1-115

PROBLEM 1-32B b. (cont.)

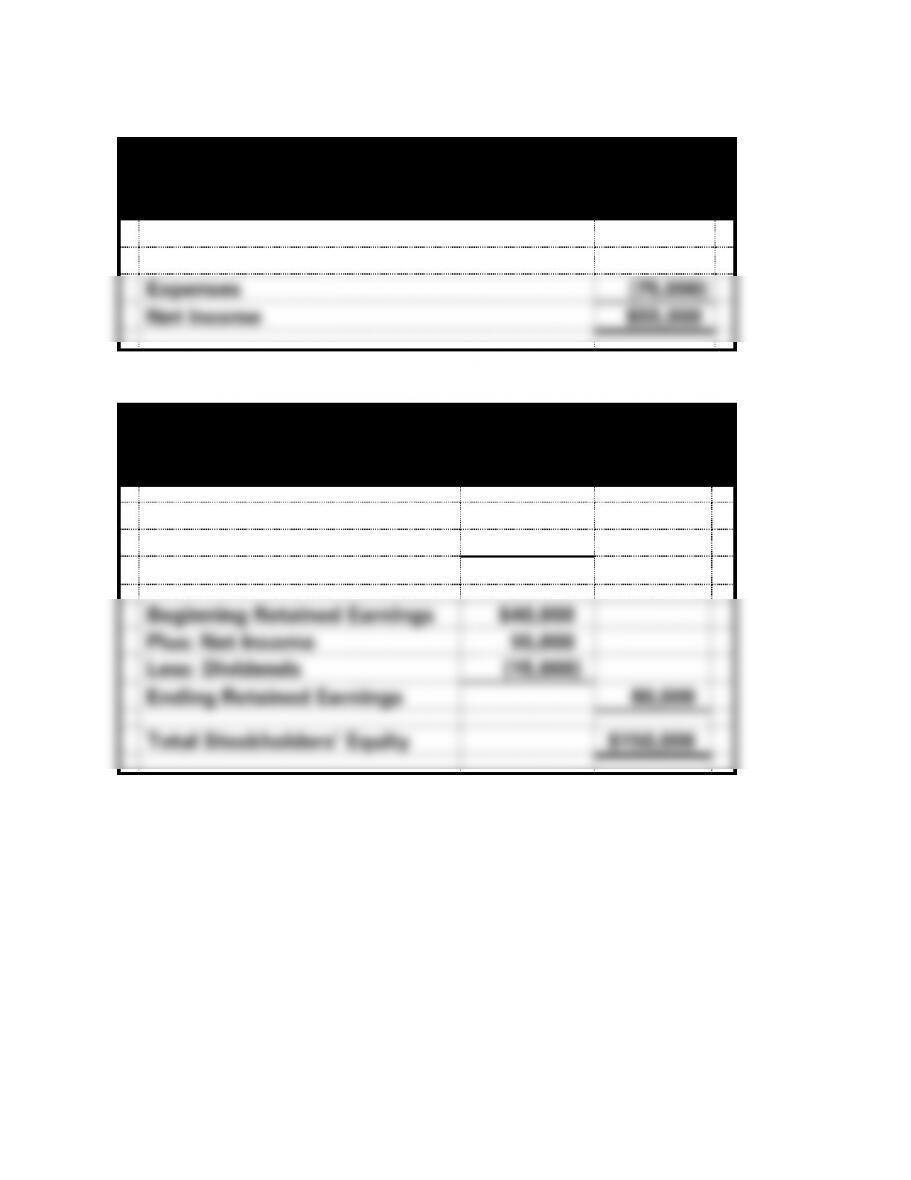

Marco’s Consulting

Income Statement

For the Period Ended December 31, 2017

Service Revenue

$130,000

Expenses

(75,000)

