1-61

PROBLEM 1-32A b. (cont.)

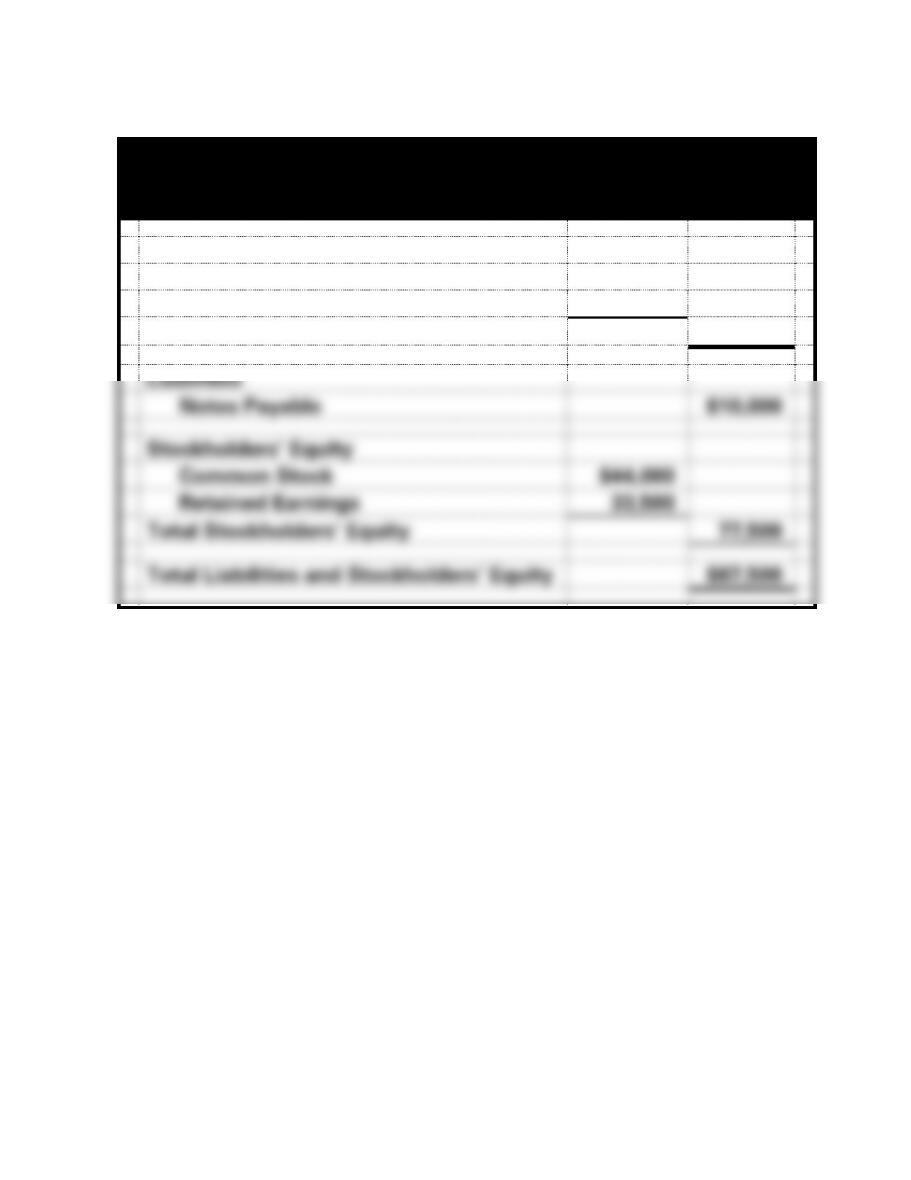

Mark’s Consulting Services

Balance Sheet

As of December 31, 2017

Assets

Cash

$57,500

Land

30,000

Total Assets

$87,500

Liabilities

Notes Payable

$10,000

Stockholders’ Equity

Common Stock

$44,000

Retained Earnings

33,500

Total Stockholders’ Equity

77,500

Total Liabilities and Stockholders’ Equity

$87,500

1-62

PROBLEM 1-32A b. (cont.)

Mark’s Consulting Services

Statement of Cash Flows

For the Year Ended December 31, 2017

Cash Flows From Operating Activities:

Cash Receipts from Customers

$95,000

Cash Payments for Expenses

(71,500)

Net Cash Flow from Operating Activities

$23,500

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities:

Cash Receipts from Stock Issue

$24,000

Cash Payment on Debt

(15,000)

Cash Payment for Dividends

(3,000)

Net Cash Flow from Financing Activities

6,000

Net Increase in Cash

29,500

Plus: Beginning Cash Balance

28,000

Ending Cash Balance

$57,500

1-63

PROBLEM 1-32A (cont.)

