Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

2-52

Ending Cash Balance

$55,300

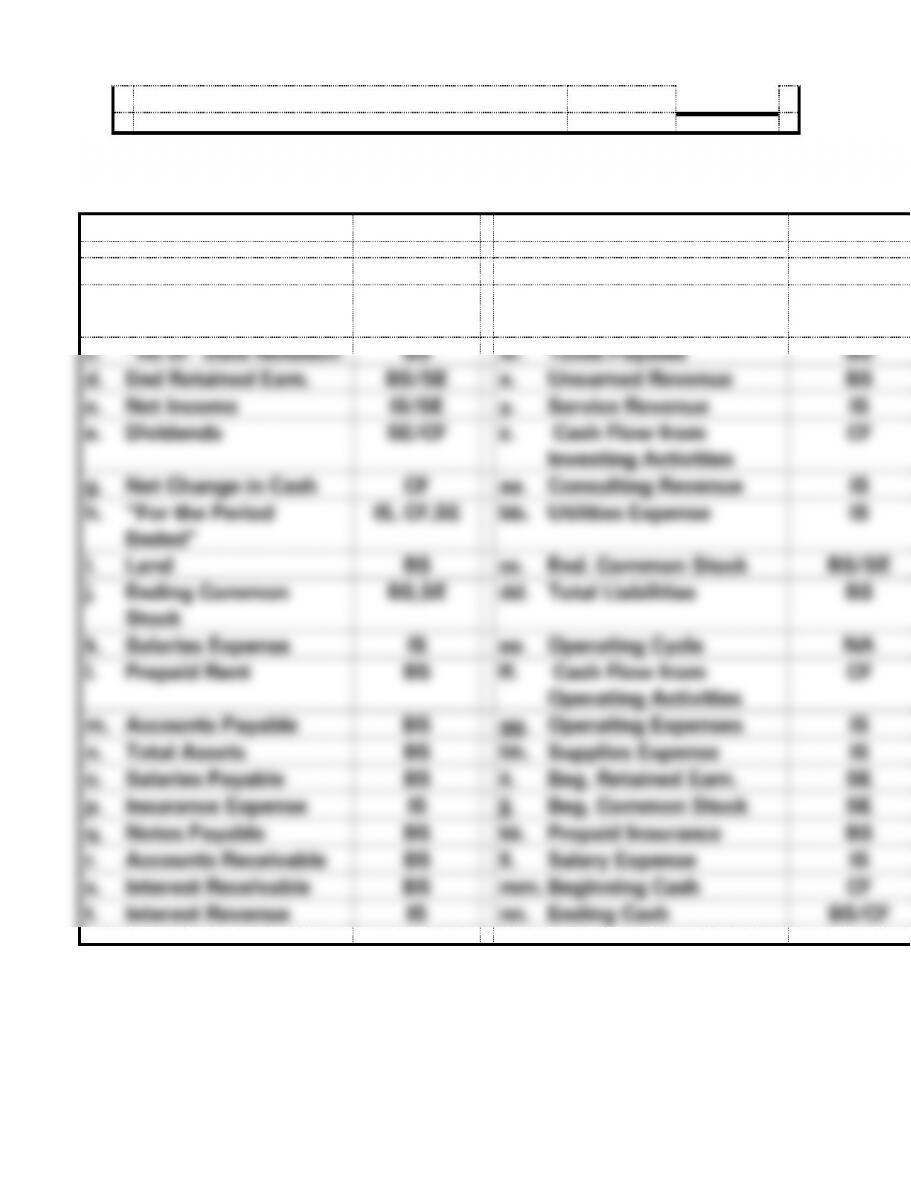

EXERCISE 2-26A

Item/Account

Statement

Item/Account

Statement

a. Supplies

BS

u. Rent Exp.

IS

b. Cash Flow from

Financing Act.

CF

v. P/E Ratio

NA

c. “As of” Date Notation

BS

w. Taxes Payable

BS

d. End Retained Earn.