Net Income

$55,000

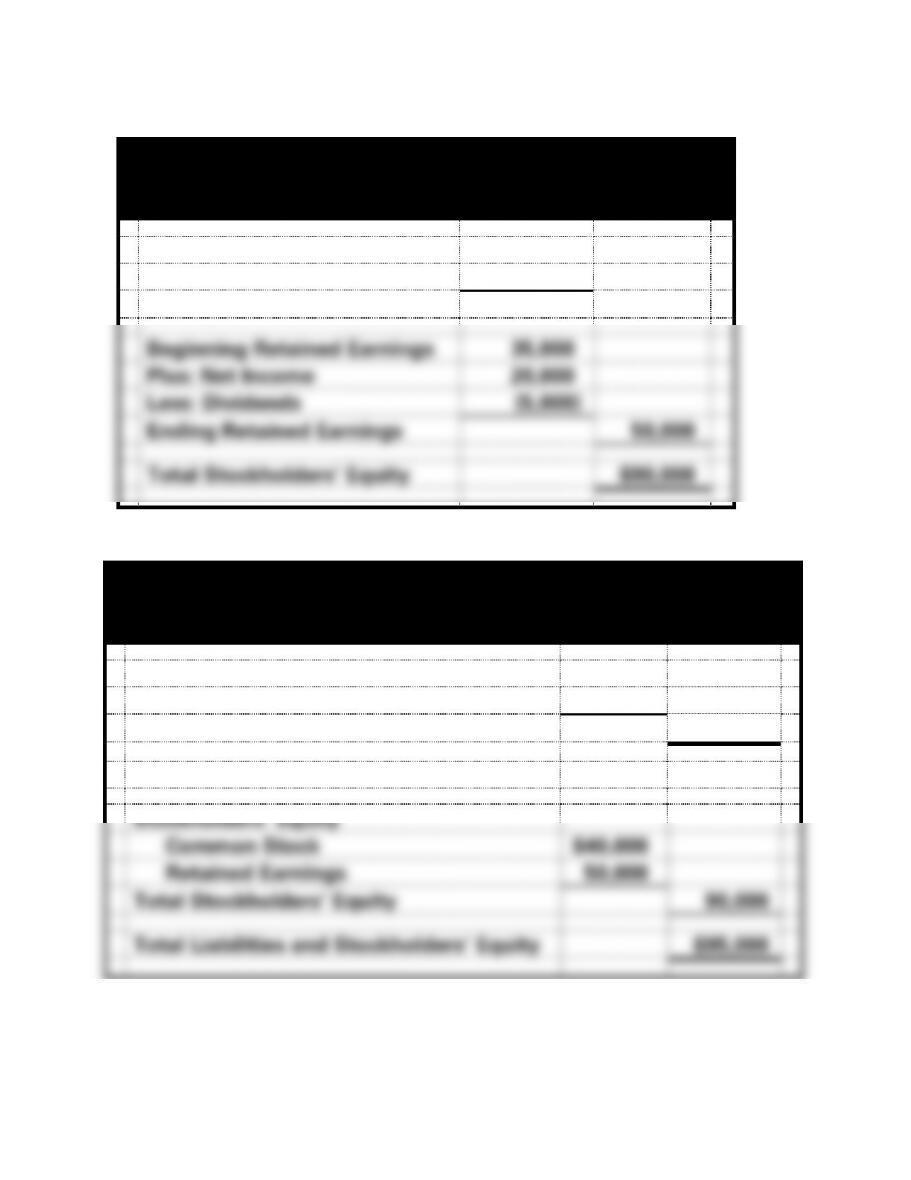

Marco’s Consulting

Statement of Changes in Stockholders’ Equity

For the Period Ended December 31, 2017

Beginning Common Stock

$50,000

Plus: Common Stock Issued

20,000

Ending Common Stock

$ 70,000

Beginning Retained Earnings

$40,000

Plus: Net Income

55,000

Less: Dividends

(15,000)

Ending Retained Earnings

80,000

Total Stockholders’ Equity

$150,000

1-116

PROBLEM 1-32B b. (cont.)

