Chapter 12 Statement of Cash Flows

12–95

PROBLEM 12–21B

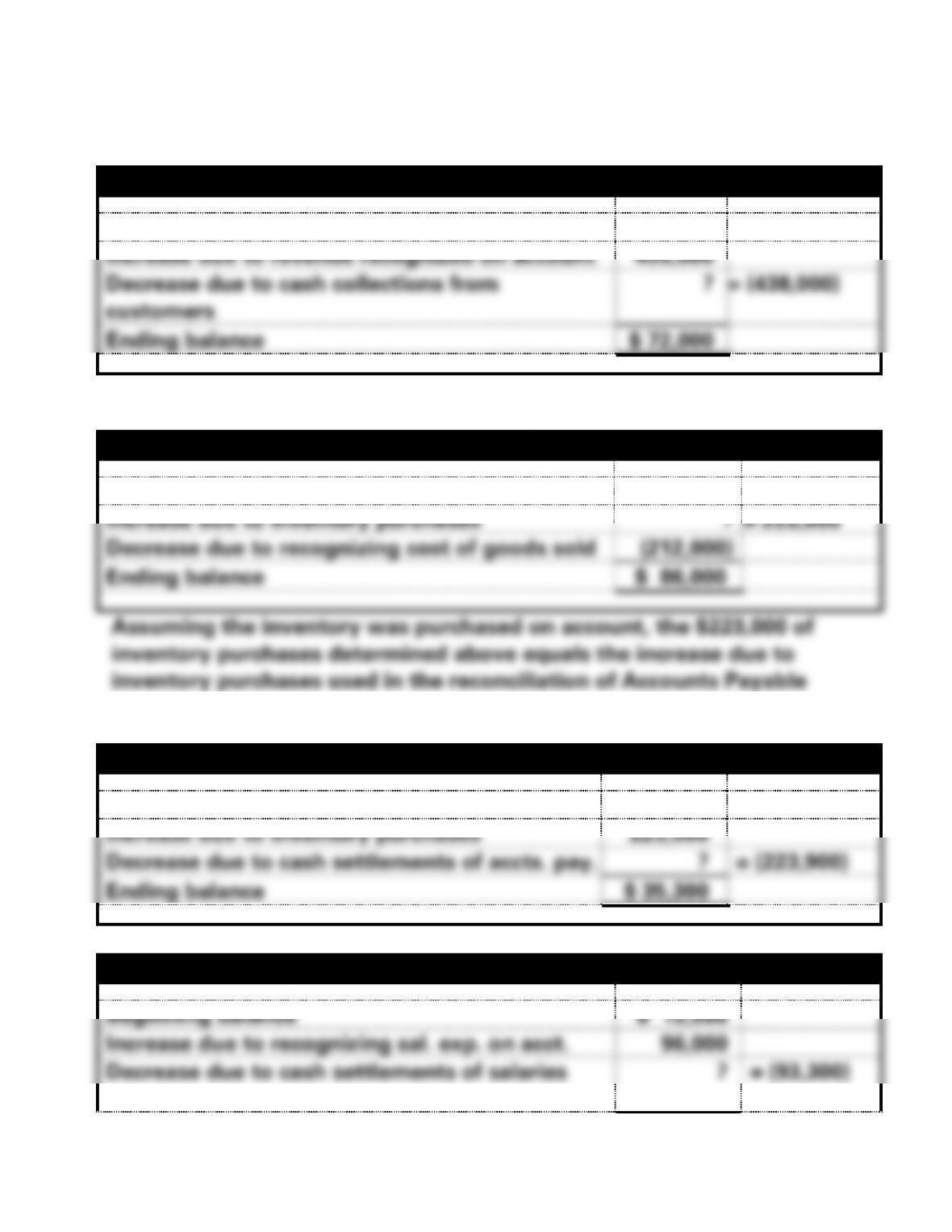

(1) Reconciliation of Accounts Receivable

Beginning balance

$ 60,000

Increase due to revenue recognized on account

450,000

Decrease due to cash collections from

customers

?

= (438,000)

Ending balance

$ 72,000

(2) Reconciliation of Inventory

Beginning balance

$ 75,000

Increase due to inventory purchases

?

= 223,000

Decrease due to recognizing cost of goods sold

(212,000)

Ending balance

$ 86,000

below.