BS/SE

x. Unearned Revenue

BS

e. Net Income

IS/SE

y. Service Revenue

IS

e. Dividends

SE/CF

z. Cash Flow from

Investing Activities

CF

g. Net Change in Cash

CF

aa. Consulting Revenue

IS

h. “For the Period

Ended”

IS, CF,SE

bb. Utilities Expense

IS

i. Land

BS

cc. End. Common Stock

BS/SE

j. Ending Common

Stock

BS,SE

dd. Total Liabilities

BS

k. Salaries Expense

IS

ee. Operating Cycle

NA

l. Prepaid Rent

BS

ff. Cash Flow from

Operating Activities

CF

m. Accounts Payable

BS

gg. Operating Expenses

IS

n. Total Assets

BS

hh. Supplies Expense

IS

o. Salaries Payable

BS

ii. Beg. Retained Earn.

SE

p. Insurance Expense

IS

jj. Beg. Common Stock

SE

q. Notes Payable

BS

kk. Prepaid Insurance

BS

r. Accounts Receivable

BS

ll. Salary Expense

IS

s. Interest Receivable

BS

mm. Beginning Cash

CF

t. Interest Revenue

IS

nn. Ending Cash

BS/CF

2-53

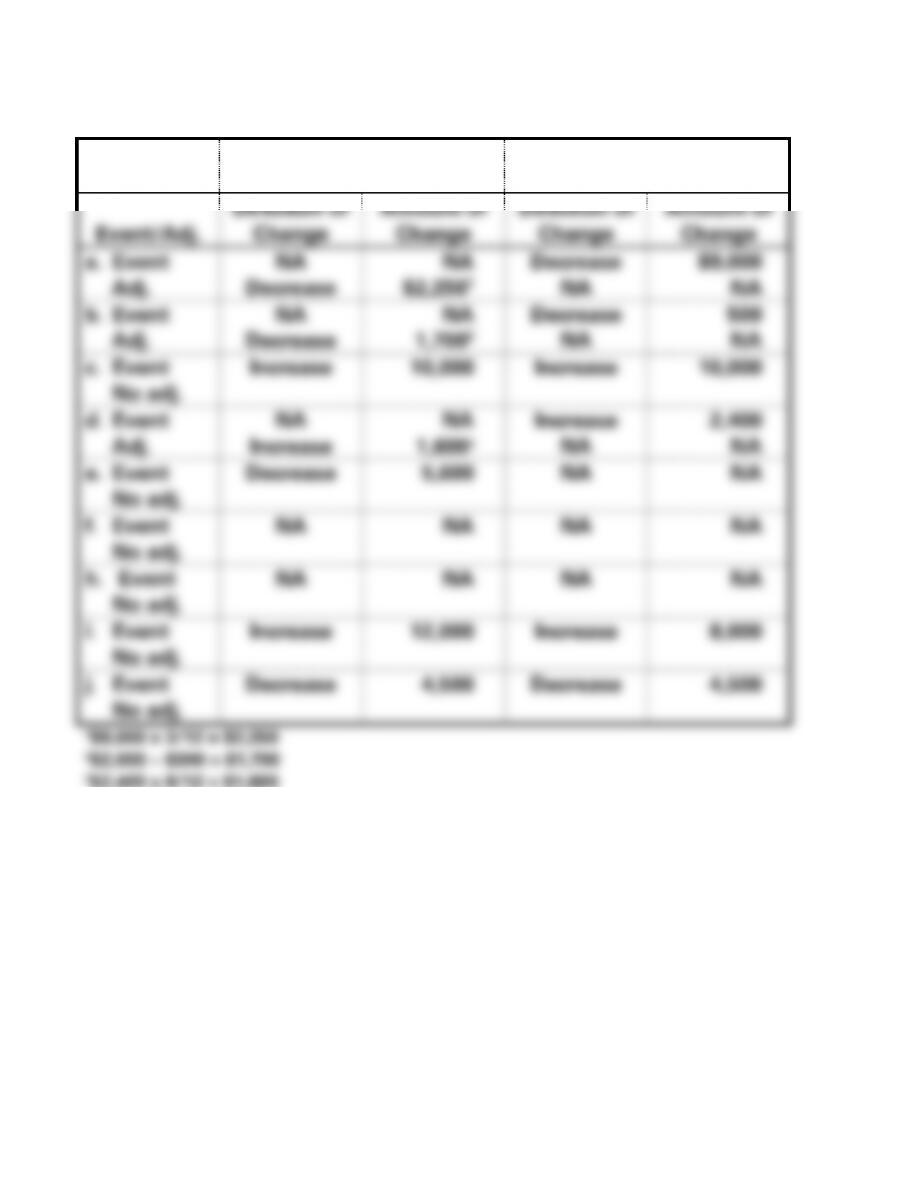

EXERCISE 2-27A

Net Income

Cash Flow from

Operating Activities

Event/Adj.

