Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

8-105

PROBLEM 8-30B

Depreciation Calculation:

Straight Line:

Company A ($64,000 − $6,000) 5 = $11,600 per year

Double-Declining Balance:

8-106

PROBLEM 8-30B (cont.)

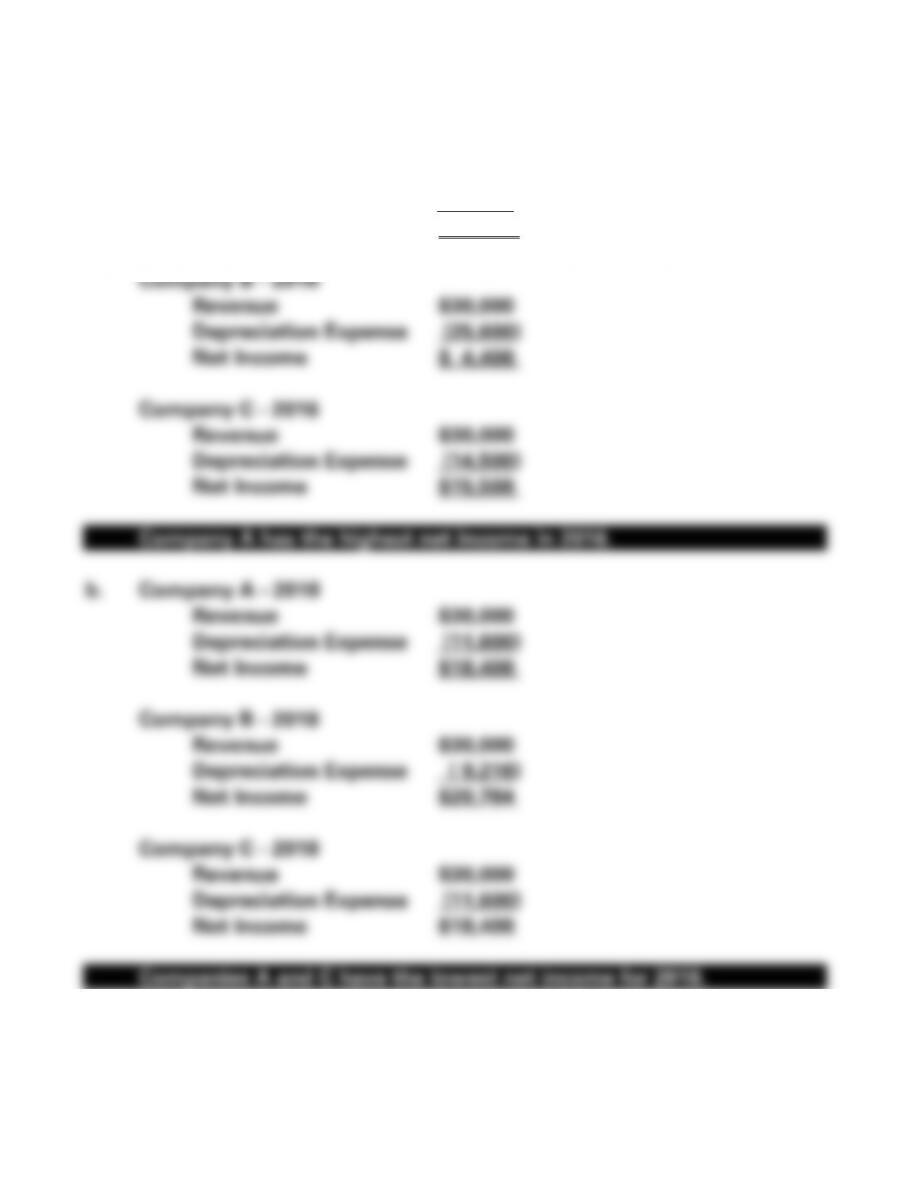

a. Company A - 2016

Revenue $30,000

Depreciation Expense (11,600)

Net Income $18,400

8-107

PROBLEM 8-30B (cont.)

c. Company A Accumulated Depreciation

2016 $11,600

2017 11,600

2018 11,600

8-108

PROBLEM 8-30B (cont.)

d. Company A: Sales (four years) $120,000

Depreciation (four years) (46,400)

Retained Earnings - 2019 $ 73,600

8-109

PROBLEM 8-31B

a.

Metals Exploration Company

General Journal

Date

Account Titles

Debit

Credit

2016

1/1

Coal Mine

900,000

Cash

900,000

7/1

Timber

1,800,000

Land

200,000

Cash

2,000,000

12/31

Depletion Expense (80,000 x $3)

240,000

Coal Mine

240,000

12/31

Depletion Expense (1,000,000 x $.60)

600,000

Timber

600,000

2017

2/1

Silver Mine

850,000

Cash

850,000

8/1

Oil Reserves

875,000

Cash

875,000

12/31

Depletion Expense (68,000 x $3)

204,000

Coal Mine

204,000

12/31

Depletion Expense (1,200,000 x $.60)

720,000

Timber

720,000

12/31

Depletion Expense (9,000 x $28.33)

254,970

Silver Mine

254,970

12/31

Depletion Expense (80,000 x $3.50)

280,000

Oil Reserves

280,000

8-110

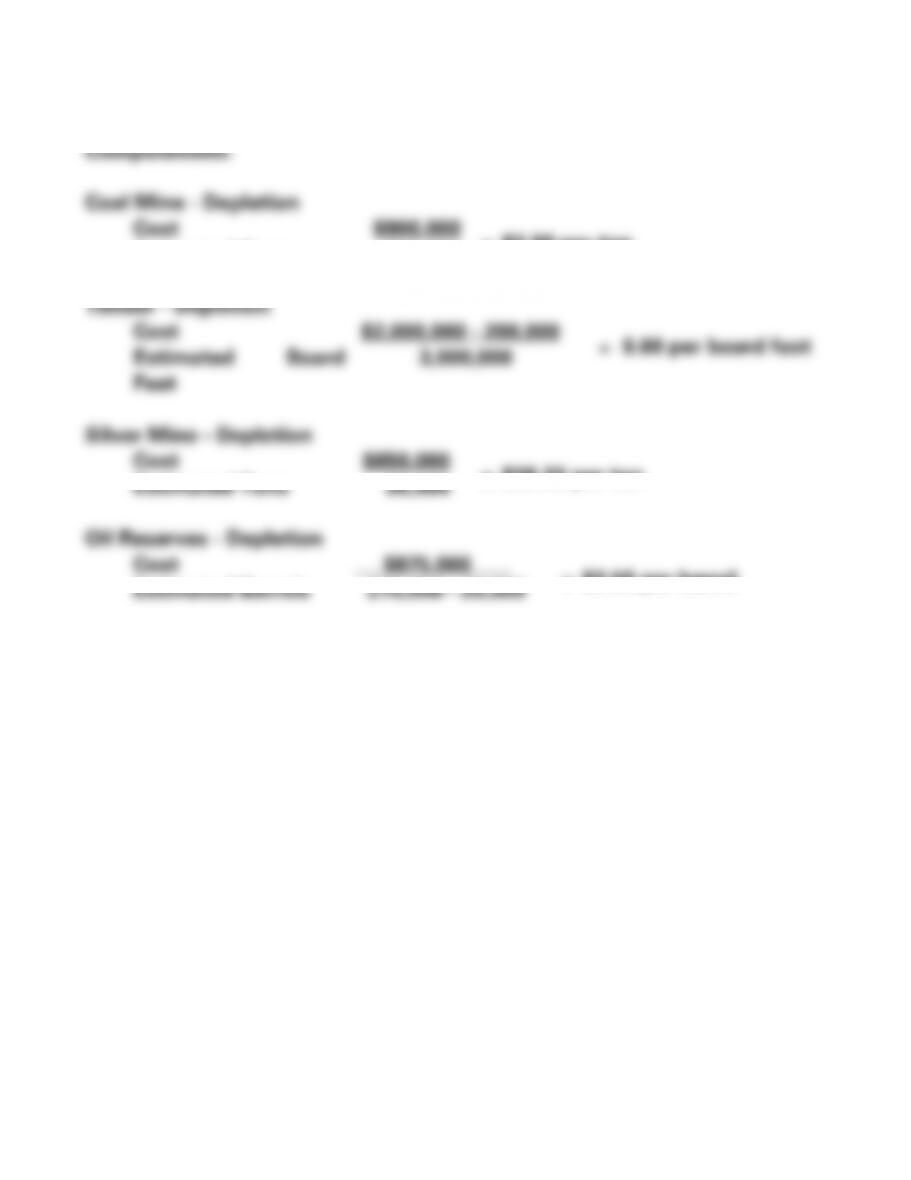

PROBLEM 8-31B (cont.)

Cost

$900,000

=

$3.00 per ton

Estimated Tons

300,000

Cost

$2,000,000 - 200,000

=

$.60 per board foot

Estimated Board

Feet

3,000,000

Silver Mine - Depletion

Cost

$850,000

=

$28.33 per ton

Estimated Tons

30,000

Oil Reserves - Depletion

Cost

$875,000

=

$3.50 per barrel

Estimated Barrels

270,000 - 20,000

PROBLEM 8-31B (cont.)

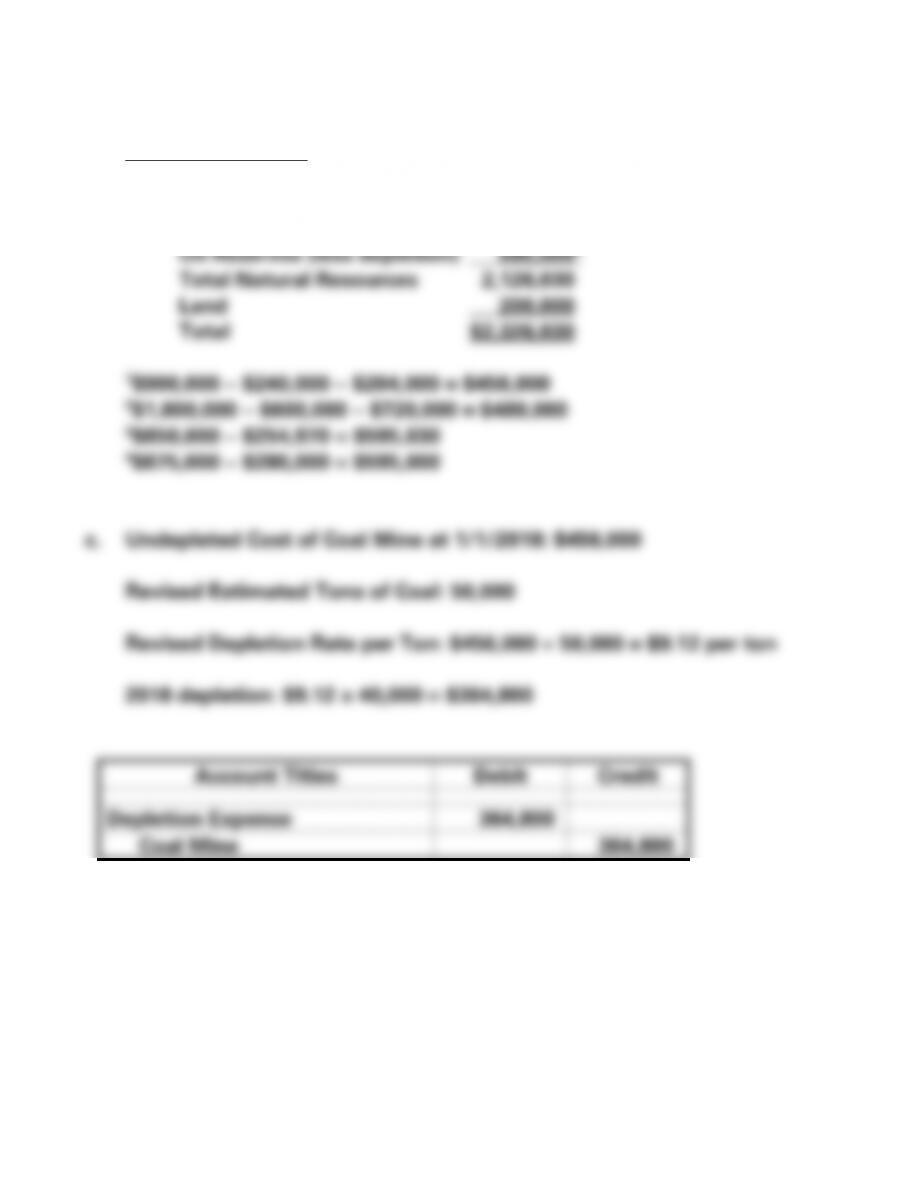

b. Natural Resources

Coal Mine (less depletion) $ 456,0001

Timber (less depletion) 480,0002

Silver Mine (less depletion) 595,0303

8-112

PROBLEM 8-32B

a.

Horizontal Statements Model

Date

Assets

=

Liab.

+

Equity

Net Income

Cash Flows

1/1/16

+−

NA

NA

NA

− IA

12/31/16

−

NA

−

−

NA

5/5/17

−

NA

−

−

− OA

12/31/17

−

NA

−

−

NA

1/1/18

+−

NA

NA

NA

− IA

12/31/18

−

NA

−

−

NA

3/1/19

−

NA

−

−

− OA

12/31/19

−

NA

−

−

NA

1/1/20

+−

NA

NA

NA

− IA

12/31/20

−

NA

−

−

NA

7/1/21*

−

NA

−

−

NA

7/1/21**

+

NA

+

+

+ IA

*To record depreciation for 2021.

8-113

PROBLEM 8-32B (cont.)

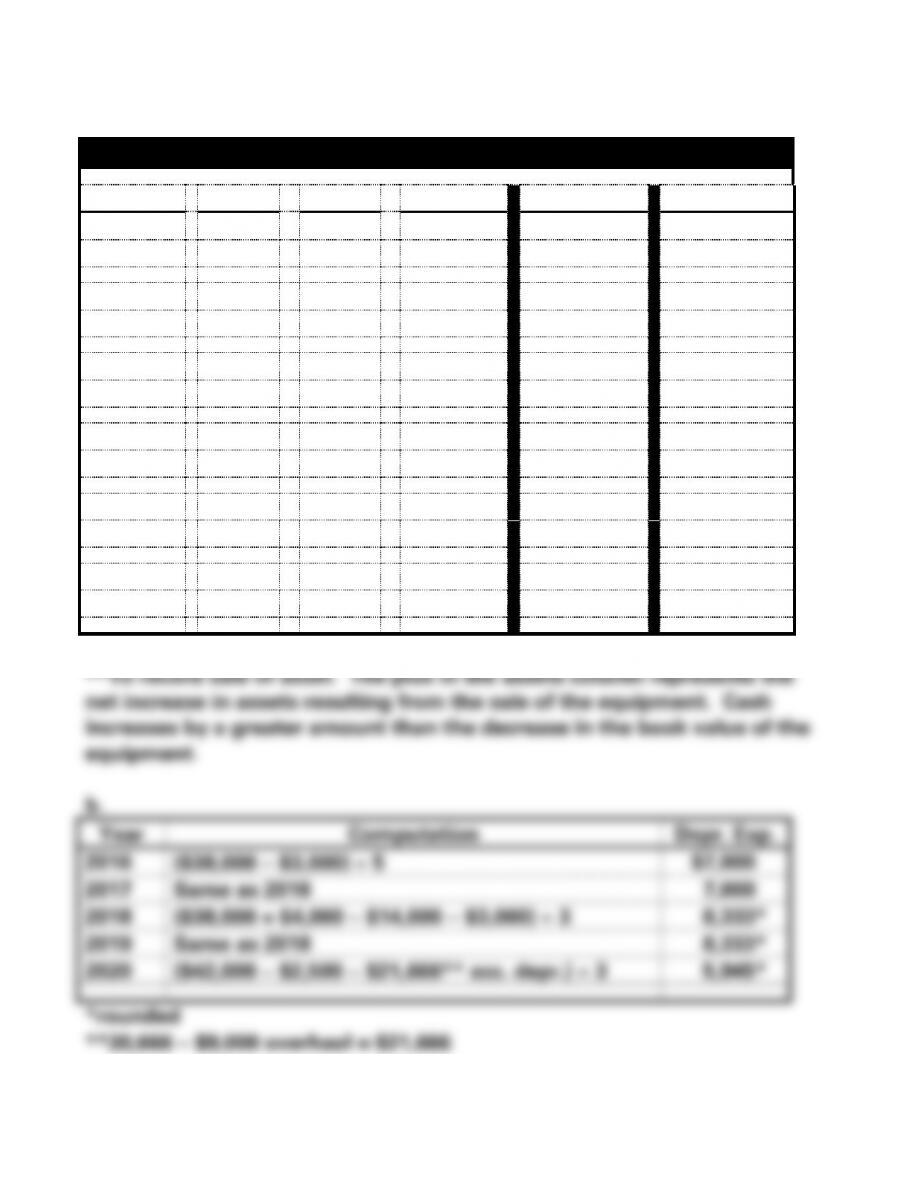

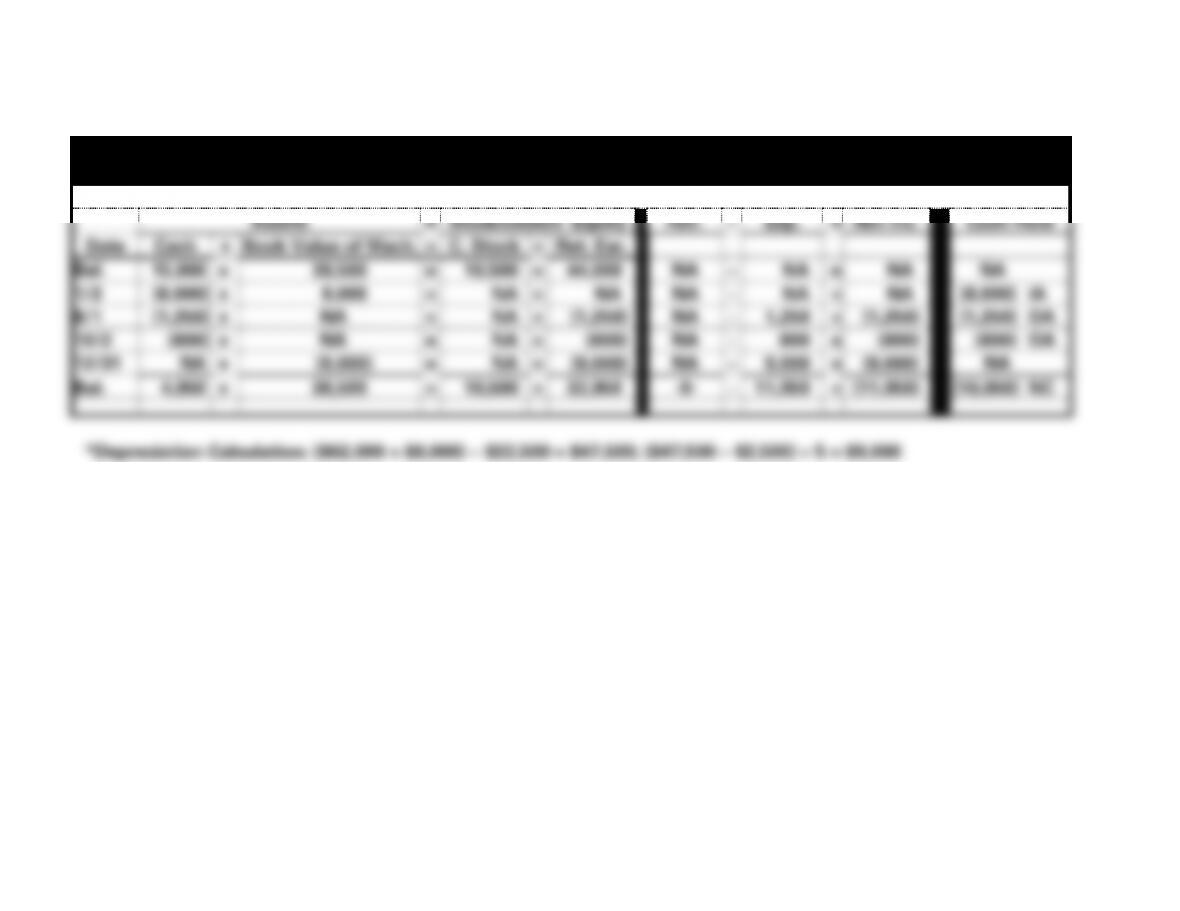

c.

Computation of Book Value

Year

Cost

−

Acc. Depr.

=

Book Value

2016

$38,000

−

$7,000

=

$31,000

2017

38,000

−

14,000

=

24,000

2018

42,000

−

22,333

=

19,667

2019

42,000

−

30,666

=

11,334

2020

42,000

−

27,611*

=

14,389

*$30,666 − $9,000 overhaul + $5,945 depreciation expense.

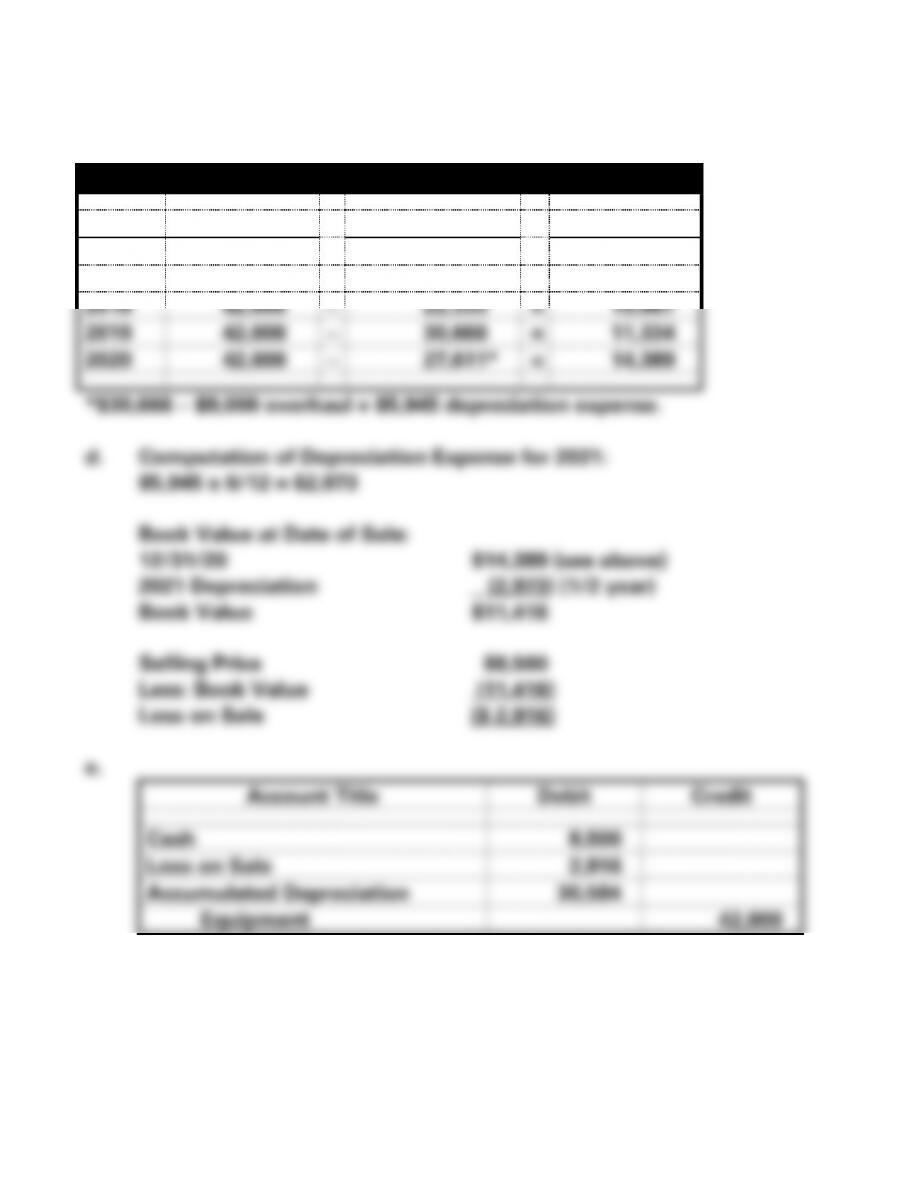

d. Computation of Depreciation Expense for 2021:

$5,945 x 6/12 = $2,973

Book Value at Date of Sale:

12/31/20 $14,389 (see above)

2021 Depreciation (2,973) (1/2 year)

Book Value $11,416

Selling Price $8,500

Less: Book Value (11,416)

Loss on Sale ($ 2,916)

e.

Account Title

Debit

Credit

Cash

8,500

Loss on Sale

2,916

Accumulated Depreciation

30,584

Equipment

42,000

8-114

PROBLEM 8-33B

a. NC = Net Change in Cash

Delta Manufacturing

Statements Model - 2019

Assets

=

Stockholders’ Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

Date

Cash

+

Book Value of Mach.

=

C. Stock

+

Ret. Ear.

Bal.

15,000

+

39,500

=

10,500

+

44,000

NA

−

NA

=

NA

NA

1/2

(8,000)

+

8,000

=

NA

+

NA

NA

−

NA

=

NA

(8,000) IA

8/1

(1,250)

+

NA

=

NA

+

(1,250)

NA

−

1,250

=

(1,250)

(1,250) OA

10/2

(800)

+

NA

=

NA

+

(800)

NA

−

800

=

(800)

(800) OA

12/31

NA

+

(9,000)

=

NA

+

(9,000)

NA

−

9,000

=

(9,000)

NA

Bal.

4,950

+

38,500

=

10,500

+

32,950

-0-

−

11,050

=

(11,050)

(10,050) NC

*Depreciation Calculation: ($62,000 + $8,000) − $22,500 = $47,500; ($47,500 − $2,500) 5 = $9,000

8-8

PROBLEM 8-33B (cont.)

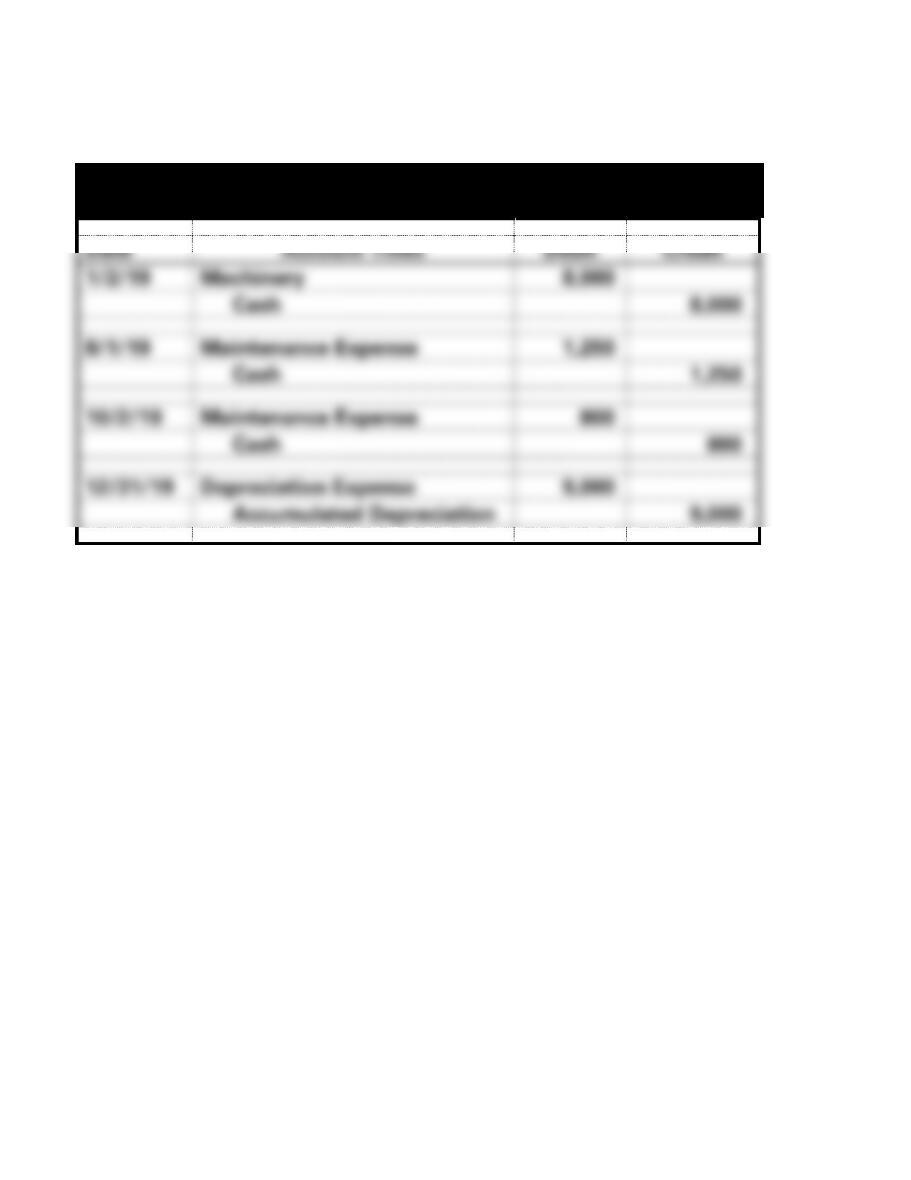

b.

Delta Manufacturing

General Journal

Date

Account Titles

Debit

Credit

1/2/19

Machinery

8,000

Cash

8,000

8/1/19

Maintenance Expense

1,250

Cash

1,250

10/2/19

Maintenance Expense

800

Cash

800

12/31/19

Depreciation Expense

9,000

Accumulated Depreciation

9,000

8-9

PROBLEM 8-34B

a. Acquisition Price $1,500,000

Less: FV of Assets Acquired

8-10

PROBLEM 8-35B

a. Any permanent impairment will be written off in the year the

8-11

1. Long-term operational assets are those assets that are used by a

2. Tangible assets are those assets that have a physical existence. Some

3. Specifically identifiable intangible assets are those assets that are

4. Depreciation is the systematic allocation of the cost of property, plant

5. Natural resources are assets that are produced by nature. Some

6. Land is not a depreciable asset because land has an infinite life. Land

8-12

resources are purchased together, the cost of each must be accounted

7. Amortization is the systematic allocation of the cost of intangible

8. The historical cost concept requires that long-term operational assets

be recorded at the amount paid for them. This is the amount that will

be shown on the balance sheet as long as the asset is owned. As time

9. The cost of a building includes the amount paid for the building plus

10. A basket purchase of assets is the purchase of a group of assets for a

single purchase price. For example, building, land and equipment

could be purchased for one price, $80,000. When a group of assets are

11. The life cycle of a long-term operational asset simply describes the

12. Straight-line depreciation. This method allocates an equal amount of

8-13

value would produce a depreciation expense of $1,000 per year. This

method is appropriate when the usefulness of an asset is consistent

over the asset's life.

Units-of-production depreciation. When this method of depreciation

.25)]. The amount of depreciation expense will decrease each year of

13. Recognition of depreciation expense reduces total assets; while

the asset account containing the asset that is being depreciated is not

14. The recognition of depreciation expense does not affect cash flows.

8-14

asset is purchased, when an improvement is made to the asset, and

15. Total assets will be lower at the end of the first year of the asset’s life

if MalMax chooses the double-declining balance method of computing

16. When the total cost of an asset is expensed in the year acquired, total

expense will be overstated and net income will be understated.

17. Salvage value is the estimated value of a plant asset at the end

18. Accumulated depreciation is a contra asset account. As the cost of a

19. Book value of an asset is its historical cost less any accumulated

20. Recording the depreciation recognized in the contra asset account

allows the total cost of the asset and the total amount expensed to be

21. Book value is computed as the cost of an asset less the accumulated

8-15

accumulated depreciation is only an allocation of the cost based on

22. The method of depreciation chosen should represent as closely

as possible the pattern of usage of that piece of equipment. For

23. MACRS, Modified Accelerated Cost Recovery System, is the

prescribed method to be used for tax purposes. Under MACRS, useful

24. The method required for tax purposes, MACRS, does not necessarily

reflect the use of the asset. The recovery period and method is set by

25. Deferred income taxes are taxes that will be paid in future years that

26. When an asset is purchased and put into service, an estimate is

made of the expected useful life of the asset. However, as the asset is

8-16

arise, it is necessary to revise the estimated useful life of the asset and,

consequently, the amount of depreciation expense per period. The

27. When an expenditure improves the quality of an asset, this

improvement is accounted for as if a new asset is purchased; the

equipment account is debited. The improvement is depreciated over

28. When a long-term operational asset is sold for a gain, total assets and

equity increase by the amount of the gain. The gain is the amount the

29. Depletion is the process of systematically allocating the cost of

natural resources to expense based on estimated production of the

8-17

30. Some of the most common intangible assets include patents,

31. One major difference between U.S. GAAP and IFRS for long-term

operational assets is that U.S. GAAP requires the use of historical

cost for its long-term assets, but under IFRS a company has two

32. If two companies in the same industry have the same asset with the

same cost and each makes a different estimate of useful life or

salvage value, and/or uses a different depreciation method, the

depreciation expense will be of differing amounts. More depreciation