e. Immediately after Event 2 in 2016 is recorded the balance in the

Retained Earnings account is zero. The revenue is recorded in a

Revenue account, not in the Retained Earnings account. The

1-64

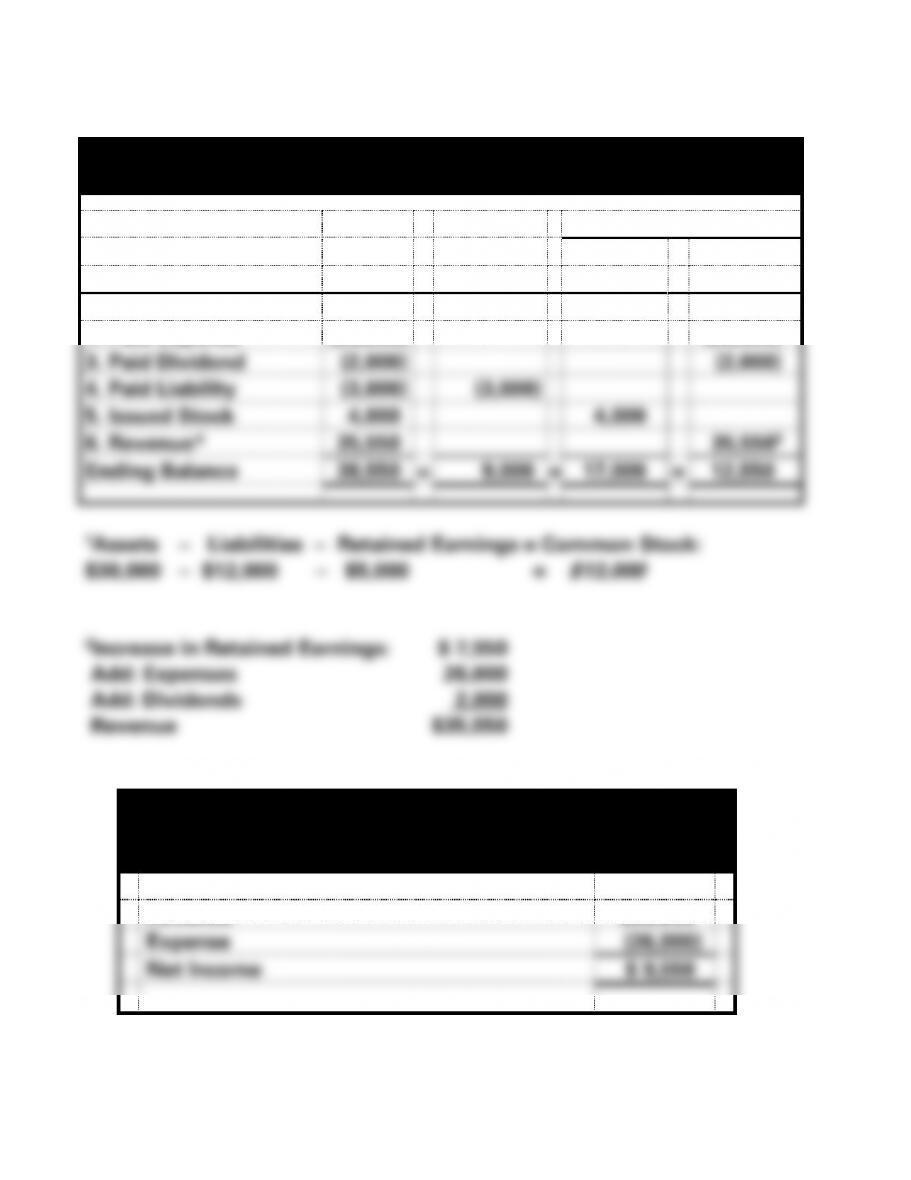

PROBLEM 1-33A

a.

Pratt Corp.

Accounting Equation

Stockholders’ Equity

Common

Retained

Event

Assets

=

Liabilities

+

Stock

+

Earnings

Beginning Balances

30,000

=

12,000

+

13,0001

+

5,000

1. Paid Expense

(26,000)

(26,000)

3. Paid Dividend

(2,000)

(2,000)

4. Paid Liability

(3,000)

(3,000)

5. Issued Stock

4,000

4,000

6. Revenue*

35,550

35,5502

Ending Balance

38,550

=

9,000

+

17,000

+

12,550

1Assets − Liabilities − Retained Earnings = Common Stock:

$30,000 − $12,000 − $5,000 =

$13,000

2Increase in Retained Earnings: $ 7,550

Add: Expenses 26,000

Add: Dividends 2,000

Revenue $35,550

Pratt Corp.

Income Statement

For the Year Ended December 31, 2016

Revenue

$35,550

Expense

(26,000)