Direction of

Change

Amount of

Change

Direction of

Change

Amount of

Change

a. Event

Adj.

NA

Decrease

NA

$2,2501

Decrease

NA

$9,000

NA

b. Event

Adj.

NA

Decrease

NA

1,7002

Decrease

NA

500

NA

c. Event

No adj.

Increase

10,000

Increase

10,000

d. Event

Adj.

NA

Increase

NA

1,6003

Increase

NA

2,400

NA

e. Event

No adj.

Decrease

5,600

NA

NA

f. Event

No adj.

NA

NA

NA

NA

h. Event

No adj.

NA

NA

NA

NA

i. Event

No adj.

Increase

12,000

Increase

8,000

j. Event

No adj.

Decrease

4,500

Decrease

4,500

1$9,000 x 3/12 = $2,250

2$2,000 − $300 = $1,700

3$2,400 x 8/12 = $1,600

2-54

EXERCISE 2-28A

The following are only example transactions. There are also other

transactions that would cause the desired effect.

a. The business acquired cash by issuing stock to its owners.

2-55

EXERCISE 2-29A

a. Asset Source

b. Asset Use

2-56

EXERCISE 2-30A

Note: These are only sample transactions. Other similar transactions will

2-57

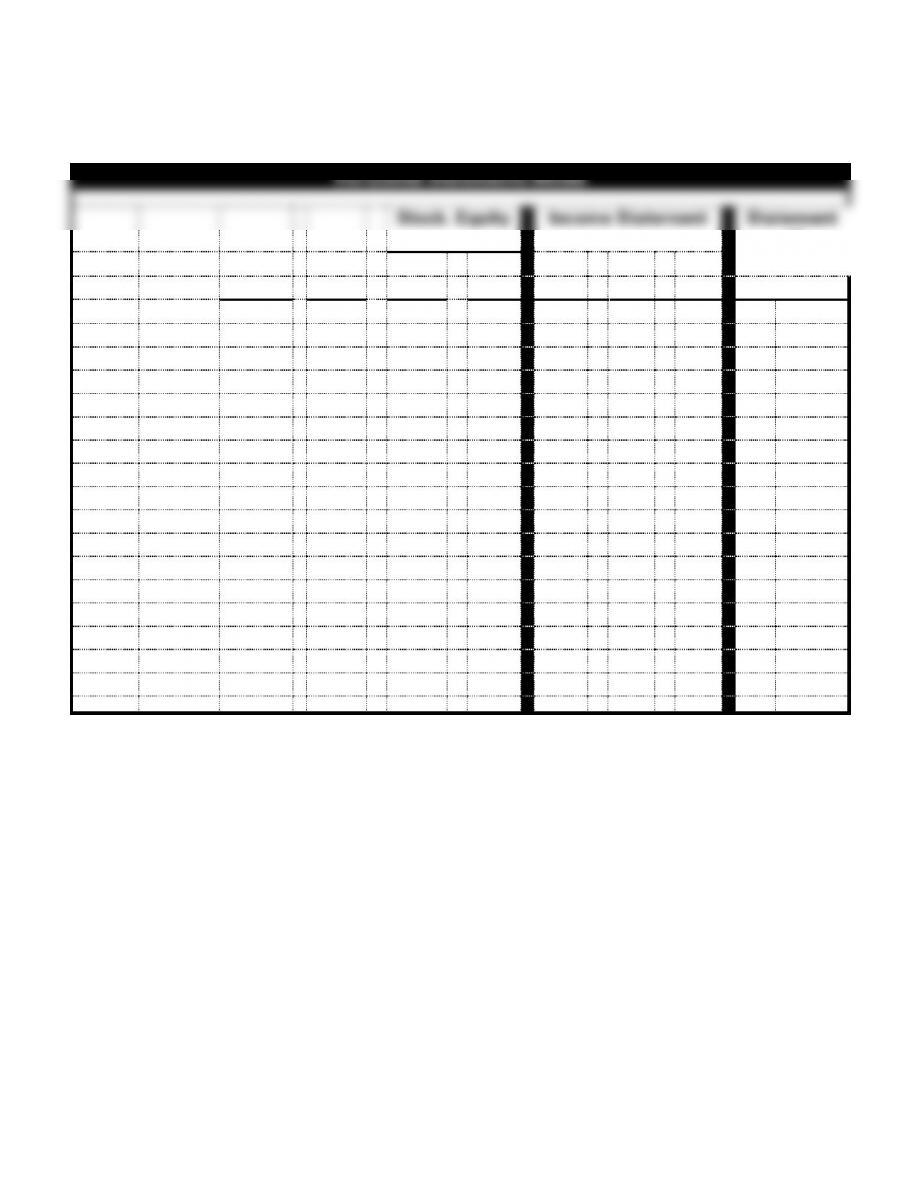

EXERCISE 2-31A

Horizontal Statements Model

Stock. Equity

Income Statement

Statement

of

Type of

Com.

Ret.

Net

Cash

Event

Event

Assets

=

Liab.

+

Stock

+

Earn

Rev.

−

Exp

=

Inc.

Flows

a.

AS

I

NA

NA

I

I

NA

I

I

OA

b.

AS

I

I

NA

NA

NA

NA

NA

NA

c.

AE

I/D

NA

NA

NA

NA

NA

NA

D

OA

d.

AE

I/D

NA

NA

NA

NA

NA

NA

D

IA

e.

AU

D

NA

NA

D

NA

NA

NA

D

FA

f.

AS

I

NA

I

NA

NA

NA

NA

I

FA

g.

AU

D

D

NA

NA

NA

NA

NA

D

OA

h.

AE

I/D

NA

NA

NA

NA

NA

NA

I

OA

i.

AS

I

I

NA

NA

NA

NA

NA

I

OA

j.

CE

NA

I

NA

D

NA

I

D

NA

k.

AS

I

NA

NA

I

I

NA

I

NA

l.

AU

D

NA

NA

D

NA

I

D

NA

m.

AU

D

NA

NA

D

NA

I

D

D

OA

n.

AU

D

NA

NA

D

NA

I

D

NA

o.

CE

NA

I

NA

D

NA

I

D

NA

p.

AU

D

D

NA

NA

NA

NA

NA

D

OA

q.

AS

I

NA

NA

I

I

NA

I

NA

2-58

EXERCISE 2-32A

The six principles of the AICPA Code of Professional Conduct and a brief

explanation is as follows:

Responsibilities Principle

In carrying out their responsibilities as professionals, members should

2-59

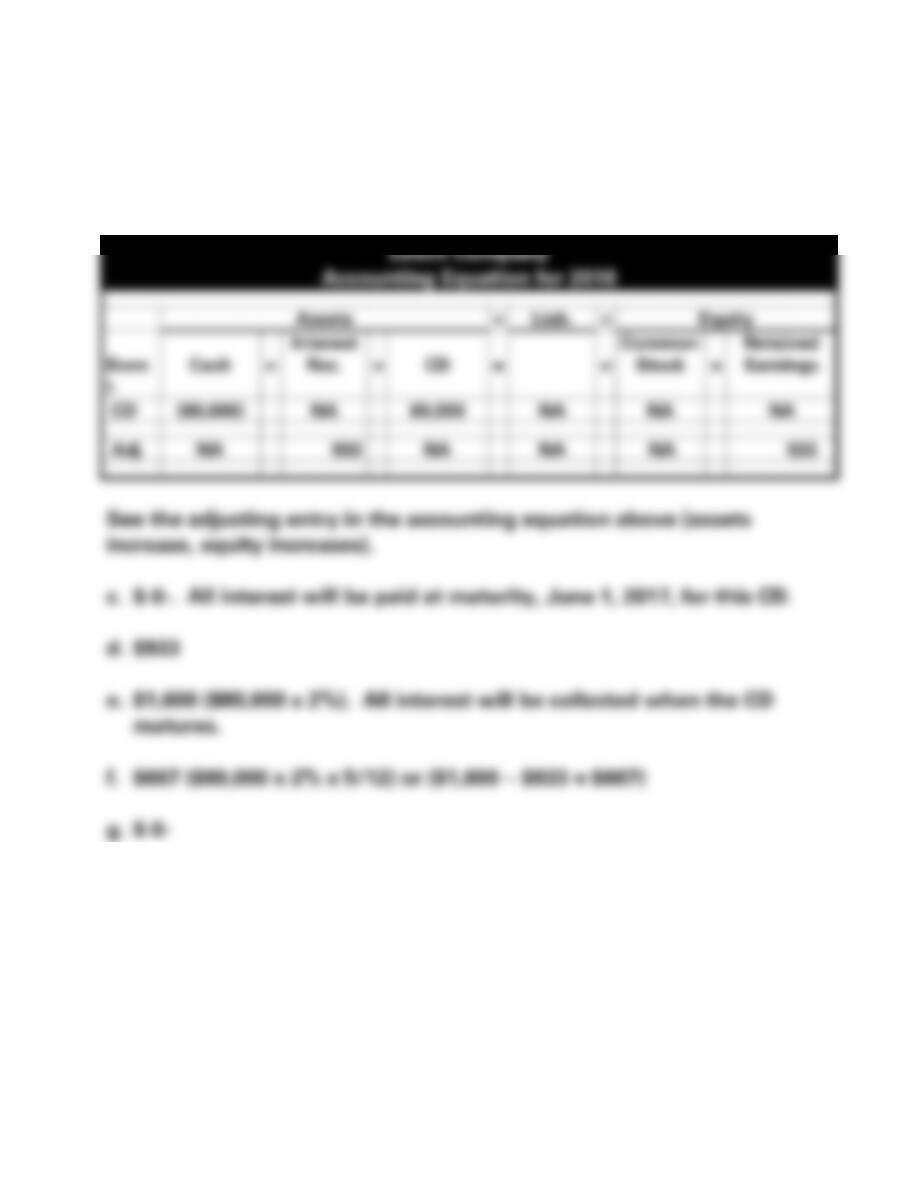

EXERCISE 2-33A (Appendix)

a.

Tracey’s Restaurant

Accounting Equation for 2016

Assets

=

Stockholders’ Equity

Event

Cash

Cook Top

Accum.

Depr.

=

Com.

Stock

+

Retained

Earnings

1. Issue Stk.

21,000

21,000

2. Pur. Cooktop

(22,000)

22,000

3. Rev.

32,000

32,000

4. Paid Sal Exp.

(16,000)

(16,000)

5. Paid Op. Exp.

(7,000)

(7,000)

6. Depr. Exp.

(4,000)*

(4,000)

Totals

8,000

22,000

(4,000)

=

21,000

+

5,000

2-60

EXERCISE 2-34A (Appendix)

d. Compute the depreciation expense per year.

(Cost – Salvage) ÷ Useful Life = Depreciation expense per year.

expense.

EXERCISE 2-35A (Appendix)

a. $8,000 x 6% = $480; $480 x 5/12 = $200

2-62

EXERCISE 2-36A (Appendix)

a. Interest revenue recognized for 2016: $80,000 x 2% = $1,600;

$1,600 x 7/12 = $933 (rounded)

b.

Leach Company

Accounting Equation for 2016

Assets

=

Liab.

+

Equity

Even

t

Cash

+

Interest

Rec.

+

CD

=

