4-115

EXERCISE 4-13B (cont.)

c. Net income decreased by 34%.

4-116

EXERCISE 4-14B

a.

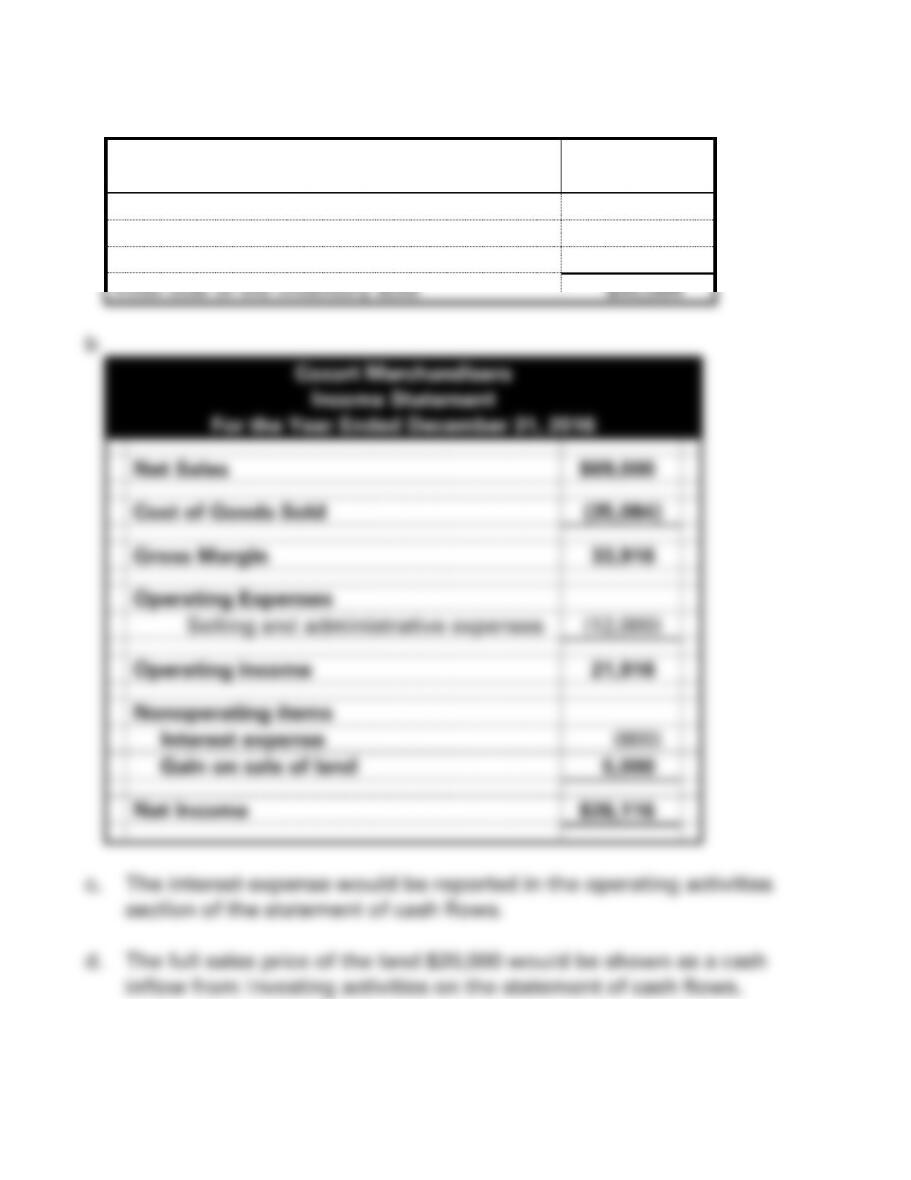

Cozart Merchandisers

Cost of inventory purchase

$40,000

Minus Purchase returns

(4,200)

Minus Purchase discounts ($35,800 x .02)

(716)

Total cost of the inventory sold

$35,084

4-117

e. A loss occurs from activities that are not part of the normal recurring

4-118

EXERCISE 4-15B

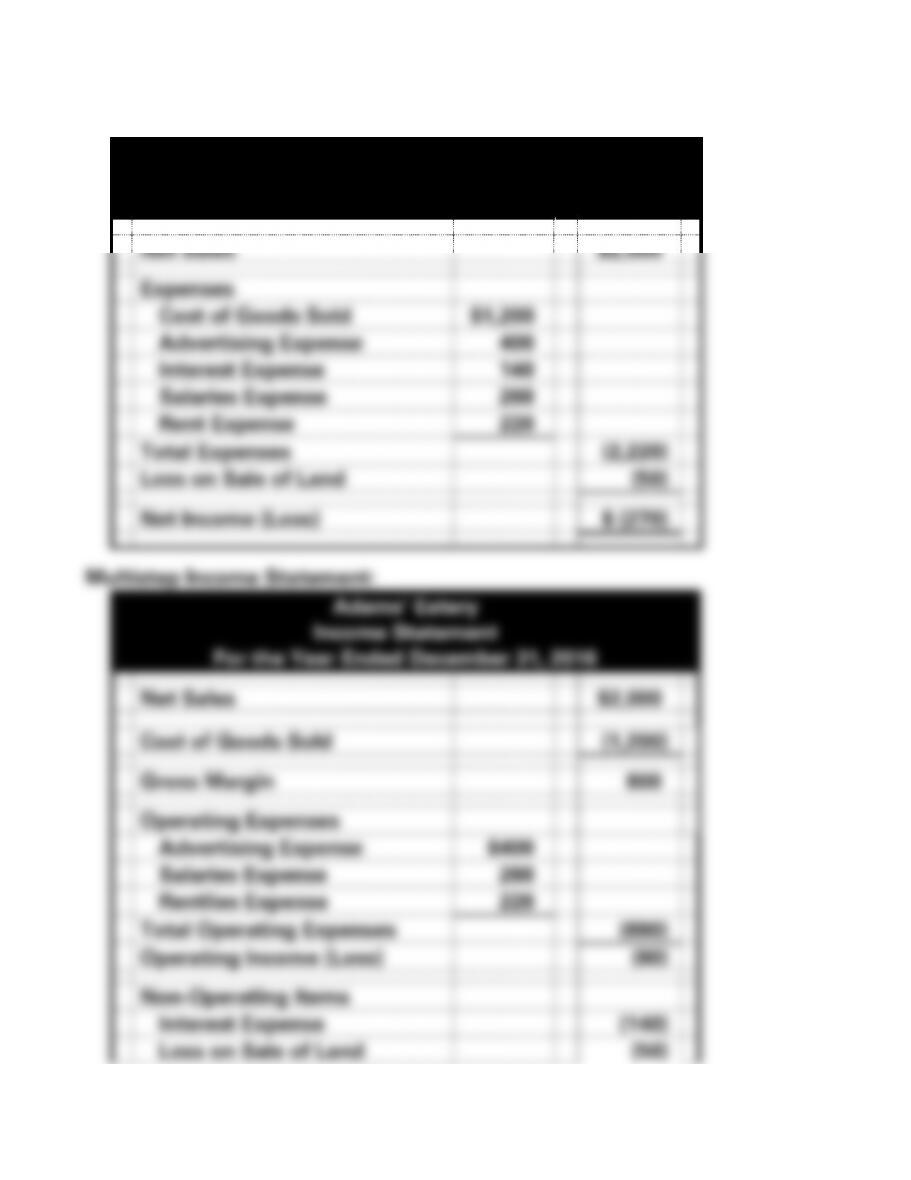

Single-Step Income Statement:

Adams’ Eatery

Income Statement

For the Year Ended December 31, 2016

Net Sales

$2,000

Expenses

Cost of Goods Sold

$1,200

Advertising Expense

400

Interest Expense

140

Salaries Expense

260

Rent Expense

220

Total Expenses

(2,220)

Loss on Sale of Land

(50)

Net Income (Loss)

$ (270)

Multistep Income Statement:

Adams’ Eatery

Income Statement

For the Year Ended December 31, 2016

Net Sales

$2,000

Cost of Goods Sold

(1,200)

Gross Margin

800

Operating Expenses

Advertising Expense

$400

Salaries Expense

260

Rentlies Expense

220

Total Operating Expenses

(880)

Operating Income (Loss)

(80)

Non-Operating Items

Interest Expense

(140)

Loss on Sale of Land

(50)

4-119

Net Income (Loss)

$ (270)

EXERCISE 4-16B

a.

Hollis Company

General Journal for 2016

Date

Account Titles

Debit

Credit

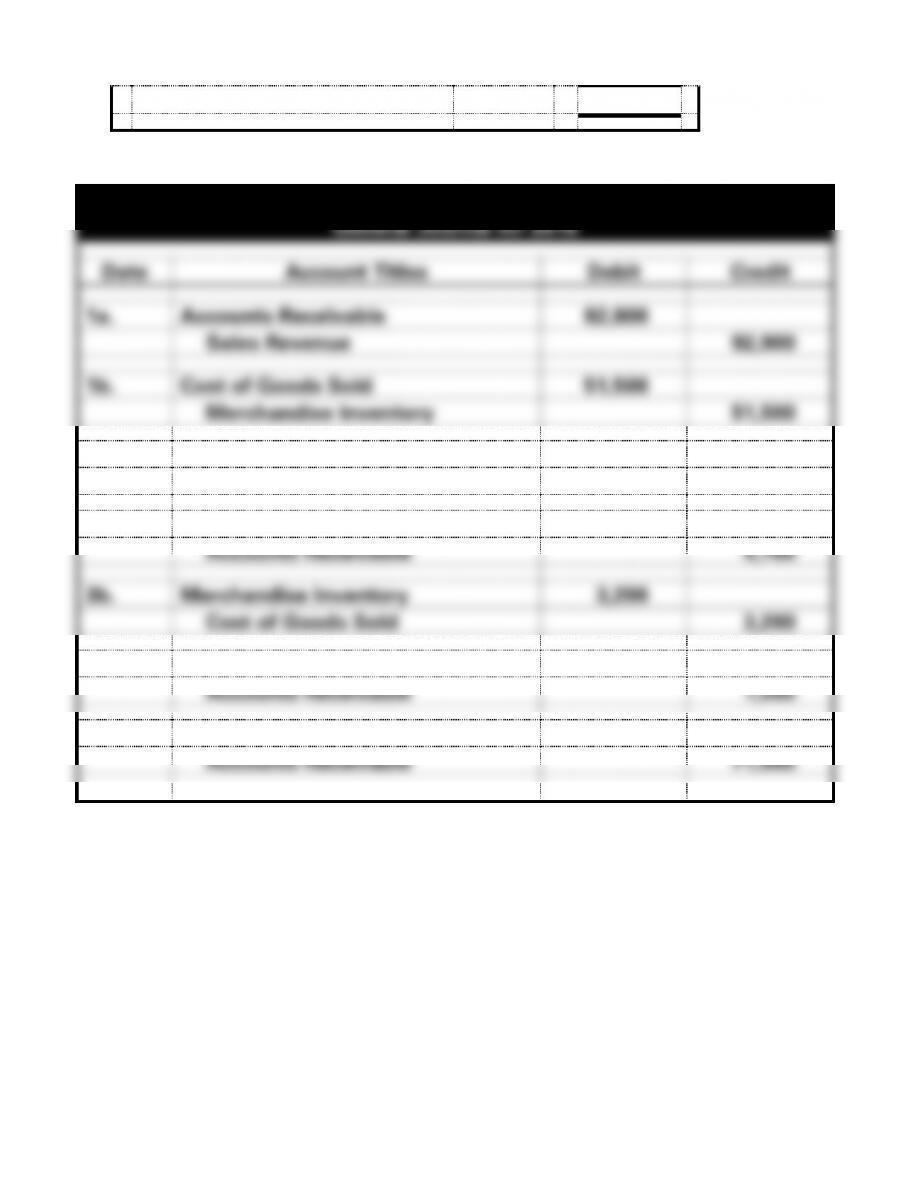

1a.

Accounts Receivable

92,900

Sales Revenue

92,900

1b.

Cost of Goods Sold

51,500

Merchandise Inventory

51,500

2.

Transportation-out

500

Cash

500

3a.

Sales Revenue

4,700

Accounts Receivable

4,700

3b.

Merchandise Inventory

3,200

Cost of Goods Sold

3,200

4.

Sales Revenue

1,500

Accounts Receivable

1,500

5.

Cash

71,000

Accounts Receivable

71,000

4-120

EXERCISE 4-16B (cont.)

b.

