2-12

ANSWERS TO QUESTIONS – CHAPTER 2

1. Accrual accounting attempts to record the effects of accounting

2. Recognition is the act of recording an event in the financial

3. Deferral is the recognition of revenue or expenses in a period after

4. If cash is collected in advance for services, the revenue is recognized

5. An asset source transaction increases assets and increases either

6. The issue of common stock, which is capital acquired from owners,

7. The recognition of revenue on account increases the corresponding

8. Asset Source Transaction Effect on Accounting Equation

Issue of Common Stock Increases Assets, Increases

2-13

9. Revenue is recognized under accrual accounting when a revenue-

10. The collection of cash for accounts receivable is an asset exchange

transaction. Only the asset side of the accounting equation is

11. If cash is collected in advance for services, a liability is created

equation.

12. Unearned revenue is cash that has been collected for services that

13. The recognition of expenses affects the accounting equation by

14. A claims exchange transaction is one where the claims of creditors

15. Cash payments to creditors are asset use transactions. These

16. Expenses are recognized under accrual accounting at the time the

17. Net cash flows from operations on the cash flow statement may be

2-14

payment of cash that is reported on the cash flow statement.

18. The income statement reflects the change in net assets associated

with operating a business, as shown by revenues and expenses.

19. Net income increases stockholders’ claims on business assets by

20. A cost can be either an asset or an expense. If the item acquired has

21. A cost is held in the asset account until the item is used to produce

revenue. When the revenue is generated, the asset is converted into

22. Supplies used during the accounting period are recognized in a

single adjusting entry at the end of the period. The amount of

23. An expense is a decrease in assets or an increase in liabilities that

24. Revenue is an increase in assets or a decrease in liabilities that

25. The purpose of the statement of changes in stockholders’ equity is

2-15

that an entity’s equity increased and decreased as a result of its

26. The purpose of the balance sheet is to provide information about an

entity’s assets, liabilities, and stockholders’ equity and their

27. The balance sheet is dated as of a specific date because it shows

information about an entity’s assets, liabilities, and stockholders’

28. Assets are listed on the balance sheet in accordance with their

cash).

29. The statement of cash flows explains the change in cash from one

used.

30. An adjusting entry is an entry that updates account balances prior to

preparation of the financial statements. The entry means that there

31. Temporary accounts (revenue, expense and dividends) are closed at

2-16

32. Period costs are costs that are recognized in an accounting period.

33. Salary of the tax return preparer could be directly matched with the

34. The four stages of the accounting cycle: Record transactions; adjust

the accounts; prepare statements; and close the temporary accounts.

The adjustment and closing processes have been added to the cycle

2-17

EXERCISE 2-1A

Holloway Company

Effect of Events on the 2016 Accounting Equation

Assets

=

Liabilities

+

Stockholders’ Equity

Event

Cash

+

Accounts

Rec.

=

+

Common

Stock

+

Retained

Earnings

Earned Revenue

+

18,000

=

+

+

18,000

Coll. Acct. Rec.

14,000

+

(14,000)

=

+

+

Ending Balance

14,000

+

4,000

=

-0-

+

-0-

+

18,000

f. Accounts Receivable: $18,000 – $14,000 = $4,000

g. $18,000 Net Income

h. $14,000 cash collected from accounts receivable.

i. $18,000

j. $18,000 of revenue was earned but only $14,000 of it was collected.

