5-13

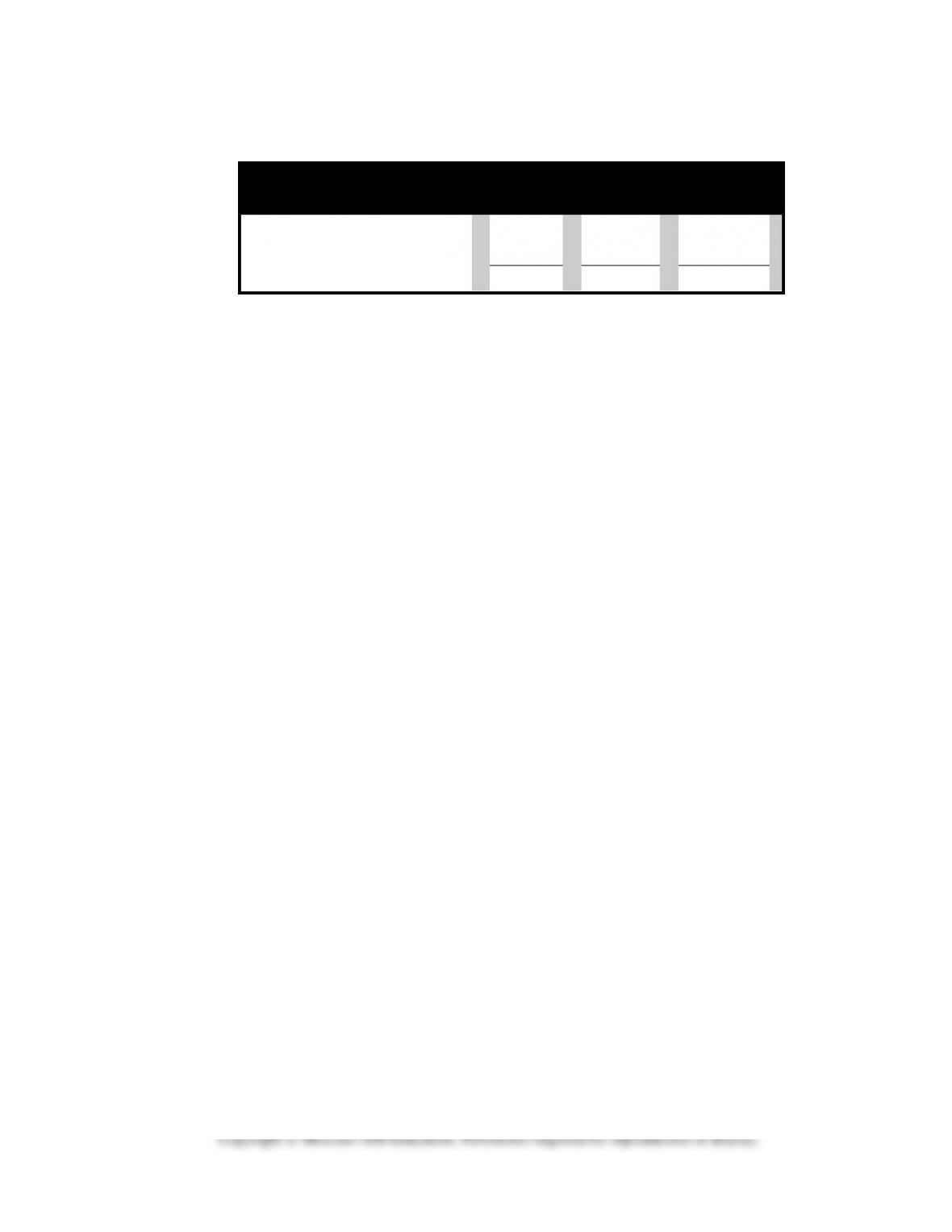

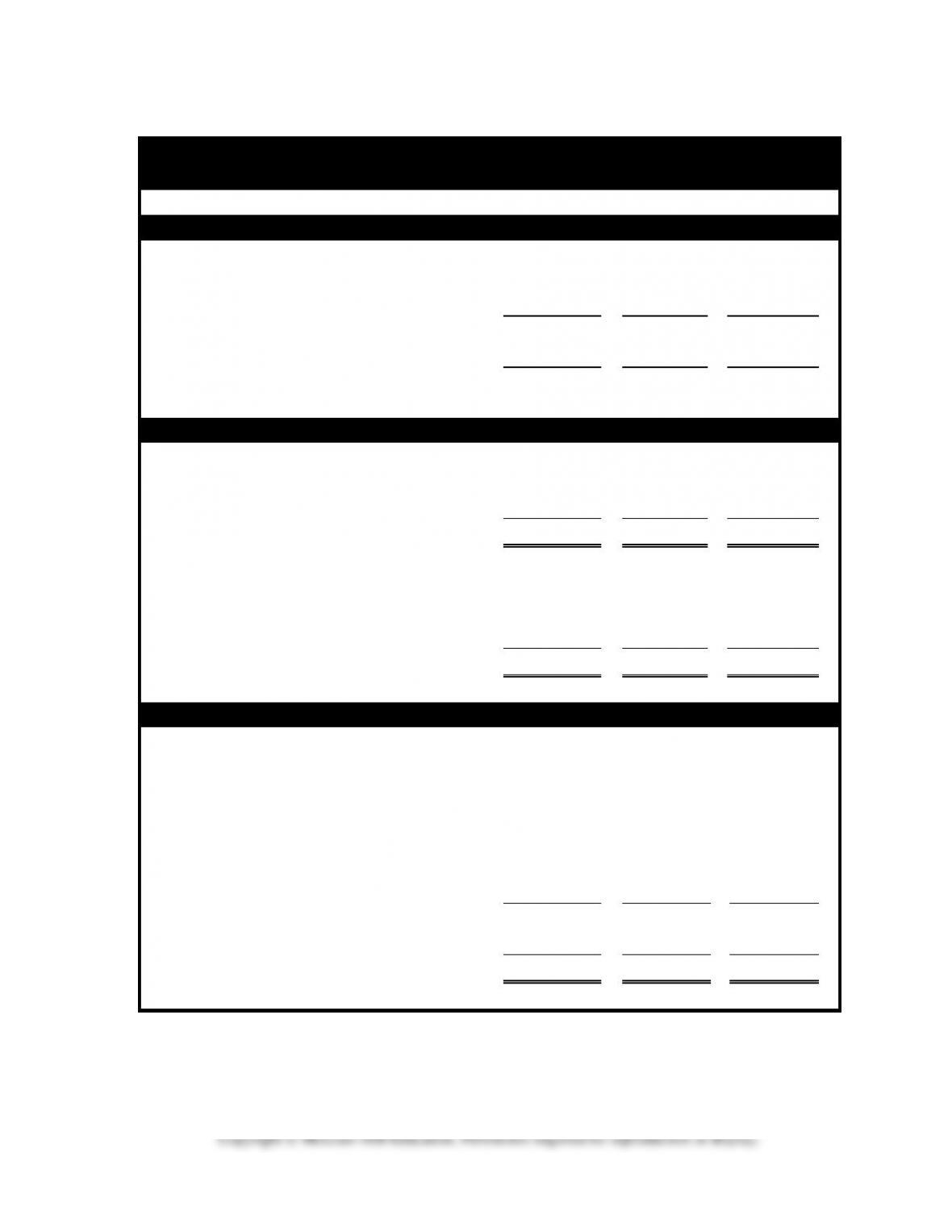

Demonstration Problem 5-3 Solution

Determination of Ending Inventory at Lower of Cost or Market

Type

Quantity

Unit

Cost

Unit

Market

Total

Cost

Total

Market

Lower of

C or M

A

100

$12.00

$15.00

$ 1,200

$ 1,500

$ 1,200

B

550

8.00

6.00

4,400

3,300

3,300

C

710

25.00

24.00

17,750

17,040

17,040

D

240

20.00

22.00

4,800

5,280

4,800

$28,150

$27,120

$26,340

Applying the lower of cost or market rule on an individual basis requires a

$1,810 write-down ($28,150 – $26,340). Use the horizontal financial state-

ments model to show the effect of the write-down on the financial state-

ments:

Assets

=

Liab.

+

Equity

Rev.

–

Exp.

=

Net Inc.

Cash Flow

(1,810)

=

0

+

(1,810)

0

–

1,810

=

(1,810)

0

5-14

Demonstration Problem 5-1 Workpaper

FIFO

LIFO

Weighted

Average

Sales

Cost of goods sold

Gross margin

5-15

Demonstration Problem 5-2 Workpaper – Inventory Summary

Crystal Apple’s 2015 inventory contains the following layers.

Units

Cost per Unit

Total Cost

Beginning balance

200

x

$18

=

$ 3,600

First purchase

800

x

20

=

16,000

Second purchase

1,200

x

24

=

28,800

Total available

2,200

$48,400

Demonstration Problem 5-2 Workpaper, part a. Ledger T-accounts

Ledger T-Accounts – FIFO Cost Flow

Cash

Accounts Payable

Common Stock

Bal. 2,000

2,500 Bal.

