2-12

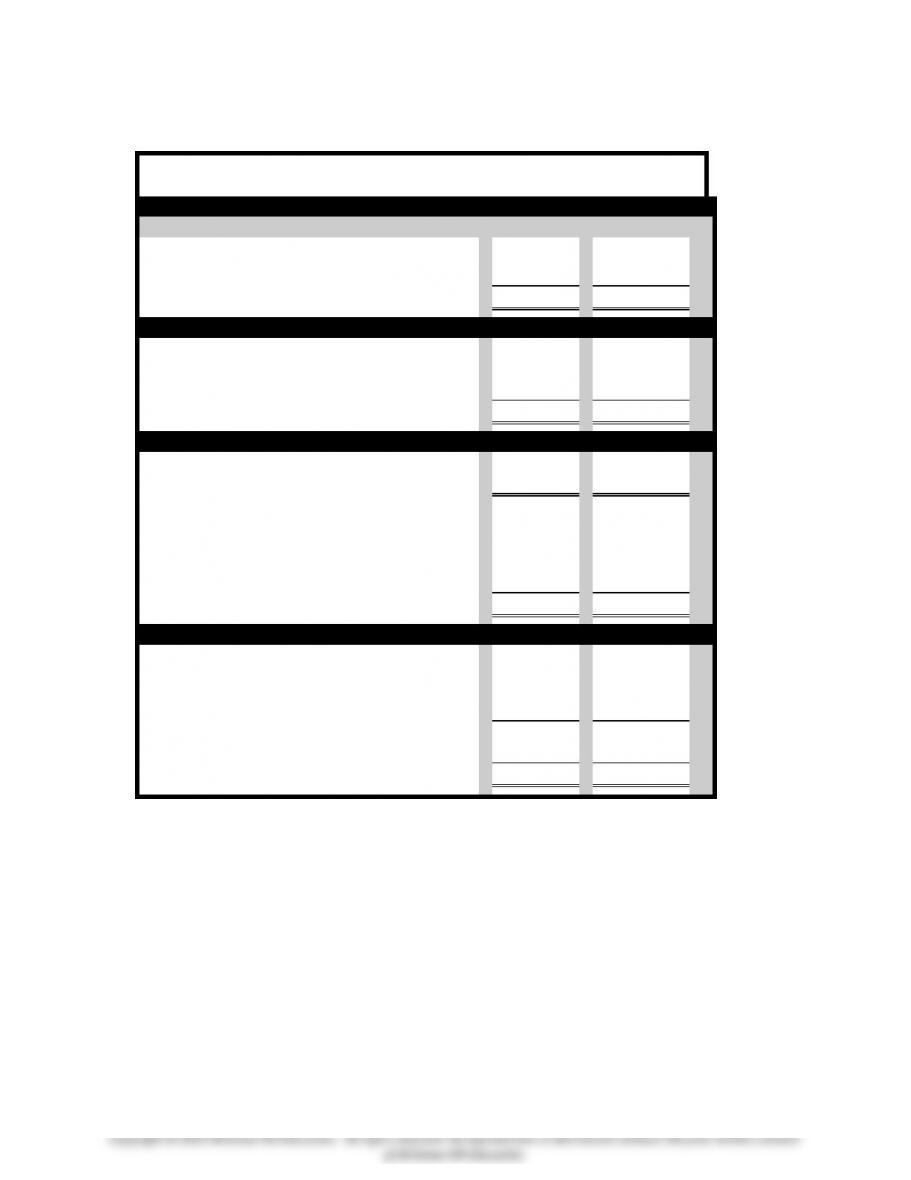

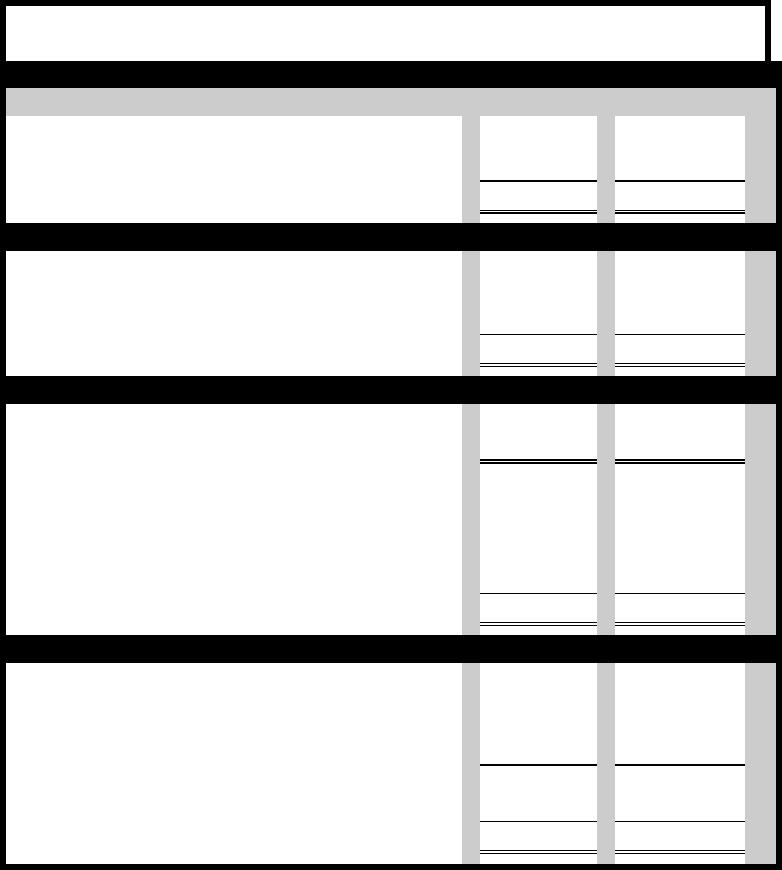

Demonstration Problem 2-1B Solution, part 2. Financial Statements

Jackson Legal Services

Financial Statements

Income Statements

For the Years Ended December 31,

2014

2015

Fees revenue

$ 3,000

$ 9,000

Expenses

0

0

Net income

$ 3,000

$ 9,000

Statements of Retained Earnings

Beginning retained earnings

$ 0

$ 3,000

Plus: Net income

3,000

9,000

Less: Dividends

0

0

Ending retained earnings

$ 3,000

$12,000

Balance Sheets as of December 31

Assets

Cash

$12,000

$12,000

Liabilities

Unearned revenue

$ 9,000

$ 0

Equity

Retained earnings

3,000

12,000

Total liabilities and equity

$12,000

$12,000

Statements of Cash Flows

Cash flows from operating activities

$12,000

$ 0

Cash flows from investing activities

0

0

Cash flows from financing activities

0

0

Net change in cash

12,000

0

Beginning cash balance

0

12,000

Ending cash balance

$12,000

$12,000

2-13

Demonstration Problem 2-2 Solution, part A. Horizontal Financial Statements Model for 2014

A spreadsheet is embedded to reflect the solution to this question. This spreadsheet covers both 2014

and 2015. The workpaper for students’ use in answering this question would basically be the solution with

the amounts deleted for all events except for the 2014 beginning balance.

Worksheet Edmonds

FFAC8e Ch 2 IM.xls

2-14

Demonstration Problem 2-2 Solution, part B. Horizontal Financial Statements Model for 2015

2-15

Demonstration Problem 2-2 Solution, parts A & B. Financial Statements

Income Statements for the Years Ended 12/31

2014

2015

Consulting revenue

$ 1,980

$ 5,100

Total revenue

1,980

5,100

Salary expense

(900)

(1,500)

Insurance Expense

(300)

(410)

Net income

780

$ 3,190

Statements of Changes in Stockholders’ Equity

Beginning common stock

$ 0

$ 2,000

Plus: Common stock issued

2,000

3,000

Ending common stock

2,000

5,000

Beginning retained earnings

0

680

Plus: Net income

780

3,190

Less: Dividends

(100)

