5-46

PROBLEM 5-18A (cont.)

b. (3) Weighted Average

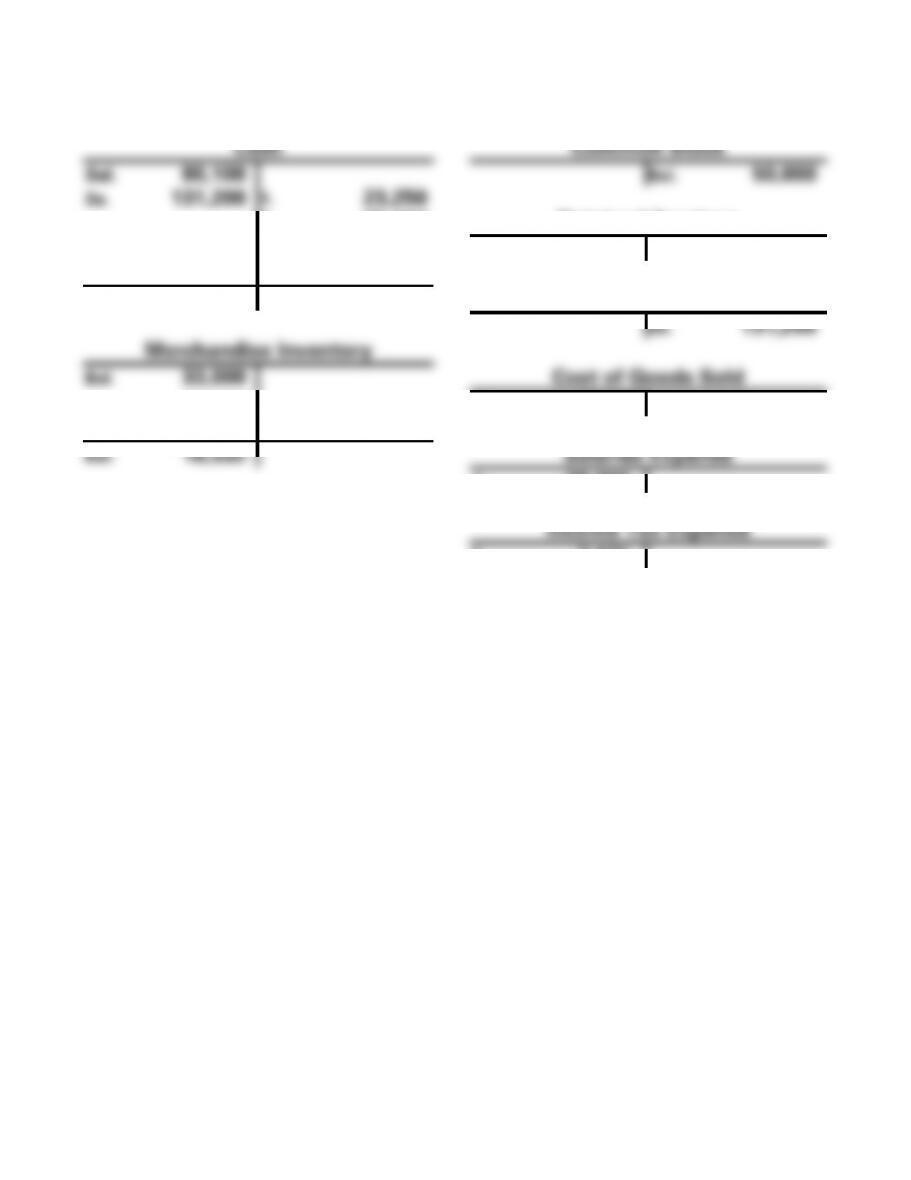

Cash

Common Stock

Bal. 80,100

Bal. 50,000

3a. 131,200

1. 23,250

2. 25,600

Retained Earnings

4. 38,000

Bal. 63,100

5. 7,471

Bal. 116,979

Sales Revenue

3a. 131,200

Merchandise Inventory

Bal. 33,000

Cost of Goods Sold

1. 23,250

3b. 63,318

2. 25,600

3b. 63,318

Bal. 18,532

Salaries Expense

4. 38,000

Income Tax Expense

5. 7,471

5-47

PROBLEM 5-18A (cont.)

c.