(2) Continued: Reconciliation of Accounts Payable

Beginning balance

$ 36,200

Increase due to inventory purchases

223,000

Decrease due to cash settlements of accts. pay.

?

= (223,900)

Ending balance

$ 35,300

(3) Reconciliation of Salaries Payable

Beginning balance

$ 15,500

Increase due to recognizing sal. exp. on acct.

96,000

Decrease due to cash settlements of salaries

pay.

?

= (93,300)

Chapter 12 Statement of Cash Flows

12–96

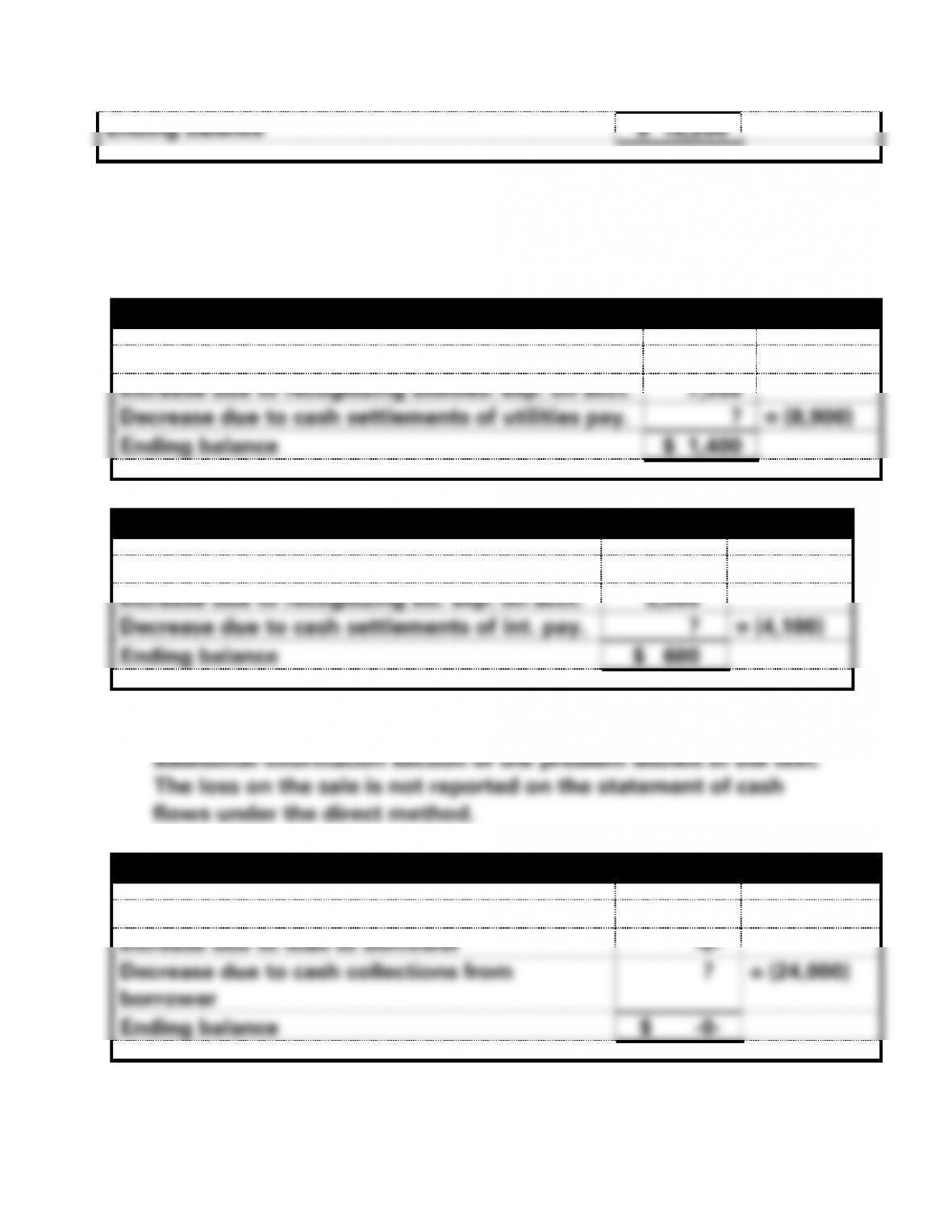

Ending balance

$ 18,200

PROBLEM 12-21B (cont.)

