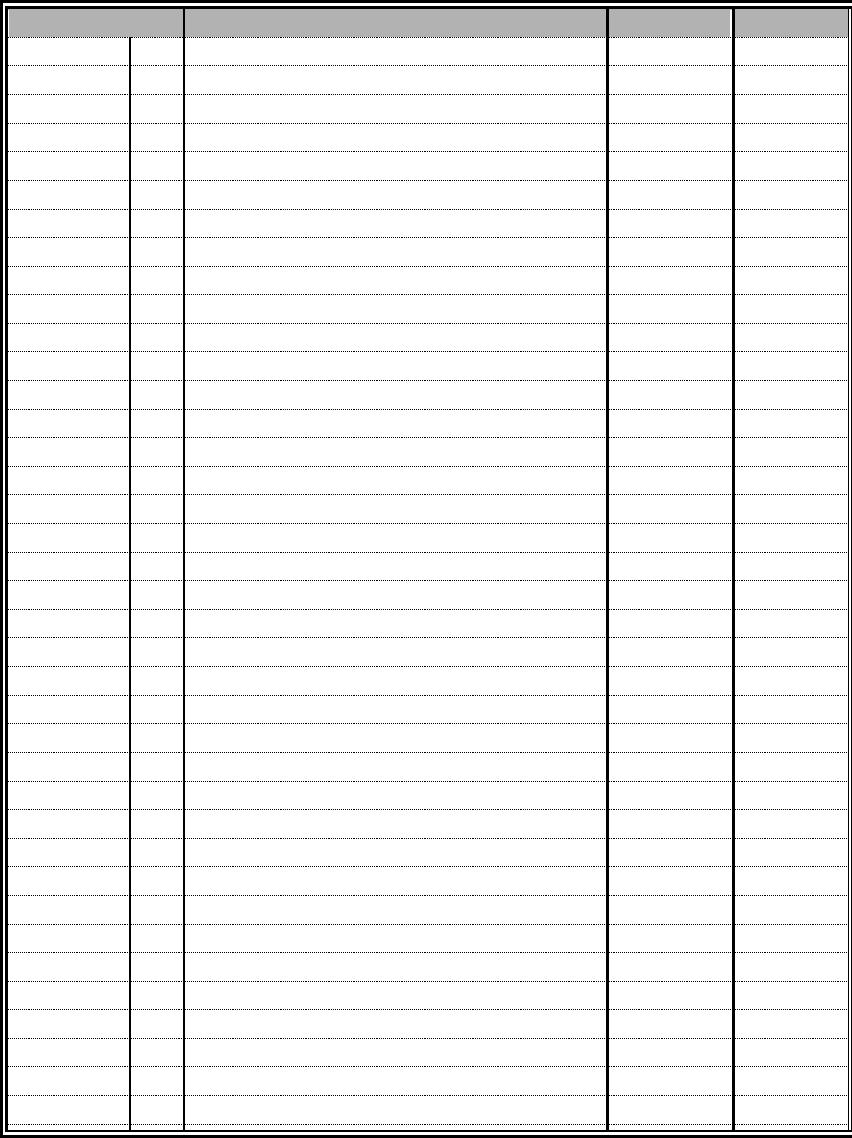

3-13

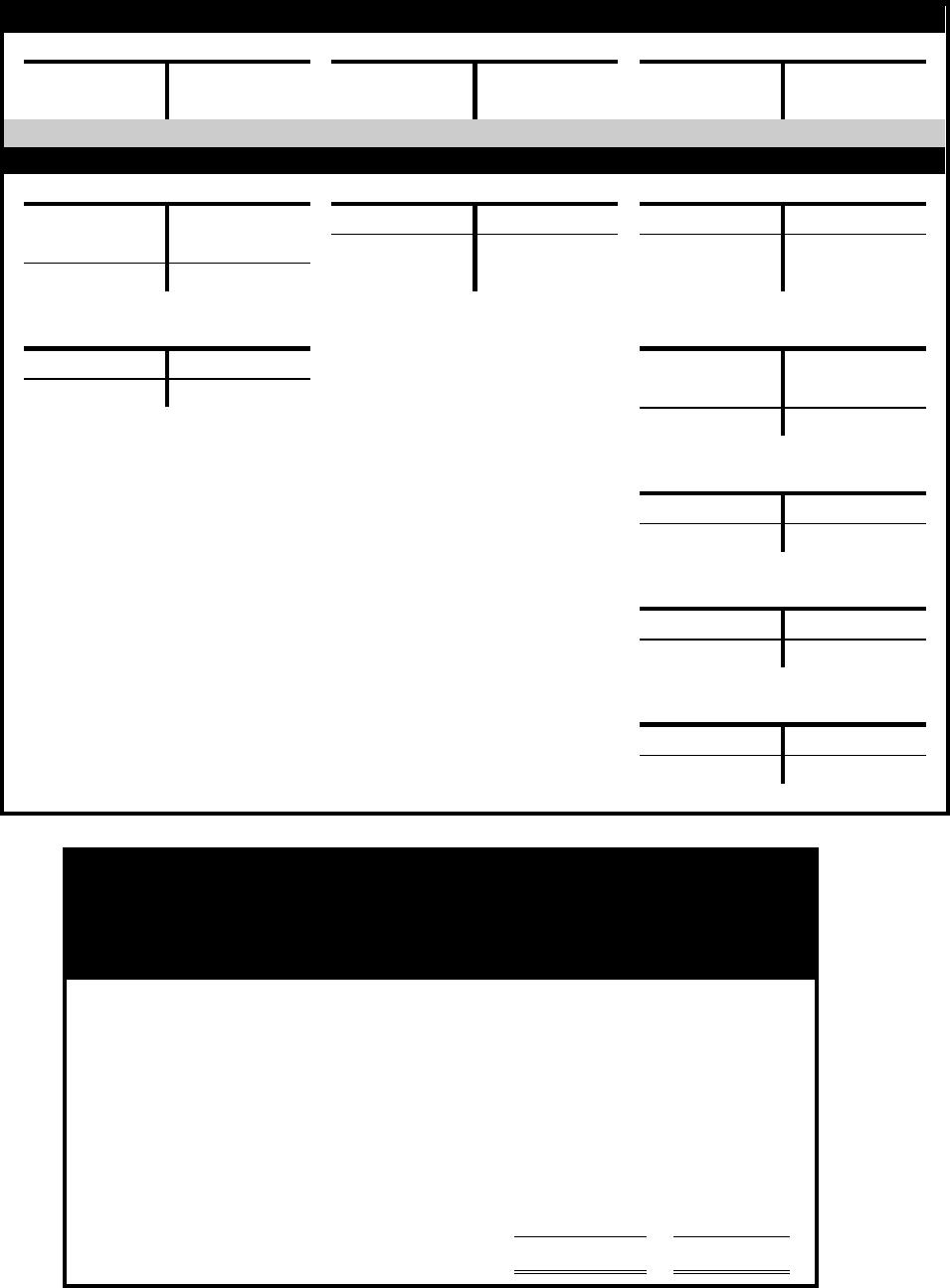

Demonstration Problem 3-2 Solution

Date

Account Titles

Debit

Credit

Event No.

1

Cash

5,000

Common Stock

5,000

Event No.

2

Cash

4,000

Notes Payable

4,000

Event No.

3

Supplies

500

Accounts Payable

500

Event No.

4

Accounts Receivable

8,000

Service Revenue

8,000

Event No.

5

Salaries Expense

3,900

Cash

3,900

Event No.

6

Prepaid Rent

2,400

Cash

2,400

Event No.

7

Office Furniture

3,500

Accounts Payable

3,500

Event No.

8

Cash

1,800

Unearned Revenue

1,800

Event No.

9

Cash

3,000

Accounts Receivable

3,000

Event No.

10

Utilities Expense

1,200

Cash

1,200

Event No.

11

Dividends

1,000

Cash

1,000

Event No.

12

Certificate of Deposit

2,000

Cash

2,000

Event No.

13

Notes Payable

1,600

Cash

1,600

Event No.

14

Land

2,700

Cash

2,700

Event No.

15

Interest Expense

400

Interest Payable

400

Event No.

16

Unearned Revenue

1,800

Service Revenue

1,800

Event No.

17

Supplies Expense

400

Supplies

400

Event No.

18

Salaries Expense

2,300

Salaries Payable

2,300

Event No.