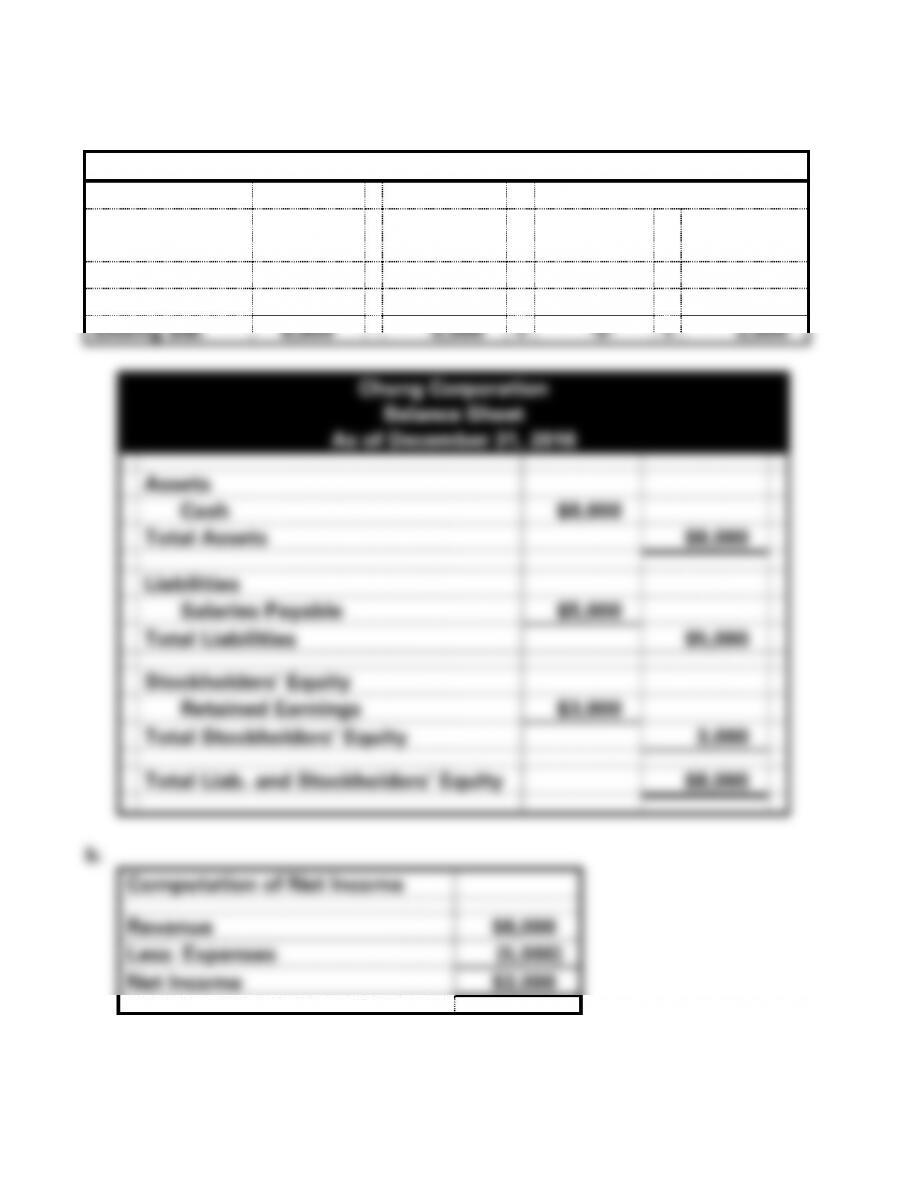

EXERCISE 2-2A

a.

Chung Corporation Accounting Equation – 2016

Event

Assets

=

Liabilities

+

Stockholders’ Equity

Cash

=

Salaries

Payable

+

Common

Stock

+

Retained

Earnings

Earned Rev.

8,000

8,000

Accrued Sal.

5,000

(5,000)

Ending Bal.

8,000

=

5,000

+

-0-

+

3,000

Assets

Cash

$8,000

Total Assets

Liabilities

Salaries Payable

$5,000

Total Liabilities

$3,000

Total Stockholders’ Equity

Computation of Net Income

Revenue

Less: Expenses

Net Income

2-19

EXERCISE 2-2A (cont.)

c.

Cash Flow from Operating Activities

Cash from Revenue

$8,000

Net Cash Flow from Operating Act.

$8,000

e. The salary expense is deducted from revenue in computing net

income, but it has not been paid. This creates a difference of $5,000

between net income and cash flow from operating activities. The

revenue is the same because it has been earned and collected.