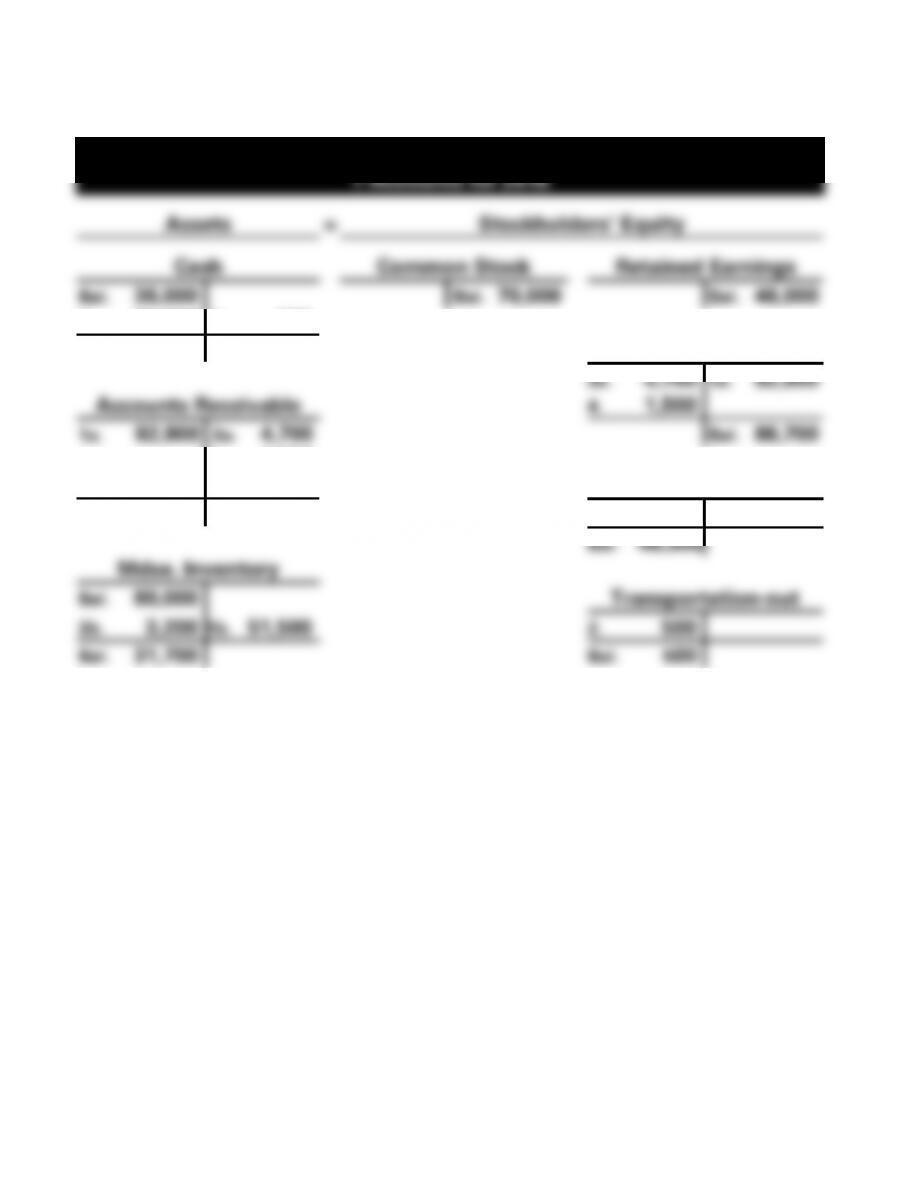

Hollis Company

T-Accounts for 2016

Assets

=

Stockholders’ Equity

Cash

Common Stock

Retained Earnings

Bal. 36,000

Bal. 70,000

Bal. 46,000

5. 71,000

2. 500

Bal. 106,500

Sales Revenue

3a. 4,700

1a. 92,900

Accounts Receivable

4. 1,500

1a. 92,900

3a. 4,700

Bal. 86,700

4. 1,500

5. 71,000

Cost of Goods Sold

Bal. 15,700

1b. 51,500

3b. 3,200

Bal. 48,300

Mdse. Inventory

Bal. 80,000

Transportation-out

3b. 3,200

1b. 51,500

2. 500

Bal. 31,700

Bal. 500

4-121

EXERCISE 4-16B (cont.)

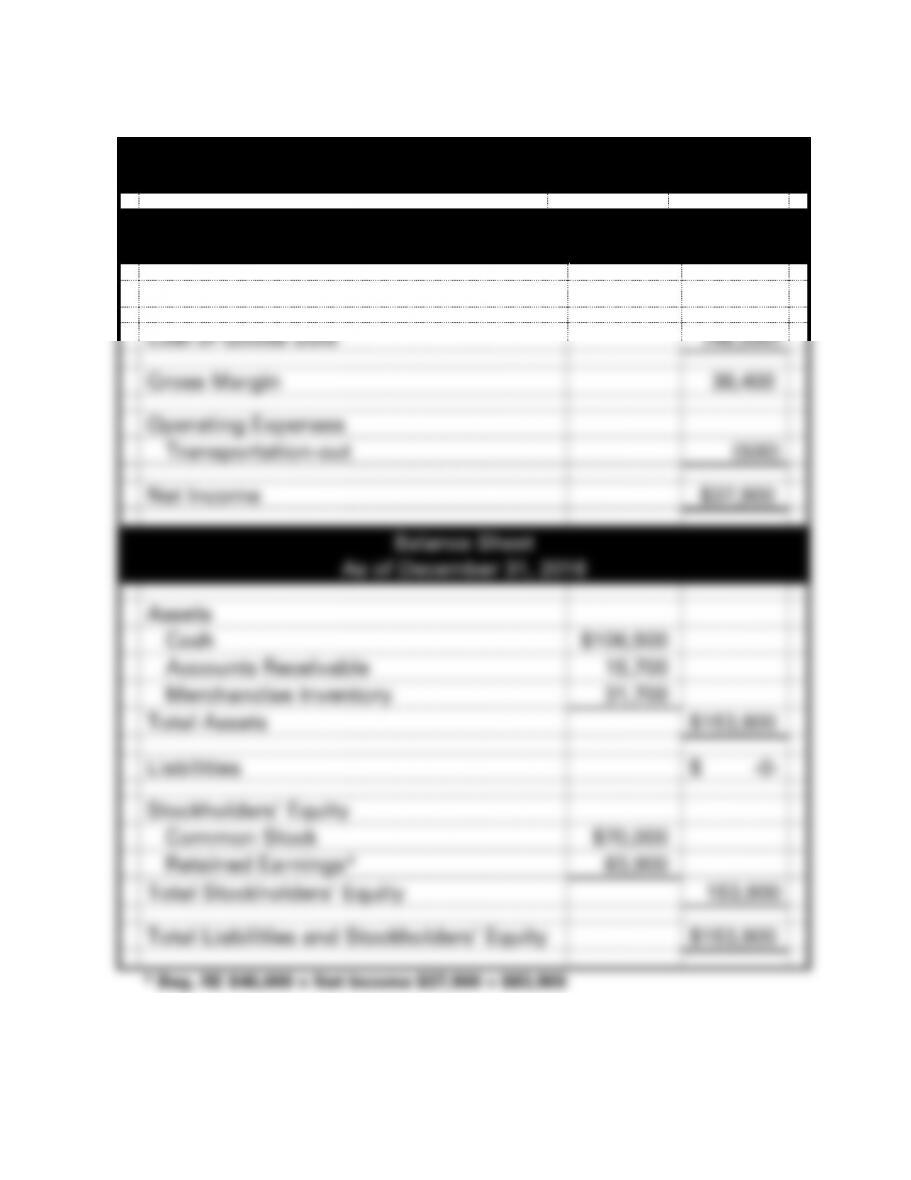

c.

Hollis Company

Financial Statements

Income Statement

For the Year Ended December 31, 2016

Net Sales

$86,700

Cost of Goods Sold

(48,300)

Gross Margin

38,400

Operating Expenses

Transportation-out

(500)

Net Income

$37,900

Balance Sheet

As of December 31, 2016

Assets

Cash

$106,500

Accounts Receivable

15,700

Merchandise Inventory

31,700

Total Assets

$153,900

Liabilities

$ -0-

Stockholders’ Equity

Common Stock

$70,000

Retained Earnings*

83,900

Total Stockholders’ Equity

153,900

Total Liabilities and Stockholders’ Equity

$153,900

4-122

EXERCISE 4-16B c. (cont.)

