3-1–5

PROBLEM 3-33B g. (cont.)

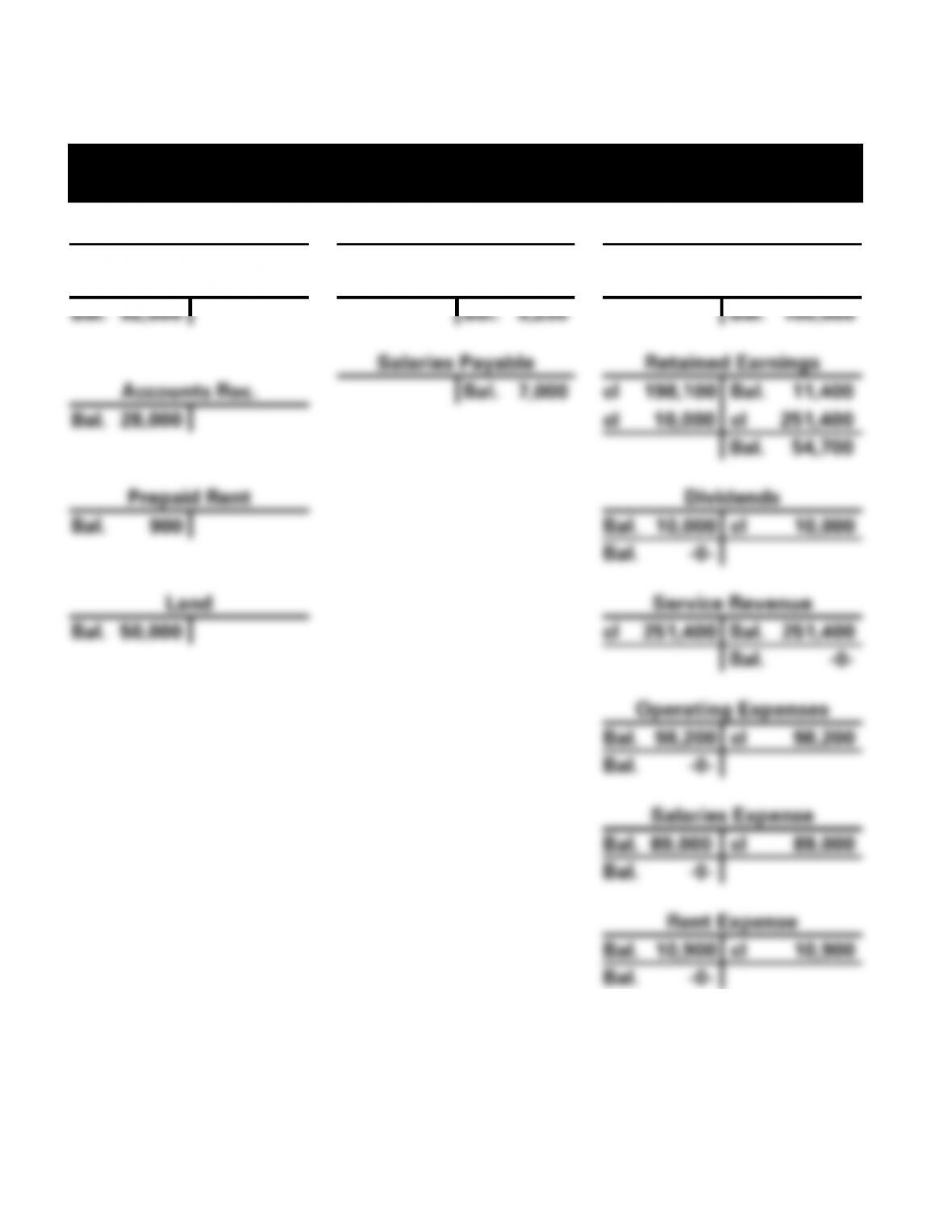

Anchor Machining

T-Accounts for Closing Entries, 2017

Assets

=

Liabilities

+

Stockholders’ Equity

Cash

Accounts Payable

Common Stock

Bal. 92,000

Bal. 9,200

Bal. 100,000

Salaries Payable

Retained Earnings

Accounts Rec.

Bal. 7,000

cl 198,100

Bal. 11,400

Bal. 28,000

cl 10,000

cl 251,400

Bal. 54,700

Prepaid Rent

Dividends

Bal. 900

Bal. 10,000

cl 10,000

Bal. -0-

Land

Service Revenue

Bal. 50,000

cl 251,400

Bal. 251,400

Bal. -0-

Operating Expenses

Bal. 98,200

cl 98,200

Bal. -0-

Salaries Expense

Bal. 89,000

cl 89,000

Bal. -0-

Rent Expense

Bal. 10,900

cl 10,900

Bal. -0-

3-1–6

PROBLEM 3-33B g. (cont.)

