4-155

PROBLEM 4-28B (cont.) (Appendix)

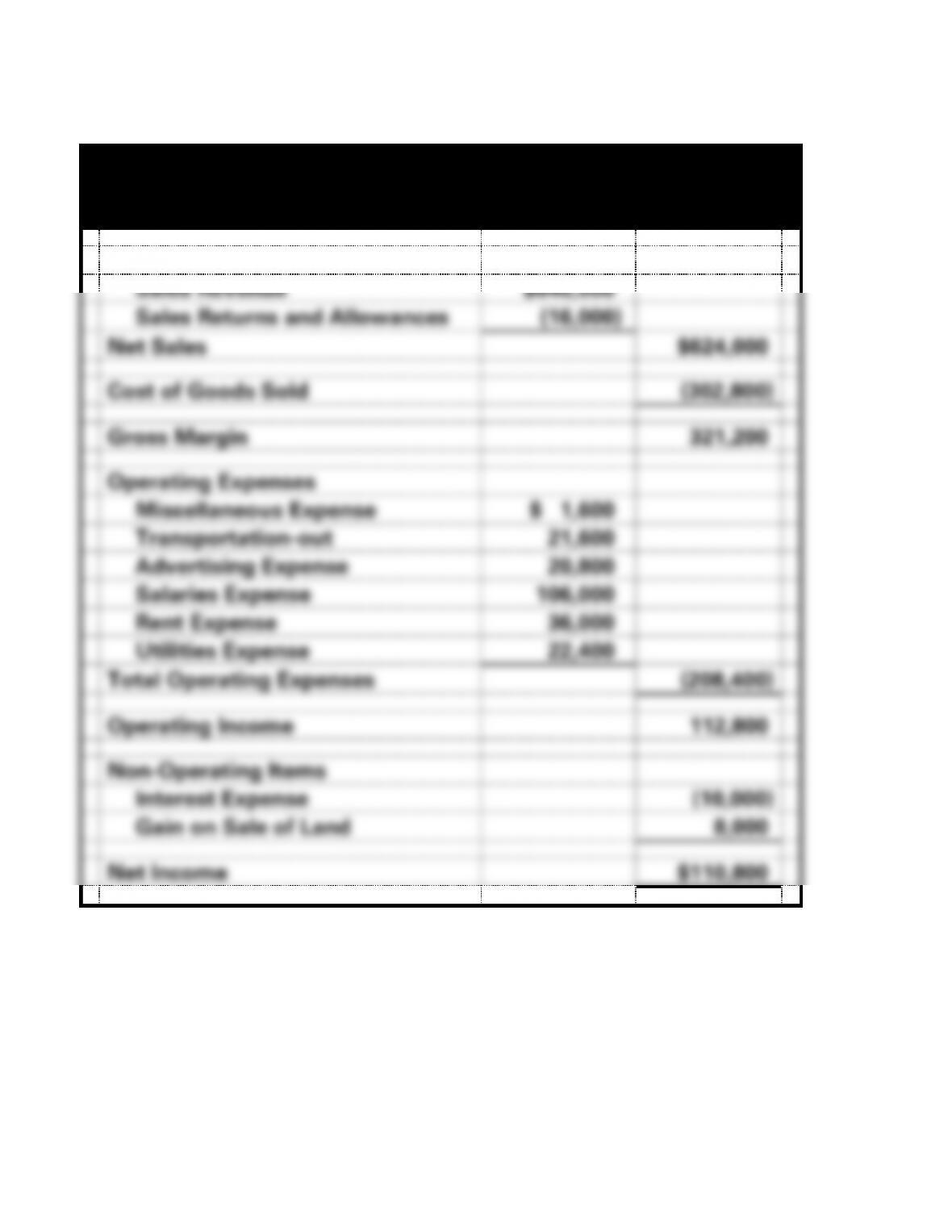

b. Multistep income statement

Hogan Sales Co.

Income Statement

For the Year Ended December 31, 2016

Sales

Sales Revenue

$640,000

Sales Returns and Allowances

(16,000)

Net Sales

$624,000

Cost of Goods Sold

(302,800)

Gross Margin

321,200

Operating Expenses

Miscellaneous Expense

$ 1,600

Transportation-out

21,600

Advertising Expense

20,800

Salaries Expense

106,000

Rent Expense

36,000

Utilities Expense

22,400

Total Operating Expenses

(208,400)

Operating Income

112,800

Non-Operating Items

Interest Expense

(10,000)

Gain on Sale of Land

8,000

Net Income

$110,800

4-156

PROBLEM 4-28B (cont.) (Appendix)

