11–44

EXERCISE 11-18A

The memo should contain a definition of the price-earnings ratio. It is one

of the most commonly reported measures of a company’s value. It is

of $0.01 whose stock is trading at $0.50 has a P/E ratio of 50, but this is

SOLUTIONS TO PROBLEMS – SERIES A – CHAPTER 11

PROBLEM 11-19A

Transactions

Cash Acquired from Owner(s)

$60,000

Revenues

35,000

Expenses

18,100

Distributions/Withdrawals

4,000

11–46

PROBLEM 11-19A a. (cont.)

Cascade Company

Financial Statements

Balance Sheet

As of December 31, 2016

Assets

Cash

$72,900

Total Assets

$72,900

Liabilities

$ -0-

Equity

Carl Cascade, Capital

72,900

Total Liabilities and Equity

$72,900

Statement of Cash Flows

For the Year Ended December 31, 2016

Cash Flows From Operating Activities:

Receipts from Revenues

$35,000

Paid for Expenses

(18,100)

Net Cash Flow from Operating Activities

$16,900

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities:

Proceeds from Owner

$60,000

Paid for Owner’s Withdrawals

(4,000)

Net Cash Flow from Financing Activities

56,000

Net Change in Cash

72,900

Plus: Beginning Cash Balance

-0-

Ending Cash Balance

$72,900

11–47

11–48

PROBLEM 11-19A (cont.)