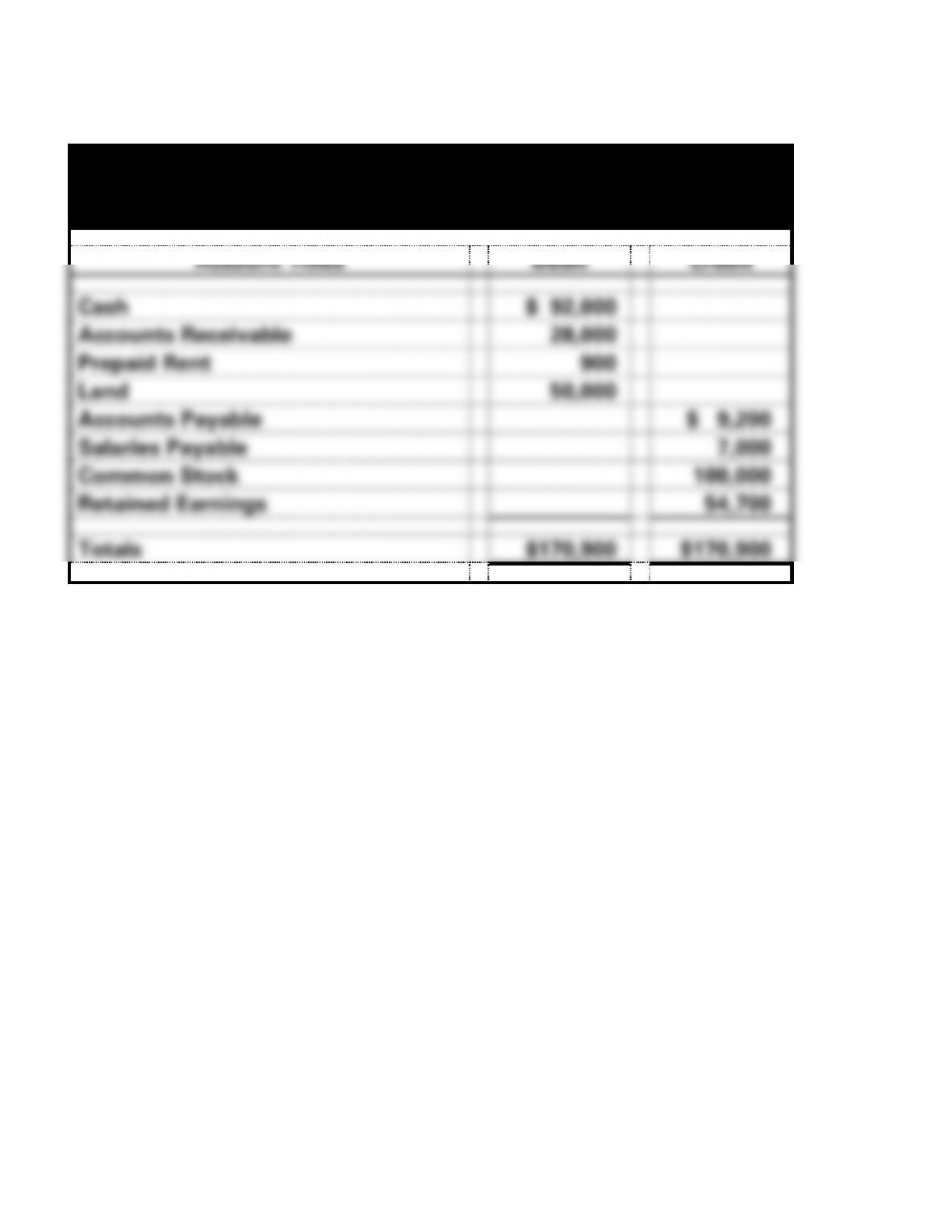

Anchor Machining

Post-Closing Trial Balance

December 31, 2017

Account Titles

Debit

Credit

Cash

$ 92,000

Accounts Receivable

28,000

Prepaid Rent

900

Land

50,000

Accounts Payable

$ 9,200

Salaries Payable

7,000

Common Stock

100,000

Retained Earnings

54,700

Totals

$170,900

$170,900

3-1–7

PROBLEM 3-34B

a. Debt to Assets Ratio: Total debt ÷ Total assets

Delaware $ 93,000 ÷ $127,000 = 73.2%

Florida $452,000 ÷ $753,000 = 60.0%

3-1–8

PROBLEM 3-35B

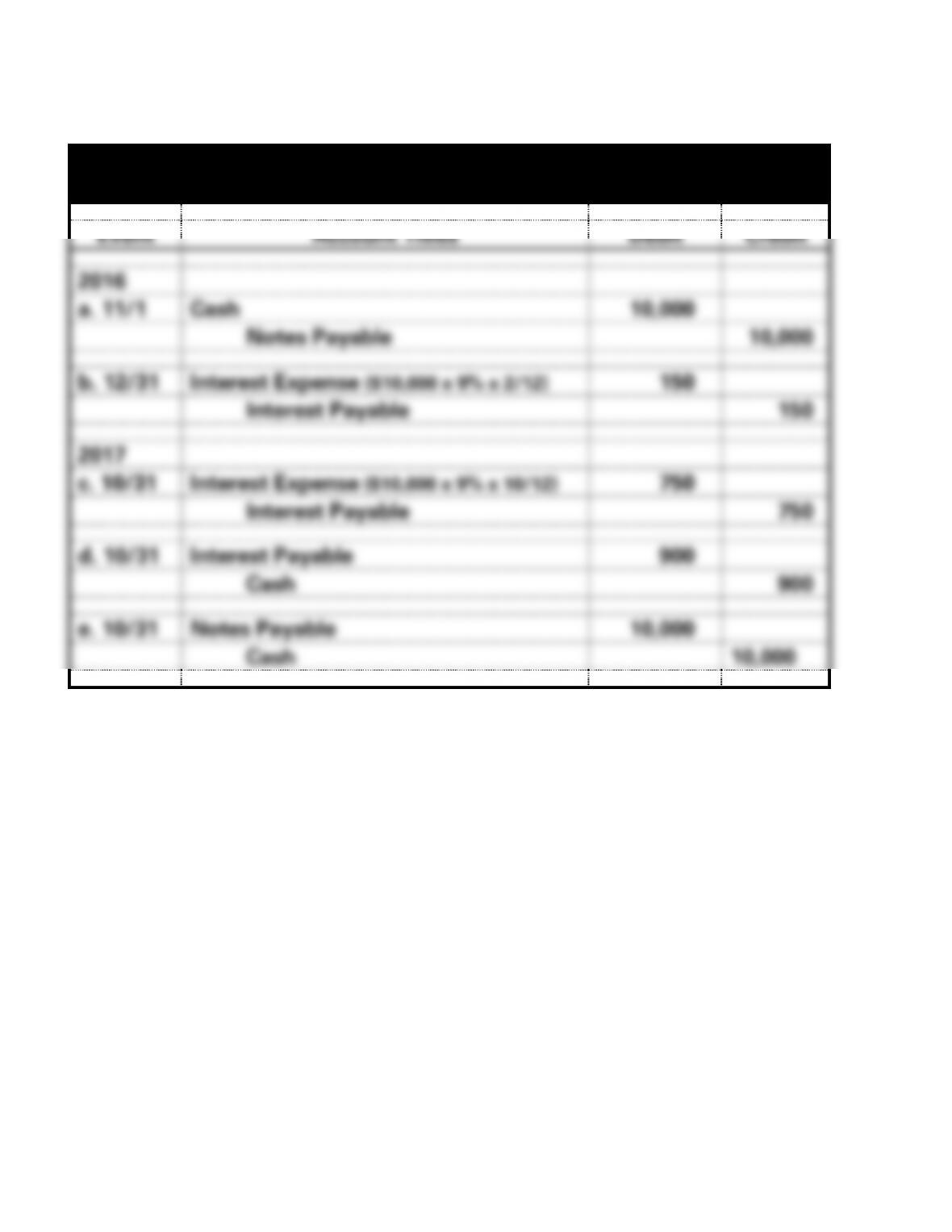

Black, Inc.

General Journal

Event

Account Titles

Debit

Credit

2016

a. 11/1

Cash

10,000

Notes Payable

10,000

b. 12/31

Interest Expense ($10,000 x 9% x 2/12)

150

Interest Payable

150

2017

c. 10/31

Interest Expense ($10,000 x 9% x 10/12)

