8-14

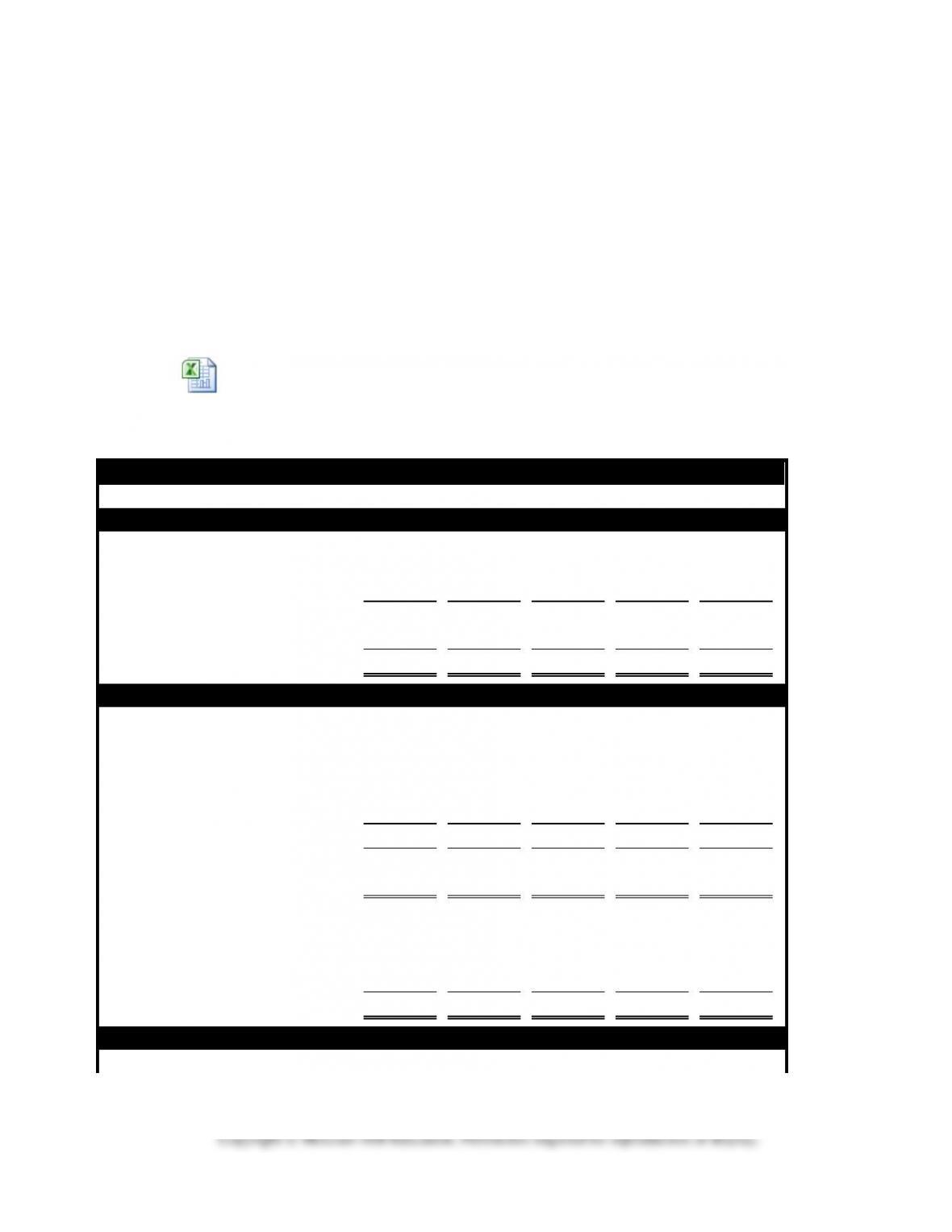

Ending cash balance

$9,000

$13,800

$23,400

$29,800

$34,100

8-15

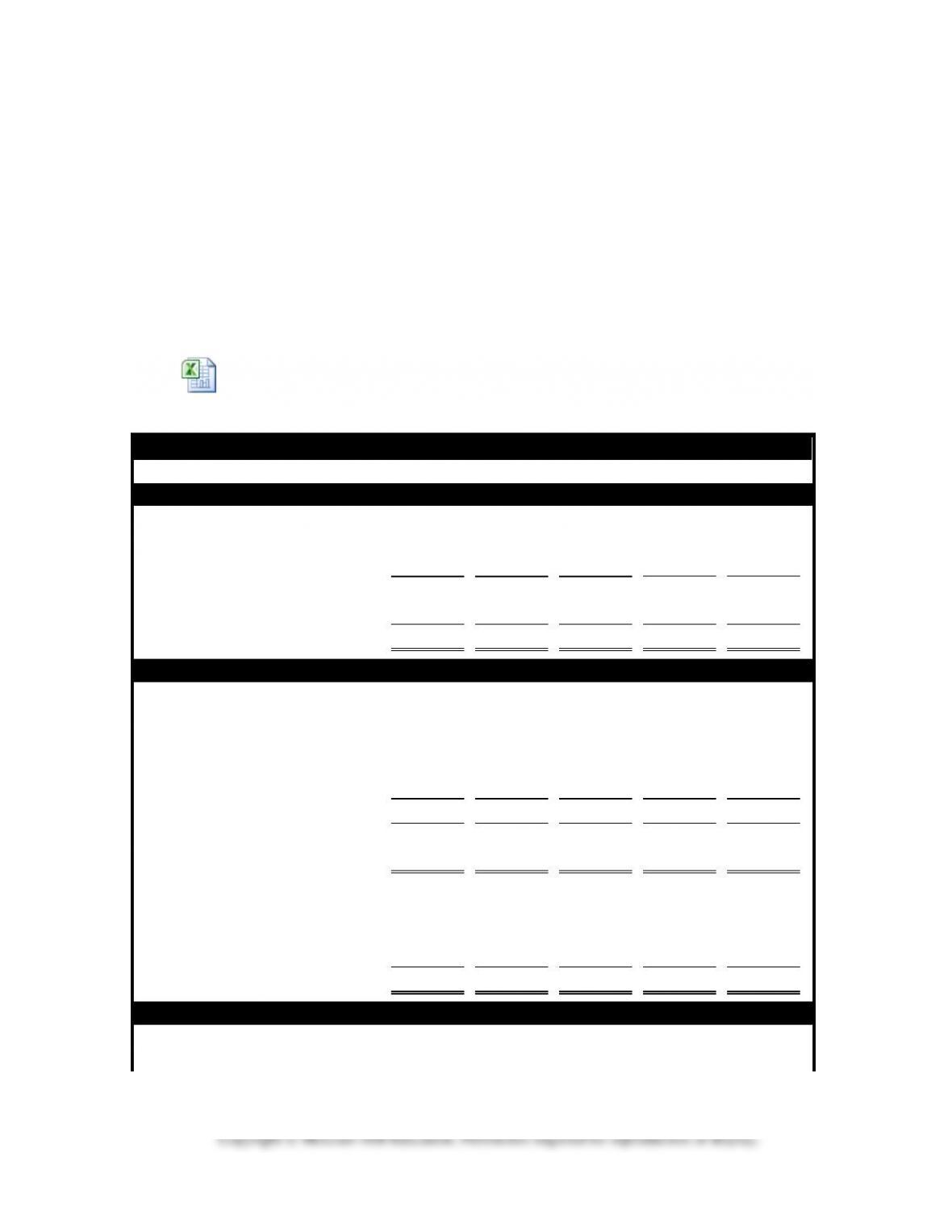

Demonstration Problem 8-2 Solution

1. Paid $1,000 cash for maintenance cost.

Assets

=

Liab.

+

Equity

Rev.

–

Exp.

=

Net Inc.

Cash Flow

Cash

+

Equip.

–

Accum.

Depr.

=

Ret. Earn.

1,000

+

5,000

–

2,000

=

0

+

4,000

0

–

0

=

0

(1,000)

+

0

–

0

=

0

+

(1,000)

0

–

1,000

=

(1,000)

(1,000) OA

0

+

5,000

–

2,000

=

0

+

3,000

0

–

1,000

=

(1,000)

2. Paid $1,000 cash to improve the quality of the equipment.

Assets

=

Liab.

+

Equity

Rev.

–

Exp.

=

Net Inc.

