7-12

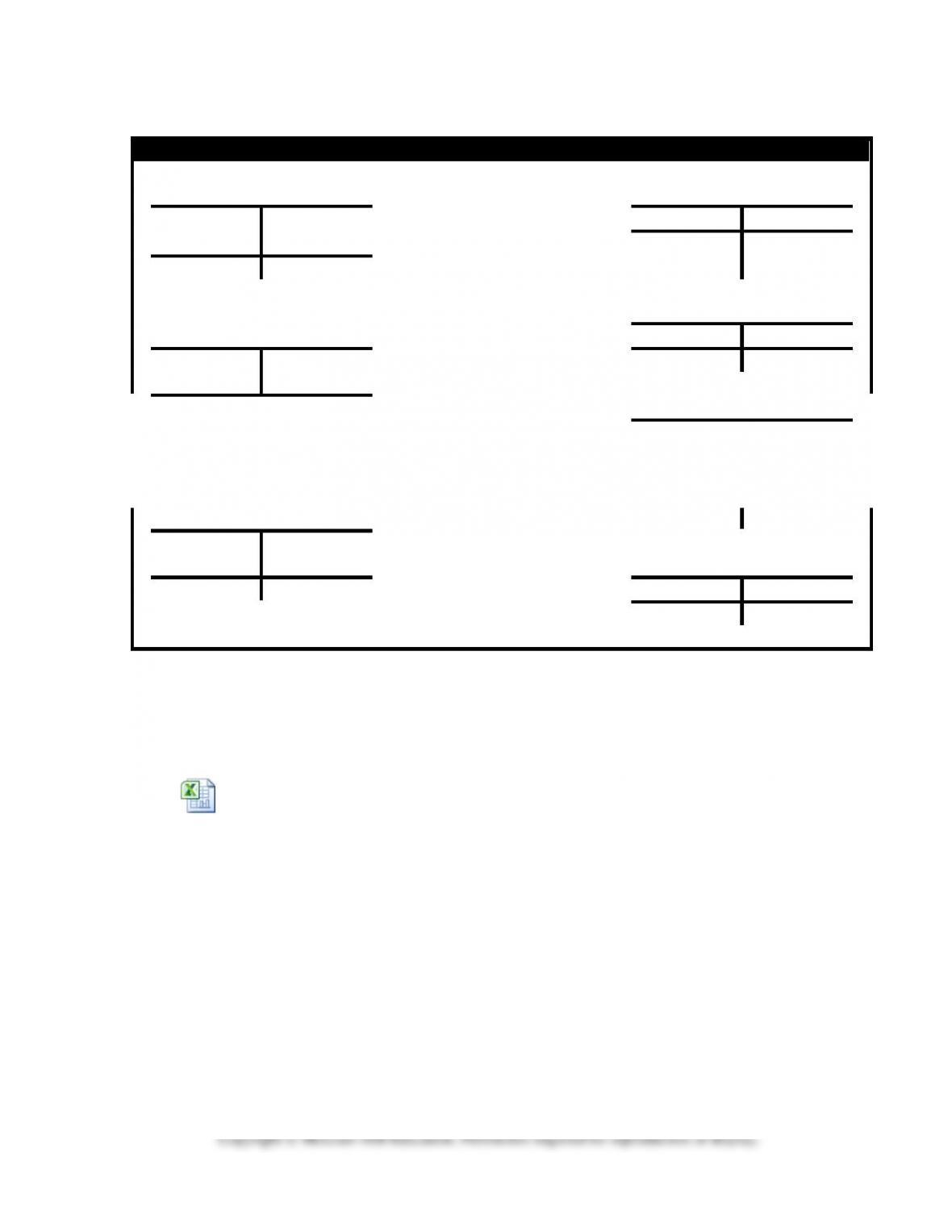

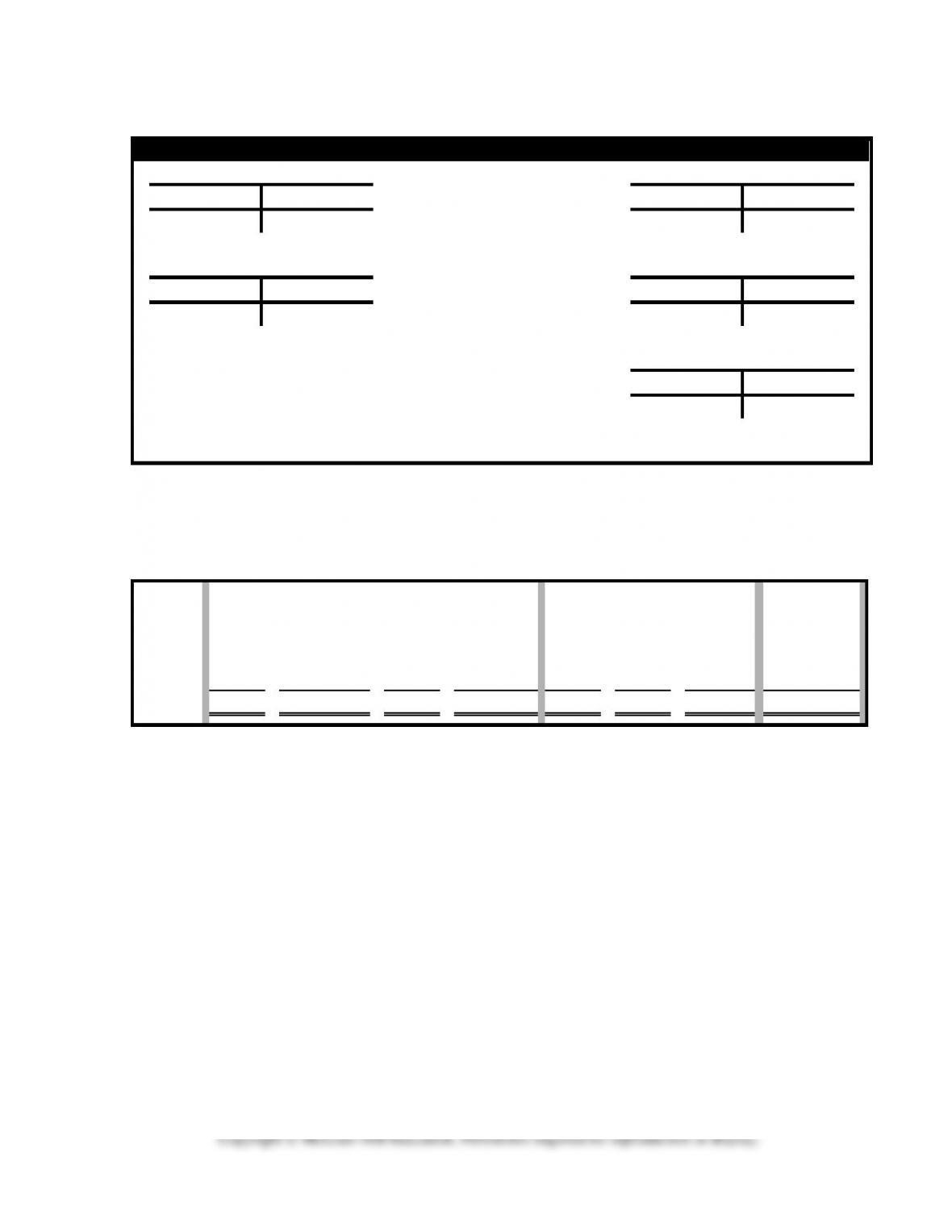

Demonstration Problem 7-3 Solution, part a. 2015 T-accounts

Ledger T-Accounts

Cash

Common Stock

(1) 50,000

4,200 (2)

50,000 (1)

(3) 7,300

10,000 (4)

50,000 Bal.

Bal. 43,100

Retained Earnings

Notes Rec.

cl. 4,200

7,550 cl

(4) 10,000

3,350 Bal

Bal. 10,000

Revenue

7,300

(3)

7550

cl

250

(4)

Int. Rec.