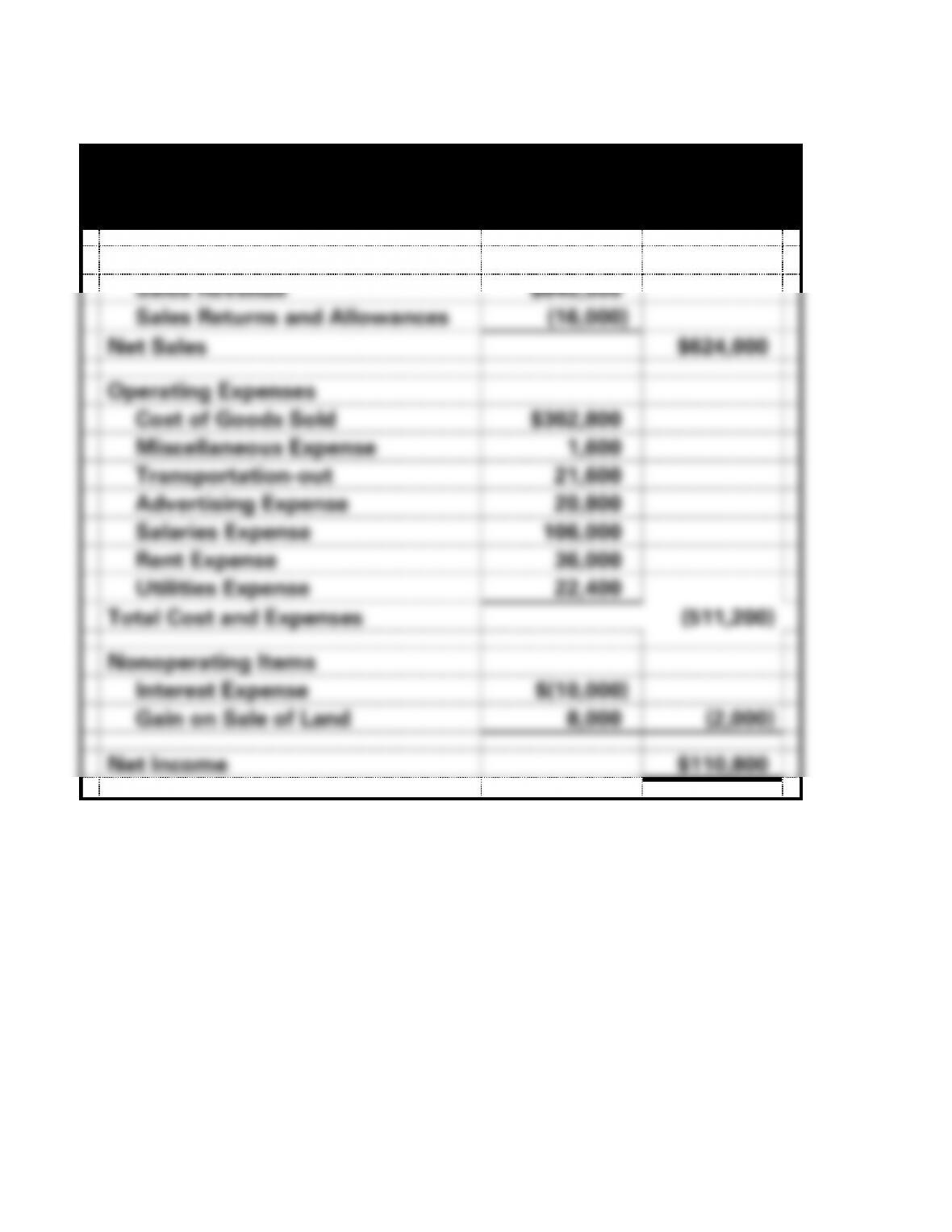

c. Single-step income statement

Hogan Sales Co.

Income Statement

For the Year Ended December 31, 2016

Sales

Sales Revenue

$640,000

Sales Returns and Allowances

(16,000)

Net Sales

$624,000

Operating Expenses

Cost of Goods Sold

$302,800

Miscellaneous Expense

1,600

Transportation-out

21,600

Advertising Expense

20,800

Salaries Expense

106,000

Rent Expense

36,000

Utilities Expense

22,400

Total Cost and Expenses

(511,200)

Nonoperating Items

Interest Expense

$(10,000)

Gain on Sale of Land

8,000

(2,000)

Net Income

$110,800

4-157

PROBLEM 4-29B (Appendix)

a.

Simmons Hardware

General Journal, 2016

Event

Account Titles

Debit

Credit

1.

Land

16,000

Cash

16,000

2.

Purchases

46,000

Accounts Payable

46,000

3.

Transportation-in

460

Cash

460

4.

Accounts Payable

4,000

Purchase Returns and Allow.

4,000

5.

Cash

54,000

Sales Revenue

54,000

6.