Hollis Company

Financial Statements

For the Year Ended December 31, 2016

Statement of Cash Flows

Cash Flows From Operating Activities:

Inflow from Customers

$71,000

Outflow for Expenses

(500)

Net Cash Flow from Operating Activities

$ 70,500

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities

-0-

Net Change in Cash

70,500

Plus: Beginning Cash Balance

36,000

Ending Cash Balance

$106,500

4-123

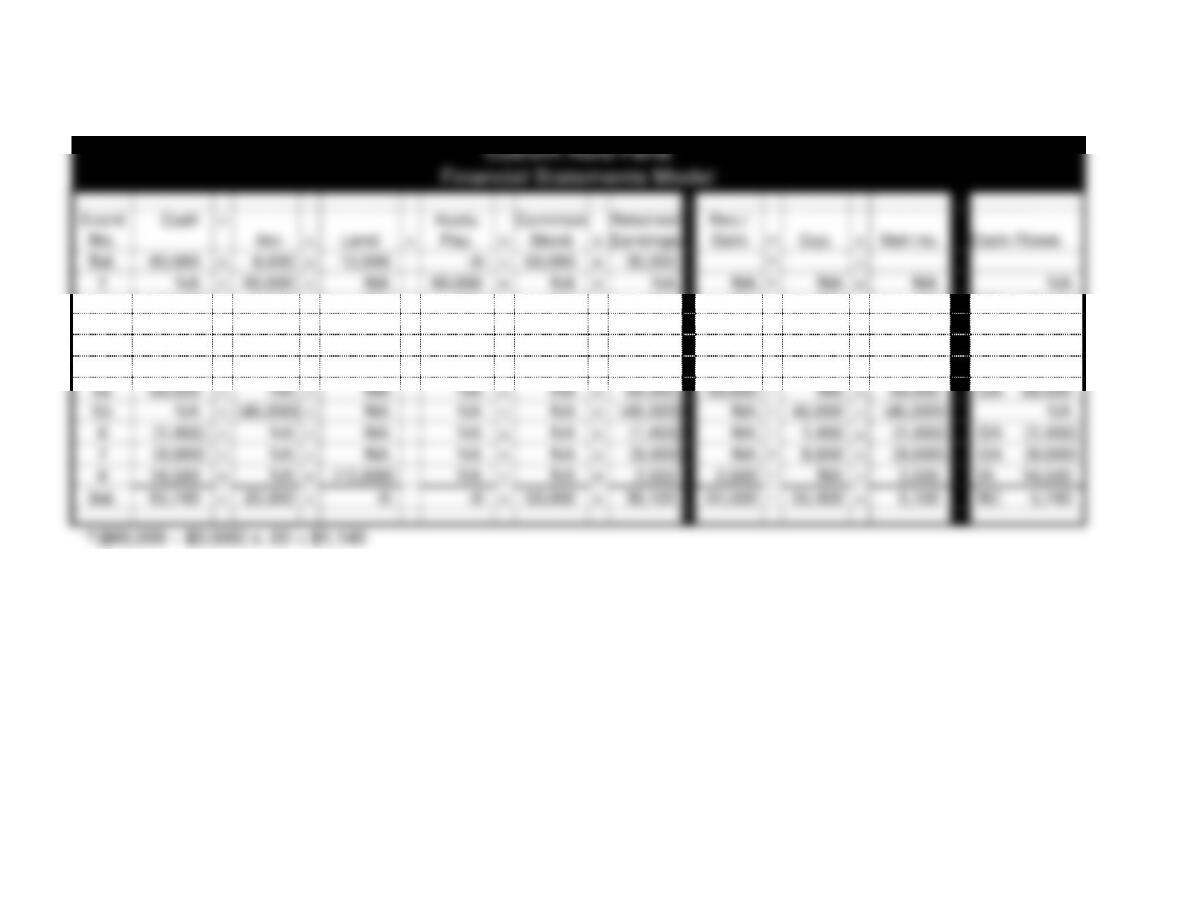

EXERCISE 4-17B

a. NC = Net Change in Cash

Custom Auto Parts

Financial Statements Model

Event

No.

Cash

+

Inv.

+

Land

+

Accts.

Pay.

=

Common

Stock

+

Retained

Earnings

Rev./

Gain

─

Exp.

=

Net Inc.

Cash Flows

Bal.

60,000

+

8,000

+

12,000

-0-

=

50,000

+

30,000

─

=

1

NA

+

60,000

+

NA

60,000

=

NA

+

NA

NA

─

NA

=

NA

NA

2.

(1,500)

+

1,500

+

NA

NA

=

NA

+

NA

NA

─

NA

=

NA

OA (1,500)

3.

NA

+

(3,000)

+

NA

(3,000)

=

NA

+

NA

NA

─

NA

=

NA

NA

4a*

NA

+

(1,140)

+

NA

(1,140)

=

NA

+

NA

NA

─

NA

=

NA

NA

4b

(55,860)

+

NA

+

NA

(55,860)

=

NA

+

NA

NA

─

NA

=

NA

OA (55,860)

5a

59,000

+

NA

+

NA

NA

=

NA

+

59,000

59,000

─

NA

=

59,000

OA 59,000

5b

NA

+

(45,000)

+

NA

NA

=

NA

+

(45,000)

NA

─

45,000

=

(45,000)

NA

6

(1,400)

+

NA

+

NA

NA

=

NA

+

(1,400)

NA

─

1,400

=

(1,400)

OA (1,400)

7

(9,000)

+

NA

+

NA

NA

=

NA

+

(9,000)

NA

─

9,000

=

(9,000)

OA (9,000)

8

14,500

+

NA

+

(12,000)

NA

=

NA

+

2,500

2,500

─

NA

=

2,500

IA 14,500

Bal.

