5-1

Chapter 5

Accounting for Inventories

General Comments for Chapter 5

This chapter explains inventory valuation methods, how to determine cost of goods sold, and

other accounting issues related to inventory. It shows students that a company may report

certain assets in financial statements at different amounts depending on the accounting meth-

ods chosen. For example, a company using the FIFO method will report inventory at a dif-

ferent value than it would if it used LIFO. Students learn that companies experiencing com-

parable economic events can report balance sheet and income statement data that differ sig-

nificantly. It may be the accounting principles chosen rather than economic conditions that

affect the amounts reported in the financial statements. Since asset valuation affects expense

recognition, this chapter offers opportunities to emphasize the relationship between the bal-

ance sheet and the income statement.

Be alert to the inconsistency between the acronyms FIFO and LIFO and computing the end-

ing inventory balance. The acronyms refer to the amount of product cost expensed as cost of

goods sold on the income statement. FIFO means the costs of the first items purchased are

the first costs to be charged to cost of goods sold. Since the number of units sold is usually

much larger than the number of units in ending inventory, it is quicker to indirectly calculate

cost of goods sold by computing the amount of ending inventory and then subtracting that

amount from cost of goods available for sale. So we often teach students to calculate the

ending inventory amount. This approach creates an inconsistency between the cost flow ac-

ronyms and the computations; the acronyms refer to cost of goods sold and the computations

focus on ending inventory.

If you value comprehension over faster computations, compute cost of goods sold in a man-

ner consistent with the acronyms, namely by multiplying the number of units sold by the cost

per unit. Although this approach requires more arithmetic, the benefits derived from logical

consistency are worth the effort. This method is also consistent with the way companies

keeping perpetual inventory records practice. Cost of goods sold is computed as sales occur.

If you would like to begin the chapter with a problem-based learning exercise, see the notes

below.

Problem-Based Learning Case: Inventory Cost

Instructions: The case appears on the following page in a format you can copy or display.

Distribute copies of the case to the class before providing any explanation of alternate inven-

tory costing methods. Ask students to read the case and individually develop answers. After

allowing students time to develop their individual answers, put them into groups to reach

5-2

consensus on an answer. Also, ask each group to select a spokesperson. Allow groups time

to develop answers, then call on some of the spokespersons to share their solutions. As you

respond to the student solutions, explain the basic concepts of inventory cost flow assump-

tions. Emphasize the concept of gross margin.

The possible answers are:

FIFO

LIFO

WAVG

Sales revenue

$40

$40

$40

Cost of goods sold

(25)

(31)

(28)

Gross margin

15

$9

$12

Other operating expenses

(5)

(5)

(5)

Net income

$10

$4

$7

Chapter 5 Problem-Based Learning Case: Inventory Cost

John Smith purchased two toy cars to resell. The cars were identi-

cal in every respect except that John purchased them at different

times for different costs. The first car purchased cost $25. The

second one purchased cost $31. John sold one of the cars for $40.

John’s other operating expenses were $5. Based on this infor-

mation alone, what was John’s net income?

Detailed Outline of a Lesson Plan for Chapter 5

5-3

I. Two factors affect the complexity of product cost allocations: (1) the number of

layers of inventory and (2) the number of units in each layer. The simplest model has

two layers with only one product in each layer. Start your explanation at this level.

Introduce Demonstration Problem 5-1 by telling your students that a furniture store

owns two beds which are identical with respect to appearance, quality, and brand

name. However, the store purchased the beds at different times for different prices.

The first bed cost the store $400; the second bed cost $450. The store sold one of the

beds for $600, and the store manager cannot identify which of the beds it was. First,

review how gross margin is computed. Then, instruct your students to compute the

gross margin on the sale. Be patient while they struggle for a while. Your objective

is for them to discover the problem before you provide a solution. Given a reasonable

length of time, someone is likely to subtract the average cost [($400 + $450) ÷ 2 =

$425] from the sales price ($600) to get a gross margin of $175. When this happens,

identify this method as weighted average and broaden the subject to include FIFO and

LIFO. Write the solution on the board as follows:

FIFO

LIFO

Weighted

Average

Sales

600

600

600

Cost of goods sold

(400)

(450)

(425)

Gross margin

200

150

175

In this simplified context you can make the critical points that distinguish each meth-

od from the others. For example, tell your students to assume that three different

companies use the different cost flow methods. Company A uses FIFO, Company B

LIFO, and Company C weighted average. Then ask which company is the best per-

former. Most students will choose FIFO because of the higher reported gross margin.

Of course, all three are the same. Each company experienced exactly the same eco-

nomic events. The only difference is in how they reported the events. You may also

want to point out that, in an inflationary economy, LIFO produced the lowest gross

margin. This is a good time to discuss the tax implications of FIFO versus LIFO.