Net Income

$ 9,550

1-65

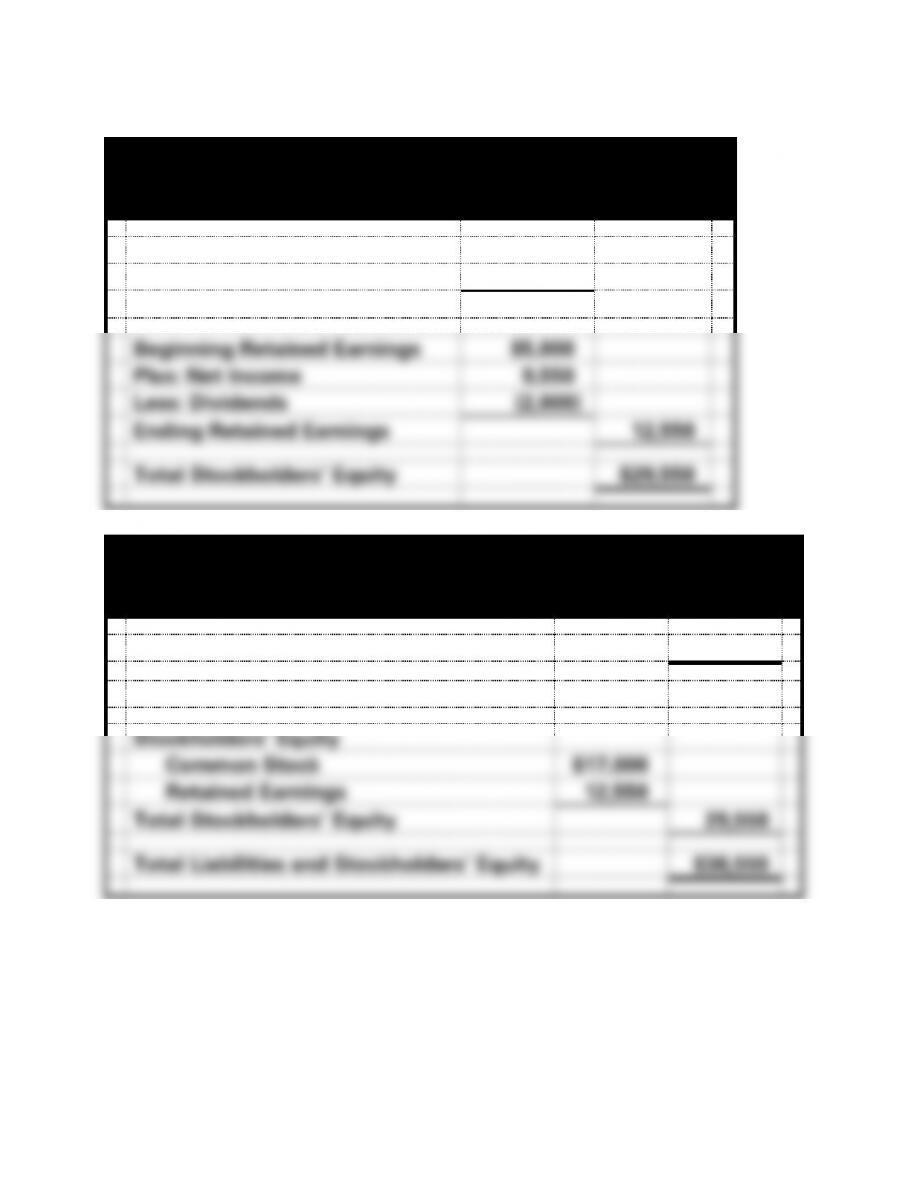

PROBLEM 1-33A (cont.)

Pratt Corp.

Statement of Changes in Stockholders’ Equity

For the Year Ended December 31, 2016

Beginning Common Stock

$13,000

Plus: Common Stock Issued

4,000

Ending Common Stock

$17,000

Beginning Retained Earnings

$5,000

Plus: Net Income

9,550

Less: Dividends

(2,000)

Ending Retained Earnings

12,550

Total Stockholders’ Equity

$29,550

Pratt Corp.