2-20

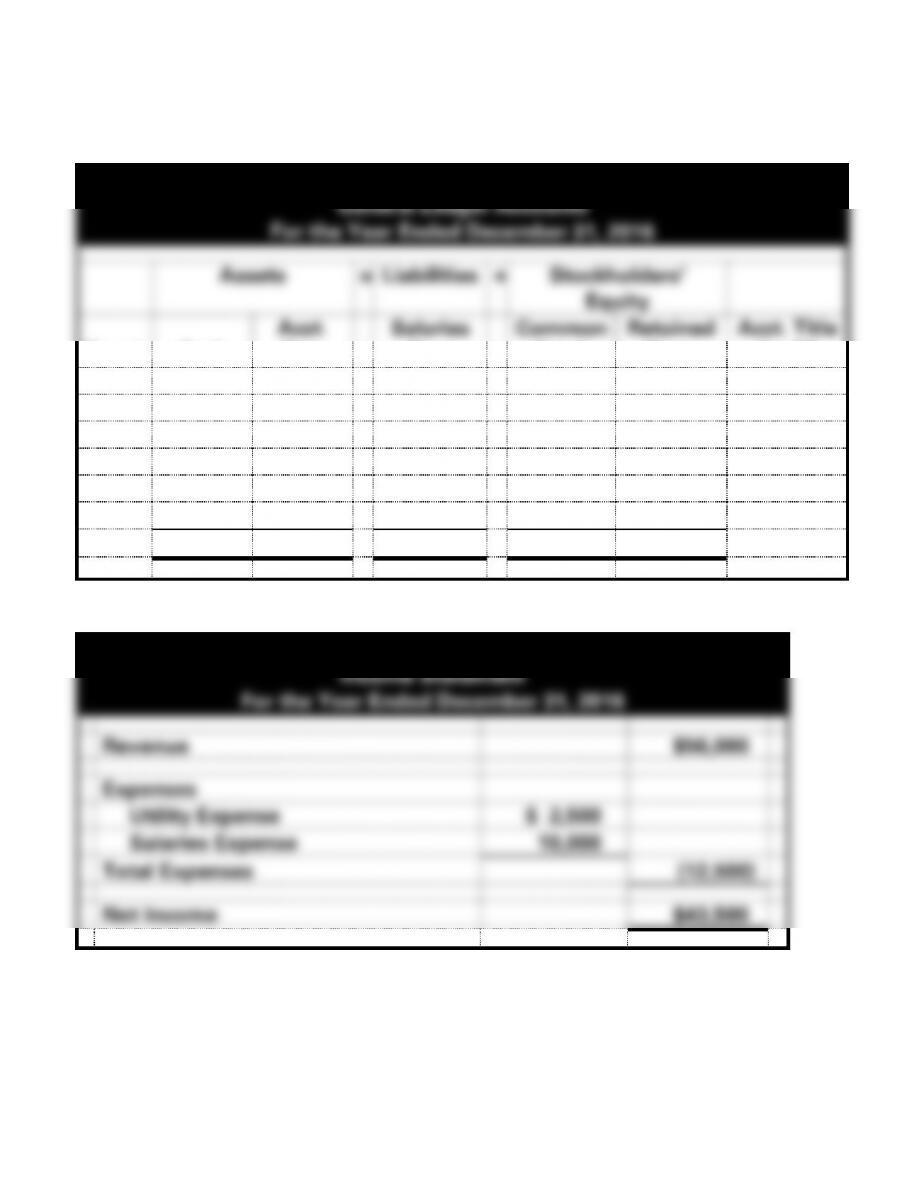

EXERCISE 2-3A

a.

Milea, Inc.

General Ledger Accounts

For the Year Ended December 31, 2016

Assets

=

Liabilities

+

Stockholders’

Equity

Event

Cash

Acct.

Rec.

=

Salaries

Pay.

+

Common

Stock

Retained

Earn.

Acct. Title

for RE

1.

20,000

20,000

2.

56,000

56,000

Revenue

3.

(2,500)

(2,500)

Util. Exp.

4.

48,000

(48,000)

5.

10,000

(10,000)

Sal. Exp.

6.

(2,000)

(2,000)

Dividends

Totals

63,500

8,000

=

10,000

+

20,000

41,500

b.

Milea, Inc.

Income Statement

For the Year Ended December 31, 2016

Revenue

$56,000

Expenses

Utility Expense

$ 2,500

Salaries Expense

10,000

Total Expenses

(12,500)