(4) 250

Operating Expenses

Bal. 250

(2) 4,200

4,200 cl

Demonstration Problem 7-3 Solution, part b. Horizontal Financial

Statements Model, 2015

Worksheet Edmonds

FFAC9e Ch 7 IM.xls

7-13

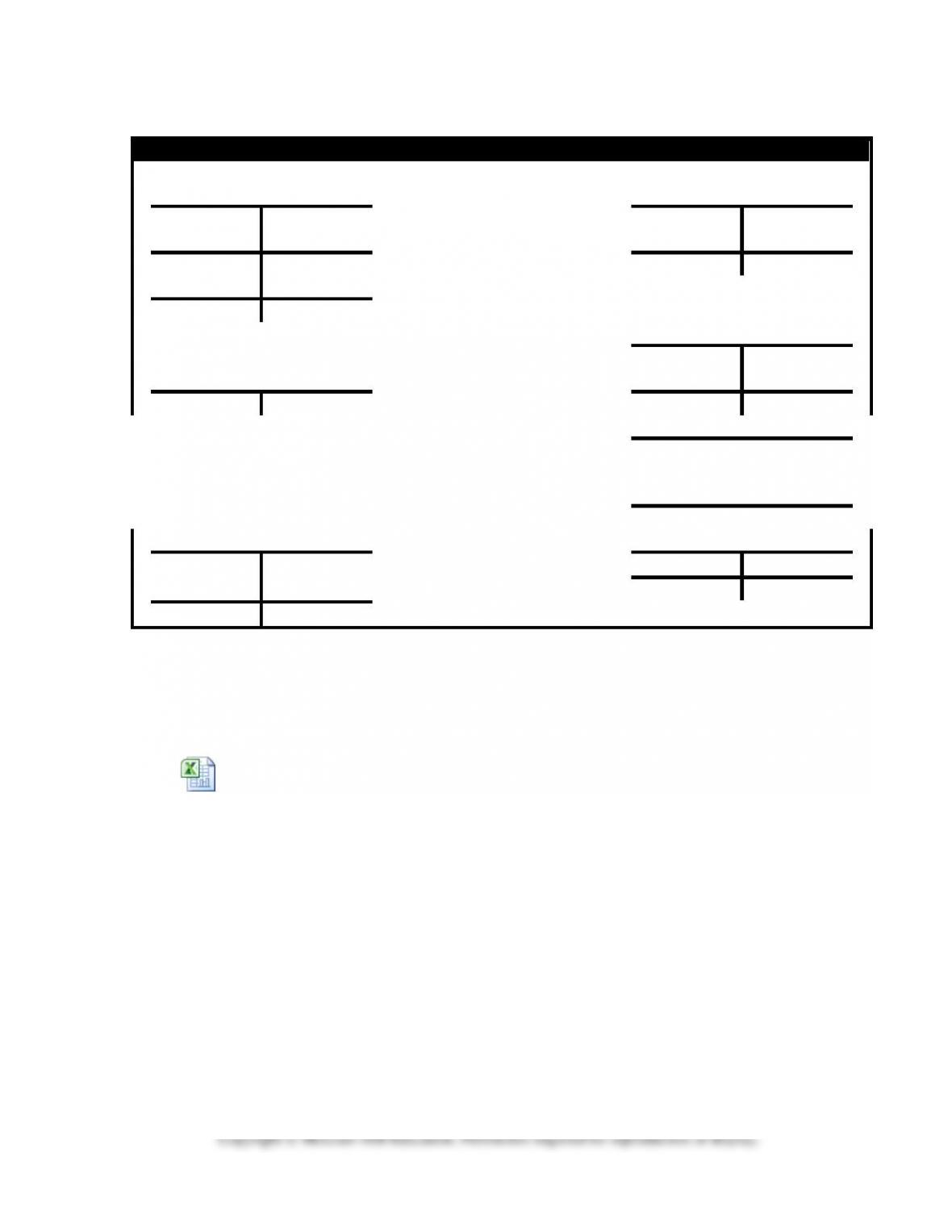

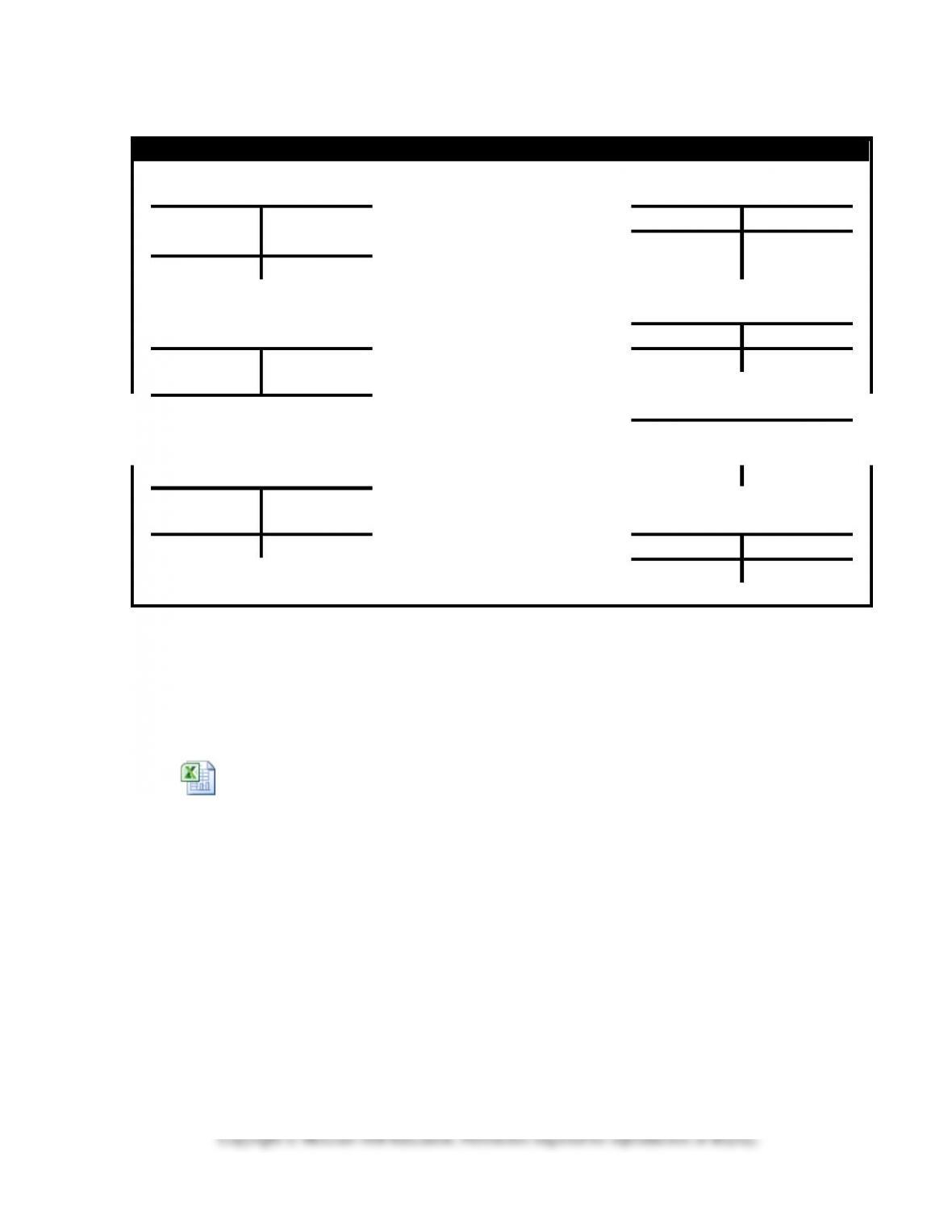

Demonstration Problem 7-3 Solution, part a. 2016 T-accounts

Ledger T-Accounts

Cash

Common Stock

Bal. 43,100

50,000 Bal.

(1b) 10,000

(1c) 500

50,000Bal.

(2) 9,500

6,400 (3)

Bal 56,700

Retained Earnings

Bal.

3,350

Note Rec.

cl 6,400

9,750 cl

Bal. 10,000

10,000 (1b)

Bal.

6,700

Revenue

Bal. 0

250 (1a)

cl

9,750

9,500 (2)

Int. Rec.

Operating Expense

Bal. 250

(3) 6,400

6,400 cl

(1a) 250

500 (1c)