65,740

+

20,360

+

-0-

-0-

=

50,000

+

36,100

61,500

─

55,400

=

6,100

NC 5,740

*($60,000 − $3,000) x .02 = $1,140

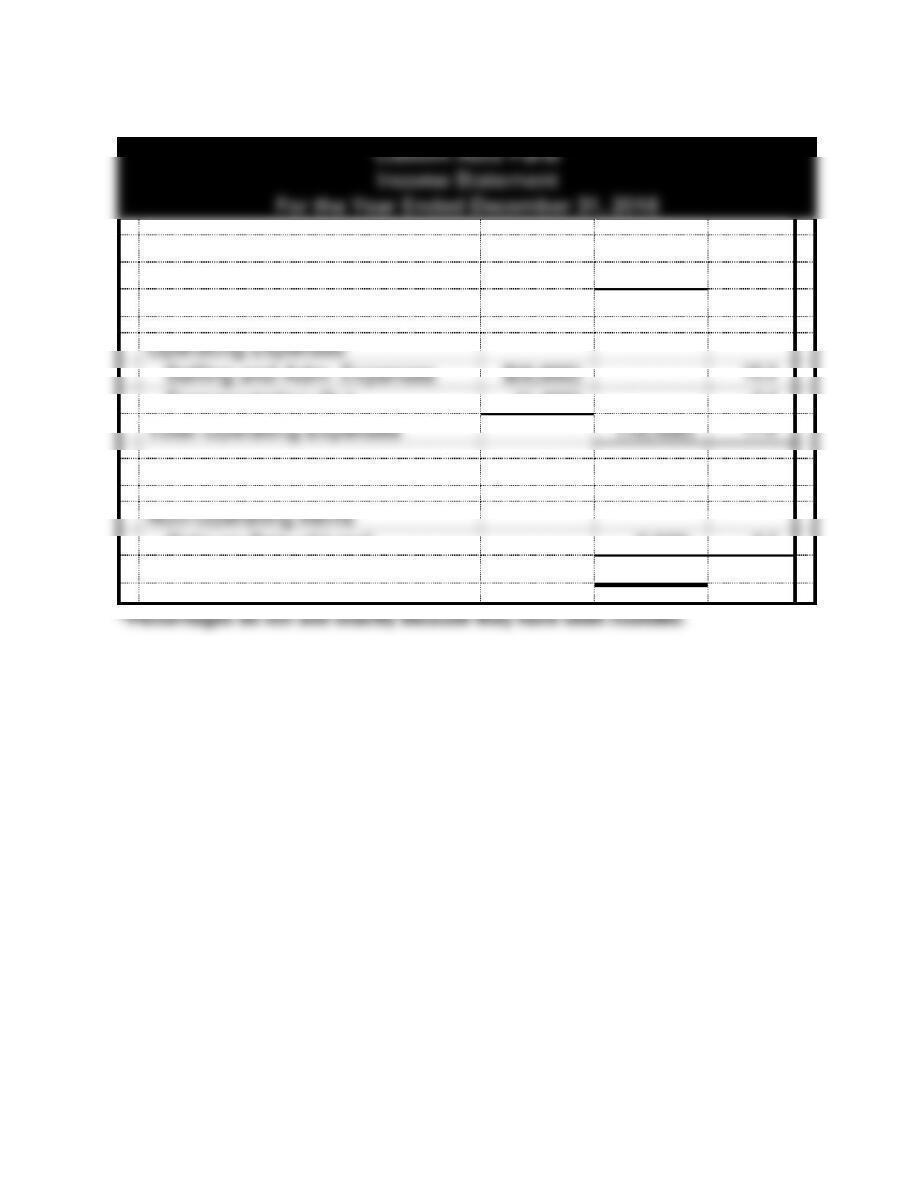

EXERCISE 4-17B (cont.)

b.

Custom Auto Parts

Income Statement

For the Year Ended December 31, 2016

Net Sales

$59,000

100.0%

Cost of Goods Sold

(45,000)

76.3

Gross Margin

14,000

23.7

Operating Expenses

Selling and Adm. Expenses

$(9,000)

15.3

Transportation-Out

(1,400)

2.4

Total Operating Expenses

(10,400)

17.6

Operating Income

3,600

6.1

Non-Operating Items

Gain on Sale of Land

2,500

4.2

Net Income

$6,100

10.3

4-125

EXERCISE 4-17B (cont.)

c. All other things being equal, the higher the gross margin percentage,

recur.

4-126

EXERCISE 4-18B

a. Gross Margin Percentages:

Athens: 25% ($ 8,150 ÷ $32,600)

Boulder: 45% ($38,790 ÷ $86,200)

4-127

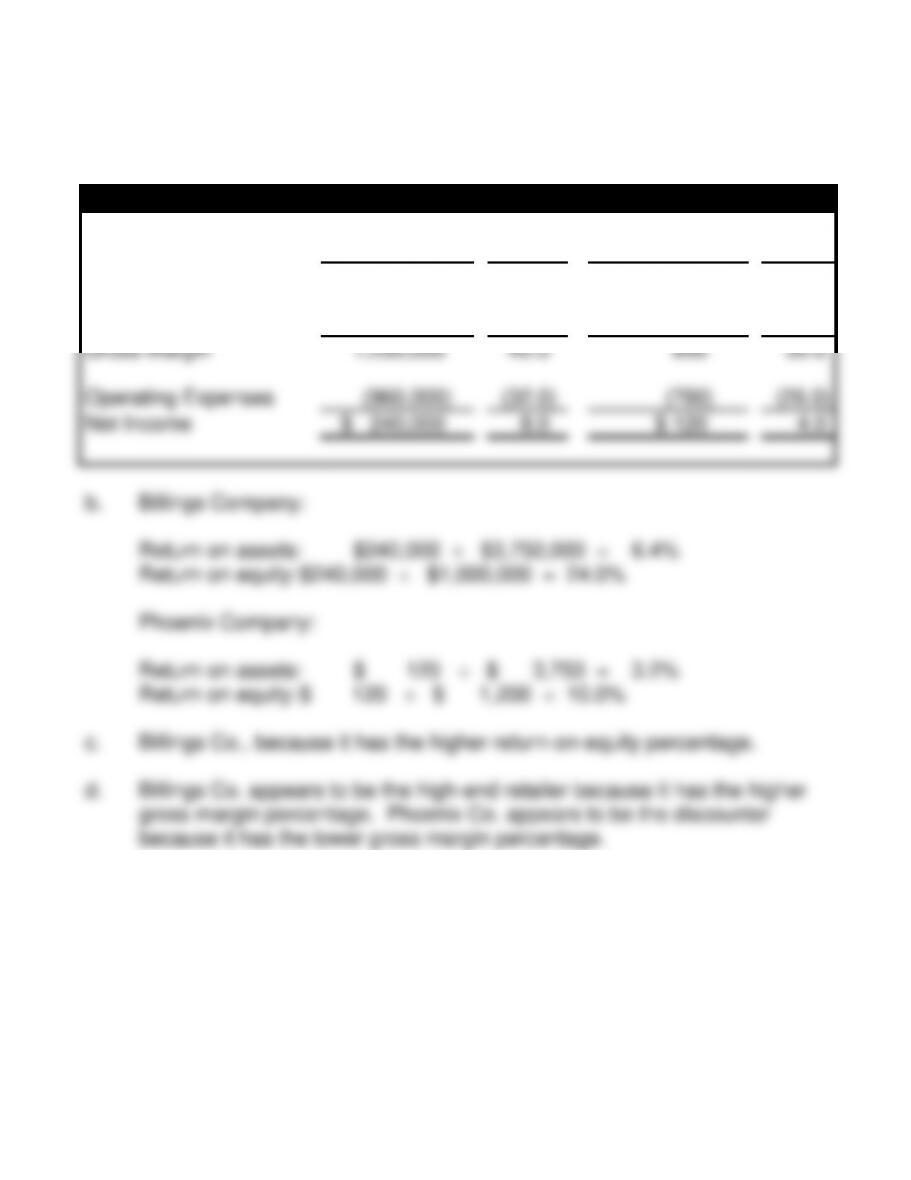

EXERCISE 4-19B

a.

Common Size Income Statements

Billings

%

Phoenix

%

Sales

$3,000,000

100.0

$3,000

100.0

Cost of Goods Sold

(1,800,000)

(60.0)

(2,100)

(70.0)

Gross Margin

1,200,000

40.0

900

30.0

Operating Expenses

(960,000)

(32.0)

(780)

(26.0)

Net Income

$ 240,000

8.0

$ 120

4.0

b. Billings Company:

Return on assets: $240,000 ÷ $3,750,000 = 6.4%

Return on equity: $240,000 ÷ $1,000,000 = 24.0%

Phoenix Company:

Return on assets: $ 120 ÷ $ 3,750 = 3.2%

Return on equity: $ 120 ÷ $ 1,200 = 10.0%

c. Billings Co., because it has the higher return–on-equity percentage.

d. Billings Co. appears to be the high-end retailer because it has the higher

gross margin percentage. Phoenix Co. appears to be the discounter

because it has the lower gross margin percentage.