19

Interest Receivable

150

Interest Revenue

150

3-14

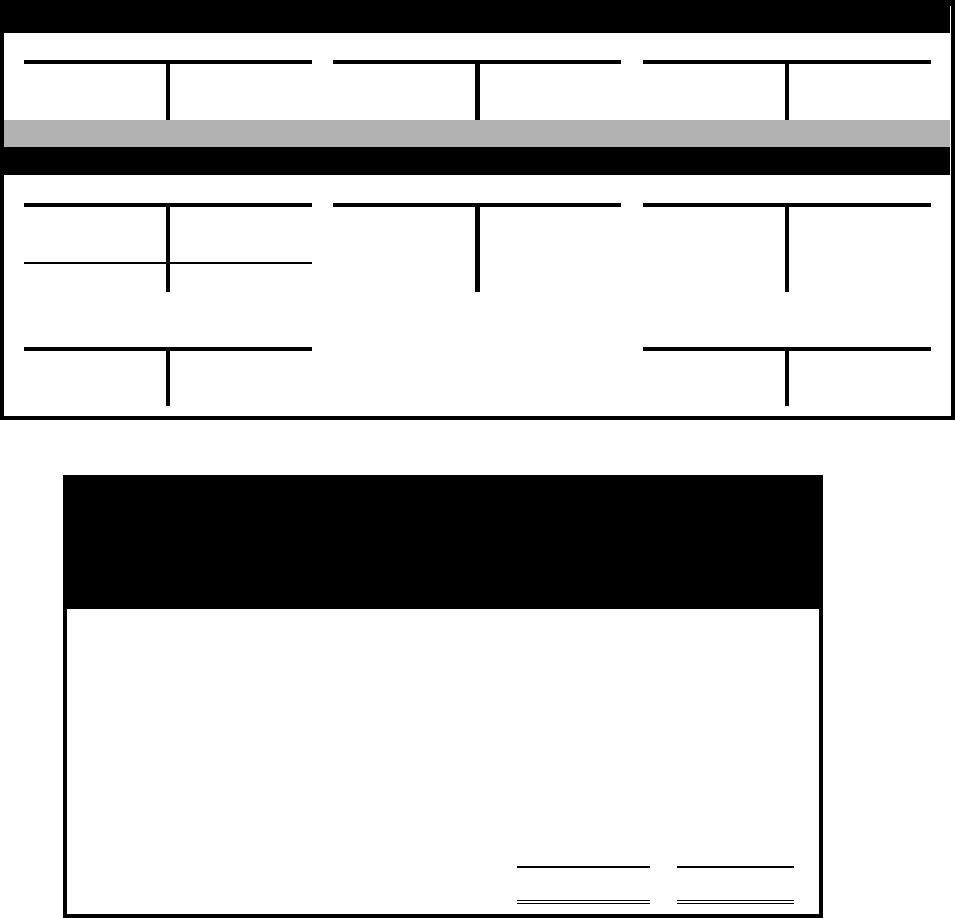

Demonstration Problem 3-1 Workpaper, part a.