Balance Sheet

As of December 31, 2016

Assets

$38,550

Liabilities

$ 9,000

Stockholders’ Equity

Common Stock

$17,000

Retained Earnings

12,550

Total Stockholders’ Equity

29,550

Total Liabilities and Stockholders’ Equity

$38,550

1-66

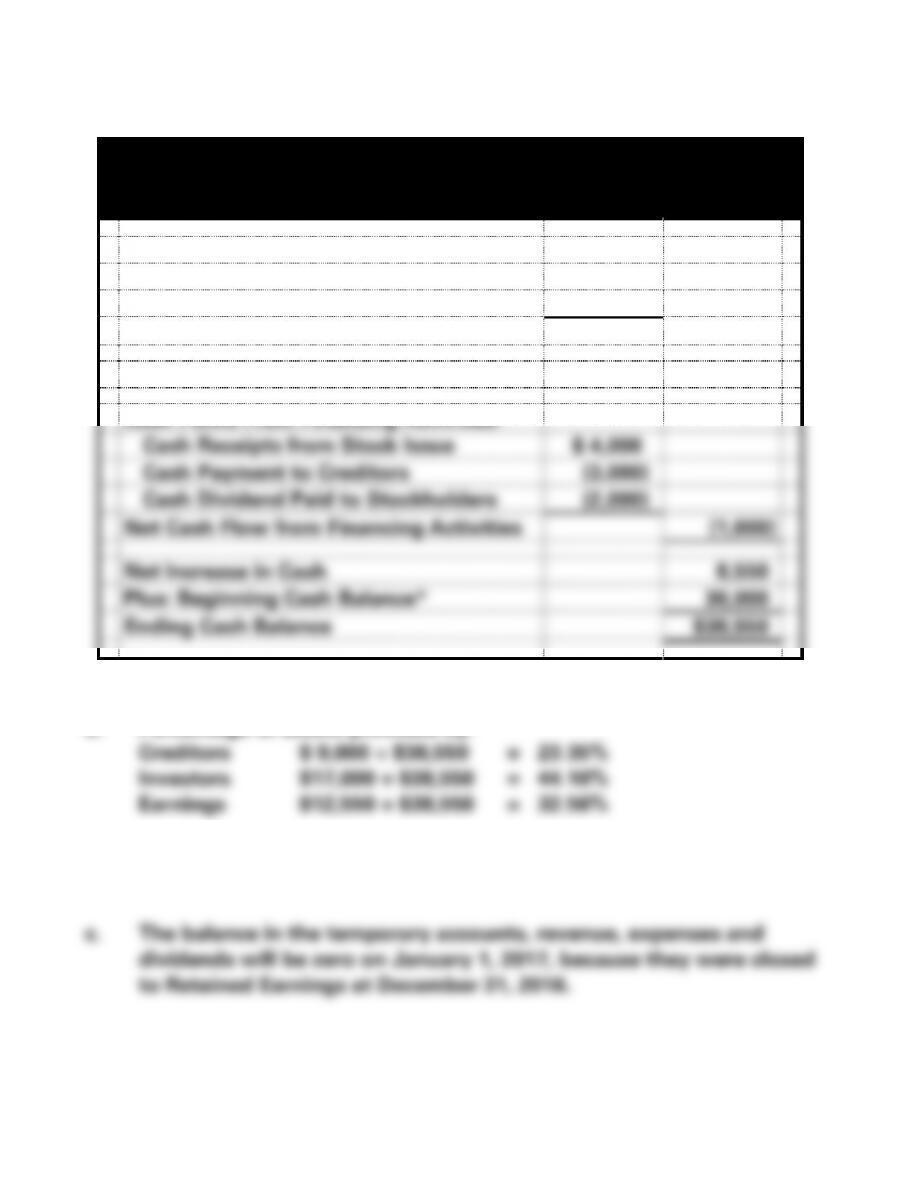

PROBLEM 1-33A (cont.)

Pratt Corp.

Statement of Cash Flows

For the Year Ended December 31, 2016

Cash Flows From Operating Activities:

Cash Receipt from Revenue

$35,550

Cash Payment for Expense

(26,000)

Net Cash Flow from Operating Activities

$ 9,550

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities:

Cash Receipts from Stock Issue

$ 4,000

Cash Payment to Creditors

(3,000)

Cash Dividend Paid to Stockholders

(2,000)

Net Cash Flow from Financing Activities

(1,000)

Net Increase in Cash

8,550

Plus: Beginning Cash Balance*

30,000

Ending Cash Balance

$38,550

*Assumes all assets are cash.

b. Percentage of assets provided by:

1-67

PROBLEM 1-34A

a.

Maben Company

Horizontal Statements Model for 2016

Balance Sheet

Income Statement

Statement of

Assets

=

Liab.

+

Stockholders’ Equity

Revenue

−

Expense

=

Net Inc.

Cash Flows

Event

No.

Cash

+

Land

=

Notes

Payable

+

Common

Stock

+

Retained

Earnings

1

30,000

+

NA

=

NA

+

30,000

+

NA

NA

−

NA

=

NA

30,000FA

2

40,000

+

NA

=

40,000

+

NA

+

NA

NA

−

NA

=

NA

40,000 FA

3

48,000

+

NA

=

NA

+

NA

+

48,000

48,000

−

NA

=

48,000

48,000 OA

4

(25,000)

+

NA

=

NA

+

NA

+

(25,000)

NA

−

25,000

=

(25,000)

(25,000) OA

5.

(1,000)

+

NA

=

NA

+

NA

+

(1,000)

NA

−

NA

=

NA

(1,000) FA

6.

20,000

+

NA

=

NA

+

20,000

+

NA

NA

−

NA

=

NA

20,000 FA

7.

(10,000)

+

NA

=

(10,000)

+

NA

+

NA

NA

−

NA

=

NA

(10,000) FA

8.

(53,000)

+

53,000

=

NA

+

NA

+

NA

NA

−

NA

=

NA

(53,000) IA

9.