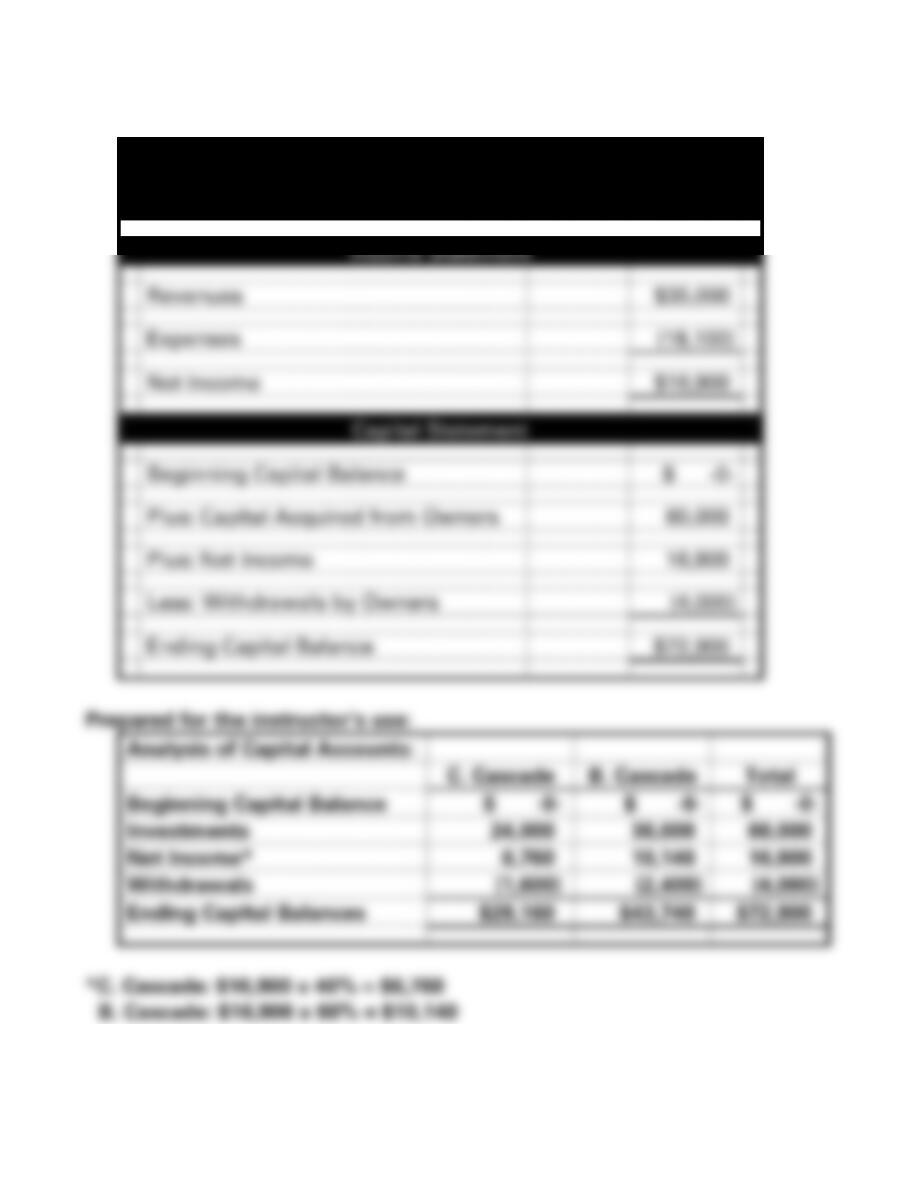

b. Partnership

Cascade Company

Financial Statements

For the Year Ended December 31, 2016

Income Statement

Revenues

$35,000

Expenses

(18,100)

Net Income

$16,900

Capital Statement

Beginning Capital Balance

$ -0-

Plus: Capital Acquired from Owners

60,000

Plus: Net Income

16,900

Less: Withdrawals by Owners

(4,000)

Ending Capital Balance

$72,900

Prepared for the instructor’s use:

Analysis of Capital Accounts:

C. Cascade

B. Cascade

Total

Beginning Capital Balance

$ -0-

$ -0-

$ -0-

Investments

24,000

36,000

60,000

Net Income*

6,760

10,140

16,900

Withdrawals

(1,600)

(2,400)

(4,000)