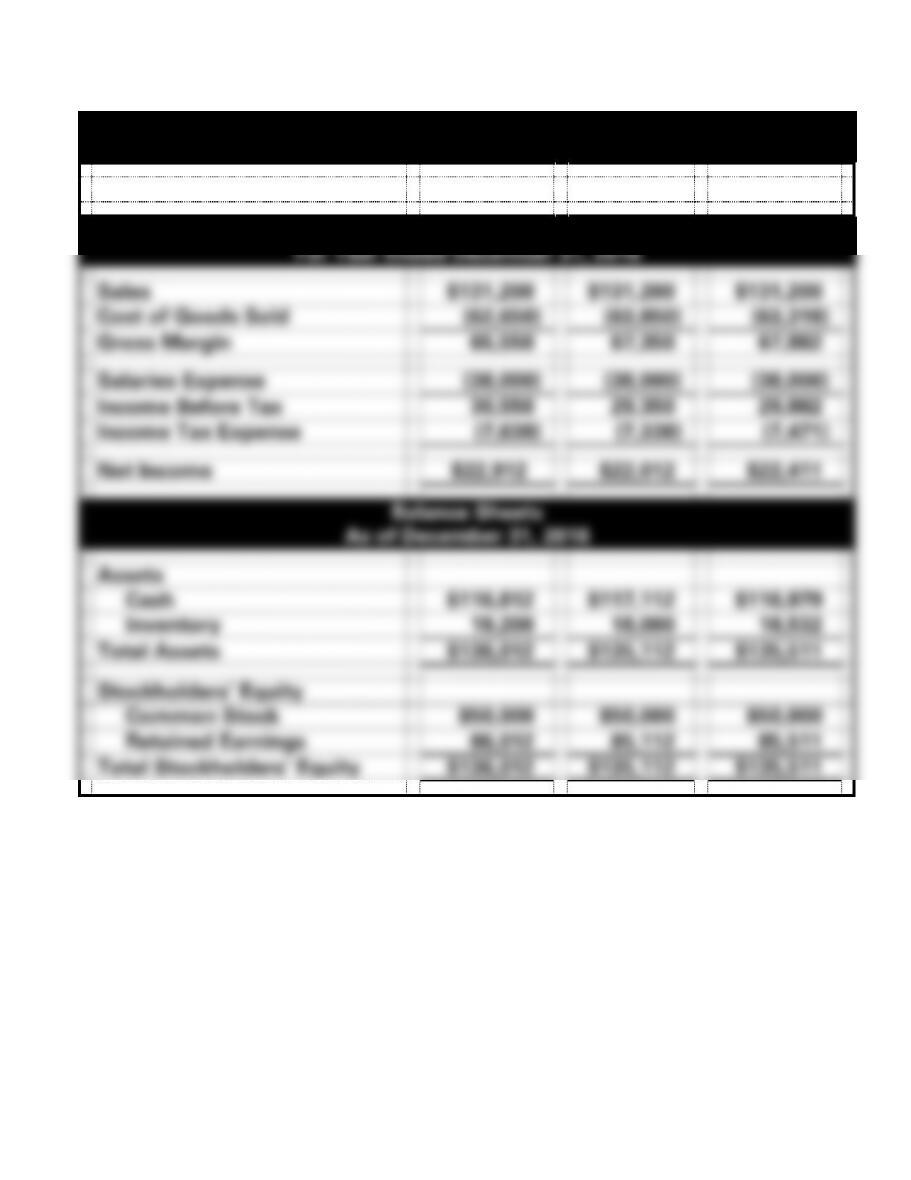

Wall’s China Shop

Financial Statements

FIFO

LIFO

Weight. Av.

Income Statements

For Year Ended December 31, 2016

Sales

$131,200

$131,200

$131,200

Cost of Goods Sold

(62,650)

(63,850)

(63,318)

Gross Margin

65,550

67,350

67,882

Salaries Expense

(38,000)

(38,000)

(38,000)

Income Before Tax

30,550

29,350

29,882

Income Tax Expense

(7,638)

(7,338)

(7,471)

Net Income

$22,912

$22,012

$22,411

Balance Sheets

As of December 31, 2016

Assets

Cash

$116,812

$117,112

$116,979

Inventory

19,200

18,000

18,532

Total Assets

$136,012

$135,112

$135,511

Stockholders’ Equity

Common Stock

$50,000

$50,000

$50,000

Retained Earnings

86,012

85,112

85,511

Total Stockholders’ Equity

$136,012

$135,112

$135,511

5-48

PROBLEM 5-18A c. (cont.)