750

Interest Payable

750

d. 10/31

Interest Payable

900

Cash

900

e. 10/31

Notes Payable

10,000

Cash

10,000

3-1–9

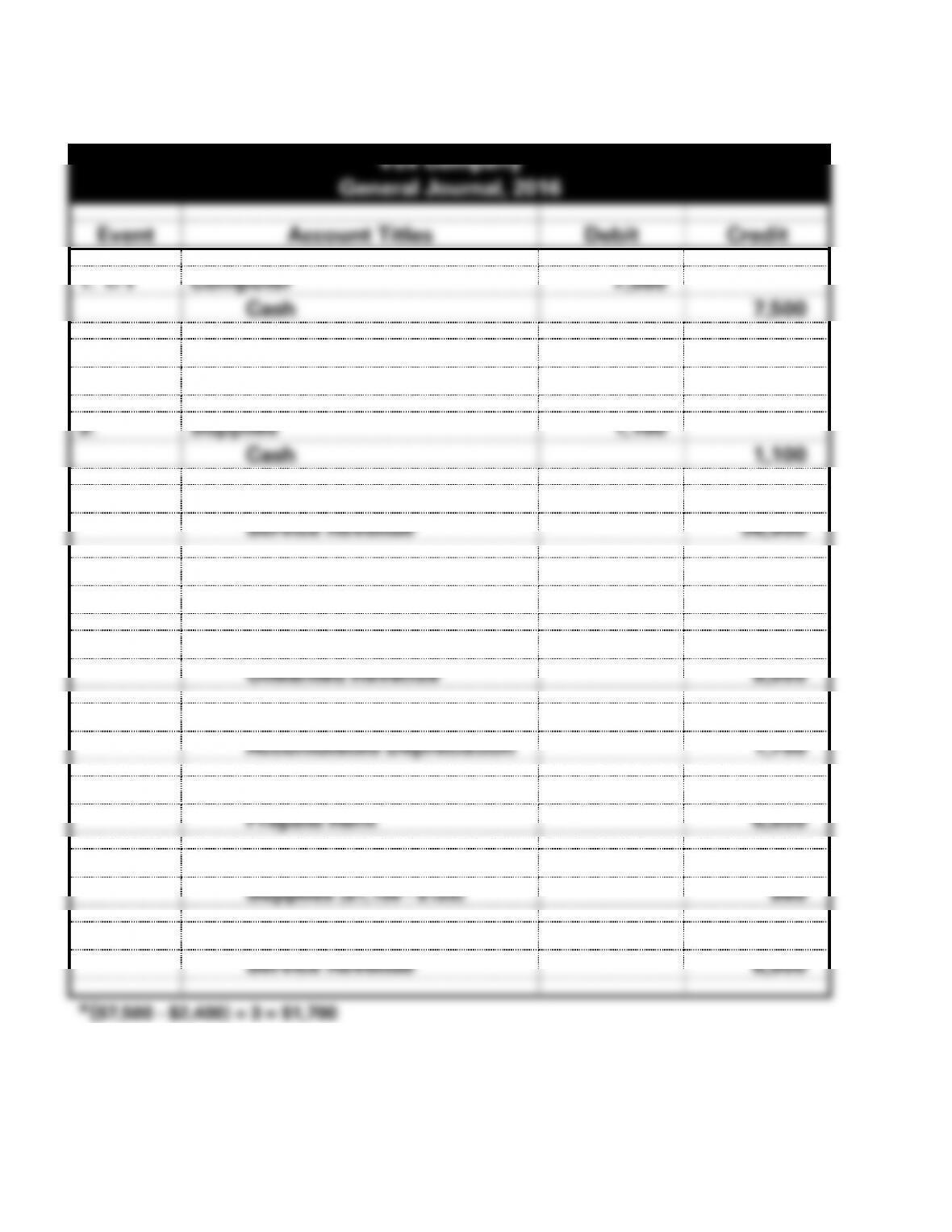

PROBLEM 3-36B

Vox Company

General Journal, 2016

Event

Account Titles

Debit

Credit

1. 1/1

Computer

7,500

Cash

7,500

2. 2/1

Prepaid Rent

6,600

Cash

6,600

3.

Supplies

1,100

Cash

1,100

4.

Cash

56,000

Service Revenue

56,000

5.

Salaries Expense

18,000

Cash

18,000

6. 5/1

Cash

9,000

Unearned Revenue

9,000

7.

Depreciation Expense*

1,700

Accumulated Depreciation

1,700

8.

Rent Expense ($6,600 x 11/12)

6,050

Prepaid Rent

6,050

9.

Supplies Expense

980

Supplies ($1,100 – $120)

980

10.

Unearned Revenue ($9,000 x 8/12)

6,000

Service Revenue

6,000

3-1–10

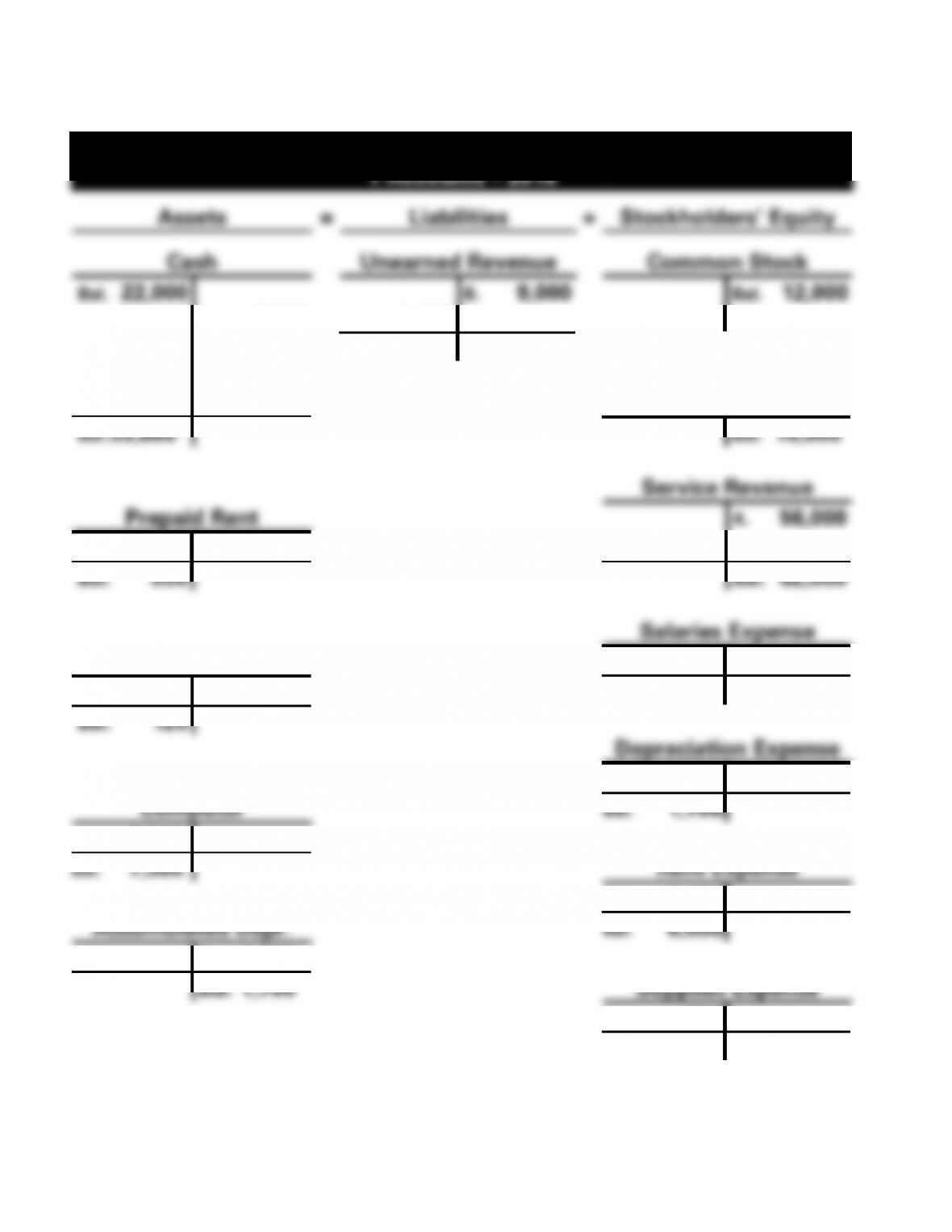

PROBLEM 3-36B a. (cont.)

Vox Company

T-Accounts – 2016

Assets

=

Liabilities

+

Stockholders’ Equity

Cash

Unearned Revenue

Common Stock

Bal. 22,000

6. 9,000

Bal. 12,000

4. 56,000

1. 7,500

10. 6,000

6. 9,000

2. 6,600

Bal. 3,000

3. 1,100

5. 18,000

Retained Earnings

Bal. 53,800

Bal. 10,000

Service Revenue

Prepaid Rent

4. 56,000

2. 6,600

8. 6,050

10. 6,000

Bal. 550

Bal. 62,000

Salaries Expense

Supplies

5. 18,000

3. 1,100

9. 980

Bal. 18,000

Bal. 120

Depreciation Expense

7. 1,700

Computer

Bal. 1,700

1. 7,500

Bal. 7,500

Rent Expense

81. 6,050

Accumulated Depr.