Net Income

$43,500

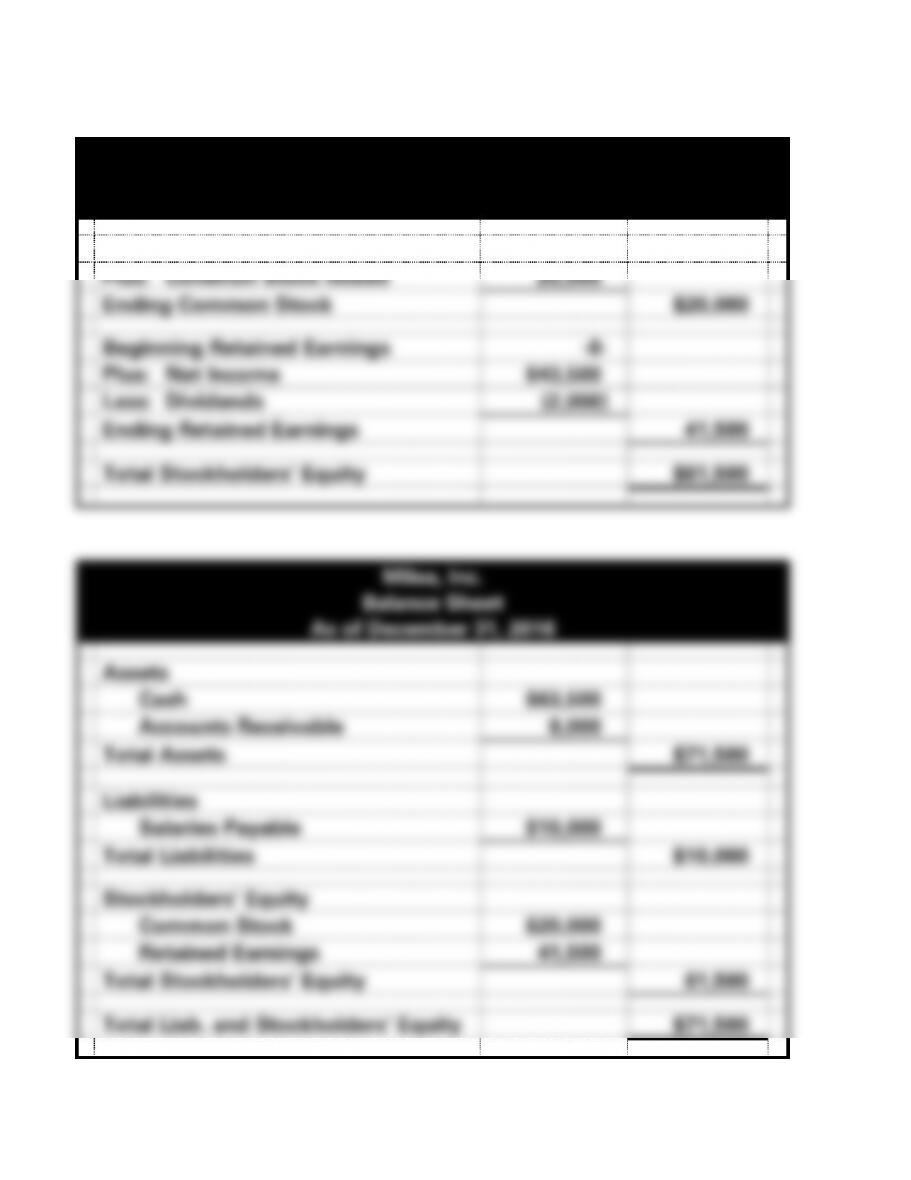

EXERCISE 2-3A b. (cont.)

Milea, Inc.

Statement of Changes in Stockholders’ Equity

For the Year Ended December 31, 2016

Beginning Common Stock

$ -0-

Plus: Common Stock Issued

20,000

Ending Common Stock

$20,000

Beginning Retained Earnings

-0-

Plus: Net Income

$43,500

Less: Dividends

(2,000)

Ending Retained Earnings

41,500

Total Stockholders’ Equity

$61,500

Assets

Cash

$63,500

Accounts Receivable

Total Assets

$71,500

Liabilities

Salaries Payable

$10,000

Stockholders’ Equity

Common Stock

41,500

Total Stockholders’ Equity

61,500

2-22

2-23

EXERCISE 2-3A b. (cont.)

Milea, Inc.

Statement of Cash Flows

For the Year Ended December 31, 2016

Cash Flow From Operating Activities

Cash Received from Customers

$48,000

Cash Paid for Expenses

(2,500)

Net Cash Flow from Operating Act.

$45,500

Cash Flow From Investing Activities

-0-

Cash Flow From Financing Activities

Issue of Stock

$20,000

Paid Dividends

(2,000)

Net Cash Flow from Financing Act.