+

Common

Stock

+

Retained

Earnings

CD

(80,000)

NA

80,000

NA

NA

NA

Adj.

NA

933

NA

NA

NA

933

See the adjusting entry in the accounting equation above (assets

increase, equity increases).

c. $-0-. All interest will be paid at maturity, June 1, 2017, for this CD.

d. $933

e. $1,600 ($80,000 x 2%). All interest will be collected when the CD

matures.

f. $667 ($80,000 x 2% x 5/12) or ($1,600 − $933 = $667)

g. $-0-

2-63

SOLUTIONS TO PROBLEMS – SERIES A

PROBLEM 2-37A

The Accounting Equation

Total Assets

=

Liabilities

+

Stockholders’ Equity

Event/

Adjust.

Cash

+

Other

Assets

=

+

Common

Stock

+

Retained

Earnings

a.

(4,800)

+4,800

NA

NA

NA

a. Adj.

NA

(1,200)1

NA

NA

(1,200)

b.

+3,600

NA

+3,600

NA

NA

b. Adj.

NA

NA

(2,700)2

NA

+2,700

c.

NA

+1,200

+1,200

NA

NA

c. Adj.

NA

(1,025)

NA

NA

(1,025)

d.

(9,600)

+9,600

NA

NA

NA

d. Adj.

NA

(4,000)4

NA

NA

(4,000)

1$4,800 x 3/12 = $1,200

2$3,600 x 9/12 = $2,700

3$1,200 − $175 = $1,025

4$9,600 x 5/12 = $4,000

2-64

EXERCISE 2-38A a.