Ending Capital Balances

$29,160

$43,740

$72,900

*C. Cascade: $16,900 x 40% = $6,760

B. Cascade: $16,900 x 60% = $10,140

11–49

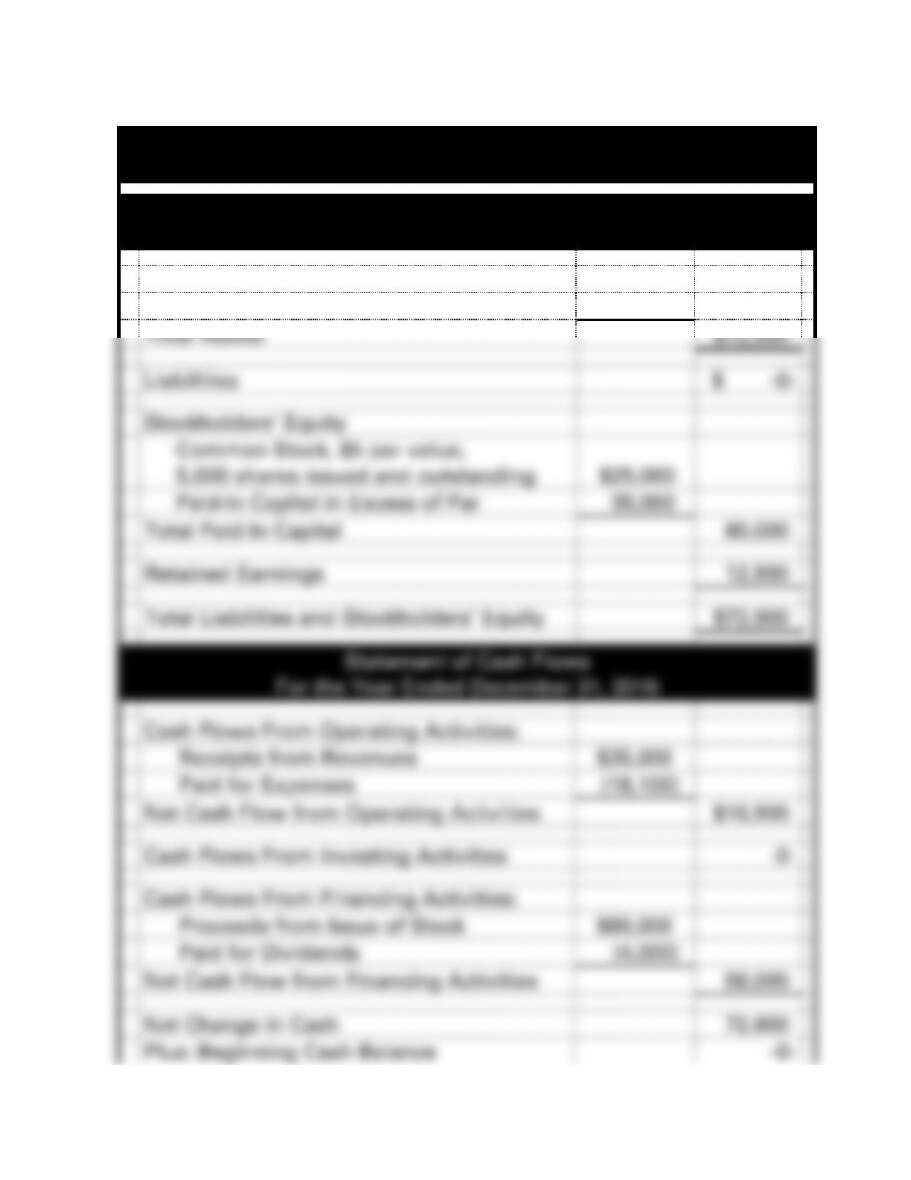

PROBLEM 11-19A b. (cont.)

Cascade Company

Financial Statements

Balance Sheet

As of December 31, 2016

Assets

Cash

$72,900

Total Assets

$72,900

Liabilities

$ -0-

Equity

Carl Cascade, Capital

29,160

Beth Cascade, Capital

43,740

Total Liabilities and Equity

$72,900

Statement of Cash Flows

For the Year Ended December 31, 2016

Cash Flows From Operating Activities:

Receipts from Revenues

$35,000

Paid for Expenses

(18,100)

Net Cash Flow from Operating Activities

$16,900

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities:

Proceeds from Partners

$60,000

Paid for Partners’ Withdrawals

(4,000)

Net Cash Flow from Financing Activities

56,000

Net Change in Cash

72,900

Plus: Beginning Cash Balance

-0-

Ending Cash Balance

$72,900

11–50

11–51

PROBLEM 11-19A (cont.)

c. Corporation

Cascade, Inc.

Financial Statements

For the Year Ended December 31, 2016

Income Statement

Revenues

$35,000

Expenses

(18,100)

Net Income

$16,900

Statement of Changes in Stockholders’ Equity

Beginning Common Stock

$ -0-

Plus: Issuance of Common Stock

60,000

Ending Common Stock

$60,000

Beginning Retained Earnings

$ -0-

Plus: Net Income

16,900

Less: Dividends

(4,000)

Ending Retained Earnings

12,900

Total Stockholders’ Equity

$72,900

11–52

PROBLEM 11-19A c. (cont.)

Cascade, Inc.

Financial Statements

Balance Sheet

As of December 31, 2016

Assets

Cash

$72,900

Total Assets

$72,900

Liabilities

$ -0-

Stockholders’ Equity

Common Stock, $5 par value,

5,000 shares issued and outstanding

$25,000

Paid-In Capital in Excess of Par

35,000

Total Paid-In Capital

60,000

Retained Earnings

12,900

Total Liabilities and Stockholders’ Equity

$72,900

Statement of Cash Flows

For the Year Ended December 31, 2016

Cash Flows From Operating Activities:

Receipts from Revenues

$35,000

Paid for Expenses

(18,100)

Net Cash Flow from Operating Activities

$16,900

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities:

Proceeds from Issue of Stock

$60,000

Paid for Dividends

(4,000)

Net Cash Flow from Financing Activities

56,000

Net Change in Cash

72,900

Plus: Beginning Cash Balance

-0-

11–53

Ending Cash Balance

$72,900

11–54

PROBLEM 11-20A

Note: The memo incorporates a schedule showing the after-tax cash

flows under each form of ownership and discusses LLCs.

Memo

To: Owners of Cagle and Associates

From: John Q CPA

11–55

PROBLEM 11-20A (cont.)