Accounts Receivable

100,000

Sales Revenue

100,000

7a.

Accounts Payable [$46,000 – $4,000) x .02]

840

Purchase Discounts

840

7b.

Accounts Payable ($46,000 – $4,000 – $840)

41,160

Cash

41,160

8.

Selling Expenses

2,400

Cash

2,400

9a.

Sales Discounts ($70,000 x .01)

700

Accounts Receivable

700

9b.

Cash ($70,000 − $700)

69,300

Accounts Receivable

69,300

4-158

PROBLEM 4-29B a. (cont.)

Simmons Hardware

General Journal, 2016

Event

Account Titles

Debit

Credit

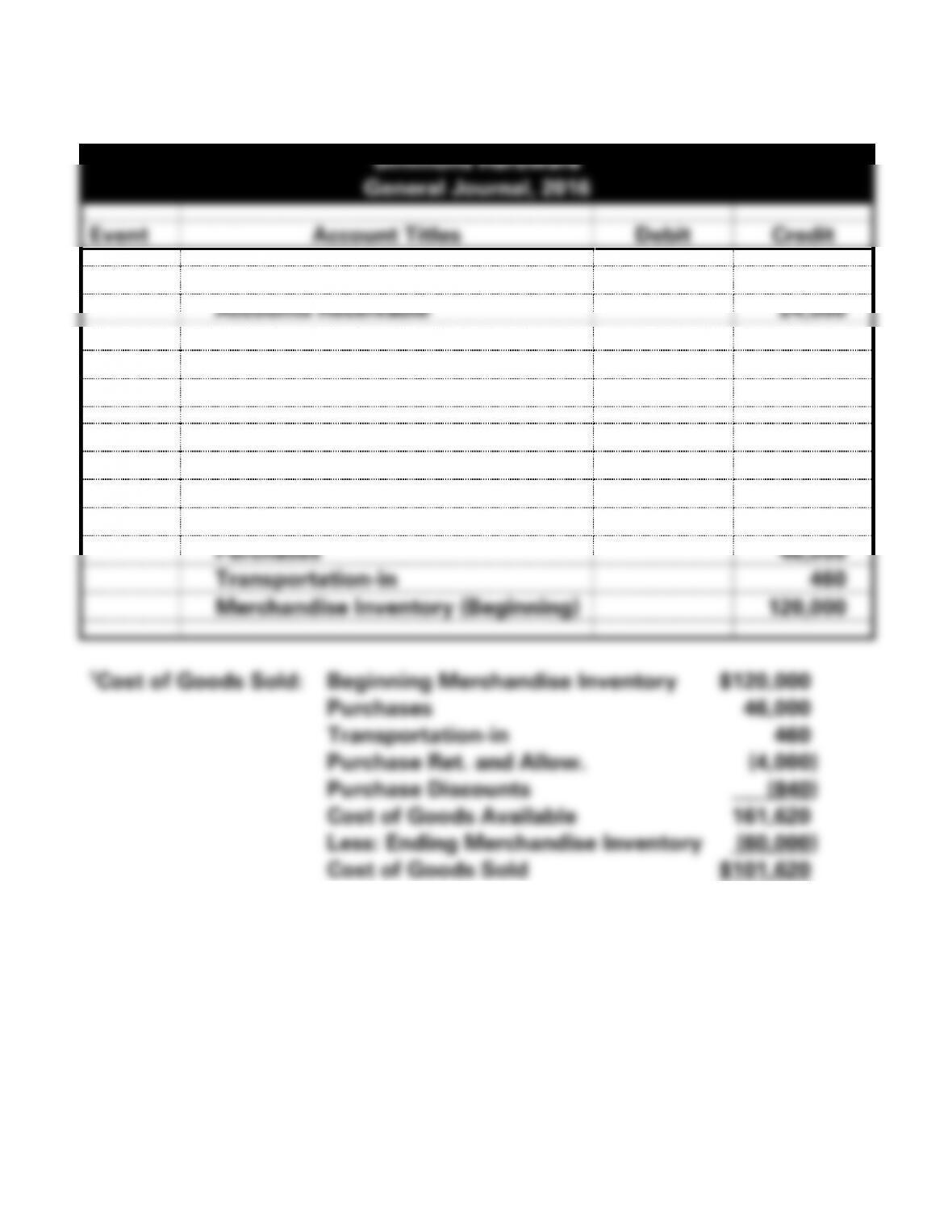

10.

Cash

24,000

Accounts Receivable

24,000

11.

Operating Expenses

6,400

Cash

6,400

12.