T-Account Entries

Panel 1 Recording Scheme Provided for Convenience

ASSETS

LIABILITIES

EQUITY

Debit

Credit

Debit

Credit

Debit

Credit

+

–

–

+

–

+

Panel 2 Ledger T-Accounts

Cash

Unearned Revenue

Common Stock

Prepaid Rent

Dividends

Braxton Personnel Advisory Services Company

Unadjusted Trial Balance

December 31, 2015

Account Title

Debit

Credit

Cash

Prepaid rent

Unearned revenue

Common stock

Retained earnings

Services revenue

Rent expense

Dividends

Totals

7,400

7,400

3-15

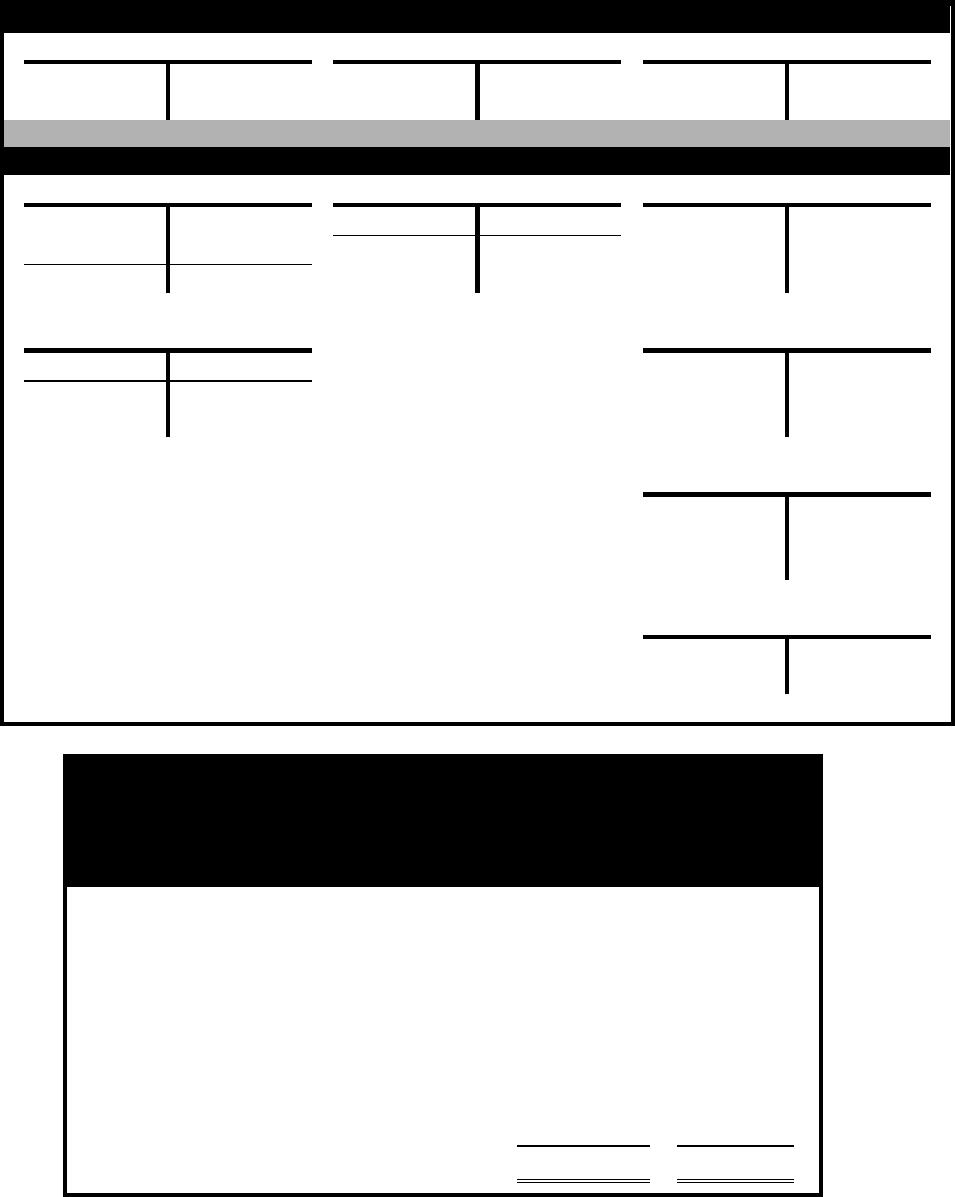

Demonstration Problem 3-1 Workpaper, part b.

T-Account Adjusting Entries

Panel 1 Recording Scheme Provided for Convenience

ASSETS

LIABILITIES

EQUITY

Debit

Credit

Debit

Credit

Debit

Credit

+

–

–

+

–

+

Panel 2 Ledger T-Accounts

Cash

Unearned Revenue

Common Stock

(1) 5,000

1,800 (2)

2,400 (3)

5,000 (1)

(3) 2,400

200 (4)