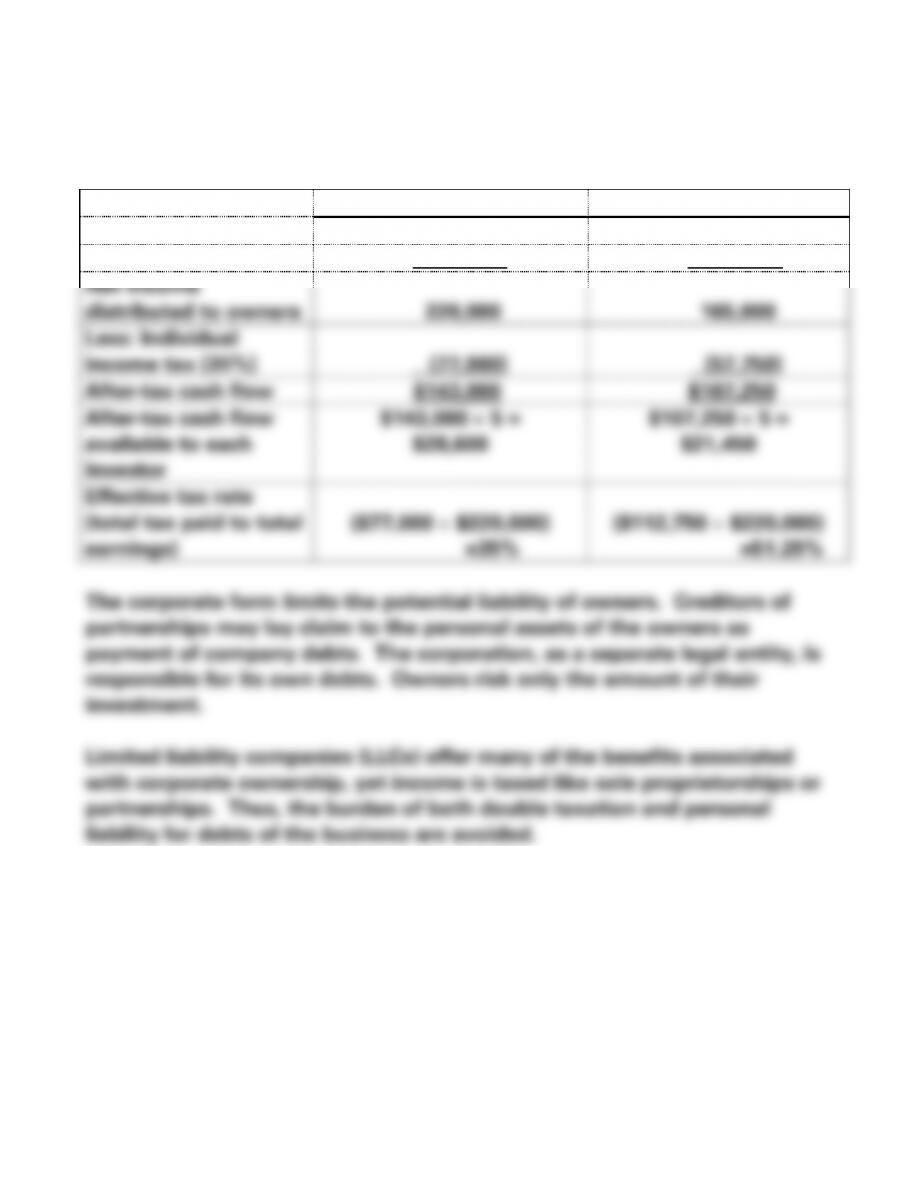

The schedule below illustrates the after-tax cash flows under each form:

Partnership

Corporation

Income before taxes

$220,000

$220,000

Tax at entity level

-0-

(55,000)

Net income

distributed to owners

220,000

165,000

Less: Individual

income tax (35%)

(77,000)

(57,750)

After-tax cash flow

$143,000

$107,250

After-tax cash flow

available to each

investor

$143,000 5 =

$28,600

$107,250 5 =

$21,450

Effective tax rate

(total tax paid to total

earnings)

($77,000 $220,000)

=35%

($112,750 $220,000)

=51.25%

The corporate form limits the potential liability of owners. Creditors of

partnerships may lay claim to the personal assets of the owners as

payment of company debts. The corporation, as a separate legal entity, is

responsible for its own debts. Owners risk only the amount of their

investment.

Limited liability companies (LLCs) offer many of the benefits associated

with corporate ownership, yet income is taxed like sole proprietorships or

partnerships. Thus, the burden of both double taxation and personal

liability for debts of the business are avoided.

