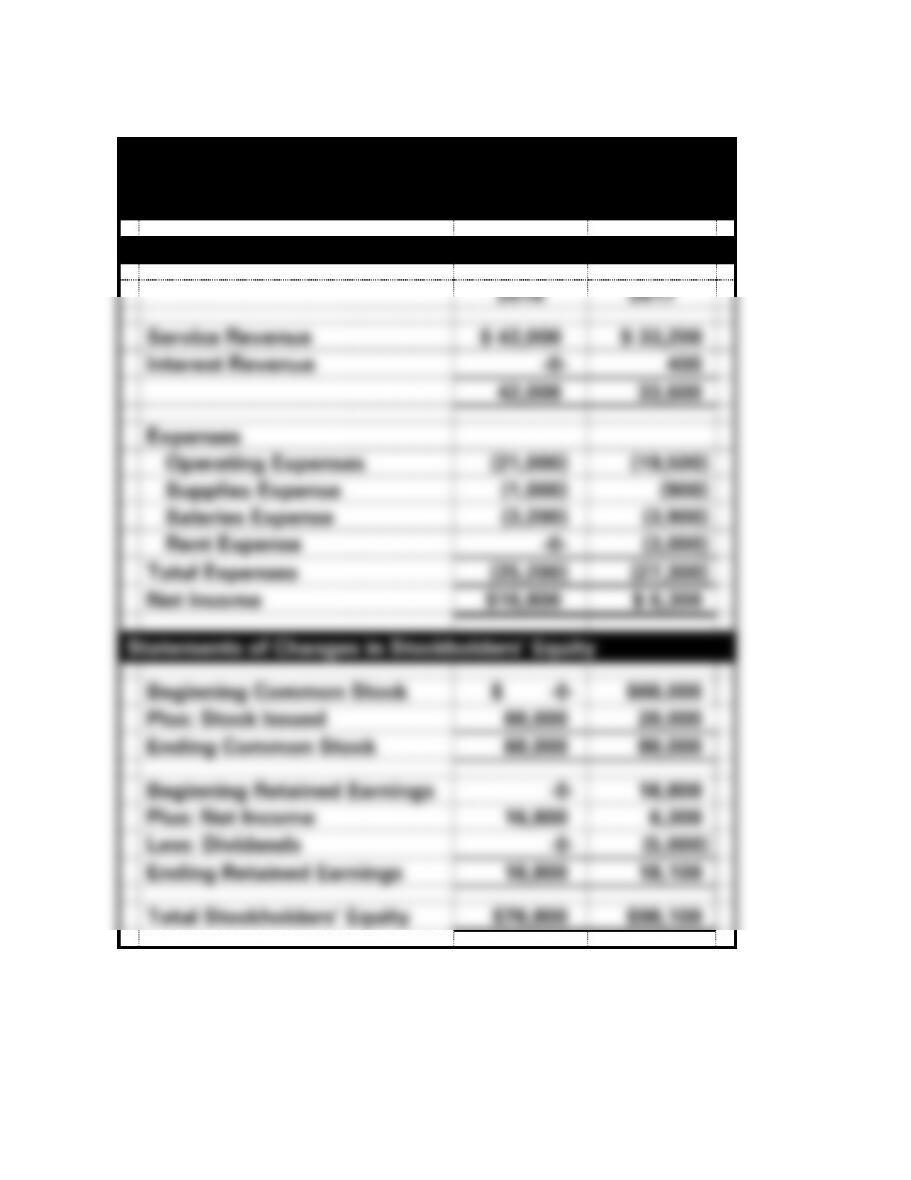

Income Statements

2016

2017

Service Revenue

$ 42,000

$ 33,200

Interest Revenue

-0-

400

42,000

33,600

Expenses

Operating Expenses

(21,000)

(19,500)

Supplies Expense

(1,000)

(900)

Salaries Expense

(3,200)

(3,900)

Rent Expense

-0-

(3,000)

Total Expenses

(25,200)

(27,300)

Net Income

$16,800

$ 6,300

Statements of Changes in Stockholders’ Equity

Beginning Common Stock

$ -0-

$60,000

Plus: Stock Issued

60,000

20,000

Ending Common Stock

60,000

80,000

Beginning Retained Earnings

-0-

16,800

Plus: Net Income

16,800

6,300

Less: Dividends

-0-

(5,000)

Ending Retained Earnings

16,800

18,100

Total Stockholders’ Equity

$76,800

$98,100

2-132

PROBLEM 2-43B b. (cont.)