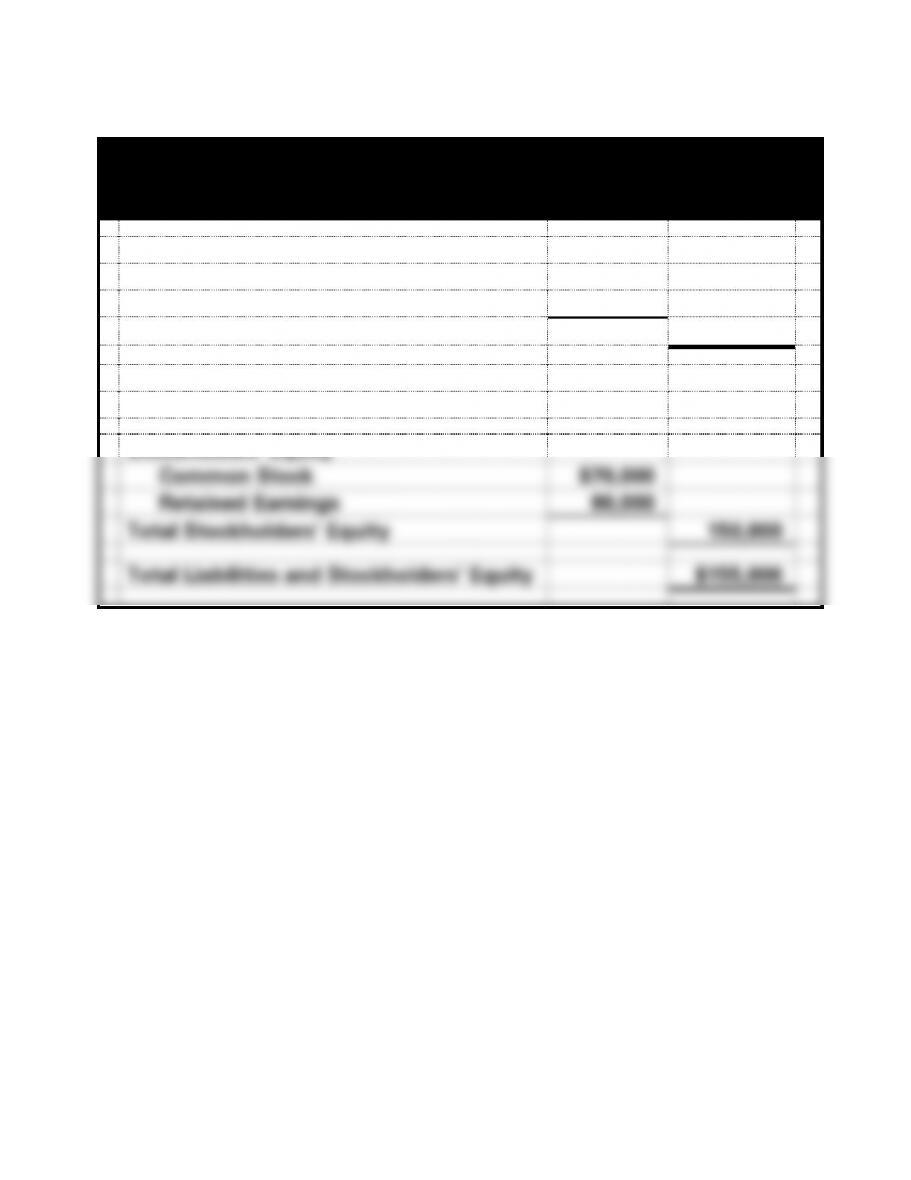

Marco’s Consulting

Balance Sheet

As of December 31, 2017

Assets

Cash

$115,000

Land

40,000

Total Assets

$155,000

Liabilities

Notes Payable

$ 5,000

Stockholders’ Equity

Common Stock

$70,000

Retained Earnings

80,000

Total Stockholders’ Equity

150,000

Total Liabilities and Stockholders’ Equity

$155,000

1-117

PROBLEM 1-32B b. (cont.)