PROBLEM 11-21A

a. $1,000,000 400,000 shares =$2.50 per share

b. $24,000 $5 per share = 4,800 shares

11–57

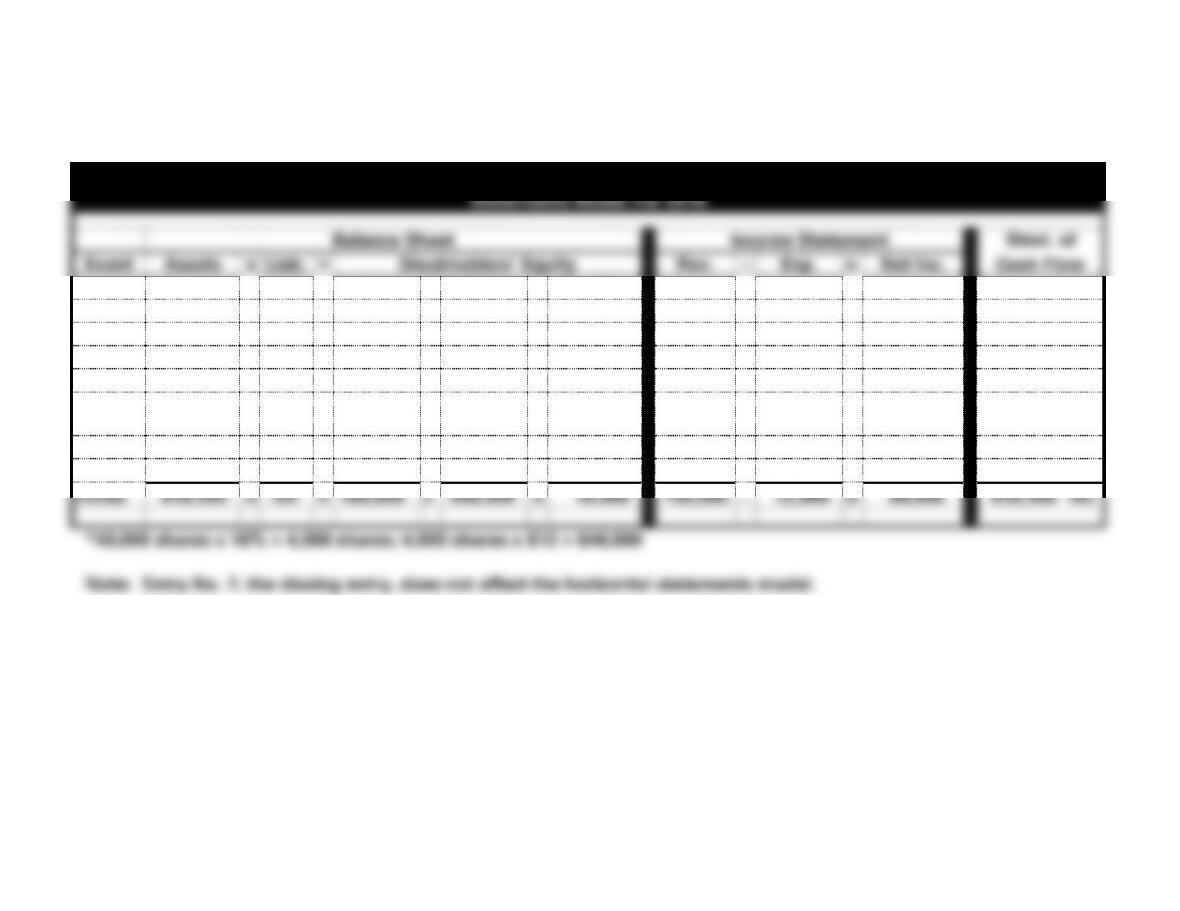

PROBLEM 11-22A

a. NC = Net Change in Cash

Brice Co.

Statements Model For 2016

Balance Sheet

Income Statement

Stmt. of

Event

Assets

=

Liab.

+

Stockholders’ Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

P. Stock

+

C. Stock

+

Ret. Ear.

1.

400,000

=

NA

+

NA

+

400,000

+

NA

NA

−

NA

=

NA

400,000 FA

2.

160,000

=

NA

+

160,000

+

NA

+

NA

NA

−

NA

=

NA

160,000 FA

3.

(9,600)

=

NA

+

NA

+

NA

+

(9,600)

NA

−

NA

=

NA

(9,600) FA

4.*

NA

=

NA

+

NA

+

48,000

+

(48,000)

NA

−

NA

=

NA

NA

5.

memo

NA

=

NA

+

NA

+

NA

+

NA

NA

−

NA

=

NA

NA

6a.

140,000

=

NA

+

NA

+

NA

+

140,000

140,000

−

NA

=

140,000

140,000 OA

6b.

(72,000)

=

NA

+

NA

+

NA

+

(72,000)

NA

−

72,000

=

(72,000)

(72,000) OA

Totals

618,400

=

NA

+

160,000

+

448,000

+

10,400

140,000

−

72,000

=

68,000

618,400 NC

*40,000 shares x 10% = 4,000 shares; 4,000 shares x $12 = $48,000

Note: Entry No. 7, the closing entry, does not affect the horizontal statements model.