Cost of Goods Sold1

101,620

Merchandise Inventory (Ending)

60,000

Purchase Discounts

840

Purchase Returns and Allowances

4,000

Purchases

46,000

Transportation-in

460

Merchandise Inventory (Beginning)

120,000

4-159

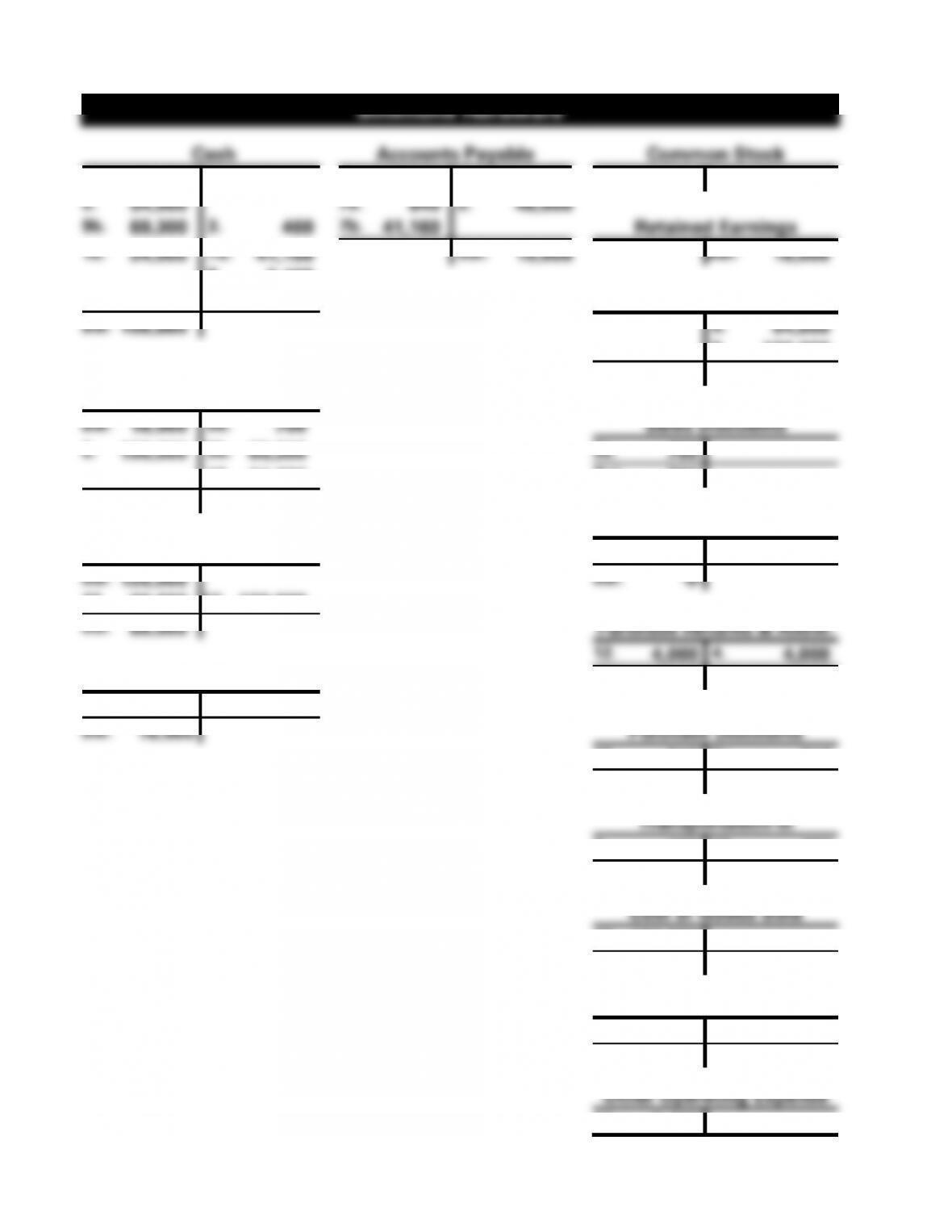

PROBLEM 4-29B (cont.) b.

Simmons Hardware

Cash

Accounts Payable

Common Stock

Bal.

28,000

1.

16,000

4.

4,000

Bal.

10,000

Bal.

140,000

5.

54,000

7a.

840

2.

46,000

9b.

69,300

3.

460

7b.

41,160

Retained Earnings

10.

24,000

7b.

41,160

Bal.

10,000

Bal.

16,000

8.

2,400

11.

6,400

Sales Revenue

Bal.

108,880

5.

54,000

6.

100,000

Bal.

154,000

Accounts Receivable

Bal.

18,000

9a.

700

Sales Discounts

6.

100,000

9b.

69,300

9a.

700

10.

24,000

Bal.

700

Bal.

24,000

Purchases

Merchandise Inventory

2.

46,000

12.

46,000

Bal.

120,000

Bal.

-0-

12.

60,000

12.

120,000

Bal.

60,000

Purchase Returns & Allow.