4-128

EXERCISE 4-20B (Appendix)

Beginning Mdse. Inventory

$ 4,800

Plus: Merchandise Purchased

26,000

Goods Available for Sale

30,800

Less: Ending Mdse. Inventory

(3,600)

Cost of Goods Sold

$27,200

a. Goods Available for Sale $30,800

b. Cost of Goods Sold $27,200

c. Merchandise Inventory on year-end balance sheet $3,600

4-129

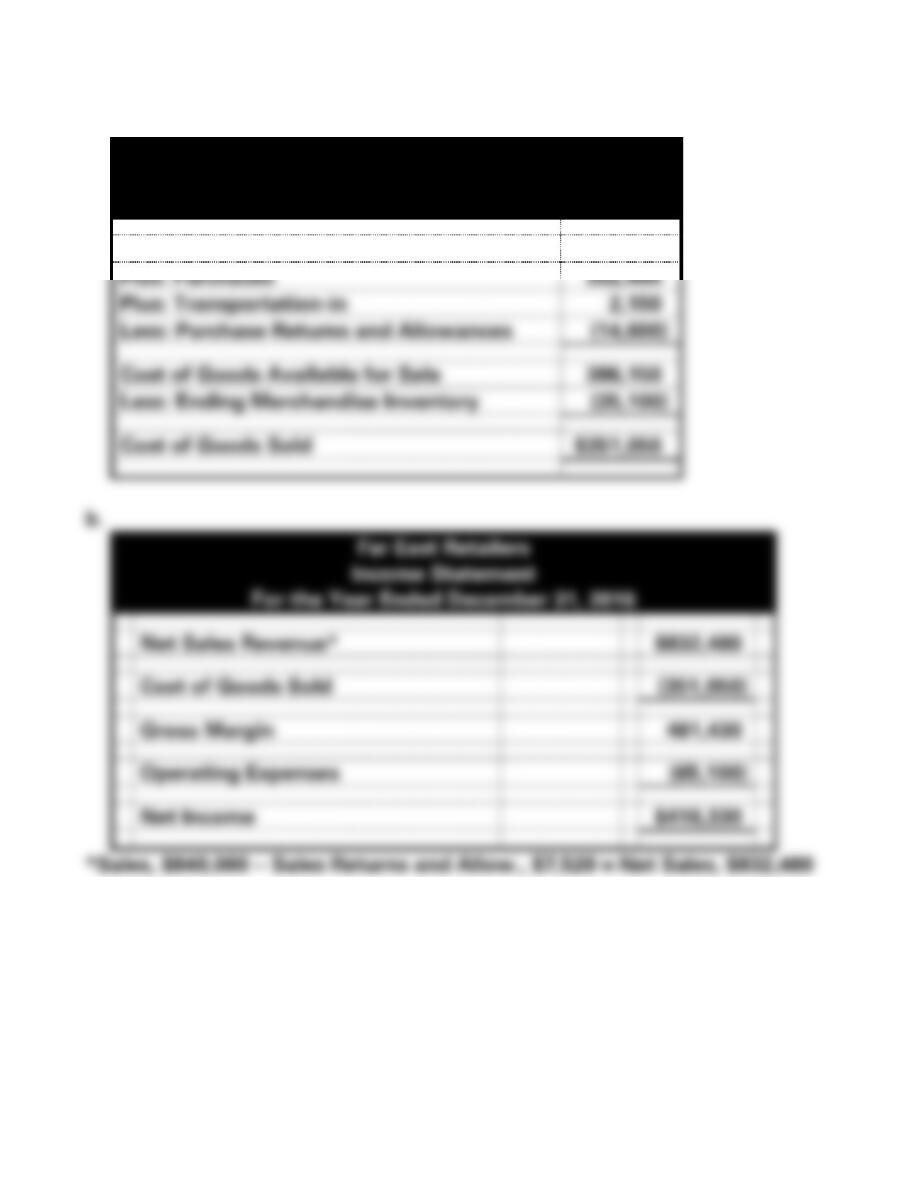

EXERCISE 4-21B (Appendix)

a.

Far East Retailers

Schedule of Cost of Goods Sold

For the Year Ended 2016

Beginning Merchandise Inventory

$ 46,200

Plus: Purchases

352,400

Plus: Transportation-in

2,150

Less: Purchase Returns and Allowances

(14,600)

Cost of Goods Available for Sale

386,150

Less: Ending Merchandise Inventory

(35,100)

Cost of Goods Sold

$351,050

b.

Far East Retailers

Income Statement

For the Year Ended December 31, 2016

Net Sales Revenue*

$832,480

Cost of Goods Sold

(351,050)

Gross Margin

481,430

Operating Expenses

(65,100)

Net Income

$416,330

*Sales, $840,000 − Sales Returns and Allow., $7,520 = Net Sales, $832,480

4-130

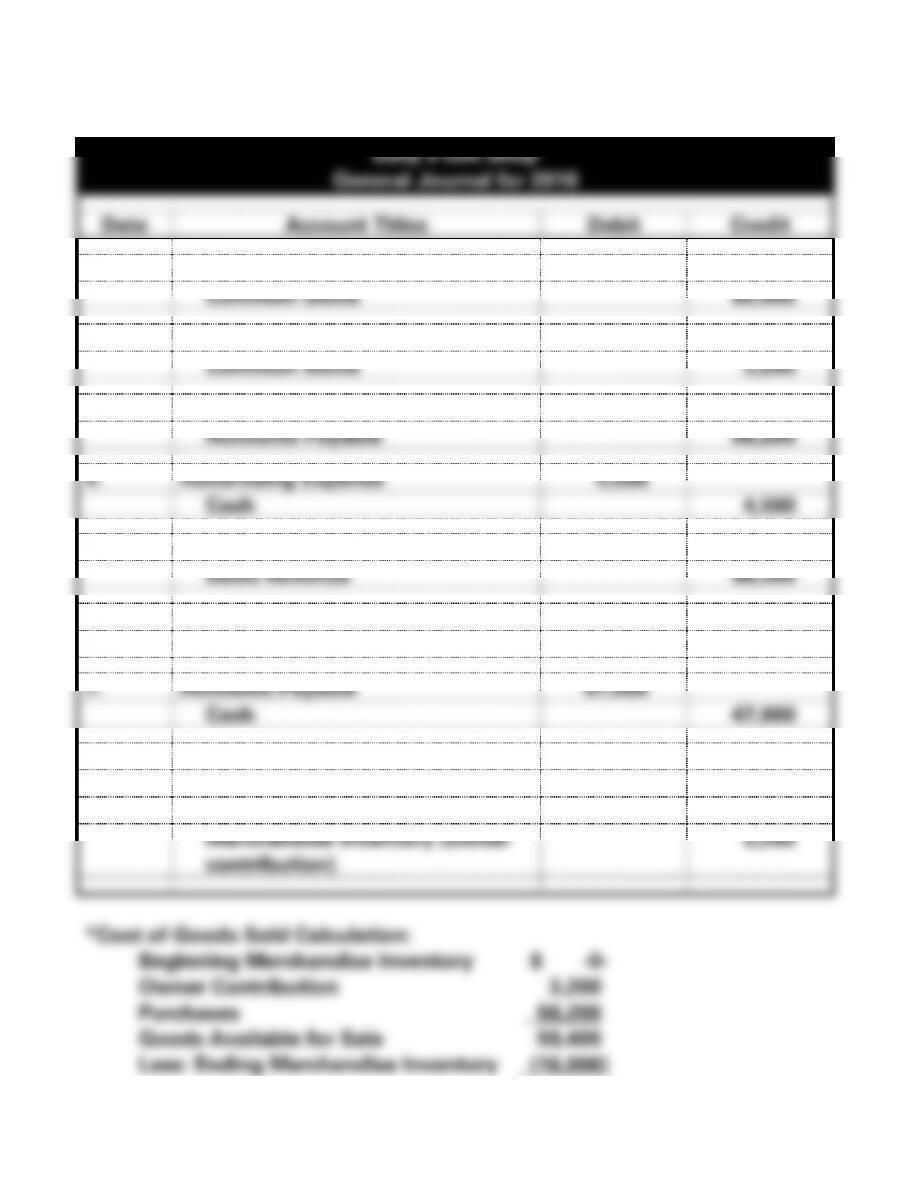

EXERCISE 4-22B (Appendix)

a.