NA

+

NA

=

NA

+

NA

+

NA

NA

−

NA

=

NA

NA

Total

49,000

+

53,000

=

30,000

+

50,000

+

22,000

48,000

−

25,000

23,000

49,000 NC

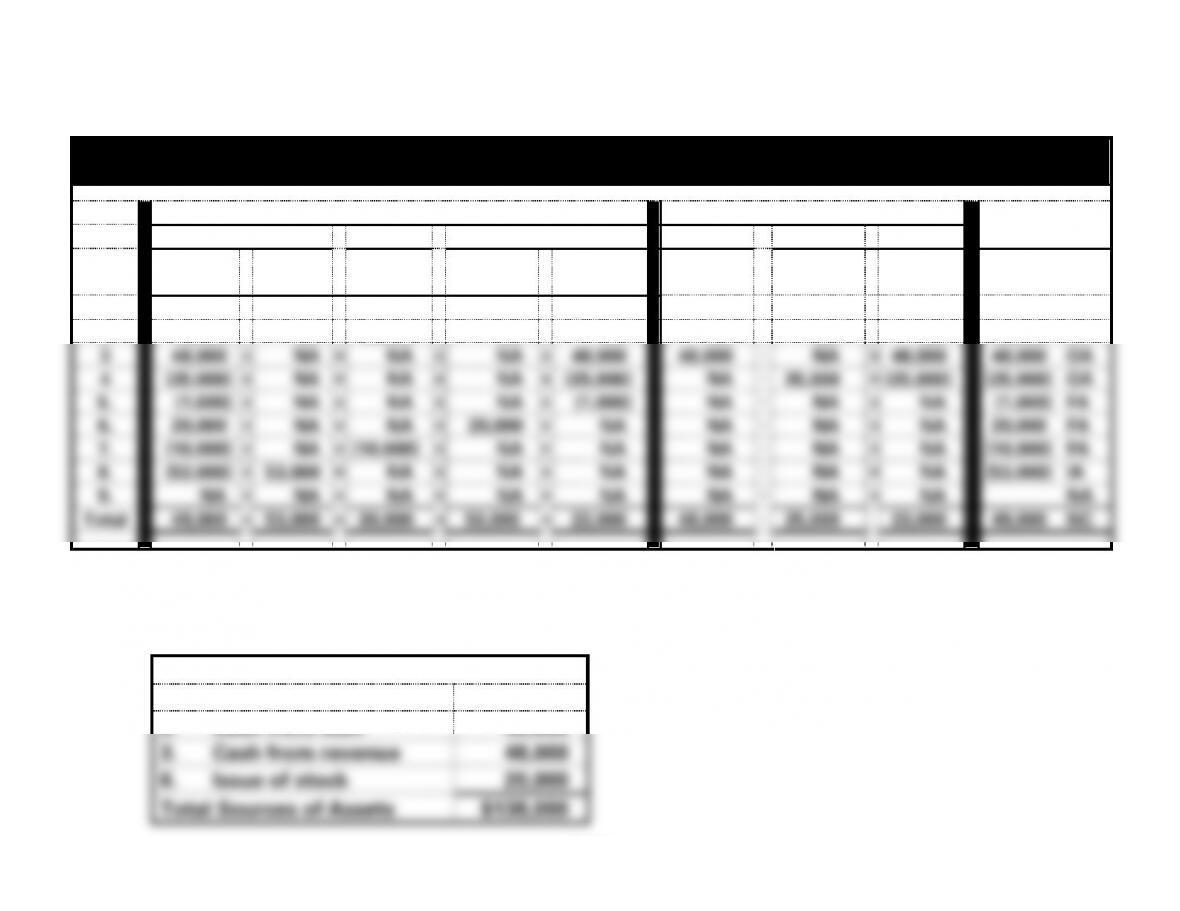

b. Total Assets = $49,000 + $53,000 = $102,000

c.

Sources of Assets

1. Issue of stock

$ 30,000

2. Cash from loan

40,000

3. Cash from revenue

48,000

6. Issue of stock

20,000

Total Sources of Assets

$138,000

1-62

PROBLEM 1-34A (cont.)

d. Net income amounts to $23,000 (see part a.) Dividends are not

expenses and do not appear on the income statement.

e.

