Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

11-77

EXERCISE 11-3B (cont.)

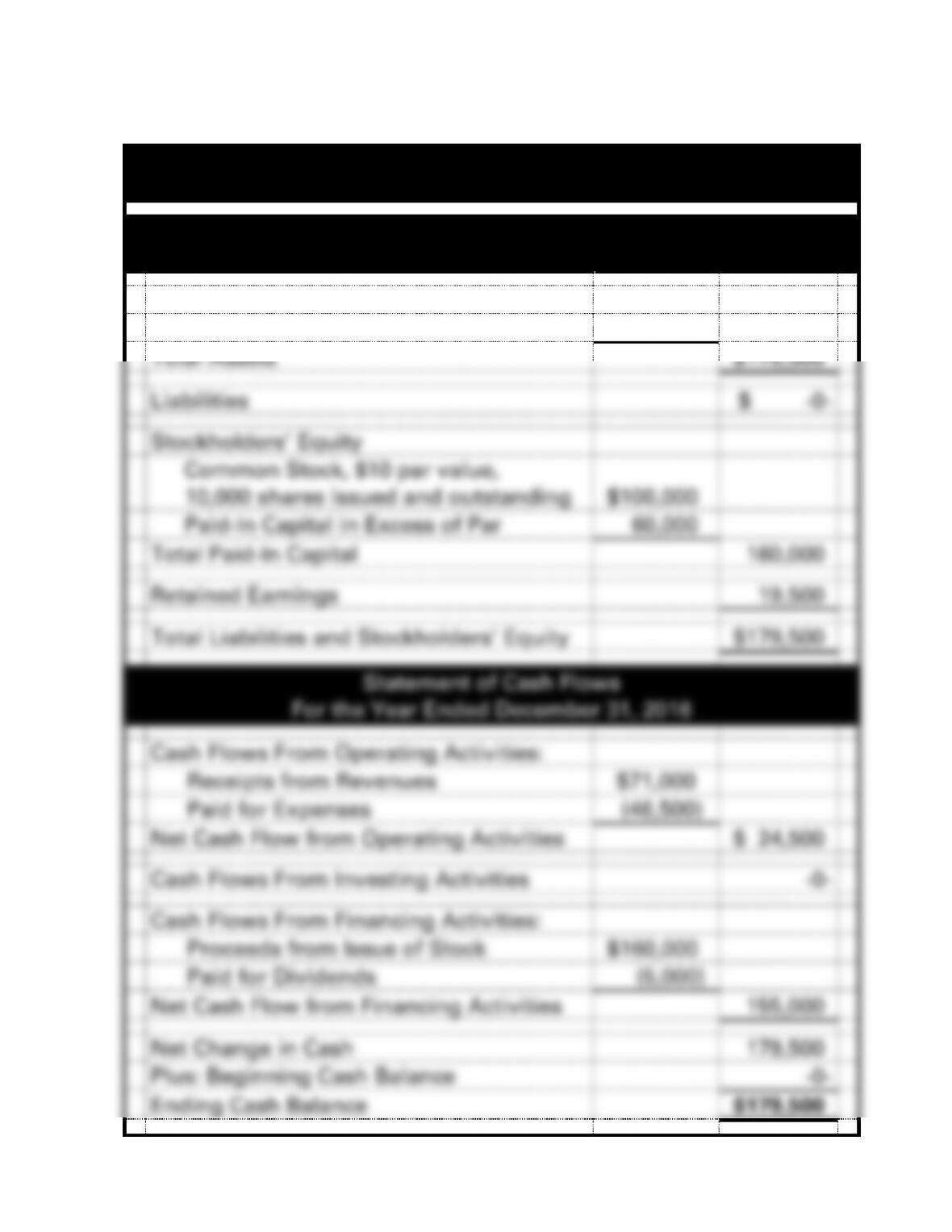

Bozeman Corporation

Financial Statements

Balance Sheet

As of December 31, 2016

Assets

Cash

$179,500

Total Assets

$179,500

Liabilities

$ -0-

Stockholders’ Equity

Common Stock, $10 par value,

10,000 shares issued and outstanding

$100,000

Paid-In Capital in Excess of Par

60,000

Total Paid-In Capital

160,000

Retained Earnings

19,500

Total Liabilities and Stockholders’ Equity

$179,500

Statement of Cash Flows

For the Year Ended December 31, 2016

Cash Flows From Operating Activities:

Receipts from Revenues

$71,000

Paid for Expenses

(46,500)

Net Cash Flow from Operating Activities

$ 24,500

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities:

Proceeds from Issue of Stock

$160,000

Paid for Dividends

(5,000)

Net Cash Flow from Financing Activities

155,000

Net Change in Cash

179,500

Plus: Beginning Cash Balance

-0-

Ending Cash Balance

$179,500

11-78

EXERCISE 11-4B

a.

