10–93

PROBLEM 10-29B

White Co.

Event

No.

Type of

Event

Assets

=

Liabilities

+

Common

Stock

+

Retained

Earnings

Net

Income

Cash Flow

1.

AS

+

NA

+

NA

NA

+ FA

2.

AS

+

+

NA

NA

NA

+ FA

3.

AE

+−

NA

NA

NA

NA

− IA

4.

AS

+

NA

NA

+

+

+ OA

5.

AU/CE

−

+

NA

−

−

− OA

6.

Closing

NA

NA

NA

NA

NA

NA

7.

Closing

NA

NA

NA

NA

NA

NA

8.

AS

+

NA

NA

+

+

+ OA

9.

AU/CE

−

+

NA

−

−

− OA

10.

Closing

NA

NA

NA

NA

NA

NA

11.

Closing

NA

NA

NA

NA

NA

NA

12.

AS/AE

+

NA

NA

+

+

+ IA

13.

AU

−

−

NA

NA

NA

− FA

PROBLEM 10-30B

a. The market rate of interest was greater than the stated rate of

interest. Consequently, the bonds sold at a discount. If the bonds had

sold at face value, Cook would have received $200,000.

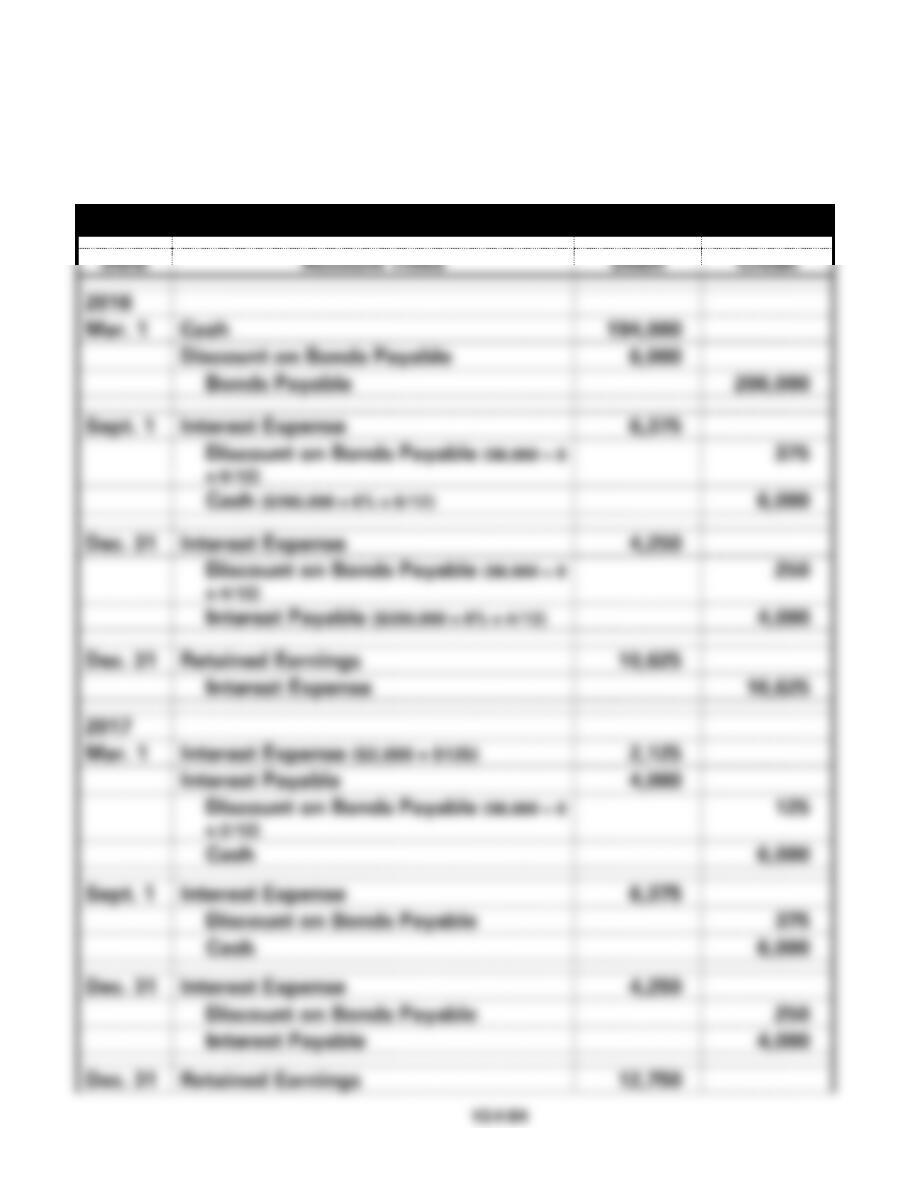

b.