Nowell Company

Income Statement

For the Year Ended December 31, 2016

Consulting Revenue

$18,200

Expenses

Travel Expense

$2,100

Rent Expense

3,500

Salary Expense

7,200

Other Operating Expenses

2,300

Total Expenses

(15,100)

Net Income

$3,100

Accounts to be Closed:

Consulting Revenue

Travel Expense

Dividends

Rent Expense

Salary Expense

Other Operating Expenses

Computation of Retained Earnings:

Beginning Retained Earnings

$16,200

Add: Net Income

3,100

Less: Dividends

(4,000)

Ending Retained Earnings

$15,300

Net income only includes revenues and expenses for the current

year. Retained earnings not only includes current year net

income, but also the balance from previous years and reductions

for dividends.

e. The balances are zero; they were closed to Retained Earnings on

2-65

December 31, 2016. The December 31 closing balance of one

2-66

PROBLEM 2-39A

Super Cleaning Co.

Effect of Events on the Financial Statements

Balance Sheet

Income Statement

Stmt. of

Assets

=

Liabilities

+

Stockholders’

Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flows

Event

No.

Cash

+

Accts

Rec.

+

Pp. Rent

=

Accts.

Pay.

+

Unearn

Rev.

+

Com.

Stock

+

Ret.

Earn.

1.

10,000

+

NA

+

NA

=

NA

+

NA

+

10,000

+

NA

NA

−

NA

=

NA

10,000 FA

2.

NA

+

15,000

+

NA

=

NA

+

NA

+

NA

+

15,000

15,000

−

NA

=

15,000

NA

3.

5,000

+

NA

+

NA

=

NA

+

NA

+

NA

+

5,000

5,000

−

NA

=

5,000

5,000 OA

4.

2,800

+

NA

+

NA

=

NA

+

2,800

+

NA

+

NA

NA

−

NA

=

NA

2,800 OA

5.

12,200

+

(12,200)

+

NA

=

NA

+

NA

+

NA

+

NA

NA

−

NA

=

NA

12,200 OA

6.

(1,900)

+

NA

+

NA

=

NA

+

NA

+

NA

+

(1,900)

NA

−

1,900

=

(1,900)

(1,900) OA

7.

NA

+

NA

+

NA

=

NA

+

(1,400)

+

NA

+

1,400

1,400

−

NA

=

1,400

NA

8.

NA

+

NA

+

NA

=

3,600

+

NA

+

NA

+

(3,600)

NA

−

3,600

=

(3,600)

NA

9.

(4,800)

+

NA

+

4,800

=

NA

+

NA

+

NA

+

NA

NA

−

NA

=

NA

(4,800) OA

10.

(2,800)

+

NA

+

NA

=

(2,800)

+

NA

+

NA

+

NA

NA

−

NA

=

NA

(2,800) OA

11.

(1,500)

+

NA

+

NA

=

NA

+

NA

+

NA

+

(1,500)

NA

−

NA

=

NA

(1,500) FA

12.

NA

+

NA

+

(3,600)*

=

NA

+

NA

+

NA

+

(3,600)

NA

−

3,600

=

(3,600)

NA

Bal.

