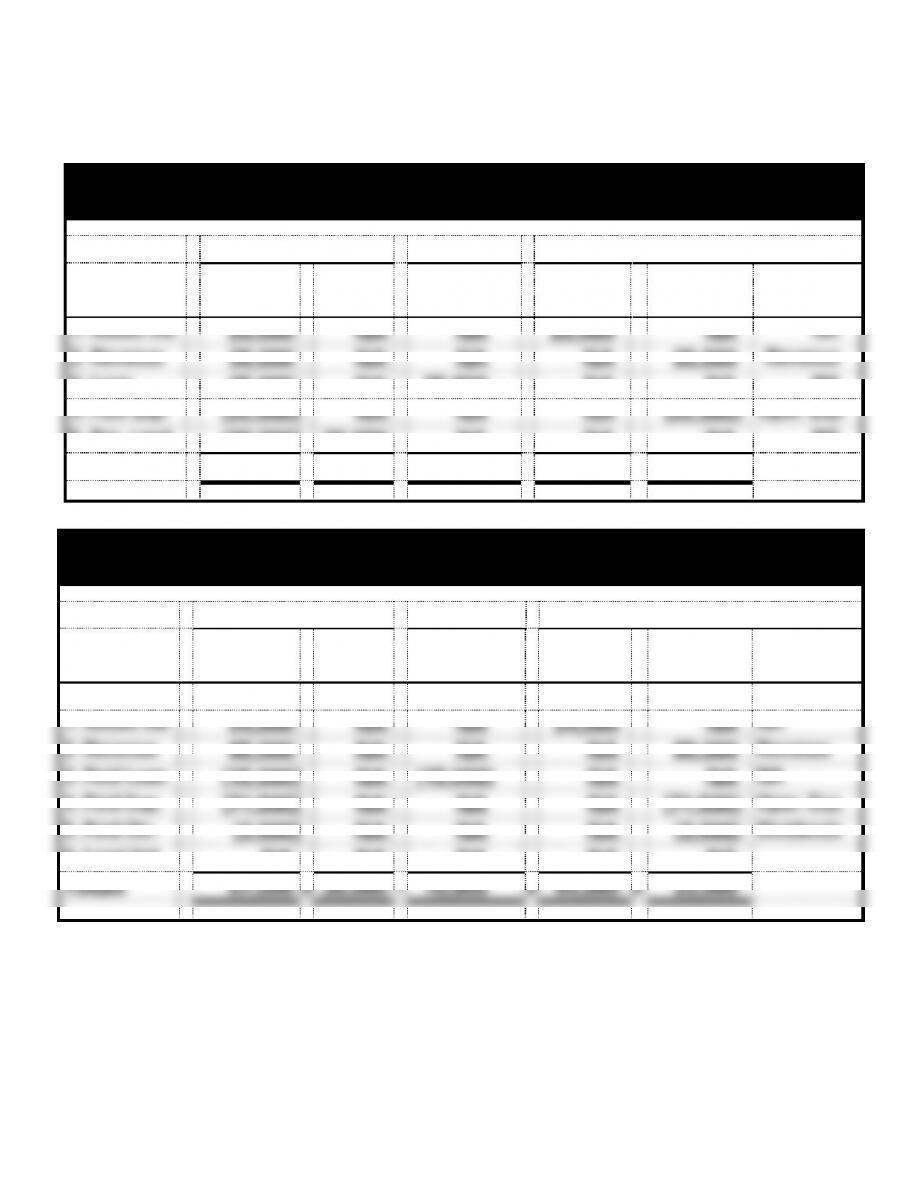

EXERCISE 1-21A g. (cont,)

Carter Company

Statement of Changes in Stockholders’ Equity

For the Year Ended December 31, 2016

Beginning Common Stock

$1,000

Plus: Common Stock Issued

-0-

Ending Common Stock

$1,000

Beginning Retained Earnings

$1,700

Plus: Net Income

600

Less: Dividends

(500)

Ending Retained Earnings

1,800

Total Stockholders’ Equity

$2,800

Assets

Cash

Land

Total Assets

$4,400

Liabilities

Notes Payable

Total Liabilities

$1,600

Stockholders’ Equity

Common Stock

Retained Earnings

Total Stockholders’ Equity

2,800

1-42

EXERCISE 1-21A g.(cont.)

Carter Company

Statement of Cash Flows

For the Year Ended December 31, 2016

Cash Flows From Operating Activities:

Cash Receipts from Customers

$1,800

Cash Payments for Expenses

(1,200)

Net Cash Flow from Operating Activities

$ 600

Cash Flows From Investing Activities:

0

Cash Flows From Financing Activities:

Cash Payments for Dividends

(500)

Net Cash Flow from Financing Activities

(500)

Net Increase in Cash

100

Plus: Beginning Cash Balance

800

Ending Cash Balance

$ 900

EXERCISE 1-22A

a. Since the amount in the Notes Payable account increased from zero to

$9,000, Room Designs Inc. must have received a cash inflow of $9,000

from the issue of the note payable. Similarly, since the balance in the

common stock account increased from $3,500 to $7,500, Room Design

EXERCISE 1-22A c. (cont.)

Room Designs Inc.

Statement of Changes in Stockholders’ Equity

For the Year Ended December 31, 2016

Beginning Common Stock

$ 3,500

Plus: Common Stock Issued

4,000

Ending Common Stock

$7,500

Beginning Retained Earnings

$ 6,400

Plus: Net Income

9,800

Less: Dividends

(2,000)

Ending Retained Earnings

14,200

Total Stockholders’ Equity

$21,700

Assets

Cash

Land

Total Assets

$30,700

Liabilities

Notes Payable

Total Liabilities

$ 9,000

Common Stock

Retained Earnings

21,700

1-45

EXERCISE 1-22A c. (cont.)