Bal. 5,400

Prepaid Rent

Services Revenue

(2) 1,800

Rent Expense

Dividends

(4) 200

Braxton Personnel Advisory Services Company

Adjusted Trial Balance

December 31, 2015

Account Title

Debit

Credit

Cash

Prepaid rent

Unearned revenue

Common stock

Retained earnings

Services revenue

Rent expense

Dividends

Totals

7,400

7,400

3-16

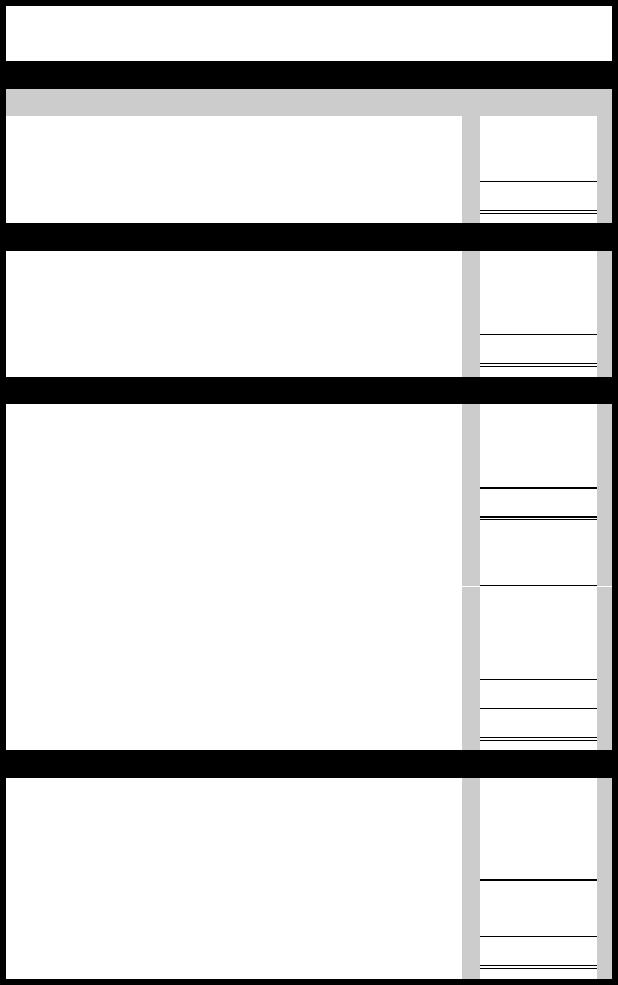

Demonstration Problem 3-1 Workpaper, part c. Financial Statements

Braxton Personnel Advisory Services Company

Financial Statements

Income Statement

For the Year Ended December 31,

2015

Services revenue

$

Rent expense

Net income

$ 350

Statement of Retained Earnings

Beginning retained earnings

$ 0

Plus: Net income

Less: Dividends

Ending retained earnings

$ 150

Balance Sheet as of December 31, 2015

Assets

Cash

$

Prepaid rent

Total assets

$ 5,550

Liabilities

Unearned revenue

$

Stockholders’ equity

Common stock

5,000

Retained earnings

Total stockholders’ equity

Total liabilities and stockholders’ equity

$

Statement of Cash Flows

Net cash flow from operating activities

$

Net cash flow from investing activities

Net cash flow from financing activities

Net change in cash

Beginning cash balance

Ending cash balance

$ 5,400

3-17

Demonstration Problem 3-1 Workpaper, part d. T-Acct. Closing Entries

Panel 1 Recording Scheme Provided for Convenience

ASSETS

LIABILITIES

EQUITY

Debit

Credit

Debit

Credit

Debit

Credit

+

−

−

+

−

+

Panel 2 Ledger T-Accounts

Cash

Unearned Revenue

Common Stock

(1) 5,000

1,800 (2)

(adj2) 2,000

2,400 (3)

5,000 (1)

(3) 2,400

200 (4)

400 Bal.

5,000 Bal.

Bal. 5,400

Prepaid Rent

Retained Earnings

(2) 1,800

1,650 (adj1)

Bal. 150

Services Revenue

2,000 (adj2)