12.

4,000

4.

4,000

Land

Bal.

-0-

1.

16,000

Bal.

16,000

Purchase Discounts

12.

840

7a.

840

Bal.

-0-

Transportation-in

3.

460

12.

460

Bal.

-0-

Cost of Goods Sold

12.

101,620

Bal.

101,620

Selling Expenses

8.

2,400

Bal.

2,400

Other Operating Expense

11.

6,400

4-160

Bal.

6,400

4-7

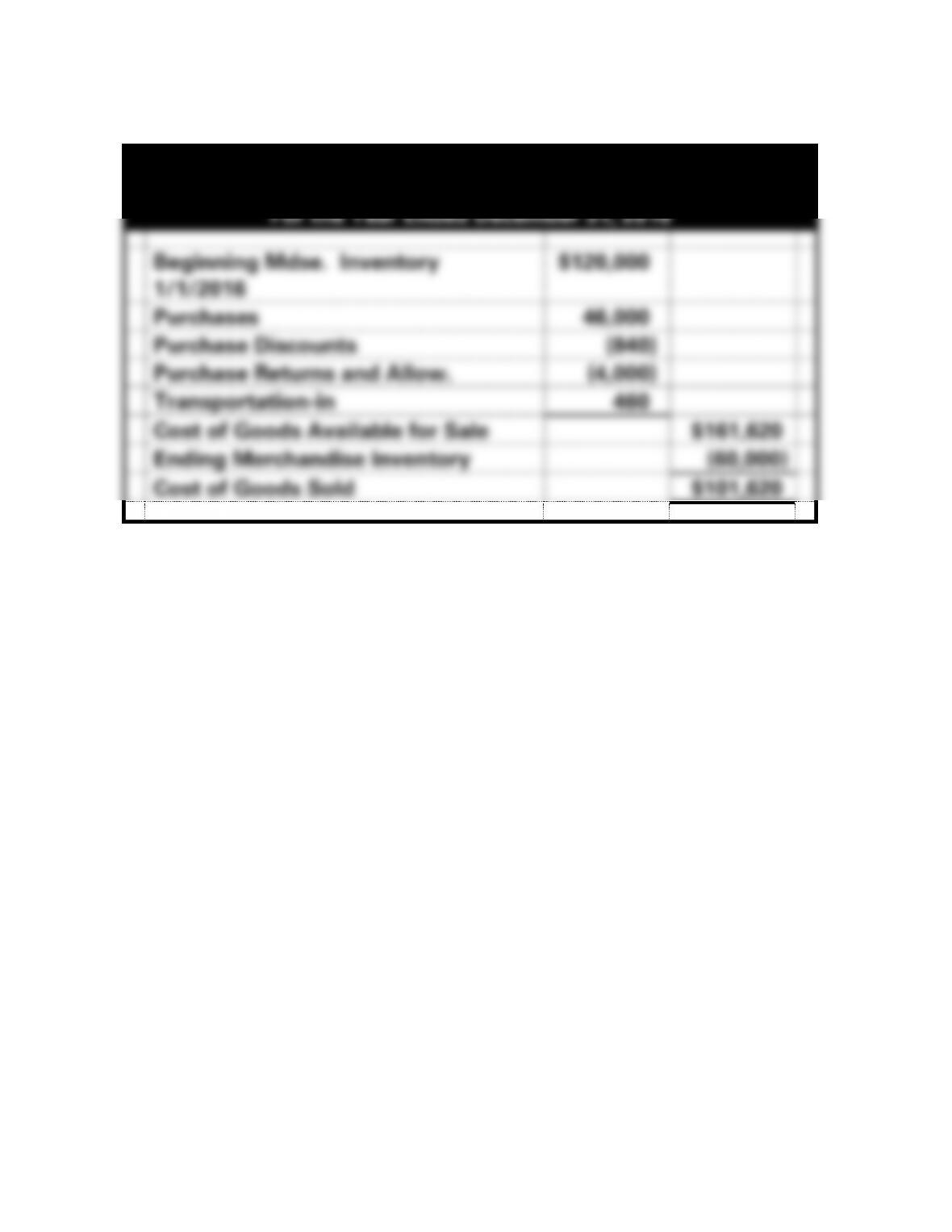

PROBLEM 4-29B (cont.)

c.

Simmons Hardware

Schedule of Cost of Goods Sold

For the Year Ended December 31, 2016

Beginning Mdse. Inventory

1/1/2016

$120,000

Purchases

46,000

Purchase Discounts

(840)

Purchase Returns and Allow.