Floor Design, Inc.

Statement of Cash Flows

For the Year Ended December 31, 2016

Cash Flows From Operating Activities:

Cash Receipts from Customers

$ 18,100

Cash Payments for Expenses

(8,300)

Net Cash Flow from Operating Activities

$ 9,800

Cash Flows From Investing Activities:

Cash Paid to Purchase Land

$(16,500)

Net Cash Flow from Investing Activities

(16,500)

Cash Flows From Financing Activities:

Cash Receipts from Loan

$ 9,000

Cash Receipts from Stock Issue

4,000

Cash Payments for Dividends

(2,000)

Net Cash Flow from Financing Activities

11,000

Net Increase in Cash

4,300

Plus: Beginning Cash Balance

9,900

Ending Cash Balance

$14,200

1-46

EXERCISE 1-23A

a.

Flowers Company

Accounting Equation as of December 31, 2016

Assets

=

Liabilities

+

Common Stock

+

Retained Earnings

$130,000

$50,000

$70,000

?

Retained Earnings = $130,000 – $70,000 – $50,000 = $10,000

Retained Earnings after closing:

$10,000

Less, Revenue

(30,000)

Add, Expenses

18,000

Add, Dividends

3,000

Retained Earnings before closing

$ 1,000

b. Retained Earnings after closing is $10,000 (see the equation above).

c. The balances in revenue, expense and dividends before closing are:

Revenue

30,000

Expenses

18,000

Dividends

3,000

d. After closing revenue, expense and dividends, the all of the balances

will be zero.

e. Both Common Stock and Retained Earnings represent obligations the

business has to stockholders. The Common Stock represents the

assets a business has acquired from owners. Retained earnings

represent assets a business has acquired by conducting its operations.

1-47

EXERCISE 1-23A (cont.)

f. The owners are no better off immediately after they contributed capital

to the business. While equity increased $30,000, the amount invested

1-48

EXERCISE 1-24A

a.

Year

Cash

Revenues

Cash

Expenses

Net

Income

Retained

Earnings

2016

$20,000

$11,000

9,000

9,000

2017

30,000

14,000

16,000

25,000

2018

40,000

22,000

18,000

43,000

Year

Cash

Revenues

Cash

Expenses

Net

Income

Retained

Earnings

2016

$20,000

$11,000

9,000

9,000

2017

30,000

14,000

16,000

20,000*

2018

40,000

22,000

18,000

38,000**

1-49

EXERCISE 1-25A

a. The balance in the Retained Earnings account as of January 31, 2016

is zero.

Explanation: The revenue is recorded in the Revenue account and is not transferred into

retained earnings until the year-end closing process is accomplished.

is $93,500 ($7,500 + $86,000). The December 31, 2016 before closing

balance in the Expense account is $55,800 ($4,800 + $51,000).

Explanation: The revenue and expense amounts accumulate in the Revenue and

Expense accounts throughout the year.