Cash Flow

Cash

+

Equip.

–

Accum.

Depr.

=

Ret. Earn.

1,000

+

5,000

–

2,000

=

0

+

4,000

0

–

0

=

0

(1,000)

+

1,000

–

0

=

0

+

0

0

–

0

=

0

(1,000) IA

0

+

6,000

–

2,000

=

0

+

4,000

0

–

0

=

0

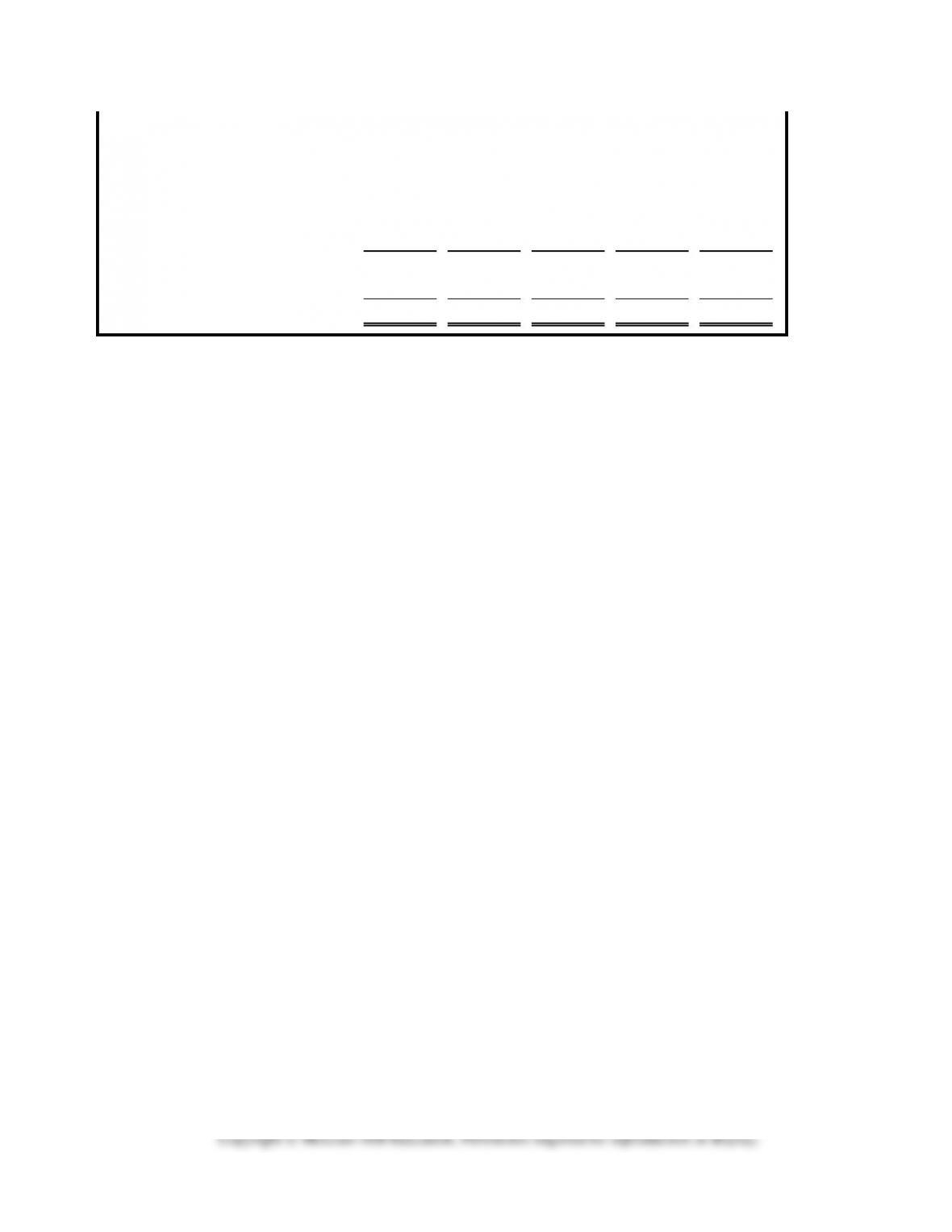

3. Paid $1,000 cash to extend the useful life of the equipment.

Assets

=

Liab.