0 Bal.

Bal. 12,800

Inventory

Retained Earnings

Bal. 3,600

3,100 Bal.

Bal. 3,840

Sales Revenue

Cost of Goods Sold

Operating Expenses

Computation of Cost of Goods Sold using FIFO

Units

Cost per Unit

Total Cost

x

$

=

$

x

=

x

=

5-16

Demonstration Problem 5-2 Workpaper, part a. Ledger T-accounts

Ledger T-Accounts – LIFO Cost Flow

Cash

Accounts Payable

Common Stock

Bal. 2,000

2,500 Bal.

(2a) 81,600

26,000 (4)

0 Bal.

Bal. 12,800

Inventory

Retained Earnings

Bal. 3,600

3,100 Bal.

Bal. 2,880

Sales Revenue

81,600 (2a)

Cost of Goods Sold

Operating Expenses

(4) 26,000

Computation of Cost of Goods Sold using LIFO

Units

Cost per Unit

Total Cost

x

$

=

$

x

=

x

=

5-17

Demonstration Problem 5-2 Workpaper, part a. Ledger T-accounts

Ledger T-Accounts – Weighted Average Cost Flow

Cash

Accounts Payable

Common Stock

Bal. 2,000

2,500 Bal.

(2a) 81,600

26,000 (4)

0 Bal.

Bal. 12,800

Inventory

Retained Earnings

Bal. 3,600

3,100 Bal.

Bal. 3,520

Sales Revenue

81,600 (2a)

Cost of Goods Sold

Operating Expenses

(4) 26,000

Demonstration Problem 5-2 Workpaper, part a. Horizontal Financial

Statements Model

C:\ACCT 2100\

Edmonds 7e Instructor

Computation of Cost of Goods Sold using WA

Cost per Unit = $ ÷ units = $

Units

Cost per Unit

Total Cost

x

$

=

$

5-18

Demonstration Problem 5-2 Workpaper, part b. Financial Statements

Crystal Apple Sales Company

Comparative Financial Statements

Income Statements for the Year Ended December 31, 2015

FIFO

LIFO

Wt. Avg.

Sales

$81,600

$81,600

$81,600

Cost of goods sold

Gross margin

37,040

36,080

36,720

Operating expenses

Net Income

$11,040

$10,080

$10,720

Balance Sheets at December 31, 2015

Assets

FIFO

LIFO

Wt. Avg.

Cash

Inventory

Total assets

$16,640

$15,680

$16,320

Stockholders’ equity

Common stock

$ 2,500

$ 2,500

$ 2,500

Retained earnings

Total stockholders’ equity

Statements of Cash Flows for the Year Ended December 31, 2015

Cash flow from oper. activities

FIFO

LIFO

Wt. Avg.

Cash inflow from customers

$81,600

$81,600

$81,600

Cash outflow for inventory

Cash outflow for oper. exp.

Net cash inflow from oper. act.

10,800

10,800

10,800

Cash flow from investing act.

0

0

0

Cash flow from financing act.

0

0

0

Net increase in cash

10,800

10,800

10,800

Beginning cash balance

2,000

2,000

2,000

Ending cash balance

$12,800

$12,800

$12,800

5-19

Demonstration Problem 5-3 Workpaper

Determination of Ending Inventory at Lower of Cost or Market

Type

Quantity

Unit

Cost

Unit

Market

Total

Cost

Total

Market

Lower of

C or M

A

100

$12.00

$15.00

$

$

$

B

550

8.00

6.00

C

710

25.00

24.00

D

240

20.00

22.00

$28,150

$27,120

$26,340

Applying the lower of cost or market rule on an individual basis requires a

$1,810 write-down ($28,150 – $26,340). Use the statements model to show

the effect of the write-down on the financial statements:

Assets

=

Liab.

+

Equity

Rev.

–

Exp.

=

Net Inc.

Cash Flow

=

+

–

=

5-20

Quiz Questions for Chapter 5

The following data apply to the next three questions.

Units

Price

Beginning inventory

200

$1.20

First purchase

400

$1.30

Second purchase

250

$1.40

Sales

550

$2.00

1. Assuming a FIFO cost flow, the amount of gross margin reported on the income statement would be

a. $415.

b. $695.

c. $405.

d. None of the above.

2. Assuming a LIFO cost flow, the amount of ending inventory reported on the balance sheet would be

a. $240.

b. $370.

c. $130.

d. $415.

