3-1–121

PROBLEM 3-36A b. (cont.)

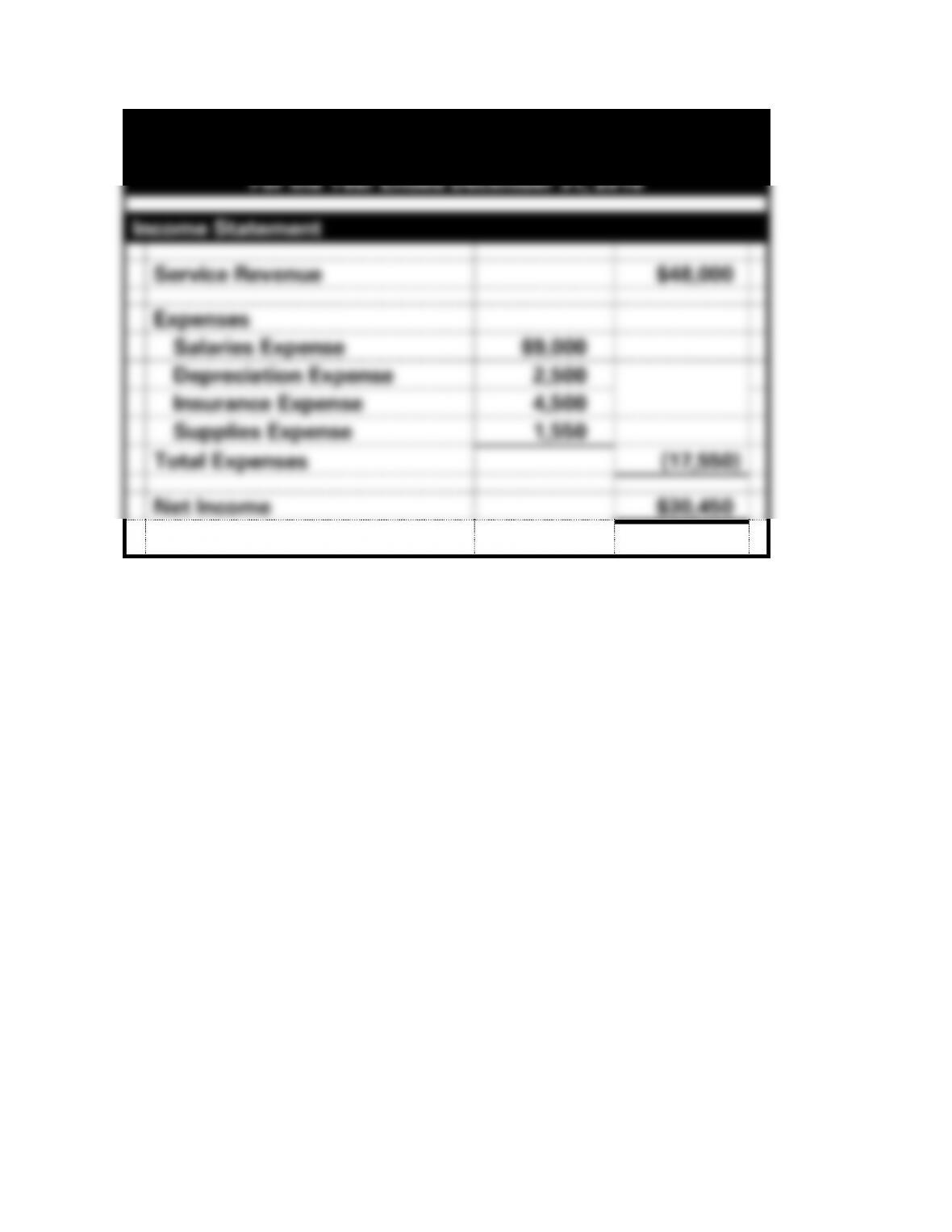

Bower Consulting Company

Financial Statements

For the Year Ended December 31, 2016

Income Statement

Service Revenue

$48,000

Expenses

Salaries Expense

$9,000

Depreciation Expense

2,500

Insurance Expense

4,500

Supplies Expense

1,550

Total Expenses

(17,550)

Net Income

$30,450

3-1–122

PROBLEM 3-36A b. (cont.)

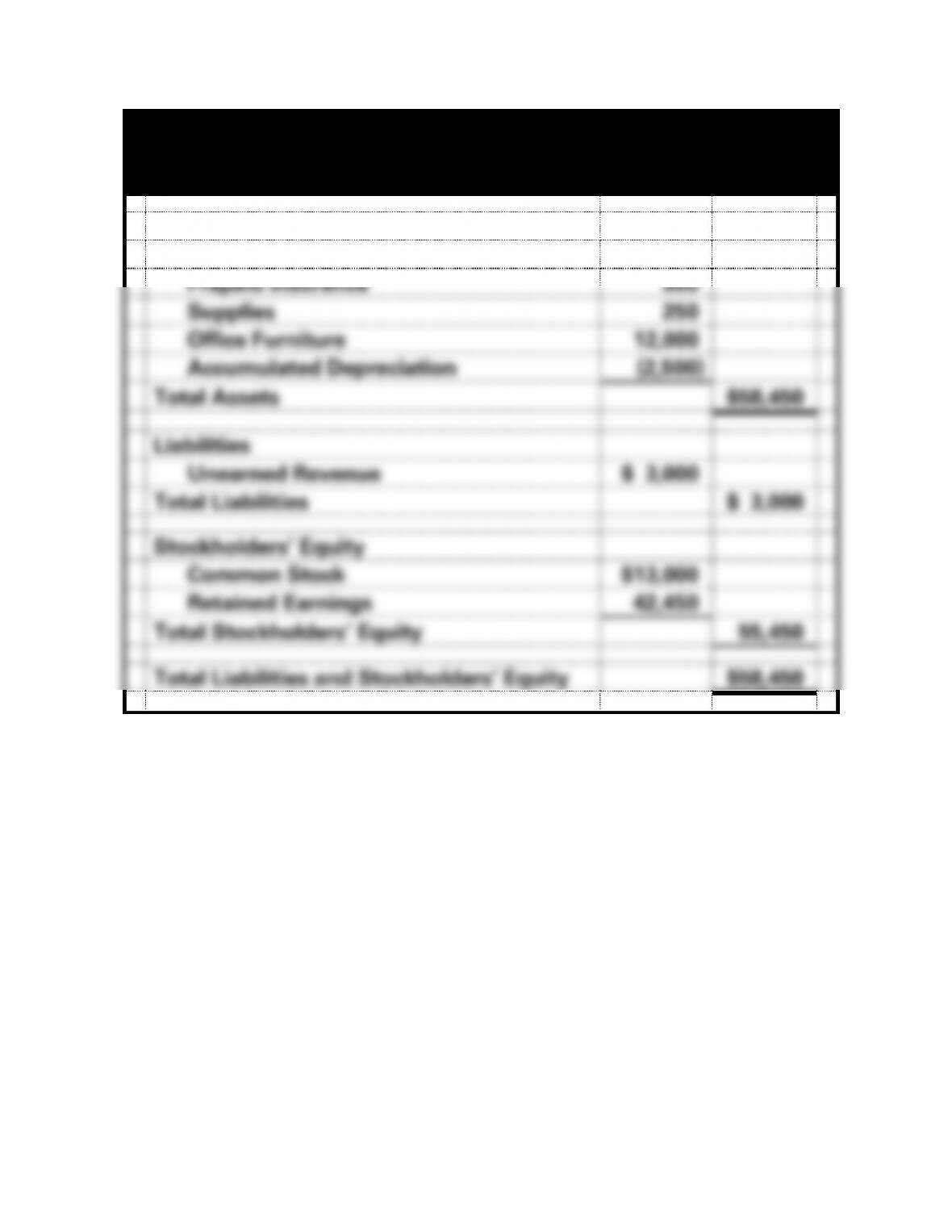

Bower Consulting Company

Balance Sheet

As of December 31, 2016

Assets

Cash

$47,800

Prepaid Insurance

900

Supplies

250

Office Furniture

12,000

Accumulated Depreciation

(2,500)

Total Assets

$58,450

Liabilities

Unearned Revenue

$ 3,000

Total Liabilities

$ 3,000

Stockholders’ Equity

Common Stock

$13,000

Retained Earnings

42,450

Total Stockholders’ Equity

55,450

Total Liabilities and Stockholders’ Equity

$58,450

3-1–123

PROBLEM 3-36A b. (cont.)