General Journal

Date

Account Titles

Debit

Credit

2016

Mar. 1

Cash

194,000

Discount on Bonds Payable

6,000

Bonds Payable

200,000

Sept. 1

Interest Expense

6,375

Discount on Bonds Payable ($6,000 8

x 6/12)

375

Cash ($200,000 x 6% x 6/12)

6,000

Dec. 31

Interest Expense

4,250

Discount on Bonds Payable ($6,000 8

x 4/12)

250

Interest Payable ($200,000 x 6% x 4/12)

4,000

Dec. 31

Retained Earnings

10,625

Interest Expense

10,625

2017

Mar. 1

Interest Expense ($2,000 + $125)

2,125

Interest Payable

4,000

Discount on Bonds Payable ($6,000 8

x 2/12)

125

Cash

6,000

Sept. 1

Interest Expense

6,375

Discount on Bonds Payable

375

Cash

6,000

Dec. 31

Interest Expense

4,250

Discount on Bonds Payable

250

Interest Payable

4,000

Dec. 31

Retained Earnings

12,750

Interest Expense

12,750

PROBLEM 10-30B (cont.)

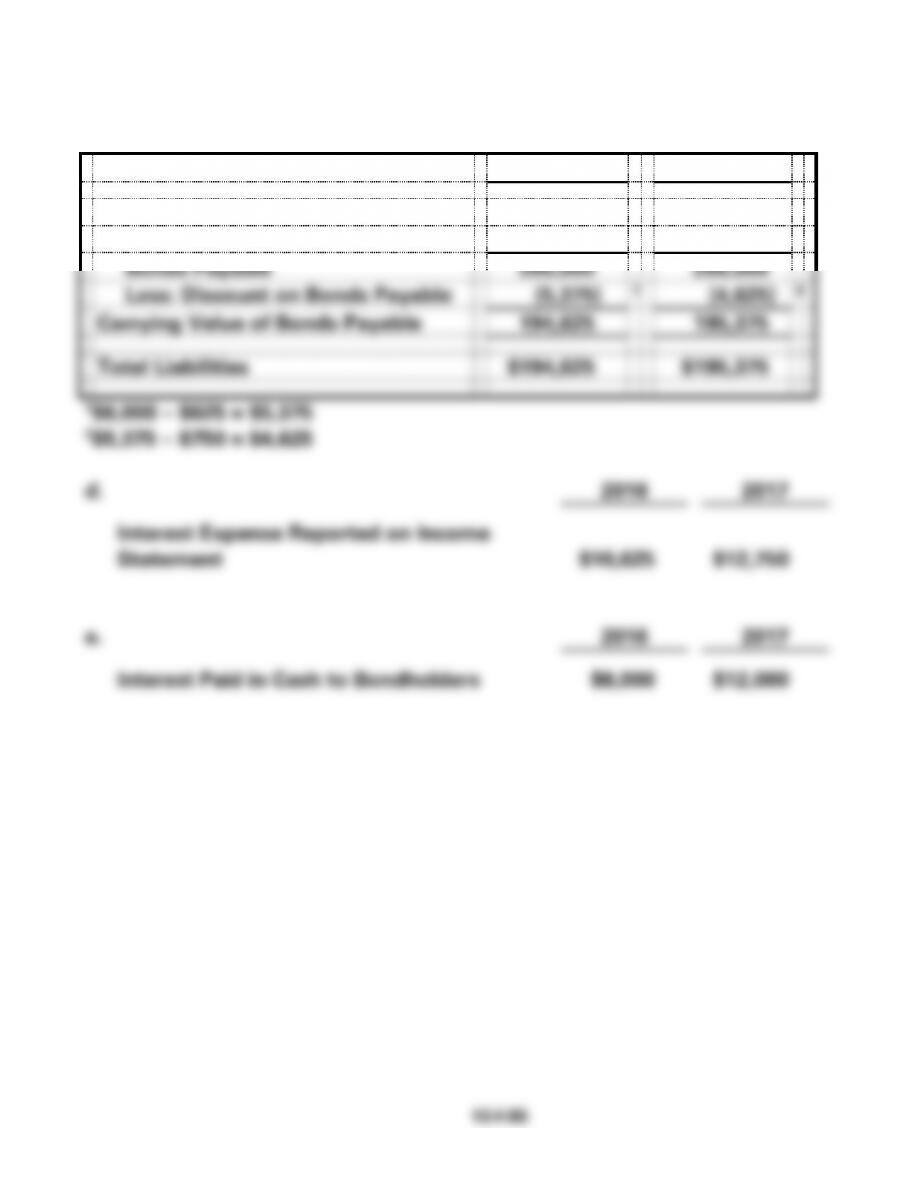

c.

2016

2017

Liabilities

Interest Payable

$ 4,000

$ 4,000

Bonds Payable

200,000

200,000

Less: Discount on Bonds Payable

(5,375)

1

(4,625)

2

Carrying Value of Bonds Payable

194,625

195,375

Total Liabilities

$194,625

$195,375

d.

2016

2017

Interest Expense Reported on Income

Statement

$10,625

$12,750

e.

2016

2017

Interest Paid in Cash to Bondholders

$6,000

$12,000

PROBLEM 10-31B

1. Issued bonds at 103. Cash proceeds = $309,000; Premium = $9,000,

1/1/16.

2. Purchased land for $309,000, 1/1/16.

3. Land rental, $36,000 per year, 2016, 2017, 2018.

4. Interest payments per year, ($300,000 x 6%), $18,000 (years 2016, 2017,

2018).