(4) Reconciliation of Utilities Payable

Beginning balance

$ 2,800

Increase due to recognizing utilities. exp. on acct.

7,500

Decrease due to cash settlements of utilities pay.

?

= (8,900)

Ending balance

$ 1,400

(5) Reconciliation of Interest Payable

Beginning balance

$ 1,200

Increase due to recognizing int. exp. on acct.

3,500

Decrease due to cash settlements of int. pay.

?

= (4,100)

Ending balance

$ 600

(6) The sales price ($23,500) of the equipment is provided in the

(7) Reconciliation of Notes Receivable

Beginning balance

$24,000

Increase due to loan to borrower

-0-

Decrease due to cash collections from

borrower

?

= (24,000)

Ending balance

$ -0-

12–97

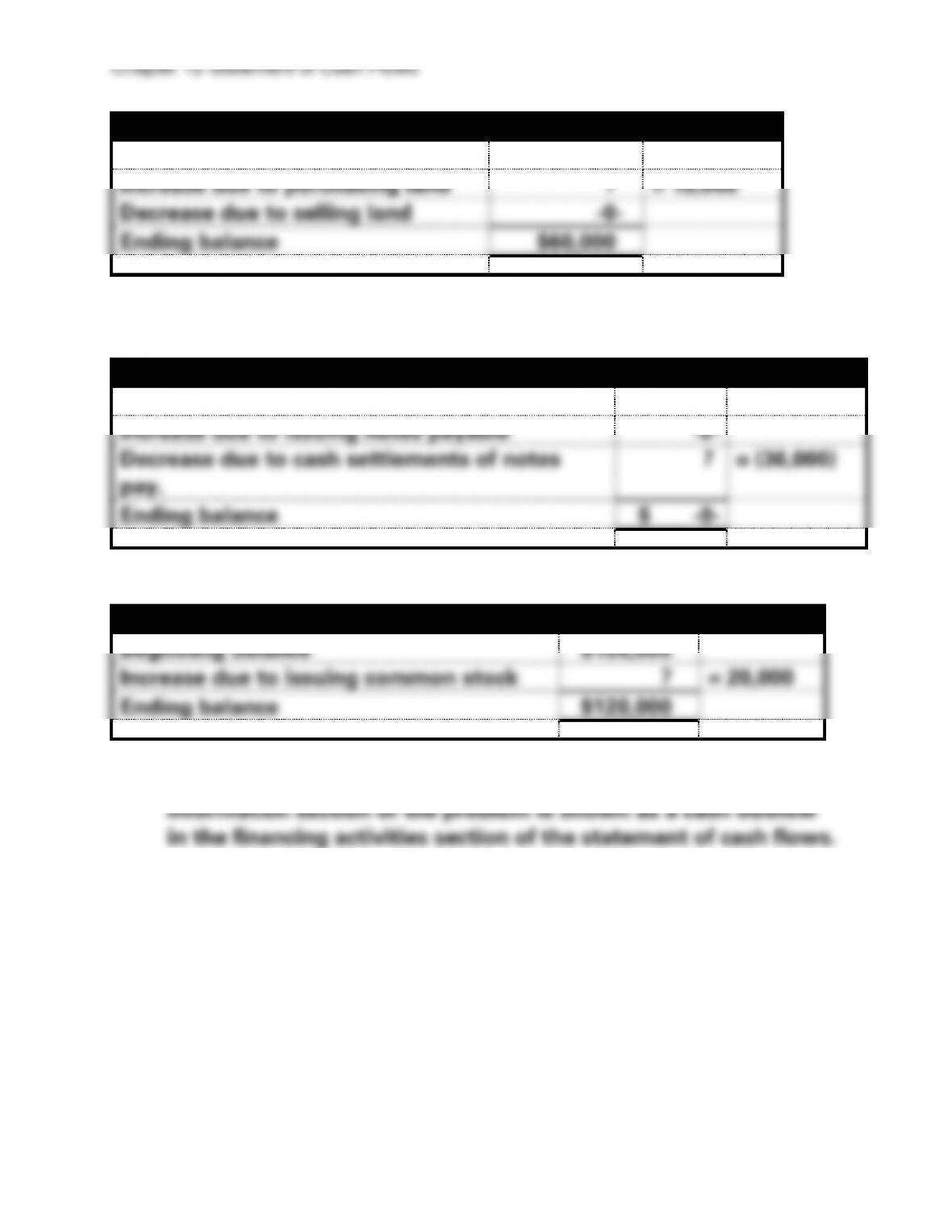

(8) Reconciliation of Land Account

Beginning balance

$45,000

Increase due to purchasing land

?