Bower Consulting Company

Statement of Cash Flows

For the Year Ended December 31, 2016

Cash Flows From Operating Activities:

Received Cash from Customers1

$51,000

Paid Cash for Expenses2

(16,200)

Net Cash Flow from Operating Activities

$34,800

Cash Flows From Investing Activities

Purchased Office Furniture

(12,000)

Net Cash Flow from Financing Activities

(12,000)

Cash Flows From Financing Activities:

-0-

Net Change in Cash

22,800

Plus: Beginning Cash Balance

25,000

Ending Cash Balance

$47,800

1(4) $39,000 + (6) $12,000 = $51,000

2(2) $5,400 + (3) $1,800 + (5) $9,000 = $16,200

3-1–124

SOLUTIONS TO PROBLEMS – SERIES A – CHAPTER 3

PROBLEM 3-25B

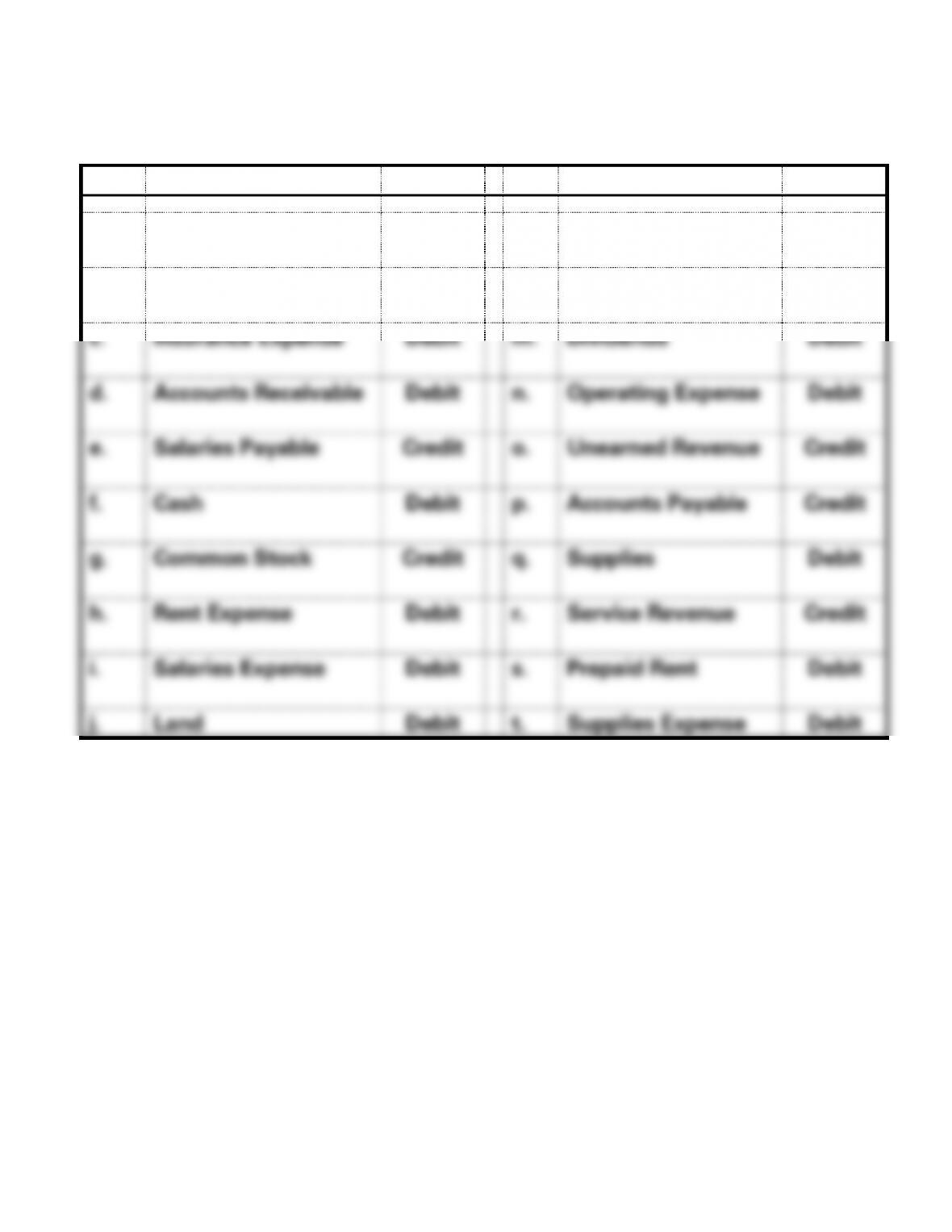

Item

Account

Balance

No.

Account

Balance

a.

Retained Earnings

Credit

k.

Interest Receivable

Debit

b.

Prepaid Insurance

Debit

l.

Interest Revenue

Credit

c.

Insurance Expense

Debit

m.

Dividends

Debit

d.

Accounts Receivable

Debit

n.

Operating Expense

Debit

e.

Salaries Payable

Credit

o.

Unearned Revenue

Credit

f.

Cash

Debit

p.

Accounts Payable

Credit

g.

Common Stock

Credit

q.

Supplies

Debit

h.

Rent Expense

Debit

r.

Service Revenue

Credit

i.

Salaries Expense

Debit

s.

Prepaid Rent

Debit

j.

Land

Debit

t.

Supplies Expense

Debit

3-1–125

PROBLEM 3-26B

Event

Type of Event

Account Debited

Account Credited

1.

AS

Cash

Common Stock

2.

AS

Accounts Receivable

Service Revenue

3.

AE

Prepaid Rent

Cash

4.

AU

Operating Expenses

Cash

5.

AS

Cash

Unearned Revenue

6.

AU

Salaries Expense

Cash

7.

AU

Utilities Expense

Cash

8.

AU

Accounts Payable

Cash

9.

AU

Dividends

Cash

10.

AS

Supplies

Accounts Payable

11.

AS

Cash

Service Revenue

12.

AS

Interest Receivable

Interest Revenue

13.

AU

Rent Expense

Prepaid Rent

14.

CE

Unearned Revenue

Service Revenue

15.