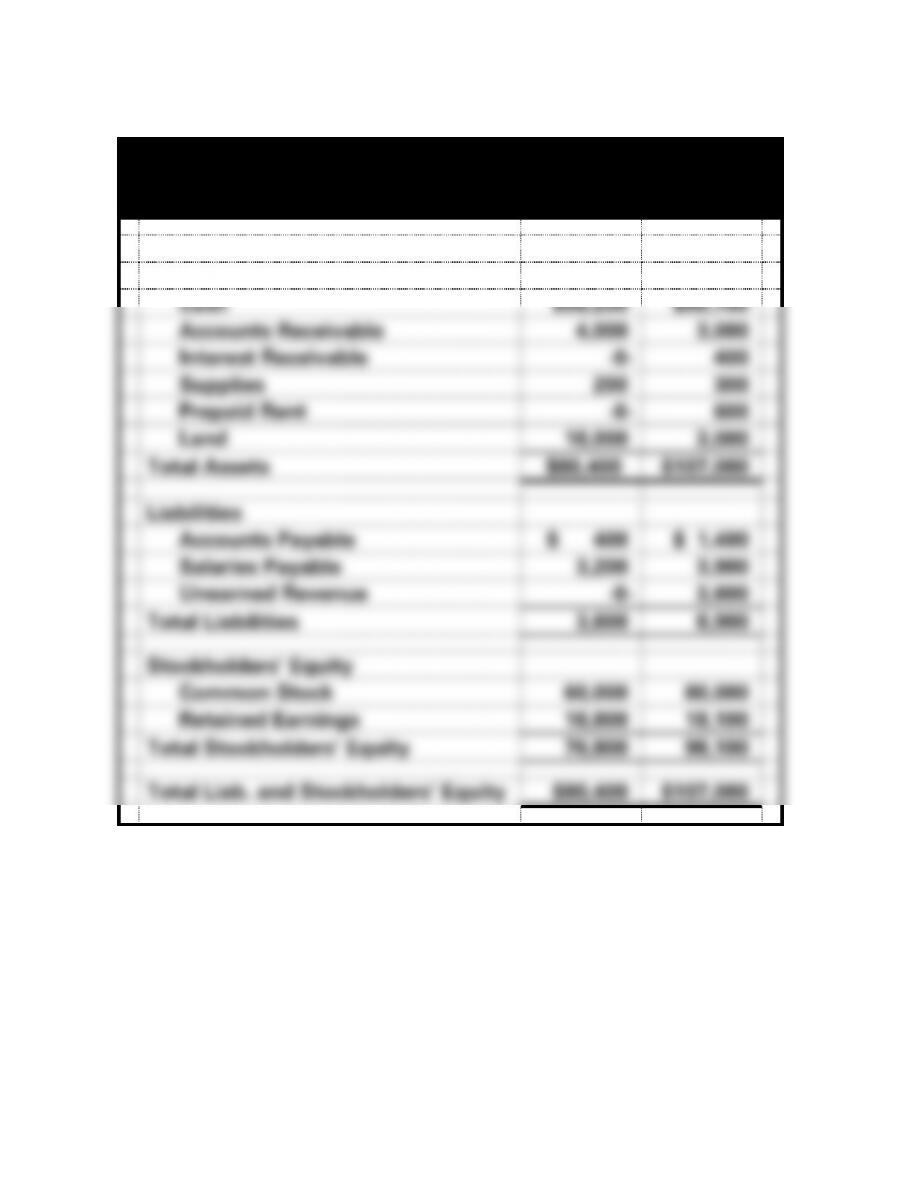

Iowa Service Company

Balance Sheets

As of December 31, 2016 and 2017

2016

2017

Assets

Cash

$58,200

$99,700

Accounts Receivable

4,000

3,000

Interest Receivable

-0-

400

Supplies

200

300

Prepaid Rent

-0-

600

Land

18,000

3,000

Total Assets

$80,400

$107,000

Liabilities

Accounts Payable

$ 400

$ 1,400

Salaries Payable

3,200

3,900

Unearned Revenue

-0-

3,600

Total Liabilities

3,600

8,900

Stockholders’ Equity

Common Stock

60,000

80,000

Retained Earnings

16,800

18,100

Total Stockholders’ Equity

76,800

98,100

Total Liab. and Stockholders’ Equity

$80,400

$107,000

2-133

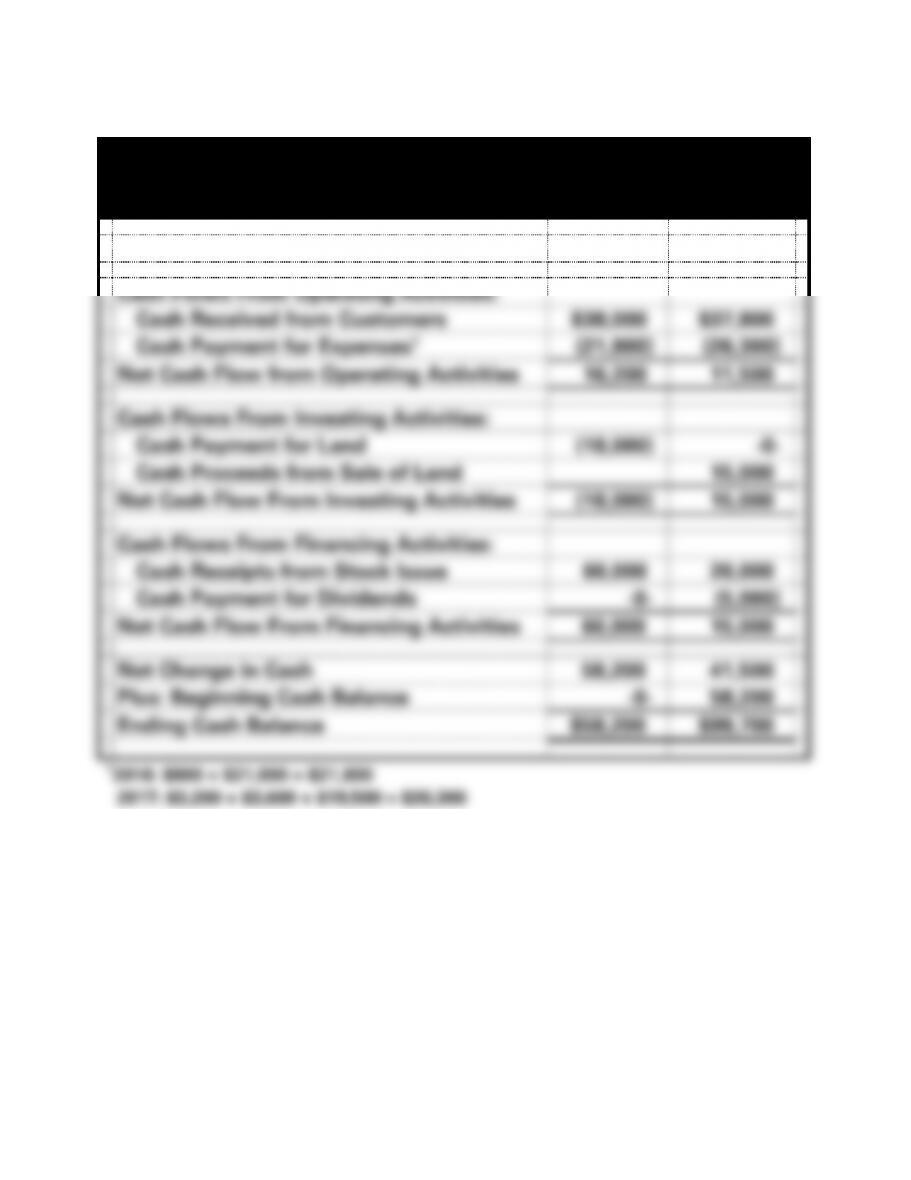

PROBLEM 2-43B b. (cont.)

Iowa Service Company

Statements of Cash Flows

For the Years Ended December 31, 2016 and 2017

2016

2017

Cash Flows From Operating Activities:

Cash Received from Customers

$38,000

$37,800

Cash Payment for Expenses1

(21,800)

(26,300)

Net Cash Flow from Operating Activities

16,200

11,500

Cash Flows From Investing Activities:

Cash Payment for Land

(18,000)

-0-

Cash Proceeds from Sale of Land

15,000

Net Cash Flow From Investing Activities

(18,000)

15,000

Cash Flows From Financing Activities:

Cash Receipts from Stock Issue

60,000

20,000

Cash Payment for Dividends

-0-

(5,000)

Net Cash Flow From Financing Activities

60,000

15,000

Net Change in Cash

58,200

41,500

Plus: Beginning Cash Balance

-0-

58,200

Ending Cash Balance

$58,200

$99,700

2-134

PROBLEM 2-44B

a.