5. Amortized premium per year, $600 ($9,000 15), 2016, 2017, 2018.

6. Sold the land for $310,000, 1/1/19. (Gain = $1,000)

7. Paid off bonds at 104, cash payment of ($300,000 x 104%) $312,000,

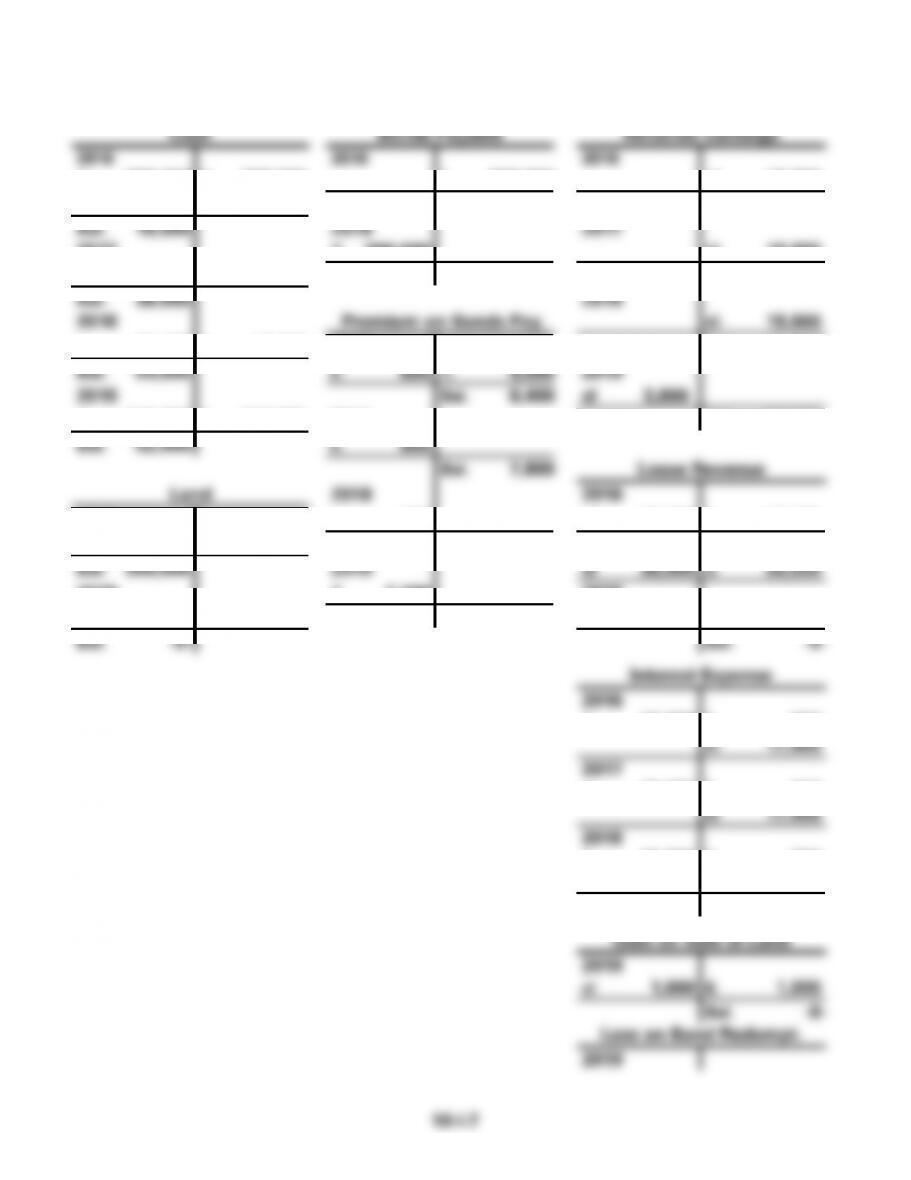

PROBLEM 10-31B (cont.) T-Accounts Provided for Instructor’s Use:

Cash

Bonds Payable

Retained Earnings

2016

2016

2016

1. 309,000

2. 309,000

1. 300,000

cl 18,600

3. 36,000

4. 18,000

Bal. 300,000

Bal. 18,600

Bal. 18,000

2019

2017

2017

7. 300,000

cl. 18,600

3. 36,000

4. 18,000

Bal. -0-

Bal. 37,200

Bal. 36,000

2018

2018

Premium on Bonds Pay.

cl. 18,600

3. 36,000

4. 18,000

2016

Bal. 55,800

Bal. 54,000

5. 600

1. 9,000

2019

2019

Bal. 8,400

cl 3,800

6. 310,000

7. 312,000

2017

Bal. 52,000

Bal. 52,000

5. 600

Bal. 7,800

Lease Revenue

Land

2018

2016

2016

5. 600

cl 36,000

3. 36,000

2. 309,000

Bal. 7,200

2017

Bal. 309,000

2019

cl 36,000

3. 36,000

2019

7. 7,200

2018

6. 309,000

Bal. -0-

cl 36,000

3. 36,000

Bal. -0-

Bal. -0-

Interest Expense

2016

4. 18,000

5. 600

cl 17,400

2017

4. 18,000

5. 600

cl 17,400

2018

4. 18,000

5. 600

cl 17,400

Bal. -0-

Gain on Sale of Land

2019

cl 1,000

6. 1,000

Bal. -0-

Loss on Bond Redempt.