Bal. 0

Demonstration Problem 7-3 Solution, part b. Horizontal Financial

Statements Model, 2016

Worksheet Edmonds

FFAC9e Ch 7 IM.xls

7-14

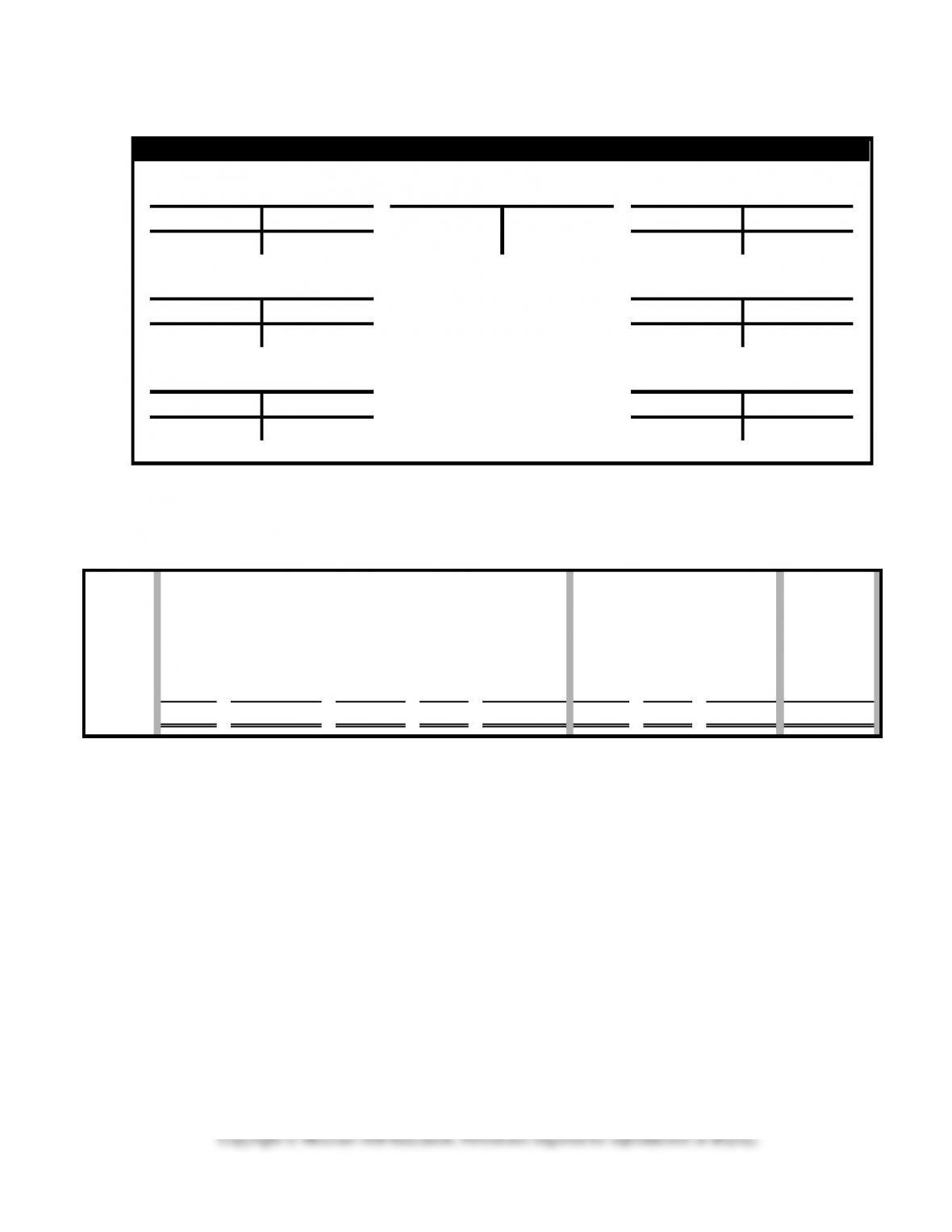

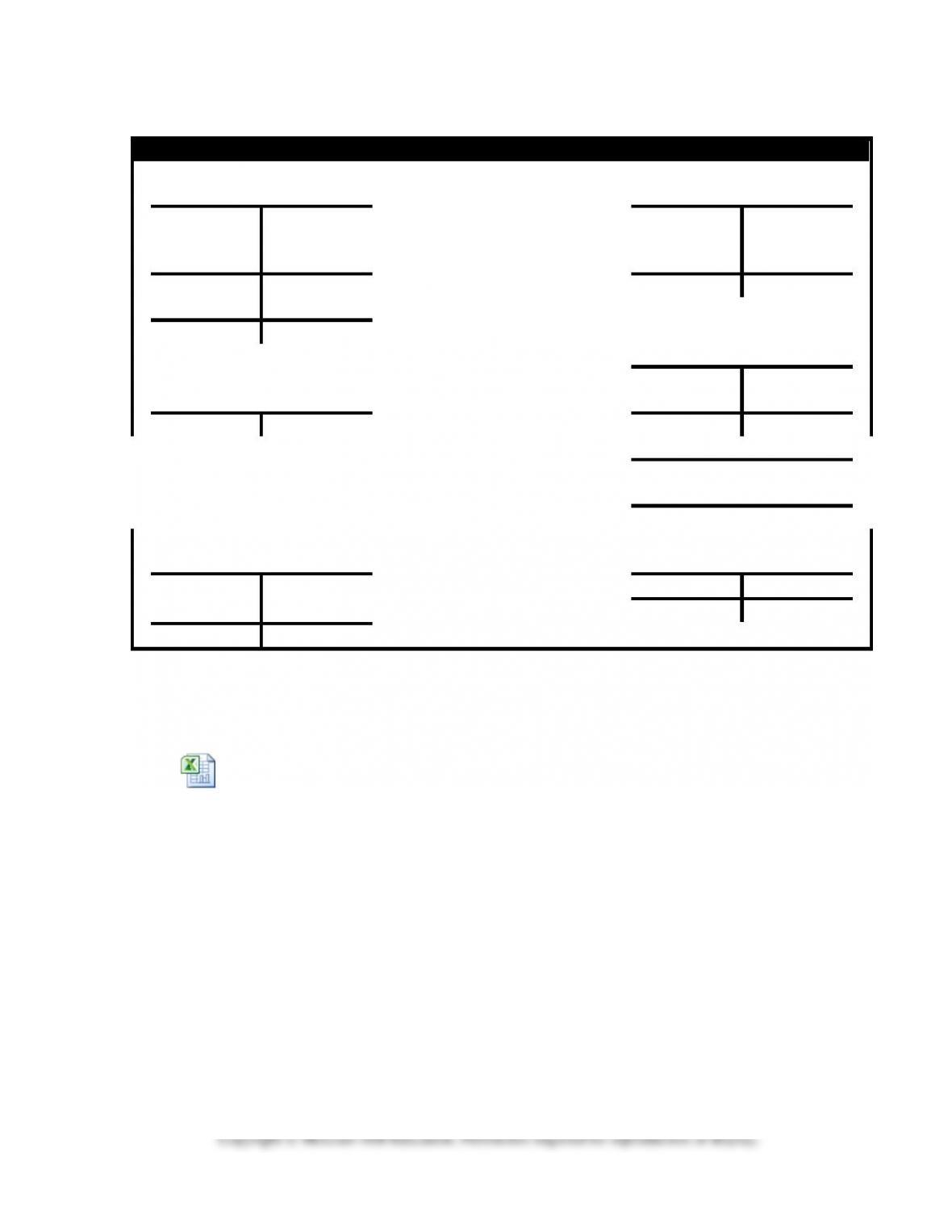

Demonstration Problem 7-1 Workpaper, part a. T-accounts, 2015

Ledger T-Accounts

Cash

Liabilities

Retained Earnings

Bal. 3,000

3,940Bal.

Accounts Receivable

Services Revenue

Bal. 1,000

Allow. for Doubt. Accts.

Bad Debts Expense

60 Bal.

Demonstration Problem 7-1 Workpaper, part b. Horizontal Financial State-

ments Model, 2015

Event

Assets

=

Liab.

+

Equity

Rev.

–

Exp.

=

Net Inc.

Cash Flow

No.

Cash

+

Accts. Rec.

+

(Allow.)

=

Ret. Earn.

Beg. bal.

0

+

0

+

0

=

0

+

0

0

–

0

=

0

0

1.

+

+

=

+

–

=

2.

+

+

=

+

–

=

3.

+

+

=

+

–

=

Totals

3,000

+

1,000

+

(60)