Bal. 6,050

7. 1,700

Bal. 1,700

Supplies Expense

9. 980

Bal. 980

3-1–11

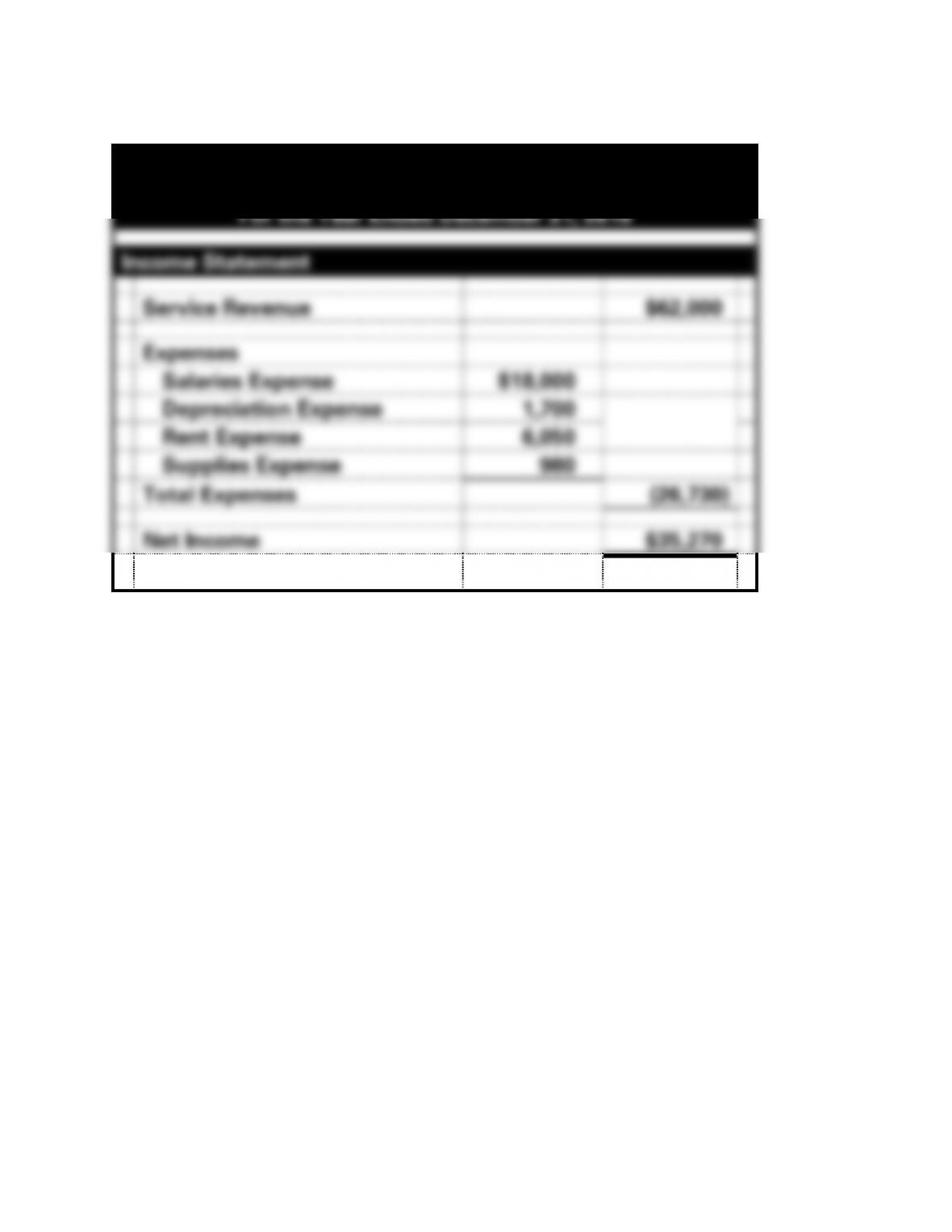

PROBLEM 3-36B b. (cont.)

Vox Company

Financial Statements

For the Year Ended December 31, 2016

Income Statement

Service Revenue

$62,000

Expenses

Salaries Expense

$18,000

Depreciation Expense

1,700

Rent Expense

6,050

Supplies Expense

980

Total Expenses

(26,730)

Net Income

$35,270

3-1–12

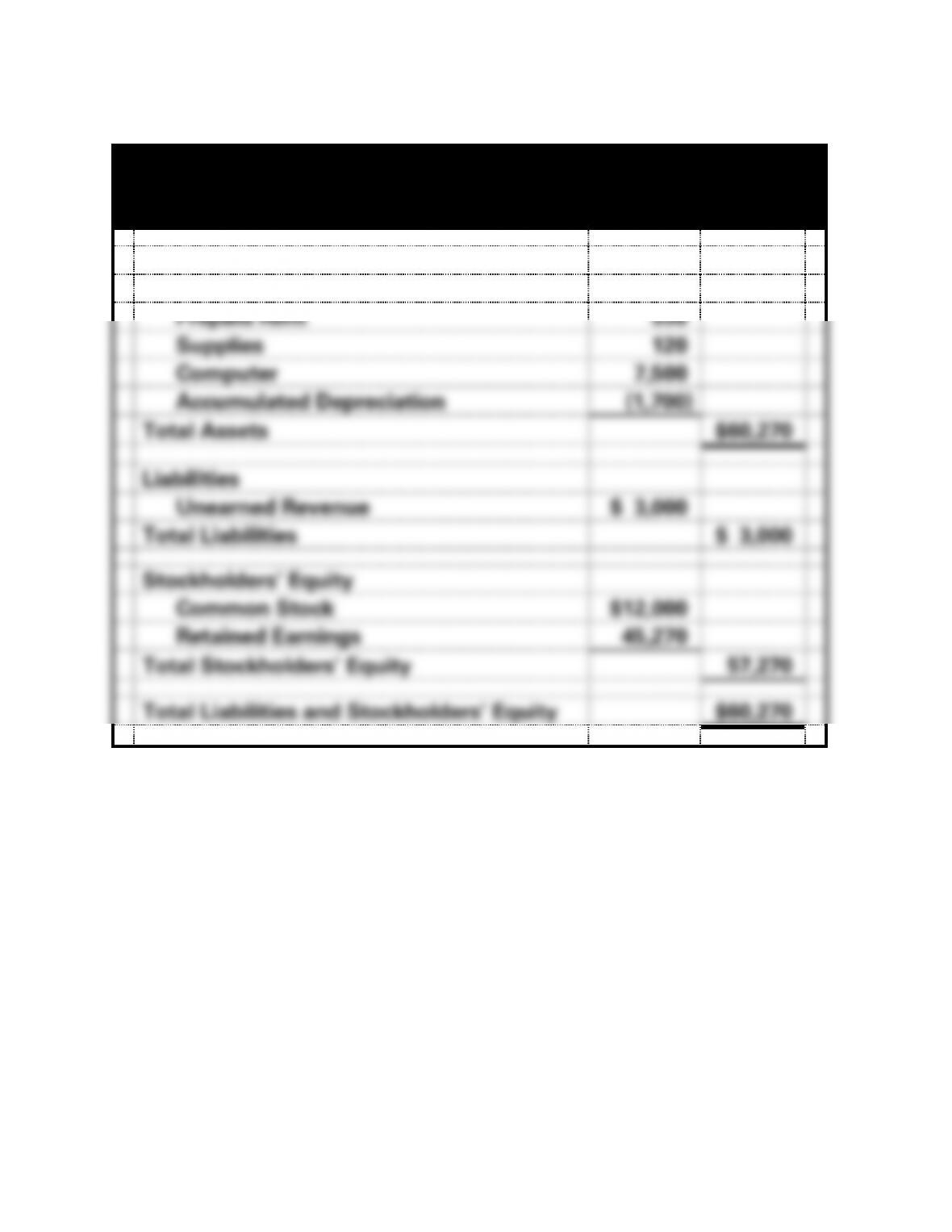

PROBLEM 3-36B b. (cont.)