19,000

+

2,800

+

1,200

=

800

+

1,400

+

10,000

+

10,800

21,400

−

9,100

=

12,300

19,000 NC

*$4,800 x 9/12 = $3,600

2-67

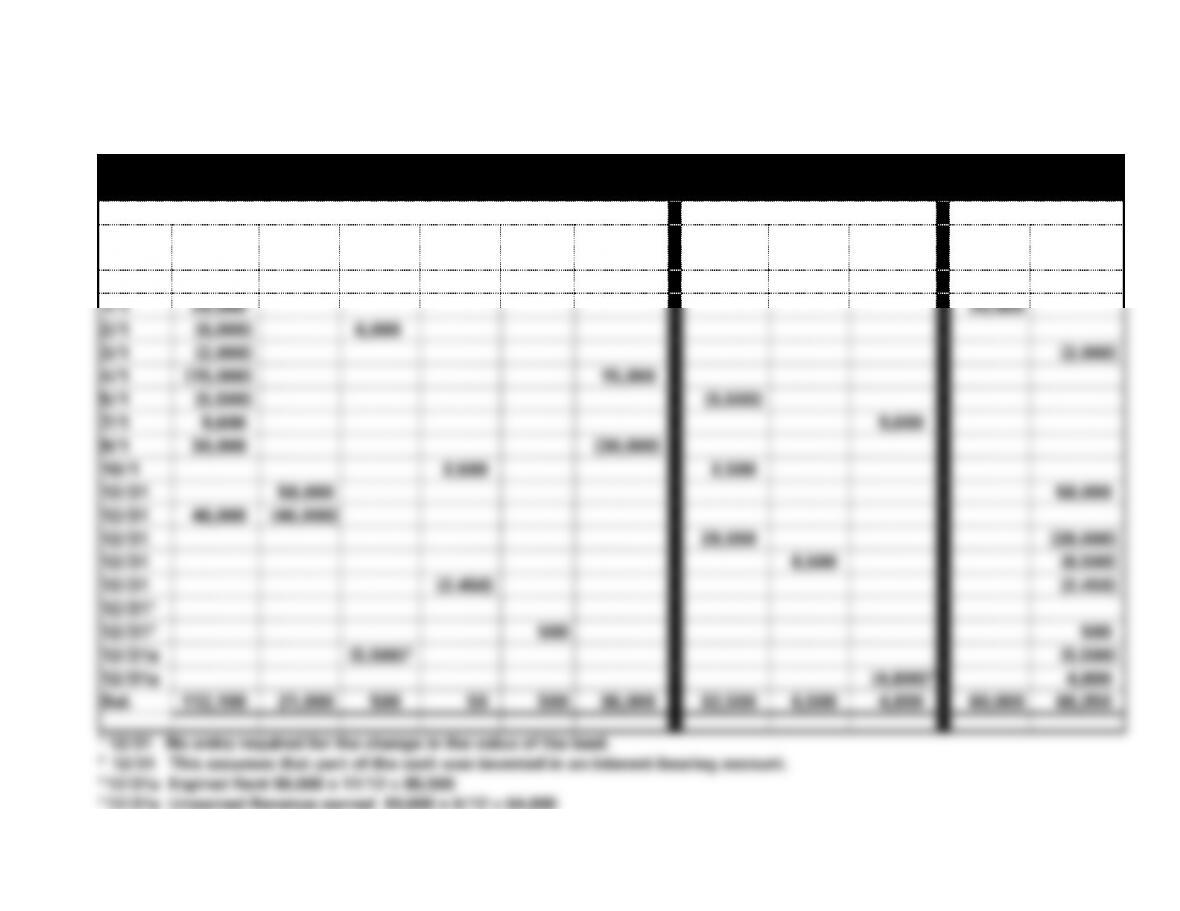

PROBLEM 2-40A

Accounting Equation (Prepared for Instructor's Use)

Accounting Equation

Assets

Liabilities

Stk. Equity

Date

Cash

Acc Rec.

Pp. Rent

Supp.

Int.

Rec.

Land

Acc. Pay.

Sal. Pay.

Unear.

Rev.

Com.

Stock

Ret. Earn

Bal.

35,000

9,000

51,000

7,500

40,000

47,500

1/1

20,000

20,000

2/1

(6,000)

6,000

3/1

(2,000)

(2,000)

4/1

(15,000)

15,000

5/1

(5,500)

(5,500)

7/1

9,600

9,600

9/1

30,000

(30,000)

10/1

2,500

2,500

12/31

58,000

58,000

12/31

46,000

(46,000)

12/31

28,000

(28,000)

12/31

6,500

(6,500)

12/31

(2,450)

(2,450)

12/311

12/312

500

500

12/31a

(5,500)3

(5,500)

12/31a

(4,800)4

4,800

Bal.

112,100

21,000

500

50

500

36,000

32,500

6,500

4,800

60,000

66,350

1 12/31 No entry required for the change in the value of the land.

2 12/31 This assumes that part of the cash was invested in an interest-bearing account.

3 12/31a Expired Rent $6,000 x 11/12 = $5,500

4 12/31a Unearned Revenue earned $9,600 x 6/12 = $4,800

2-68

PROBLEM 2-40A (cont.)

1. Feb. 1, prepaid rent.

2. July 1, unearned revenue; cash was received in advance.

b. $36,000; its historical cost.

c. $46,000 + $9,600 − $6,000 − $5,500 = $44,100