=

0

+

3,940

4,000

–

60

=

3,940

3,000 NC

7-15

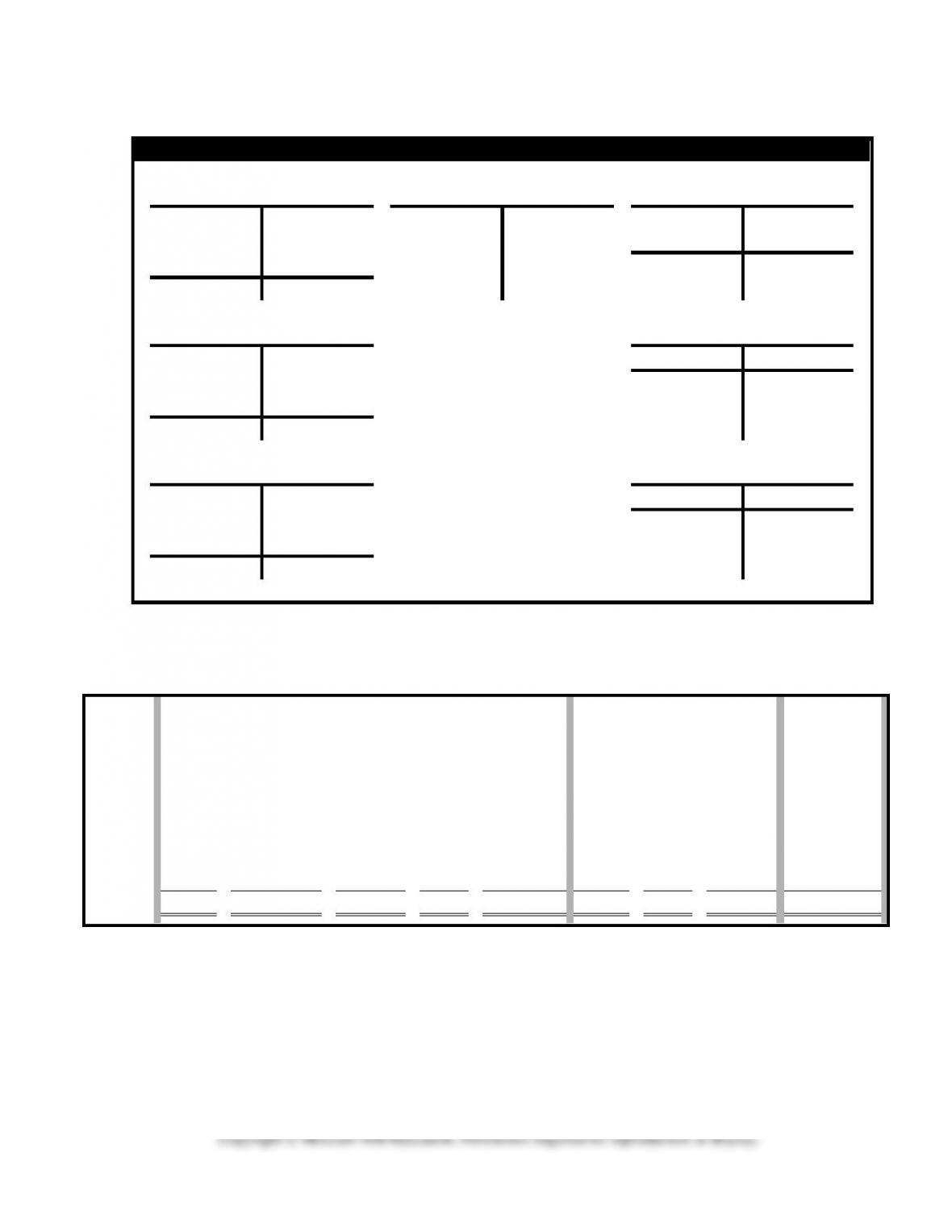

Demonstration Problem 7-1 Workpaper, part a. T-accounts, 2016

Ledger T-Accounts

Cash

Liabilities

Retained Earnings

Bal. 3,000

3,940Bal.

10,375

Bal. 8,405

Accounts Receivable

Services Revenue

Bal. 1,000

Bal. 2,060

Allow. for Doubt. Accts.

Bad Debts Expense

60 Bal.

90 Bal.

Demonstration Problem 7-1 Workpaper, part b. Statements Model, 2016

Event

Assets

=

Liab.

+

Equity

Rev.

–

Exp.

=

Net Inc.

Cash Flow

No.

Cash

+

Accts. Rec.

+

(Allow.)

=

Ret. Earn.

Beg. bal.

3,000

+

1,000

+

(60)

=

0

+

3,940

0

–

0

=

0

0

1.

+

+

=

+

–

=

2.

+

+

=

+

–

=

3.

+

+

=

+

–

=

4.

+

+

=

+

–

=

5.

+

+

=

+

–

=

6.

+

+

=

+

–

=

Totals

8,405

+

2,060

+

(90)

=

0

+

10,375

6,500

–

65

=

6,435

5,405 NC

7-16

Demonstration Problem 7-2 Workpaper, part a. T-accounts

Ledger T-Accounts

Cash

Retained Earnings

Bal. 7,600

7,600 Bal.

Accounts Receivable

Services Revenue

Credit Card Expense

Demonstration Problem 7-2 Workpaper, part b. Horizontal Finan-

cial Statements Model

Event

Assets

=

Liab.

+

Equity

Rev.

–

Exp.

=

Net Inc.

Cash Flow

No.

Cash

+

Accts. Rec.

=

W. Pay

Ret. Earn.

Beg. bal.

0

+

0

=

0

+

0

0

–

0

=

0

0

1.

+

=

+

–

=

2.

+

=

+

–

=

Totals

7,200

+

0

=

1,200

+

6,000

8,000

–

2,000

=

6,000

7,200 NC

7-17

Demonstration Problem 7-3 Workpaper, part a. 2015 T-accounts

Ledger T-Accounts

Cash

Common Stock

50,000 Bal.

Bal. 43,100

Retained Earnings

Notes Rec.

3,350 Bal.

Bal. 10,000

Revenue

Int. Rec.

Operating Expense

Bal. 250

Demonstration Problem 7-3 Workpaper, part b. Statements Model, 2015

Worksheet Edmonds

FFAC9e Ch 7 IM.xls

7-18

Demonstration Problem 7-3 Workpaper, part a. 2016 T-accounts

Ledger T-Accounts

Cash

Common Stock

Bal. 43,100

50,000

Bal.

50,000 Bal.

Bal. 56,700

Retained Earnings

Bal.

3,350

Note Rec.

Bal. 10,000

Bal.