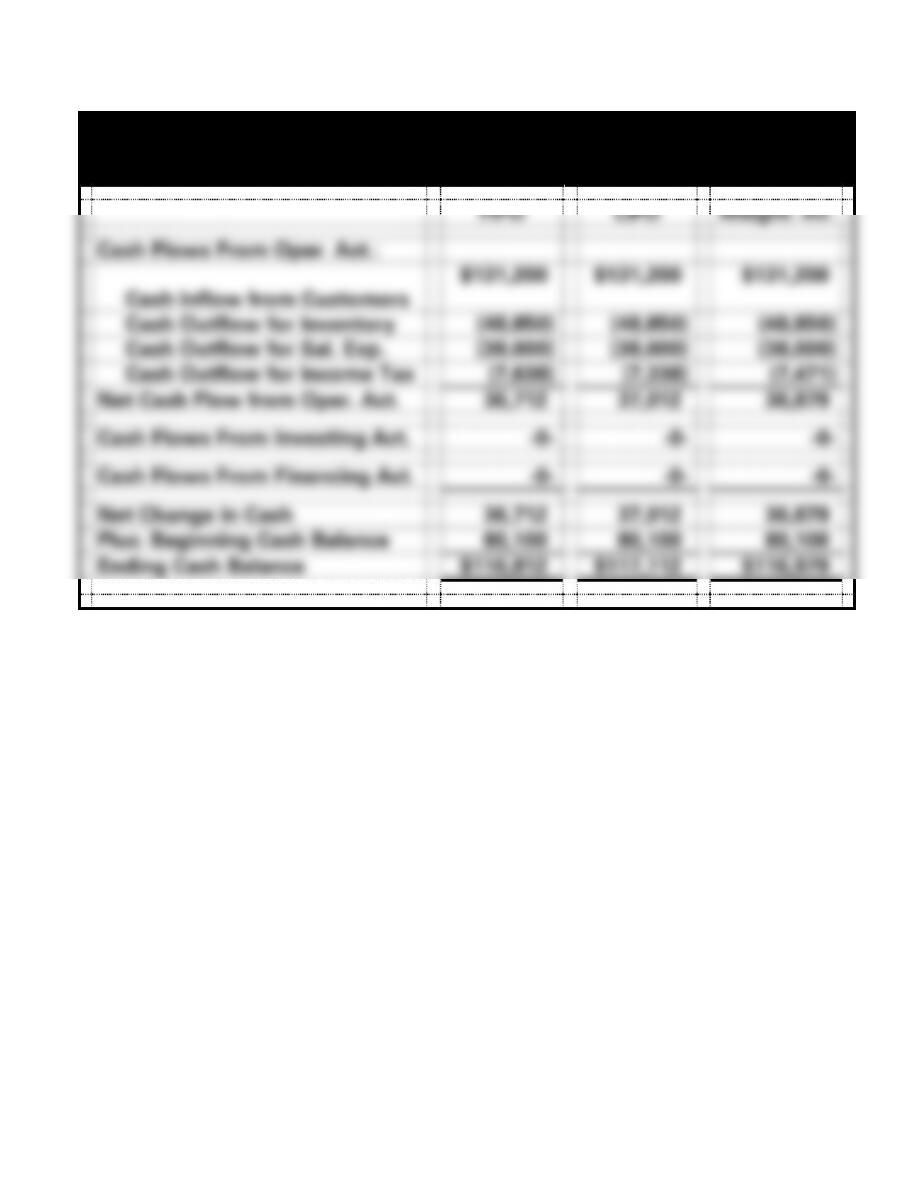

Wall’s China Shop

Statements of Cash Flows

For the Year Ended December 31, 2016

FIFO

LIFO

Weight. Av.

Cash Flows From Oper. Act.:

Cash Inflow from Customers

$131,200

$131,200

$131,200

Cash Outflow for Inventory

(48,850)

(48,850)

(48,850)

Cash Outflow for Sal. Exp.

(38,000)

(38,000)

(38,000)

Cash Outflow for Income Tax

(7,638)

(7,338)

(7,471)

Net Cash Flow from Oper. Act.

36,712

37,012

36,879

Cash Flows From Investing Act.

-0-

-0-

-0-

Cash Flows From Financing Act.

-0-

-0-

-0-

Net Change in Cash

36,712

37,012

36,879

Plus: Beginning Cash Balance

80,100

80,100

80,100

Ending Cash Balance

$116,812

$117,112

$116,979

5-49

PROBLEM 5-19A

Provided for the use of the instructor:

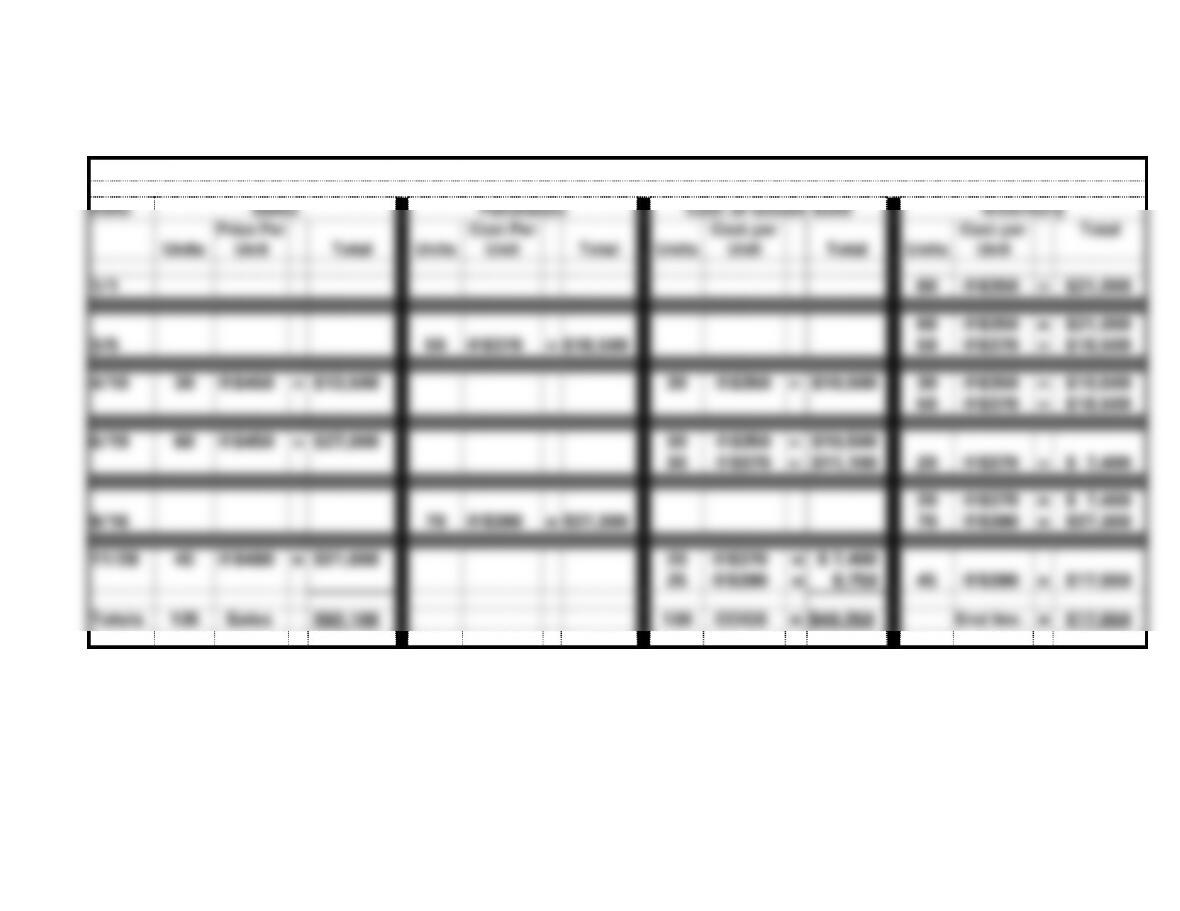

Pam’s Creations

Sales and Purchase Transactions for 2016

Date

Sales

Purchases

Cost of Goods Sold

Inventory

Units

Price Per

Unit

Total

Units

Cost Per

Unit

Total

Units

Cost per

Unit

Total

Units

Cost per

Unit

Total

1/1

60

@$350

=

$21,000

3/5

50

@$370

=

$18,500

60

50

@$350

@$370

=

=

$21,000

$18,500

4/10

30

@$450

=

$13,500

30

@$350

=

$10,500

30

50

@$350

@$370

=

=

$10,500

$18,500

6/19

60

@$450

=

$27,000

30

30

@$350

@$370

=

=

$10,500

$11,100

20

@$370

=

$ 7,400

9/16

70

@$390

=

$27,300

20

70

@$370

@$390

=

=

$ 7,400

$27,300

11/28

45

@$480

=

$21,600

20

25

@$370

@$390

=

=

$ 7,400

9,750

45

@$390

=

$17,550

Totals

135

Sales

$62,100

130

COGS

=

$49,250

End Inv.