Vox Company

Balance Sheet

As of December 31, 2016

Assets

Cash

$53,800

Prepaid Rent

550

Supplies

120

Computer

7,500

Accumulated Depreciation

(1,700)

Total Assets

$60,270

Liabilities

Unearned Revenue

$ 3,000

Total Liabilities

$ 3,000

Stockholders’ Equity

Common Stock

$12,000

Retained Earnings

45,270

Total Stockholders’ Equity

57,270

Total Liabilities and Stockholders’ Equity

$60,270

3-1–13

PROBLEM 3-36B b. (cont.)

Vox Company

Statement of Cash Flows

For the Year Ended December 31, 2016

Cash Flows From Operating Activities:

Received Cash from Customers1

$65,000

Paid Cash for Expenses2

(25,700)

Net Cash Flow from Operating Activities

$39,300

Cash Flows From Investing Activities

Purchased Computer

(7,500)

Net Cash Flow from Financing Activities

(7,500)

Cash Flows From Financing Activities:

-0-

Net Change in Cash

31,800

Plus: Beginning Cash Balance

22,000

Ending Cash Balance

$53,800

1(4) $56,000 + (6) $9,000 = $65,000

2(2) $6,600 + (3) $1,100 + (5) $18,000 = $25,700

3-1–14

1. The two fundamental equality requirements of the double-entry

2.

Debit

means left side of an account and

credit

means right side of an

account.

Debits Credits

3. The balance of an account is the difference between total debits and total

4. The three primary asset sources are (1) assets acquired from owners, (2)

5. The three primary asset uses are (1) assets used by a business in the

6. Some examples of assets exchange transactions include:

7. A debit to an expense account increases the expense. Since expenses

3-1–15

expense account ultimately reduces retained earnings and stockholders’

equity.

8. Debit Balance Credit Balance

Assets Liabilities

9. The ledger accounts are used to prepare financial statements. (These

10. The purpose of a journal is to maintain a chronological record of all

11. Special journals are used to record only specific types of transactions

12. The ledger is a collection of all accounts of the organization. It is the

13. Closing entries transfer the balances of the temporary (nominal)

14. A company closes its books at its accounting year-end but not all

companies end their year on December 31. Some companies choose a

15. The information recorded in the general journal includes the date,

16. The trial balance is a listing of all accounts and amounts in a

3-1–16

17. The trial balance should be prepared when there is a need to test the

18. The process of copying information from journals to ledgers is called

posting

.

19. The return on assets ratio, net income divided by total assets, is used to

20. The debt to assets ratio, total debt divided by total assets, helps to

21. Financial leverage is using borrowed money to increase stockholders’

equity.

22. Return on equity is computed by dividing net income by stockholders’

equity. When net income increases as a result of borrowing money and

3-1–17

ATC 3-1

(All dollar amounts are in millions.)

a. Debt to assets:

2013 $28,322* ÷ $44,553 = 63.6%

2012 $31,605* ÷ $48,163 = 65.6%

3-1–18

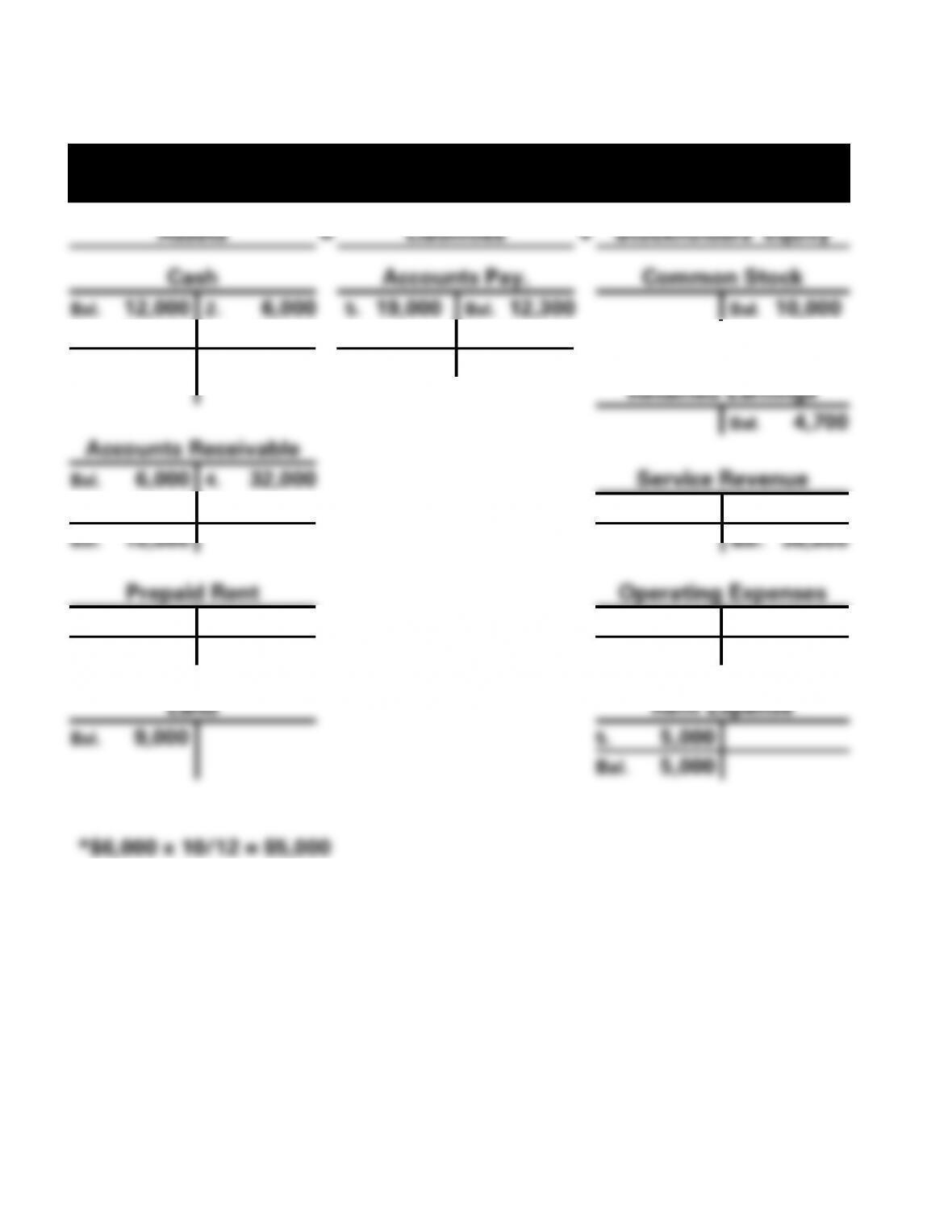

ATC 3-2

a.

Miller Company

T-Accounts, 2016

Assets

=

Liabilities

+

Stockholders’ Equity

Cash

Accounts Pay.