= 15,000

Decrease due to selling land

-0-

Ending balance

$60,000

PROBLEM 12-21B (cont.)

(9) Reconciliation of Notes Payable Account

Beginning balance

$36,000

Increase due to issuing notes payable

-0-

Decrease due to cash settlements of notes

pay.

?

= (36,000)

Ending balance

$ -0-

(10) Reconciliation of Common Stock Account

Beginning balance

$100,000

Increase due to issuing common stock

?

= 20,000

Ending balance

$120,000

(11) The $50,000 cash dividend referenced in the additional

Chapter 12 Statement of Cash Flows

12–98

PROBLEM 12-21B (cont.)

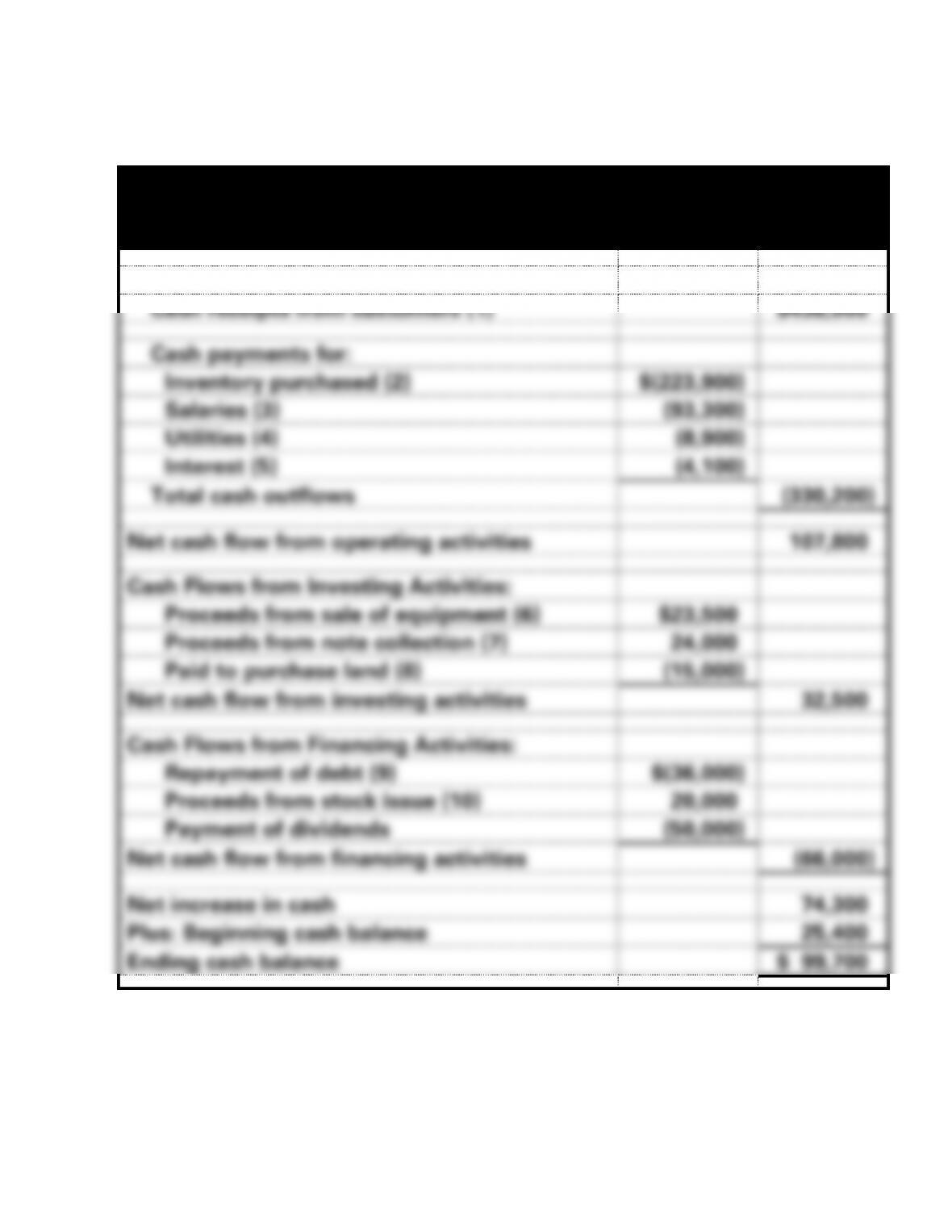

Boston Materials, Inc.