CE

Salaries Expense

Salaries Payable

3-1–126

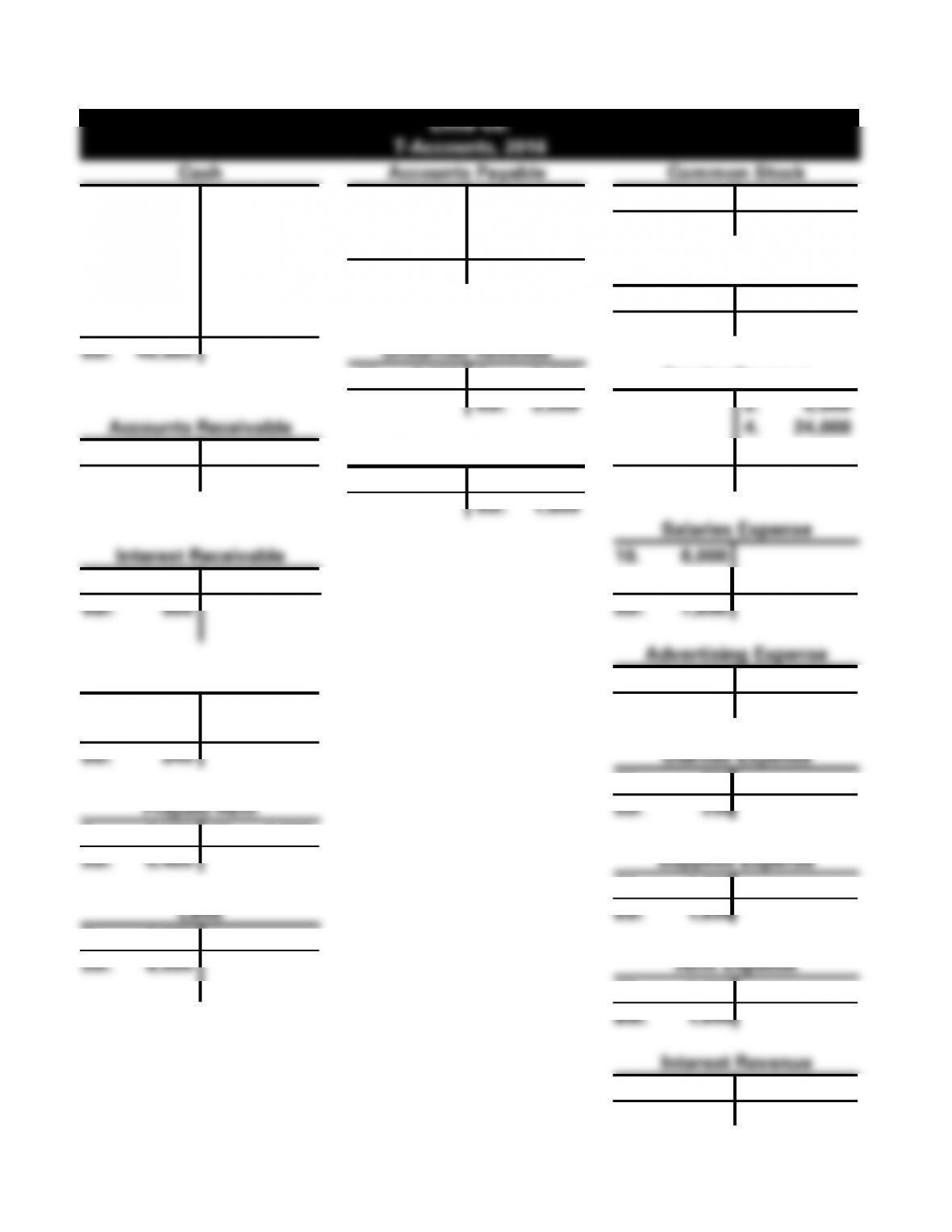

PROBLEM 3-27B

a.

Little Co.

T-Accounts, 2016

Cash

Accounts Payable

Common Stock

1. 40,000

6. 8,000

12. 840

5. 840

1. 40,000

2. 2,000

8. 1,000

13. 300

Bal. 40,000

3. 9,000

9. 7,200

14. 250

7. 17,000

10. 6,000

Bal. 550

Dividends

11. 4,000

11. 4,000

12. 840

Bal. 4,000

Bal. 40,960

Unearned Revenue

15. 6,000

3. 9,000

Service Revenue

Bal. 3,000

2. 2,000

Accounts Receivable

4. 24,000

4. 24,000

7. 17,000

Salaries Payable

15. 6,000

Bal. 7,000

16. 1,800

Bal. 32,000

Bal. 1,800

Salaries Expense

Interest Receivable

10. 6,000

19. 900

16. 1,800

Bal. 900

Bal. 7,800

Advertising Expense

Supplies

13. 300

5. 840

17. 1,600

Bal. 300

8. 1,000

Bal. 240

Utilities Expense

14. 250

Prepaid Rent

Bal. 250

9. 7,200

18. 1,800

Bal. 5,400

Supplies Expense

17. 1,600

Land

Bal. 1,600

6. 8,000

Bal. 8,000

Rent Expense

18. 1,800

Bal. 1,800

Interest Revenue

19. 900

Bal. 900

3-127

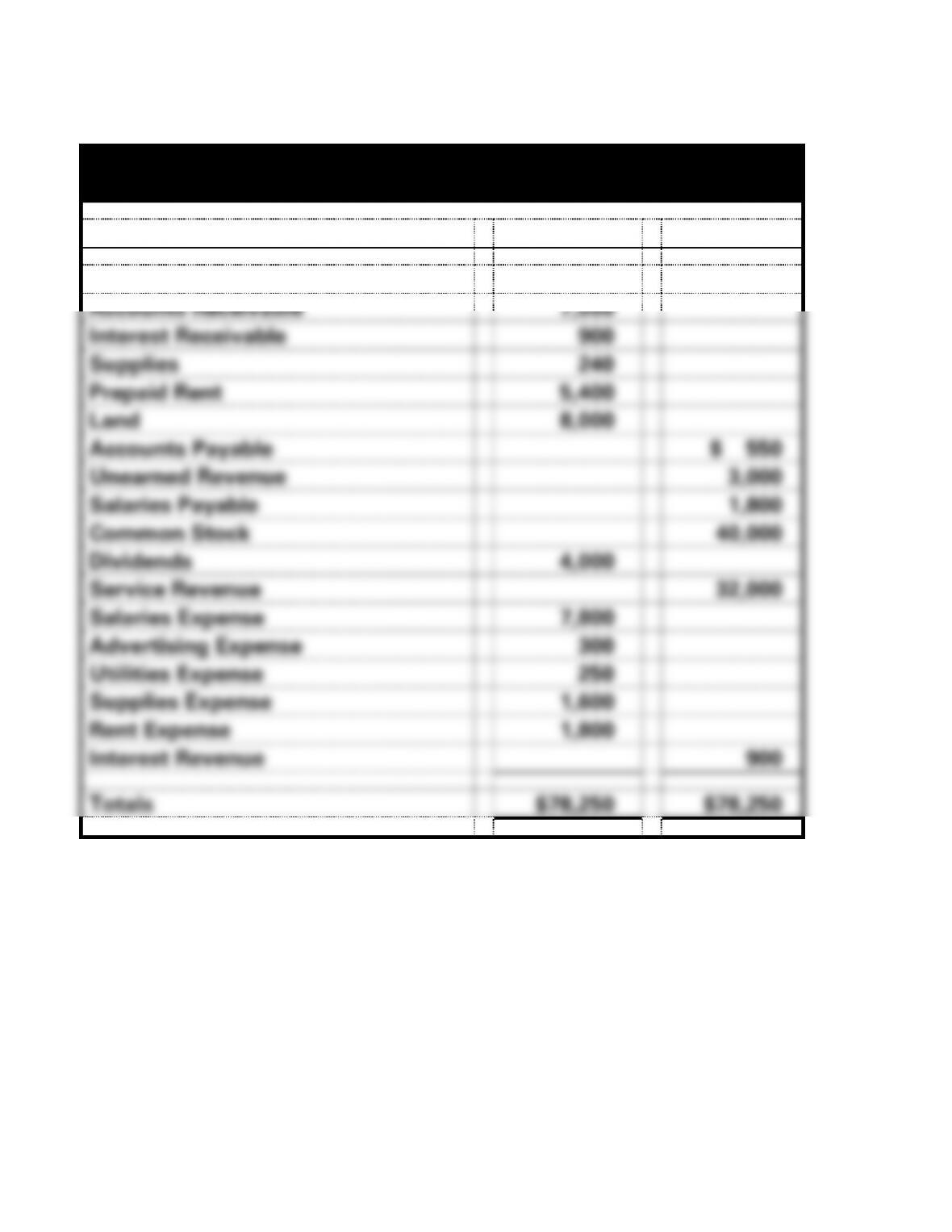

PROBLEM 3-27B (cont.)

b.

