11-117

PROBLEM 11-23B (cont.)

c.

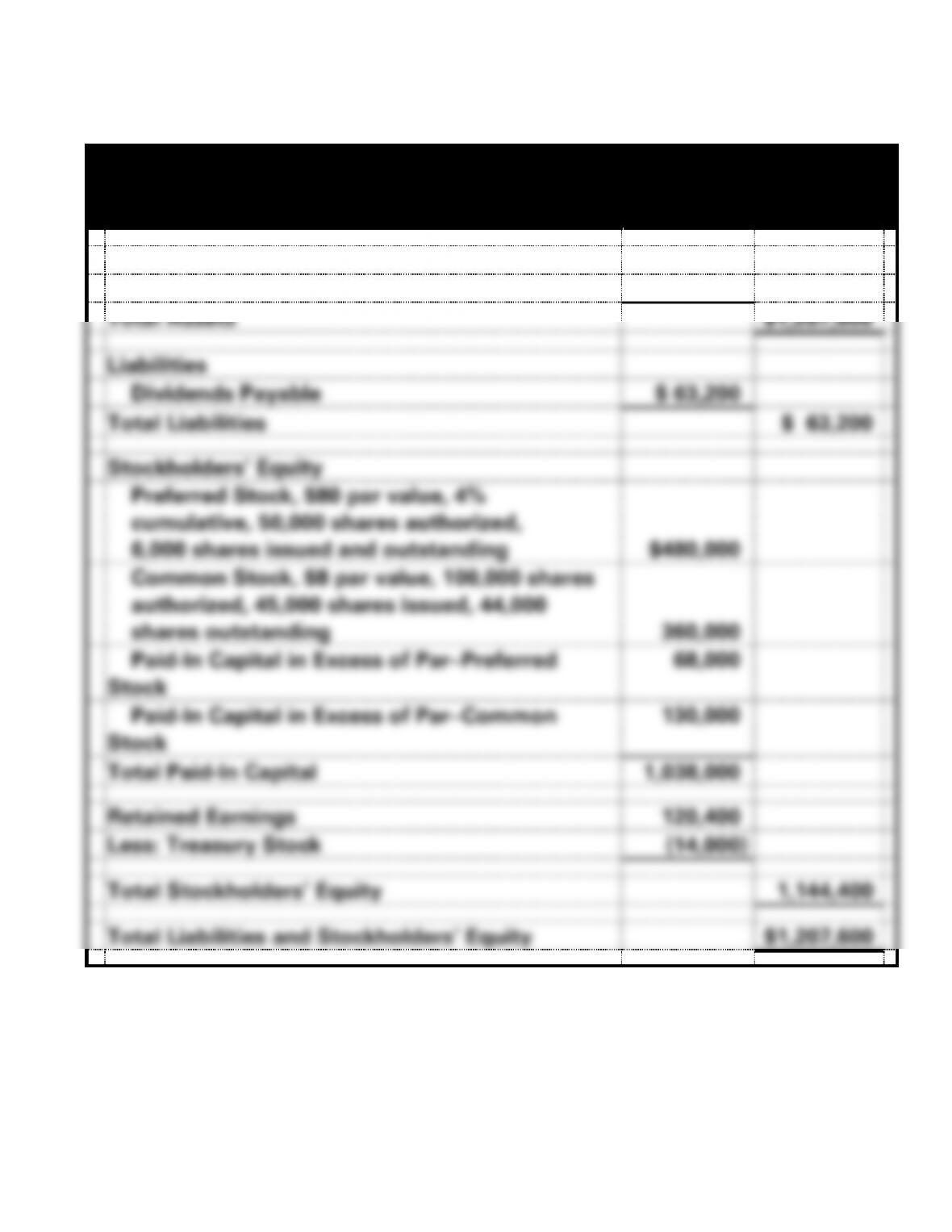

Edgar Corporation

Balance Sheet

As of December 31, 2017

Assets

Cash

$1,207,600

Total Assets

$1,207,600

Liabilities

Dividends Payable

$ 63,200

Total Liabilities

$ 63,200

Stockholders’ Equity

Preferred Stock, $80 par value, 4%

cumulative, 50,000 shares authorized,

6,000 shares issued and outstanding

$480,000

Common Stock, $8 par value, 100,000 shares

authorized, 45,000 shares issued, 44,000

shares outstanding

360,000

Paid-In Capital in Excess of Par−Preferred

Stock

68,000

Paid-In Capital in Excess of Par−Common

Stock

130,000

Total Paid-In Capital

1,038,000

Retained Earnings

120,400

Less: Treasury Stock

(14,000)