(300)

Ending retained earnings

680

2,890

Total stockholders’ equity

$ 2,680

$ 8,570

Balance Sheets as of December 31

Cash

$ 4,920

$ 8,650

Accounts receivable

300

200

Prepaid Insurance

60

70

Total assets

$ 5,280

$ 8,920

Salaries payable

$ 200

$ 350

Unearned Revenue

2,400

0

Total liabilities

2,600

350

Common stock

2,000

5,000

Retained earnings

680

3,570

Total stockholders’ equity

2,680

8,570

Total liabilities and stockholders’ equity

$ 5,280

$ 8,920

Statements of Cash Flows

Cash flows from operating activities

Cash receipts from consulting revenue

$ 4,080

$ 2,800

Cash payments for salaries

(700)

(1,350)

Cash payments for insurance

(360)

(420)

Net cash inflow from operating activities

3,020

1,030

Cash flows from investing activities

Net cash outflow for investing activities

0

0

Cash flows from financing activities

Cash receipt from common stock issue

2,000

3,000

Cash payment for dividends

(100)

(300)

Net cash inflow from financing activities

1,900

2,700

Net change in cash

4,920

3,730

Beginning cash balance

0

4,920

Ending cash balance

$ 4,920

$ 8,650

2-16

Demonstration Problem 2-1 Workpaper, part 1.