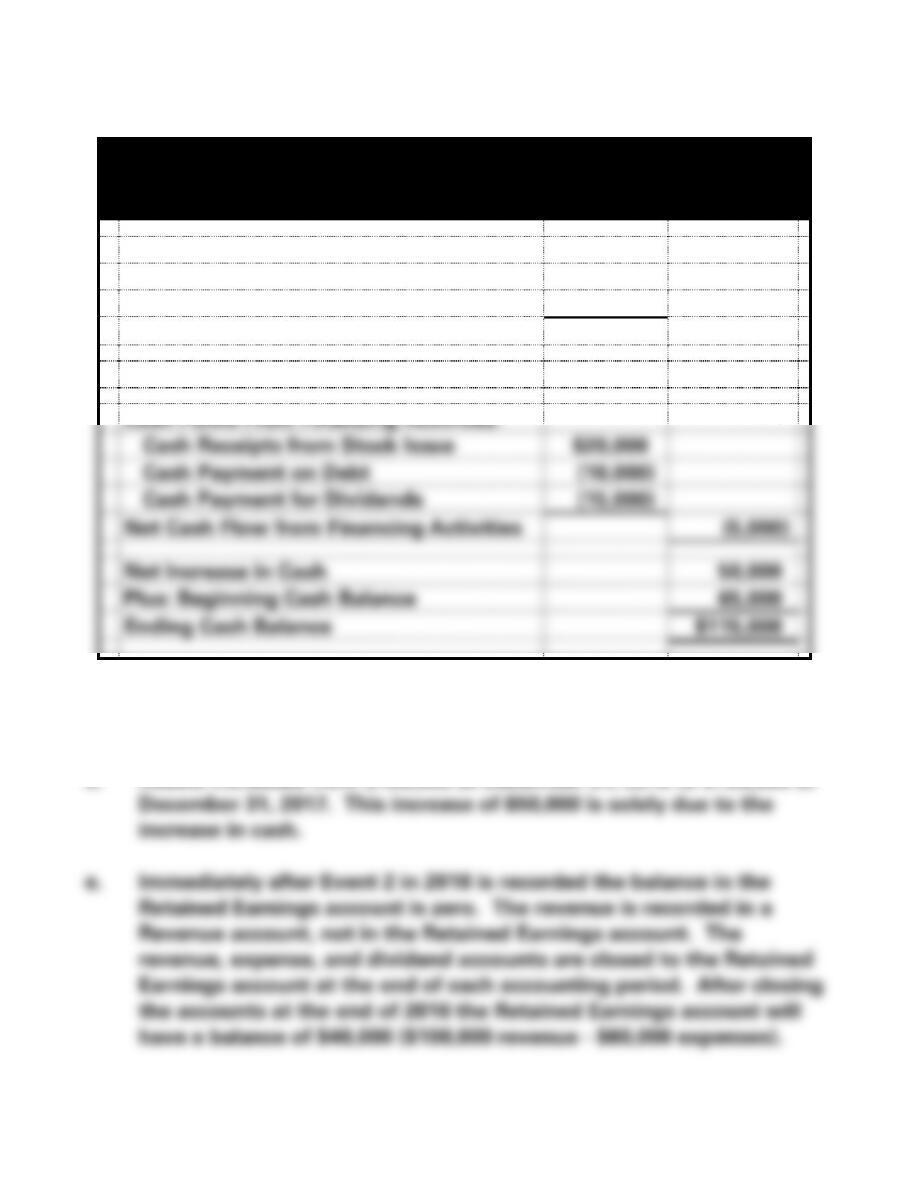

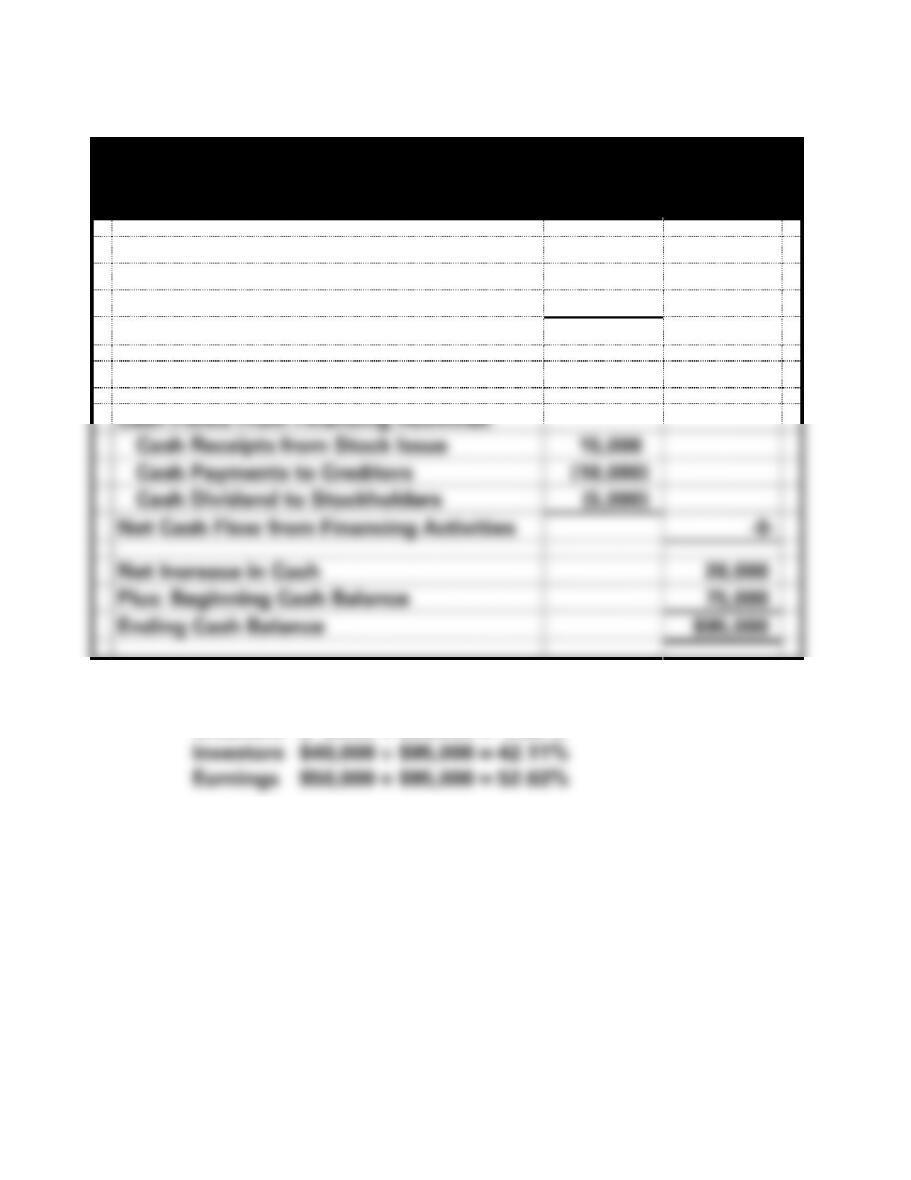

Marco’s Consulting

Statement of Cash Flows

For the Year Ended December 31, 2017

Cash Flows From Operating Activities:

Cash Receipts from Customers

$130,000

Cash Payments for Expenses

(75,000)

Net Cash Flow from Operating Activities

$55,000

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities:

Cash Receipts from Stock Issue

$20,000

Cash Payment on Debt

(10,000)

Cash Payment for Dividends

(15,000)

Net Cash Flow from Financing Activities

(5,000)

Net Increase in Cash

50,000

Plus: Beginning Cash Balance

65,000

Ending Cash Balance

$115,000

c. Retained earnings does not contain cash.

d. Assets increased from $105,000 at December 31, 2016 to $155,000 at

1-118

PROBLEM 1-32B (cont.)

The 2016 ending balance in Retained Earnings becomes next year’s

1-119

PROBLEM 1-33B

Not required:

Pearson Enterprises

Accounting Equation

Assets

=

Liabilities

+

Stockholders’ Equity

Cash

=

Liabilities

+

Common

Stock

+

Retained

Earnings

Beg. Balances

75,000

15,000

25,000

35,000

Earned Revenue

46,000

46,000

Paid Expenses

(26,000)

(26,000)

Paid Dividends

(5,000)

(5,000)

Issued Stock

15,000

15,000

Paid Liability

(10,000)

(10,000)

95,000

=

5,000

+

40,000

+

50,000

a.

Pearson Enterprises

Income Statement

For the Period Ended December 31, 2016

Revenue

$46,000

Expenses

(26,000)

Net Income

$20,000

1-120

PROBLEM 1-33B a. (cont.)

Pearson Enterprises

Statement of Changes in Stockholders’ Equity

For the Period Ended December 31, 2016

Beginning Common Stock

$25,000

Plus: Common Stock Issued

15,000

Ending Common Stock

$40,000

Beginning Retained Earnings

35,000

Plus: Net Income

20,000

Less: Dividends

(5,000)

Ending Retained Earnings

50,000

Total Stockholders’ Equity

$90,000

Pearson Enterprises

Balance Sheet

As of December 31, 2016

Assets

Cash

$95,000

Total Assets

$95,000

Liabilities

$ 5,000

Stockholders’ Equity

Common Stock

$40,000

Retained Earnings

50,000

Total Stockholders’ Equity

90,000

Total Liabilities and Stockholders’ Equity

$95,000

1-121

PROBLEM 1-33B a. (cont.)