(4,000)

Transportation-in

460

Cost of Goods Available for Sale

$161,620

Ending Merchandise Inventory

(60,000)

Cost of Goods Sold

$101,620

4-8

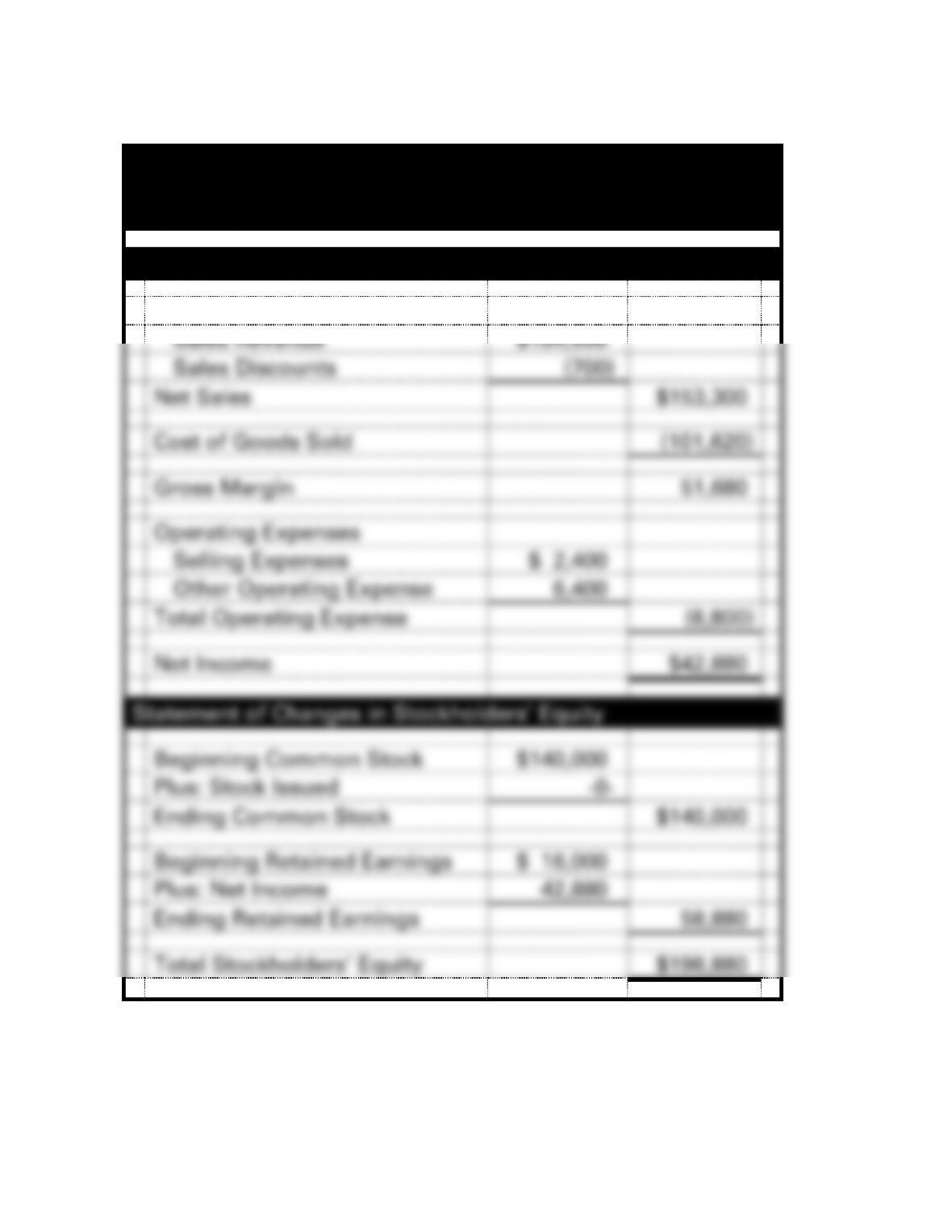

PROBLEM 4-29B c. (cont.)

Simmons Hardware

Financial Statements

For the Year Ended December 31, 2016

Income Statement

Revenue

Sales Revenue

$154,000

Sales Discounts

(700)

Net Sales

$153,300

Cost of Goods Sold

(101,620)

Gross Margin

51,680

Operating Expenses

Selling Expenses

$ 2,400

Other Operating Expense

6,400

Total Operating Expense

(8,800)