Little Company

Before-Closing Trial Balance for 2016

Account Titles

Debit

Credit

Cash

$40,960

Accounts Receivable

7,000

Interest Receivable

900

Supplies

240

Prepaid Rent

5,400

Land

8,000

Accounts Payable

$ 550

Unearned Revenue

3,000

Salaries Payable

1,800

Common Stock

40,000

Dividends

4,000

Service Revenue

32,000

Salaries Expense

7,800

Advertising Expense

300

Utilities Expense

250

Supplies Expense

1,600

Rent Expense

1,800

Interest Revenue

900

Totals

$78,250

$78,250

3-128

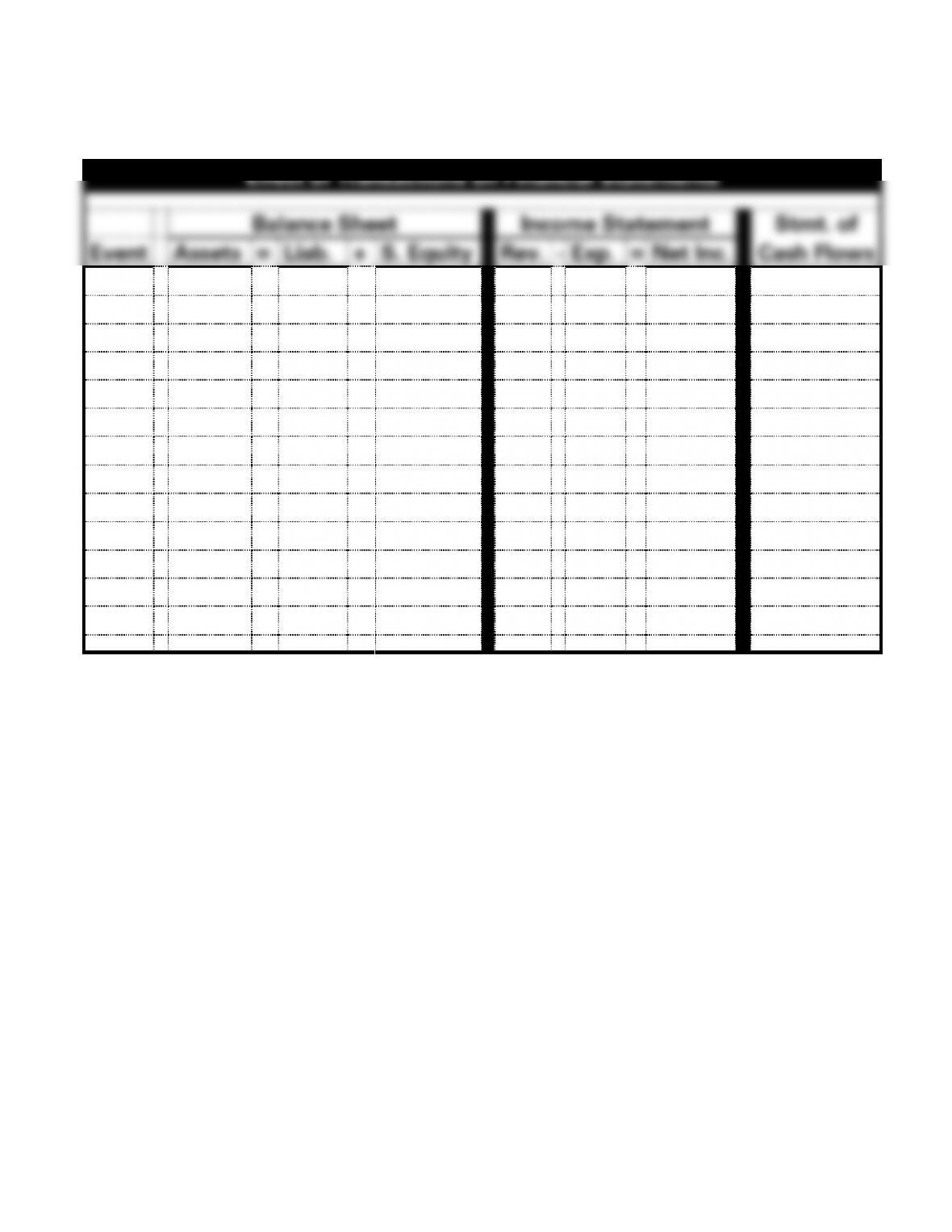

PROBLEM 3-27A (cont.)

c.

Little Co.

Effect of Transactions on Financial Statements for 2016

Balance Sheet

Income Statement

Stmt. of

Event

Assets

=

Liab.

+

S. Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flows

1.

+

NA

+

NA

NA

NA

+ FA

2.

+

NA

+

+

NA

+

+ OA

3.

+

+

NA

NA

NA

NA

+ OA

4.

+

NA

+

+

NA

+

NA

5.

+

+

NA

NA

NA

NA

NA

6.

+ −

NA

NA

NA

NA

NA

− IA

7.

+ −

NA

NA

NA

NA

NA

+ OA

8.

+ −

NA

NA

NA

NA

NA

− OA

9.

+ −

NA

NA

NA

NA

NA

− OA

10.

−

NA

−

NA

+

−

− OA

11.

−

NA

−

NA

NA

NA

− FA

12.

−

−

NA

NA

NA

NA

− OA

13.

NA

+

−

NA

+

−

NA

14.

NA

+

−

NA

+

−

NA

15.

NA

−

+

+

NA

+

NA

16.

NA

+

−

NA

+

−

NA

17.

−

NA

−

NA

+

−

NA

18.

−

NA

−

NA

+

−

NA

19.

+

NA

+

+

NA

+

NA

3-129

PROBLEM 3-28B

Effect of Transactions on Financial Statements

Balance Sheet

Income Statement

Stmt. of

Event

Assets

=

Liab.

+

S. Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flows

1.

+

NA

+

NA

NA

NA

+ FA

2.

+

NA

+

+

NA

+

NA

3.

+/–

NA

NA

NA

NA

NA

+ OA

4.

+

+

NA

NA

NA

NA

NA

5.

+

+

NA

NA

NA

NA

+ OA

6.

+

NA

+

+

NA

+

+ OA

7.

−

NA

−

NA

+

−

− OA

8.

+/−

NA

NA

NA

NA

NA

− OA

9.

−

NA

−

NA

+

−

− OA

10.

NA

−

+

+

NA

+

NA

11.

−

NA

−

NA

+

−

NA

12.

−

NA

−

NA

+

−

NA

13.

−

NA

−

NA

NA

NA

− FA

3-130

PROBLEM 3-29B

Entry Date

Description of Transaction

January 1

Acquired cash from the issuance of common stock.

February 1

Paid cash in advance to rent space.

March 1

Collected cash for services to be performed in the

future.

April 1

Performed services on account.

May 1

Purchased supplies on account.

May 31

Paid cash for salaries.

June 30

Paid cash for property taxes.

September 1

Performed services for cash.

October 2

Received cash from customers on account.

December 1

Paid a cash dividend to stockholders.

December 31

Recognized expense for supplies that had been used

during the period.

December 31

Recognized rent expense. Cash had been paid in a

prior transaction.

December 31

Recognized revenue that had been earned during the

period. Cash had been received in a prior transaction.