Several of the principles should be mentioned in the memo.

Responsibilities Principle

As a professional, Kato should exercise professional and moral

2-135

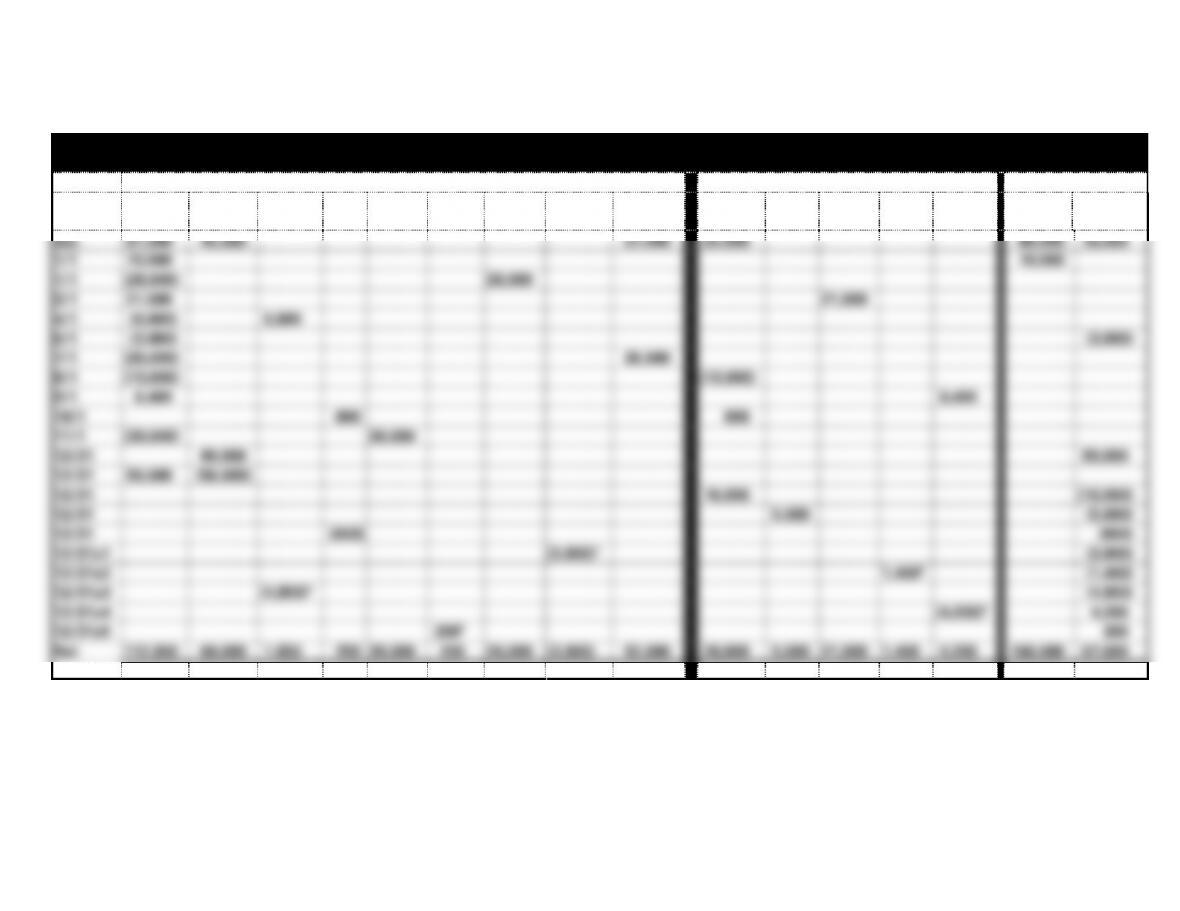

PROBLEM 2-45B

(Prepared for Instructor’s Use)

Accounting Equation

Assets

Liabilities

Stk. Equity

Date

Cash

Acc.

Rec.

Pp. Rent

Supp

CD

Int.

Rec.

Van

Acc.

Depr.

Land

Acc.

Pay.

Sal.

Pay.

Note

Pay.

Int.

Pay.

Unear.

Rev.

Com.

Stock

Ret. Earn.

Bal.