Net Income

$42,880

Statement of Changes in Stockholders’ Equity

Beginning Common Stock

$140,000

Plus: Stock Issued

-0-

Ending Common Stock

$140,000

Beginning Retained Earnings

$ 16,000

Plus: Net Income

42,880

Ending Retained Earnings

58,880

Total Stockholders’ Equity

$198,880

4-9

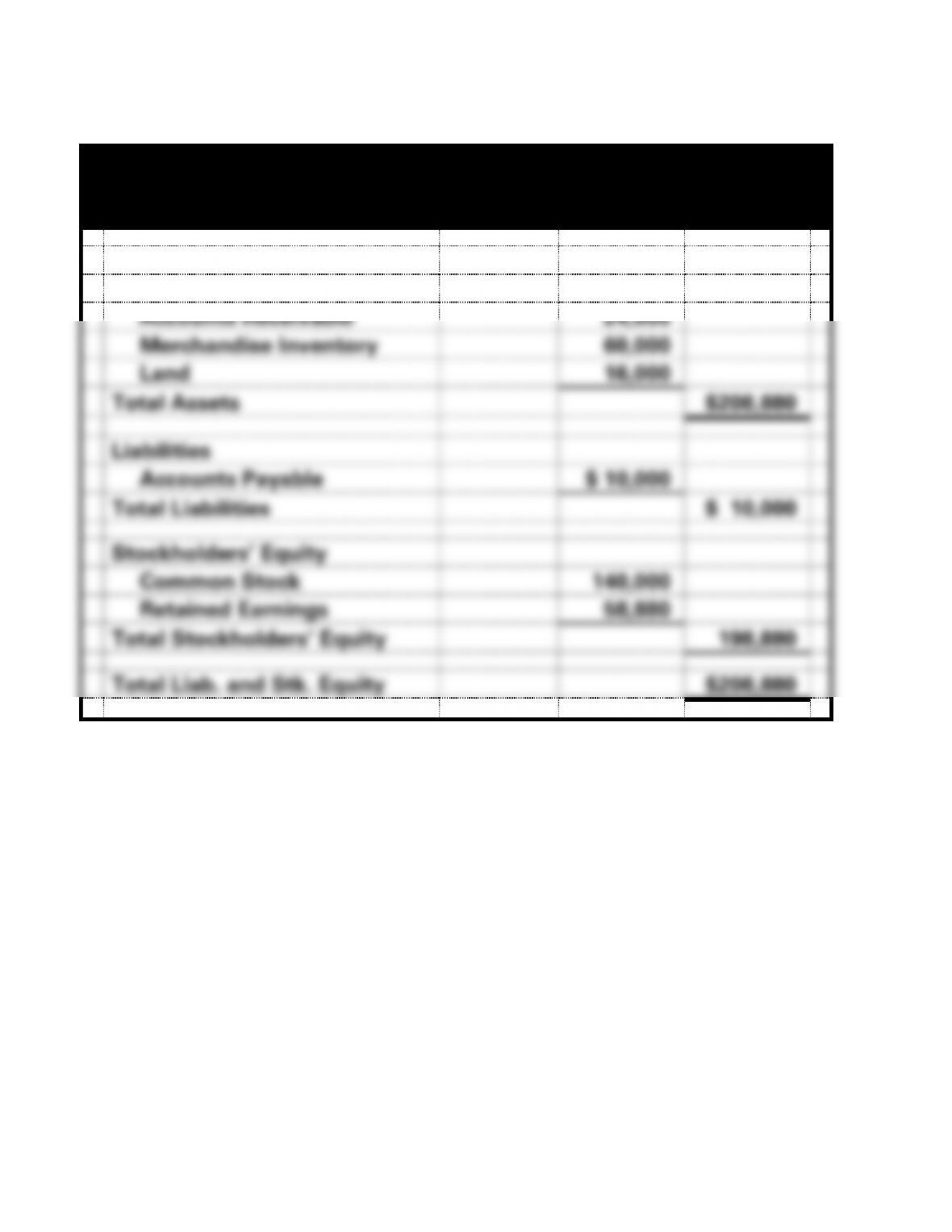

PROBLEM 4-29B c. (cont.)

Simmons Hardware

Balance Sheet

As of December 31, 2016

Assets

Cash

$108,880

Accounts Receivable

24,000

Merchandise Inventory

60,000

Land

16,000

Total Assets

$208,880

Liabilities

Accounts Payable

$ 10,000

Total Liabilities

$ 10,000

Stockholders’ Equity

Common Stock

140,000

Retained Earnings

58,880

Total Stockholders’ Equity

198,880

Total Liab. and Stk. Equity

$208,880

4-10

PROBLEM 4-29B c. (cont.)