Total Stockholders’ Equity

1,144,400

Total Liabilities and Stockholders’ Equity

$1,207,600

11-118

PROBLEM 11-24B

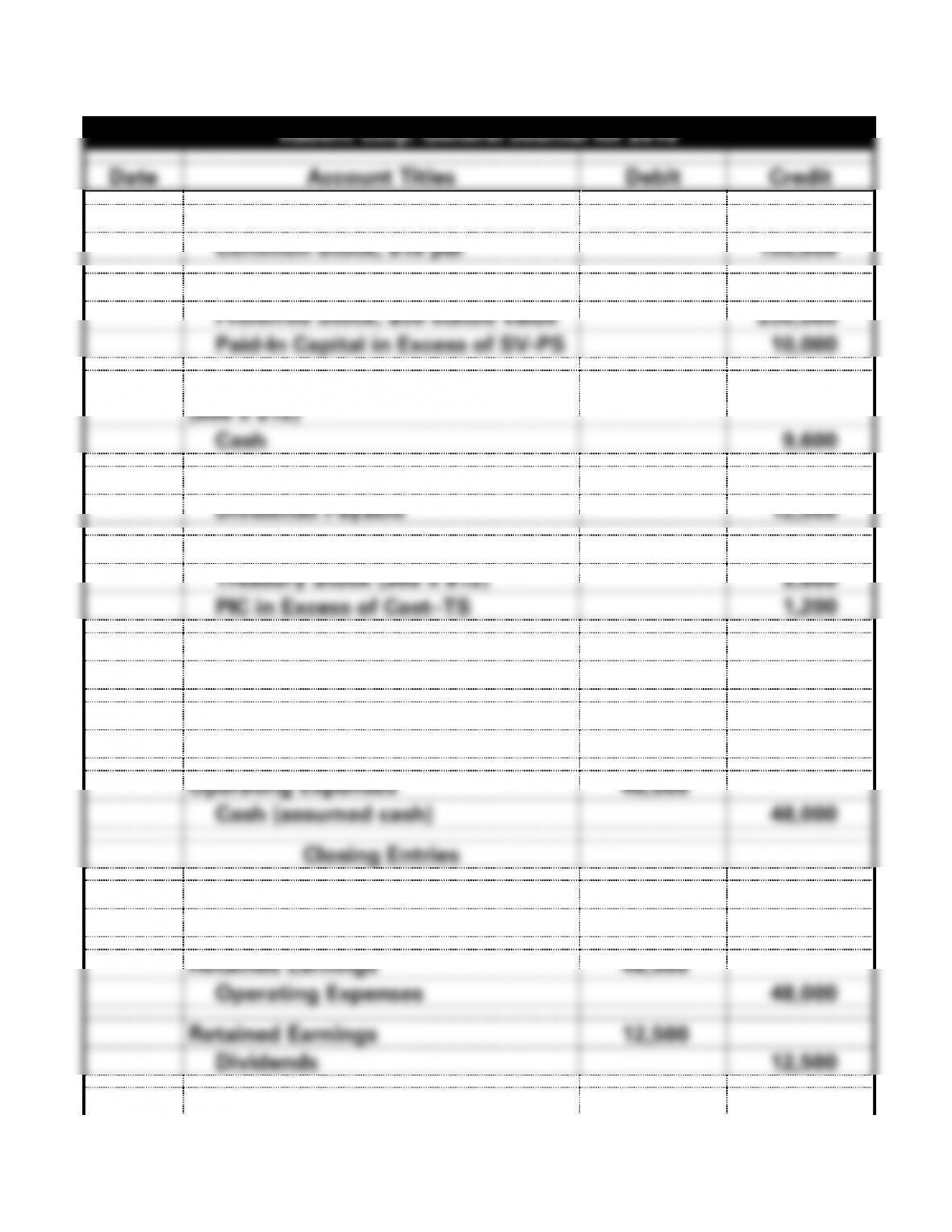

Rabern Corp. General Journal for 2016

Date

Account Titles

Debit

Credit

1.

Cash (15,000 x $10)

150,000

Common Stock, $10 par

150,000

2.

Cash (5,000 x $52)

260,000

Preferred Stock, $50 stated value

250,000

Paid-In Capital in Excess of SV-PS

10,000

3.

Treasury Stock (Common Stock)

(800 x $12)

9,600

Cash

9,600

4.

Dividends ($50 x 5% x 5,000)

12,500

Dividends Payable

12,500

5.

Cash (300 x $16)

4,800

Treasury Stock (300 x $12)

3,600

PIC in Excess of Cost−TS

1,200

6.

Dividends Payable

12,500

Cash

12,500

7.

Cash (assumed cash)

80,000

Service Revenue

80,000

Operating Expenses

48,000

Cash (assumed cash)

48,000

Closing Entries

8.

Service Revenue

80,000

Retained Earnings

80,000

Retained Earnings

48,000

Operating Expenses

48,000

Retained Earnings

12,500

Dividends

12,500

9.

Retained Earnings

6,000

11-119

Appropriated Retained Earnings

6,000

11-120

PROBLEM 11-24B a. (cont.)