3-131

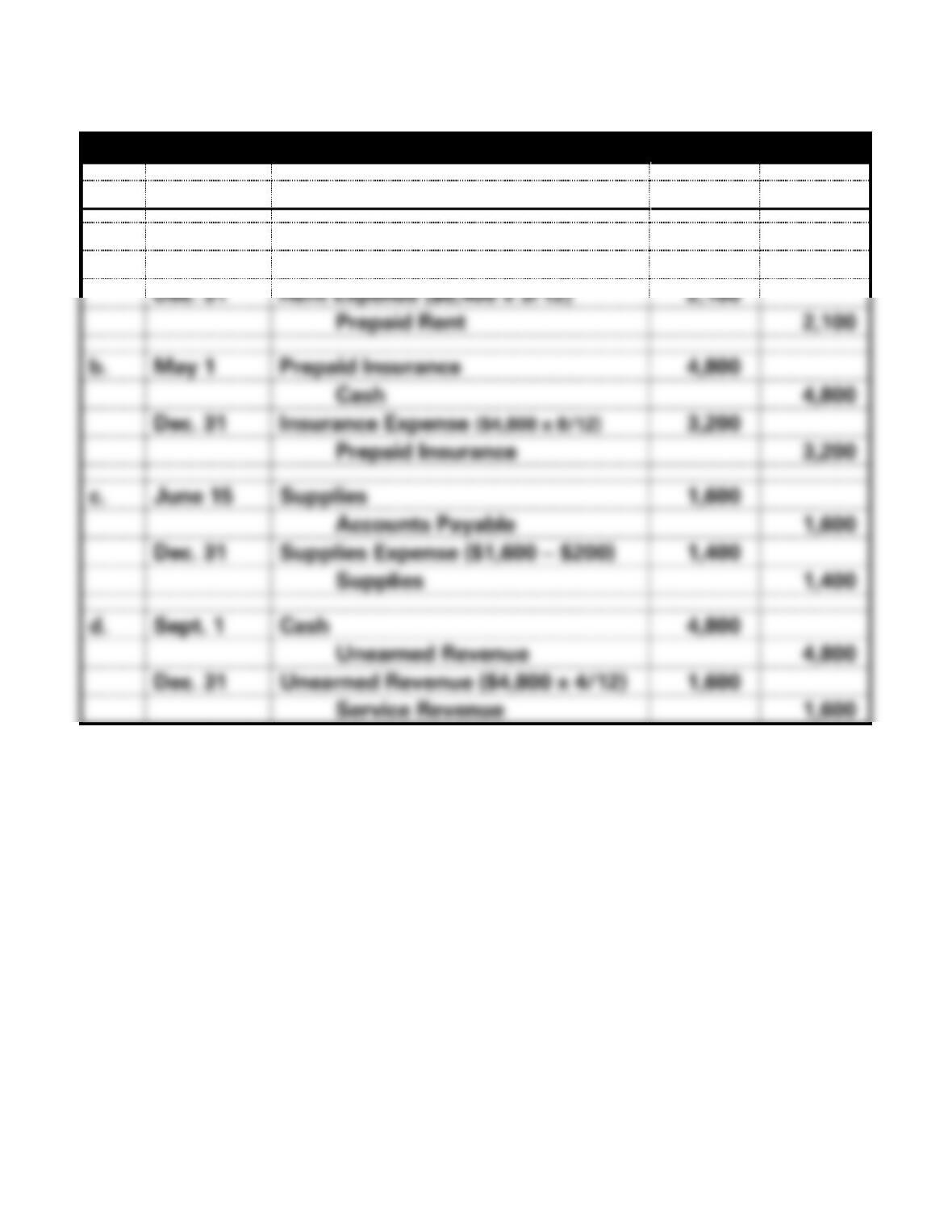

PROBLEM 3-30B

General Journal

No.

Date

Account Titles

Debit

Credit

a.

Oct. 1

Prepaid Rent

8,400

Cash

8,400

Dec. 31

Rent Expense ($8,400 x 3/12)

2,100

Prepaid Rent

2,100

b.

May 1

Prepaid Insurance

4,800

Cash

4,800

Dec. 31

Insurance Expense ($4,800 x 8/12)

3,200

Prepaid Insurance

3,200

c.

June 15

Supplies

1,600

Accounts Payable

1,600

Dec. 31

Supplies Expense ($1,600 − $200)

1,400

Supplies

1,400

d.

Sept. 1

Cash

4,800

Unearned Revenue

4,800

Dec. 31

Unearned Revenue ($4,800 x 4/12)

1,600

Service Revenue

1,600

PROBLEM 3-31B

a.

1. Debits would be greater by $2,000. Assets are overstated by $2,000.

2. Debits and credits would be equal, but assets are understated and

3. Debits and credits would be equal; both assets and equity (revenue)

4. Debits and credits would be equal; total debits and total credits would

5. Debits and credits would be equal; assets and liabilities would both be

6. Debits and credits would be equal; liabilities would be understated,

3-133

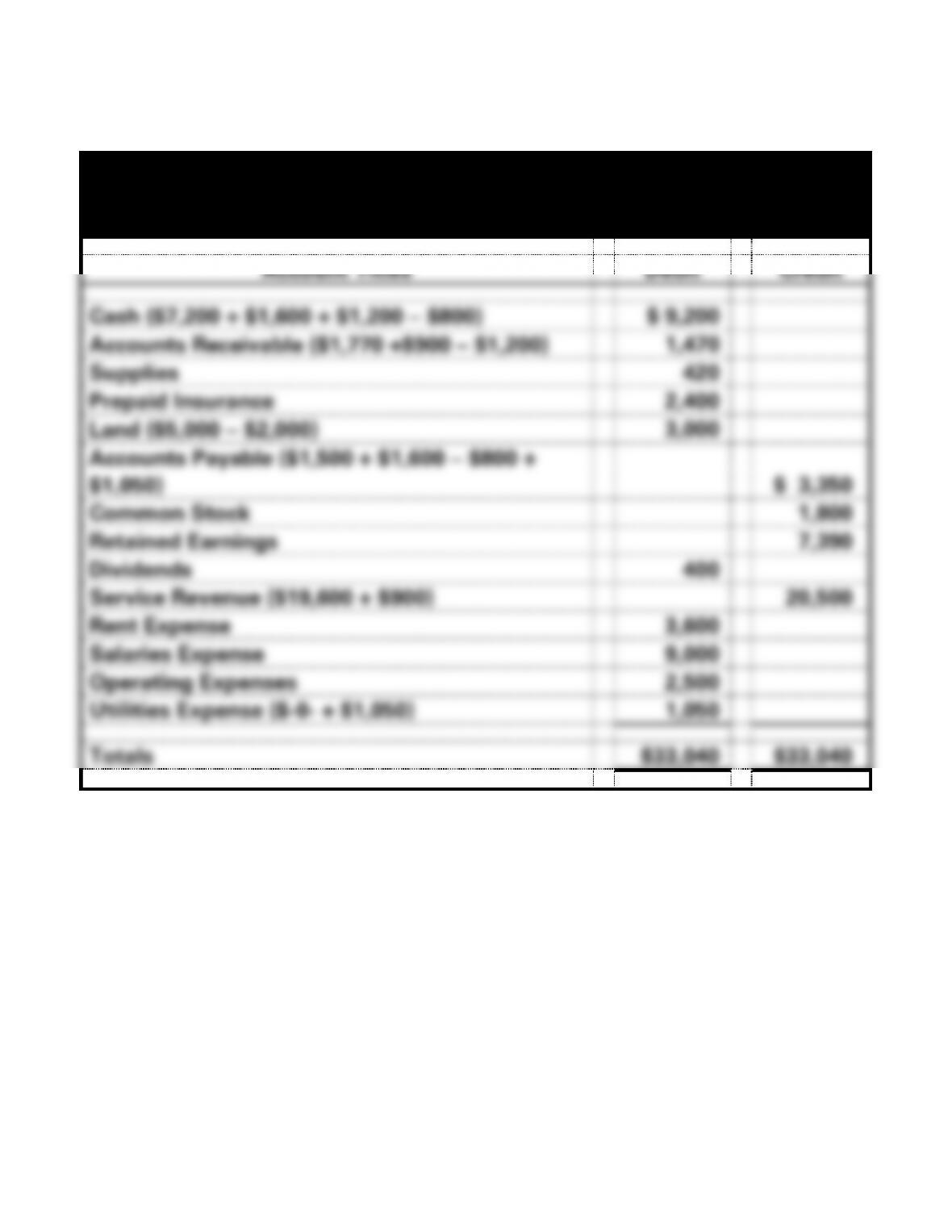

PROBLEM 3-31B (cont.)

c.

Klein Inc.