Rent Expense

(adj1) 1,650

Dividends

(4) 200

Braxton Personnel Advisory Services Company

Post-closing Trial Balance

December 31, 2015

Account Title

Debit

Credit

Cash

Prepaid rent

Unearned revenue

Common stock

Retained earnings

Services revenue

Rent expense

Dividends

Totals

5,550

5,550

3-18

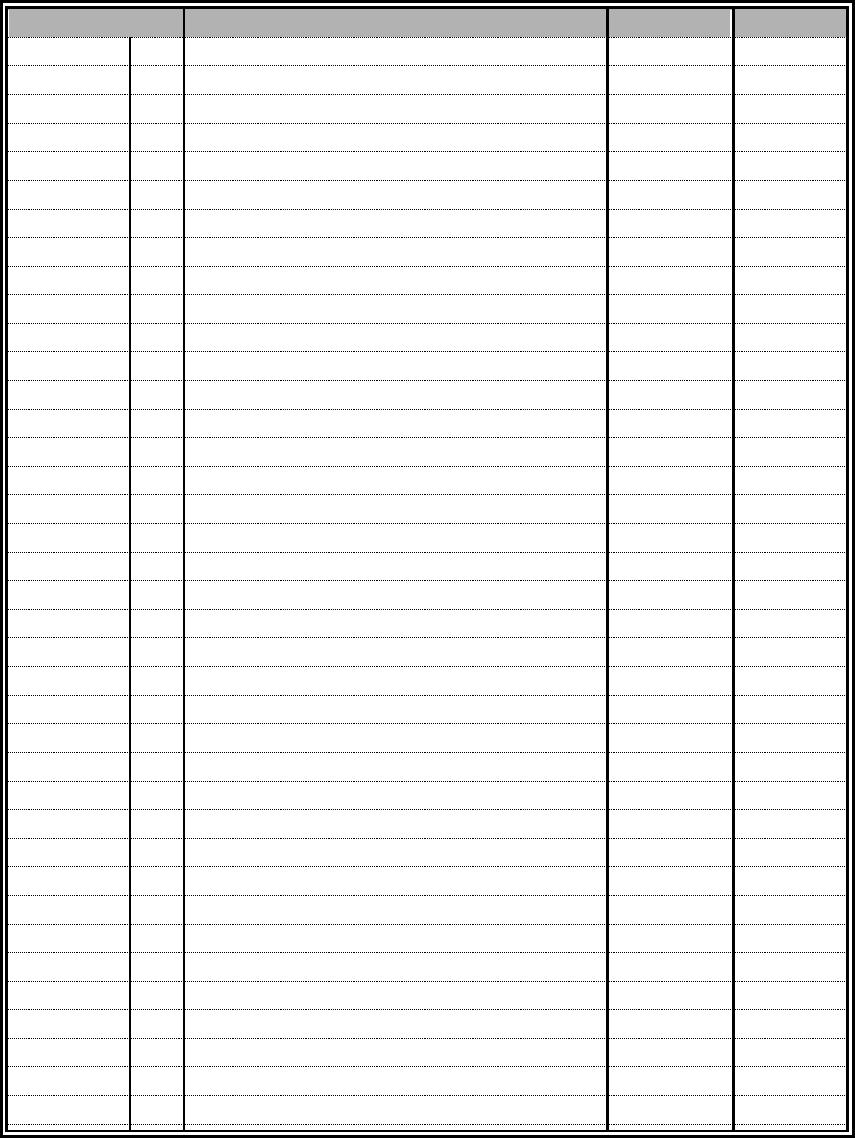

Demonstration Problem 3-2 Workpaper

Date

Account Titles

Debit

Credit

Event No.

1

Cash

5,000

Common Stock

5,000

Event No.

2

Event No.

3

Event No.

4

Event No.

5

Event No.

6

Event No.

7

Event No.

8

Event No.

9

Event No.

10

Event No.

11

Event No.

12

Event No.

13

Event No.

14

Event No.

15

Event No.

16

Event No.

17

Event No.

18

Event No.

19

3-19

Quiz Questions for Chapter 3

1. The following general journal entry was recorded in the books of Miles Company:

Accounts Payable

700

Cash

700

Based on this entry,

a. net income was unaffected.

b. assets increased.

c. equity decreased.

d. liabilities increased.

2. Company A collected $9,000 cash that was due on an account receivable. Company A’s account-

ant recorded the entry as a debit to cash and a credit to service revenue. As a result of this error

a. the totals of the trial balance will not be equal.

b. retained earnings will be overstated.

c. dividends will be understated.

d. the amount of cash will be overstated.

3. The following adjusted trial balance was drawn from the records of the Dakota Company.

Account Title Dr Cr

Cash 500

Equipment 2,000

Common Stock 1700

Retained Earnings 500

Service Revenue 900

Operating Expenses 600

——– ——–

Totals 3,100 3,100

Based on the information in the trial balance, the amount of retained earnings reported on the year–

end balance sheet would be

a. $500.

b. $600.

c. $1,400.

d. $800.