61,000

45,000

27,000

25,000

90,000

18,000

1/1

70,000

70,000

1/1

(26,000)

26,000

3/1

21,000

21,000

4/1

(6,600)

6,600

6/1

(3,000)

(3,000)

7/1

(25,000)

25,000

8/1

(13,000)

(13,000)

9/1

8,400

8,400

10/1

900

900

11/1

(30,000)

30,000

12/31

80,000

80,000

12/31

56,000

(56,000)

12/31

16,000

(16,000)

12/31

5,000

(5,000)

12/31

(650)

(650)

12/31a1

(3,800)1

(3,800)

12/31a2

1,4002

(1,400)

12/31a3

(4,950)3

(4,950)

12/31a4

(4,200)4

4,200

12/31a5

2005

200

Bal.

112,800

69,000

1,650

250

30,000

200

26,000

(3,800)

52,000

28,900

5,000

21,000

1,400

4,200

160,000

67,600

(1) 12/31a Depreciation Expense ($26,000 − $7,000 = $19,000; $19,000 5 = $3,800 per year)

(2) 12/31a Interest Expense ($21,000 x 8% = $1,680; $1,680 x 10/12 = $1,400)

(3) 12/31a Expired Rent ($6,600 x 9/12 = $4,950)

(4) 12/31a Unearned Revenue Earned ($8,400 x 4/8 = $4,200)

(5) 12/31a Interest Earned ($30,000 x 4% = $1,200; $1,200 x 2/12 = $200)

2-1

PROBLEM 2-45B (cont.)

1. Jan. 1, purchase of delivery van. Depreciation expense is recorded.

2. March 1, note payable issued. Interest expense is recorded.

3. April 1, prepaid rent. Expired rent is recorded.

4. Sept. 1, unearned revenue; cash was received in advance. Earned

5. Nov. 1, purchase of CD. Interest revenue is recorded.

b. $21,000 X 8% X 10/12=$1,400.

c. $56,000 + $8,400 − $6,600 − $13,000 = $44,800

d. $6,600 X 9/12 = $4,950

2-2

2-3

ATC 2-1 (All dollar amounts are in millions.)

1. Target’s accrual accounts are: Credit card receivables (2012 only),

Accounts payable, Accrued and other current liabilities. Note 16

2. Target’s deferral accounts are: Inventories, Buildings and

improvements, Fixtures and equipment, Computer hardware and

3. Net income for 2013 was $1,971

4. Net income decreased by $1,028 from 2012 to 2013 ($1,971 – $2,999).

2-4

ATC 2-2

a. 1. (in millions)

2013

2012

2011

Revenue

$120,550

$115,846

$110,875

Less: Operating expenses

88,582

102,686

97,995

Operating income

$ 31,968

$ 13,160

$ 12,880

2. The balance in Retained earnings is affected as follows:

3. Growth rates for operating income are:

2-5

ATC 2-3

Dollar amounts are in thousands.

a.

2012

2013

Revenues

$2,434,435

$2,644,630

– Expenses

2,331,354

2,527,365

Net income

$ 103,081

$ 117,265

Beg. retained earnings

$ 298,757

$ 374,932

+ Net income

103,081

117,265

– Dividends

26,915

53,515

End. Retained earnings

$ 374,932

$ 438,673

2-6

ATC 2-4

Dollar amounts in thousands.

a. and b.

2012

2013

Cash from operating activities

$ 145,188

$ 179,360

Cash from investing activities

(142,753)

(145,741)

Cash from financing activities

(1,588)

3,039

Net change in cash

847

36,658

+ Beg. cash balance

20,530

21,377

= End. Cash balance

$ 21,377

$ 58,035

2-7

ATC 2-5

Dollar amounts are in thousands.

a.

Aeropostale

American

Eagle

Outfitters

Revenues

$ 2,386,178

$ 3,475,802

Expenses

2,351,255

3,243,694

Net income

$ 34,923

$ 232,108

Beg. retained earnings

$ 459,279

$ 1,771,464

+ Net income

34,923

232,108

– Dividends

–

(414,301)

End. Retained earnings

$ 494,202

$ 1,589,271

2-8

ATC 2-6

Dollar amounts in thousands.

a. and b.