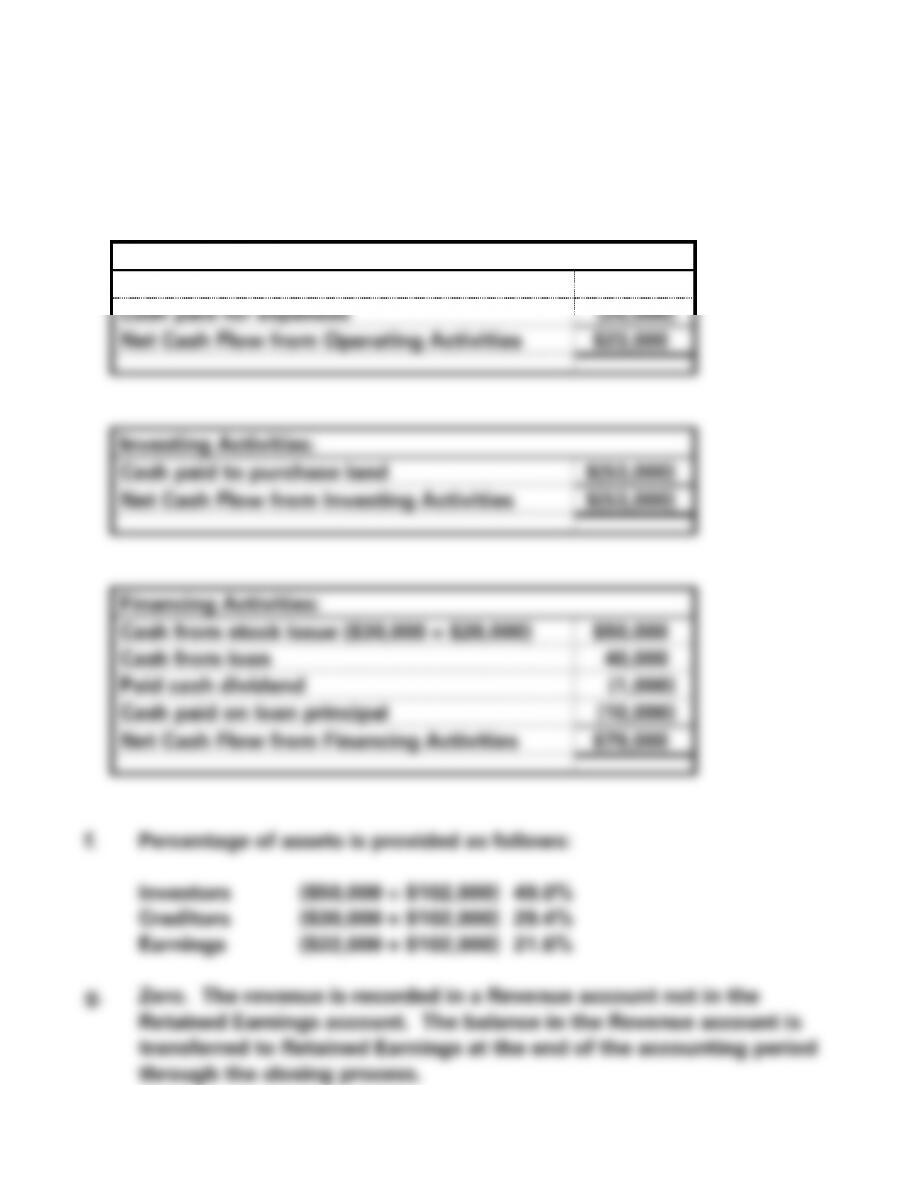

Operating Activities:

Cash from revenue

$48,000

Cash paid for expenses

(25,000)

Net Cash Flow from Operating Activities

$23,000

Investing Activities:

Cash paid to purchase land

$(53,000)

Net Cash Flow from Investing Activities

$(53,000)

Financing Activities:

Cash from stock issue ($30,000 + $20,000)

$50,000

Cash from loan

40,000

Paid cash dividend

(1,000)

Cash paid on loan principal

(10,000)

Net Cash Flow from Financing Activities

$79,000

f. Percentage of assets is provided as follows:

Investors ($50,000 ÷ $102,000) 49.0%

Creditors ($30,000 ÷ $102,000) 29.4%

Earnings ($22,000 ÷ $102,000) 21.6%

g. Zero. The revenue is recorded in a Revenue account not in the

Retained Earnings account. The balance in the Revenue account is

transferred to Retained Earnings at the end of the accounting period

through the closing process.

1-63

SOLUTIONS TO EXERCISES – SERIES B – CHAPTER 1

EXERCISE 1-1B

The three types of resources available to conversion agents are:

Note to instructor:

The memo should discuss the fact that the resource owners are those

who own resources that are desired by others, either in the original form

1-64

EXERCISE 1-2B

a. The three areas of service provided by public accountants are

auditing, tax and consulting.

EXERCISE 1-3B

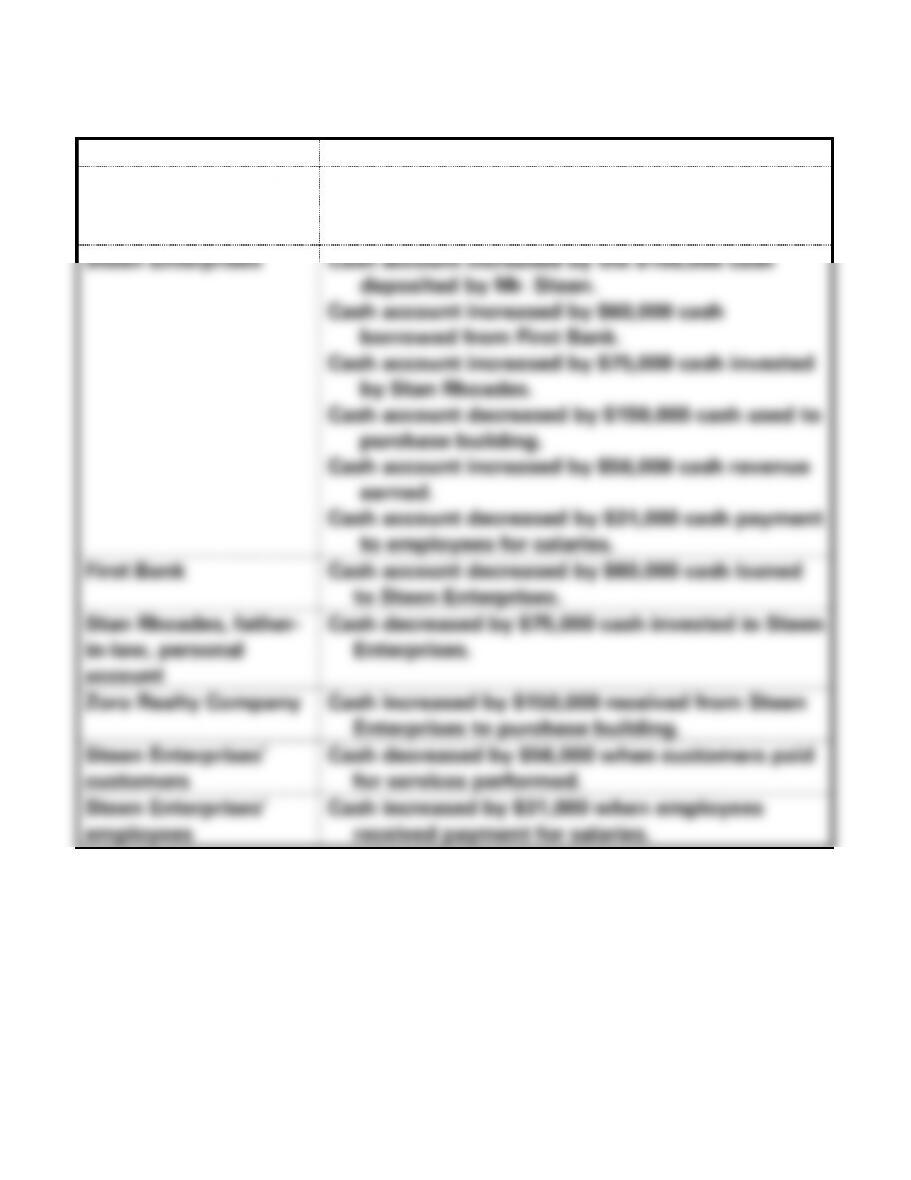

Entities

Distribution of Cash

Ray Steen (personal

account)

Personal account was decreased by the $100,000

cash deposited in the Steen Enterprises’

business account.