e. The January 1, 2015 balance in the Retained Earnings account is

1-50

EXERCISE 1-26A

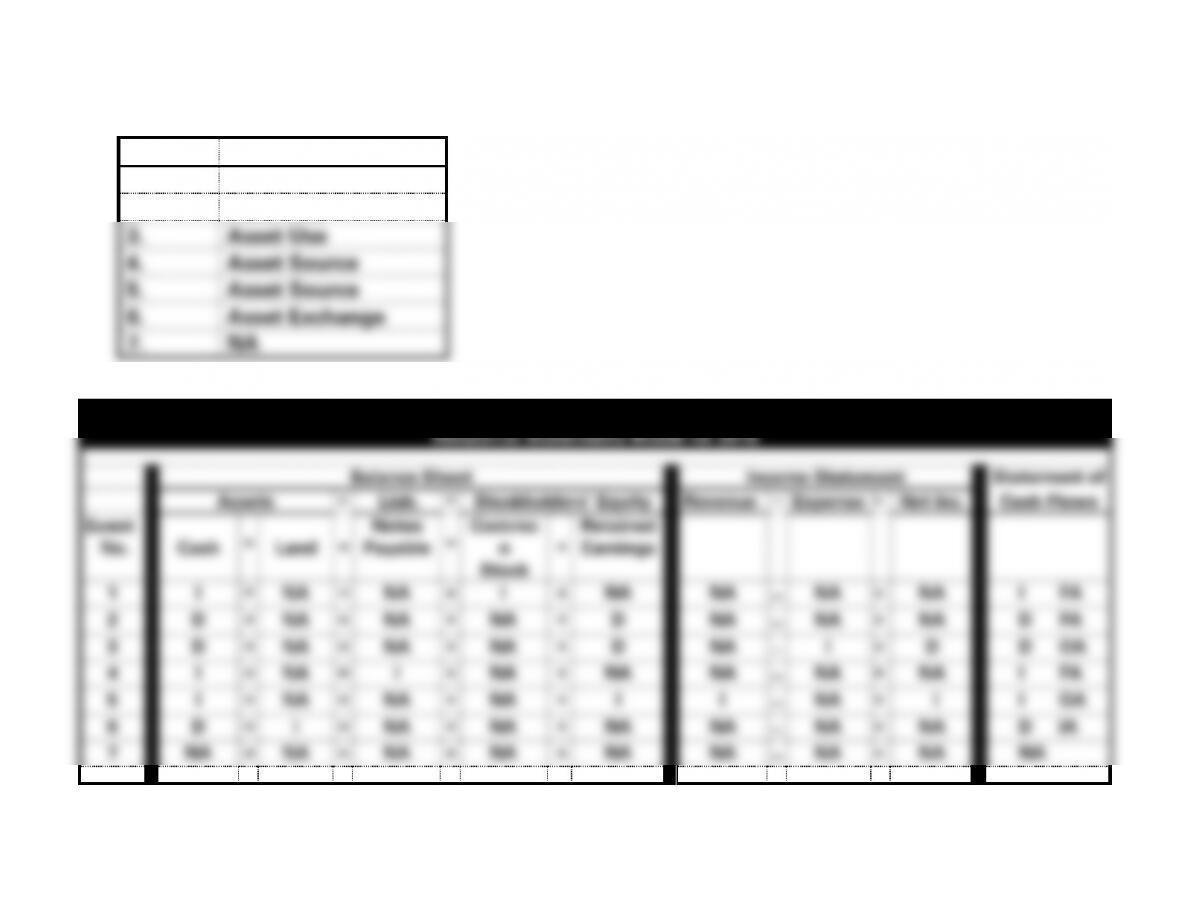

a.

Event

1.

Asset Source

2.

Asset Use

3.

Asset Use

4.

Asset Source

5.

Asset Source

6.

Asset Exchange

7.

NA

b.

The Candle Shop

Horizontal Statements Model for 2016

Balance Sheet

Income Statement

Statement of

Assets

=

Liab.

+

Stockholders’ Equity

Revenue

−

Expense

=

Net Inc.

Cash Flows

Event

No.

Cash

+

Land

=

Notes

Payable

+

Commo

n

Stock

+

Retained

Earnings

1

I

+

NA

=

NA

+

I

+

NA

NA

−

NA

=

NA

I FA

2

D

+

NA

=

NA

+

NA

+

D

NA

−

NA

=

NA

D FA

3

D

+

NA

=

NA

+

NA

+

D

NA

−

I

=

D

D OA

4

I

+

NA

=

I

+

NA

+

NA

NA

−

NA

=

NA

I FA

5

I

+

NA

=

NA

+

NA

+

I

I

−

NA

=

I

I OA

6

D

+

I

=

NA

+

NA

+

NA

NA

−

NA

=

NA

D IA

7

NA

+

NA

=

NA

+

NA

+

NA

NA

−

NA

=

NA

NA

1-51

EXERCISE 1-27A

a. The assets would be worth the same, but would be shown at

1-52

PROBLEM 1-28A

a. The memo should explain that all entities must account for the use

of assets, even though they may not be for-profit entities. The

stakeholders are interested in the use of assets as well as the

financial health of the entity.

1-53

PROBLEM 1-29A

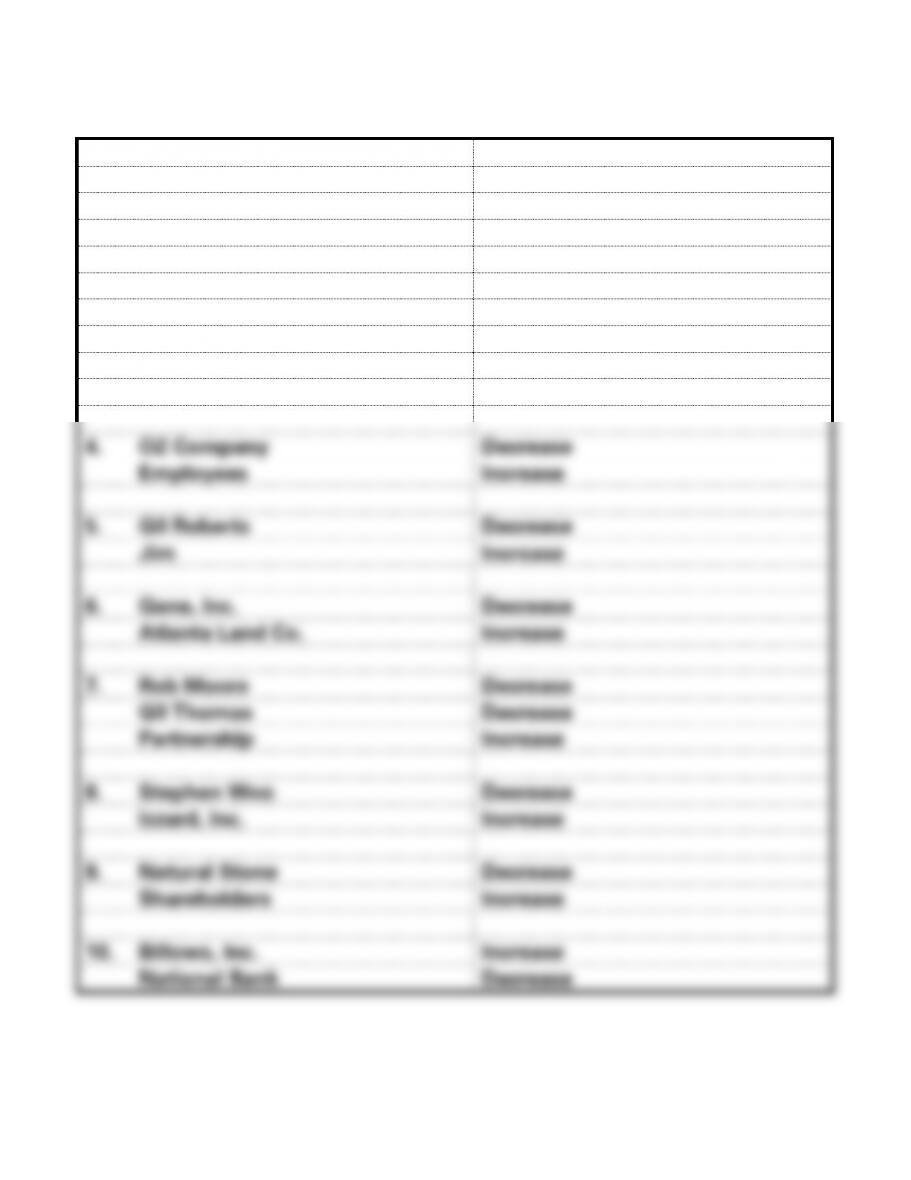

a. Entities mentioned:

b. Effect on the cash account:

1. Bob Wilder

Decrease

Wilder Co.