Common Stock

Bal. 12,000

2. 6,000

5. 19,000

Bal. 12,300

Bal. 10,000

4. 32,000

5. 19,000

3. 18,000

Bal. 19,000

Bal. 11,300

Retained Earnings

Bal. 4,700

Accounts Receivable

Bal. 6,000

4. 32,000

Service Revenue

1. 36,000

1. 36,000

Bal. 10,000

Bal. 36,000

Prepaid Rent

Operating Expenses

2. 6,000

5.* 5,000

3. 18,000

Bal. 1,000

Bal. 18,000

Land

Rent Expense

Bal. 9,000

5. 5,000

Bal. 5,000

*$6,000 x 10/12 = $5,000

3-1–19

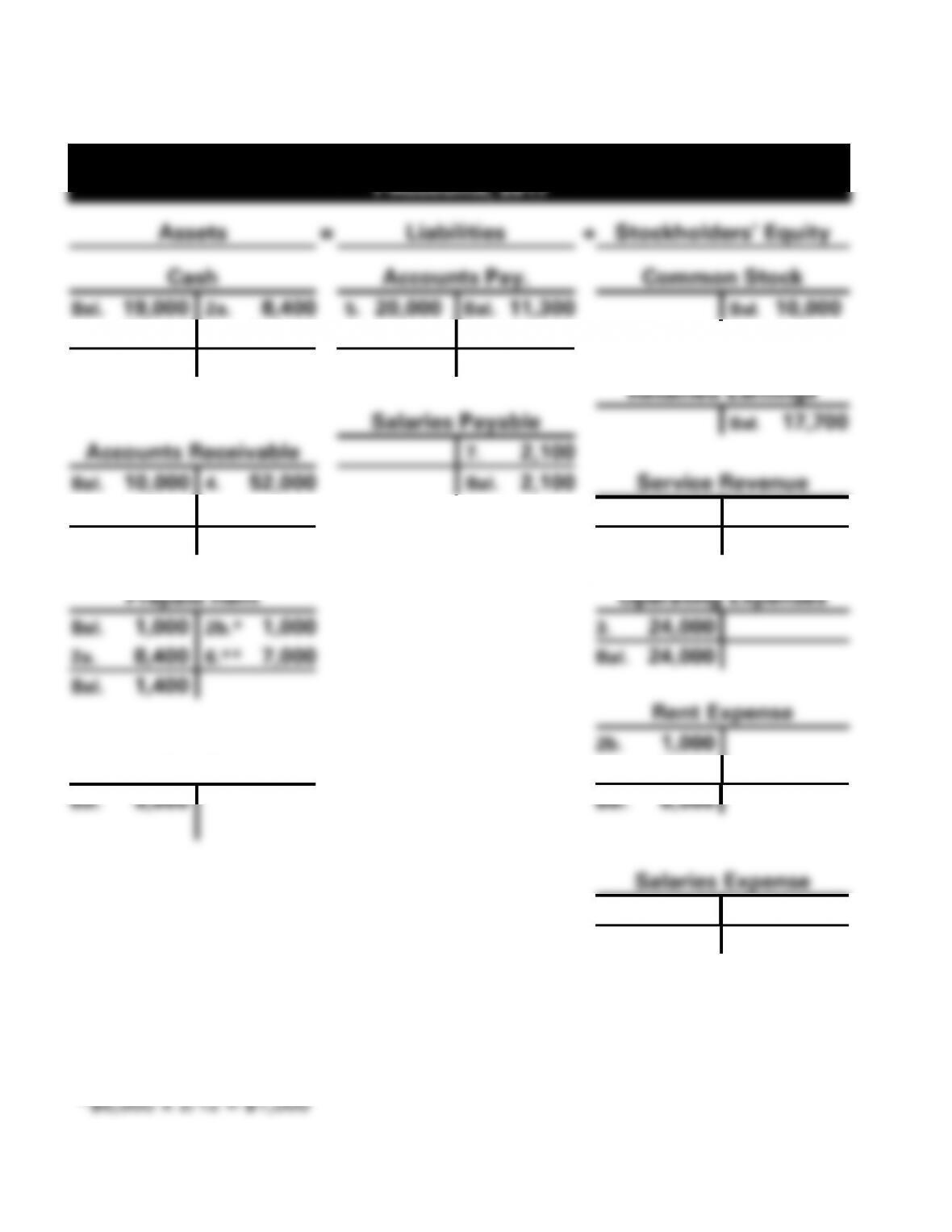

ATC 3-2 a. (cont.)

Miller Company

T-Accounts, 2017

Assets

=

Liabilities

+

Stockholders’ Equity

Cash

Accounts Pay.

Common Stock

Bal. 19,000

2a. 8,400

5. 20,000

Bal. 11,300

Bal. 10,000

4. 52,000

5. 20,000

3. 24,000

Bal. 42,600

Bal. 15,300

Retained Earnings

Salaries Payable

Bal. 17,700

Accounts Receivable

7. 2,100

Bal. 10,000

4. 52,000

Bal. 2,100

Service Revenue

1. 48,000

1. 48,000

Bal. 6,000

Bal. 48,000

Prepaid Rent

Operating Expenses

Bal. 1,000

2b.* 1,000

3. 24,000

2a. 8,400

6.** 7,000

Bal. 24,000

Bal. 1,400

Rent Expense

2b. 1,000

Land

6. 7,000

Bal. 9,000

Bal. 8,000

Salaries Expense

7. 2,100

Bal. 2,100

3-1–20

3-1–21

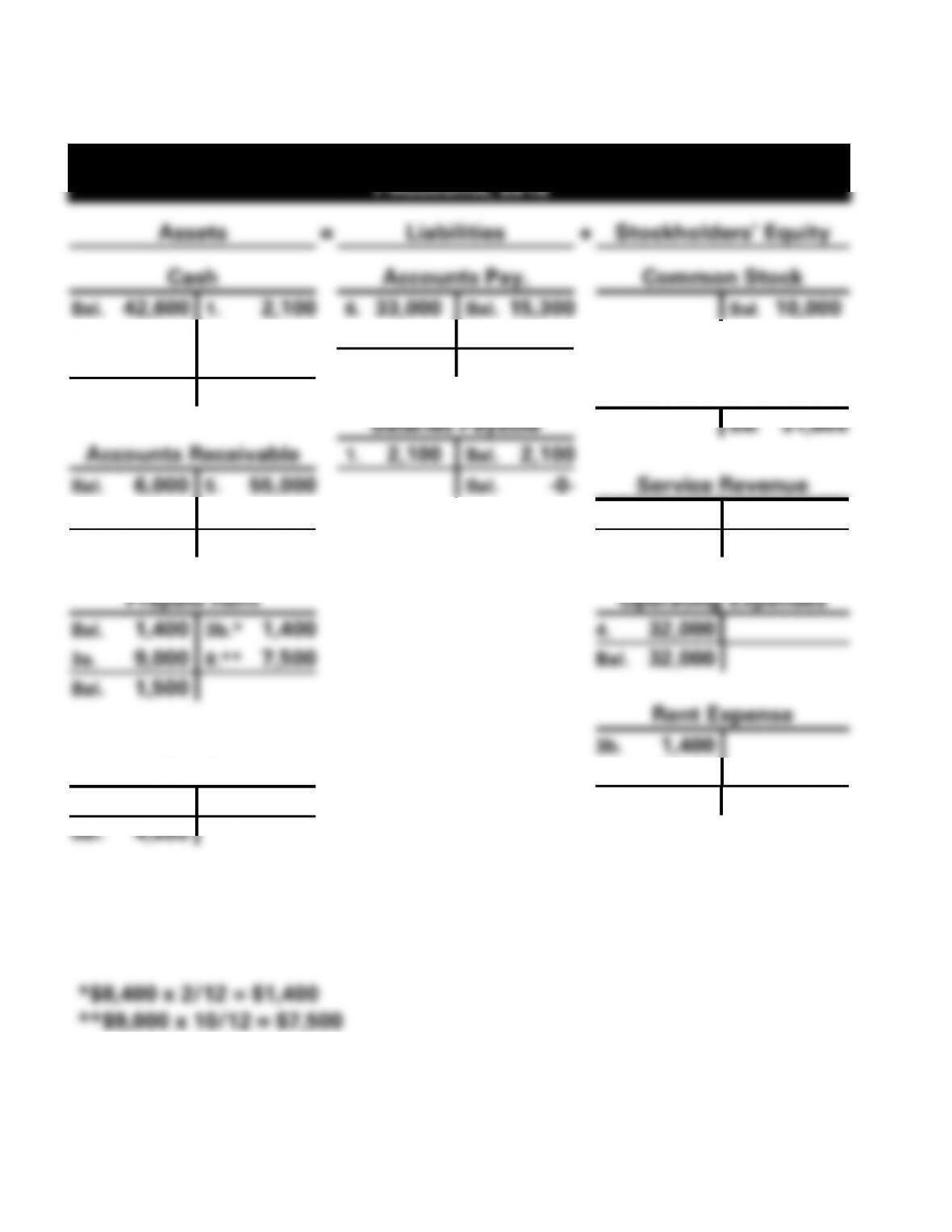

ATC 3-2 a. (cont.)