Steen Enterprises

Cash account increased by the $100,000 cash

deposited by Mr. Steen.

Cash account increased by $60,000 cash

borrowed from First Bank.

Cash account increased by $75,000 cash invested

by Stan Rhoades.

Cash account decreased by $150,000 cash used to

purchase building.

Cash account increased by $56,000 cash revenue

earned.

Cash account decreased by $31,000 cash payment

to employees for salaries.

First Bank

Cash account decreased by $60,000 cash loaned

to Steen Enterprises.

Stan Rhoades, father-

in-law, personal

account

Cash decreased by $75,000 cash invested in Steen

Enterprises.

Zoro Realty Company

Cash increased by $150,000 received from Steen

Enterprises to purchase building.

Steen Enterprises’

customers

Cash decreased by $56,000 when customers paid

for services performed.

Steen Enterprises’

employees

Cash increased by $31,000 when employees

received payment for salaries.

1-66

EXERCISE 1-4B

Accounting Equation

Stockholders’ Equity

Common

Retained

Company

Assets

=

Liabilities

+

Stock

+

Earnings

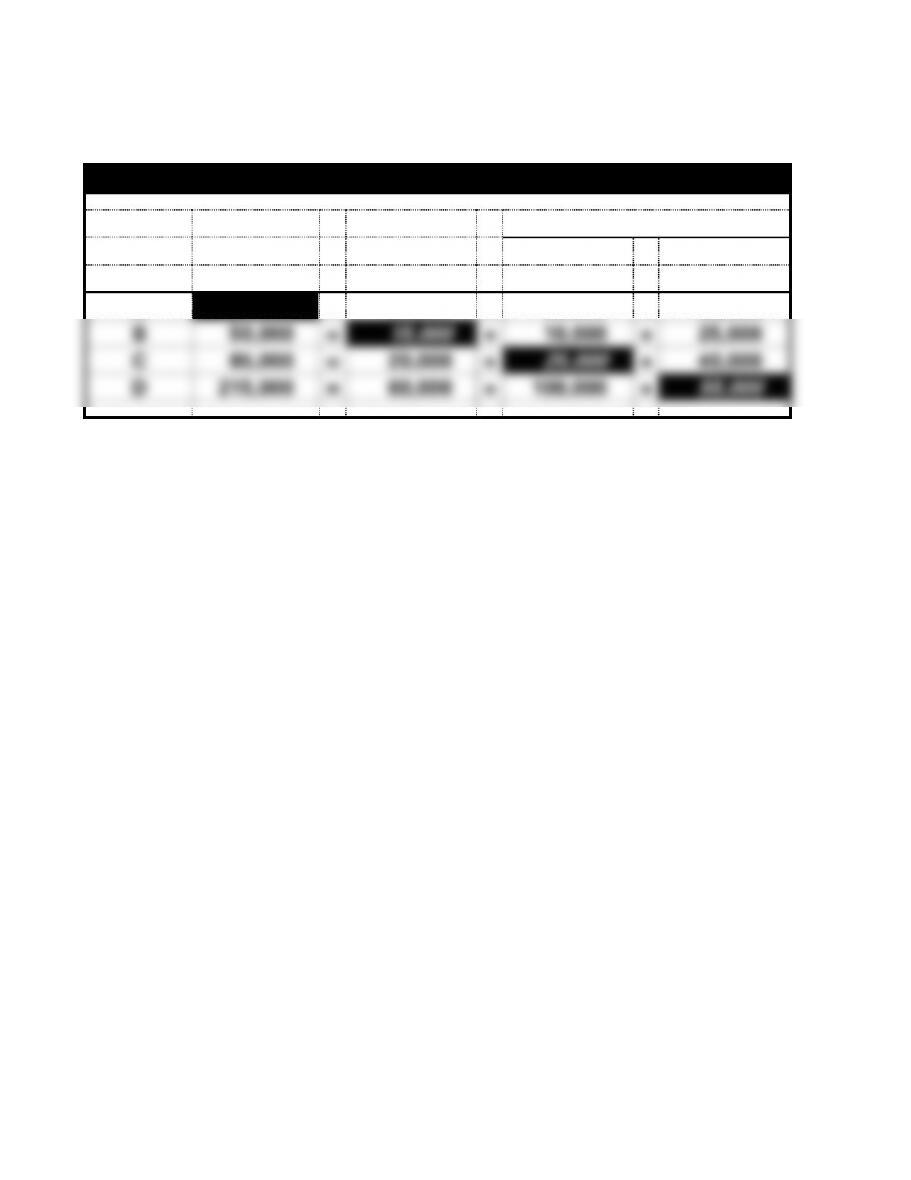

A

142,000

=

30,000

+

50,000

+

62,000

B

50,000

=

15,000

+

10,000

+

25,000

C

85,000

=

20,000

+

25,000

+

40,000

D

215,000

=

60,000

+

100,000

+

55,000

1-67

EXERCISE 1-5B

Morrison Co.