Pearson Enterprises

Statement of Cash Flows

For the Year Ended December 31, 2017

Cash Flows From Operating Activities:

Cash Receipts from Customers

$46,000

Cash Payments for Expenses

(26,000)

Net Cash Flow from Operating Activities

$20,000

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities:

Cash Receipts from Stock Issue

15,000

Cash Payments to Creditors

(10,000)

Cash Dividend to Stockholders

(5,000)

Net Cash Flow from Financing Activities

-0-

Net Increase in Cash

20,000

Plus: Beginning Cash Balance

75,000

Ending Cash Balance

$95,000

b. Percentage of assets provided by:

Creditors $ 5,000 ÷ $95,000 = 5.26%

c. The balance in the temporary accounts, revenue, expenses and

dividends will be zero on January 1, 2017, because they were closed

to Retained Earnings at December 31, 2016.

1-122

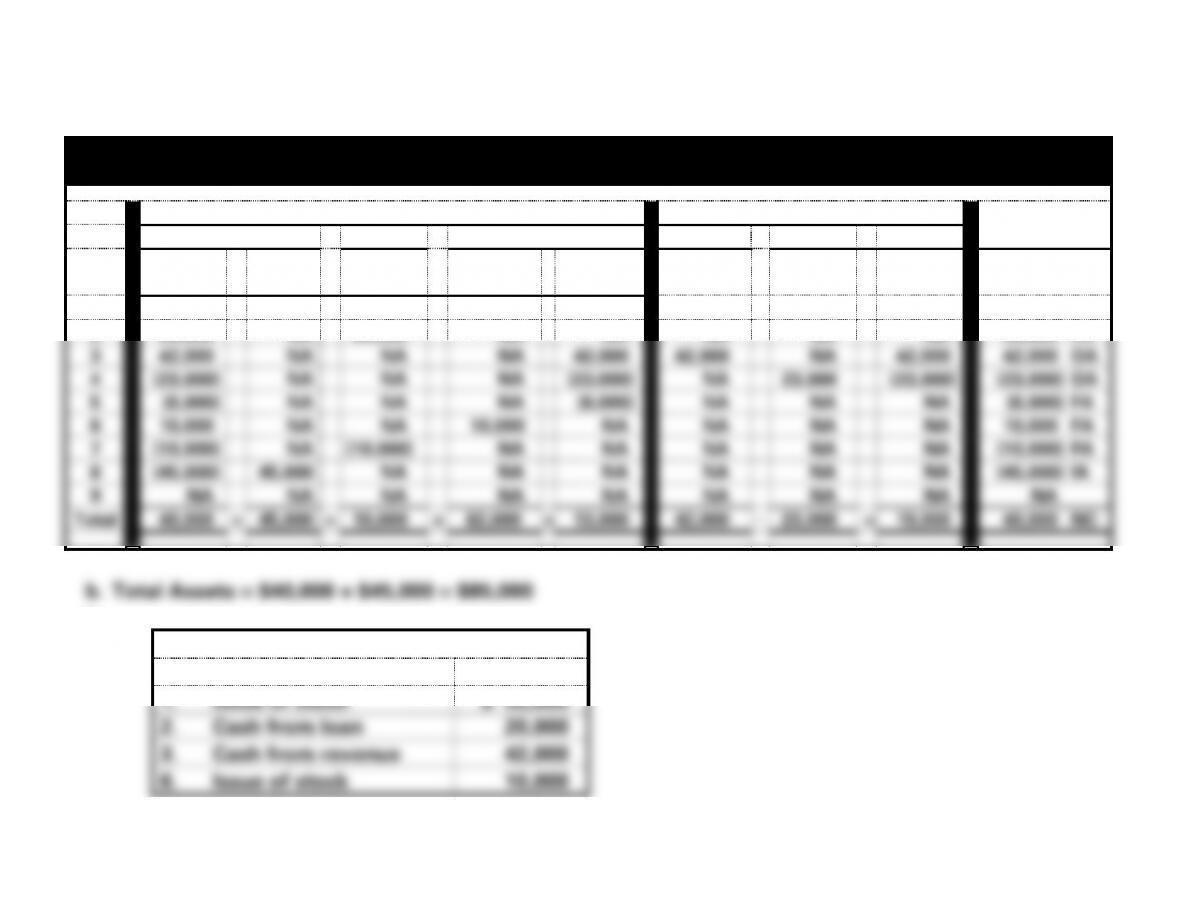

PROBLEM 1-34B

a.

Daley Company

Horizontal Statements Model for 2016

Balance Sheet

Income Statement

Statement of

Assets

=

Liab.

+

Stockholders’ Equity

Revenue

−

Expense

=

Net Inc.

Cash Flows

Event

No.

Cash

+

Land

=

Notes

Payable

+

Common

Stock

+

Retained

Earnings

1

52,000

NA

NA

52,000

NA

NA

NA

NA

52,000 FA

2

20,000

NA

20,000

NA

NA

NA

NA

NA

20,000 FA

3

42,000

NA

NA

NA

42,000

42,000

NA

42,000

42,000 OA

4

(23,000)

NA

NA

NA

(23,000)

NA

23,000

(23,000)

(23,000) OA

5

(6,000)

NA

NA

NA

(6,000)

NA

NA

NA

(6,000) FA

6

10,000

NA

NA

10,000

NA

NA

NA

NA

10,000 FA

7

(10,000)

NA

(10,000)

NA

NA

NA

NA

NA

(10,000) FA

8

(45,000)

45,000

NA

NA

NA

NA

NA

NA

(45,000) IA

9

NA

NA

NA

NA

NA

NA

NA

NA

NA

Total

40,000

+

45,000

=

10,000

+

62,000

+

13,000

42,000

−

23,000

=

19,000

40,000 NC

b. Total Assets = $40,000 + $45,000 = $85,000

c.