Miller Company

T-Accounts, 2018

Assets

=

Liabilities

+

Stockholders’ Equity

Cash

Accounts Pay.

Common Stock

Bal. 42,600

1. 2,100

6. 33,000

Bal. 15,300

Bal. 10,000

5. 55,000

3a. 9,000

4. 32,000

7. 5,000

6. 33,000

Bal. 14,300

Bal. 58,500

Retained Earnings

Salaries Payable

Bal. 31,600

Accounts Receivable

1. 2,100

Bal. 2,100

Bal. 6,000

5. 55,000

Bal. -0-

Service Revenue

2. 56,000

2. 56,000

Bal. 7,000

Bal. 56,000

Prepaid Rent

Operating Expenses

Bal. 1,400

3b.* 1,400

4. 32,000

3a. 9,000

8.** 7,500

Bal. 32,000

Bal. 1,500

Rent Expense

3b. 1,400

Land

8. 7,500

Bal. 9,000

7. 5,000

Bal. 8,900

Bal. 4,000

3-1–22

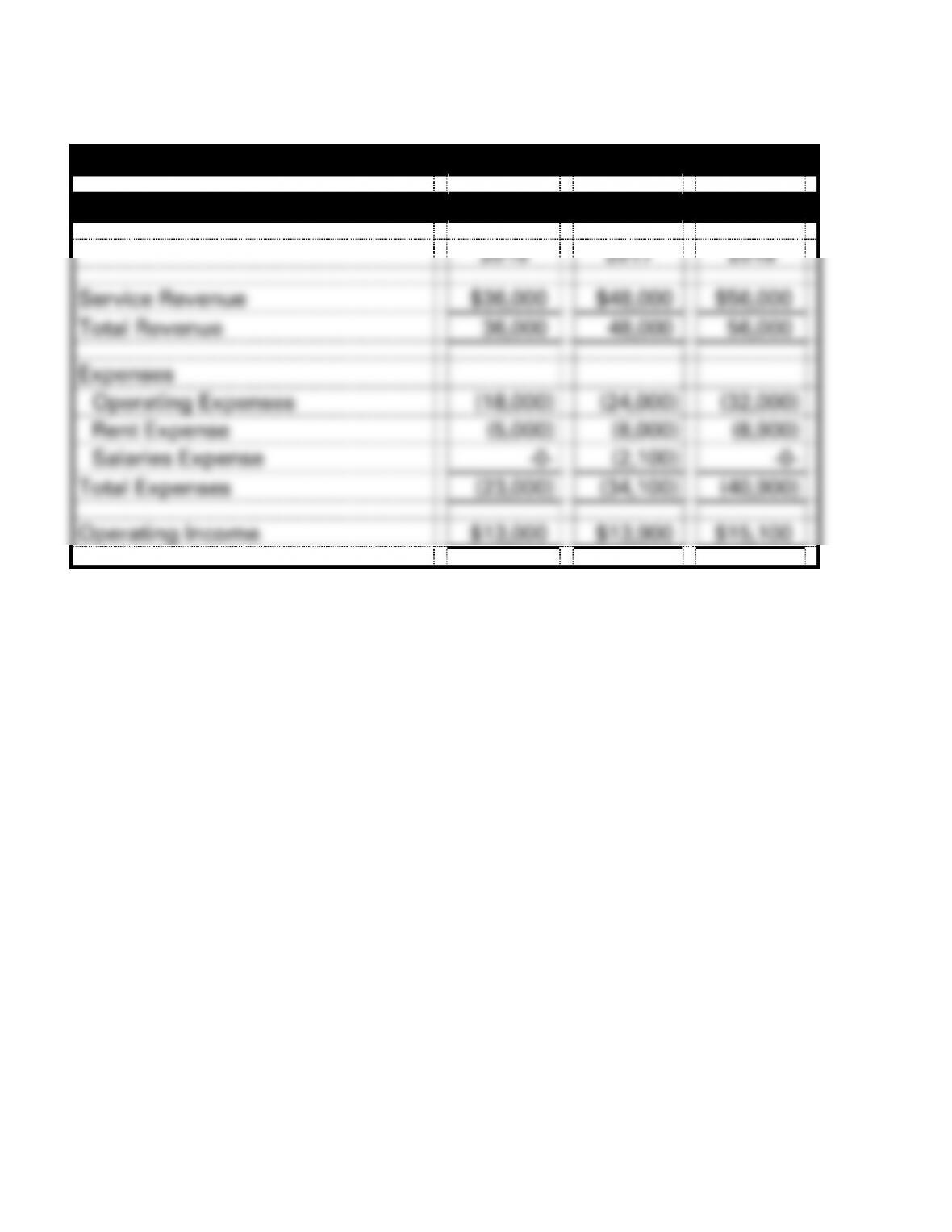

ATC 3-2 a. (cont.)

Miller Company

Income Statements

2016

2017

2018

Service Revenue

$36,000

$48,000

$56,000

Total Revenue

36,000

48,000

56,000

Expenses

Operating Expenses

(18,000)

(24,000)

(32,000)

Rent Expense

(5,000)

(8,000)

(8,900)

Salaries Expense

-0-

(2,100)

-0-

Total Expenses

(23,000)

(34,100)

(40,900)