Increase

2. Sam Pace Business

Increase

Customers

Decrease

3. Jim Sneed

Increase/Decrease

National Bank

Decrease

Iuka Ford

Increase

4. OZ Company

Decrease

Employees

Increase

5. Gil Roberts

Decrease

Jim

Increase

6. Gane, Inc.

Decrease

Atlanta Land Co.

Increase

7. Rob Moore

Decrease

Gil Thomas

Decrease

Partnership

Increase

8. Stephen Woo

Decrease

Izzard, Inc.

Increase

9. Natural Stone

Decrease

Shareholders

Increase

10. Billows, Inc.

Increase

National Bank

Decrease

1-54

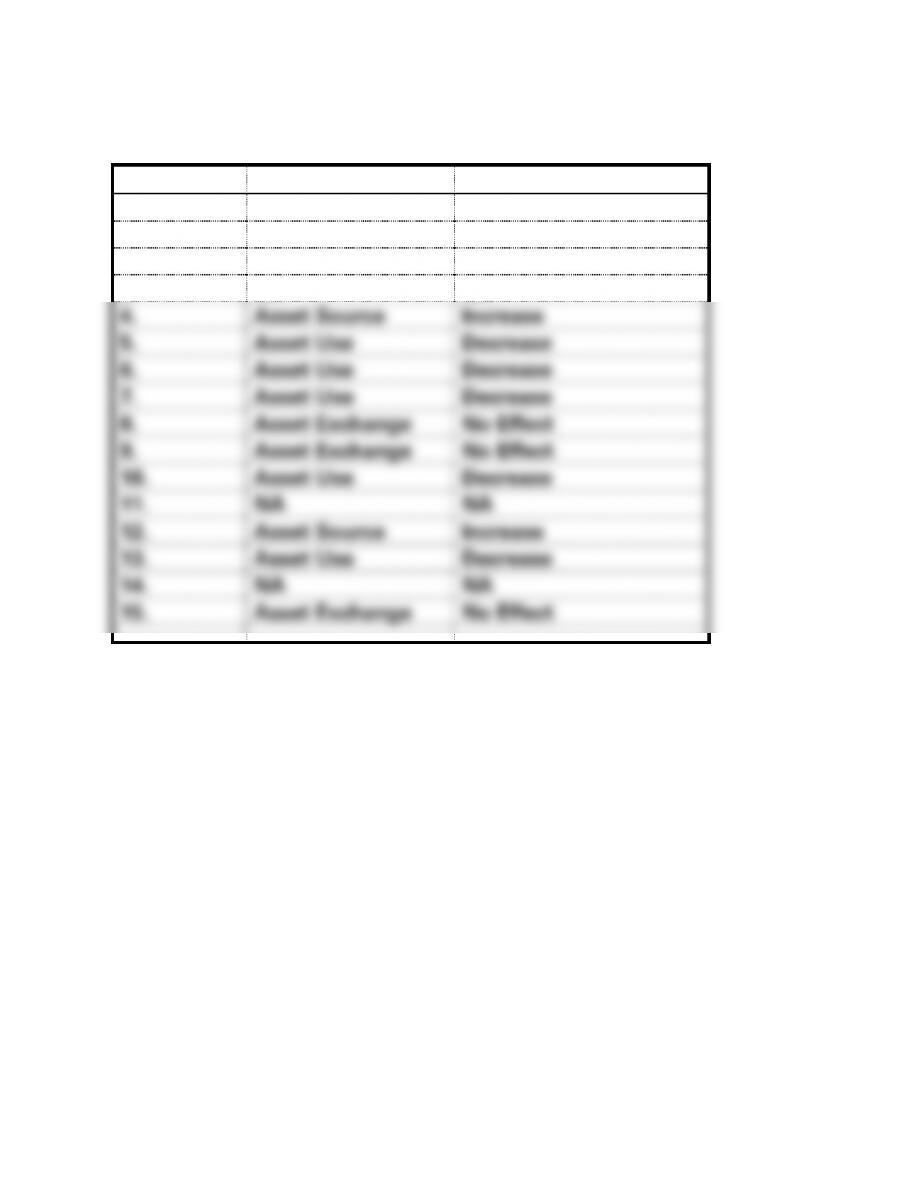

PROBLEM 1-30A

Event No.

Type of Event

Effect on Total Assets

1.

Asset Source

Increase

2.

Asset Use

Decrease

3.

NA

NA

4.

Asset Source

Increase

5.

Asset Use

Decrease

6.

Asset Use

Decrease

7.

Asset Use

Decrease

8.

Asset Exchange

No Effect

9.

Asset Exchange

No Effect

10.

Asset Use

Decrease

11.

NA

NA

12.

Asset Source

Increase

13.

Asset Use

Decrease

14.

NA

NA

15.