Statement of Cash Flows

For the Year Ended December 31, 2017

Cash Flows from Operating Activities:

Cash receipts from customers (1)

$438,000

Cash payments for:

Inventory purchased (2)

$(223,900)

Salaries (3)

(93,300)

Utilities (4)

(8,900)

Interest (5)

(4,100)

Total cash outflows

(330,200)

Net cash flow from operating activities

107,800

Cash Flows from Investing Activities:

Proceeds from sale of equipment (6)

$23,500

Proceeds from note collection (7)

24,000

Paid to purchase land (8)

(15,000)

Net cash flow from investing activities

32,500

Cash Flows from Financing Activities:

Repayment of debt (9)

$(36,000)

Proceeds from stock issue (10)

20,000

Payment of dividends

(50,000)

Net cash flow from financing activities

(66,000)

Net increase in cash

74,300

Plus: Beginning cash balance

25,400

Ending cash balance

$ 99,700

12–99

ATC 12-1

All dollar amounts are in millions.

a. In 2013 Target’s net income was $3,549 higher than its cash flow

from operating activities ($5,520 − $1,971). In 2012 its net

Chapter 12 Statement of Cash Flows

12-100

ATC 12-2

Dollar amounts in thousands.

a. Tesla Motors reported a net loss and a negative net cash flow

from operating activities in 2011, 2012, and 2013, but its losses

were much worse than its negative cash flows. Net losses for

the three years totaled $804,952 (thousand), while negative cash

12-101

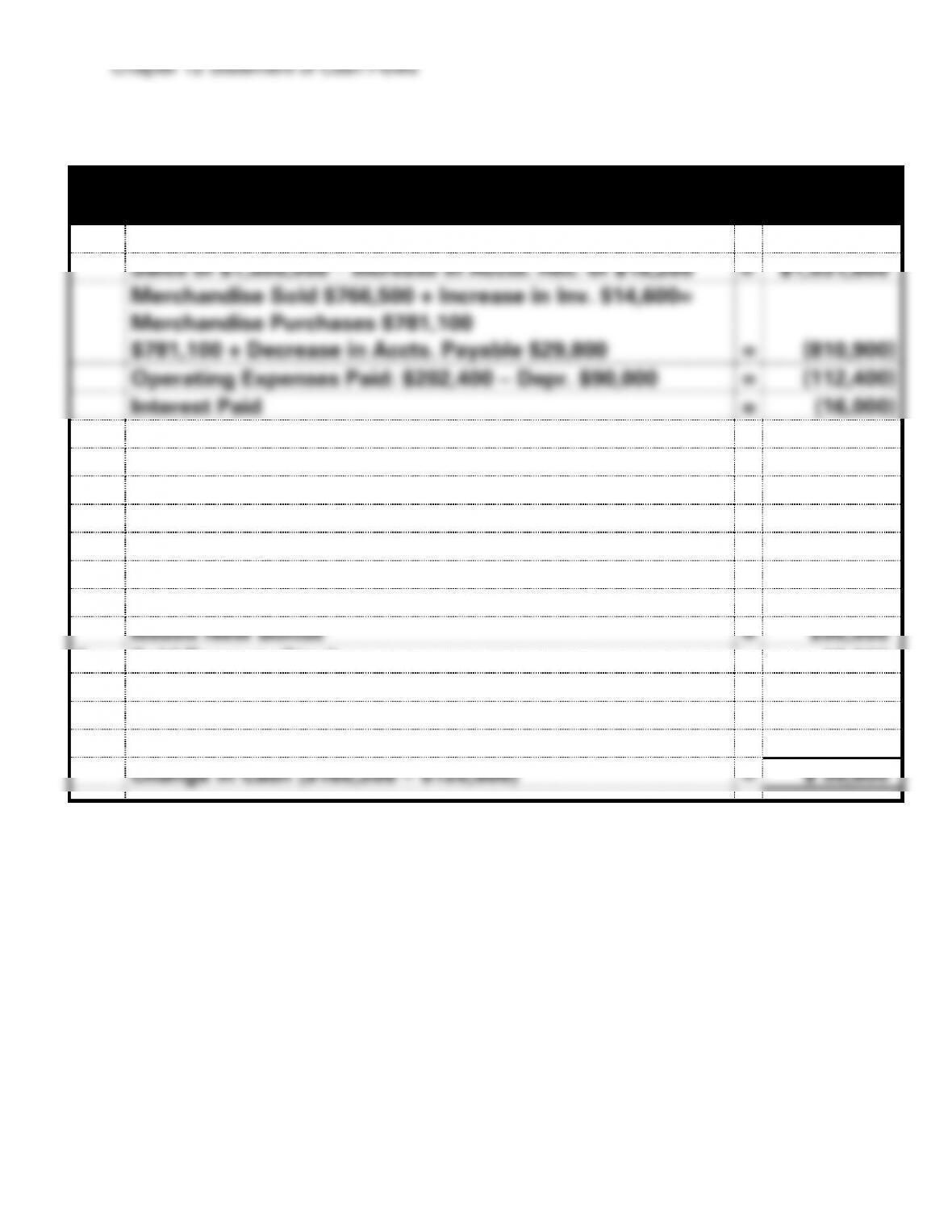

ATC 12-3

Transactions

Effect on

Cash Flow

Cash Received from Sales:

Sales of $1,050,000 − Increase in Accts. Rec. of $18,200

=

$1,031,800

Merchandise Sold $766,500 + Increase in Inv. $14,600=

Merchandise Purchases $781,100

$781,100 + Decrease in Accts. Payable $29,800

=

(810,900)

Operating Expenses Paid: $202,400 − Depr. $90,000

=

(112,400)

Interest Paid

=

(16,000)

1.

Sold Land

=

44,000

2.

Sold Equipment

=

18,000

3.

Purchased Equipment

=

(190,000)

4.

Sold Marketable Securities

=

70,000

5.

Purchased Marketable Securities

=

(104,000)

6.

Paid Loan

=

(20,000)

7.

Paid off Bond Issue

=

(100,000)

Issued New Bonds

=

200,000

8.

Sold Treasury Stock

=

10,000

9.

Issued Common Stock

=

40,000

10.

Issued Preferred Stock

=

17,600

11.

Paid Dividends

=

(38,500)

Change in Cash ($160,200 − $120,600)