Sources of Assets

Event

1. Issue of stock

$ 52,000

2. Cash from loan

20,000

3. Cash from revenue

42,000

6. Issue of stock

10,000

1-123

Total Sources of Assets

$124,000

1-114

PROBLEM 1-34B (cont.)

d. Net income is $19,000 (see part a.) Dividends are not expenses so they

do not appear on the income statement.

e.

Operating Activities:

Cash from customers

$42,000

Cash paid for expenses

(23,000)

Net Cash Flow from Operating Activities

$19,000

Investing Activities:

Cash paid to purchase land

$(45,000)

Net Cash Flow from Investing Activities

$(45,000)

Financing Activities:

Cash from stock issues ($52,000 + $10,000)

$62,000

Cash from loan

20,000

Paid cash dividend

(6,000)

Cash paid on loan principal

(10,000)

Net Cash Flow from Financing Activities

$66,000

f. Percentage of assets provided by:

Creditors $10,000 ÷ $85,000 = 11.76%

Investors $62,000 ÷ $85,000 = 72.94%

Earnings $13,000 ÷ $85,000 = 15.29%

g. Zero. The revenue is recorded in a Revenue account not in the

Retained Earnings account. The balance in the Revenue account is

transferred to Retained Earnings at the end of the accounting period

through the closing process.

1-115

SOLUTIONS TO ANALYZE, THINK, COMMUNICATE – CHAPTER 1

ATC 1-1 (All dollar amounts are in millions.)

a. $ 1,971

b. Net income decreased by $1,028

STOCKHOLDERS’

1-116

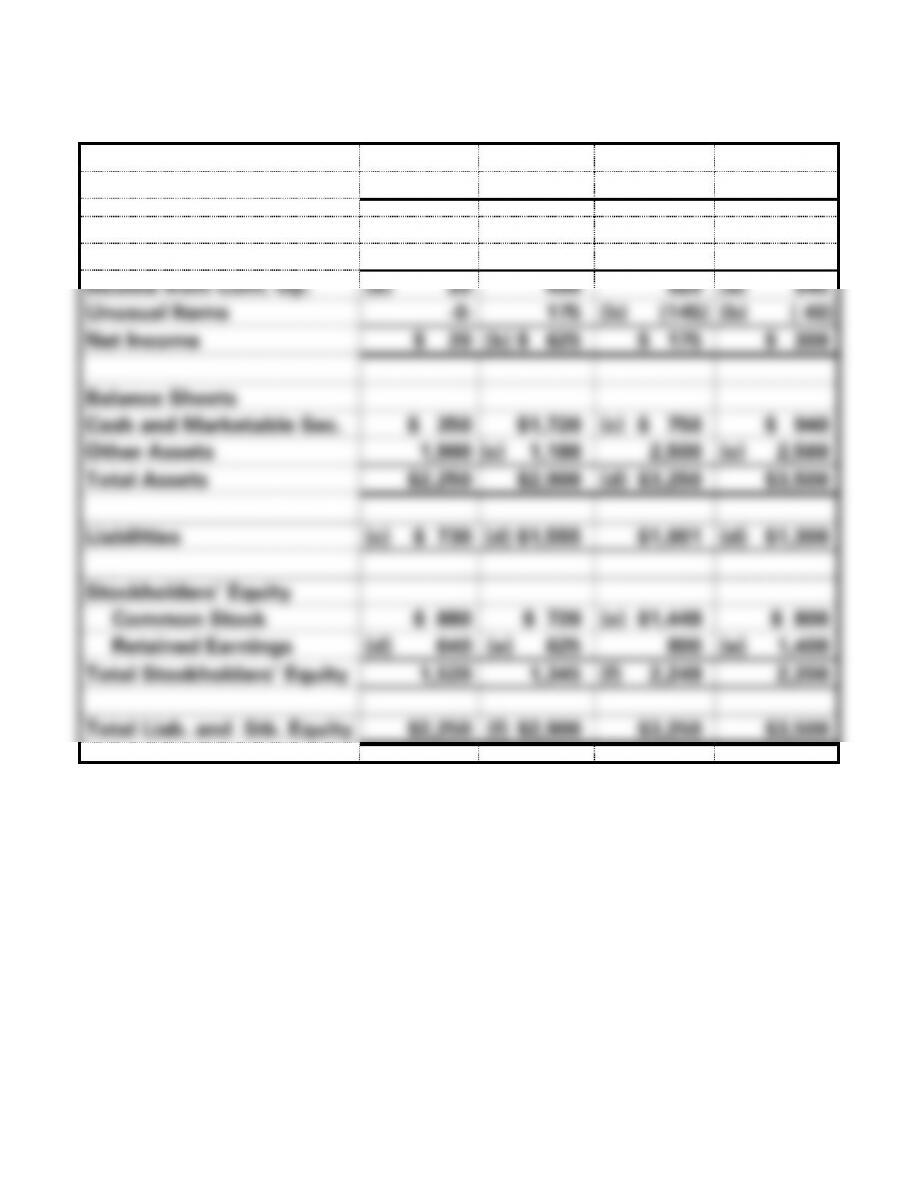

ATC 1-2

a.

Income Statements (amounts given are in millions)

2016

2017

2018

2019

Revenue

$ 860

$1,520

(a) $2,720

$1,200

Cost and Expenses

(a) (840)

(a) (1,070)

(2,400)

(860)

Income from Cont. Op.