+

Equity

Rev.

–

Exp.

=

Net Inc.

Cash Flow

Cash

+

Equip.

–

Accum.

Depr.

=

Ret. Earn.

1,000

+

5,000

–

2,000

=

0

+

4,000

0

–

0

=

0

(1,000)

+

0

–

(1,000)

=

0

+

-0-

0

–

0

=

0

(1,000) IA

0

+

5,000

–

1,000

=

0

+

4,000

0

–

0

=

0

8-16

Demonstration Problem 8-1 Scenario 1 Workpaper

In order to create the financial statements, it is helpful to first record the transactions

using the horizontal financial statements model even though the problem does not

require you to do so. This will then allow you to quickly see how information is

summarized on the financial statements.

The embedded spreadsheet includes a tab for workpapers using the horizontal fi-

nancial statements model. This may help students first record the transactions and

then see how those transactions would impact the financial statements. Then stu-

dents would be able to complete the financial statements worksheet below.

Worksheet Edmonds

FFAC9e Ch 8 IM DP8-

Straight-Line Depreciation

Income Statements

2015

2016

2017

2018

2019

Rent revenue

$7,200

$7,200

$7,200

$7,200

$ 0

Depreciation expense

Operating income

Gain on sale of automobile

Net income

$

$

$

$

$

Balance Sheets

Assets

Cash

$

$

$

$

$

Automobile

Accumulated depreciation

Book value, auto

Total assets

$

$

$

$

$

Stockholders’ equity

Common stock

$21,000

$21,000

$21,000

$21,000

$21,000

Retained earnings

Total stockholders’ equity

$24,200

$27,400

$30,600

$33,800

$34,100

Statements of Cash Flows

Operating activities

Inflow from customer

$ 7,200

$ 7,200

$ 7,200

$ 7,200

$ 0

8-17

Investing activities

Outflow for automobile

Inflow from sale of auto

Financing activities

Inflow from stock issue

Net change in cash

Beginning cash balance

Ending cash balance

$ 8,200

$15,400

$22,600

$29,800

$ 34,100

8-18

Demonstration Problem 8-1 Scenario 2 Workpaper

In order to create the financial statements, it is helpful to first record the transactions

using the horizontal financial statements model even though the problem does not

require you to do so. This will then allow you to quickly see how information is

summarized on the financial statements.

The embedded spreadsheet includes a tab for workpapers using the horizontal fi-

nancial statements model. This may help students first record the transactions and

then see how those transactions would impact the financial statements. Then stu-

dents would be able to complete the financial statements worksheet below.

Worksheet Edmonds

FFAC9e Ch 8 IM DP8-

Double-Declining-Balance Depreciation

Income Statements

2015

2016

2017

2018

2019

Rent revenue

$13,200

$8,200

$4,200

$3,200

$ 0

Depreciation expense

Operating income

Gain on sale of automobile

Net income

$

$

$

$

$

Balance Sheets

Assets

Cash

$

$

$

$

$

Automobile

Accumulated depreciation

Book value, auto

Total assets

$

$

$

$

$

Stockholders’ equity

Common stock

$21,000

$21,000

$21,000

$21,000

$21,000

Retained earnings

Total stockholders’ equity

$24,200

$27,400

$30,600

$33,800

$34,100

Statements of Cash Flows

Operating activities

8-19

Inflow from customer

$13,200

$8,200

$4,200

$3,200

$ 0

Investing activities

Outflow for automobile

Inflow from sale of auto

Financing activities

Inflow from stock issue

Net change in cash

Beginning cash balance

Ending cash balance

$14,200

$22,400

$26,600

$29,800

$34,100

8-20

Demonstration Problem 8-1 Scenario 3 Workpaper

NOTE: After completing Scenarios 1 and 2, you are now able to see what parts of

the financial statements would change as a result of a change in depreciation meth-

ods. Therefore, you should now be able to create the financial statements without

first recording the transactions using the horizontal financial statements model.