Trial Balance

As of May 31, 2016

Account Titles

Debit

Credit

Cash ($7,200 + $1,600 + $1,200 − $800)

$ 9,200

Accounts Receivable ($1,770 +$900 − $1,200)

1,470

Supplies

420

Prepaid Insurance

2,400

Land ($5,000 − $2,000)

3,000

Accounts Payable ($1,500 + $1,600 − $800 +

$1,050)

$ 3,350

Common Stock

1,800

Retained Earnings

7,390

Dividends

400

Service Revenue ($19,600 + $900)

20,500

Rent Expense

3,600

Salaries Expense

9,000

Operating Expenses

2,500

Utilities Expense ($-0- + $1,050)

1,050

Totals

$33,040

$33,040

3-134

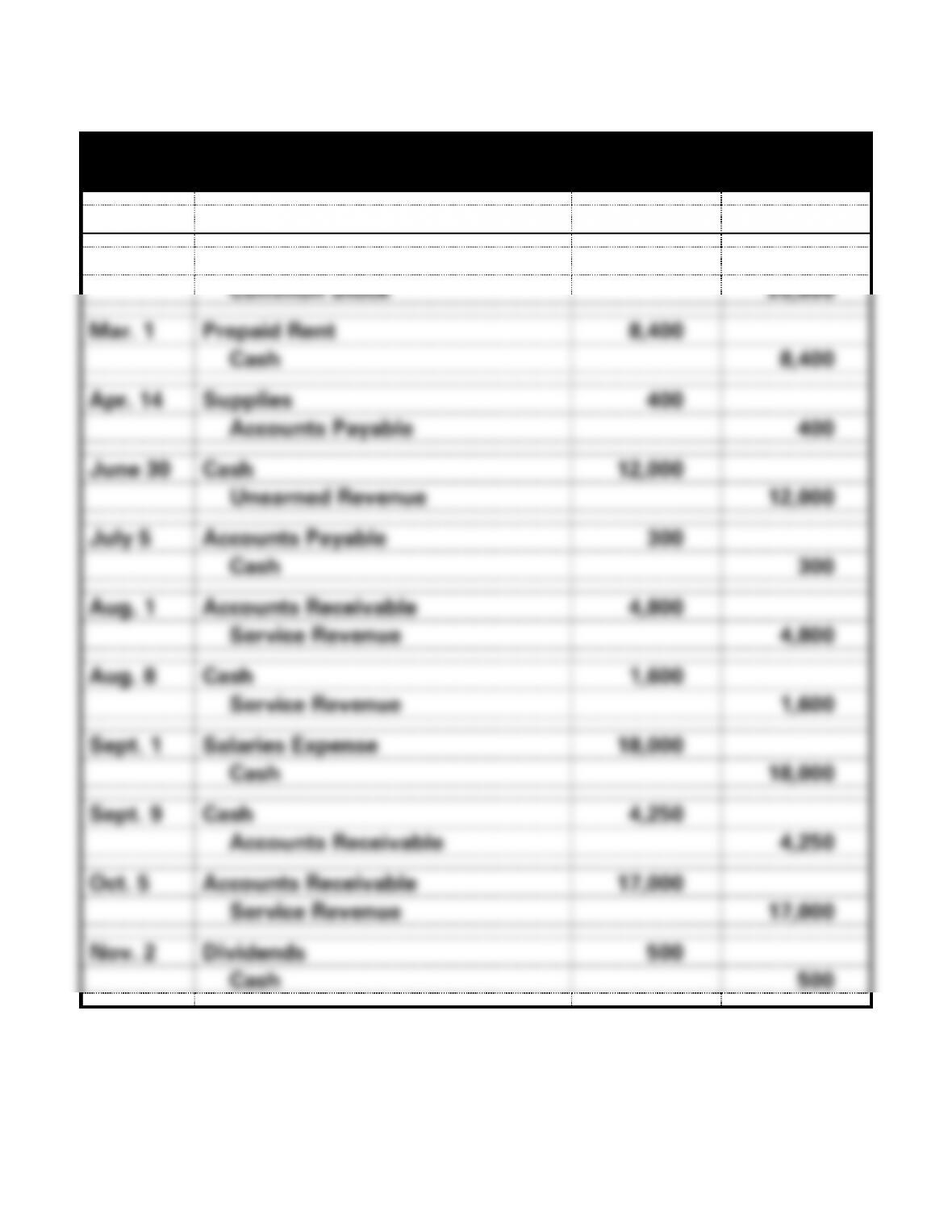

PROBLEM 3-32B

Price Corporation

General Journal, 2016

Date

Account Titles

Debit

Credit

Jan. 1

Cash

25,000

Common Stock

25,000

Mar. 1

Prepaid Rent

8,400

Cash

8,400

Apr. 14

Supplies

400

Accounts Payable

400

June 30

Cash

12,000

Unearned Revenue

12,000

July 5

Accounts Payable

300

Cash

300

Aug. 1

Accounts Receivable

4,800

Service Revenue

4,800

Aug. 8

Cash

1,600

Service Revenue

1,600

Sept. 1

Salaries Expense

18,000

Cash

18,000

Sept. 9

Cash

4,250

Accounts Receivable

4,250

Oct. 5

Accounts Receivable

17,000

Service Revenue

17,000

Nov. 2

Dividends

500

Cash

500

3-135

PROBLEM 3-32B a. (cont.)

Price Corporation

General Journal (cont)

Date

Account Titles

Debit

Credit

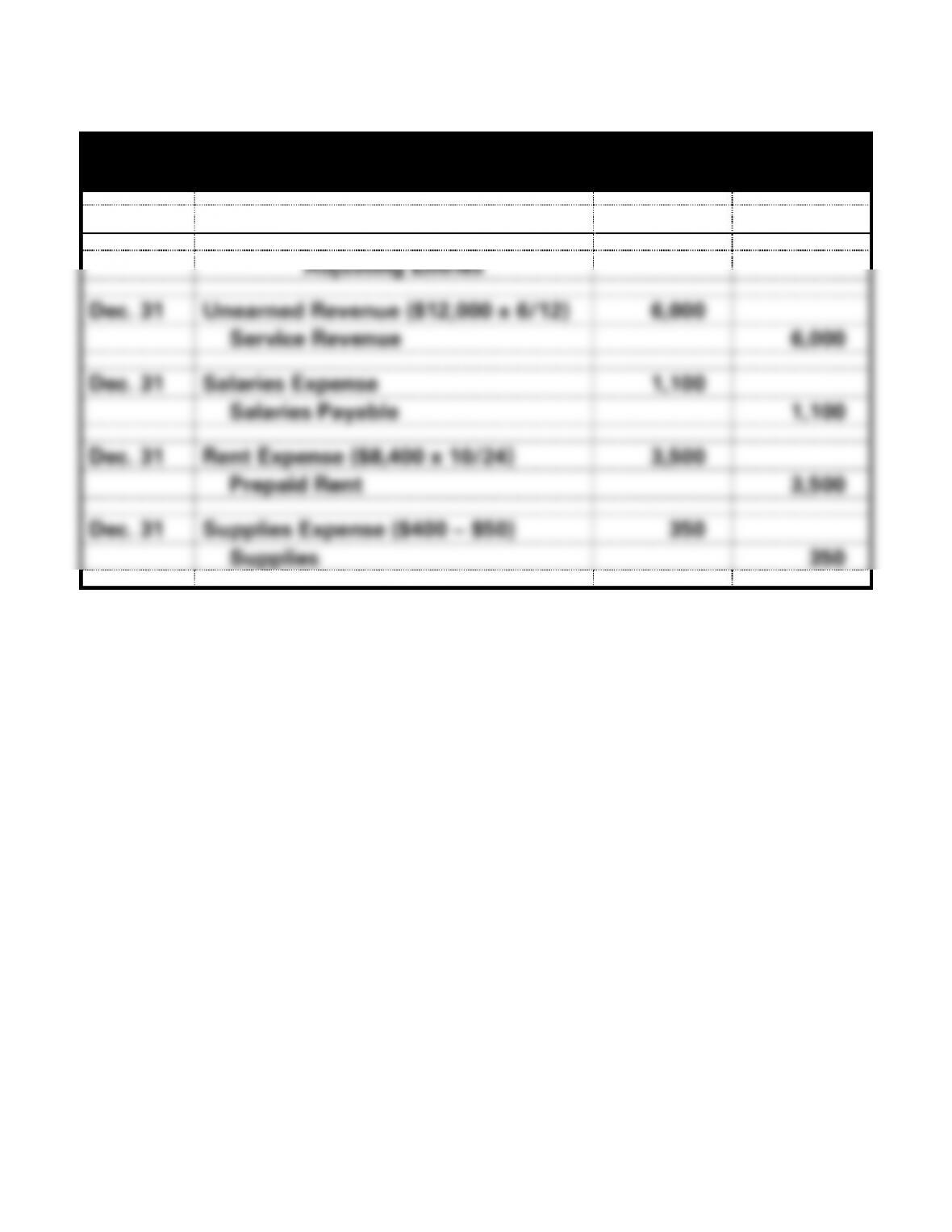

Adjusting Entries

Dec. 31

Unearned Revenue ($12,000 x 6/12)