Sally’s Gift Shop

General Journal for 2016

Date

Account Titles

Debit

Credit

1.

Cash

60,000

Common Stock

60,000

2.

Merchandise Inventory

3,200

Common Stock

3,200

3.

Purchases

56,200

Accounts Payable

56,200

4.

Advertising Expense

4,500

Cash

4,500

5.

Cash

98,300

Sales Revenue

98,300

6.

Salaries Expense

12,000

Cash

12,000

7.

Accounts Payable

47,000

Cash

47,000

8. (adj.)

Cost of Goods Sold*

43,400

Merchandise Inventory (Ending)

16,000

Purchases

56,200

Merchandise Inventory (owner

contribution)

3,200

4-131

Cost of Goods Sold $43,400

4-132

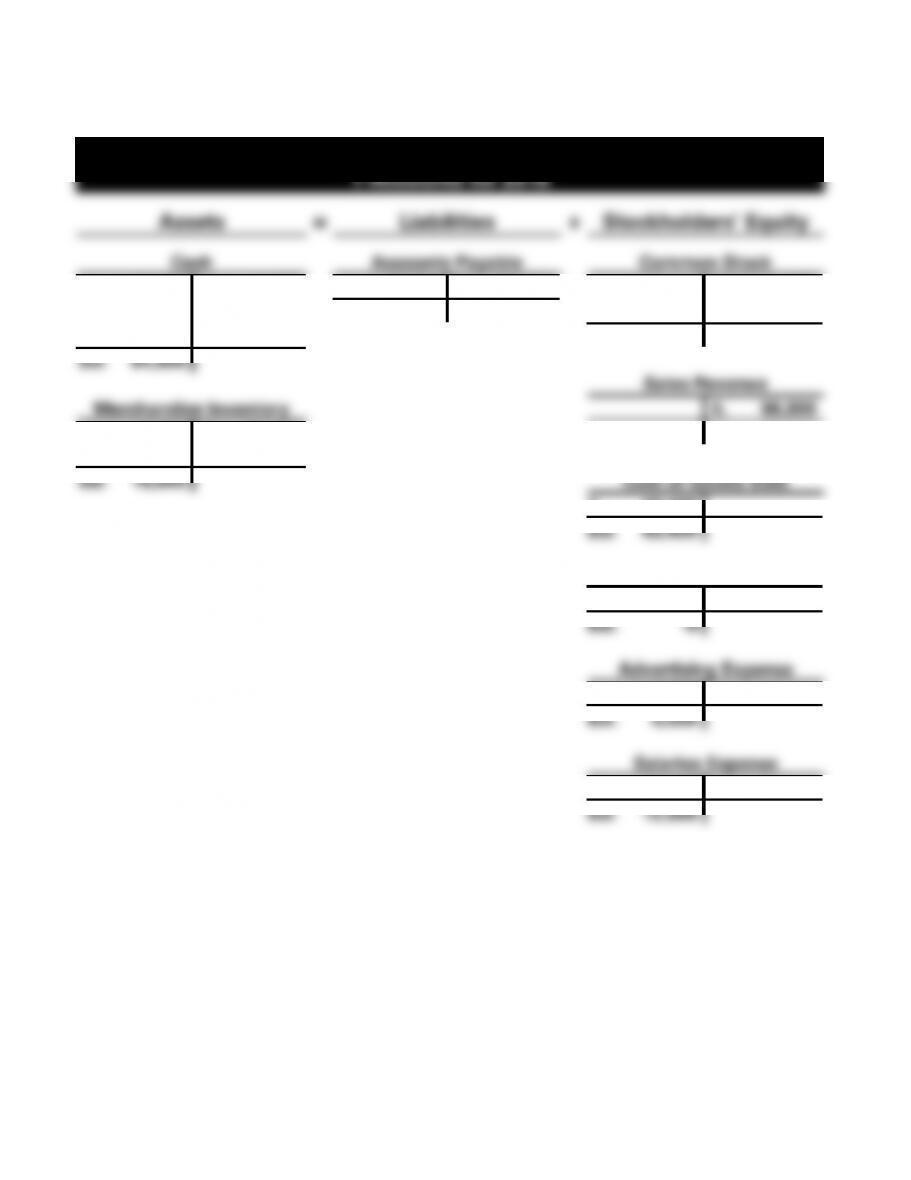

EXERCISE 4-22B (cont.)

b.