=

$17,550

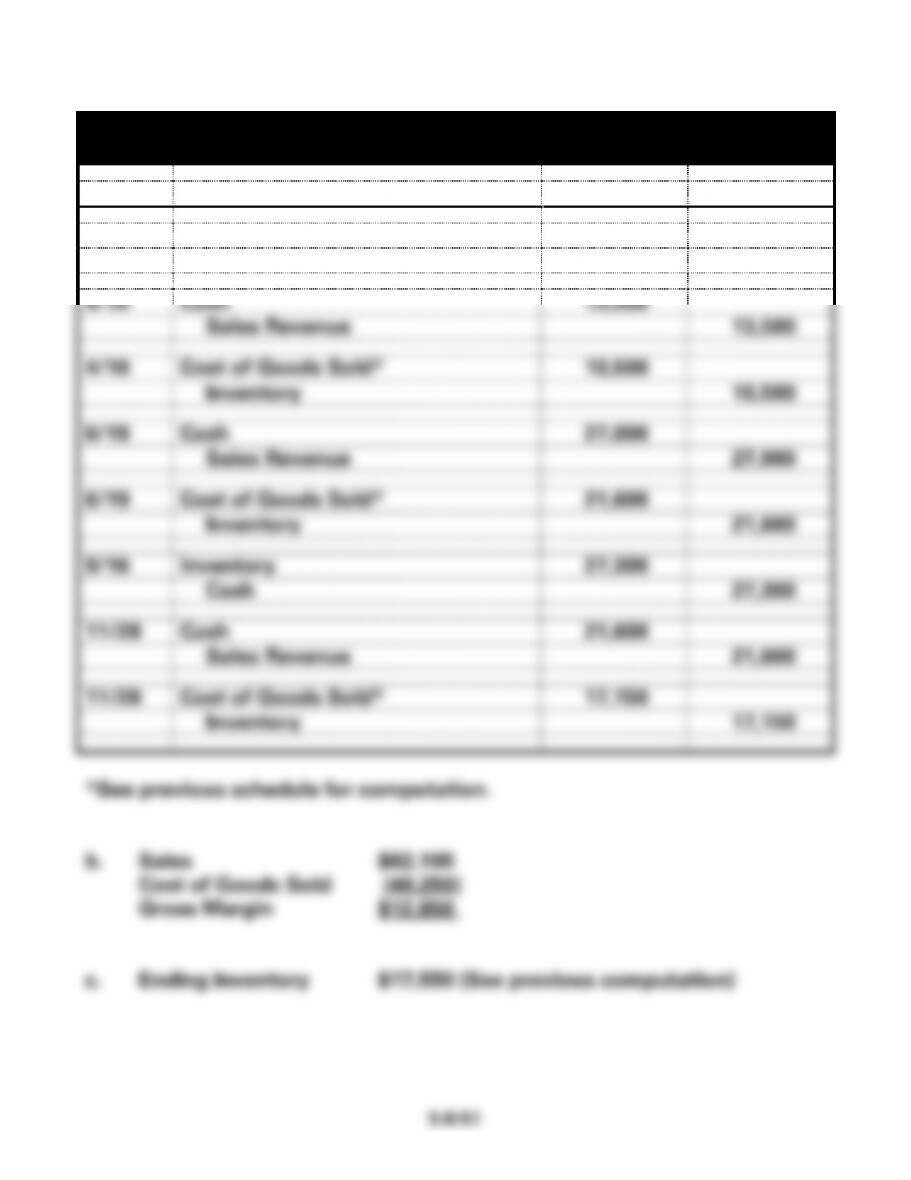

PROBLEM 5-19A (cont.)

a.

Pam’s Creations

General Journal, 2016

Date

Account Titles

Debit

Credit

3/5

Inventory

18,500

Cash

18,500

4/10

Cash

13,500

Sales Revenue

13,500

4/10

Cost of Goods Sold*

10,500

Inventory

10,500

6/19

Cash

27,000

Sales Revenue

27,000

6/19

Cost of Goods Sold*

21,600

Inventory

21,600

9/16

Inventory

27,300

Cash

27,300

11/28

Cash

21,600

Sales Revenue

21,600

11/28

Cost of Goods Sold*

17,150

Inventory

17,150

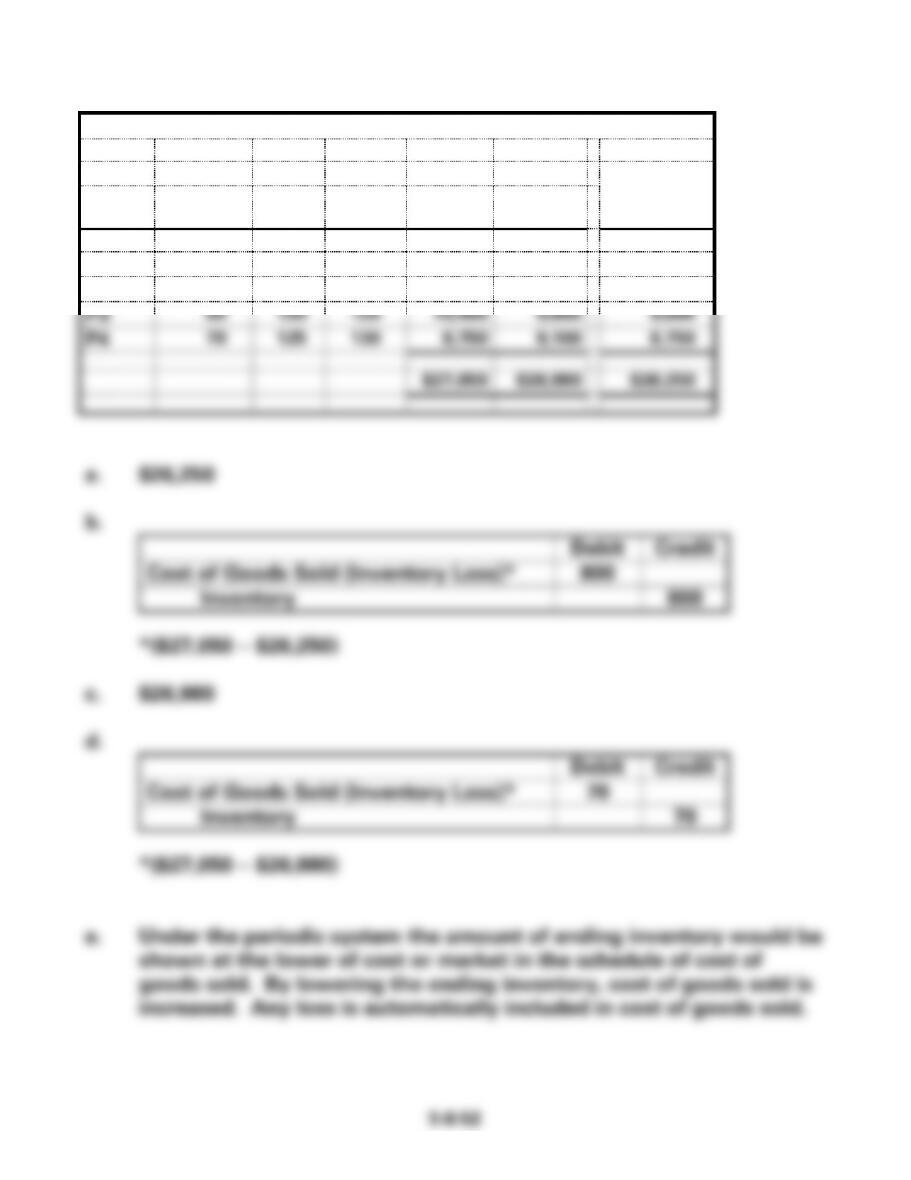

PROBLEM 5-20A

Randy’s Parts Co.