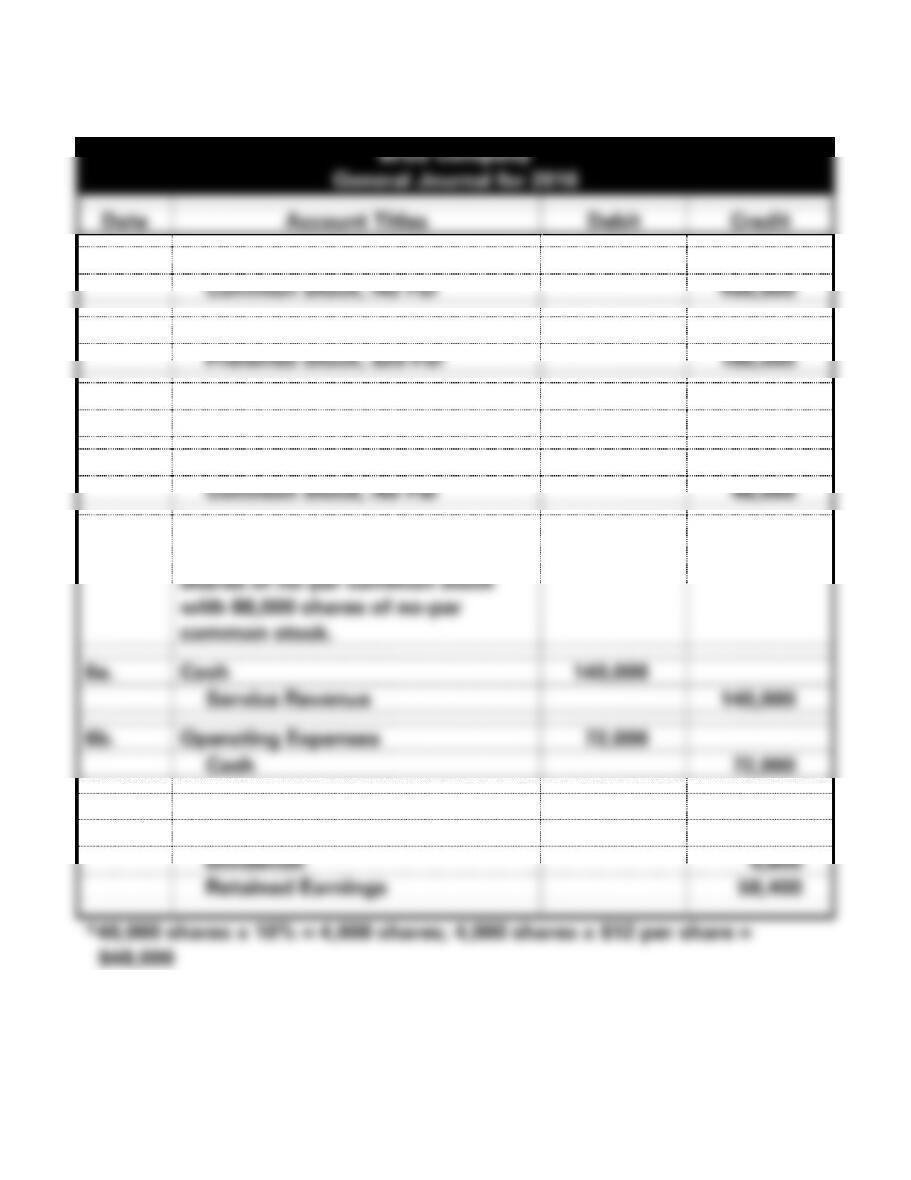

PROBLEM 11-22A (cont.)

b.

Brice Company

General Journal for 2016

Date

Account Titles

Debit

Credit

1.

Cash (40,000 x $10)

400,000

Common Stock, No Par

400,000

2.

Cash (8,000 x $20)

160,000

Preferred Stock, $20 Par

160,000

3.

Dividends

9,600

Cash

9,600

4.

Retained Earnings*

48,000

Common Stock, No Par

48,000

5.

Brice’s declaration of a 2-for-1

stock split will replace the 44,000

shares of no-par common stock

with 88,000 shares of no-par

common stock.

6a.

Cash

140,000

Service Revenue

140,000

6b.

Operating Expenses

72,000

Cash

72,000

7.

Service Revenue

140,000

Operating Expenses

72,000

Dividends

9,600

Retained Earnings

58,400

11–59

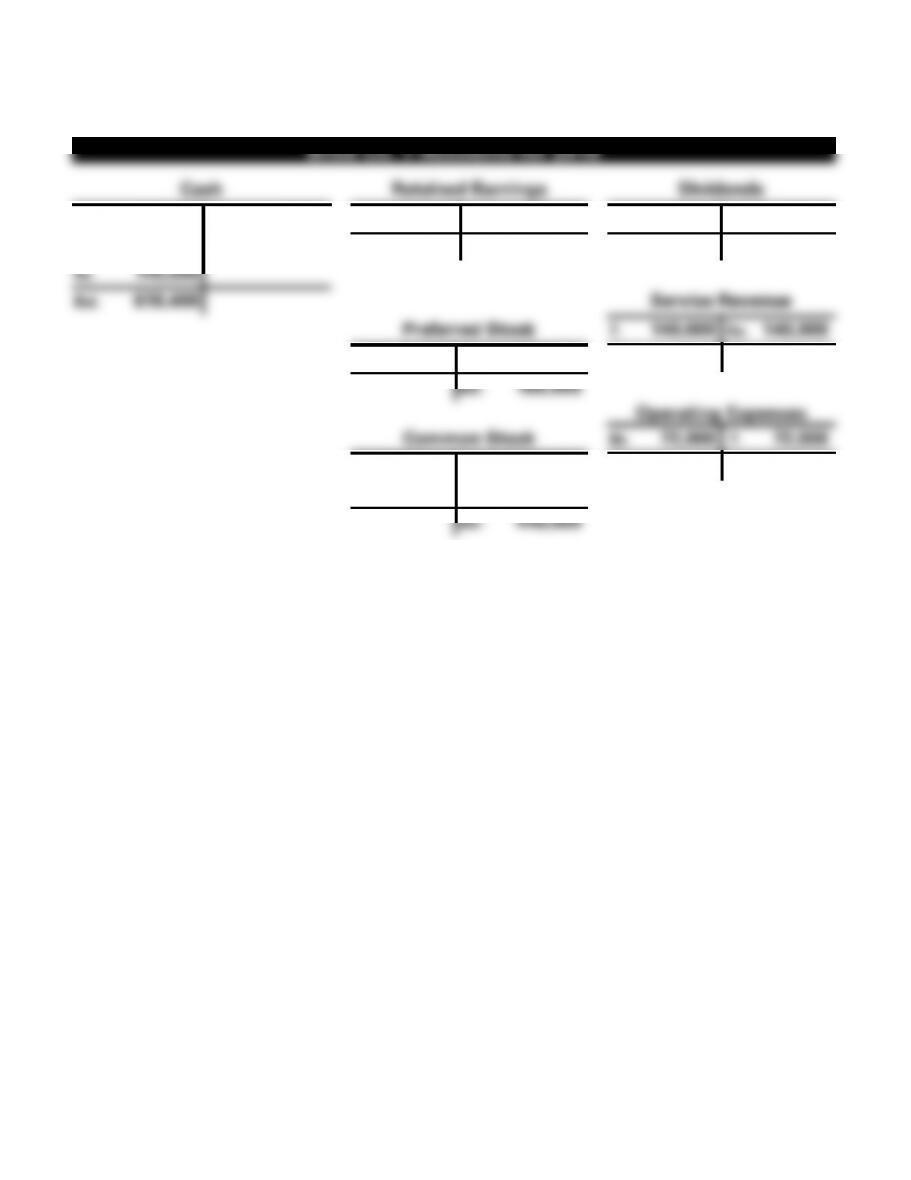

PROBLEM 11-22A b. (cont.)

Brice Co. T-Accounts for 2016

Cash

Retained Earnings

Dividends

1. 400,000

3. 9,600

4. 48,000

7. 58,400

3. 9,600

7. 9,600

2. 160,000

6b. 72,000

Bal. 10,400

Bal. -0-

6a. 140,000

Bal. 618,400

Service Revenue

Preferred Stock

7. 140,000

6a. 140,000

2. 160,000

Bal. -0-

Bal. 160,000

Operating Expenses

Common Stock

6b. 72,000

7. 72,000

1. 400,000

Bal. -0-

4. 48,000

Bal. 448,000