Units-of-Production Depreciation

Income Statements

2015

2016

2017

2018

2019

Rent revenue

$8,000

$4,800

$9,600

$6,400

$ 0

Depreciation expense

Operating income

Gain on sale of automobile

Net income

$

$

$

$

$

Balance Sheets

Assets

Cash

$

$

$

$

$

Automobile

Accumulated depreciation

Book value, auto

Total assets

$

$

$

$

$

Stockholders’ equity

Common stock

$21,000

$21,000

$21,000

$21,000

$21,000

Retained earnings

Total stockholders’ equity

$24,200

$27,400

$30,600

$33,800

$34,100

Statements of Cash Flows

Operating activities

Inflow from customer

$ 8,000

$ 4,800

$ 9,600

$ 6,400

$ 0

Investing activities

Outflow for automobile

Inflow from sale of auto

Financing activities

Inflow from stock issue

Net change in cash

Beginning cash balance

Ending cash balance

$9,000

$13,800

$23,400

$29,800

$34,100

8-21

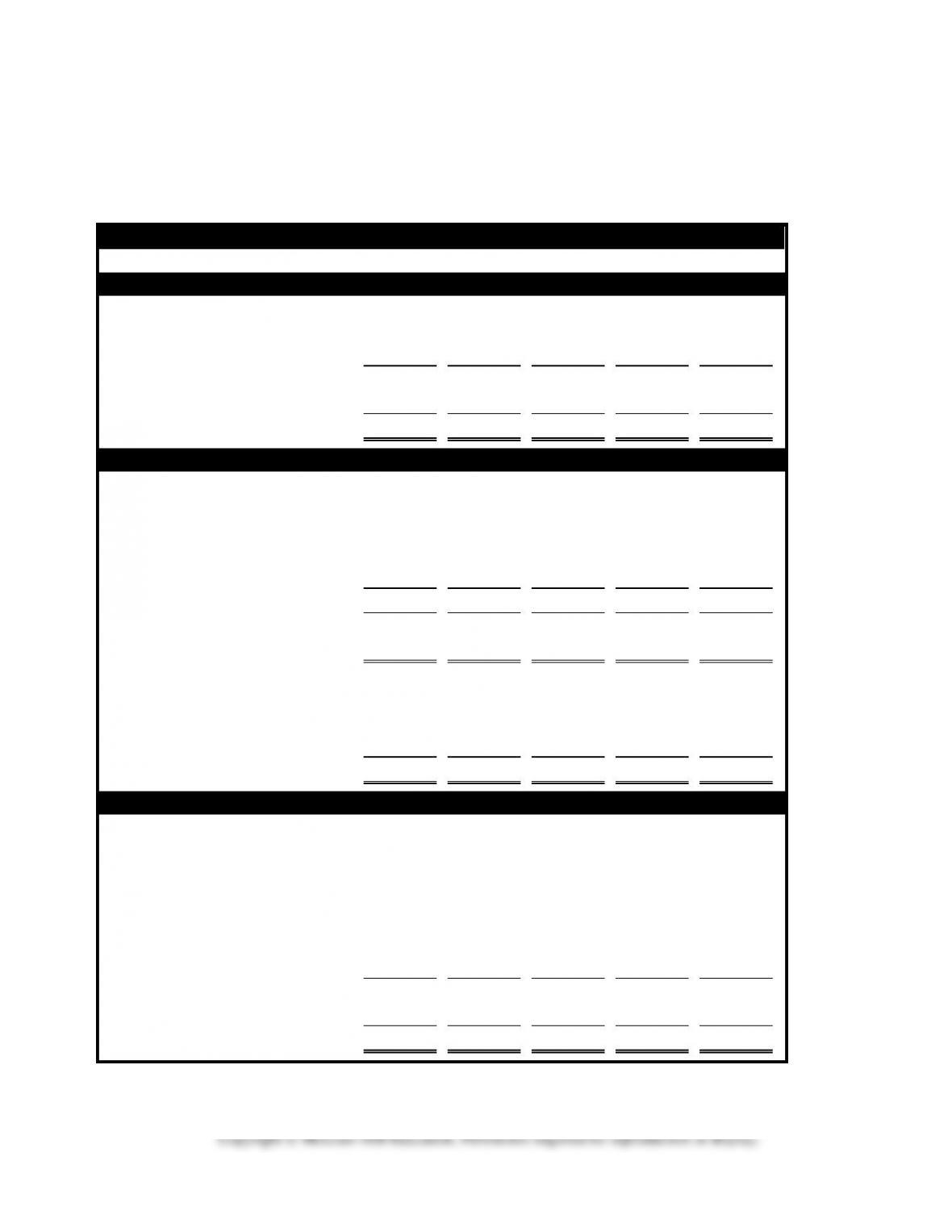

Demonstration Problem 8-2 Workpaper

1. Paid $1,000 cash for maintenance cost.

Assets

=

Liab.

+

Equity

Rev.

–

Exp.

=

Net Inc.

Cash Flow

Cash

+

Equip.

–

Accum.

Depr.

=

Ret. Earn.

1,000

+

5,000

–

2,000

=

0

+

4,000

0

–

0

=

0

0

+

5,000

–

2,000

=

0

+

3,000

0

–

1,000

=

(1,000)

2. Paid $1,000 cash to improve the quality of the equipment.

Assets

=

Liab.

+

Equity

Rev.

–

Exp.

=

Net Inc.

Cash Flow

Cash

+

Equip.

–

Accum.

Depr.

=

Ret. Earn.

1,000

+

5,000

–

2,000

=

0

+

4,000

0

–

0

=

0

0

+

6,000

–

2,000

=

0

+

4,000

0

–

0

=

0

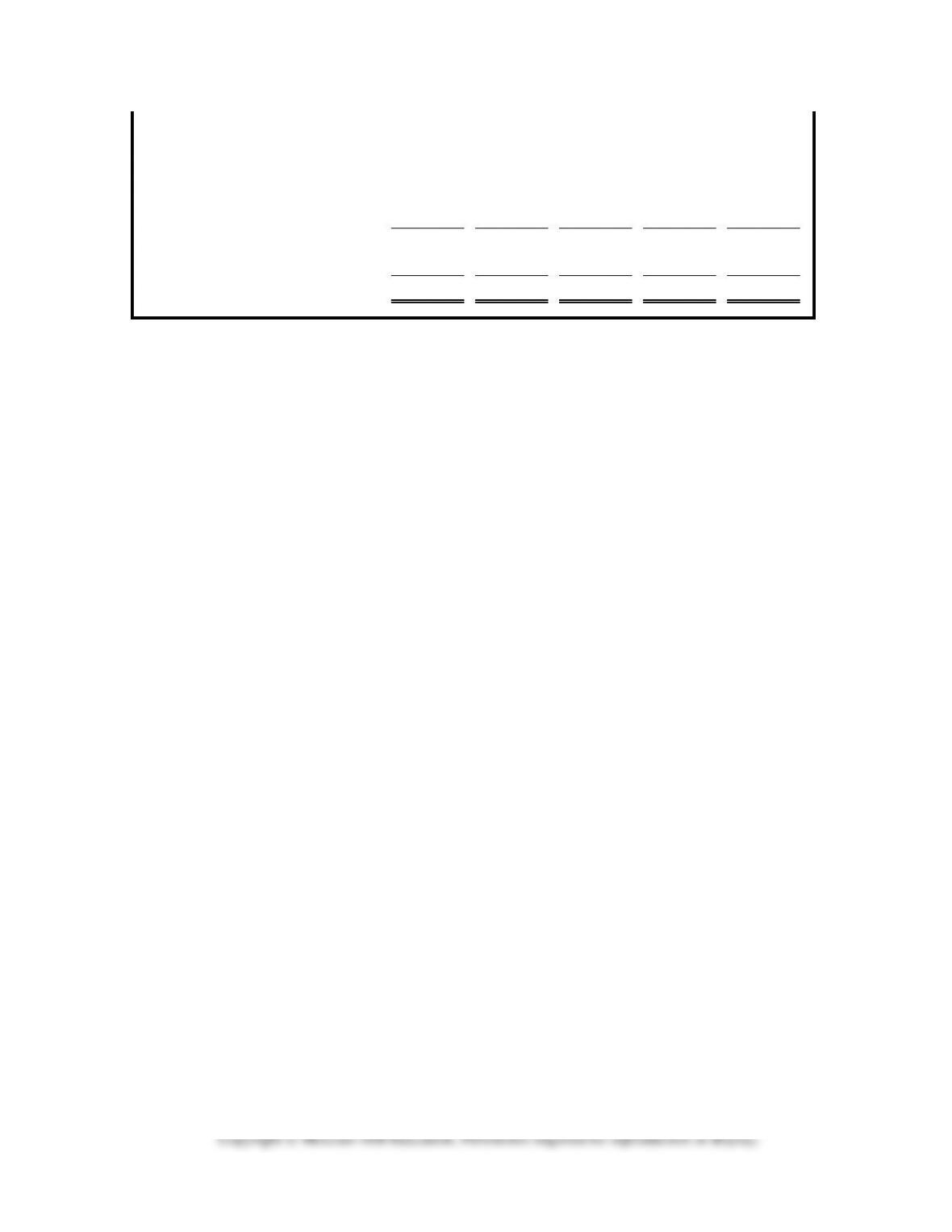

3. Paid $1,000 cash to extend the useful life of the equipment.

Assets

=

Liab.

+

Equity

Rev.

–

Exp.

=

Net Inc.

Cash Flow

Cash

+

Equip.

–

Accum.

Depr.

=

Ret. Earn.

1,000

+

5,000

–

2,000

=

0

+

4,000

0

–

0

=

0

0

+

5,000

–

1,000

=

0

+

4,000

0

–

0

=

0

8-22

Quiz Questions for Chapter 8

1. A truck was purchased for $25,000. It has a six-year life and a $4,000 salvage value. Using straight-line

depreciation, what is the asset’s carrying value (book value) after 3 years?

a. $12,500.

b. $25,000.

c. $21,000.

d. $14,500.

2. On January 1, 2015, Superior Landscaping Company paid $17,000 to buy a stump grinder. If Superior

uses the grinder to remove 2,500 stumps per year, it would have an estimated useful life of 10 years and a

salvage value of $4,500. The amount of depreciation expense for the year 2015, using units–of–

production depreciation and assuming that 3,500 stumps were removed, is

a. $2,380.

b. $1,750.

c. $1,700.

d. $1,250.

3. The sale for $2,000 of equipment that cost $8,000 and has accumulated depreciation of $6,700 would

result in a

a. gain of $2,000.

b. gain of $700.

c. loss of $700.

d. loss of $1,300.

4. Underestimating the number of tons of a mineral that can be mined over a mineral deposit’s life will re-

sult in

a. overstated net income each year.

b. overstated total assets each year.

c. overstated depletion expense each year.

d. no effect on total assets each year.

5. A copyright is obtained for what becomes a very successful book. The publisher expects the book to

generate sales for 10 years. The copyright should be amortized over

a. 2 to 4 years.

b. 10 years.

c. 40 years.

d. the author’s life plus 50 years.

8-23

The following information pertains to the next two questions. Z Company purchased an asset for $24,000

on January 1, 2015. The asset was expected to have a four-year life and a $4,000 salvage value.

6. The amount of depreciation expense for 2015 using double–declining-balance would be

a. $12,000.

b. $3,000.

c. $6,000.

d. $2,000.

7. Assume that Z Company uses straight-line depreciation. If on January 1, 2016, Z Company sells the as-

set for $10,000, the statement of cash flows would report a

a. $1,000 cash inflow from gain on the sale of the asset in the operating activities section.

b. $10,000 cash inflow from an asset disposal in the investing activities section.

c. $9,000 cash inflow from an asset disposal in the financing activities section.

d. a and c.

8. On January 1, 2015, Fulsom Corporation purchased a machine for $50,000. Fulsom paid shipping ex–

penses of $500 as well as installation costs of $1,200. Fulsom estimated the machine would have a use-

ful life of ten years and an estimated salvage value of $3,000. If Fulsom records depreciation using the

straight-line method, depreciation expense for 2016 is

a. $4,870.

b. $5,170.

c. $5,270.

d. $5,570.

9. Hickory Ridge Company purchased land and a building for cash of $920,000. The individual assets were

appraised at the following market values:

Land $614,400

Building $345,600

Recording the land in the accounting records would

a. increase land by $588,800.

b. increase land by $614,400.

c. increase assets by $920,000.

d. Both a and c.