6,000

Service Revenue

6,000

Dec. 31

Salaries Expense

1,100

Salaries Payable

1,100

Dec. 31

Rent Expense ($8,400 x 10/24)

3,500

Prepaid Rent

3,500

Dec. 31

Supplies Expense ($400 − $50)

350

Supplies

350

3-136

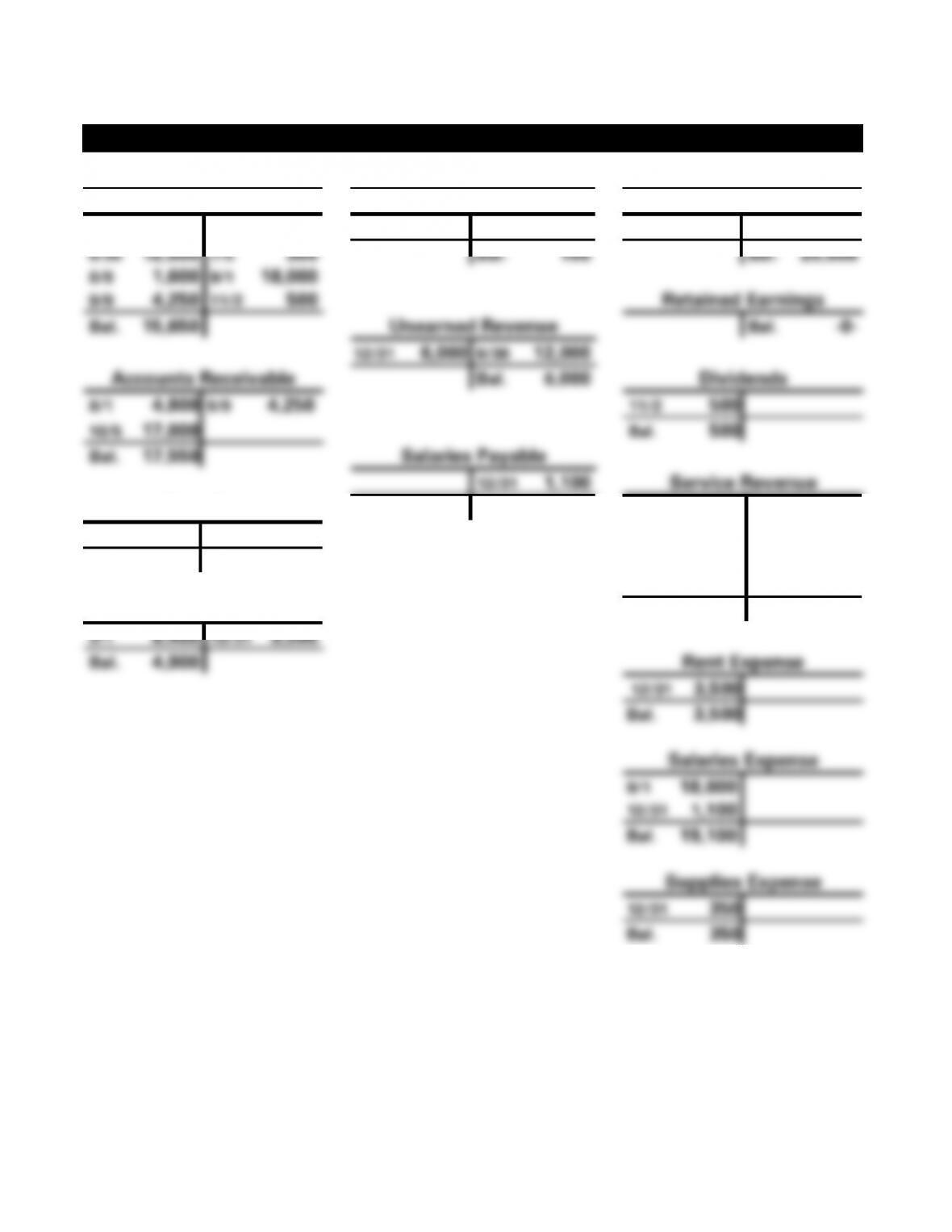

PROBLEM 3-32B (cont.) b.

Price Corporation T-Accounts

Assets

=

Liabilities

+

Stockholders’ Equity

Cash

Accounts Payable

Common Stock

1/1 25,000

3/1 8,400

7/5 300

4/14 400

1/1 25,000

6/30 12,000

7/5 300

Bal. 100

Bal. 25,000

8/8 1,600

9/1 18,000

9/9 4,250

11/2 500

Retained Earnings

Bal. 15,650

Unearned Revenue

Bal. -0-

12/31 6,000

6/30 12,000

Accounts Receivable

Bal. 6,000

Dividends

8/1 4,800

9/9 4,250

11/2 500

10/5 17,000

Bal. 500

Bal. 17,550

Salaries Payable

12/31 1,100

Service Revenue

Supplies

Bal. 1,100

8/1 4,800

4/14 400

12/31 350

8/8 1,600

Bal. 50

10/5 17,000

12/31 6,000

Prepaid Rent

Bal. 29,400

3/1 8,400

12/31 3,500

Bal. 4,900

Rent Expense

12/31 3,500

Bal. 3,500

Salaries Expense

9/1 18,000

12/31 1,100

Bal. 19,100

Supplies Expense

12/31 350

Bal. 350

3-137

PROBLEM 3-32B (cont.)

c.