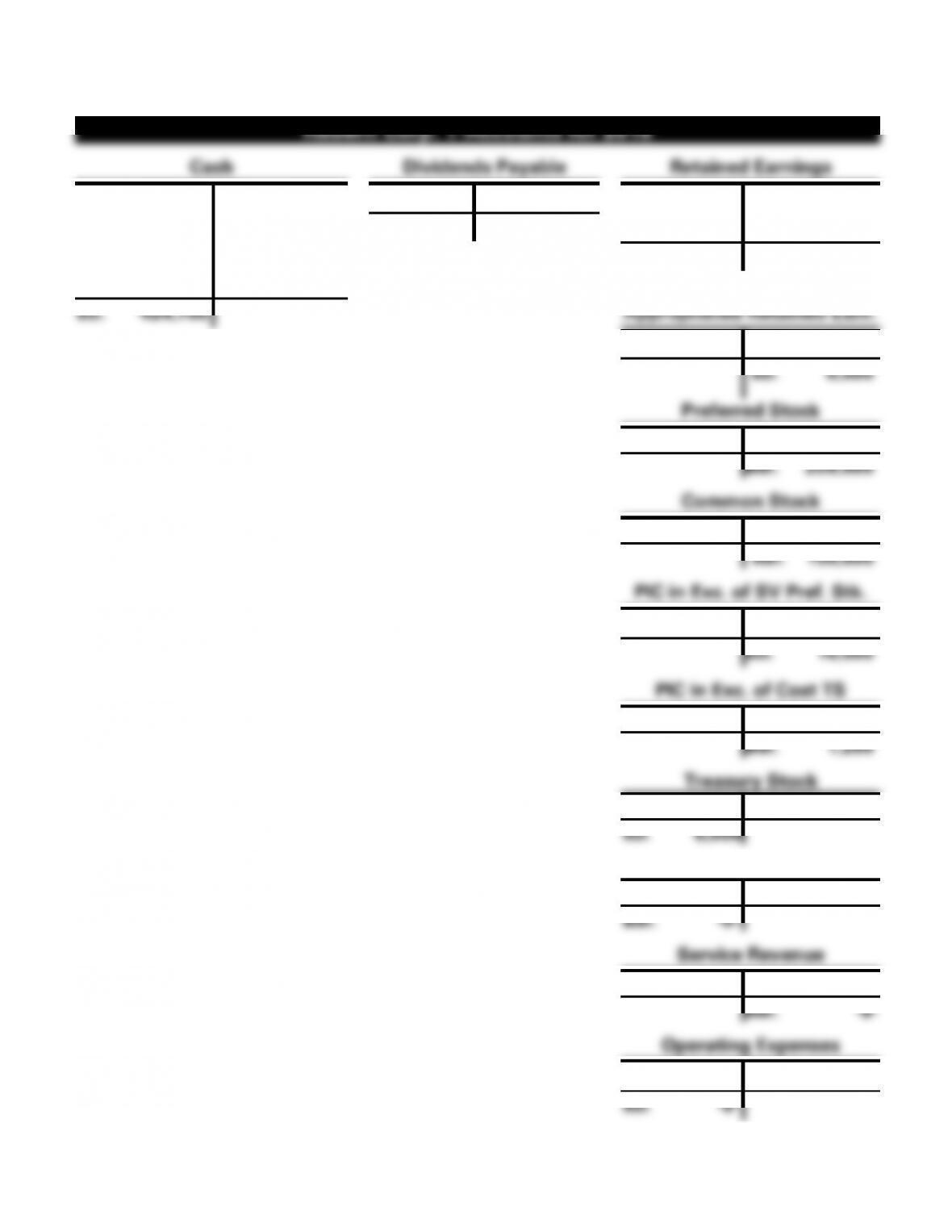

Rabern Corp. T-Accounts for 2016

Cash

Dividends Payable

Retained Earnings

1. 150,000

3. 9,600

6. 12,500

4. 12,500

cl 8. 60,500

cl 8 80,000

2. 260,000

6. 12,500

Bal. -0-

cl 9. 6,000

5. 4,800

7. 48,000

Bal. 13,500

7. 80,000

Bal. 424,700

Appropriated Retained Earn.

cl 9. 6,000

Bal. 6,000

Preferred Stock

2. 250,000

Bal. 250,000

Common Stock

1. 150,000

Bal. 150,000

PIC in Exc. of SV Pref. Stk.