We suggest you provide a follow-up exercise by creating an alternative two-layer sin-

gle-product problem. Have the students work this problem in class to make sure they

know how to apply the different approaches before you move on to more complex

problems that include multiple layers with differing prices.

II. Demonstration Problem 5-2 introduces accounting for inventories with multiple

layers and prices. The objective here is to show students how cost flow methods dif-

fer from each other. For example, does FIFO or LIFO produce a higher gross mar-

gin? The horizontal financial statements model is not suited to this type of analysis

because we are not interested in comparing statements (e.g., does an event affect the

income statement differently than the statement of cash flows?). Instead, we want to

5-4

see how different cost flow methods affect a particular statement (e.g., what does the

income statement look like under FIFO, LIFO, and weighted average?).

You can easily illustrate the distinction between cost of goods sold under FIFO versus

LIFO in a multilayer example. Draw a picture of a barrel on the board. Show differ-

ent layers of inventory piling up in the barrel. For FIFO, draw a hole in the bottom of

the barrel. Explain that the first items in inventory are the first ones out (sold). Then

erase the hole in the bottom of the barrel and replace it with a hole in the top of the

barrel. Removing inventory items from the top illustrates LIFO. The illustration be-

low is labeled to match the inventory available in Demonstration Problem 6-2.

Have your students complete Demonstration Problem 5-2 using a vertical format to

prepare income statements, balance sheets, and statements of cash flows. If your stu-

dents have trouble going directly to preparing statements, you may have them first

record the events in T-accounts or using the horizontal financial statements model.

Once they have prepared the statements, have them make the following observations.

A. Notice that the cost flow method does not affect revenue.

B. Have the students verify that the amount of cost of goods sold plus ending inven-

tory is equal to the amount of cost of goods available for sale. In other words, the

total product cost is the same for all cost flow methods. The difference lies in

how the cost is allocated between cost of goods sold and ending inventory.

C. With the exception of tax consequences, cash flow is not affected by the cost flow

method.

5-5

III. The text covers accounting for inventories when purchases and sales occur in–

termittently. If you include this subject, you may use Exercise 5-8A or B as a

demonstration problem and Exercise 5-9A or B as a follow-up problem.

IV. Use Demonstration Problem 5-3 to show students how to write down inventory

to lower of cost or market. Use the horizontal financial statements model to illus-

trate the effect of the write-down on the financial statements.

V. The text covers the gross margin method of estimating the ending inventory bal-

ance. Use Exercise 5-12 A or B to illustrate this approach to inventory estimation.

VI. Use Exercise 5-14 A or B to illustrate the effects of inventory misstatements on

the elements of financial statements.

VII. Time considerations and homework assignments. Allot approximately one class

hour to inventory topics. Students seem to grasp the inventory cost flow concepts

relatively easily when the method of calculating cost of goods sold is presented in a

manner consistent with the cost flow acronyms. Problem 5-19 A or B provides good

follow-up to Demonstration Problem 5-2. Problem 5-20 A or B can be used as

homework to reinforce the lower of cost or market concepts illustrated in Demonstra-

tion Problem 5-3. Problem 5-21 A or B provides practice estimating ending invento-

ry. As with other chapters, you will not have time to cover everything. Choose what

you deem appropriate. Avoid assigning too much. Unrealistically high expectations

demotivate students and discourage learning.

5-6

Demonstration Problem 5-1 – Inventory Cost Issue

A furniture store inventory includes two beds that are identical with respect to appearance,

quality, and brand name. However, the store purchased the beds at different times for differ-

ent prices. The first bed cost the store $400, and the second bed cost $450. Assume the store

sells one of the beds for $600. Also assume the store manager cannot identify which bed was

sold.

Required

Determine the gross margin on the sale of the bed.