3. Assuming a weighted average cost flow, the amount of ending inventory reported on the balance sheet

would be closest to:

a. $392.

b. $415.

c. $370.

d. $417.

4. In a period of rising prices, which inventory cost flow method results in the lowest balance sheet figure for

inventory?

a. Weighted average.

b. FIFO.

c. LIFO.

d. Cannot tell without more information.

5. In a period of rising prices, which inventory cost flow method results in the lowest income tax liability, all

other things being equal?

a. Weighted average.

b. FIFO.

c. LIFO.

d. Both a and b.

6. Which of the following statements is true regarding how cost of goods sold is determined under the perpet-

ual inventory system using LIFO?

a. The units sold are multiplied by the first costs in inventory.

b. The units sold are multiplied by the last costs in inventory.

c. Multiply the units in ending inventory by the last costs in inventory. This amount is subtracted from

cost of goods available for sale.

d. The cost of goods available for sale is divided by total units to get an average cost which is multiplied

by units sold.

5-21

7. The following information was taken from the records of Trudy’s Trinkets:

Cost

Market Value

Item

Quantity

per Unit

per Unit

A

50

$24

$18

B

20

40

42

C

10

20

10

Trudy’s reports inventory at the lower of cost or market (applied individually). The necessary adjusting

entry would

a. reduce assets and equity by $400.

b. increase assets and equity by $2,200.

c. reduce assets and equity by $360.

d. reduce assets and increase liabilities by $400.

8. Tucker Company uses the periodic inventory method and wants to estimate the amount of ending inventory

in order to prepare quarterly financial statements. Sales for the quarter were $13,000. Based on historical

records, the company earns an average gross margin of 25 percent on sales. Beginning inventory for the

quarter was $3,500 and purchases were $7,100. The amount of ending inventory was

a. $3,250.

b. $850.

c. $10,600.

d. $9,750.

Use the following information to answer the next two questions. ABC Company reports the following in-

formation about inventory activity for 2015:

Quantity

Per Unit

Cost/Sales

Price

Beginning inventory

200

$2.00

1st purchase

150

$2.10

2nd purchase

110

$2.15

Sales

220

$3.20

9. Assuming the company uses the periodic inventory method and LIFO cost flow, cost of goods sold reported

on the 2015 income statement would be

a. $473.00.

b. $704.00.

c. $455.00.

d. $467.50.

10. Using the moving weighted average inventory cost flow method, the average unit cost after the first pur-

chase would be (rounded to the nearest penny),

a. $2.15.

b. $2.12.

c. $2.04.

d. $2.09.

5-22

Quiz Answers

Question

Answer

1

C

2

B

3

A

4

C

5

C

6

B

7

A

8

B

9

D

10

C

Copyright © McGraw-Hill Education. Permission required for reproduction or display.

5-23

Summary Outline of a Lesson Plan for Chapter 5

I. Use Demonstration Problem 5-1, a two-layer, single-product model to introduce

the cost flow methods. Make up a similar problem for students to work in class.

II. Demonstration Problem 5-2 introduces accounting for inventories with multiple

layers and prices. Have students use a vertical format to prepare income statements,

balance sheets, and statements of cash flows. Once they have prepared the state-

ments, have them make the following observations.

A. The cost flow method does not affect revenue.

B. The amount of cost of goods sold plus ending inventory is equal to the amount of

cost of goods available for sale. The total product cost is the same for all cost

flow methods. The difference lies in how the cost is allocated between cost of

goods sold and ending inventory.

C. With the exception of tax consequences, cash flow is not affected by the cost flow

method.

III. The text covers accounting for inventories when purchases and sales occur in-

termittently. To cover this subject, use Exercise 5-8 A or B as a demonstration prob-

lem and Exercise 5-9 A or B as a follow-up problem.

IV. Use Demonstration Problem 5-3 to show students how to write down inventory

to lower of cost or market. Use the horizontal financial statements model to illus-

trate the effect of the write-down on the financial statements.

V. The text covers the gross margin method of estimating the ending inventory bal-

ance. Use Exercise 5-12 A or B to illustrate this approach to inventory estimation.

VI. Use Exercise 5-14 A or B to illustrate the effects of inventory misstatements on

the elements of financial statements.

VII. Time considerations and homework assignments. Allow at least one hour to cover

the inventory topics in this chapter. Select homework assignments from the follow-

ing problems: Problems 5-19 A or B (cost flow methods); 5-20 A or B (lower of cost

or market); and 5-21 A or B (inventory estimation).