Assets

=

Liabilities

+

Equity

Part A, 2014

Cash

+

Accounts

Receivable

=

Liabilities

+

Common

Stock

+

Retained

Earnings

Beginning balances

$ 0

$ 0

$ 0

$ 0

$ 0

Effect of recognizing reve-

nue

Part B, 2015

Effect of collecting cash

─────

─────

─────

─────

─────

Ending balances

$5,000

+

$ 0

=

$ 0

+

$ 0

+

$5,000

═════

════

═════

═════

═════

Demonstration Problem 2-1 Workpaper, part 2. Financial Statements

Packard Consultants

Income Statements

For the Years Ended December 31,

2014

2015

Consulting revenue

$

$

Expenses

Net income

$ 5,000

$ 0

Statements of Retained Earnings

Beginning retained earnings

$ 0

$

Plus: Net income

Less: Dividends

Ending retained earnings

$5,000

$5,000

Balance Sheets at December 31

Assets

Cash

$

$

Accounts receivable

Total assets

$

$

Equity

Retained earnings

$5,000

$5,000

Statements of Cash Flows

Cash flows from operating activities

$

$

Cash flows from investing activities

0

0

Cash flows from financing activities

0

0

Net change in cash

Beginning cash balance

Ending cash balance

$ 0

$5,000

2-17

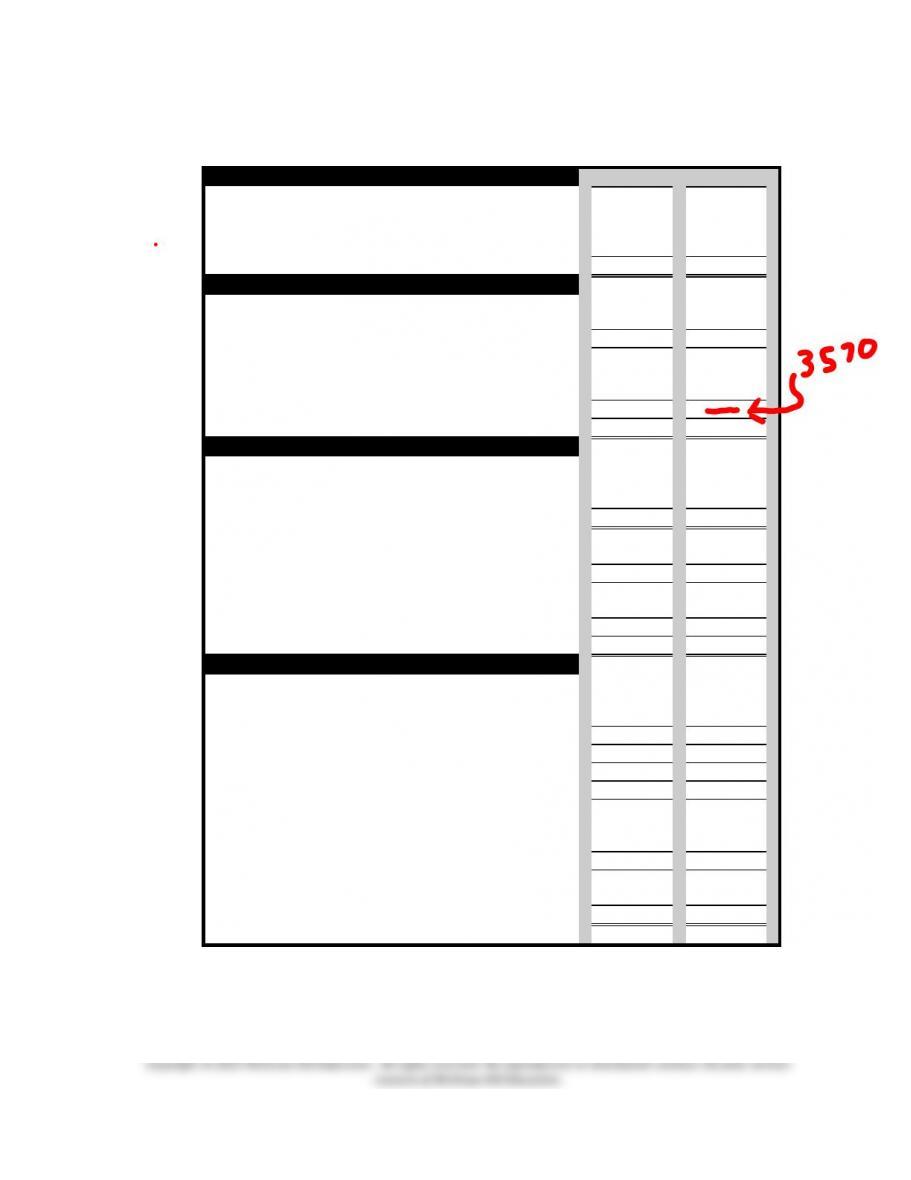

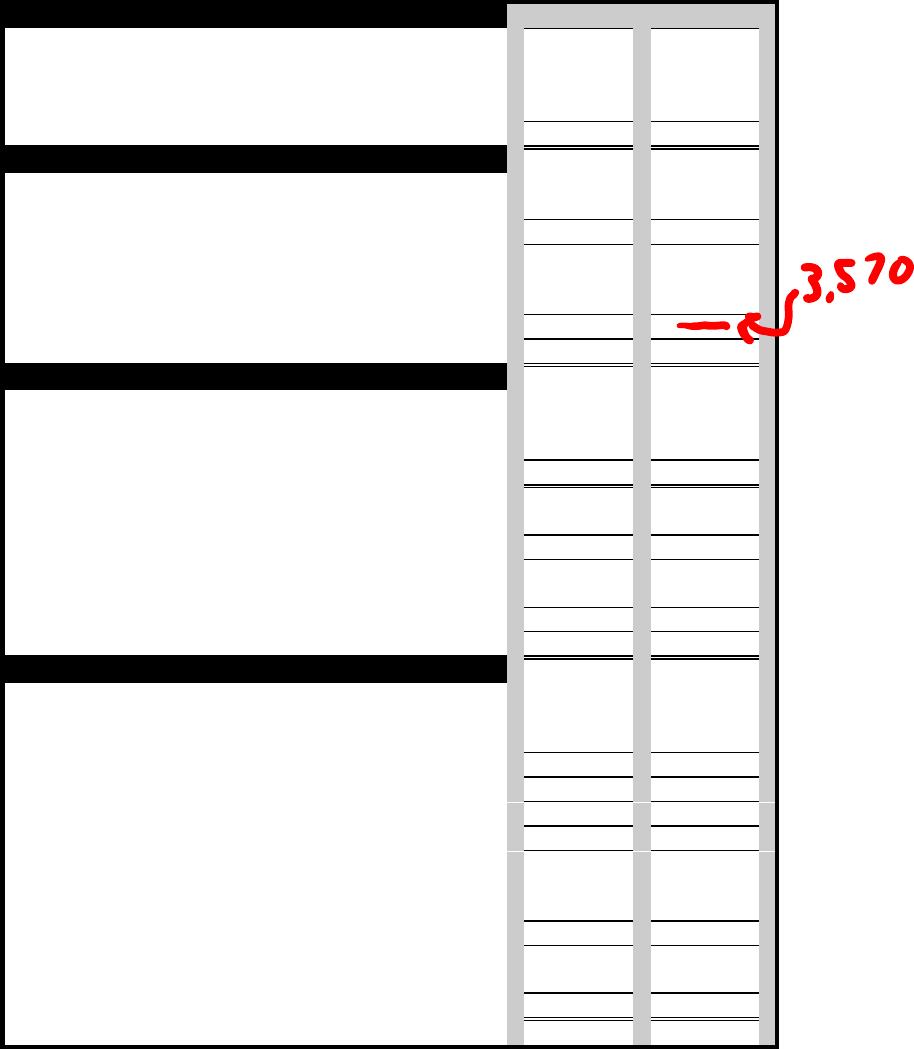

Demonstration Problem 2-1B Workpaper, part 2