2. 10,000

Bal. 10,000

PIC in Exc. of Cost TS

5. 1,200

Bal. 1,200

Treasury Stock

3. 9,600

5. 3,600

Bal. 6,000

Dividends

4. 12,500

cl 8. 12,500

Bal. -0-

Service Revenue

cl 8. 80,000

7. 80,000

Bal. -0-

Operating Expenses

7. 48,000

cl 8. 48,000

Bal. -0-

11-121

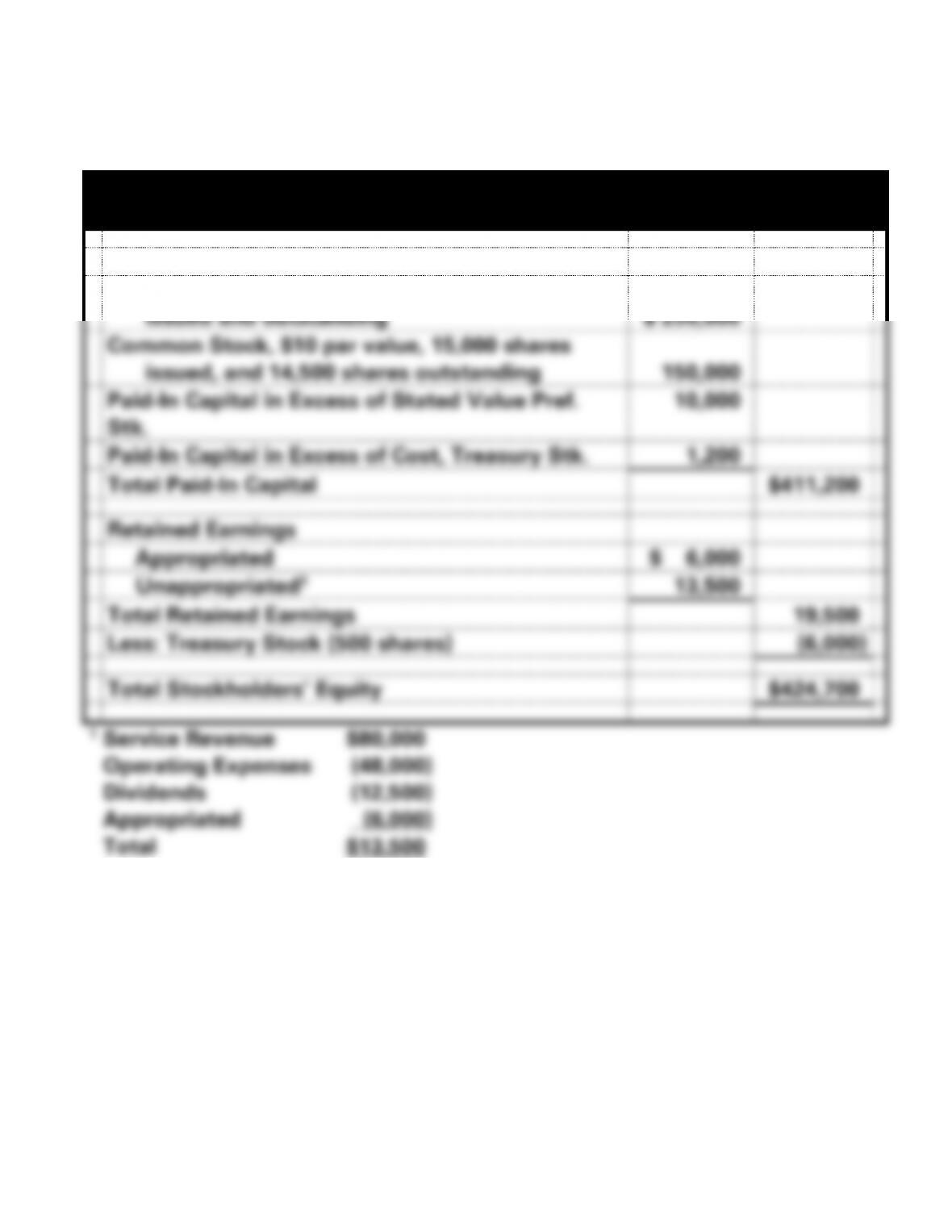

PROBLEM 11-24B (cont.)

b.

Rabern Corp.

December 31, 2016

Stockholders’ Equity

Preferred Stock, $50 stated value, 5,000 shares

issued and outstanding

$ 250,000

Common Stock, $10 par value, 15,000 shares

issued, and 14,500 shares outstanding

150,000

Paid-In Capital in Excess of Stated Value Pref.

Stk.

10,000

Paid-In Capital in Excess of Cost, Treasury Stk.

1,200

Total Paid-In Capital

$411,200

Retained Earnings

Appropriated

$ 6,000

Unappropriated1

13,500

Total Retained Earnings

19,500

Less: Treasury Stock (500 shares)

(6,000)

Total Stockholders’ Equity

$424,700

11-9

PROBLEM 11-25B

a. $400,000 40,000 shares = $10 per share

b. $10 par value per share x 5% = $.50 per share

f. 1. 38,000 x 2 = 76,000 shares outstanding after the split.