Accounting Equation

Stockholders’

Equity

Event

Number

Assets

=

Liabilities

+

Common

Stock

Retained

Earnings

1.

I

NA

I

NA

2.

I

I

NA

NA

3.

I

NA

NA

I

4.

I/D

NA

NA

NA

5.

D

NA

NA

D

6.

D

NA

NA

D

1-68

EXERCISE 1-6B

a.

Master Corp.

Accounting Equation for 2016

Assets

=

Liabilities

+

Stockholders’ Equity

Event

Cash

+

Land

=

Notes

Payable

+

Com.

Stock

+

Retained

Earnings

Acct.

Title/RE

Bal. 1/1/16

20,000

50,000

35,000

25,000

10,000

1. Pur. Land

(12,000)

12,000

NA

NA

NA

NA

2. Issued stk.

20,000

NA

NA

20,000

NA

NA

3. Service

50,000

NA

NA

NA

50,000

Revenue

4. Paid Exp.

(42,000)

NA

NA

NA

(42,000)

Oper. Exp.

5. Loan

20,000

NA

20,000

NA

NA

NA

6. Paid Div.

(2,000)

NA

NA

NA

(2,000)

Dividend

7. Land Value

NA

NA

NA

NA

NA

NA

Totals

54,000

+

62,000

=

55,000

+

45,000

+

16,000

b.

Assets

=

Liabilities

+

Stockholders’ Equity

$116,000

=

$55,000

+

$61,000

c. The balances of total assets, liabilities and stockholders’ equity will

be the same on January 1, 2017 as the balances on December 31,

2016. (See b. above)

1-69

EXERCISE 1-7B

a.

Assets

=

Liabilities

+

Stockholders’ Equity

Cash

=

Note Payable

+

Common Stock

+

Retained Earnings

156,000

=

85,600

+

52,400

+

?

Retained Earnings = $156,000 – $85,600 – $52,400 = $18,000

b. & c.

Dunn Company

Effect of 2017 Transactions on the Accounting Equation

Assets

=

Liabilities

+

Stockholders’ Equity

Notes

Common

Retained

Event

Cash

=

Payable

+

Stock

+

Earnings

Beginning Balances

156,000

85,600

52,400

18,000

1. Earned Revenue

36,000

NA

NA

36,000

2. Paid expenses

(20,000)

NA

NA

(20,000)

3. Paid dividend

(3,000)

NA

NA

(3,000)

Ending Balance

169,000

=

85,600

+

52,400

+

31,000

d.

Cash

=

Note Payable

+

Common Stock

+

Retained Earnings

169,000

=

85,600

+

52,400

+

31,000

1-70

EXERCISE 1-8B

a.

Assets

=

Liabilities

+

Stockholders’ Equity

Cash

Notes Payable

Salaries Expense

Land

Accounts Payable

Common Stock

Office Furniture

Utilities Payable

Service Revenue

Trucks

Interest Expense

Supplies

Utilities Expense

Computers

Operating Expenses

Building

Rent Revenue

Dividends

Supplies Expense

Gasoline Expense

Retained Earnings

Dividends

b. No. The number of accounts will vary depending on the level of detail

the reporting entity chooses to provide, as well as the type of company

and industry in which it operates. More accounts provide financial

statement users with more information about the reporting entity.

1-71

1-72

EXERCISE 1-9B

a.

Cash

+

Land

=

Creditors

+

Stockholders’

Equity

$10,000

$ -0-

$4,000

$6,000

(9,000)

9,000

NA

NA

Bal.

$ 1,000

+

$9,000

=

$4,000

+

$6,000

b. Creditor’s Claim ÷ Total Assets = Percent of Total

$4,000 ÷ $10,000 = 40%

c. Stakeholder’s Claim ÷ Total Assets = Percent of Total

$6,000 ÷ $10,000 = 60%

d. The company cannot repay the debt. The company owes the creditors

$4,000 but has only $1,000 cash. Note there is no actual money in the

stockholders’ equity account. Indeed, there is no cash in any account

that appears on the right side of the accounting equation. The right

side of the accounting equation represents obligations and

commitments of a company to its creditors and stockholders. Indeed,

the accounting equation could be written as:

Cash

+

Land

=

Creditors

+

Stockholders’

Equity

Bal.

$ 1,000

+

$9,000

=

40%

+

60%

equation.

1-73

EXERCISE 1-10B

a. Dividends are paid to investors. The investor has an ownership

interest in the business that allows the investor (owner) to share in

the profits of the business. This pay out of a share of profits of a

of $800. Since creditors have first claim on the assets, all of the $800

1-74

EXERCISE 1-11B

$400) to be paid as dividends to the investors.

b. Creditors receive their $400 interest payment, leaving $100 ($500 –

c. Creditors receive their $400 interest payment. No dividend is paid to

above.