2019

7. 4,800

cl 4,800

Bal. -0-

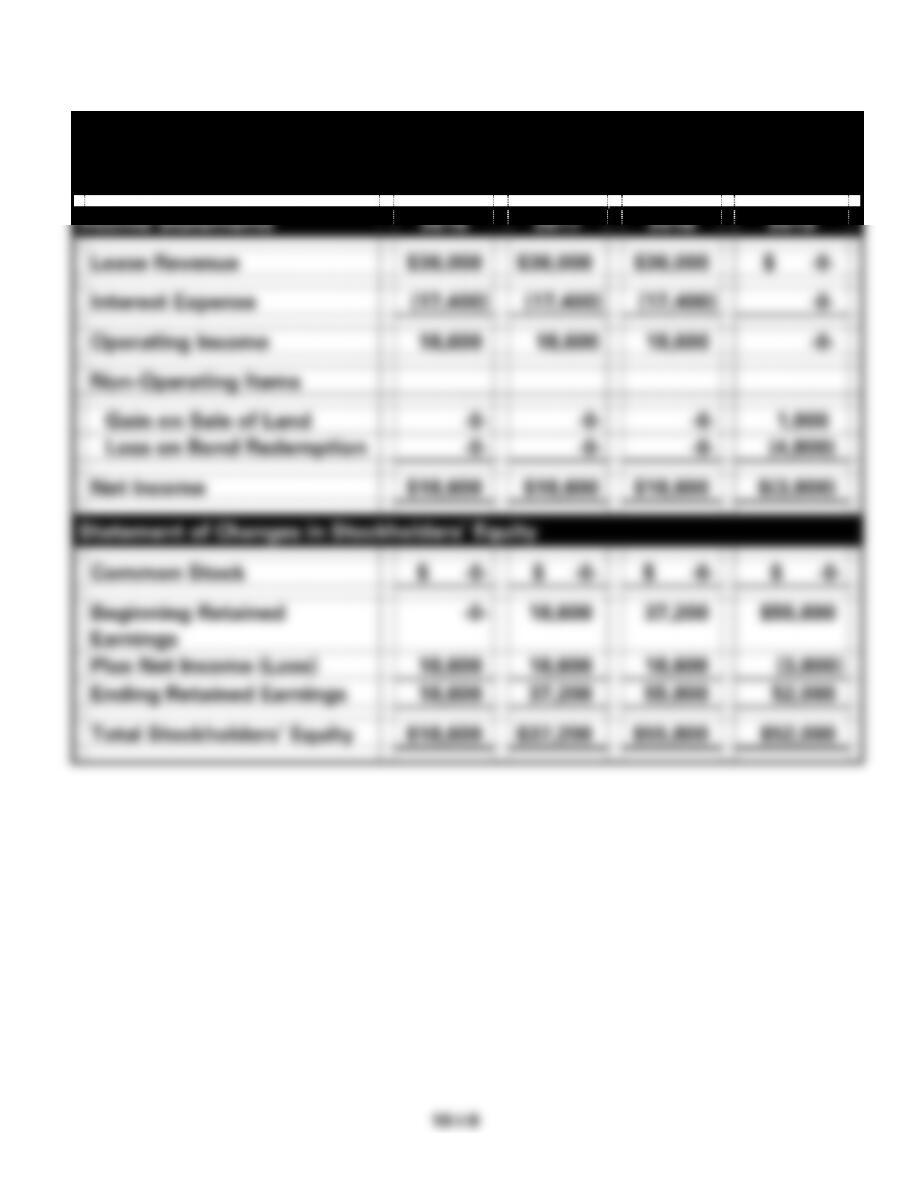

PROBLEM 10-31B (cont.)

Whitten Company

Financial Statements

For the Year Ended December 31

Income Statements

2016

2017

2018

2019

Lease Revenue

$36,000

$36,000

$36,000

$ -0-

Interest Expense

(17,400)

(17,400)

(17,400)

-0-

Operating Income

18,600

18,600

18,600

-0-

Non-Operating Items

Gain on Sale of Land

-0-

-0-

-0-

1,000

Loss on Bond Redemption

-0-

-0-

-0-

(4,800)

Net Income

$18,600

$18,600

$18,600

$(3,800)

Statement of Changes in Stockholders’ Equity

Common Stock

$ -0-

$ -0-

$ -0-

$ -0-

Beginning Retained

Earnings

-0-

18,600

37,200

$55,800

Plus Net Income (Loss)

18,600

18,600

18,600

(3,800)

Ending Retained Earnings

18,600

37,200

55,800

52,000

Total Stockholders’ Equity

$18,600

$37,200

$55,800

$52,000

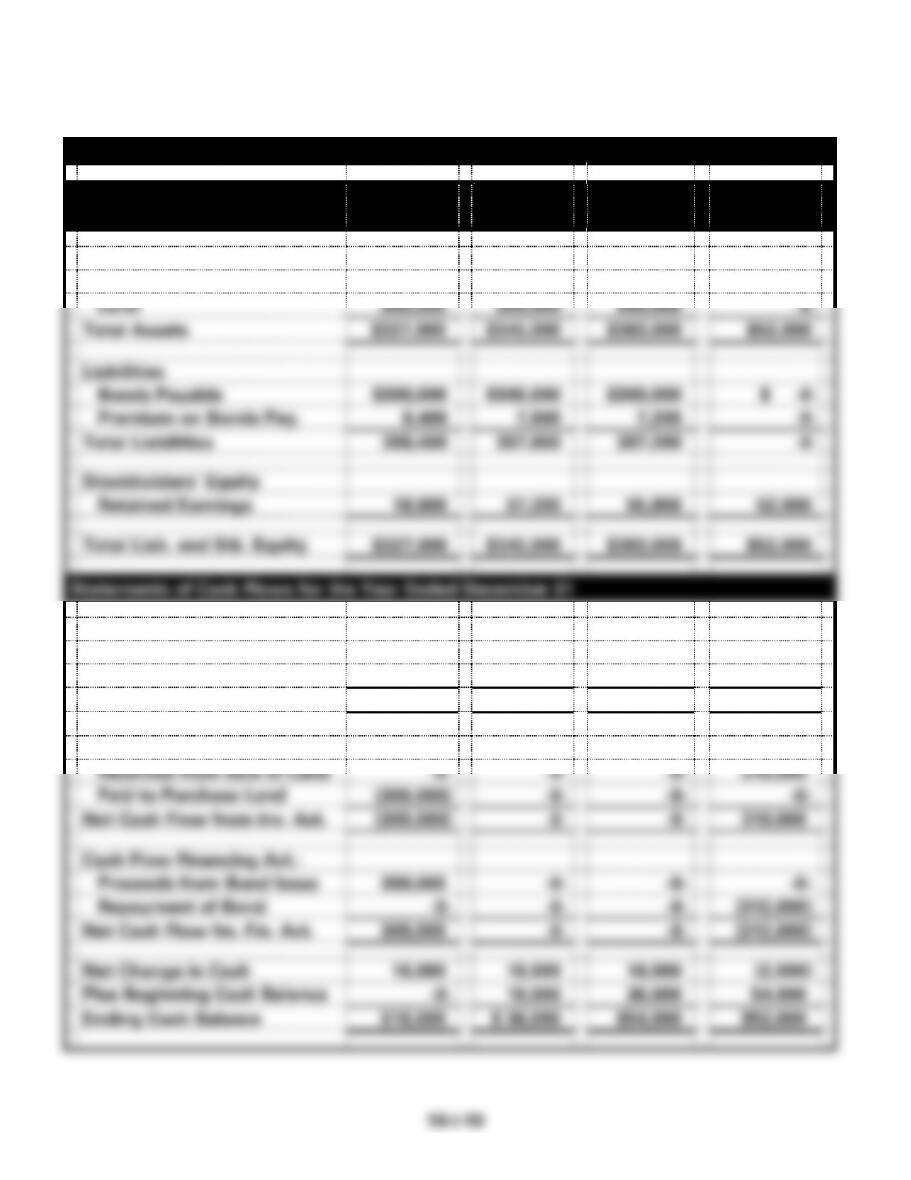

PROBLEM 10-31B (cont.)

Whitten Company Financial Statements

Balance Sheets as of December

31,

2016

2017

2018

2019

Assets

Cash

$ 18,000

$ 36,000

$ 54,000

$52,000

Land

309,000

309,000

309,000

-0-

Total Assets

$327,000

$345,000

$363,000

$52,000

Liabilities

Bonds Payable

$300,000

$300,000

$300,000

$ -0-

Premium on Bonds Pay.

8,400

7,800

7,200

-0-

Total Liabilities

308,400

307,800

307,200

-0-

Stockholders’ Equity

Retained Earnings

18,600

37,200

55,800

52,000

Total Liab. and Stk. Equity

$327,000

$345,000

$363,000

$52,000

Statements of Cash Flows for the Year Ended December 31

Cash Flow From Oper. Act.:

Receipts from Lease

$ 36,000

$36,000

$36,000

$ -0-

Paid for Interest

(18,000)

(18,000)

(18,000)

-0-

Net Cash Flow fm. Oper. Act.

18,000

18,000

18,000

-0-

Cash Flow From Inv. Act.:

Received from Sale of Land

-0-

-0-

-0-

310,000

Paid to Purchase Land

(309,000)

-0-

-0-

-0-

Net Cash Flow from Inv. Act.

(309,000)

-0-

-0-

310,000

Cash Flow Financing Act.:

Proceeds from Bond Issue

309,000

-0-

-0-

-0-

Repayment of Bond

-0-

-0-

-0-

(312,000)

Net Cash Flow fm. Fin. Act.