2. No amount will be transferred from retained earnings.

3. Theoretically, the market price will be $20 ($40 2).

11–10

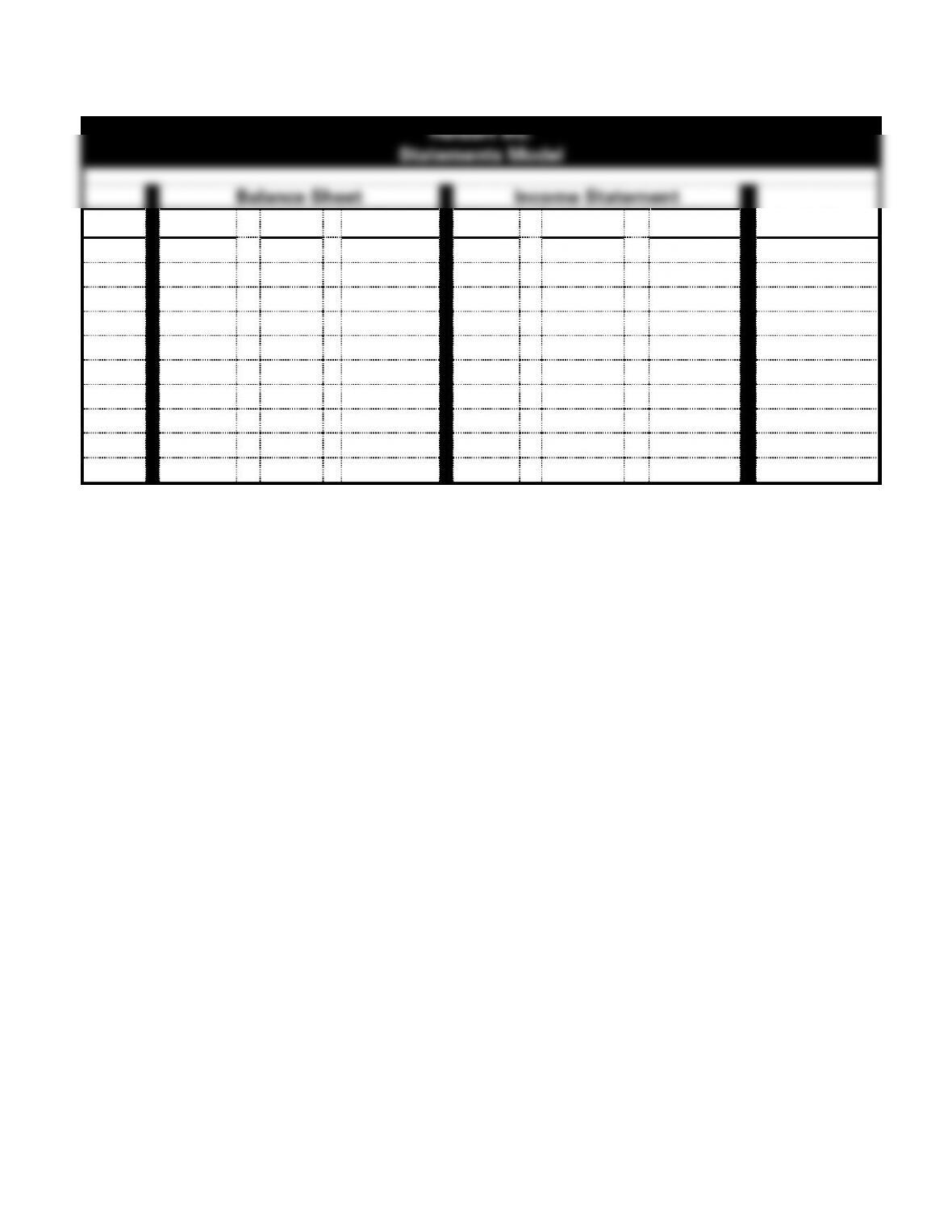

PROBLEM 11-26B

Halbart Inc.

Statements Model

Balance Sheet

Income Statement

Event

Assets

=

Liab.

+

S. Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

1.

+

NA

+

NA

NA

NA

+ FA

2.

*NA

NA

NA

NA

NA

NA

NA

3.

NA

NA

+−

NA

NA

NA

NA

4.

+

NA

+

NA

NA

NA

+ FA

5.

+

NA

+

NA

NA

NA

+ FA

6.

+

NA

+

NA

NA

NA

+ FA

7.

−

NA

−

NA

NA

NA

− FA

8.

NA

+

−

NA

NA

NA

NA

9.

NA

NA

+−

NA

NA

NA

NA

10.

−

−

NA

NA

NA

NA

− FA

*No entry: memo record of change in par value and # of shares.

11–11

1. The three major forms of business organizations are the sole

proprietorship, the partnership, and the corporation.

2. The sole proprietorship is formed when an individual decides to

3. The partnership agreement is a legal agreement that defines the

responsibilities of each partner and specifies the division of profits

4. The phrase separate legal entity simply means that the business

5. The articles of incorporation constitute a legal document that is filed

with the appropriate state agency requesting the official formation of

11–12

6. The stock certificate is issued as evidence of ownership in a

7. The stock market crash of 1929 and the subsequent economic

depression led to the passage of the Securities and Exchange Acts of

8. The corporate form of business has both advantages and

(1) Limited liability. Owners are not held personally responsible for

(2) Continuity of existence. Corporations do not cease to exist when

(3) Free transferability of ownership interest. An owner can readily

(4) Ease of raising capital. It is generally easier to attract many small

(1) Regulation. Corporations are subject to considerably more

regulation, both state and federal, than are sole proprietorships and

(2) Double taxation. The most important disadvantage of the

11–13

distributions are not deductible for the corporation and are taxable

9. The limited liability company is a relatively new organizational form

in the United States and operates similar to a sole proprietorship or

10. The term double taxation as it refers to a corporation means that

earnings are taxed at both the corporate level and the shareholder

level when earnings are distributed in the form of dividends. For

11. Contributed capital is the capital that is acquired by the corporation

from owners of the corporation. For example, the sale of stock to an

12. For both sole proprietorships and partnerships, contributed capital

and accumulated earnings less withdrawals are combined in one

13. Because corporations can be owned by millions of individuals, they

11–14

access to billions of dollars of capital. Proprietorships and

14. a. Legal capital: Par value multiplied by the number of

shares issued. This represents the minimum amount of

assets that should be maintained as a protection for

creditors.

b. Par value of stock: An arbitrary value that is assigned to a

11–15

j. Common stock: A class of stock that possesses certain rights

usually not given to other classes of stock. These rights include

the right to share in the distribution of profits, the right to share

15. Cumulative preferred stock: A class of preferred stock for which the

stipulated dividend, if not paid, accumulates from one year to the

next. If a corporation does not pay a dividend one year, the unpaid

16. No-par stock is stock for which a par value has not been established

by the corporation. No-par stock may have a stated value. If so,

17. Dividend per share: $100 par x 10% = $10 per share. The total

11–16

18. The amount credited to the common stock account is equal to par

19. Par value and stated value are similar in meaning in that they are

20. A company will repurchase its own stock for a number of reasons.

Some of the most common reasons include: (1) to reduce the

trading.

21. The purchase of treasury stock decreases total equity by debiting the

22. Even though the stock was purchased for $30 per share and resold

for $35 per share, there is no gain on the sale. A company can not

23. The declaration date is the date the dividend is officially declared by

the corporation’s board of directors. The declaration of the dividend

24. A stock dividend may be declared to give the shareholders some

11–17

them. The stock dividend will give each shareholder additional

shares in proportion to their stock ownership. After the stock

dividend, each shareholder owns exactly the same proportion of the

25. A stock dividend is declared either to compensate shareholders when

26. The primary reason for declaring a stock split is to reduce the market

27. In a stock split, the number of shares are increased according to the

amount of the split and the par is reduced proportionately. In a five-

28. When retained earnings are appropriated, cash in the same amount

29. Equity financing (i.e., capital acquired from owners) is the largest

30. Equity financing refers to capital acquired from owners; usually the

payable.