18,000

Net Change in Cash

63,500

Plus: Beginning Cash Balance

-0-

Ending Cash Balance

$63,500

2-24

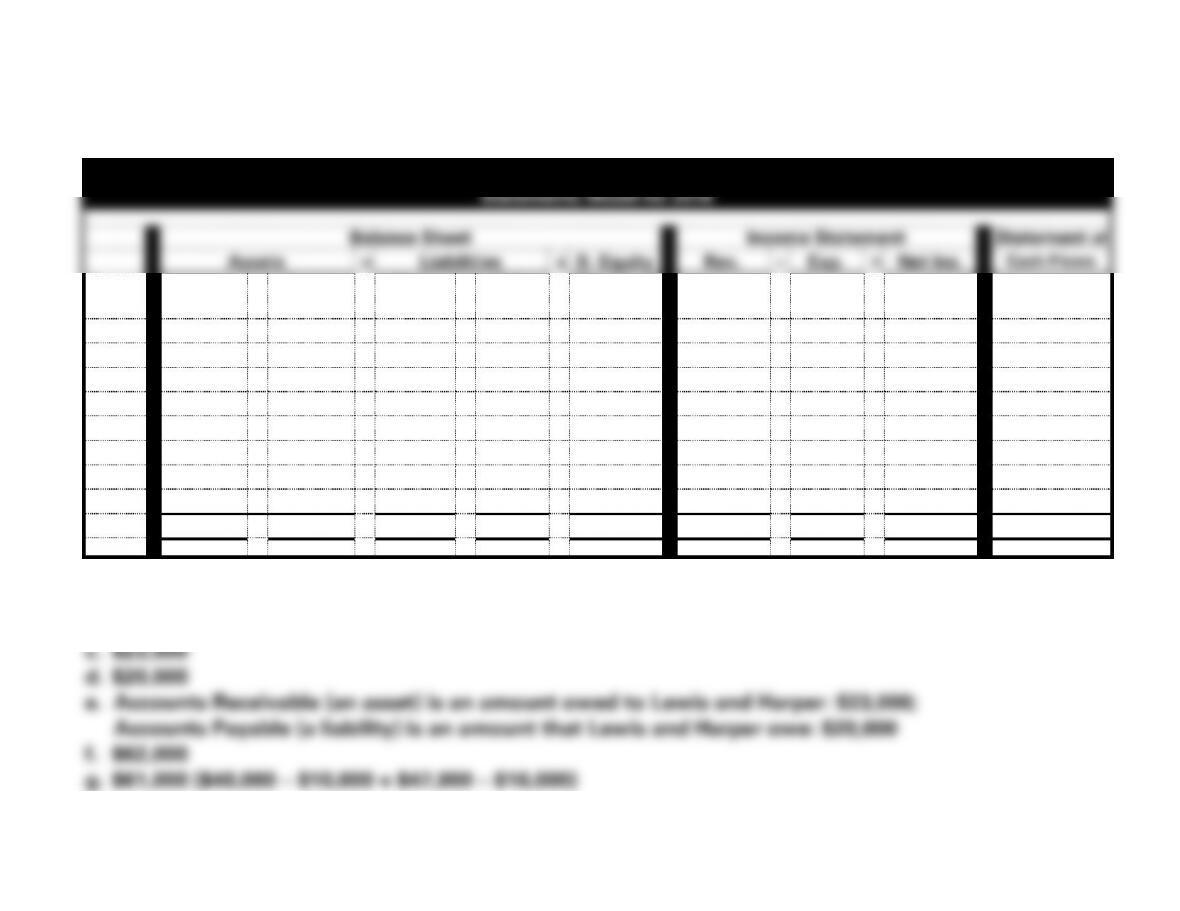

EXERCISE 2-4A

a.

Lewis and Harper

Statements Model for 2016

Balance Sheet

Income Statement

Statement of

Assets

=

Liabilities

+

S. Equity

Rev.

–

Exp.

=

Net Inc.

Cash Flows

Event

No.

Cash

+

Accts.

Rec.

=

Acct.

Payable

+

Sal.

Pay.

+

Retained

Earn.

1.

NA

70,000

NA

NA

70,000

70,000

NA

70,000

NA

2.

40,000

NA

NA

NA

40,000

40,000

NA

40,000

40,000 OA

3.

NA

NA

36,000

NA

(36,000)

NA

36,000

(36,000)

NA

4.

(10,000)

NA

NA

NA

(10,000)

NA

10,000

(10,000)

(10,000) OA

5.

47,000

(47,000)

NA

NA

NA

NA

NA

NA

47,000 OA

6.

(16,000)

NA

(16,000)

NA

NA

NA

NA

NA

(16,000) OA

7.

(8,000)

NA

NA

NA

(8,000)

NA

NA

NA

(8,000) FA

8.

NA

NA

NA

2,000

(2,000)

NA

2,000

(2,000)

NA

Totals

53,000

+

23,000

=

20,000

+

2,000

+

54,000

110,000

−

48,000

=

62,000

53,000 NC

b. Total assets: $76,000 ($53,000 + $23,000)

2-25

EXERCISE 2-5A

a.