309,000

-0-

-0-

(312,000)

Net Change in Cash

18,000

18,000

18,000

(2,000)

Plus Beginning Cash Balance

-0-

18,000

36,000

54,000

Ending Cash Balance

$18,000

$ 36,000

$54,000

$52,000

PROBLEM 10-32B

Effect of Transactions on Financial Statements

No

.

Assets

=

Liab.

+

S. Equity

Rev./

Gain

−

Exp./

Loss

=

Net Inc.

Cash Flow

a.

+

+

NA

NA

NA

NA

+ FA

b.

−

−

−

NA

+

−

− OA

c.

+

+

NA

NA

NA

NA

+ FA

d.

−

NA

−

NA

+

−

− OA

e.

−

−

−

NA

+

−

− FA/OA

f.

+

+

NA

NA

NA

NA

+ FA

g.

−

NA

−

NA

+

−

− OA

h.

+

+

NA

NA

NA

NA

+ FA

i.

−

+

−

NA

+

−

− OA

PROBLEM 10-33B

a.

Date

Account Title

Debit

Credit

1/1/16

Cash

104,330

Premium on Bonds Payable

4,330

Bonds Payable

100,000

Date

Account Title

Debit

Credit

12/31/18

Interest Expense

5,136

Premium on Bonds Payable

864

Cash

6,000

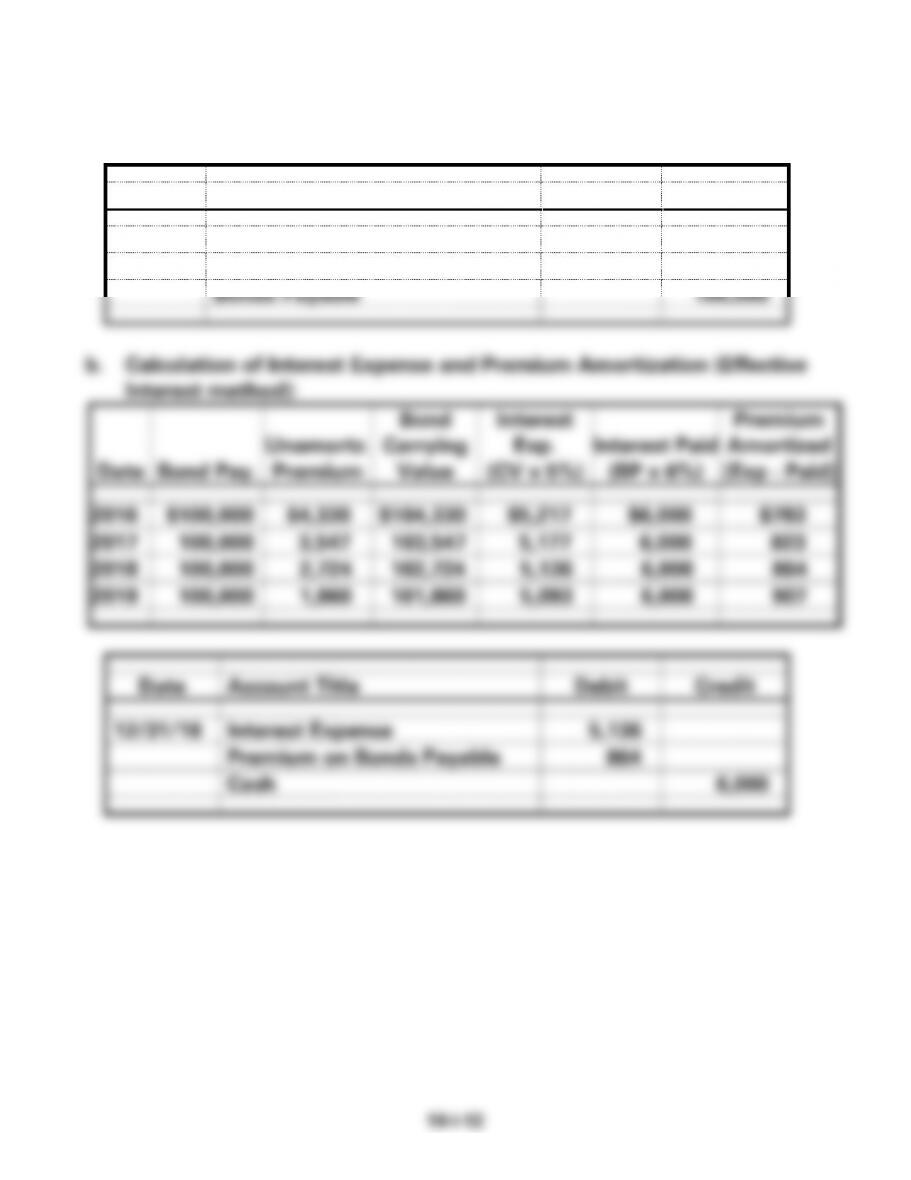

PROBLEM 10-33B (cont.)

c. Calculation of Interest Expense and Premium Amortization (Straight–

line method):

PROBLEM 10-34B

a. First, compute EBIT for each company:

Tacoma

Olympia

Net Income

$145,000

$155,000

Interest Expense

60,000

45,000

Tax Expense

95,000

100,000

EBIT

$300,000

$300,000

Problem 10-34B part b. (cont.)

Even though the return-on-assets ratios of Tacoma and Olympia are

1. Short-term notes mature within one year or one operating cycle,

whichever is longer. Long-term notes payable are used to satisfy

2.

I. Princ

ipal

II. Pay

men

t

III. Inter

est

IV. Red

ucti

on

Period

V. Bal.

1/1

12/31

VI. Exp.

8%

of Prin.

1

$ 72,000

$16,246

$5,760

$10,486

2

61,514

16,246

4,921

11,325

3

50,189

Interest expense in year 1 and 2 is $5,760 and $4,921, respectively.

The principal balance at the end of year 2 is $50,189.

3. A line of credit is a preapproved amount of credit that is available to

a business to use as needed. It eliminates the need to get loan

4. A business may need to borrow funds for a short period of time or a

longer period. Most short-term financing is in the form of loans

5. One of the primary advantages of bond financing is that the

6. One of the primary disadvantages of a bond issue is the restrictions that may be placed on management. These

7. One reason that a company may be able to borrow money at a lower

interest rate if bonds are issued rather than borrowing the money

from a financial institution is the way financial institutions make