Asset Exchange

No Effect

1-55

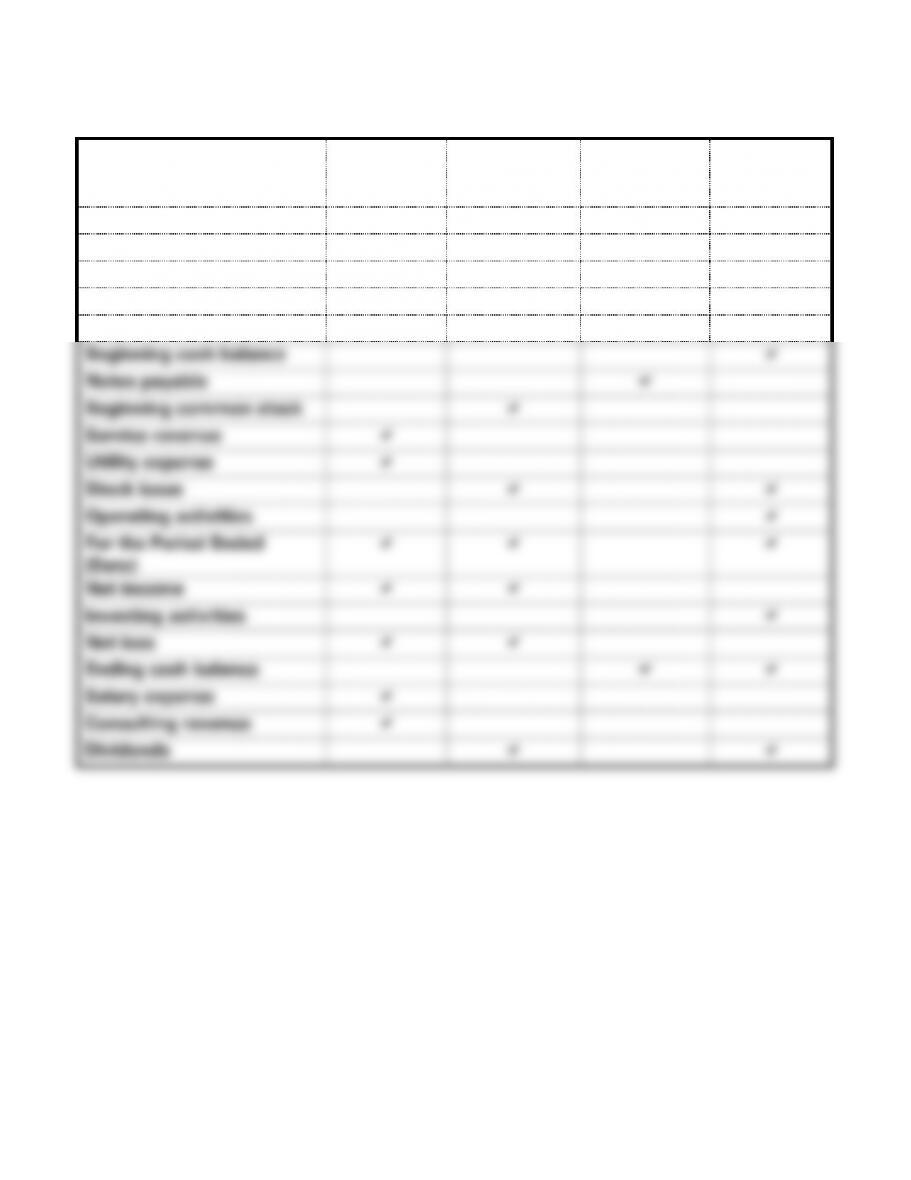

PROBLEM 1-31A

Item

Income

Statement

Statement of

Changes in

Stk. Equity

Balance

Sheet

Statement

of Cash

Flows

Financing activities

Ending common stock

Interest expense

As of (date)

Land

Beginning cash balance

Notes payable

Beginning common stock

Service revenue

Utility expense

Stock issue

Operating activities

For the Period Ended

(Date)

Net income

Investing activities

Net loss

Ending cash balance

Salary expense

Consulting revenue

Dividends

1-56

PROBLEM 1-32A

a.

Mark’s Consulting Services

Accounting Equation for 2016

Assets

=

Liabilities

+

Stockholders’ Equity

Event

Cash

+

Land

=

Notes

Payable

+

Com.

Stock

+

Retained

Earnings

Acct.

Title/RE

1. Issued stk

20,000

NA

NA

20,000

NA

NA

2. Revenue

35,000

NA

NA

NA

35,000

Revenue

3. Loan

25,000

NA

25,000

NA

NA

NA

4. Paid Exp.

(22,000)

NA

NA

NA

(22,000)

Oper. Exp.

5. Pur. Land

(30,000)

30,000

NA

NA

NA

NA

Totals

28,000

+

30,000

=

25,000

+

20,000

+

13,000

Mark’s Consulting Services

Accounting Equation for 2017

Assets

=

Liabilities

+

Stockholders’ Equity

Event

Cash

+

Land

=

Notes

Payable

+

Com.

Stock

+

Retained

Earnings

Acct.

Title/RE

Beg. Bal.

28,000

30,000

25,000

20,000

13,000

1. Issued stk

24,000

NA

NA

24,000

NA

NA

2. Revenue

95,000

NA

NA

NA

95,000

Revenue

3. Paid Loan

(15,000)

NA

(15,000)

NA

NA

NA

4. Paid Exp.

(71,500)

NA

NA

NA

(71,500)

Oper. Exp.

5. Paid Div.

(3,000)

NA

NA

NA

(3,000)

Dividends

6. Land Val.

NA

NA

NA

NA

NA

Totals

57,500

+

30,000

=

10,000

+

44,000

+

33,500

1-57

PROBLEM 1-32A (cont.)