Simmons Hardware

Statement of Cash Flows

For the Year Ended December 31, 2016

Cash Flows From Operating Activities:

Inflow from Customers1

$147,300

Outflow for Inventory2

(41,620)

Outflow for Expenses3

(8,800)

Net Cash Flow from Operating Activities

$ 96,880

Cash Flows From Investing Activities:

Outflow for Purchase of Land

(16,000)

Net Cash Flow from Investing Activities

(16,000)

Cash Flows From Financing Activities:

Net Cash Flow from Financing Activities

-0-

Net Change in Cash

80,880

Plus: Beginning Cash Balance

28,000

Ending Cash Balance

$108,880

1(5) $54,000 + (9b) $69,300 + (10) $24,000 = $147,300

2(3) $460 + (7b) $41,160 = $41,620

3(8) $2,400 + (11) $6,400 = $8,800

4-11

ANSWERS TO QUESTIONS – CHAPTER 4

1. Merchandise inventory is finished goods that are held for sale to

2. Product costs are costs associated with goods for resale, usually

3. Cost of goods available for sale is the total of inventory on hand at the

4. The cost of the items that have not been sold are allocated to

5. Period costs are expensed in the period they are incurred or used.

sold.

6. Net Sales $600,000

Cost of Goods Sold (375,000)

7. Under a perpetual inventory system, the balance in the inventory

4-12

continual basis. Another advantage of the perpetual method is that it

allows for better internal control of inventory.

8. a. Assets increase, stockholders’ equity increases – The balance sheet,

statement of cash flows, and statement of changes in stockholders’

equity are affected.

b. Assets increase, stockholders’ equity increases – This is similar to

9. Assets would both increase and decrease (cash increases by $20,000

affected.

10. Shipping cost of goods shipped FOB shipping point will be paid by the

4-13

11. Transportation-in is the cost of freight and shipping charges on goods

12. The $80 transportation-in is a product cost and is debited to the

13. When allowances are granted it is usually because the customer

received inferior or damaged merchandise. When granting an

14. 2/10 n/30 means that a 2% discount may be taken off the selling price if

15. If the $5,000 is for the purchase of inventory, this is an asset exchange

in that inventory is increased and cash is decreased. A $5,000

16. Credit terms are offered to customers to encourage prompt payment.

17. Transportation-out is the freight or shipping cost on goods sold. It is a

18. The inventory account will be debited by the gross amount of $4,000.

.02).

19. Gains are increases in assets or decreases in liabilities which result

4-14

20. Losses are decreases in assets or increases in liabilities which result

business.

21. The only amount that would be shown on the Statement of Cash Flows

22. Purchase returns refer to the situation where the buyer of the goods

returns them. Sales returns refer to the situation where goods sold by

the seller are returned to the seller. Generally a sales return on the

seller’s books is a purchase return on the buyer’s books. Sales returns

23. Net sales is gross sales less sales returns and allowances and less

24. The multistep income statement provides more information on the

results of various business activities. A gross margin is shown and

25. Common size income statements covering several accounting periods

4-15

percentage of sales. Comparison of common size income statements

action.

26. The net income percentage, (return on sales ratio) is the amount of net

27. When using the periodic method of accounting for inventory, the

28. When using the periodic inventory system, a temporary account,

Purchases, is used to accumulate the purchases transactions for the

year. Inventory is not adjusted until the end of the accounting period.

At the end of the accounting period, inventory is physically counted

and cost of goods sold is determined by adding beginning inventory

4-16

29. The periodic inventory system does not separate the cost of lost,

4-17

Note to Instructors: In this chapter the term “net sales” is used in the

income statement for all exercises and problems using the perpetual

EXERCISE 4-1A

a.

Hopkins CPAs

Income Statement

For the Year Ended December 31, 2016

Revenue

Service Revenue

$50,000

Expenses

Salaries Expense

(32,000)

Net Income

$18,000

Hopkins CPAs

Balance Sheet

As of December 31, 2016

Assets

Cash*

$108,000

Total Assets

$108,000

Liabilities

Notes Payable

$90,000

Total Liabilities

$90,000

Stockholders’ Equity

Retained Earnings

$18,000

Total Stockholders’ Equity

18,000

4-18

Total Liab. and Stockholders’ Equity

$108,000

4-19

EXERCISE 4-1A a. (cont.)

Hopkins CPAs

Statement of Cash Flows

For Year Ended December 31, 2016

Cash Flows From Operating Activities:

Cash Inflow from Clients

$50,000

Cash Outflow for Salaries

(32,000)

Net Cash Flow from Operating Activ.

$18,000

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities:

Cash Inflow from Loan

$90,000

Net Cash Flow from Financing Activ.

90,000

Net Increase in Cash

108,000

Plus: Beginning Cash Balance

-0-

Ending Cash Balance

$108,000

EXERCISE 4-1A a. (cont.)

Sports Clothing

Income Statement

For the Year Ended December 31, 2016

Net Sales Revenue

$50,000

Cost of Goods Sold

(26,000)

Gross Margin

24,000

Expenses

Operating Expenses

(8,000)

Net Income

$16,000

Assets

Cash*

$82,000

Merchandise Inventory**

Total Assets

Liabilities

Notes Payable

$90,000

Retained Earnings

$16,000

Total Liab. and Stockholders’ Equity