Operating Income

$13,000

$13,900

$15,100

3-1–23

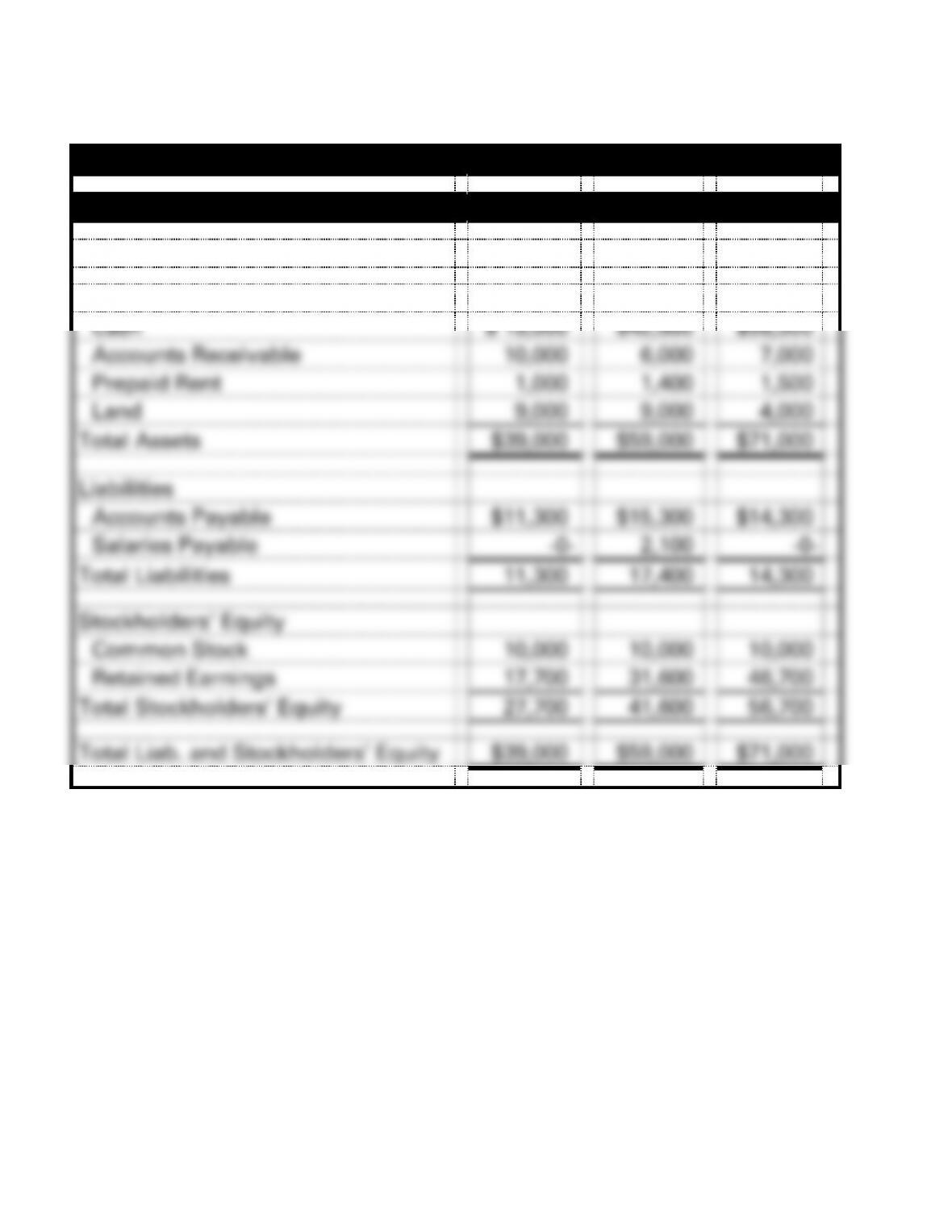

ATC 3-2 a. (cont.)

Miller Company

Balance Sheets

2016

2017

2018

Assets

Cash

$ 19,000

$42,600

$58,500

Accounts Receivable

10,000

6,000

7,000

Prepaid Rent

1,000

1,400

1,500

Land

9,000

9,000

4,000

Total Assets

$39,000

$59,000

$71,000

Liabilities

Accounts Payable

$11,300

$15,300

$14,300

Salaries Payable

-0-

2,100

-0-

Total Liabilities

11,300

17,400

14,300

Stockholders’ Equity

Common Stock

10,000

10,000

10,000

Retained Earnings

17,700

31,600

46,700

Total Stockholders’ Equity

27,700

41,600

56,700

Total Liab. and Stockholders’ Equity

$39,000

$59,000

$71,000

3-1–24

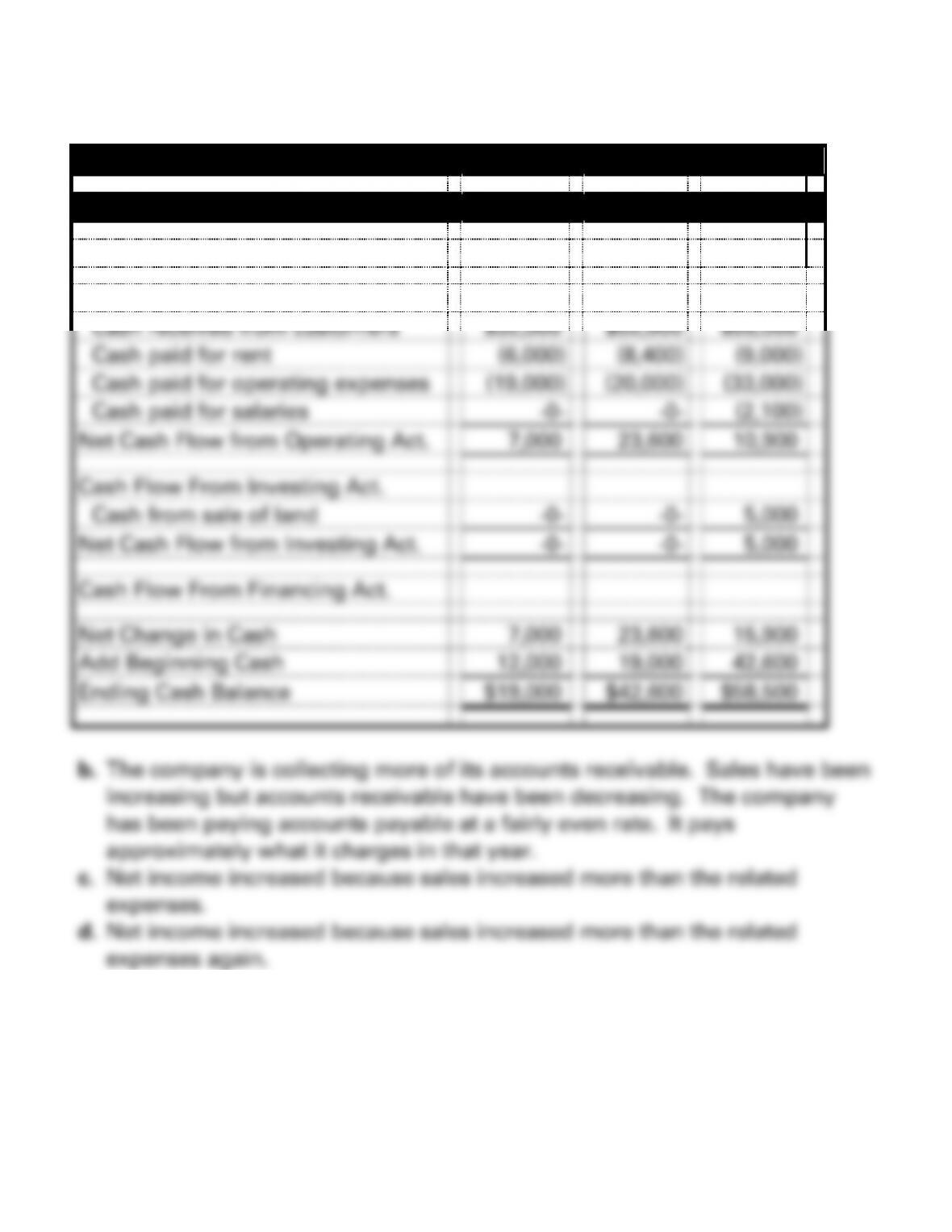

ATC 3-2 a. (cont.)

Miller Company

Statements of Cash Flows

2016

2017

2018

Cash Flow from Operating Act.

Cash received from customers

$32,000

$52,000

$55,000

Cash paid for rent

(6,000)

(8,400)

(9,000)

Cash paid for operating expenses

(19,000)

(20,000)

(33,000)

Cash paid for salaries

-0-

-0-

(2,100)

Net Cash Flow from Operating Act.

7,000

23,600

10,900

Cash Flow From Investing Act.

Cash from sale of land

-0-

-0-

5,000

Net Cash Flow from Investing Act.

-0-

-0-

5,000

Cash Flow From Financing Act.

Net Change in Cash

7,000

23,600

15,900

Add Beginning Cash

12,000

19,000

42,600

Ending Cash Balance

$19,000

$42,600

$58,500