=

$ 39,600

Chapter 12 Statement of Cash Flows

12-102

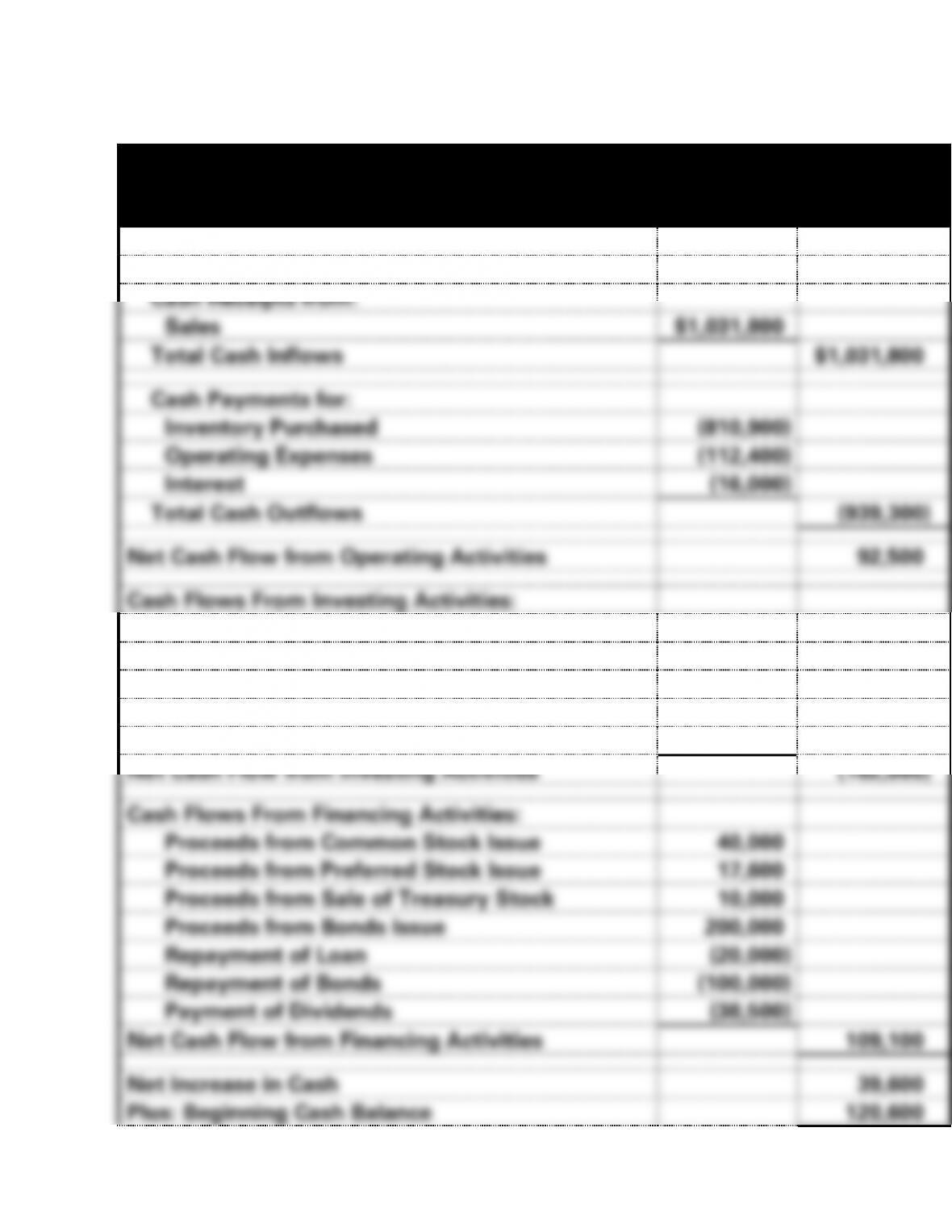

ATC 12-3 (cont.)

Blythe Industries, Inc.

Statement of Cash Flows

For the Year Ended December 31, 2017

Cash Flows From Operating Activities:

Cash Receipts from:

Sales

$1,031,800

Total Cash Inflows

$1,031,800

Cash Payments for:

Inventory Purchased

(810,900)

Operating Expenses

(112,400)

Interest

(16,000)

Total Cash Outflows

(939,300)

Net Cash Flow from Operating Activities

92,500

Cash Flows From Investing Activities:

Proceeds from Sale of Land

44,000

Proceeds from Sale of Equipment

18,000

Proceeds from Sale of Marketable Securities

70,000

Paid to Purchase Marketable Securities

(104,000)

Paid to Purchase Equipment

(190,000)

Net Cash Flow from Investing Activities

(162,000)

Cash Flows From Financing Activities:

Proceeds from Common Stock Issue

40,000

Proceeds from Preferred Stock Issue

17,600

Proceeds from Sale of Treasury Stock

10,000

Proceeds from Bonds Issue

200,000

Repayment of Loan

(20,000)

Repayment of Bonds

(100,000)

Payment of Dividends

(38,500)

Net Cash Flow from Financing Activities

109,100

Net Increase in Cash

39,600

Plus: Beginning Cash Balance

120,600

Chapter 12 Statement of Cash Flows

12-103

Ending Cash Balance

$ 160,200

ATC 12-3 (cont.)

Class Discussion:

a. Cost per share of the treasury stock was $100 ($10,000 100

shares).

12-104

ATC 12-4

This is a writing assignment that will help the students to understand

Chapter 12 Statement of Cash Flows

12-105

ATC 12-5

Some of the points the student should note are:

Inventory has more than doubled and must be paid for. However, it is

difficult to tell whether sales have increased proportionately to the

increase in inventory. If sales have not increased enough, the company

12-106

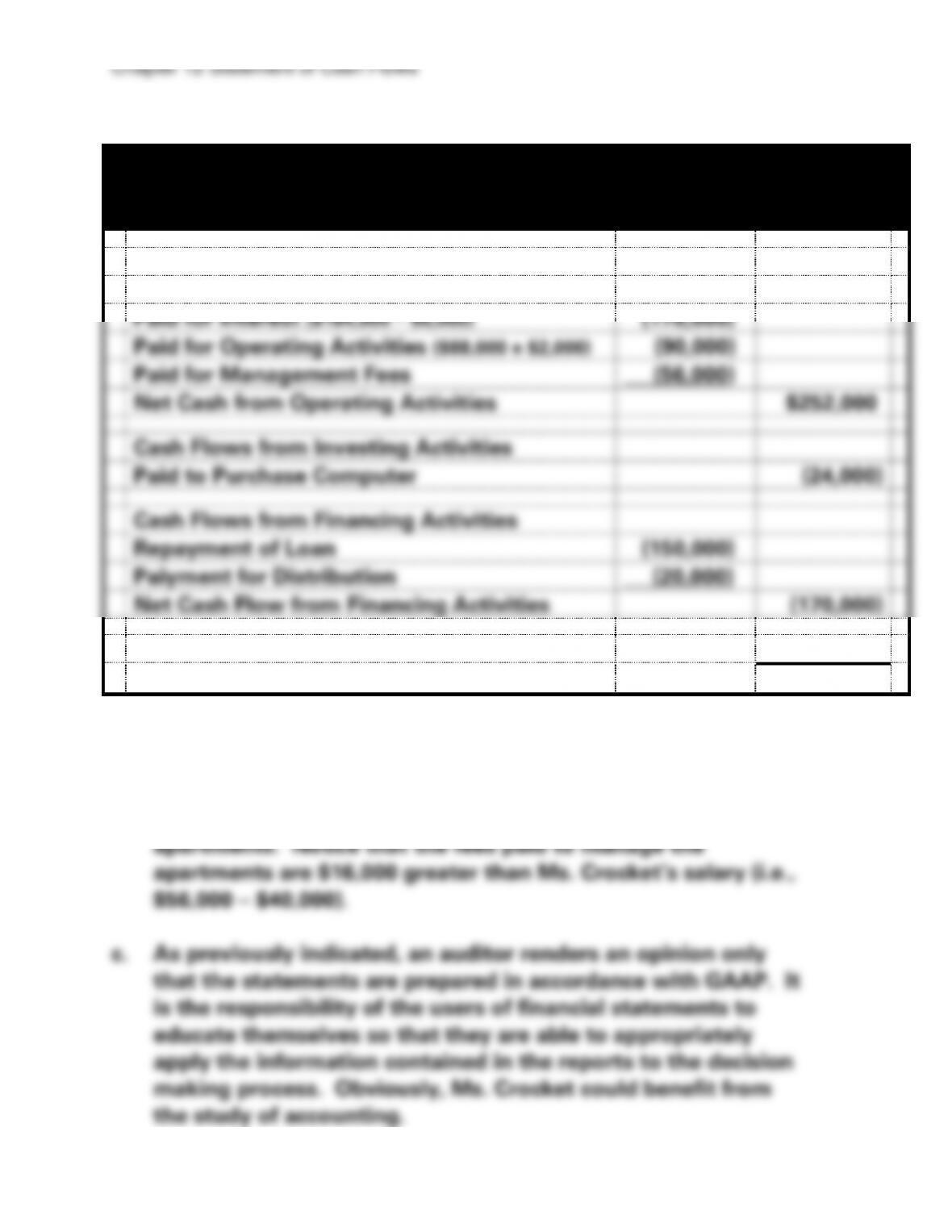

ATC 12-6

a.

Crocket Apartments

Statement of Cash Flows

For the year ended December 31, 2016

Cash Flows from Operating Activities

Receipts from Rent Revenue ($580,000 − $4,000)

$576,000

Paid for Interest ($184,000 − $6,000)

(178,000)

Paid for Operating Activities ($88,000 + $2,000)

(90,000)

Paid for Management Fees

(56,000)

Net Cash from Operating Activities

$252,000

Cash Flows from Investing Activities

Paid to Purchase Computer

(24,000)

Cash Flows from Financing Activities

Repayment of Loan

(150,000)

Paiyment for Distribution

(20,000)

Net Cash Flow from Financing Activities

(170,000)

Net Change in Cash

58,000

b. Clearly, the apartment complex is generating a positive cash

flow. If Ms. Crocket keeps the apartments, she will have more,

not less, money to spend. Also, Ms. Crocket should consider

quitting her own job thereby having time to manage the

Chapter 12 Statement of Cash Flows

12-107

ATC 12-7

This solution is based on the company’s From10-K for the fiscal year

ended February 1, 2014 (2013). Dollar amounts are in millions.

($329). It also borrowed more money issuing new long-term

($378).