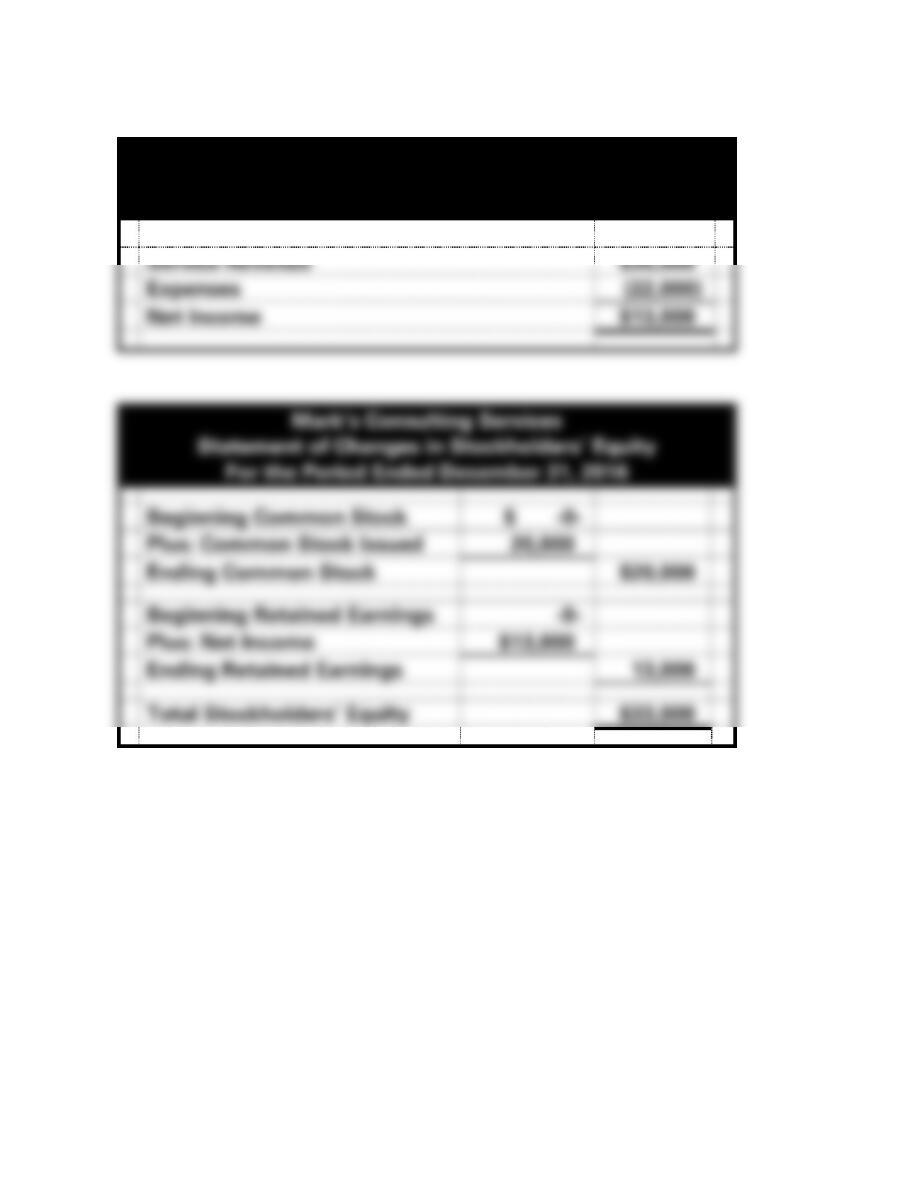

b.

Mark’s Consulting Services

Income Statement

For the Period Ended December 31, 2016

Service Revenue

$35,000

Expenses

(22,000)