Computation of Net Income

Revenue recognized on account

$68,000

Less accrued salary expense

(46,000)

Net Income

$22,000

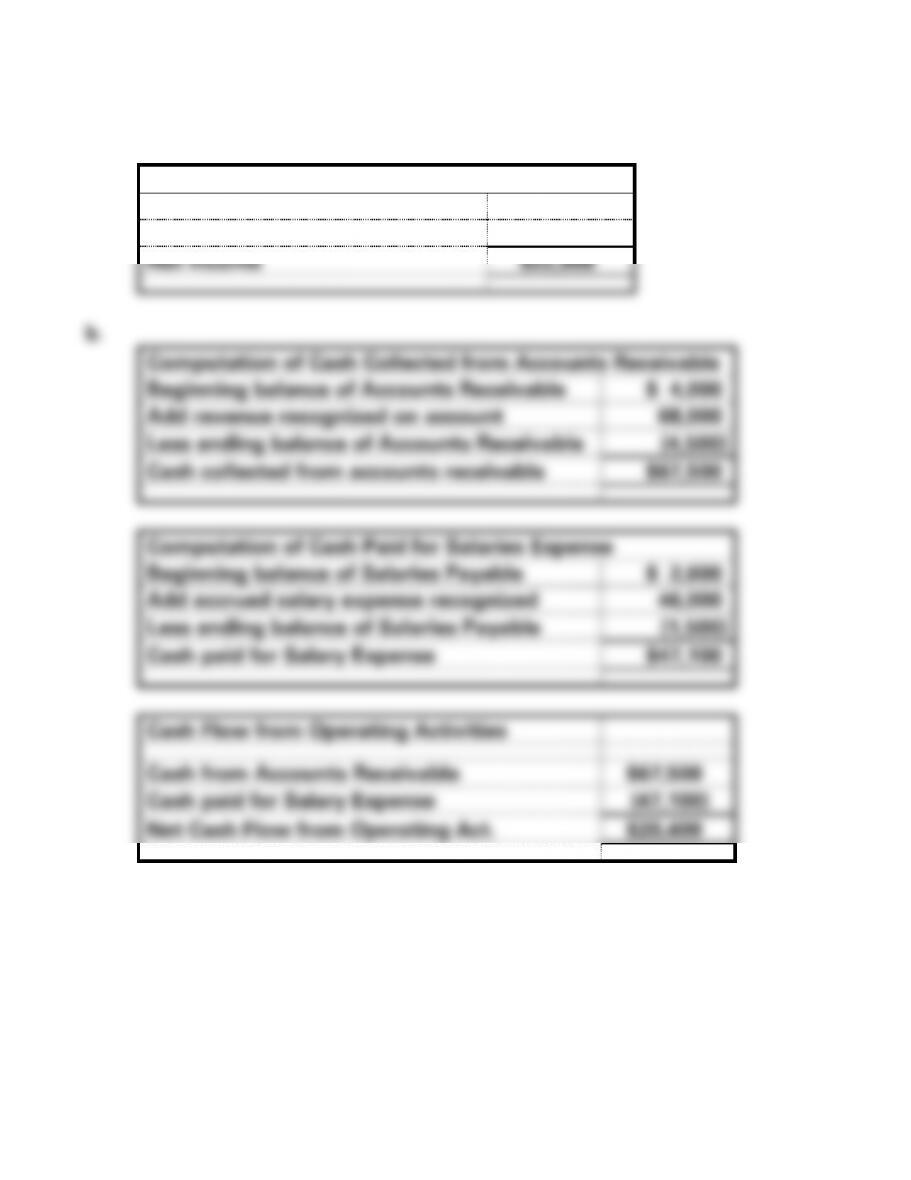

b.

Computation of Cash Collected from Accounts Receivable

Beginning balance of Accounts Receivable

$ 4,000

Add revenue recognized on account

68,000

Less ending balance of Accounts Receivable

(4,500)

Cash collected from accounts receivable

$67,500

Computation of Cash Paid for Salaries Expense

Beginning balance of Salaries Payable

$ 2,600

Add accrued salary expense recognized

46,000

Less ending balance of Salaries Payable

(1,500)

Cash paid for Salary Expense

$47,100

Cash Flow from Operating Activities

Cash from Accounts Receivable

$67,500

Cash paid for Salary Expense

(47,100)

Net Cash Flow from Operating Act.

$20,400

2-26

EXERCISE 2-6A

a. & c.

Event

Revenue

Expense

Statement of

Cash Flows

1.

NA

NA

$40,000 FA

2.

$82,000

NA

NA

3.

NA

NA

(6,000) FA

4.

NA

NA

76,000 OA

5.

NA

$53,000

(53,000) OA

6.

19,000

NA

19,000 OA

7.