11–18

31. A widely held corporation is one in which the stock is held by a large

32. In deciding whether to declare dividends, the board of directors must

consider whether the corporation has sufficient cash to cover

11–19

SOLUTIONS TO EXERCISES – SERIES A – CHAPTER 11

EXERCISE 11-1A

Transactions

Cash Acquired from Owner

$60,000

Revenues

35,300

Expenses

16,200

Withdrawal

1,000

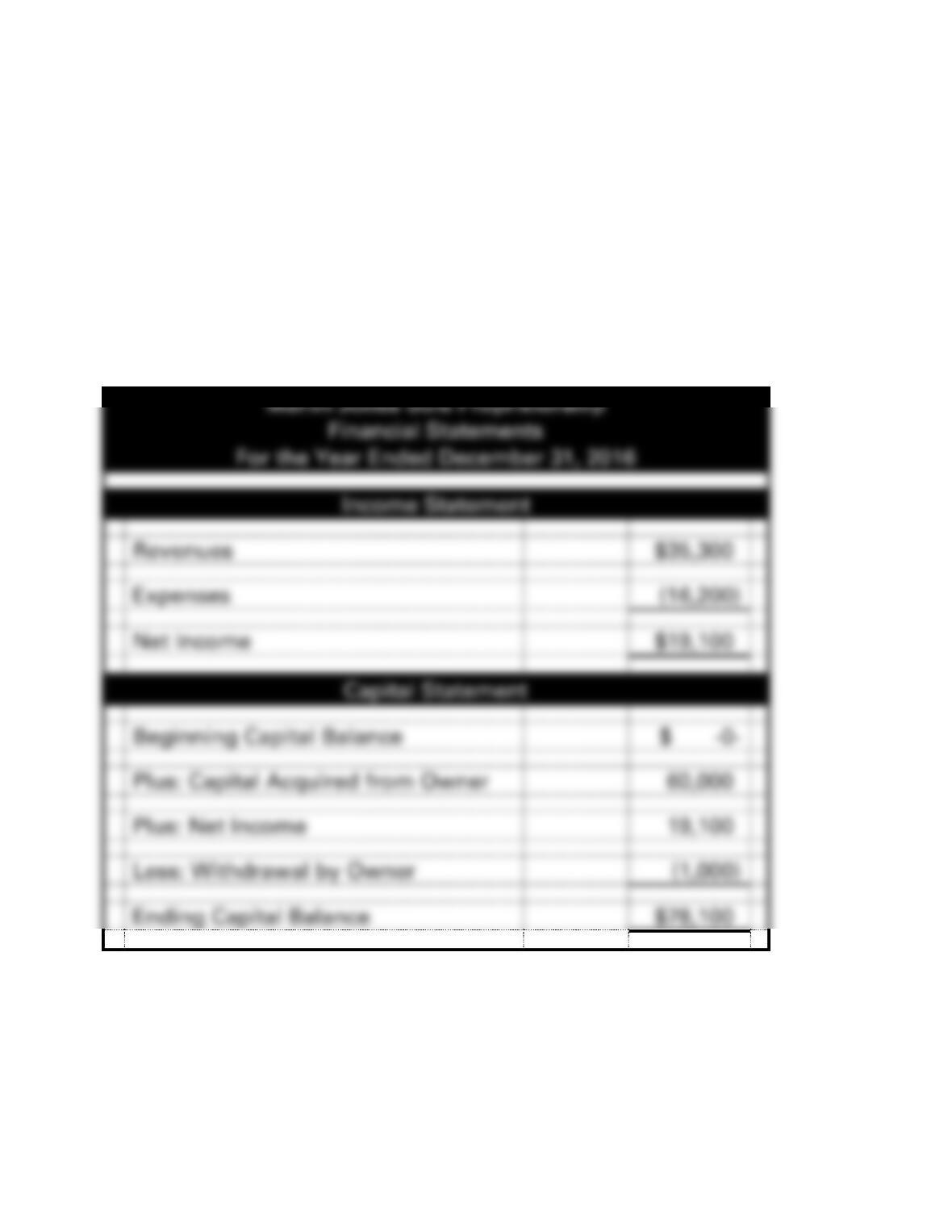

Marlin Jones Sole Proprietorship

Financial Statements

For the Year Ended December 31, 2016

Income Statement

Revenues

$35,300

Expenses

(16,200)

Net Income

$19,100

Capital Statement

Beginning Capital Balance

$ -0-

Plus: Capital Acquired from Owner

60,000

Plus: Net Income

19,100

Less: Withdrawal by Owner

(1,000)

Ending Capital Balance

$78,100

11–20

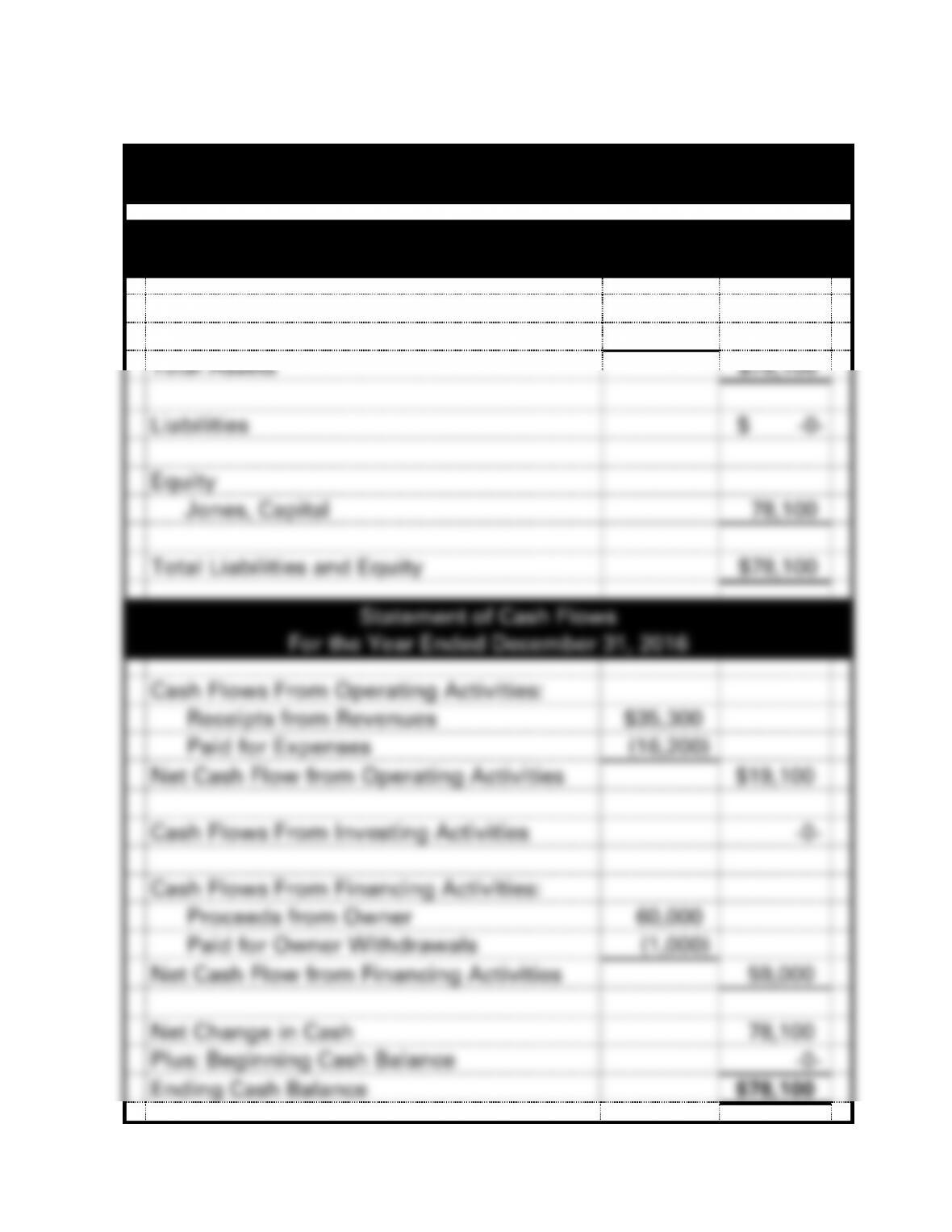

EXERCISE 11-1A (cont.)