6,700

Revenue

Bal. 0

Int. Rec.

Operating Expense

Bal. 250

Bal. 0

Demonstration Problem 7-3 Workpaper, part b. Statements Model, 2016

Worksheet Edmonds

FFAC9e Ch 7 IM.xls

7-19

Quiz Questions for Chapter 7

Use the following information to answer the next three questions. Ellis Company started the year with a

$4,600 balance in accounts receivable and a $150 balance in the allowance for doubtful accounts. The company

had credit sales of $12,000, collections on accounts receivable of $13,000, and wrote off uncollectible accounts

of $200 during the year. The company believes that 2 percent of its credit sales will be uncollectible.

1. The balance in the accounts receivable account at the end of the year would be

a. $3,600.

b. $3,400.

c. $3,250.

d. $4,360.

2. The amount of uncollectible accounts expense appearing on the year’s income statement would be

a. $532.

b. $332.

c. $240.

d. $440.

3. The net realizable value of receivables at the end of the year would be

a. $3,210.

b. $3,350.

c. $3,250.

d. $3,410.

4. Under the allowance method, recording the write-off of an uncollectible account will have what effect on

the accounting equation?

a. Total assets decrease and equity decreases.

b. Total assets remain unchanged.

c. Total assets increase and equity decreases.

d. Liabilities increase and equity decreases.

5. ABC Company accepts a credit card in payment for $1,500 of services performed for a customer. The

credit card company charges a 4 percent service fee. Recording the transaction on ABC’s records will

a. increase assets by $1,440.

b. increase expenses by $60.

c. increase revenue by $1,500.

d. All of the above.

6. Under the direct write-off method, the write-off of a $500 uncollectible account will

a. decrease assets by $500 and decrease liabilities by $500.

b. decrease assets by $500 and increase uncollectible accounts expense by $500.

c. have no effect on total assets.

d. decrease assets by $500 and increase equity by $500.

7-20

The following information pertains to the next three questions. On April 1, 2015, Needy Company issued a

$5,000 note to Money Company. The note had a 12 percent interest rate and was to be repaid, with interest, on

April 1, 2016.

7. The amount of investment that Money Company recorded on April 1, 2015, was

a. $4,250.

b. $4,400.

c. $5,000.

d. $5,500.

8. The total amount of interest receivable that Money Company recorded on December 31, 2015, would be

a. $0.

b. $600.

c. $300.

d. $450.

9. Assuming no other similar transactions, the total amount of interest revenue that Money Company recorded

in 2016 would be

a. $1,200.

b. $150.

c. $0.

d. $600.

10. EFG Company uses the allowance method to account for bad debts. The company wrote off an uncollecti-

ble account receivable. Which of the following reflects how the write–off affects EFG’s financial state-

ments?

Assets

=

Liab.

+

Equity

Rev.

–

Exp.

=

Net Inc.

Cash Flow

a.

+ –

NA

NA

NA

NA

NA

NA

b.

+ –

NA

NA

NA

+

–

NA

c.

–

NA

Ä

NA

+

–

– OA

d.

+

+

NA

NA

NA

NA

– OA

7-21

Quiz Answers

Question

Answer

1

B

2

C

3

A

4

B

5

D

6

B

7

C

8

D

9

B

10

A

Copyright © McGraw-Hill Education. Permission required for reproduction or display.

7-22

Summary Outline of a Lesson Plan for Chapter 7

I. Use multicycle Demonstration Problem 7-1 to illustrate how bad debts affect fi-

nancial statements over two cycles.

A. The first cycle illustrates recording bad debts expense and establishing an allow-

ance for doubtful accounts.

B. The second cycle illustrates accounting for the write-off of uncollectible accounts,

the recovery of an account receivable previously written off, and recognizing bad

debts expense.

II. Use Demonstration Problem 7-2 to introduce accounting for credit card sales.

III. Use Demonstration Problem 7-3 to introduce accounting for notes receivable.

The problem covers two cycles. The note has a one-year term. Date of issue is dur-

ing the first cycle and date of payment occurs in the second cycle, requiring the stu-

dent to understand how to record interest receivable.

IV. Time considerations and homework assignments. Plan to spend approximately

two hours of class time on this chapter. Most of the time will be spent coving bad

debts, since students seem to struggle with this concept – especially where the allow-

ance method is used. Homework assignments may include Exercises 7-14 A or B and

7-6 A or B for bad debts, 7-11 A or B for notes receivable and 7-14 A or B for credit

card sales. Exercise 7-15 A or B is a great comprehensive assignment, covering con-

cepts from chapters 1 – 7.