NA

3,500

NA

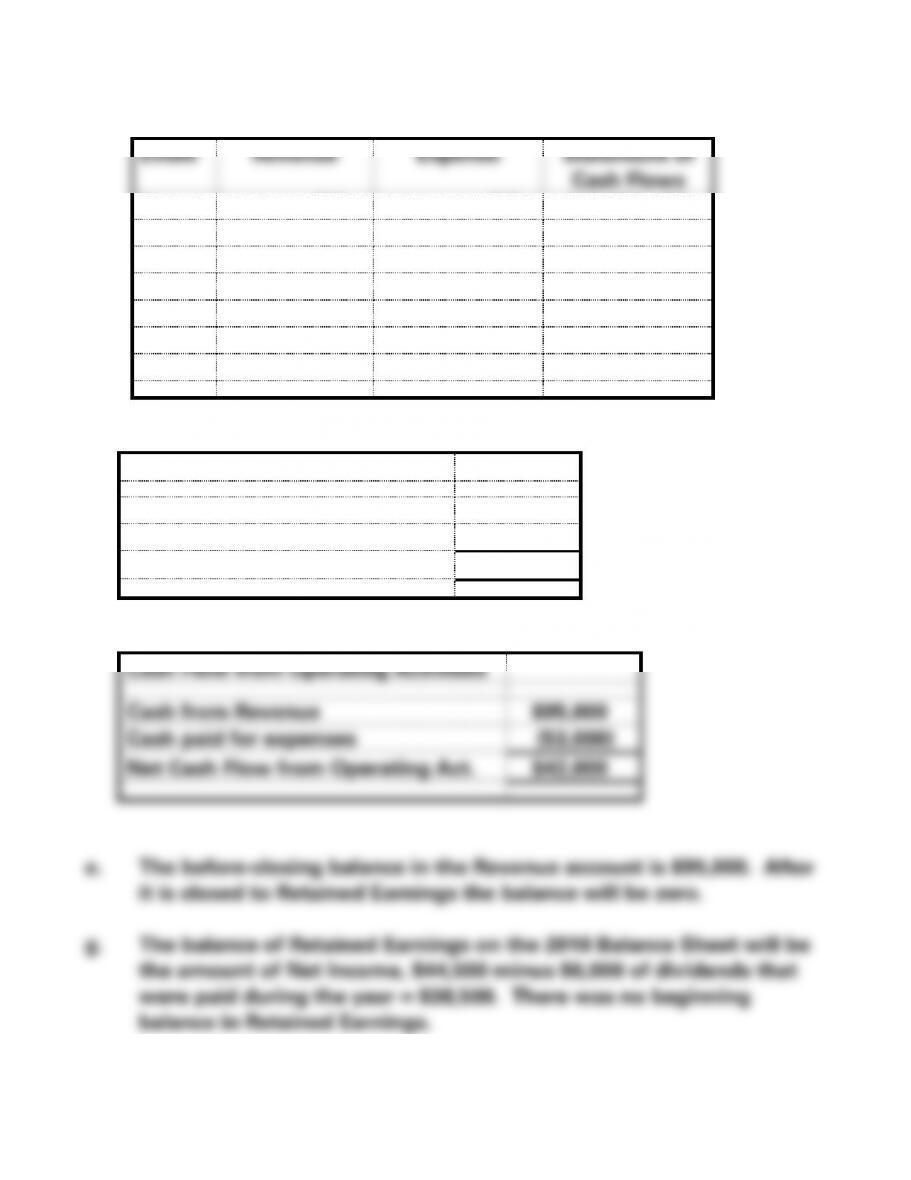

b.

Computation of Net Income

Revenue

$101,000

Less: Expenses

(56,500)

Net Income

$44,500

d.

Cash Flow from Operating Activities

Cash from Revenue

$95,000

Cash paid for expenses

(53,000)

Net Cash Flow from Operating Act.

$42,000

2-27

EXERCISE 2-7A

Lee, Inc.

Effect of Events on the General Ledger Accounts

Assets

=

Liabilities

+

Stockholders’ Equity

Event

Cash

Accounts

Receivable

Land

=

Accounts

Payable

+

Com.

Stock

+

Retained

Earnings

1. Sales on

Account

62,000

62,000

2. Coll.

Accts. Rec.

51,000

(51,000)

3. Incurred

Expense

39,000

(39,000)

4. Pd. Acc.

Pay.

(31,000)

(31,000)

5. Issue of

Stock

40,000

40,000

6. Purchase

Land

(21,000)

21,000

Totals

39,000

11,000

21,000

=

8,000

+

40,000

+

23,000

a. Revenue recognized, $62,000.