Ind. Item

Item

Quantity

Unit

Cost

Unit

Market

Total

Cost

Total

Market

Lower of

Cost/Mkt.

P1

60

$85

$90

$ 5,100

$ 5,400

$ 5,100

P2

40

70

72

2,800

2,880

2,800

P3

80

130

120

10,400

9,600

9,600

P4

70

125

130

8,750

9,100

8,750

$27,050

$26,980

$26,250

a. $26,250

b.

Debit

Credit

Cost of Goods Sold (Inventory Loss)*

800

Inventory

800

*($27,050 − $26,250)

c. $26,980

d.

Debit

Credit

Cost of Goods Sold (Inventory Loss)*

70

Inventory

70

*($27,050 − $26,980)

e. Under the periodic system the amount of ending inventory would be

shown at the lower of cost or market in the schedule of cost of

goods sold. By lowering the ending inventory, cost of goods sold is

increased. Any loss is automatically included in cost of goods sold.

PROBLEM 5-21A

Don’s Grocery

a. (1) Estimated Gross Margin:

Sales x Gross Margin %: $1,100,000 x .30 = $330,000

(2) Estimated Cost of Goods Sold:

PROBLEM 5-22A

Toyland

2016

2017

Total

Net Sales

$150,000

$190,000

$340,000

Cost of Goods Sold

(76,000)

(89,200)

(165,200)

Gross Margin

$ 74,000

$100,800

$174,800

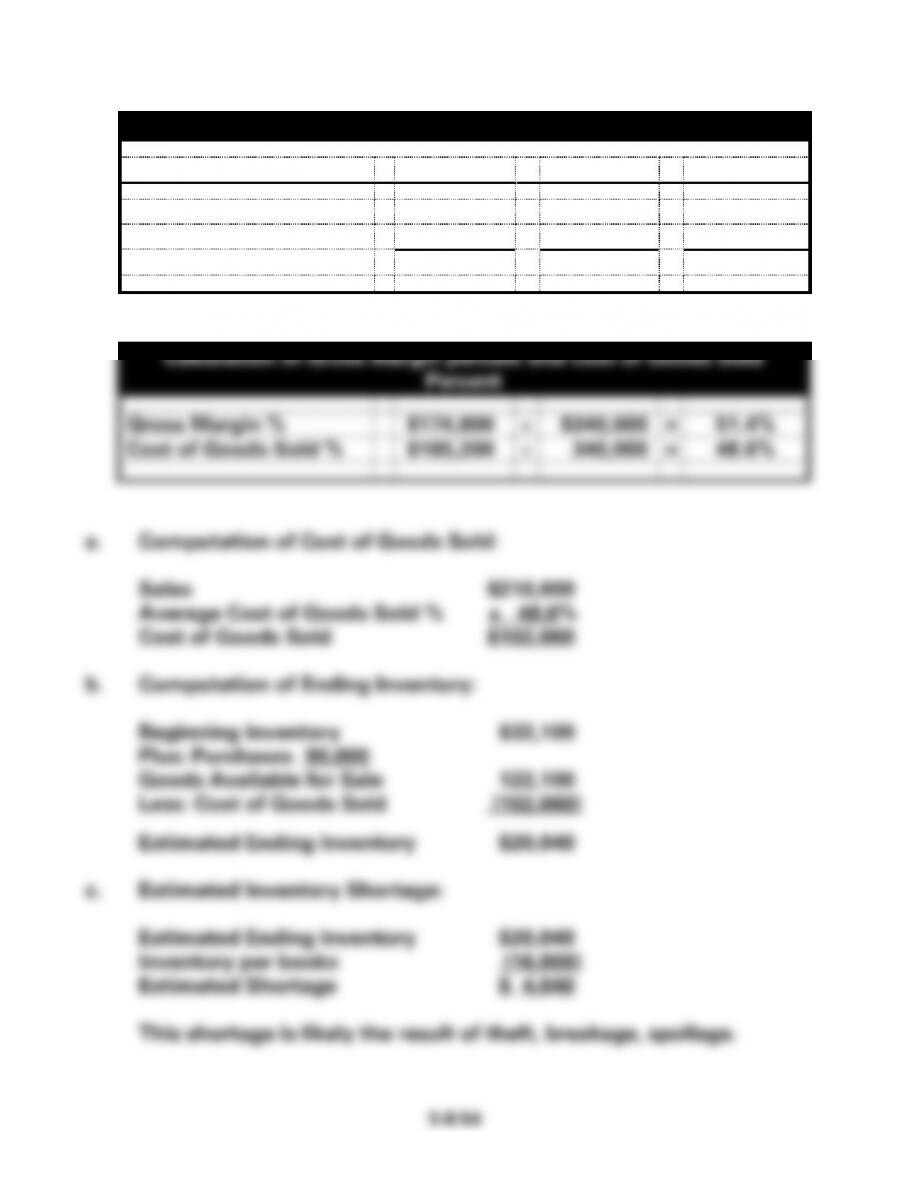

Calculation of Gross Margin percent and Cost of Goods Sold

Percent

Gross Margin %

$174,800

$340,000

=

51.4%

Cost of Goods Sold %

$165,200

340,000

=

48.6%

a. Computation of Cost of Goods Sold:

Sales $210,000

Average Cost of Goods Sold % x 48.6%

Cost of Goods Sold $102,060

b. Computation of Ending Inventory:

Beginning Inventory $32,100

Plus: Purchases 90,000

Goods Available for Sale 122,100

Less: Cost of Goods Sold (102,060)

Estimated Ending Inventory $20,040

c. Estimated Inventory Shortage:

Estimated Ending Inventory $20,040

Inventory per books (16,000)

Estimated Shortage $ 4,040

This shortage is likely the result of theft, breakage, spoilage.

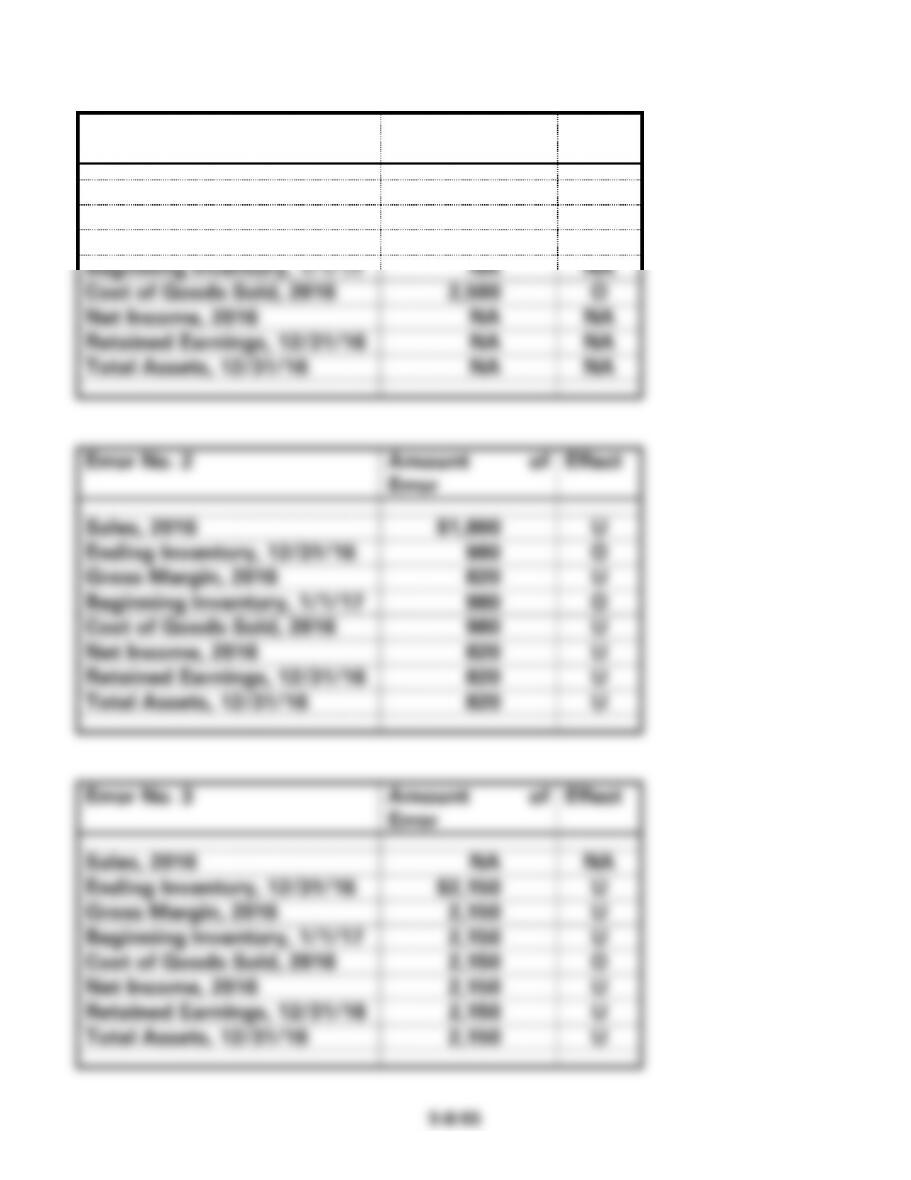

PROBLEM 5-23A

Error No.1

Amount of

Error

Effect

Sales, 2016

NA

NA

Ending Inventory, 12/31/16

NA

NA

Gross Margin, 2016

$2,500

U

Beginning Inventory, 1/1/17

NA

NA

Cost of Goods Sold, 2016

2,500

O

Net Income, 2016

NA

NA

Retained Earnings, 12/31/16

NA

NA

Total Assets, 12/31/16

NA

NA

Error No. 2

Amount of

Error

Effect

Sales, 2016

$1,800

U

Ending Inventory, 12/31/16

980

O

Gross Margin, 2016

820

U

Beginning Inventory, 1/1/17

980

O

Cost of Goods Sold, 2016

980

U

Net Income, 2016

820

U

Retained Earnings, 12/31/16

820

U

Total Assets, 12/31/16

820

U

Error No. 3

Amount of

Error

Effect

Sales, 2016

NA

NA

Ending Inventory, 12/31/16

$2,150

U

Gross Margin, 2016

2,150

U

Beginning Inventory, 1/1/17

2,150

U

Cost of Goods Sold, 2016

2,150

O

Net Income, 2016

2,150

U

Retained Earnings, 12/31/16

2,150

U

Total Assets, 12/31/16

2,150

U

PROBLEM 5-24A

a. First the company’s gross margins must be calculated:

Phoenix

Roswell

Sales

$2,400,000

$2,400,000

Cost of Goods Sold

(1,440,000)

(1,510,000)

Gross Margin

$ 960,000

$ 890,000

Phoenix appears to incur the higher costs to finance inventory

because it takes a longer time to sell its inventory.

c. Other things being equal, this would indicate a company sells its

product at a lower price. The lower the price, the more quickly

goods should sell. “Other things” are not equal in this problem.

5-II–57

A. ATC 5-1 (All dollar amounts are in millions.)

a. Inventory turnover:

2013 $51,160 ÷ $8,766 = 5.8 times

2012 $50,568 ÷ $7,903 = 6.4 times

Average days to sell inventory:

2013 365 days ÷ 5.8 = 63 days

ATC 5-2

a.

Blue Bird Co.

Inventory Purchases

Beginning Inventory

100

@

$50

=

$ 5,000

70

@

55

=

3,850

First Purchase

100

@

54

=

5,400

Second Purchase

250

@

58

=

14,500

Total

520

$28,750

From Beginning Inventory

@

=

From Beginning Inventory

@

=

From First Purchase

@

=

From Second Purchase

@

=

Total

$22,950

From Second Purchase

@

=

$14,500

From First Purchase