Jackson Legal Services

Financial Statements

Income Statements

For the Years Ended December 31,

2014

2015

Fees revenue

Expenses

Net income

$ 3,000

$ 9,000

Statements of Retained Earnings

Beginning retained earnings

$ 0

$ 3,000

Plus: Net income

Less: Dividends

Ending retained earnings

$ 3,000

$12,000

Balance Sheets as of December 31

Assets

Cash

Liabilities

Unearned revenue

Equity

Retained earnings

3,000

12,000

Total liabilities and equity

Statements of Cash Flows

Cash flows from operating activities

Cash flows from investing activities

Cash flows from financing activities

Net change in cash

Beginning cash balance

0

Ending cash balance

$12,000

$12,000

2-18

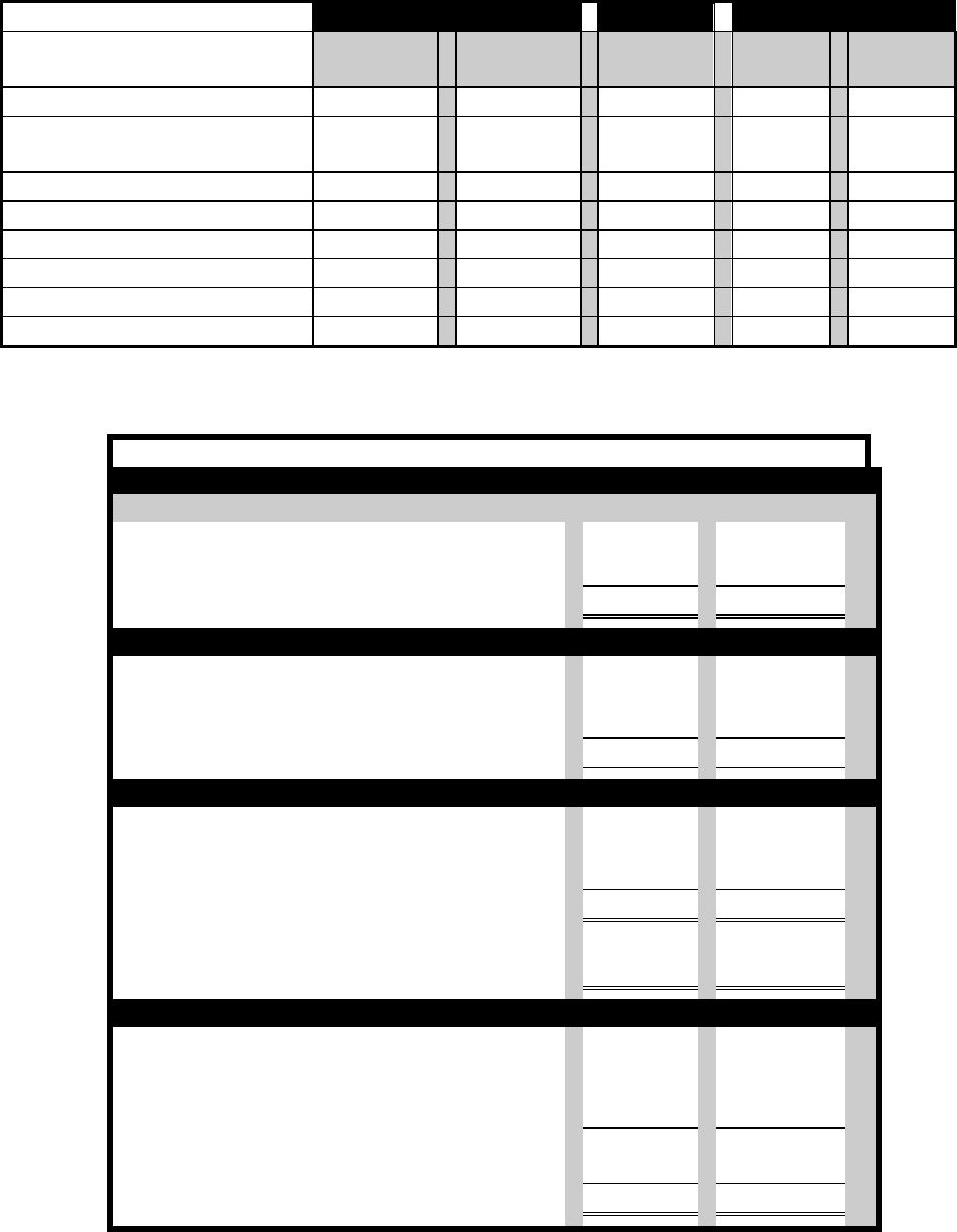

Demonstration Problem 2-2 Workpaper, parts A & B. Financial Statements

Income Statements for the Years Ended 12/31

2014

2015

Consulting revenue

$

$

Total revenue

Salary expense

Insurance Expense

Net income

780

$ 3,190

Statements of Changes in Stockholders’ Equity

Beginning common stock

$

$

Plus: Common stock issued

Ending common stock

2,000

5,000

Beginning retained earnings

Plus: Net income

Less: Dividends

Ending retained earnings

680

2,890

Total stockholders’ equity

$

$

Balance Sheets as of December 31

Cash

$

$

Accounts receivable

Prepaid Insurance

Total assets

$

Salaries payable

$

$

Unearned Income

Total liabilities

2,600

2,425

Common stock

Retained earnings

Total stockholders’ equity

Total liabilities and stockholders’ equity

$ 5,280

$10,980

Statements of Cash Flows

Cash flows from operating activities

Cash receipts from consulting revenue

$

$

Cash payments for salaries

Cash payments for insurance

Net cash inflow from operating activities

3,020

1,030

Cash flows from investing activities

Net cash outflow for investing activities

0

0

Cash flows from financing activities

Cash receipt from common stock issue

Cash payment for dividends

Net cash inflow from financing activities

1,900

2,700

Net change in cash

Beginning cash balance

Ending cash balance

$ 4,920

$ 8,650

2-19

Quiz Questions for Chapter 2

1. X Company recognized $500 of revenue on account and realized $400 of cash collections. The

company had accrued salary expense of $300 and invested $200 in a certificate of deposit. Based on

this information alone, the amount of cash flow from operating activities would be

a. $100.

b. $500.

c. $200.

d. $400.