(b) 20

450

320

(a) 340

Unusual Items

-0-

175

(b) (145)

(b) ( 40)

Net Income

$ 20

(b) $ 625

$ 175

$ 300

Balance Sheets

Cash and Marketable Sec.

$ 350

$1,720

(c) $ 750

$ 940

Other Assets

1,900

(c) 1,180

2,500

(c) 2,560

Total Assets

$2,250

$2,900

(d) $3,250

$3,500

Liabilities

(c) $ 730

(d) $1,555

$1,001

(d) $1,300

Stockholders’ Equity

Common Stock

$ 880

$ 720

(e) $1,449

$ 800

Retained Earnings

(d) 640

(e) 625

800

(e) 1,400

Total Stockholders’ Equity

1,520

1,345

(f) 2,249

2,200

Total Liab. and Stk. Equity

$2,250

(f) $2,900

$3,250

$3,500

1-117

ATC 1-3

1. Delta’s cash purchase of airplanes should be classified as a cash

outflow in the investing activities section of the statement of cash

flows.

2. Google’s cash purchase of Nest Labs should be classified as a cash

outflow in the investing activities section of the statement of cash

flows.

ATC 1-4

a. The percentage growth from 2016 to 2017 was 65% [($264,000 −

$160,000) $160,000]. However, this rate of growth will probably not

continue from 2017 to 2018 because 69% ($72,000 $104,000) of the

growth was from the lottery win. If the company continues to grow at

the current rate, shareholders should expect an increase in net income

1-119

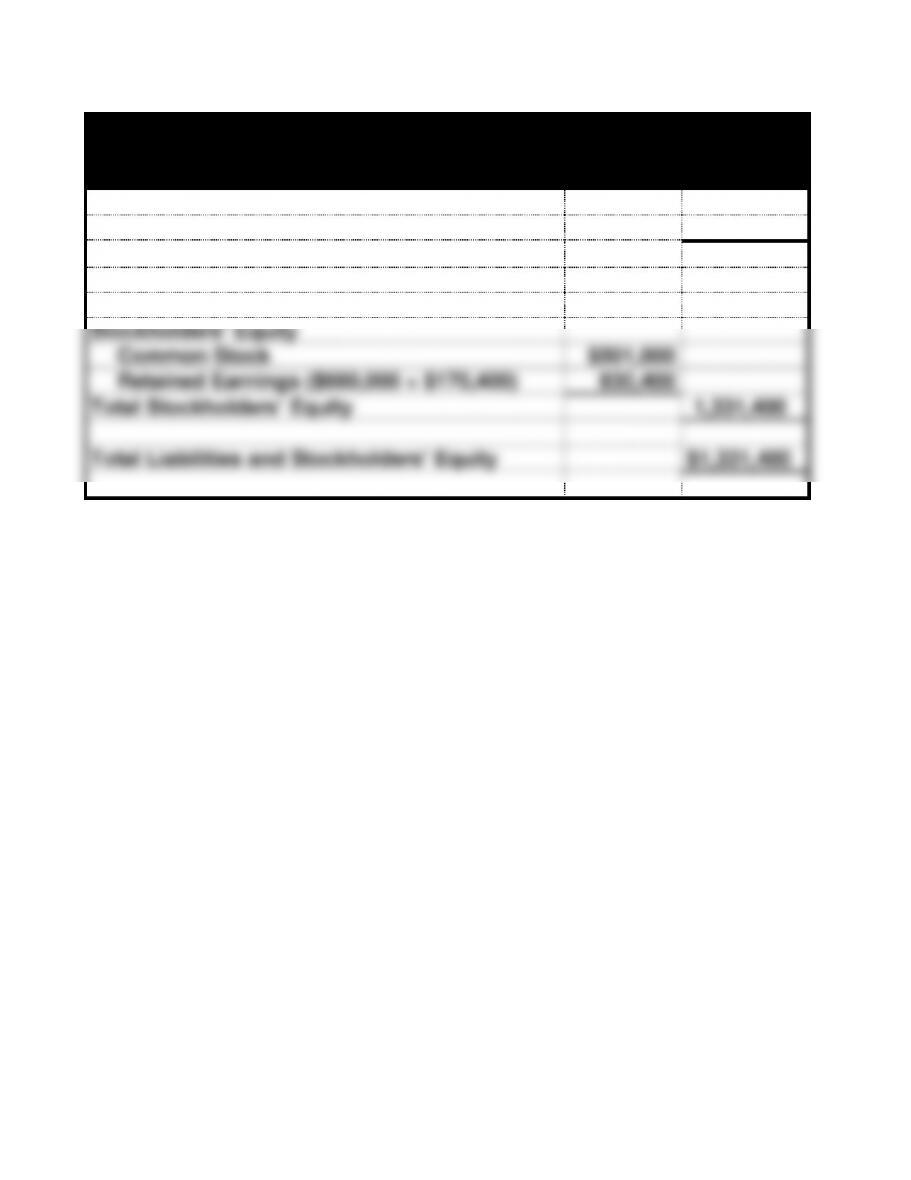

ATC 1-4 d. (cont.)