@

=

@

=

Total

$23,750

ATC 5-2 a. (cont.)

Weighted Average

Total Cost

Total Units

=

Cost per Unit

$28,750

520

=

$55.288

Cost of Goods Sold

420 units

@

$55.288

=

$23,221

Ending Inventory

100 units

@

$55.288

=

$5,529

Blue Bird Company

Income Statements

FIFO

LIFO

Weighted

Average

Sales (220 @$80; 200 @ $90)

$35,600

$35,600

$35,600

Cost of Goods Sold

(22,950)

(23,750)

(23,221)

Gross Margin

12,650

11,850

12,379

Operating Expenses

(3,200)

(3,200)

(3,200)

Income Before Tax

9,450

8,650

9,179

Income Tax (30%)

(2,835)

(2,595)

(2,754)

Net Income

$ 6,615

$ 6,055

$ 6,425

ATC 5-3

All dollar amounts are in millions.

a.

2013 2012

Gross margin $ 895.9 $ 828.3

÷ Sales $11,858.7 $ 10,453.8

= Gross margin percentage 7.55% 7.92%

ATC 5-4

Dollars are in millions.

a. Inventory turnover:

2013: $26,645.1 ÷ $2,089.6 = 12.75 times

2012: $32,486.5 ÷ $2,562.0 = 12.68 times

5-II–62

II. ATC 5-5

a. One would expect a restaurant, which sells low cost, perishable goods, to sell its

inventory faster than a company that sells expensive, nonperishable goods, such as

diamonds.

b. Inventory turnover:

Ruby Tuesday’s: $341,512 ÷ $ 21,779 = 15.68 times

Zale Corporation: $903,602 ÷ $767,540 = 1.18 times

c. Average days to sell inventory:

Ruby Tuesday’s: 365 days ÷ 15.68 = 23 days

Zale Corporation: 365 days ÷ 1.18 = 309 days

d. Definitely!

ATC 5-6

a. Using FIFO, the cost of goods sold for Leno Company would be

$289,000 ($535,000 − $246,000). If Leno Company switches to

LIFO, the cost of goods sold would increase to $360,000

5-II–64

ATC 5-7

a. When the LIFO method is used for tax purposes, tax law requires

companies to use the same cost flow method for financial

reporting. Consequently, if the company uses LIFO for tax

purposes, then it is legally bound to use the same method in

its financial statements. Accordingly, it would be illegal for

inflationary economy, the first inventory purchased, which

would be the lower cost inventory, would be the first inventory

expensed when goods are sold under FIFO. This would leave the

higher cost inventory in ending inventory which is the cost

that would appear on the balance sheet.

financial statements. Additionally, the LIFO reserve amount

would be disclosed in the notes to the financial statements and

the stockholders could make their own judgments about how the

statements would appear if FIFO had been used.

III. ATC 5-8

SOLUTIONS TO EXERCISES – SERIES B – CHAPTER 5

EXERCISE 5-1B

a. FIFO

b. FIFO

c. FIFO