7-86

PROBLEM 7-26A a. (cont.)

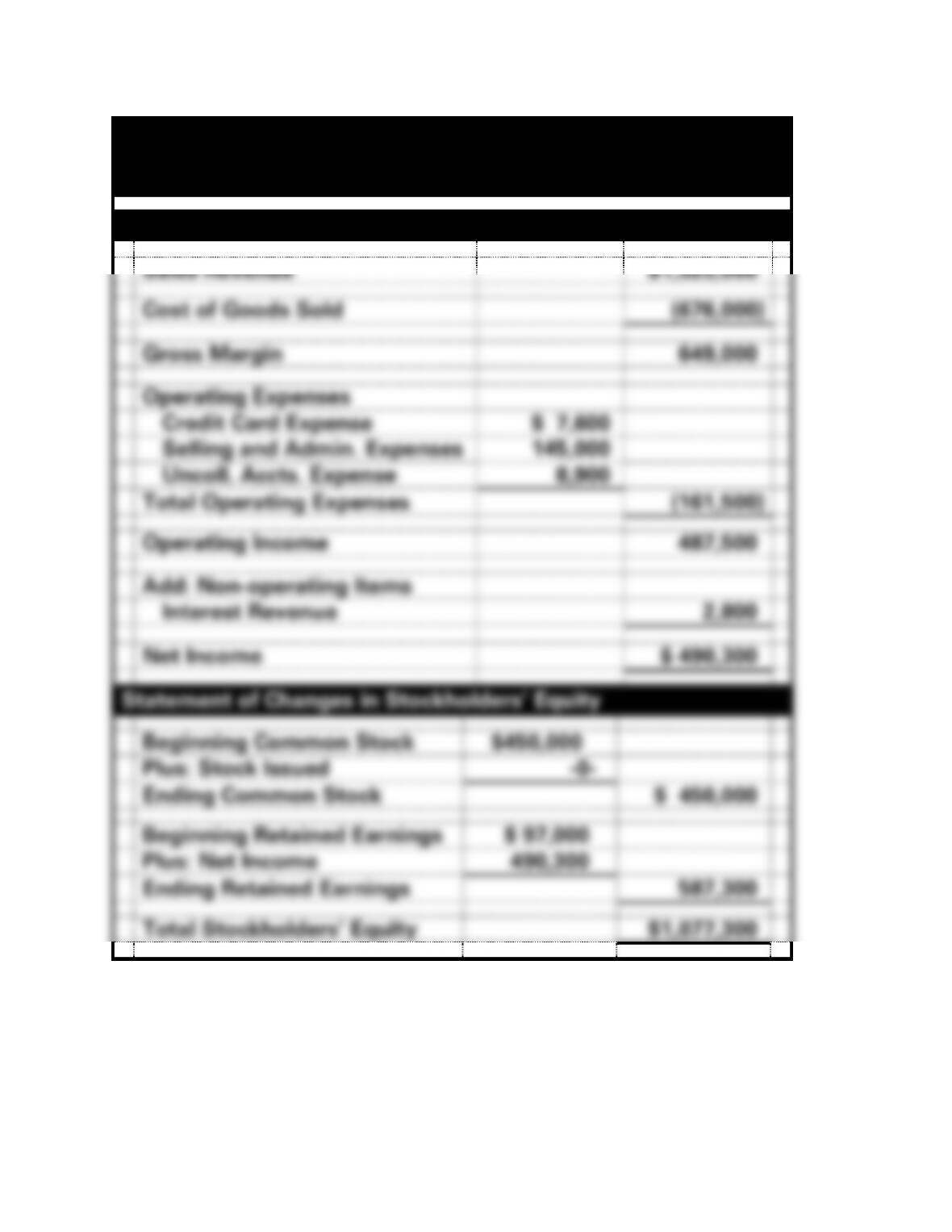

Tile, Etc., Inc.

Financial Statements

For the Year Ended December 31, 2017

Income Statement

Sales Revenue

$1,325,000

Cost of Goods Sold

(676,000)

Gross Margin

649,000

Operating Expenses

Credit Card Expense

$ 7,600

Selling and Admin. Expenses

145,000

Uncoll. Accts. Expense

8,900

Total Operating Expenses

(161,500)

Operating Income

487,500

Add: Non-operating Items

Interest Revenue

2,800

Net Income

$ 490,300

Statement of Changes in Stockholders’ Equity

Beginning Common Stock

$450,000

Plus: Stock Issued

-0-

Ending Common Stock

$ 450,000

Beginning Retained Earnings

$ 97,000

Plus: Net Income

490,300

Ending Retained Earnings

587,300

Total Stockholders’ Equity

$1,077,300

7-87

PROBLEM 7-26A a. (cont.)

Tile, Etc., Inc.

Balance Sheet

As of December 31, 2017

Assets

Cash

$342,400

Accounts Receivable

$387,500

Less: Allowance for Doubtful Accounts

(19,400)

368,100

Merchandise Inventory

329,000

Interest Receivable

2,800

Notes Receivable

60,000

Total Assets

$1,102,300

Liabilities

Accounts Payable

$ 65,000

Total Liabilities

65,000

Stockholders’ Equity

Common Stock

$450,000

Retained Earnings

587,300

Total Stockholders’ Equity

1,037,300

Total Liabilities and Stockholders’ Equity

$1,102,300

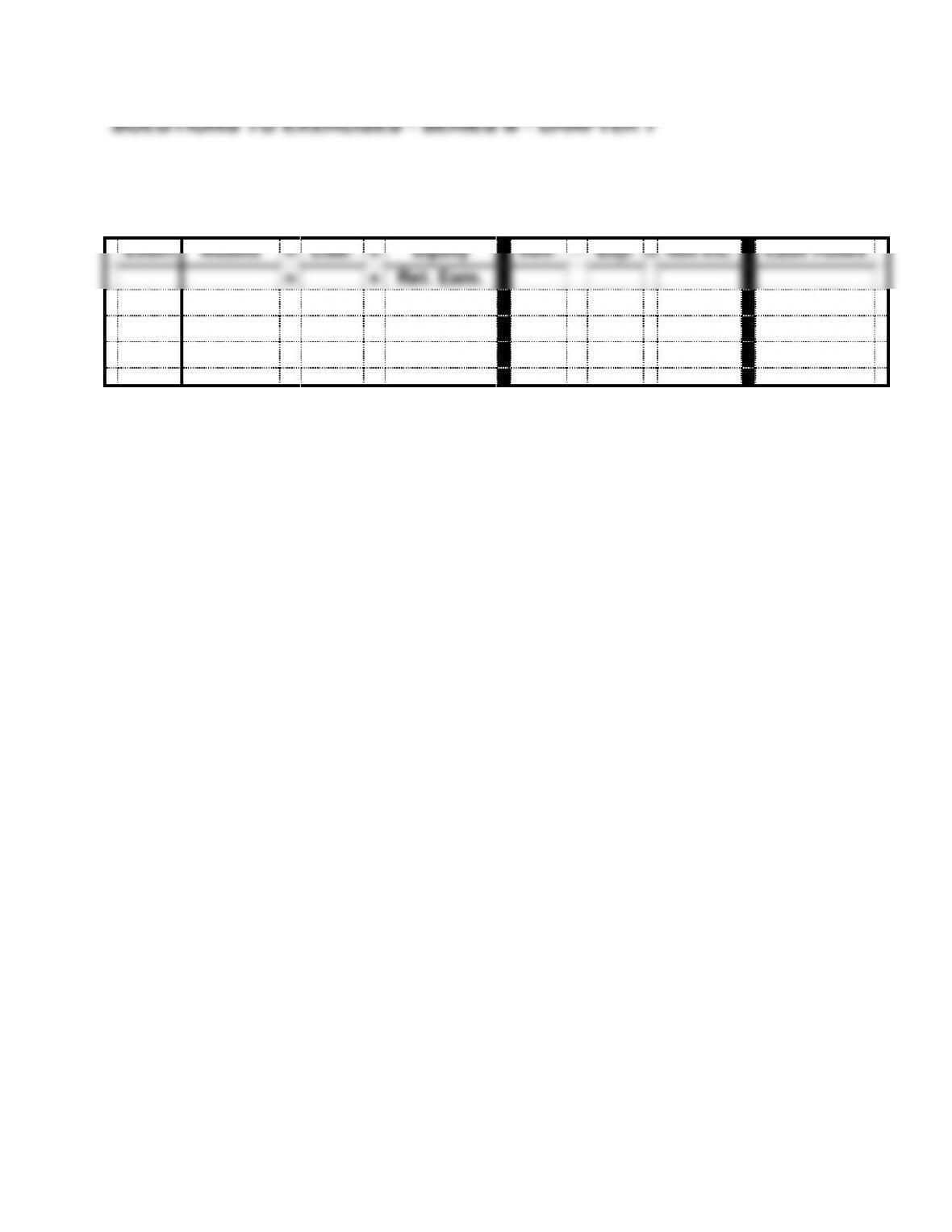

7-82

PROBLEM 7-26A a. (cont.)

Tile, Etc., Inc.

Statement of Cash Flows

For the Year Ended December 31, 2017

Cash Flows From Operating Activities:

Inflow from Customers*

$1,047,400

Outflow for Inventory

(610,000)

Outflow for Expenses

(145,000)

Net Cash Flow from Operating Activities

$292,400

Cash Flows From Investing Activities:

Outflow for Notes Receivable

$(60,000)

Net Cash Flow from Investing Activities

(60,000)

Cash Flows From Financing Activities

-0-

Net Change in Cash

232,400

Plus: Beginning Cash Balance

110,000

Ending Cash Balance

$342,400

7-83

ATC 7-1

All dollar amounts are in millions.

a. Note 6 on page 41 of the Form 10-K explains that the company sold its U.S.

7-84

ATC 7-2

a. (1)

Expo

White

Zina

Total Sales

$125,000

$210,000

$195,000

Cash Sales

85,000

26,000

120,000

Sales on Account

40,000

184,000

75,000

Accounts Receivable, 1/1/16

6,200

42,000

8,100

Accounts Receivable, 12/31/16

5,600

48,000

7,500

Allowance for Doubtful Acct, 1/1/16

186

1,840

405

Allowance for Doubtful Acct, 12/31/16

224

1,680

435

Uncoll. Accts. Expense, 2016

242

1,200

395

Uncollectible accounts charged off,

2015

204

1,360

365

Collections of accounts receivable,

2016

40,396

176,640

75,235

(2) Uncollectible Accounts

Expo – 2015: $186 $6,200 = .03 or 3%

(3) Sales on Account

(4) Accounts Receivable Turnover

Expo: $40,000 $5,600 = 7.14

87.6%.

7-85

ATC 7-2 (cont.)

d. Zina appears to be doing the best job of collecting it

accounts receivable with just .19% of its sales on account

7-86

ATC 7-3

a. The rather short collection period for Boeing will surprise many students. They

may suggest that Boeing collects its receivables soon after each airplane is

manufactured because it has been “made to order.” This, of course, is only

partly true. Boeing bills and collects payments from customers as their airplanes

7-87

ATC 7-4

a. Accounts receivable turnover:

2013: $7,146,079 ÷ $444,912 = 16.1 times

2012: $6,644,252 ÷ $461,383 = 14.4 times

7-88

ATC 7-5

a. Since AutoZone sells directly to consumers, it probably receives most of its

payments in cash or by credit card, so it collects the cash from its sales rather

quickly. Conversely, most of BorgWarner’s sales are to other businesses, and

7-89

ATC 7-6

a.

Factors Paul Smith should consider before allowing credit sales:

1. The cash flow – Can he finance his inventory while the

2. The cost of financing the inventory.

3. The creditworthiness of the customers.

4. Payment history of customers in his industry.

5. Additional business if he allows charge sales.

b. The memo should contain a discussion of the factors listed

above. It should also contain a discussion of the

7-90

ATC 7-7

a. Net income is artificially inflated because of the failure

to properly recognize bad debt expense when it became known

that some of the receivable balance was uncollectible. The

balance sheet is affected in two ways. First, retained

earnings and therefore stockholder’s equity are overstated.

receivable. He knows that the accounts receivable balance

have become impaired but would be deceiving the bank in

order to obtain the loan he needed. This deception by

deliberate omission of important facts would constitute

fraud.

c. The three elements of the fraud triangle are:

known (secret) information that if known by the bank would

preclude him from getting the loan he needs.

The capacity for rationalization—Saunders’ company is

thriving, therefore, he has every reason to believe that

repayment of the loan will not be a problem. He further

7-91

ATC 7–7 (cont.)

revenues must be realized or realizable to be recognized. Since

7-92

ATC 7-8

This solution is based on the companies’ From10-K for their 2013 fiscal year, and dollar

amounts are in thousands. (Whirlpool reports in millions, but their numbers have been

converted to thousands.)

Whirlpool Corporation

for 2013. Accounts receivable is the sum of “Accounts receivable” of $52,919

and “Accounts receivable–affiliates” of $284. The allowances for doubtful

accounts for these two sources of receivables were $24,318 and $-0-

7-93

ATC 7-8 – continued

e. Whirlpool sells appliances to dealers, who in turn sell them

to customers. Whirlpool must allow the

dealers a reasonable time to sell these

7-94

EXERCISE 7-1B

Event

Assets

=

Liab.

+

Equity

Rev.

–

Exp.

=

Net Inc.

Cash Flows

=

+

Ret. Earn.

1.

+

=

NA

+

+

+

−

NA

=

+

NA

2.

+/−

=

NA

+

NA

NA

−

NA

=

NA

+ OA

3.

−

=

NA

+

−

NA

−

+

=

−

NA

7-95

EXERCISE 7-2B

a.

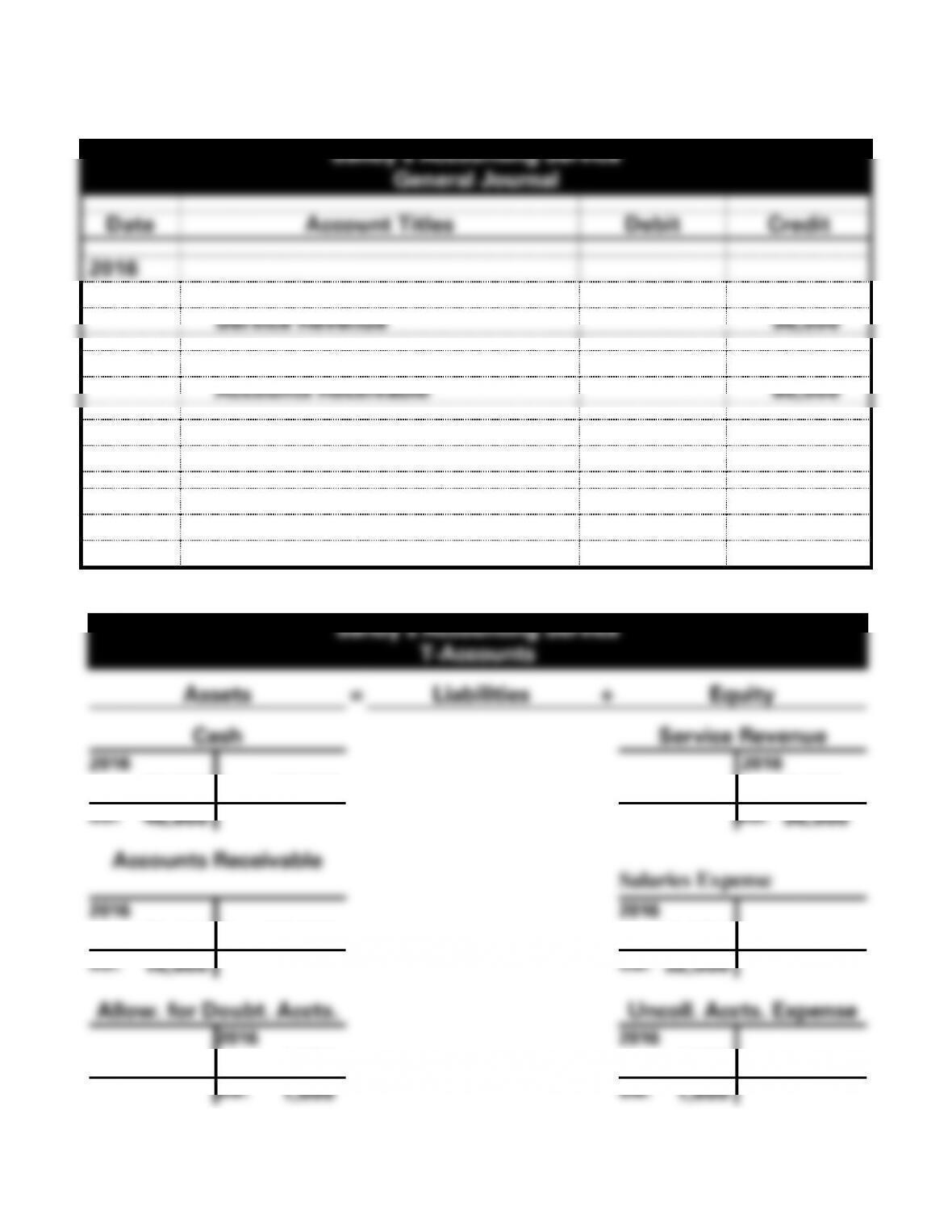

Sandy’s Accounting Service

General Journal

Date

Account Titles

Debit

Credit

2016

1.

Accounts Receivable

96,000

Service Revenue

96,000

2.

Cash

80,000

Accounts Receivable

80,000

3.

Salaries Expense

32,000

Cash

32,000

4.

Uncollectible Accounts Expense

1,600

Allowance for Doubtful Accounts

1,600

b.

Sandy’s Accounting Service

T-Accounts

Assets

=

Liabilities

+

Equity

Cash

Service Revenue

2016

2016

2.

80,000

3.

32,000

1.

96,000

Bal.

48,000

Bal.

96,000

Accounts Receivable

Salaries Expense

2016

2016

1.

96,000

2.

80,000

3.

32,000

Bal.

16,000

Bal.

32,000

Allow. for Doubt. Accts.

Uncoll. Accts. Expense

2016

2016

4.

1,600

4.

1,600

Bal.

1,600

Bal.

1,600

EXERCISE 7-2B (cont.)

c.

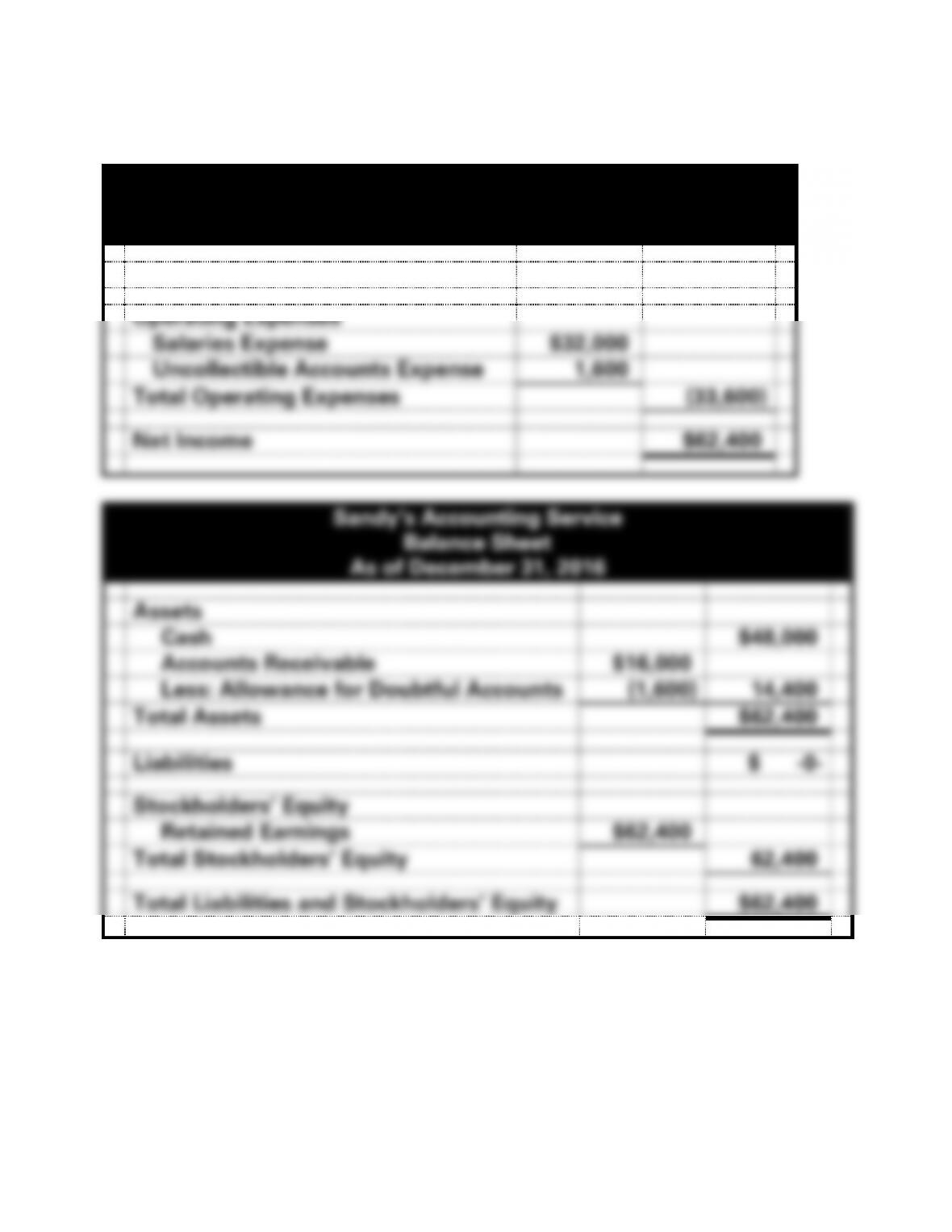

Sandy’s Accounting Service

Income Statement

For the Year Ended December 31, 2016

Service Revenue

$96,000

Operating Expenses

Salaries Expense

$32,000

Uncollectible Accounts Expense

1,600

Total Operating Expenses

(33,600)

Net Income

$62,400

Assets

Cash

$48,000

Accounts Receivable

Less: Allowance for Doubtful Accounts

Total Assets

$62,400

Liabilities

Retained Earnings

$62,400

$62,400

7-97

EXERCISE 7-2B c. (cont.)

Sandy’s Accounting Service

Statement of Cash Flows

For the Year Ended December 31, 2016

Cash Flows From Operating Activities:

Inflow from Customers

$80,000

Outflow for Expenses

(32,000)

Net Cash Flow from Operating Activities

$48,000

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities

-0-

Net Change in Cash

48,000

Plus: Beginning Cash Balance

-0-

Ending Cash Balance

$48,000

7-98

EXRECISE 7-3B

a. Analyze the Accounts Receivable account:

Accounts Receivable

Beginning Balance

$ 4,000

Plus: Revenue on Account

21,000

Less: Write-off

(180)

Less: Ending Balance

(4,500)

Collections of Accounts Rec.

$20,320

b. Analyze the Allowance for Doubtful Accounts account:

Allowance for Doubtful Accounts

Beginning Balance

$150

Less: Write-off

(180)

Less: Ending Balance

(250)

Uncollectible Accounts Expense

$280

format.

7-99

EXERCISE 7-4B

a. and c.

Reliable Auto Service

General Journal

Date

Account Titles

Debit

Credit

2016

1.

Accounts Receivable

45,000

Service Revenue

45,000

2.

Cash

32,000

Accounts Receivable

32,000

3.

Uncollectible Accounts Expense1

450

Allowance for Doubtful Accounts

450

4. cl

Service Revenue

45,000

Retained Earnings

45,000

5. cl

Retained Earnings

450

Uncollectible Accounts Exp.

450

2017

1.

Allowance for Doubtful Accounts

320

Accounts Receivable

320

2.

Accounts Receivable

65,000

Service Revenue

65,000

3.

Cash

66,000

Accounts Receivable

66,000

4.

Uncollectible Accounts Expense2

650

Allowance for Doubtful Accounts

650