2-28

2-29

EXERCISE 2-8A

a. Retained Earnings is a permanent account, meaning that one period’s

ending balance becomes the next period’s beginning balance. Since

the December 31, 2016 balance is $42,100, this was also the balance on

January 1, 2017.

EXERCISE 2-9A

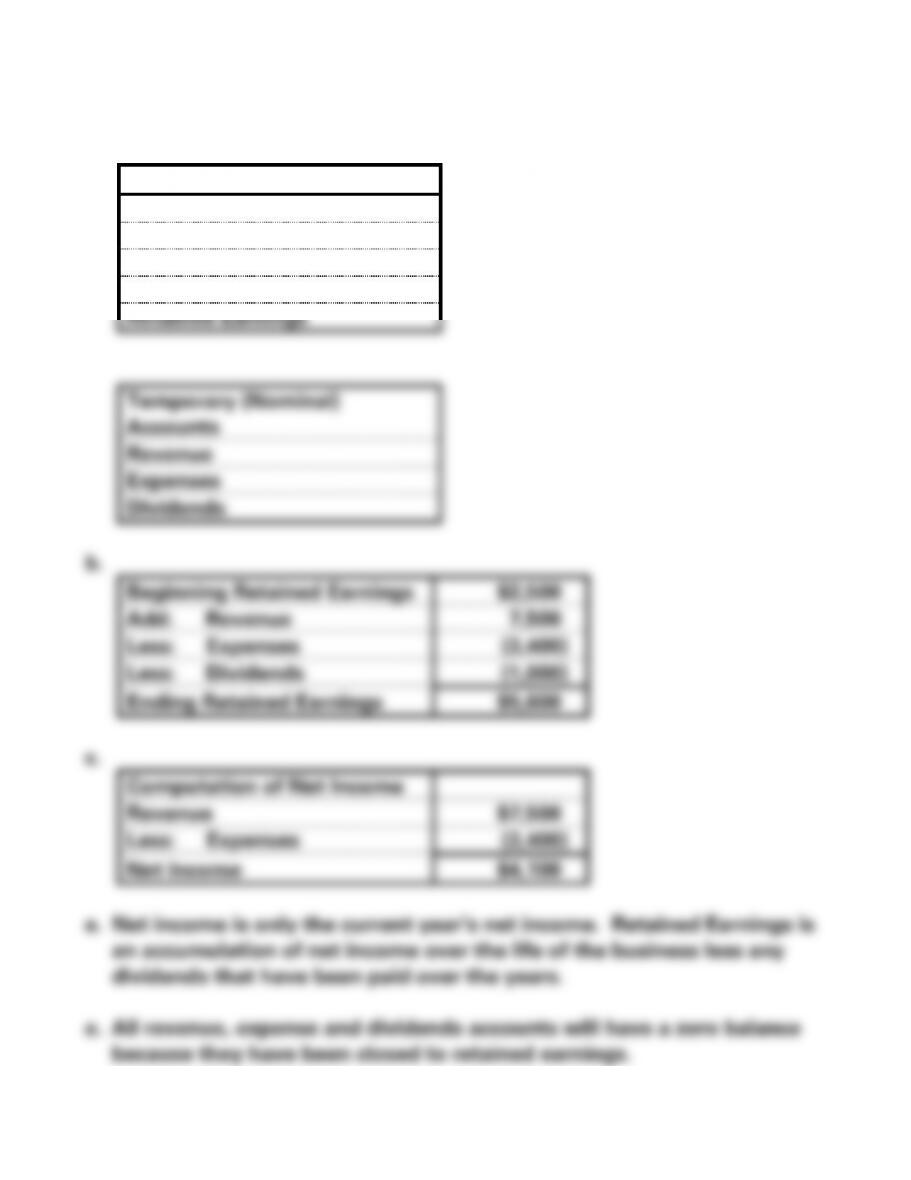

a.

Permanent Accounts

Cash

Notes Payable

Land

Common Stock

Retained Earnings

Accounts

Revenue

Expenses

Dividends

Beginning Retained Earnings

Add: Revenue

Less: Expenses

Less: Dividends

Ending Retained Earnings

Computation of Net Income

Revenue

Less: Expenses

Net Income

2-31

EXERCISE 2-10A

a.

Account

Classification

1. Other Operating Expense

T

2. Utilities Expense

T

3. Retained Earnings

P

4. Salaries Expense

T

5. Land

P

6. Dividends

T

7. Service Revenue

T

8. Cash

P

9. Salaries Payable

P

10. Common Stock

P

b. The four stages of the accounting cycle are:

recording transactions

adjusting the accounts