2. On January 1, 2012, West Company had accounts receivable of $500. During 2014 West earned

$2,500 of service revenue on account. If the accounts receivable balance as of December 31, 2014,

was $400, what was the amount of cash flow from operating activities?

a. $2,000.

b. $3,000.

c. $2,400.

d. $2,600.

3. The entry to record revenue on account

a. increases liabilities.

b. decreases equity.

c. decreases assets.

d. none of the above.

4. K Company collected $500 cash on an account receivable that was due from L Company. Based on

this information, which of the following statements is true?

a. K Company’s total assets would increase.

b. L Company’s total assets would not change.

c. K Company’s equity would decrease.

d. None of the above.

5. On April 1, Flavin Co. paid $12,000 cash for an insurance policy that provides coverage for one year

beginning immediately. On December 31, Flavin adjusted the books to recognize the amount of the

insurance policy used during the year. The amount of the adjustment would be:

a. $8,000

b. $9,000

c. $12,000

d. $0

6. Which of the following illustrates the recognition of revenue earned on account?

Balance Sheet

Income Statement

Statement of

Assets

=

Liab.

+

Equity

Rev.

─

Exp.

=

Net Inc.

Cash Flow

a.

+

NA

+

NA

NA

NA

NA

b.

+

NA

+

+

NA

+

NA

c.

─

NA

─

NA

+

─

─ OA

d.

+

NA

+

+

NA

+

+ OA

2-20

Use the following information to answer the next two questions. BBC Company received $9,900 cash

on February 1, 2014, from XYZ Company as advance payment for services BBC promised to perform for

XYZ over the next three years on a continuous basis. Assume that BBC Company’s year-end is December

31.

7. On its 2014 income statement, BBC would report revenue of

a. $3,300

b. $9,900

c. $3,025

d. $2,750

8. On its December 31, 2015 balance sheet BBC would report liabilities of

a. $3,575

b. $3,300

c. $9,900

d. $6,875

9. Which of the following illustrates purchasing supplies on account?

Balance Sheet

Income Statement

Statement of

Assets

=

Liab.

+

Equity

Rev.

─

Exp.

=

Net Inc.

Cash Flow

a.

+

NA

+

NA

NA

NA

NA

b.

+

+

NA

NA

NA

NA

NA

c.

+

+

NA

NA

NA

NA

+ OA

d.

+

NA

+

+

NA

+

+ OA

10. Which of the following illustrates receiving cash as an advance payment for future services?

Balance Sheet

Income Statement

Statement of

Assets

=

Liab.

+

Equity

Rev.

─

Exp.

=

Net Inc.

Cash Flow

a.

+

NA

+

NA

NA

NA

NA

b.

+

+

NA

+

NA

+

NA

c.

+

+

NA

NA

NA

NA

+ OA

d.

+

NA

+

+

NA

+

+ OA

2-21

Quiz Answers

Question

Answer

1

D

2

D

3

D

4

B

5

B

6

B

7

C

8

A

9

B

10

C

2-22

Summary Outline of a Lesson Plan for Chapter 2

I. Use Demonstration Problem 2-1 to define and illustrate the concept of accrual

accounting. This problem includes both an accrual (part A) and a deferral (part B) exam-

ple.

II. Use separate examples to further illustrate accrual and deferral concepts.

III. Use Demonstration Problem 2-2 as a comprehensive summary problem. Ex-

plain the first cycle to the class and use the second cycle as an in-class assignment. Allot

one hour for this assignment. Have slower students finish the problem as homework. Use

parallel problem 2-38 in the textbook as a homework assignment.

IV. Time considerations and homework assignments. Demonstration Problems 2-1

and 2-2 require approximately one hour of class time. Consider assigning exercises 2-11,

2-15, 2-18, 2-21, and Problem 2-28 from the textbook as homework.

V. Use a financial statements model to highlight the differences between accrual

and cash basis accounting.

VI. Hand out official answers to the Demonstration Problems worked in class.