Marlin Jones Sole Proprietorship

Financial Statements

Balance Sheet

As of December 31, 2016

Assets

Cash

$78,100

Total Assets

$78,100

Liabilities

$ -0-

Equity

Jones, Capital

78,100

Total Liabilities and Equity

$78,100

Statement of Cash Flows

For the Year Ended December 31, 2016

Cash Flows From Operating Activities:

Receipts from Revenues

$35,300

Paid for Expenses

(16,200)

Net Cash Flow from Operating Activities

$19,100

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities:

Proceeds from Owner

60,000

Paid for Owner Withdrawals

(1,000)

Net Cash Flow from Financing Activities

59,000

Net Change in Cash

78,100

Plus: Beginning Cash Balance

-0-

Ending Cash Balance

$78,100

11–21

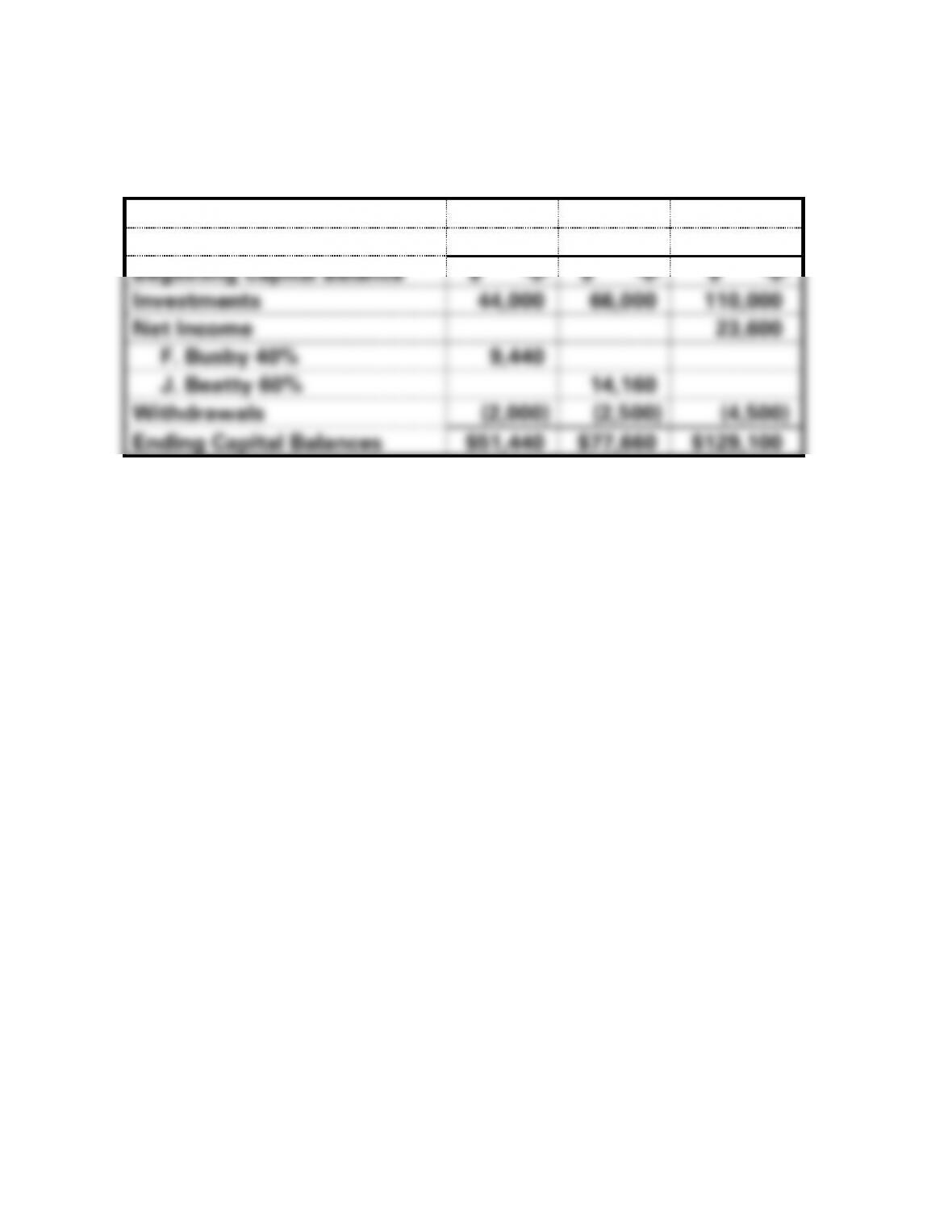

EXERCISE 11-2A

Transactions:

Cash Contributions

F. Busby

$44,000

40%

J. Beatty

66,000

60%

Total

$110,000

100%

Revenues

$42,000

Expenses

18,400

Busby, Withdrawal

2,000

Beatty, Withdrawal

2,500

11–23

EXERCISE 11-2A (cont.)

Prepared for the instructor’s use:

Analysis of Capital Accounts:

Busby

Beatty

Total

Beginning Capital Balance

$ -0-

$ -0-

$ -0-

Investments

44,000

66,000

110,000

Net Income

23,600

F. Busby 40%

9,440

J. Beatty 60%

14,160

Withdrawals

(2,000)

(2,500)

(4,500)

Ending Capital Balances

$51,440

$77,660

$129,100