H&R Block

Intuit

Revenues

$ 2,905,943

$ 4,171,000

Expenses

2,471,995

3,313,000

Net income

$ 433,948

$ 858,000

Cash from operating activities

$ 497,108

$ 1,366,000

Cash from investing activities

(110,937)

(485,000)

Cash from financing activities

(584,541)

(262,000)

Net change in cash

(198,370)

619,000

+ Beg. cash balance

1,944,334

393,000

= End. Cash balance

$1,745,964

$ 1,012,000

2-9

ATC 2-7

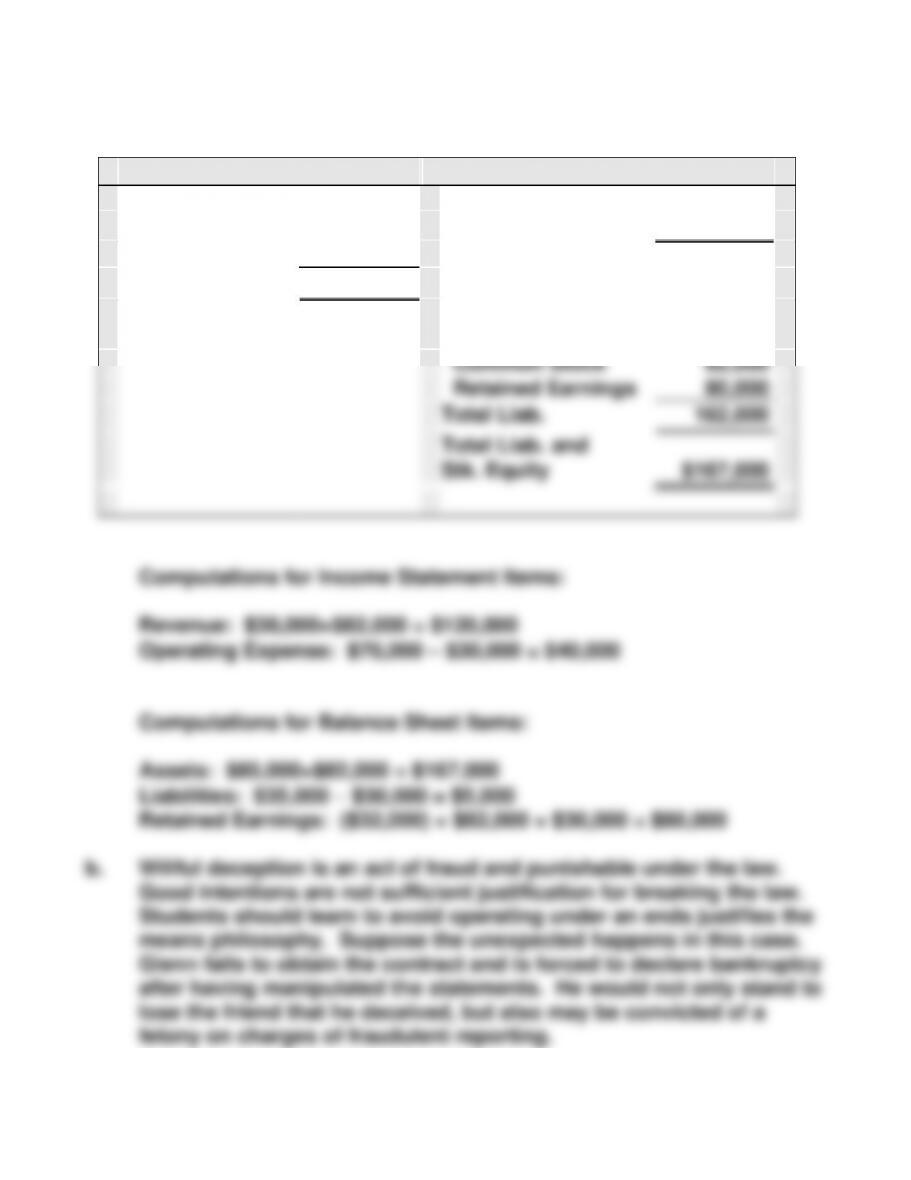

a.

Income Statement

Balance Sheet

Service Revenue

$120,000

Assets:

$167,000

Operating Exp.

(40,000)

Net Income

$ 80,000

Liabilities:

$ 5,000

Stockholders’

Equity:

Common Stock

82,000

Retained Earnings

80,000

Total Liab.

162,000

Total Liab. and

Stk. Equity

$167,000

2-10

ACT 2-7 (cont.)

c. The auditing profession has identified three elements that are

typically present when fraud occurs. They are: (1) the availability of

2-11

ATC 2-8

This solution is based on Netflix’s 2013 financial report.

a. Netflix’s accrual accounts are:

Current content liabilities (though students will probably not list

this account)