their money. Banks receive money from customers through

8. Tax rules seem to encourage borrowing (debt financing) over

stockholder financing (equity financing) because interest paid on

9. Financial leverage is the concept of acquiring additional funds

10. The secured bond will usually have the lower interest rate because

asset. The unsecured bond is issued based on the general credit of

11. Restrictive covenants are limitations placed on a company that will

12. Term bonds mature on a specific date in the future. For example, a

$1,000,000, 10-year term bond issued on Jan. 1, 2015 would mature

13. A sinking fund is a fund into which a company makes annual or

14. Callable bonds allow the company to pay off the debt prior to the

maturity date at a specified amount called the call price. The call

15. The issuance of $100,000, 5%, 10-year bonds at face will result in an

increase to assets and liabilities on the balance sheet. The income

statement is not affected by the issuance of the bonds. The cash

16. Bonds can be issued at a premium or discount (an amount above or

rate with the market interest rate. The difference in cash proceeds

17. When the effective interest rate is higher than the stated interest

18. The issuance of bonds by a company is an asset source transaction.

19. The passage of time is usually the cause of the effective interest rate

and the stated interest rate being different. When bonds are issued,

20. The cash received for the bond will be $975 ($1,000 x .975).

21. The carrying value of a bond is the face value of the bond less any

22. The carrying value of the bonds is $19,800 ($25,000 face minus

$5,200 discount). The carrying value of the bond represents the

23. When the effective interest rate is higher than the stated interest

rate, interest expense will be higher than the amount of interest

24. The issuer of a bond would prefer to pay interest annually rather

than semiannually because of the timing of the cash outflow.

25. Any loss from the redemption of bonds is reported on the income

26. Debt financing has a tax advantage over equity financing because

not.

27. The after-tax cost of the debt is $7,000, computed as follows:

Interest Expense $10,000

28. Debt financing increases the risk factor of a business. This risk

arises due to the definite liability to pay interest on the debt and

risk.

29. The times interest earned ratio (EBIT/Interest Expense) assesses the