Sally’s Gift Shop

T-Accounts for 2016

Assets

=

Liabilities

+

Stockholders’ Equity

Cash

Accounts Payable

Common Stock

1. 60,000

4. 4,500

7. 47,000

3. 56,200

1. 60,000

5. 98,300

6. 12,000

Bal. 9,200

2. 3,200

7. 47,000

Bal. 63,200

Bal. 94,800

Sales Revenue

Merchandise Inventory

5. 98,300

2. 3,200

8. 43,400

Bal. 98,300

8. 56,200

Bal. 16,000

Cost of Goods Sold

8. 43,400

Bal. 43,400

Purchases

3. 56,200

8. 56,200

Bal. -0-

Advertising Expense

4. 4,500

Bal. 4,500

Salaries Expense

6. 12,000

Bal. 12,000

4-133

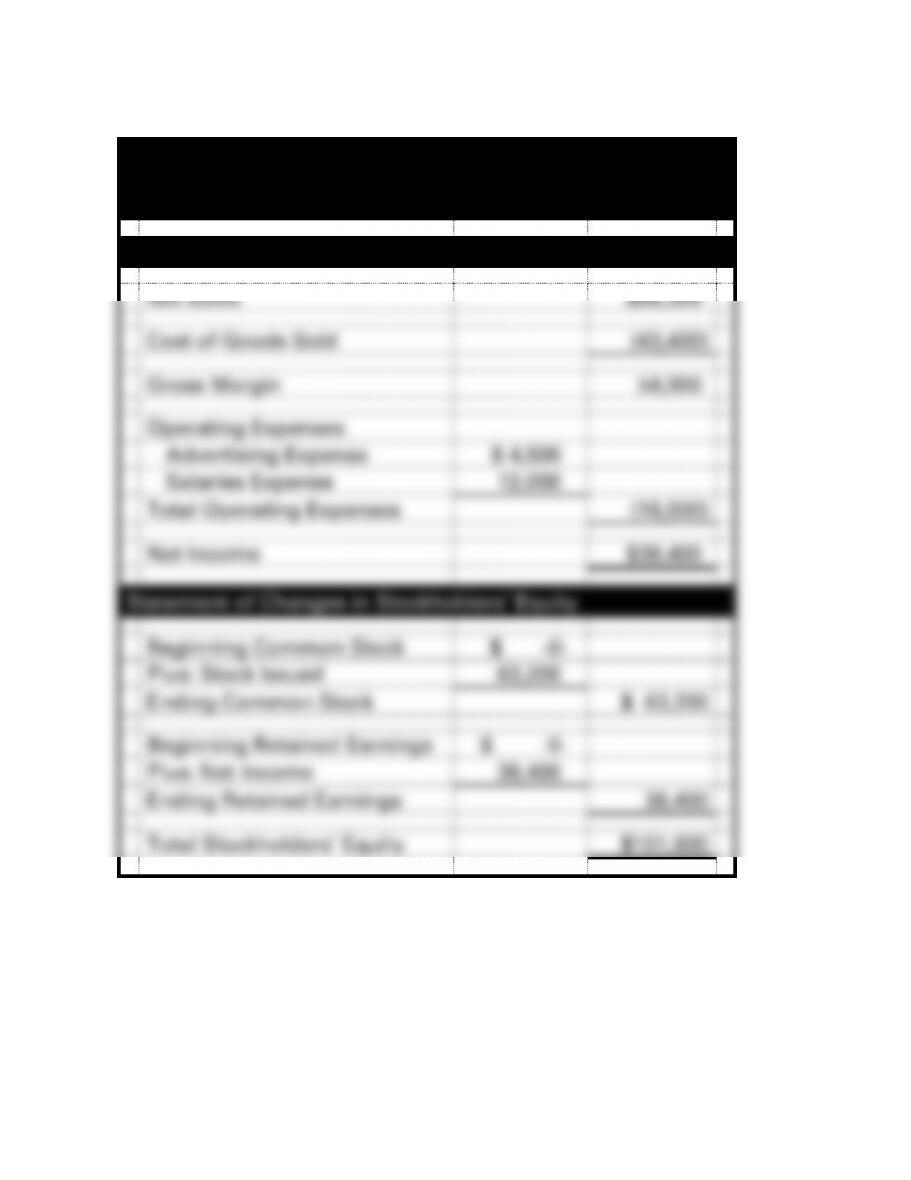

EXERCISE 4-22B (cont.)

c.

Sally’s Gift Shop

Financial Statements

For the Year Ended December 31, 2016

Income Statement

Net Sales

$98,300

Cost of Goods Sold

(43,400)

Gross Margin

54,900

Operating Expenses

Advertising Expense

$ 4,500

Salaries Expense

12,000

Total Operating Expenses

(16,500)

Net Income

$38,400

Statement of Changes in Stockholders’ Equity

Beginning Common Stock

$ -0-

Plus: Stock Issued

63,200

Ending Common Stock

$ 63,200

Beginning Retained Earnings

$ -0-

Plus: Net Income

38,400

Ending Retained Earnings

38,400

Total Stockholders’ Equity

$101,600

4-134

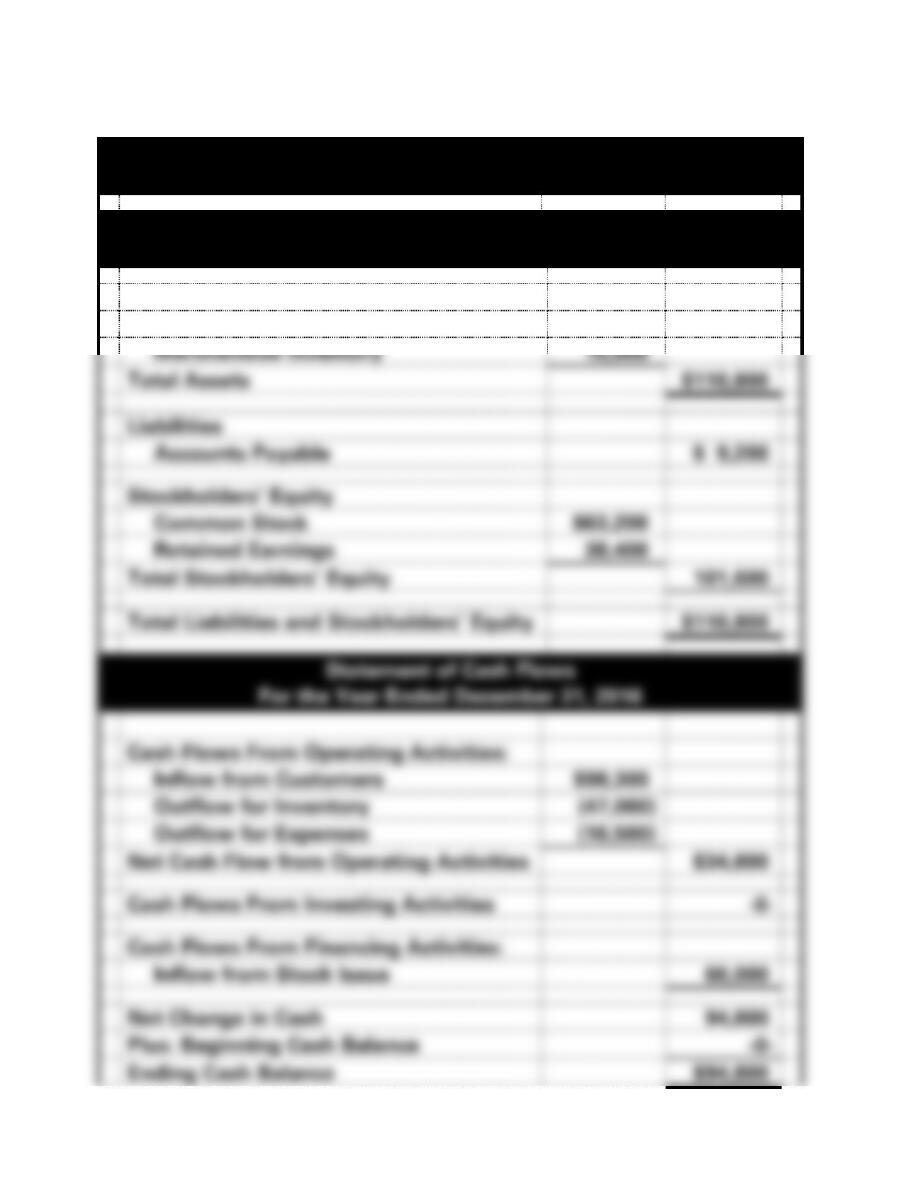

EXERCISE 4-22B c. (cont.)

Sally’s Gift Shop

Financial Statements

Balance Sheet

As of December 31, 2016

Assets

Cash

$94,800

Merchandise Inventory

16,000

Total Assets

$110,800

Liabilities

Accounts Payable

$ 9,200

Stockholders’ Equity

Common Stock

$63,200

Retained Earnings

38,400

Total Stockholders’ Equity

101,600

Total Liabilities and Stockholders’ Equity

$110,800

Statement of Cash Flows

For the Year Ended December 31, 2016

Cash Flows From Operating Activities:

Inflow from Customers

$98,300

Outflow for Inventory

(47,000)

Outflow for Expenses

(16,500)

Net Cash Flow from Operating Activities

$34,800

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities:

Inflow from Stock Issue

60,000

Net Change in Cash

94,800

Plus: Beginning Cash Balance

-0-

Ending Cash Balance

$94,800