Net Income

$13,000

Mark’s Consulting Services

Statement of Changes in Stockholders’ Equity

For the Period Ended December 31, 2016

Beginning Common Stock

$ -0-

Plus: Common Stock Issued

20,000

Ending Common Stock

$20,000

Beginning Retained Earnings

-0-

Plus: Net Income

$13,000

Ending Retained Earnings

13,000

Total Stockholders’ Equity

$33,000

1-58

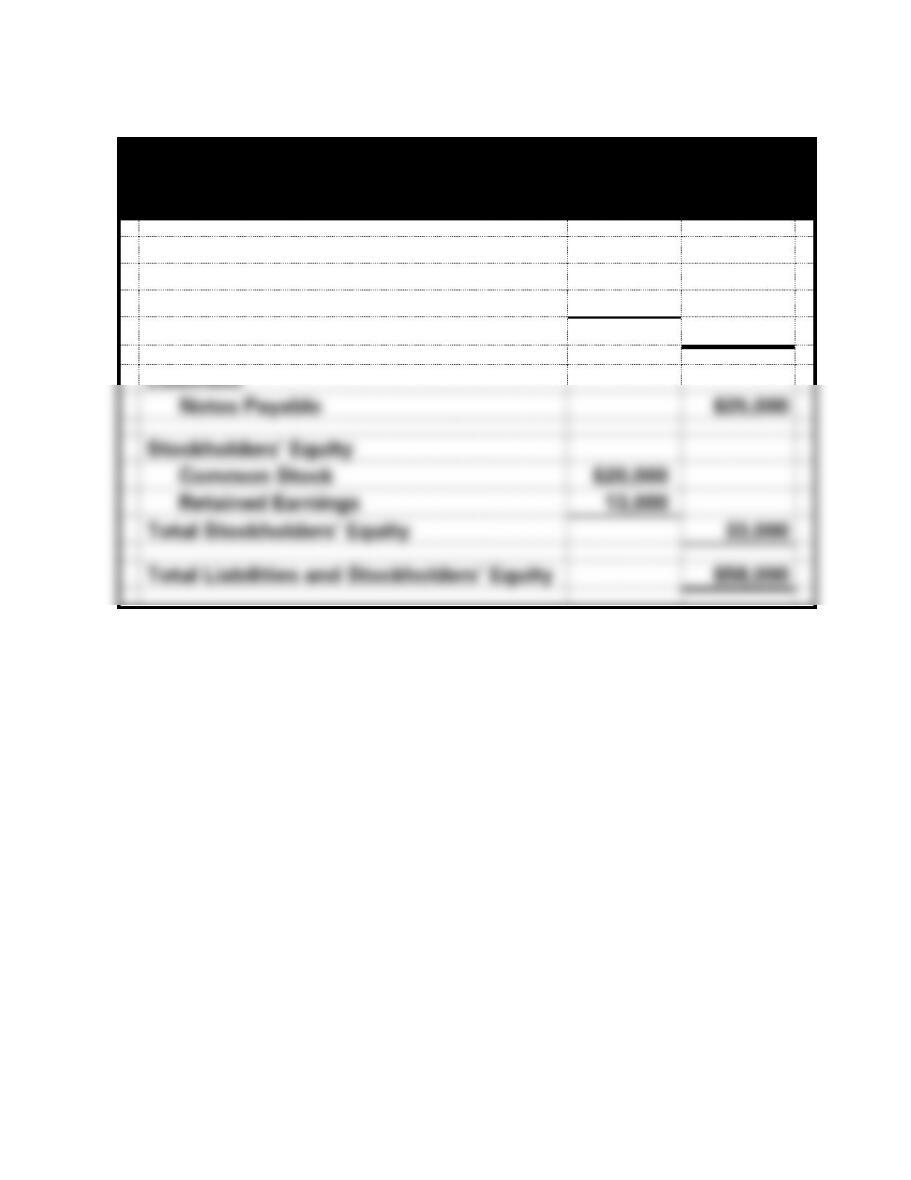

PROBLEM 1-32A b. (cont.)

Mark’s Consulting Services

Balance Sheet

As of December 31, 2016

Assets

Cash

$28,000

Land

30,000

Total Assets

$58,000

Liabilities

Notes Payable

$25,000

Stockholders’ Equity

Common Stock

$20,000

Retained Earnings

13,000

Total Stockholders’ Equity

33,000

Total Liabilities and Stockholders’ Equity

$58,000

1-59

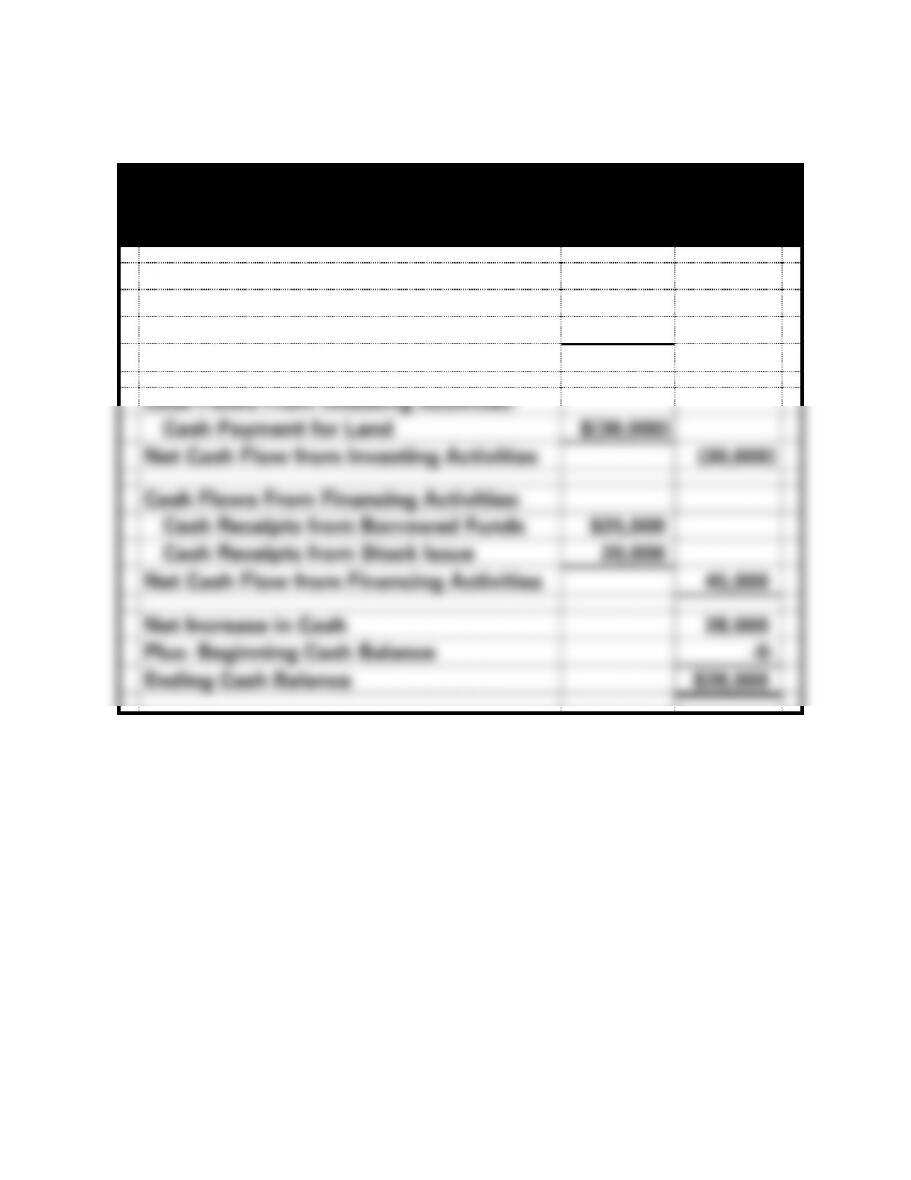

PROBLEM 1-32A b. (cont.)