Sierra Home Builders

Balance Sheet

As of December 31, 2018

Assets

$1,331,400

Liabilities

$ -0-

Stockholders’ Equity

Common Stock

$501,000

Retained Earnings ($660,000 + $170,400)

830,400

Total Stockholders’ Equity

1,331,400

Total Liabilities and Stockholders’ Equity

$1,331,400

1-120

ATC 1-5

This problem is designed to test written communication skills. The memo

should describe the balance sheet and the income statement. It should

1-121

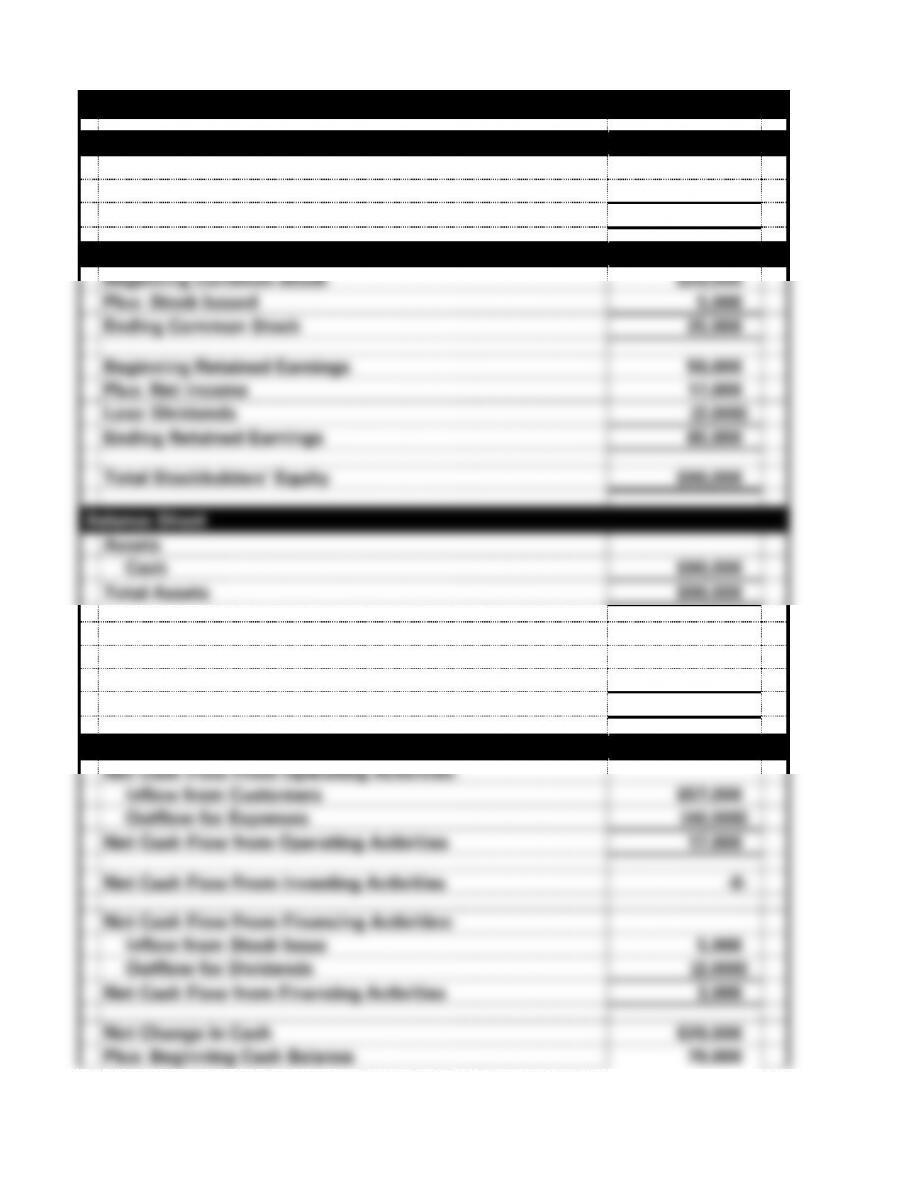

ATC 1-6 a.

Financial Statements

Income Statement

Revenue

$57,000

Expense

(40,000)

Net Income

$17,000

Statement of Changes in Stockholders’ Equity

Beginning Common Stock

$20,000

Plus: Stock Issued

5,000

Ending Common Stock

25,000

Beginning Retained Earnings

50,000

Plus: Net Income

17,000

Less: Dividends

(2,000)

Ending Retained Earnings

65,000

Total Stockholders’ Equity

$90,000

Balance Sheet

Assets

Cash

$90,000

Total Assets

$90,000

Stockholders’ Equity

Common Stock

$25,000

Retained Earnings

65,000

Total Stockholders’ Equity

$90,000

Statement of Cash Flows

Net Cash Flow From Operating Activities:

Inflow from Customers

$57,000

Outflow for Expenses

(40,000)

Net Cash Flow from Operating Activities

17,000

Net Cash Flow From Investing Activities

-0-

Net Cash Flow From Financing Activities:

Inflow from Stock Issue

5,000

Outflow for Dividends

(2,000)

Net Cash Flow from Financing Activities

3,000

Net Change in Cash

$20,000

Plus: Beginning Cash Balance

70,000

1-122

Ending Cash Balance

$90,000

1-123

ATC 1-6 (cont.)

b. In the short-run replacing Kevin would save $5,000 in cash expenses.

Accordingly, net income, assets, stockholders’ equity, and cash flow

from operating activities would increase. These effects can be

1-124

ATC 1-7

This solution is based on Sonic Drive-In’s August 31, 2013 annual report.

Dollar amounts are in thousands.

a. Sonic’s net income for 2013, 2012, and 2011 were as follows: