SOLUTIONS TO EXERCISES – SERIES B – CHAPTER 10

EXERCISE 10-1B

Points that should be noted:

a. The carrying value of the amortized note (option 2) will be reduced by

the amount of the principal payments for each period. However, the

carrying value of the note with all principal due at maturity (option 1)

EXERCISE 10-2B

Monroe Co.

Amortization Schedule

$80,000, 4-Yr. Term Note, 6% Interest Rate

Year

Prin. Bal.

on Jan 1

Cash Pay.

Dec. 31

Applied to

Interest

Applied to

Principal

Prin. Bal.

End of Period

2016

$80,000

$23,087

$4,800

$18,287

$61,713

2017

61,713

23,087

3,703

19,384

42,329

2018

42,329

23,087

2,540

20,547

21,782

2019

21,782

23,087

1,305*

21,782

-0-

*Adjusted due to rounding.

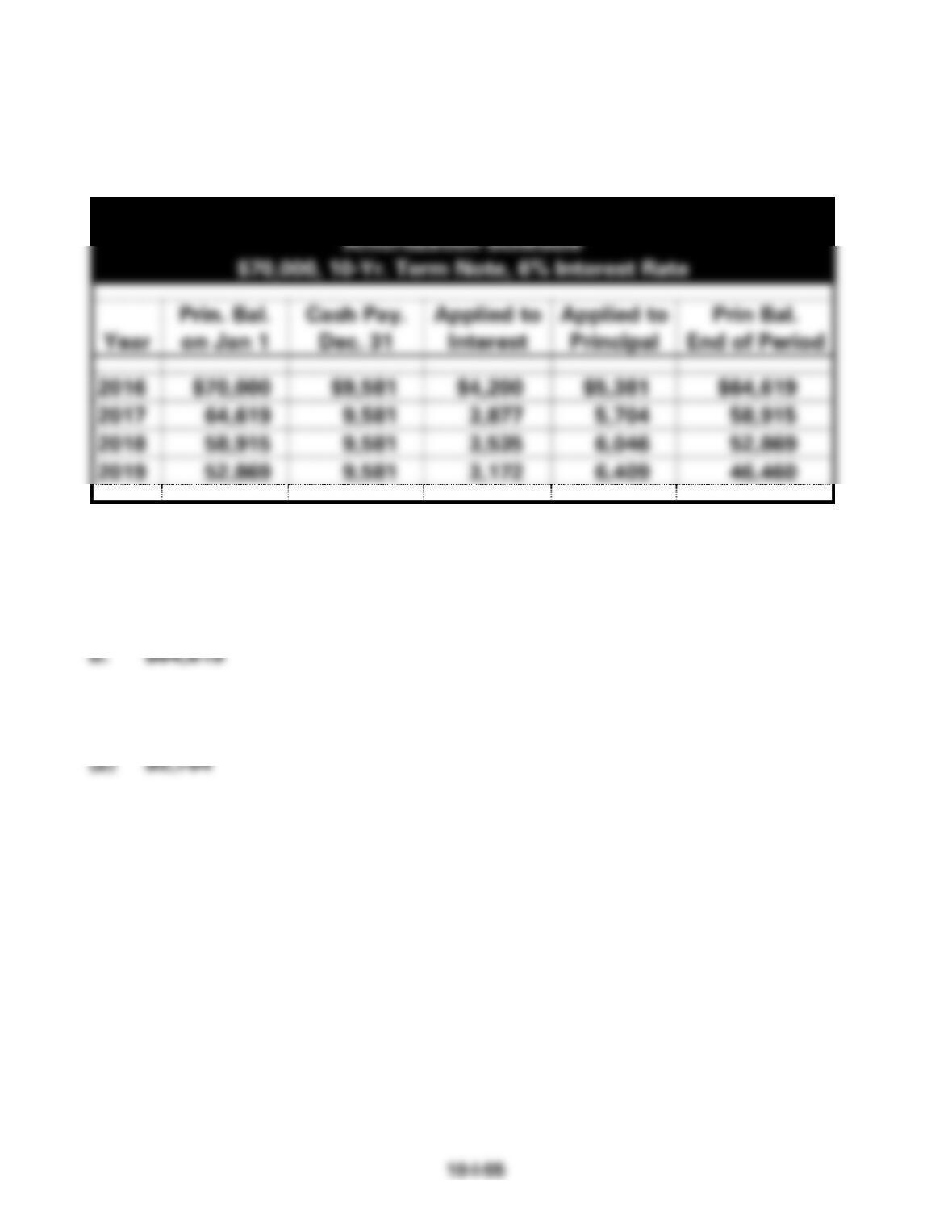

EXERCISE 10-3B

The first four years are provided for the use of the instructor:

Hood Company

Amortization Schedule

$70,000, 10-Yr. Term Note, 6% Interest Rate

Year

Prin. Bal.

on Jan 1

Cash Pay.

Dec. 31

Applied to

Interest

Applied to

Principal

Prin Bal.

End of Period

2016

$70,000

$9,581

$4,200

$5,381

$64,619

2017

64,619

9,581

3,877

5,704

58,915

2018

58,915

9,581

3,535

6,046

52,869

2019

52,869

9,581

3,172

6,409

46,460

a.

(1) $4,200

(2) $5,381

c.

(1) $3,877

EXERCISE 10-4B

10-I-57

Interest Expense: $37,741 x 5% = $1,887 (rounded)

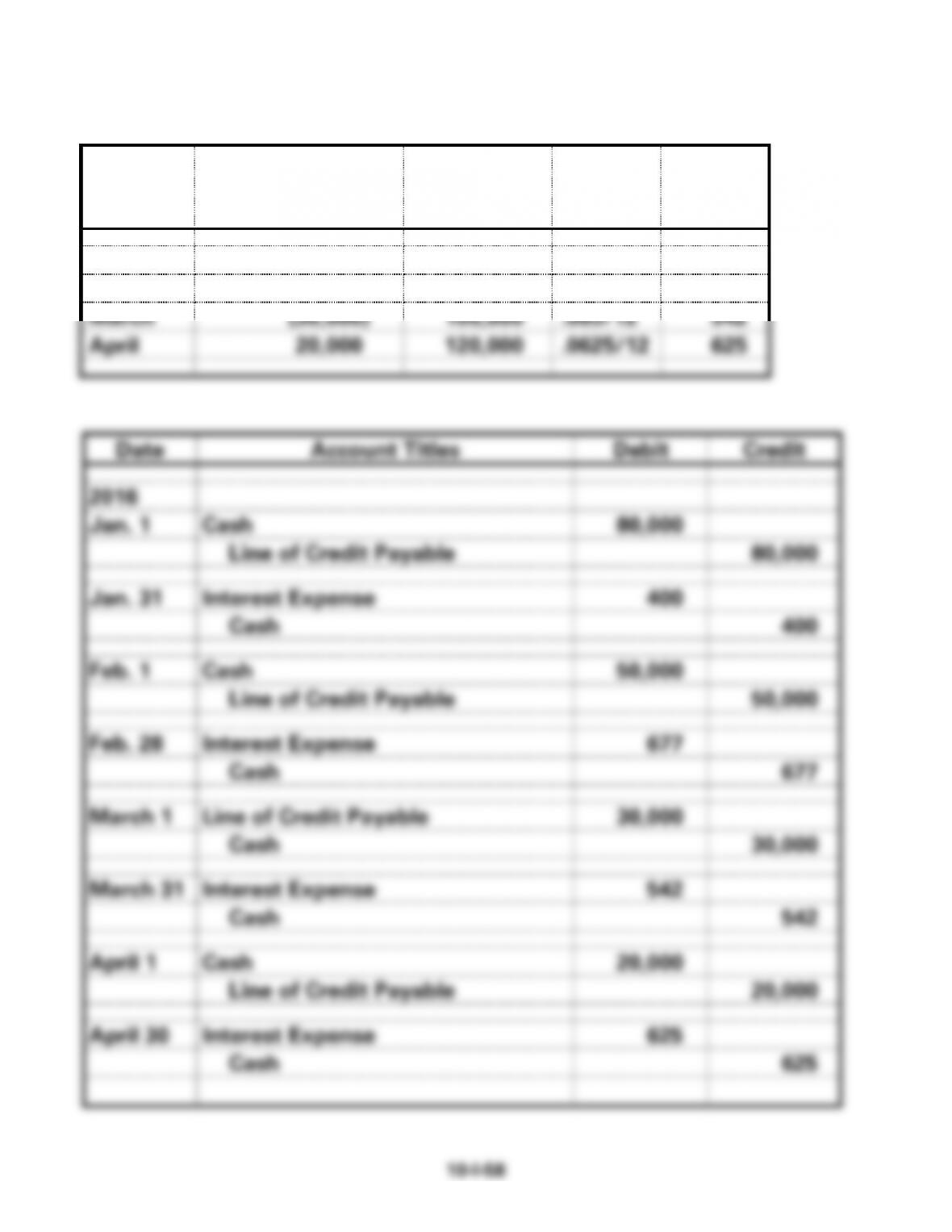

EXERCISE 10-5B

Month

Amount

Borrowed

(Repaid)

Balance End

of Month

Interest

Rate

Interest

Expense

January

$80,000

$ 80,000

.06/12

$400

February

50,000

130,000

.0625/12

677

March

(30,000)

100,000

.065/12

542

April

20,000

120,000

.0625/12

625

10-I-59

EXERCISE 10-6B

a.

Pluto Company

General Journal

Date

Account Titles

Debit

Credit

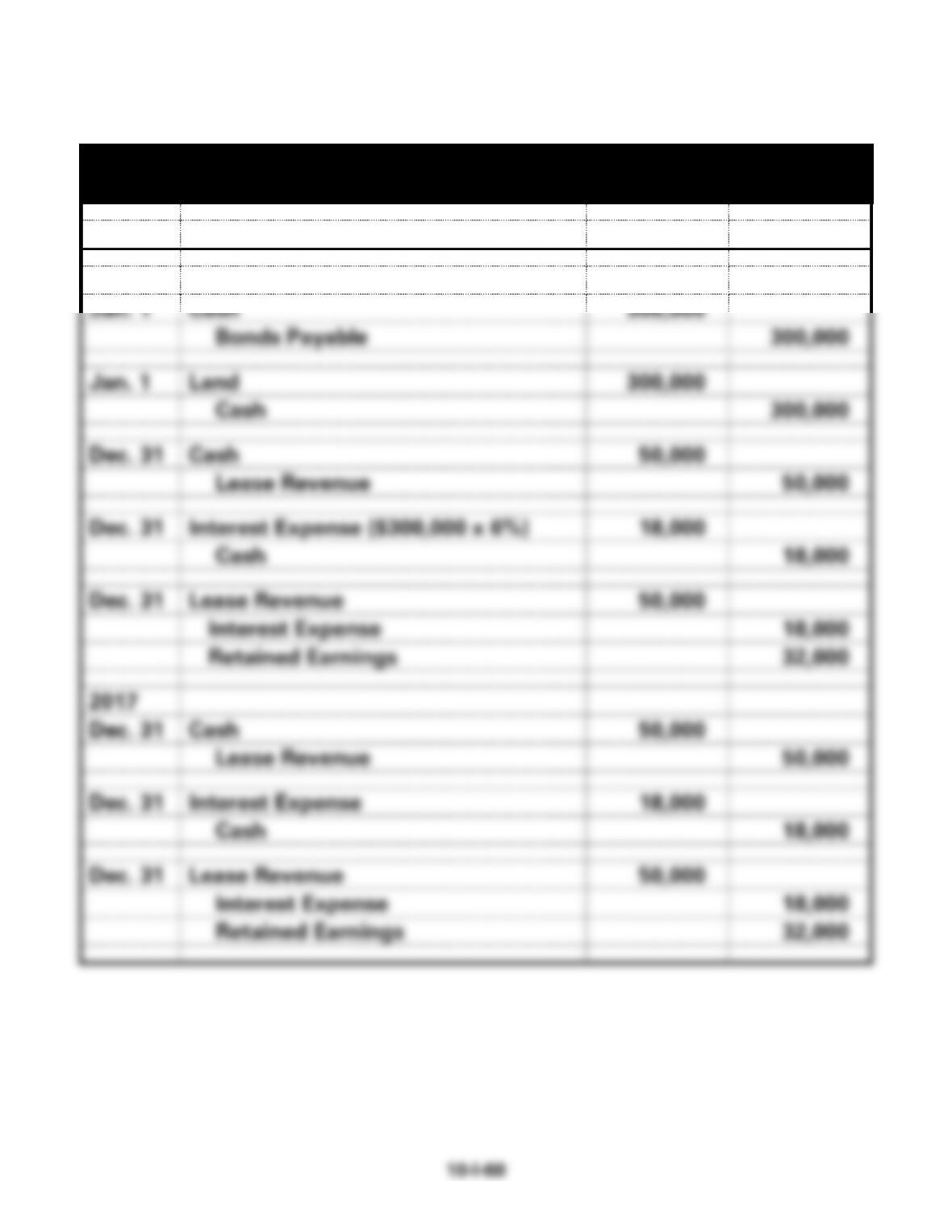

2016

Jan. 1

Cash

300,000

Bonds Payable

300,000

Jan. 1

Land

300,000

Cash

300,000

Dec. 31

Cash

50,000

Lease Revenue

50,000

Dec. 31

Interest Expense ($300,000 x 6%)

18,000

Cash

18,000

Dec. 31

Lease Revenue

50,000

Interest Expense

18,000

Retained Earnings

32,000

2017

Dec. 31

Cash

50,000

Lease Revenue

50,000

Dec. 31

Interest Expense

18,000

Cash

18,000

Dec. 31

Lease Revenue

50,000

Interest Expense

18,000

Retained Earnings

32,000

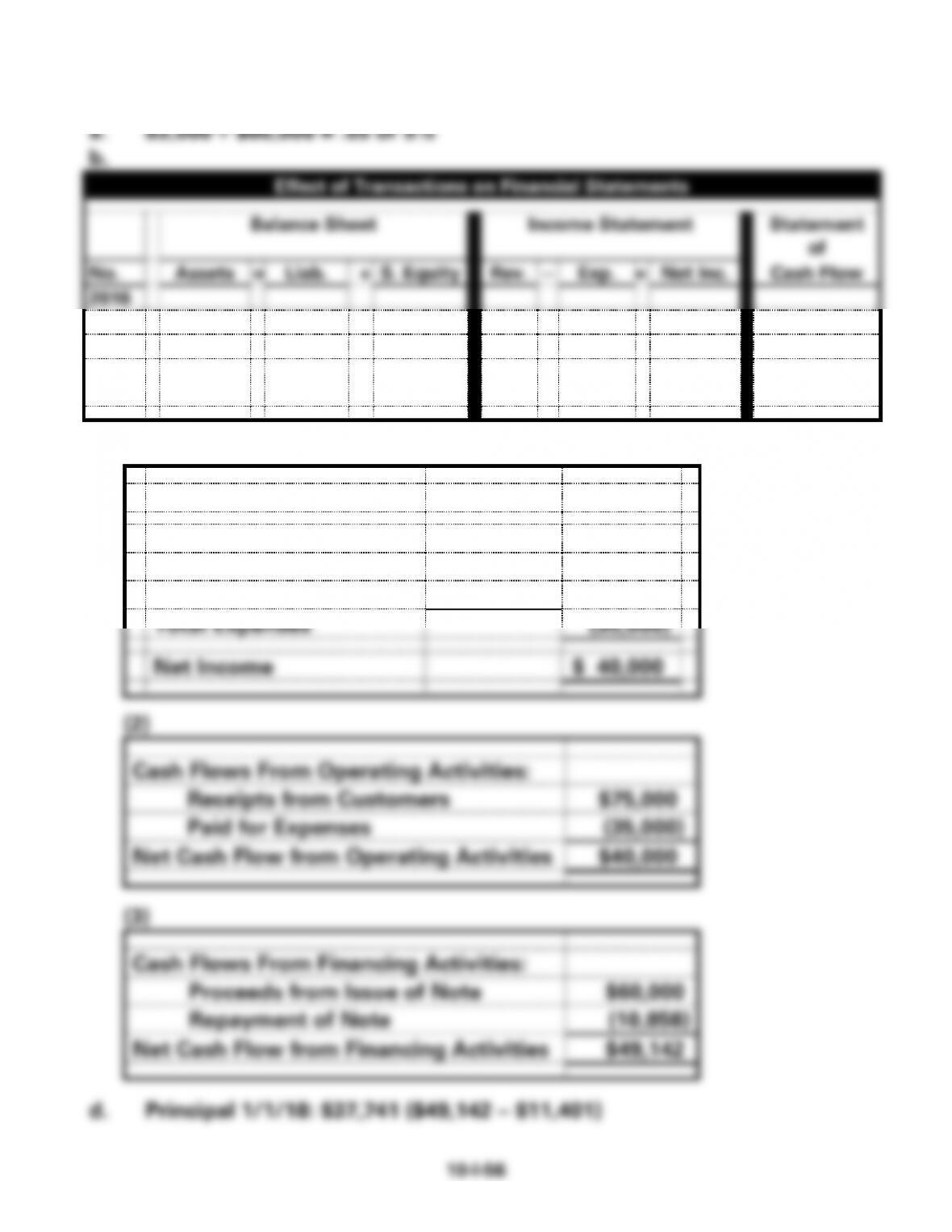

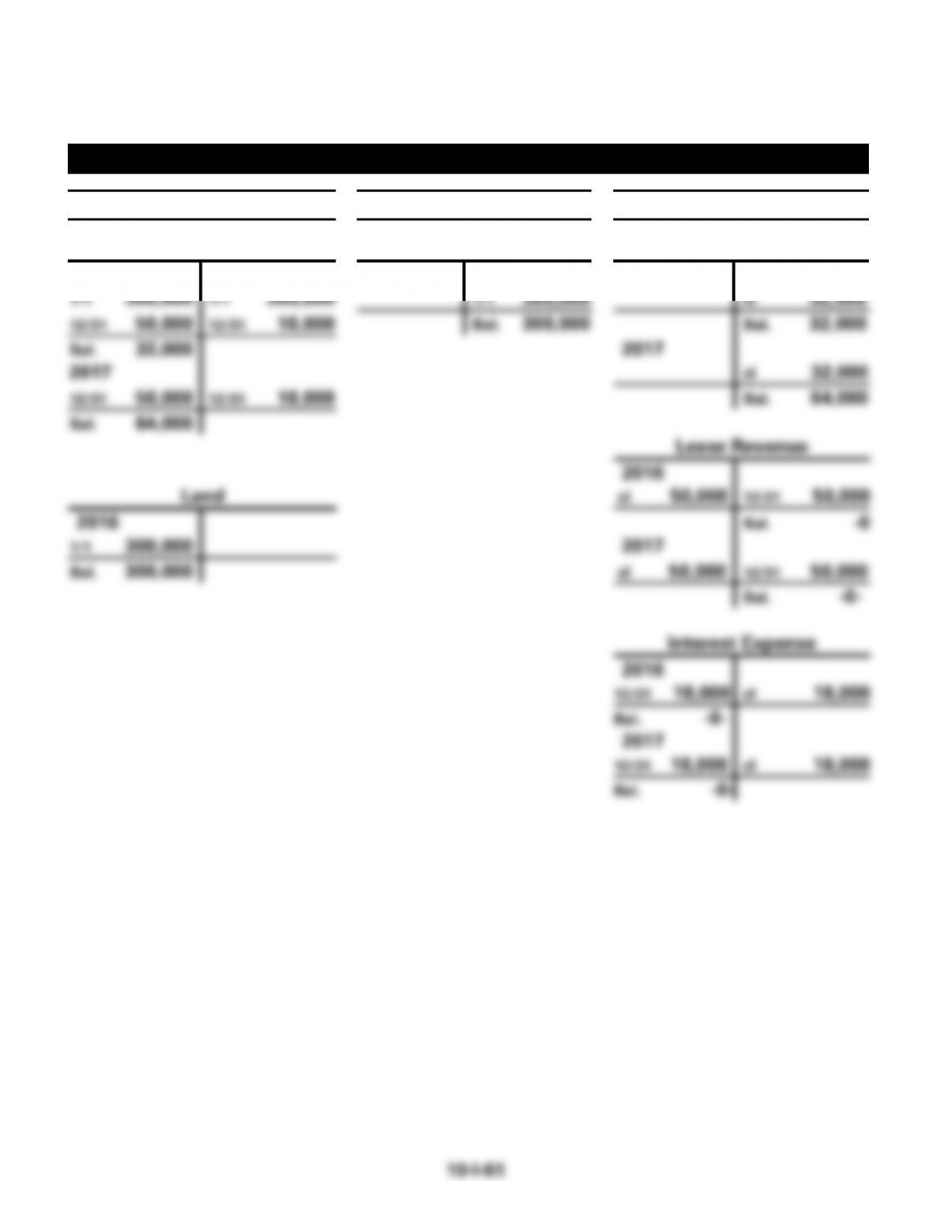

EXERCISE 10-6B a. (cont.)

Pluto Company

Assets

=

Liabilities

+

Stockholders’ Equity

Cash

Bonds Payable

Retained Earnings

2016

2016

2016

1/1 300,000

1/1 300,000

1/1 300,000

cl 32,000

12/31 50,000

12/31 18,000

Bal. 300,000

Bal. 32,000

Bal. 32,000

2017

2017

cl 32,000

12/31 50,000

12/31 18,000

Bal. 64,000

Bal. 64,000

Lease Revenue

2016

Land

cl 50,000

12/31 50,000

2016

Bal. -0

1/1 300,000

2017

Bal. 300,000

cl 50,000

12/31 50,000

Bal. -0-

Interest Expense

2016

12/31 18,000

cl 18,000

Bal. -0-

2017

12/31 18,000

cl 18,000

Bal. -0-

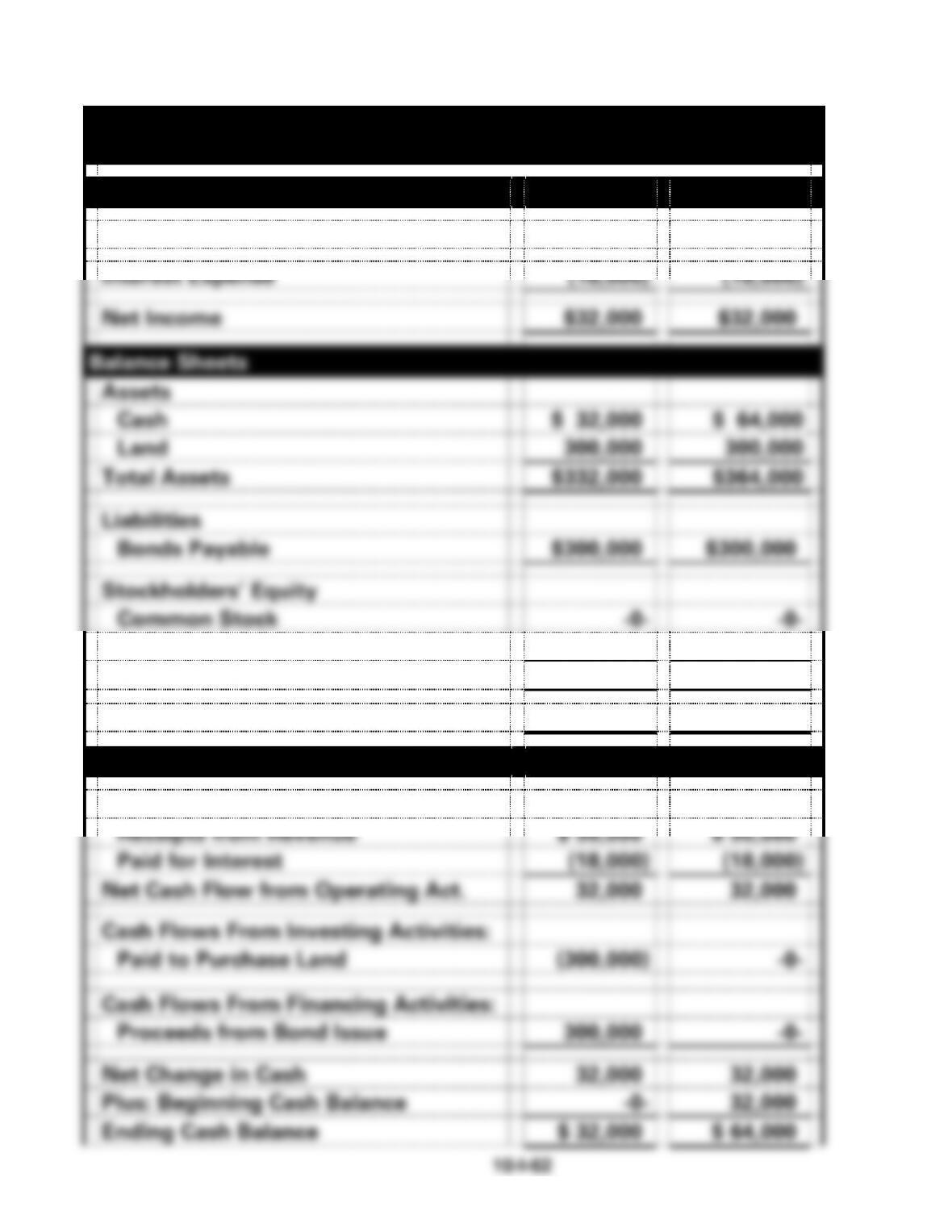

EXERCISE 10-6B b. (cont.)

Pluto Company Financial Statements

For the Year Ended December 31

Income Statements

2016

2017

Lease Revenue

$50,000

$50,000

Interest Expense

(18,000)

(18,000)

Net Income

$32,000

$32,000

Balance Sheets

Assets

Cash

$ 32,000

$ 64,000

Land

300,000

300,000

Total Assets

$332,000

$364,000

Liabilities

Bonds Payable

$300,000

$300,000

Stockholders’ Equity

Common Stock

-0-

-0-

Retained Earnings

32,000

64,000

Total Stockholders’ Equity

32,000

64,000

Total Liab. and Stockholders’ Equity

$332,000

$364,000

Statements of Cash Flows

Cash Flows From Operating Activities:

Receipts from Revenue

$ 50,000

$ 50,000

Paid for Interest

(18,000)

(18,000)

Net Cash Flow from Operating Act.

32,000

32,000

Cash Flows From Investing Activities:

Paid to Purchase Land

(300,000)

-0-

Cash Flows From Financing Activities:

Proceeds from Bond Issue

300,000

-0-

Net Change in Cash

32,000

32,000

Plus: Beginning Cash Balance

-0-

32,000

Ending Cash Balance

$ 32,000

$ 64,000

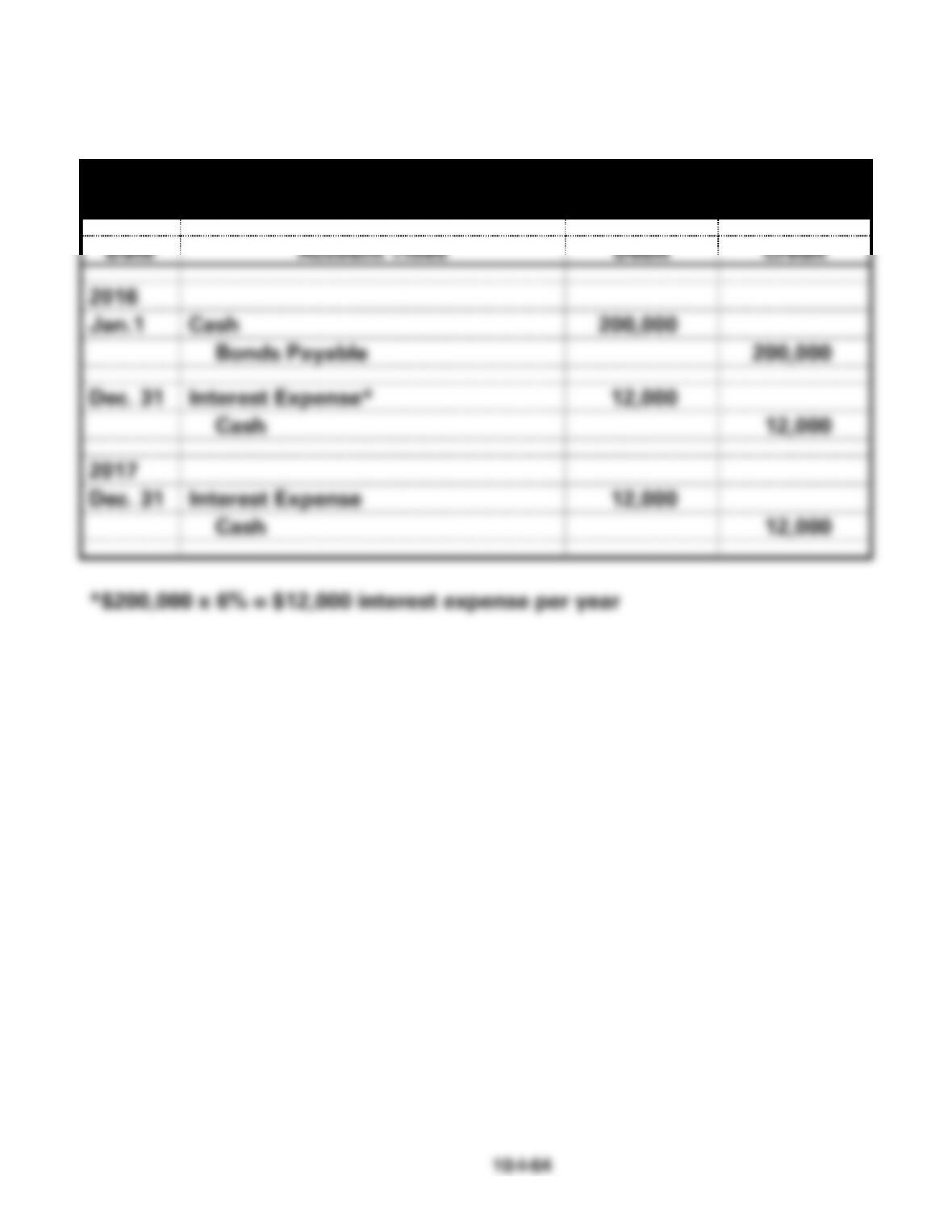

EXERCISE 10-7B

Hazman Corp.

General Journal

Date

Account Titles

Debit

Credit

2016

Jan.1

Cash

200,000

Bonds Payable

200,000

Dec. 31

Interest Expense*

12,000

Cash

12,000

2017

Dec. 31

Interest Expense

12,000

Cash

12,000

*$200,000 x 6% = $12,000 interest expense per year

EXERCISE 10-8B

Tyler Co.

Date

Account Titles

Debit

Credit

2016

Jan. 1

Cash

250,000

Bonds Payable

250,000

2017

Dec. 31

Loss on Bond Redemption*

5,000

Bonds Payable

250,000

Cash

255,000

EXERCISE 10-9B

a. $150,000 x 6% = $9,000

b. $150,000 x 6% x 6/12 = $4,500 on June 30

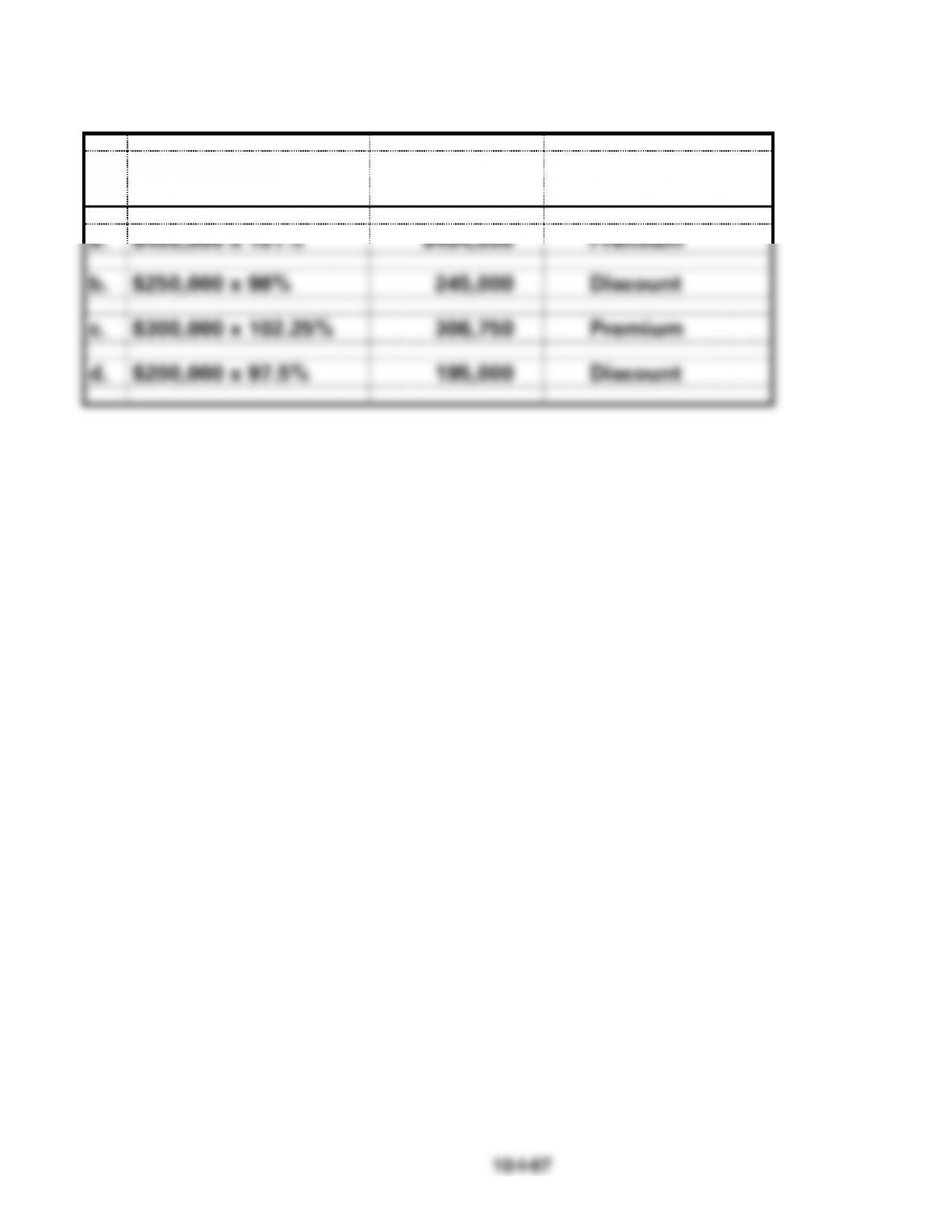

EXERCISE 10-10B

Face x Selling Price

Cash Proceeds

Discount or

Premium

a.

$400,000 x 101%

$404,000

Premium

b.

$250,000 x 98%

245,000

Discount

c.

$300,000 x 102.25%

306,750

Premium

d.

$200,000 x 97.5%

195,000

Discount

EXERCISE 10-11B

a. Discount

b. Face

EXERCISE 10-12B

EXERCISE 10-13B

a. $120,000 x 1% = $1,200; Premium

EXERCISE 10-14B

a.

Effect of Transactions on Financial Statements

Balance Sheet

Income Statement

No.

Assets

=

Liab.

+

S.

Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

1.

+

+

NA

NA

NA

NA

+ FA

2.*

−

+

−

NA

+

−

− OA

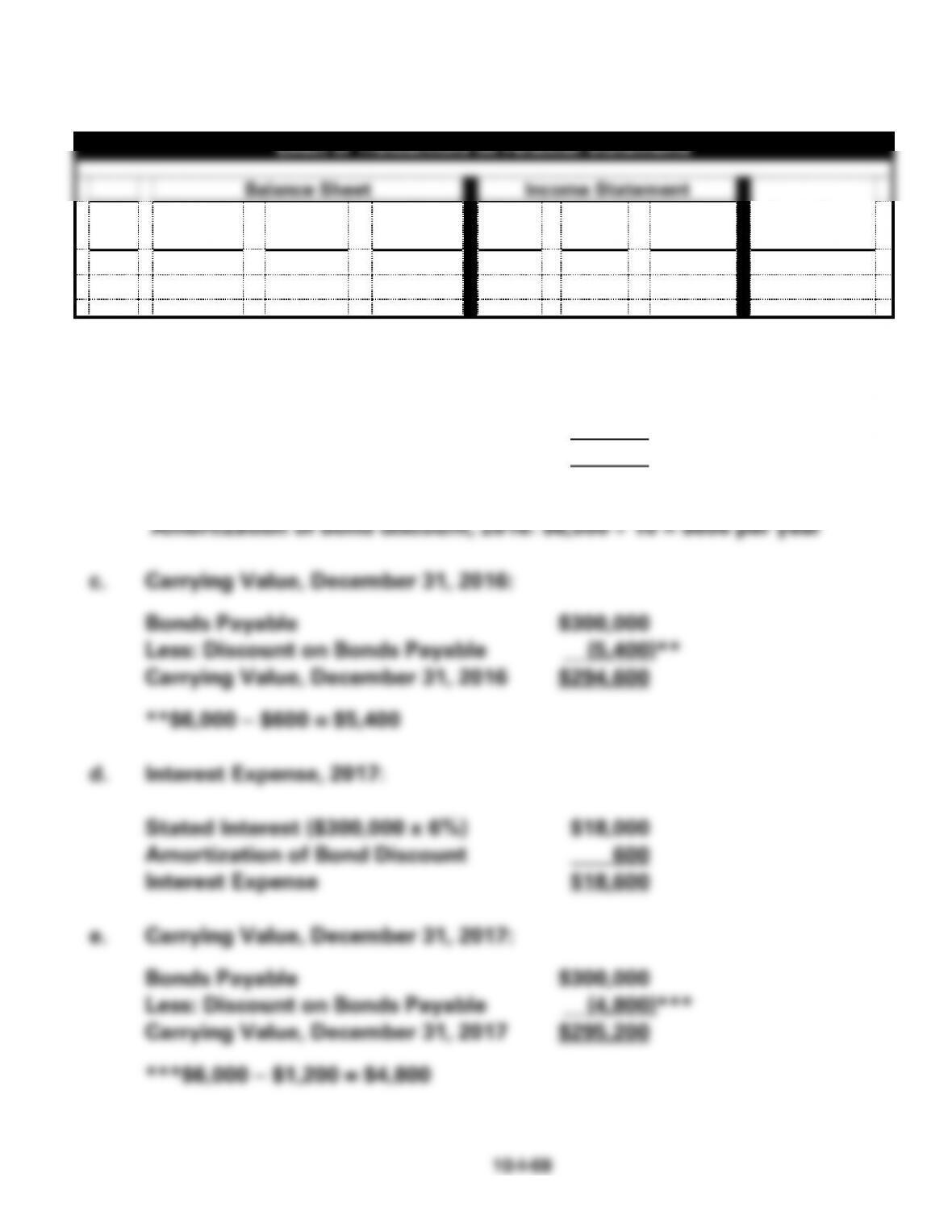

b. Interest Expense, 2016:

Stated Interest ($300,000 x 6%) $18,000

Amortization of Bond Discount* 600

Interest Expense $18,600

*Discount: $300,000 x 2% = $6,000

EXERCISE 10-15B

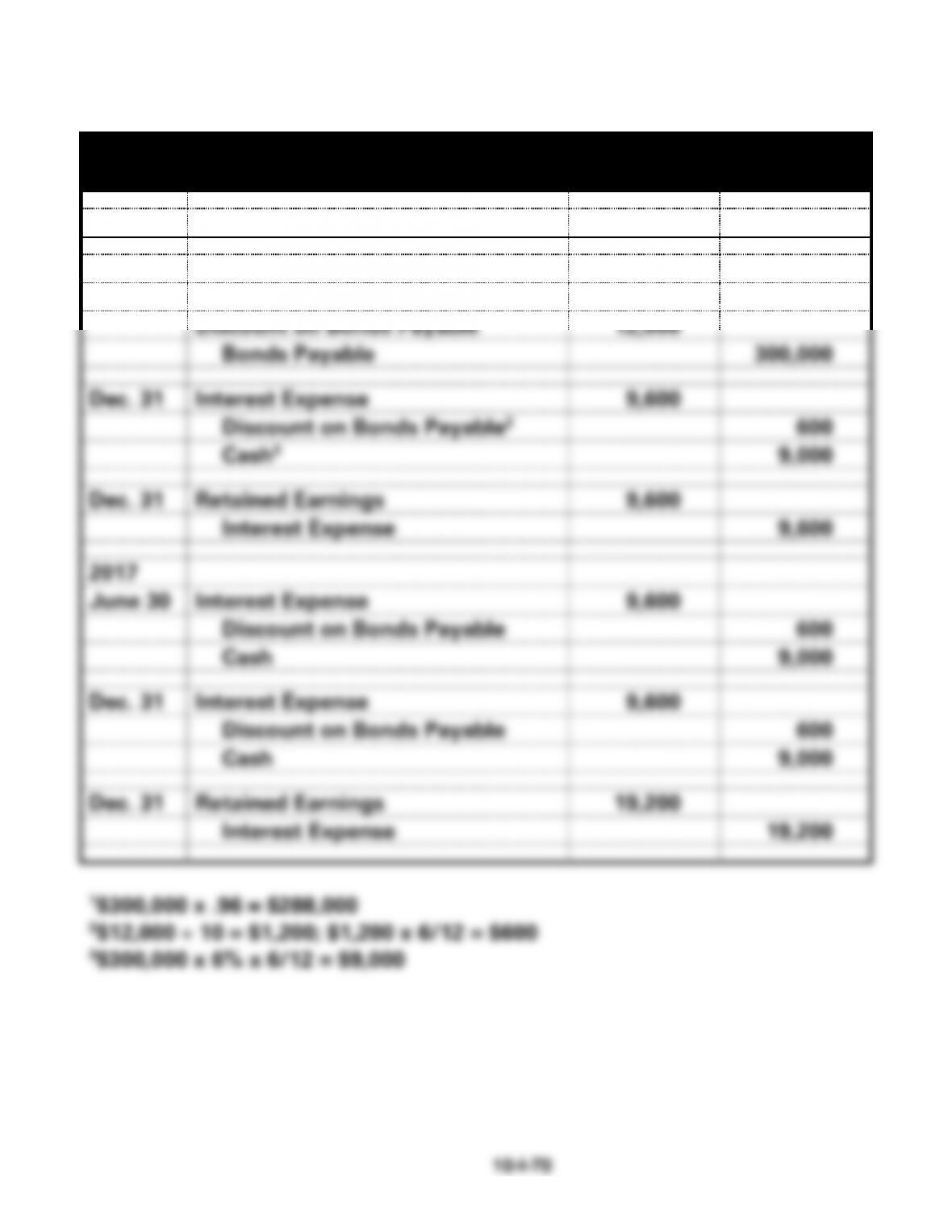

a.

Dixon Construction, Inc.

General Journal

Date

Account Titles

Debit

Credit

2016

July 1

Cash1

288,000

Discount on Bonds Payable

12,000

Bonds Payable

300,000

Dec. 31

Interest Expense

9,600

Discount on Bonds Payable2

600

Cash3

9,000

Dec. 31

Retained Earnings

9,600

Interest Expense

9,600

2017

June 30

Interest Expense

9,600

Discount on Bonds Payable

600

Cash

9,000

Dec. 31

Interest Expense

9,600

Discount on Bonds Payable

600

Cash

9,000

Dec. 31

Retained Earnings

19,200

Interest Expense

19,200

EXERCISE 10-15B a. (cont.)

Dixon Construction, Inc.

T-accounts

Assets

=

Liabilities

+

Stockholders’ Equity

Cash

Bonds Payable

Retained Earnings

2016

2016

2016

7/1 288,000

12/31 9,000

7/1 300,000

cl 9,600

Bal. 279,000

Bal. 300,000

Bal. 9,600

2017

2017

6/30 9,000

cl 19,200

12/31 9,000

Disc. on Bonds Pay.

Bal. 28,800

Bal. 261,000

2016

7/1 12,000

12/31 600

Interest Expense

Bal. 11,400

2016

2017

12/31 9,600

cl 9,600

6/30 600

Bal. -0-

12/31 600

2017

Bal. 10,200

6/30 9,600

12/31 9,600

cl 19,200

Bal. -0-

EXERCISE 10-15B (cont.)

b.

Dixon Construction, Inc.

Balance Sheet

As of December 31

2016

2017

Liabilities

Bonds Payable

$300,000

$300,000

Discount on Bonds Payable

(11,400)

(10,200)

Carrying Value of Bonds

288,600

289,800

Total Liabilities

$288,600

$289,800