Price Corporation

Trial Balance

December 31, 2016

Account Titles

Debit

Credit

Cash

$15,650

Accounts Receivable

17,550

Supplies

50

Prepaid Rent

4,900

Accounts Payable

$ 100

Unearned Revenue

6,000

Salaries Payable

1,100

Common Stock

25,000

Dividends

500

Service Revenue

29,400

Rent Expense

3,500

Salaries Expense

19,100

Supplies Expense

350

Totals

$61,600

$61,600

3-138

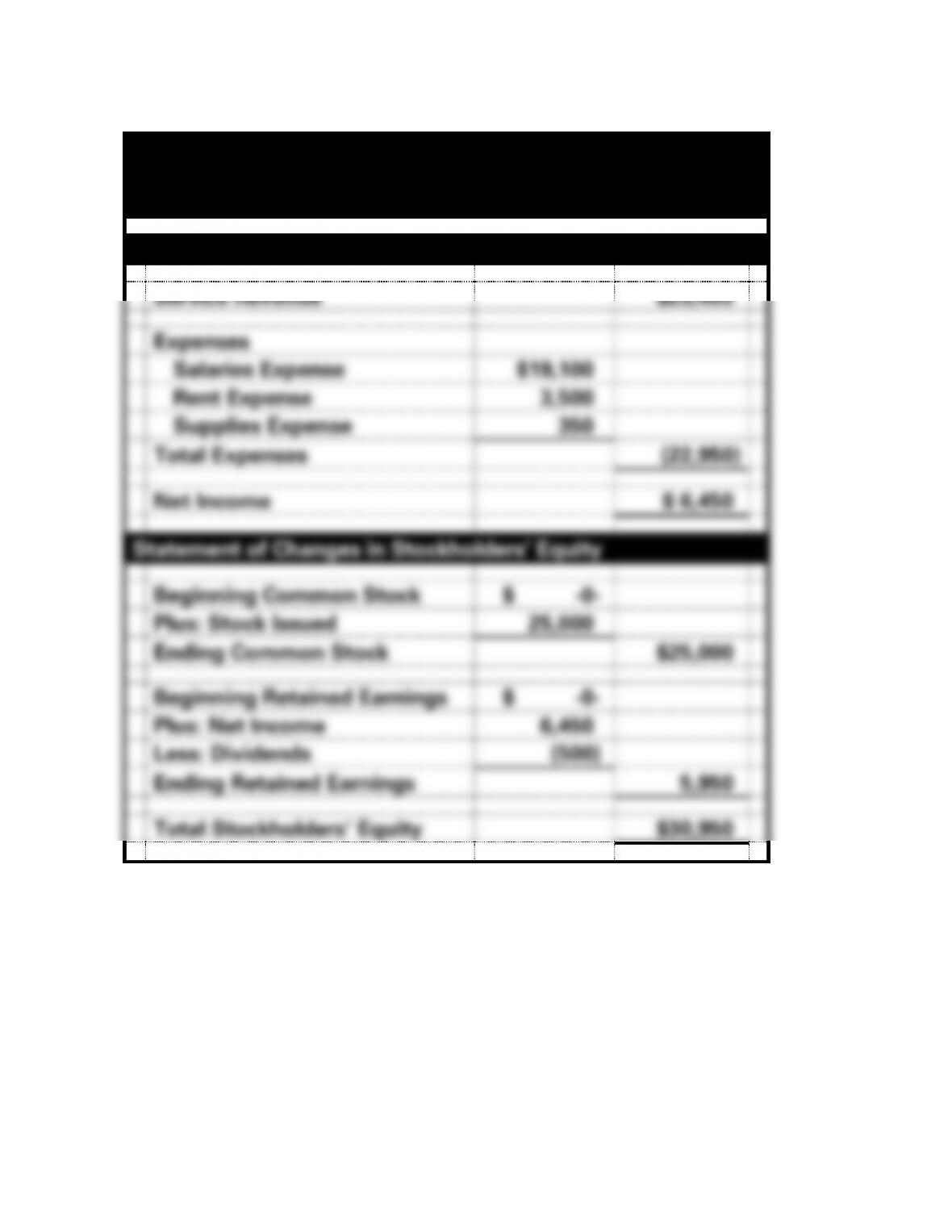

PROBLEM 3-32B (cont.)

d.

Price Corporation

Financial Statements

For the Year Ended December 31, 2016

Income Statement

Service Revenue

$29,400

Expenses

Salaries Expense

$19,100

Rent Expense

3,500

Supplies Expense

350

Total Expenses

(22,950)

Net Income

$ 6,450

Statement of Changes in Stockholders’ Equity

Beginning Common Stock

$ -0-

Plus: Stock Issued

25,000

Ending Common Stock

$25,000

Beginning Retained Earnings

$ -0-

Plus: Net Income

6,450

Less: Dividends

(500)

Ending Retained Earnings

5,950

Total Stockholders’ Equity

$30,950

3-139

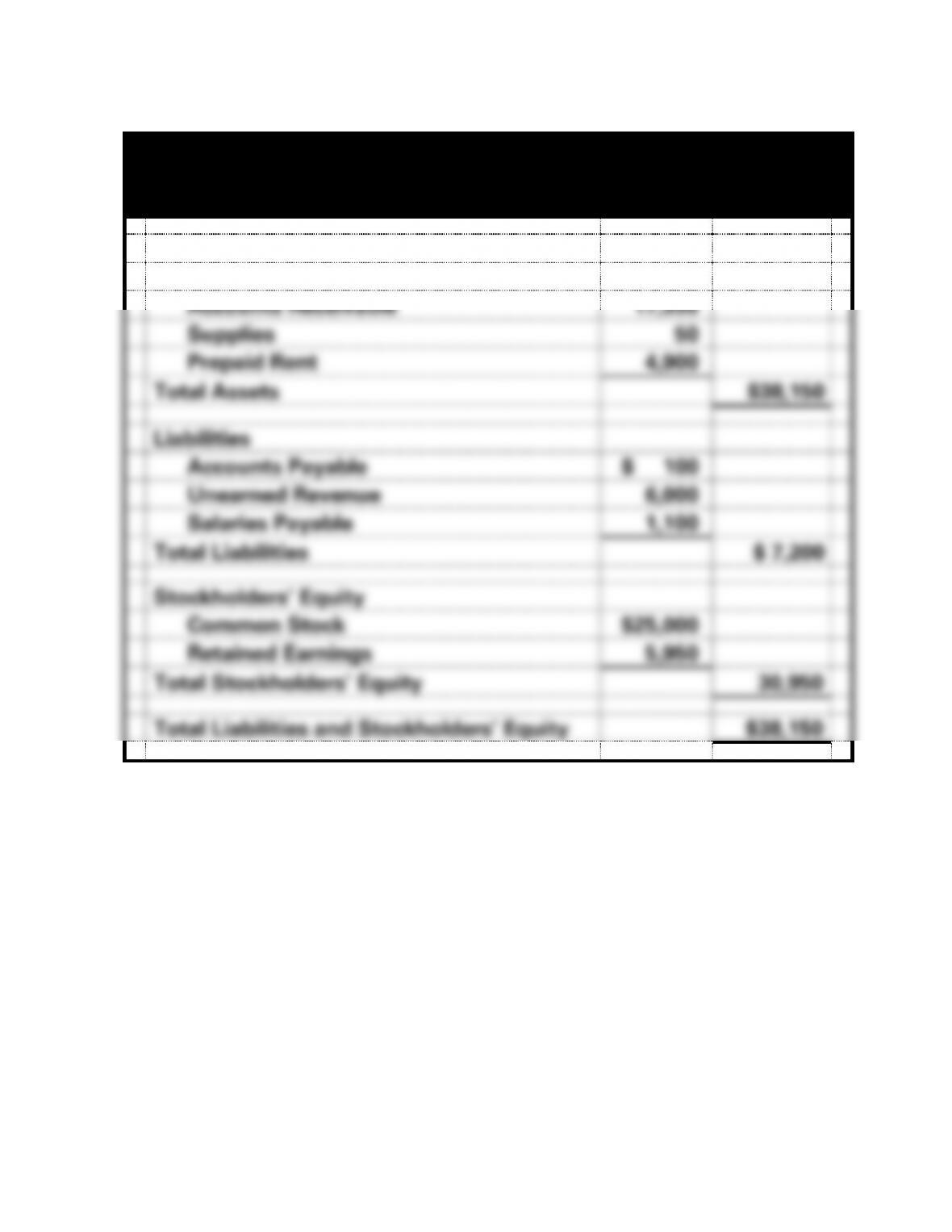

PROBLEM 3-32B d. (cont.)

Price Corporation

Balance Sheet

As of December 31, 2016

Assets

Cash

$15,650

Accounts Receivable

17,550

Supplies

50

Prepaid Rent

4,900

Total Assets

$38,150

Liabilities

Accounts Payable

$ 100

Unearned Revenue

6,000

Salaries Payable

1,100

Total Liabilities

$ 7,200

Stockholders’ Equity

Common Stock

$25,000

Retained Earnings

5,950

Total Stockholders’ Equity

30,950

Total Liabilities and Stockholders’ Equity

$38,150

3-140

PROBLEM 3-32B d. (cont.)

Price Corporation

Statement of Cash Flows

For the Year Ended December 31, 2016

Cash Flows From Operating Activities:

Received Cash from Customers*

$17,850

Paid Cash for Expenses**

(26,700)

Net Cash Flow from Operating Activities

$( 8,850)

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities:

Received Cash from Stock Issue

$25,000

Paid Cash for Dividends

(500)

Net Cash Flow from Financing Activities

24,500

Net Change in Cash

15,650

Plus: Beginning Cash Balance

-0-

Ending Cash Balance

$15,650

*(6/30) $12,000 + (8/8) $1,600 + (9/9) $4,250 = $17,850

**(3/1) $8,400 + (7/5) $300 + (9/1) $18,000 = $26,700