Mark’s Consulting Services

Statement of Cash Flows

For the Year Ended December 31, 2016

Cash Flows From Operating Activities:

Cash Receipts from Customers

$35,000

Cash Payments for Expenses

(22,000)

Net Cash Flow from Operating Activities

$13,000

Cash Flows From Investing Activities:

Cash Payment for Land

$(30,000)

Net Cash Flow from Investing Activities

(30,000)

Cash Flows From Financing Activities:

Cash Receipts from Borrowed Funds

$25,000

Cash Receipts from Stock Issue

20,000

Net Cash Flow from Financing Activities

45,000

Net Increase in Cash

28,000

Plus: Beginning Cash Balance

-0-

Ending Cash Balance

$28,000

1-60

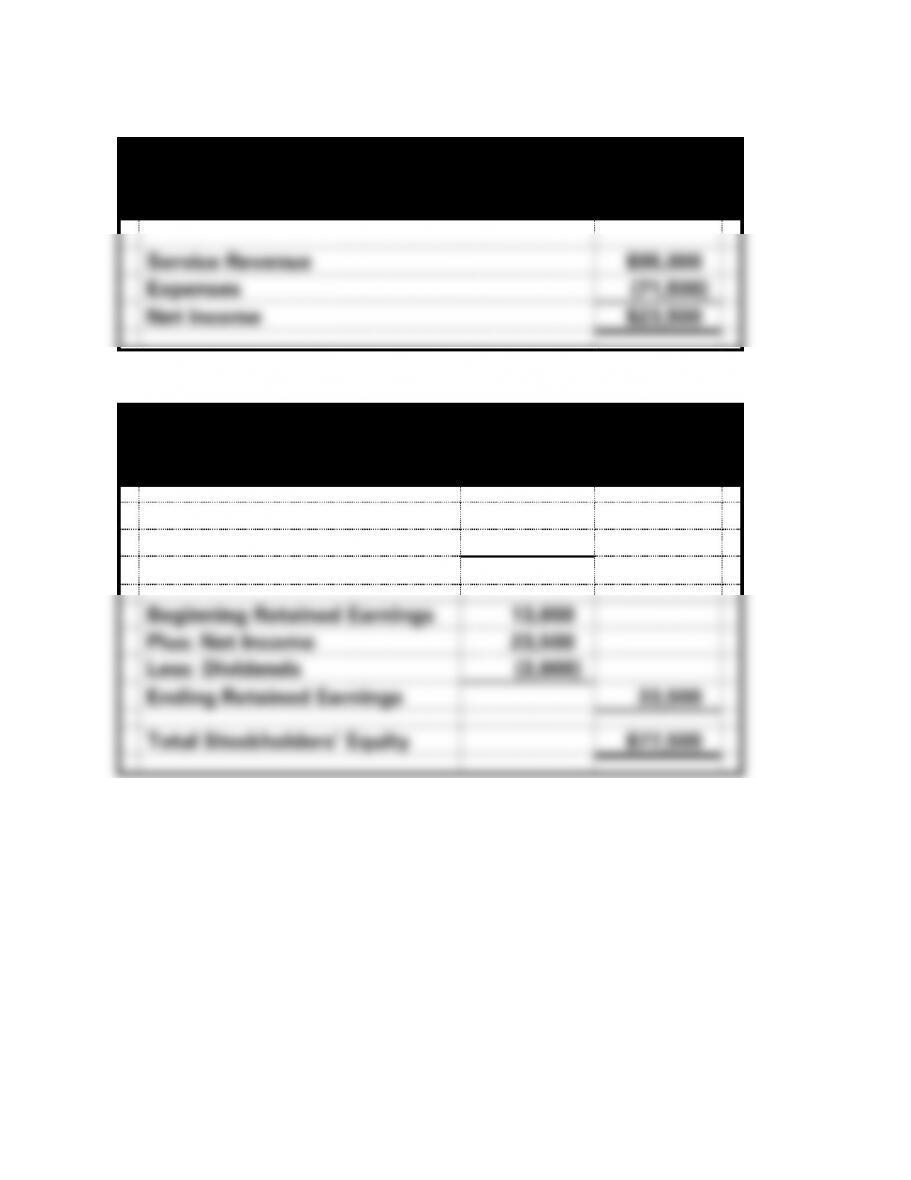

PROBLEM 1-32A b. (cont.)

Mark’s Consulting Services

Income Statement

For the Period Ended December 31, 2017

Service Revenue

$95,000

Expenses

(71,500)

Net Income

$23,500

Mark’s Consulting Services

Statement of Changes in Stockholders’ Equity

For the Period Ended December 31, 2017

Beginning Common Stock

$20,000

Plus: Common Stock Issued

24,000

Ending Common Stock

$44,000

Beginning Retained Earnings

13,000

Plus: Net Income

23,500

Less: Dividends

(3,000)

Ending Retained Earnings

33,500

Total Stockholders’ Equity

$77,500