4. Which of the following statements is true?

a. Expense accounts normally have debit balances immediately before the closing entries are recorded.

b. A debit entry in an asset account will decrease the account.

c. Adjusting entries are recorded at the beginning of an accounting cycle.

d. Equal totals in a trial balance proves that no errors have been made in the recording process.

5. Recording revenue earned on account is what kind of transaction?

a. Claims exchange.

b. Asset use.

c. Asset source.

d. Asset exchange.

3-20

6. The entry to record accrued interest on a note payable involves a

a. credit to interest expense and a debit to cash.

b. debit to interest expense and a credit to interest payable.

c. credit to interest expense and a debit to interest payable.

d. credit to interest receivable and a debit to interest expense.

7. Select the true statement.

a. A debit to a liability account will increase the balance of the account.

b. A credit to a revenue account will decrease the balance of the account.

c. A debit to an asset account will increase the balance of the account.

d. A credit to the retained earnings account will decrease the balance of the account.

8. X Company mistakenly recorded the purchase of supplies on account by debiting supplies and

crediting cash. As a result of this error

a. assets are understated.

b. liabilities are overstated.

c. expenses are understated.

d. both a and b.

9. The following account balances were drawn from the adjusted trial balance of Newton, Inc.

Service revenue

$ 700

Operating expenses

400

Accounts payable

600

Unearned revenue

100

Dividends

200

Retained earnings

1,200

After the closing entries have been recorded and posted, the balance in the retained earnings ac-

count would be

a. $1,200.

b. $1,600.

c. $1,400.

d. None of the above.

10. Smith Company issued a $10,000 face value note to the National Bank on October 1, 2015. The

note had a 12 percent annual interest rate and a one-year term. Which of the following general

journal entries would be necessary to record accrued interest on December 31, 2015?

a. Interest Expense $900

Interest Payable $900

b. Interest Expense $300

Interest Payable $300

c. Interest Payable $900

Interest Expense $900

d. Interest Payable $300

Interest Expense $300

3-21

11. LMN experienced an accounting event that affected its financial statements as follows

Assets

=

Liab.

+

Equity

Rev.

–

Exp.

=

Net Inc.

Cash Flow

+

NA

+

+

NA

+

+ OA

The general journal entry to record the event must have included

a. A debit to an asset account and a credit to unearned revenue.

b. A credit to an asset account and a debit to a revenue account.

c. A debit to cash and a credit to revenue.

d. A debit to cash and a credit to accounts receivable.

12. ABC Company experienced an accounting event that is recorded in the following T-accounts:

Cash

Unearned Revenue

5,000

5,000

Which of the following reflects how this event affects the company’s financial statements?

Assets

=

Liab.

+

Equity

Rev.

–

Exp.

=

Net Inc.

Cash Flow

a.

+

+

NA

NA

+

–

+ FA

b.

+

+

NA

NA

NA

NA

+ OA

c.

+

NA

+

+

NA

+

+ OA

d.

+

+

NA

NA

NA

NA

+ FA

3-22

Quiz Answers

Question

Answer

1

A

2

B

3

D

4

A

5

C

6

B

7

C

8

A

9

D

10

B

11

C

12

B

3-23

Summary Outline of a Lesson Plan for Chapter 3

I. Introduce debit and credit rules with T-accounts. Use the equity account as

the reference point for expense and dividend accounts and use assets in general as

the reference point for contra accounts.

II. Use Demonstration Problem 3-1 to illustrate the rules of debits and credits

and to introduce trial balances. Work the problem in steps, allowing students to

work various stages before giving them the answers.

III. Use Demonstration Problem 3-2 as a drill for recording transactions in gen-

eral journal form. Use the first few transactions to demonstrate recording pro-

cedures, then have students record the remaining transactions for reinforcement.

IV. Provide an overview of the accounting cycle using a single transaction. Use

an unearned revenue transaction as the starting point. Record the journal entry,

prepare an unadjusted trial balance, record the adjusting entry, prepare an adjusted

trial balance, prepare financial statements, record the closing entry, and prepare a

post-closing trial balance.

V. Use the horizontal financial statements model to demonstrate the effects of

business events on financial statements as you deem appropriate.

VI. Enrichment. Use ATC Case 4-7 in the textbook as an enrichment exercise.