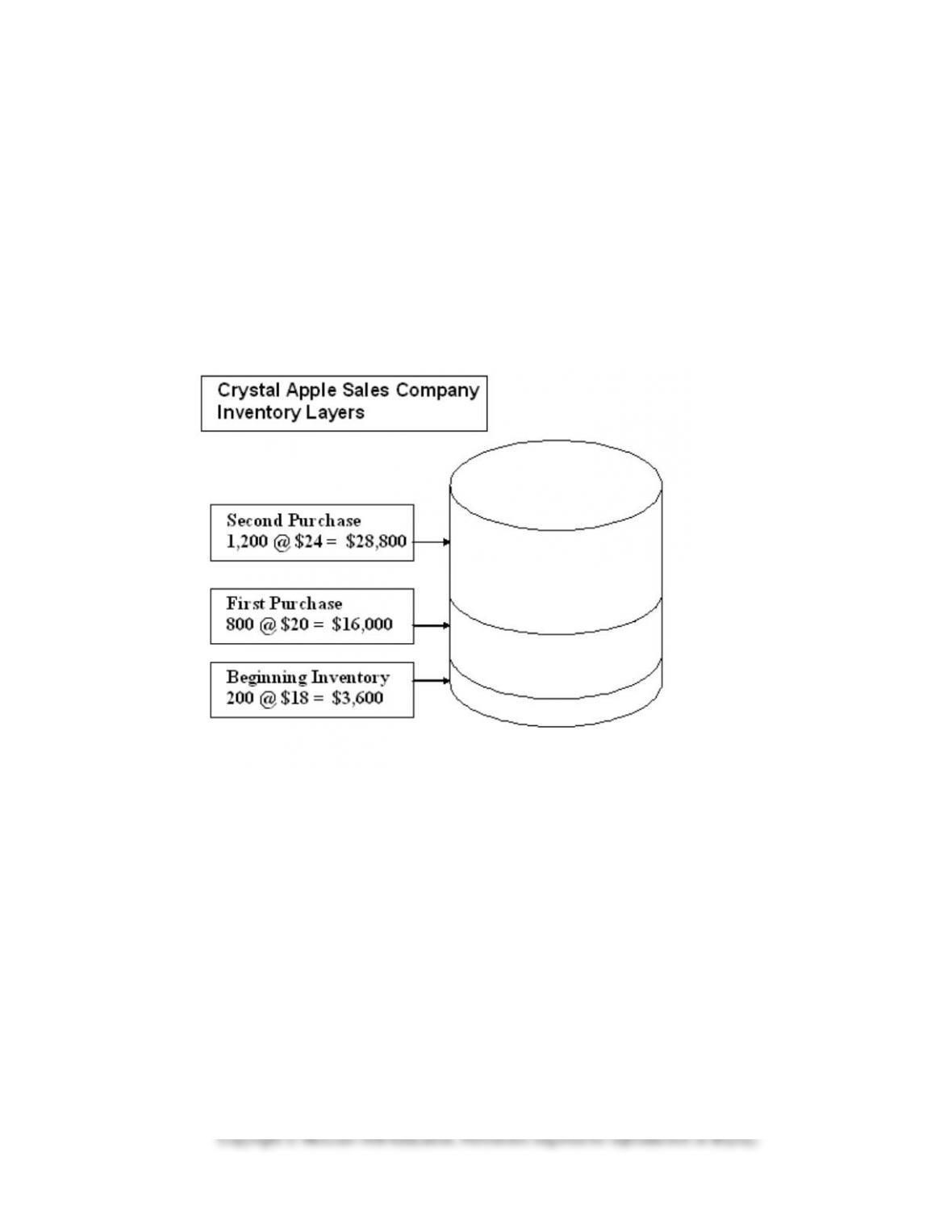

Demonstration Problem 5-2 – Inventory Cost Flow Assumptions

Crystal Apple Sales Company began 2015 with cash of $2,000, inventory of $3,600 (200

crystal apples that cost $18 each), $2,500 of common stock, and $3,100 of retained earnings.

The following events occurred during 2015.

1. Crystal Apple purchased additional inventory twice during 2015. The first purchase

consisted of 800 apples that cost $20 each, and the second consisted of 1,200 apples that

cost $24 each. The purchases were on account.

2. The company sold 2,040 apples for cash at a selling price of $40 each.

3. The company paid $44,800 cash on accounts payable for inventory purchases.

4. Crystal Apple paid $26,000 cash for operating expenses.

Required

a. Record the events in ledger T-accounts or using the horizontal financial statements mod-

el using the three different cost flow assumptions: FIFO, LIFO, and weighted average.

b. Prepare an income statement, a balance sheet, and a statement of cash flows under each

of the three cost flow assumptions.

5-7

Demonstration Problem 5-3 – Lower of Cost or Market for Inventory

Pleasant Grove Electronics carries four different types of calculators. The quantities, costs,

and market values are shown below. Based on this information, determine the necessary

lower of cost or market (LCM) write-down assuming Pleasant Grove determines LCM on an

individual basis. Use a horizontal financial statements model to show how the write-down

would affect the balance sheet, income statement, and statement of cash flows.

Type

Quantity

Unit

Cost

Unit

Market

A

100

$12.00

$15.00

B

550

8.00

6.00

C

710

25.00

24.00

D

240

20.00

22.00

5-8

Demonstration Problem 5-1 Solution

FIFO

LIFO

Weighted

Average

Sales

600

600

600

Cost of goods sold

(400)

(450)

(425)

Gross margin

200

150

175

5-9

Demonstration Problem 5-2 Solution, Inventory Summary

Crystal Apple’s 2015 inventory contains the following layers.

Units

Cost per Unit

Total Cost

Beginning balance

200

x

$18

=

$ 3,600

First purchase

800

x

20

=

16,000

Second purchase

1,200

x

24

=

28,800

Total available

2,200

$48,400

Demonstration Problem 5-2 Solution, part a. Ledger T-accounts

Ledger T-Accounts – FIFO Cost Flow

Cash

Accounts Payable

Common Stock

Bal. 2,000

44,800 (3)

(3) 44,800

16,000 (1a)

2,500 Bal.

(2a) 81,600

26,000 (4)

28,800 (1b)

0 Bal.

Bal. 12,800

Inventory

Retained Earnings

Bal. 3,600

44,560 (2b)

3,100 Bal.

(1a) 16,000

(1b) 28,800

Bal. 3,840

Sales Revenue

81,600 (2a)

Cost of Goods Sold

(2b) 44,560

Operating Expenses

(4) 26,000

Computation of Cost of Goods Sold using FIFO

Units

Cost per Unit

Total Cost

200

x

$18

=

$ 3,600

800

x

20

=

16,000

1,040

x

24

=

24,960

2,040

$44,560

5-10

Demonstration Problem 5-2 Solution, part a. Ledger T-accounts

Ledger T-Accounts – LIFO Cost Flow

Cash

Accounts Payable

Common Stock

Bal. 2,000

44,800 (3)

(3) 44,800

16,000 (1a)

2,500 Bal.

(2a) 81,600

26,000 (4)

28,800 (1b)

0 Bal.

Bal. 12,800

Inventory

Retained Earnings

Bal. 3,600

45,520 (2b)

3,100 Bal.

(1a) 16,000

(1b) 28,800

Bal. 2,880

Sales Revenue

81,600 (2a)

Cost of Goods Sold

(2b) 45,520

Operating Expenses

(4) 26,000

Computation of Cost of Goods Sold using LIFO

Units

Cost per Unit

Total Cost

1,200

x

$24

=

$28,800

800

x

20

=

16,000

40

x

18

=

720

2,040

$45,520

5-11

Demonstration Problem 5-2 Solution, part a. Ledger T-accounts

Ledger T-Accounts – Weighted Average Cost Flow

Cash

Accounts Payable

Common Stock

Bal. 2,000

44,800 (3)

(3) 44,800

16,000 (1a)

2,500 Bal.

(2a) 81,600

26,000 (4)

28,800 (1b)

0 Bal.

Bal. 12,800

Inventory

Retained Earnings

Bal. 3,600

44,880 (2b)

3,100 Bal.

(1a) 16,000

(1b) 28,800

Bal. 3,520

Sales Revenue

81,600 (2a)

Cost of Goods Sold

(2b) 44,880

Operating Expenses

(4) 26,000

Demonstration Problem 5-2 Solution, part a. Horizontal Financial

Statements Model

Worksheet Edmonds

FFAC9e Ch 5 IM.xls

Computation of Cost of Goods Sold using WA

Cost per Unit = $48,400 ÷ 2,200 units = $22

Units

Cost per Unit

Total Cost

2,040

x

$22

=

$44,880

Copyright © McGraw-Hill Education. Permission required for reproduction or display.

5-12

Demonstration Problem 5-2 Solution, part b. Financial Statements

Crystal Apple Sales Company

Comparative Financial Statements

Income Statements for the Year Ended December 31, 2015

FIFO

LIFO

Wt. Avg.

Sales

$81,600

$81,600

$81,600

Cost of goods sold

(44,560)

(45,520)

(44,880)

Gross margin

37,040

36,080

36,720

Operating expenses

(26,000)

(26,000)

(26,000)

Net Income

$11,040

$10,080

$10,720

Balance Sheets at December 31, 2015

Assets

FIFO

LIFO

Wt. Avg.

Cash

$12,800

$12,800

$ 12,800

Inventory

3,840

2,880

3,520

Total assets

$16,640

$15,680

$16,320

Stockholders’ equity

Common stock

$ 2,500

$ 2,500

$ 2,500

Retained earnings

14,140

13,180

13,820

Total stockholders’ equity

$16,640

$15,680

$16,320

Statements of Cash Flows for the Year Ended December 31, 2015

Cash flow from oper. activities

FIFO

LIFO

Wt. Avg.

Cash inflow from customers

$81,600

$81,600

$81,600

Cash outflow for inventory

(44,800)

(44,800)

(44,800)

Cash outflow for oper. exp.

(26,000)

(26,000)

(26,000)

Net cash inflow from oper. act.

10,800

10,800

10,800

Cash flow from investing act.

0

0

0

Cash flow from financing act.

0

0

0

Net increase in cash

10,800

10,800

10,800

Beginning cash balance

2,000

2,000

2,000

Ending cash balance

$12,800

$12,800

$12,800