10. The Silverman Company purchased equipment on November 1, 2015 for $35,000. The equipment has a

10-year life and a zero salvage value. The company uses straight-line depreciation for financial report-

ing and MACRS for seven-year property for tax purposes. Based on this information, which of the fol-

lowing is true?

a. In the early years of the asset’s life, higher depreciation expenses will be shown on the income

statement than on the tax return.

b. There will be deferred taxes shown on the income statement.

c. Taxes due on the tax return will be lower in the early years of the asset’s life because of the depre-

ciation charges.

d. Taxes due on the tax return will be lower in the later years of the asset’s life because of the deprecia-

tion charges.

8-24

11. Penny Lane and Associates purchased a generator on January 1, 2015, for $6,300. The generator was

estimated to have a five-year life and a salvage value of $600. At the beginning of 2017, the company

revised the expected life of the asset to six years and revised the salvage value to $300. Using straight-

line depreciation, the depreciation expense recorded in 2017 would

a. decrease assets and equity by $1,140.

b. decrease assets and equity by $930.

c. decrease assets and equity by $1,005.

d. decrease assets and equity by $1,500.

12. Which of the following statements about goodwill is true?

a. On the purchase date, the amount of goodwill is measured by subtracting the fair market value of as-

sets acquired from the amount paid for those assets.

b. The amount of goodwill is recorded as an asset.

c. Recording impairment of goodwill reduces the amount of net income.

d. All of the above.

13. XYZ Company paid cash for a capital expenditure that improved the operating efficiency of one of its

assets. Which of the following reflects how this expenditure affects the company’s financial statements?

Assets

=

Liab.

+

Equity

Rev.

–

Exp.

=

Net Inc.

Cash Flow

a.

+ –

NA

NA

NA

NA

NA

– IA

b.

+ –

NA

NA

NA

NA

NA

NA

c.

–

NA

–

NA

+

–

– OA

d.

NA

NA

NA

NA

NA

NA

NA

14. KLM Company experienced an accounting event that affected its financial statements as indicated below:

Assets

=

Liab.

+

Equity

Rev.

–

Exp.

=

Net Inc.

Cash Flow

–

NA

–

NA

+

–

– OA

Which of the following events could have caused these effects?

a. recognizing depreciation.

b. paying cash for a capital expenditure.

c. amortizing a patent.

d. none of the above.

8-25

Quiz Answers

Question

Answer

1

D

2

B

3

B

4

C

5

B

6

A

7

B

8

A

9

A

10

C

11

B

12

D

13

A

14

D

Copyright © McGraw-Hill Education. Permission required for reproduction or display.

8-26

Summary Outline of a Lesson Plan for Chapter 8

I. Begin Chapter 8 by discussing the difference between current, long-term, tangi-

ble, and intangible assets.

II. Demonstration Problem 8-1 illustrates financial statements for three different

depreciation methods across multiple accounting cycles. Explain the concepts of

depreciation and salvage value. Hand out work papers and have students work along

with you as you introduce new depreciation methods. As students work, walk around

the room and make sure that students fully understand one method before moving on

to the next.

III. Demonstration Problem 8-2 introduces accounting for capital expenditures and

maintenance costs incurred after the acquisition date. Draw or display a state-

ments model. Then show students how maintenance costs and capital expenditures af-

fect financial statements differently.

IV. Introduce accounting for natural resources. Draw the parallel between units-of-

production depreciation and depletion. Use Exercise 8-17A as a demonstration prob-

lem.

V. Introduce accounting for intangible assets. Draw the parallel between straight-line

depreciation and amortization computations. Use Exercise 8-18A as a demonstration

problem.

Time considerations and homework assignments. Plan to spend approximately three

hours of class time to cover the material in this chapter: two hours covering depreciation

methods and one hour for related topics. Consider assigning the following exercises or prob–

lems for homework: Exercise 8-2 A or B (distinguish between current and long-term assets),

Exercise 8-3 A or B (identify tangible versus intangible assets), Problem 8-26 A or B (depre-

ciation over multiple accounting cycles), Problem 8-27 A or B (compute different deprecia-

tion methods), Problem 8-32 A or B (subsequent asset expenditures), Problem 8-34 A or B

(amortization). Eliminate or select substitute problems from the text as you deem appropri-

ate.