Balance Sheet

Income Statement

Stmt. of

Event

Assets

=

Liab

+

Stkholders’ Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

Cash

=

+

C. Stk.

+

PIC Exc.

3/1

240,000

=

NA

+

200,000

+

40,000

NA

−

NA

=

NA

240,000 FA

5/2

450,000

=

NA

+

300,000

+

150,000

NA

−

NA

=

NA

450,000 FA

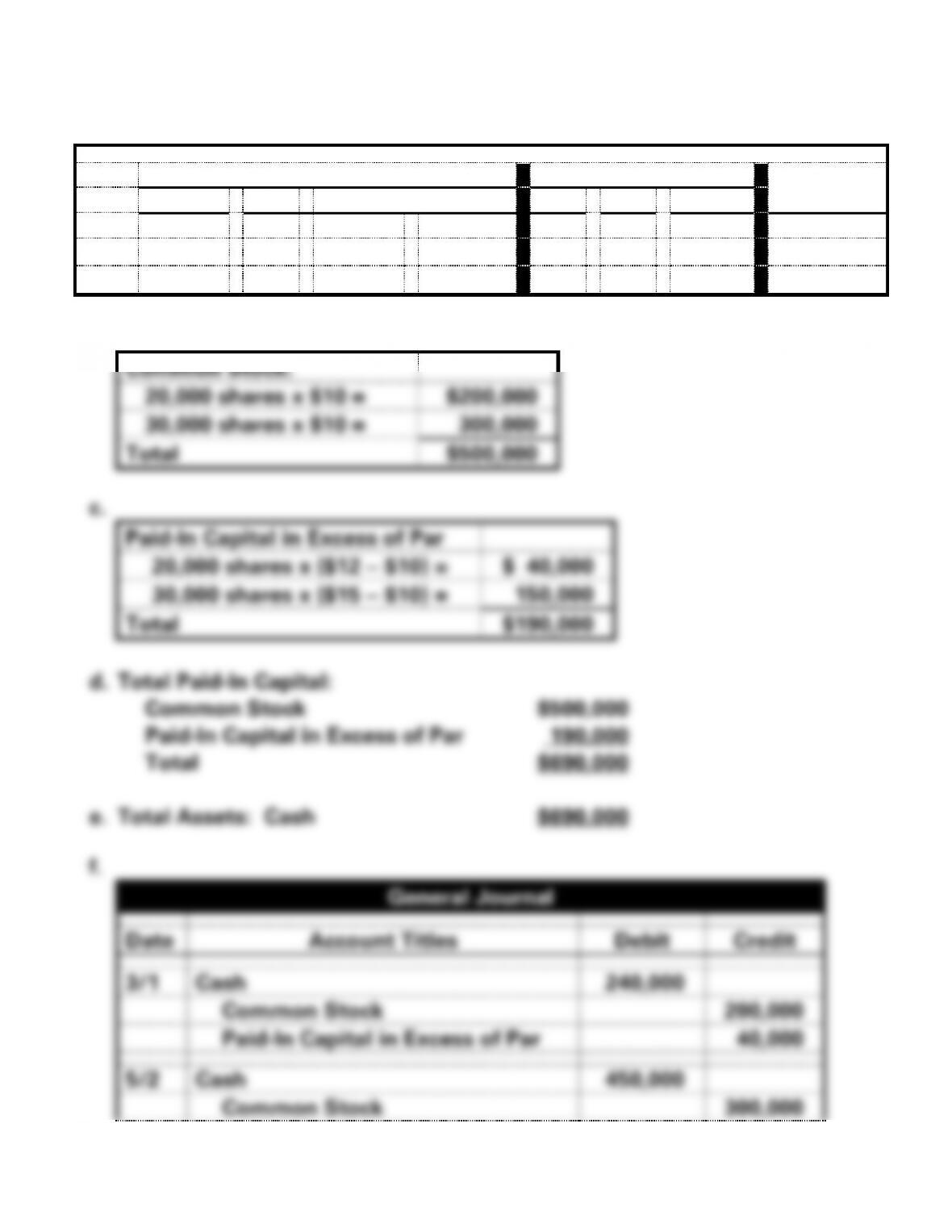

b.

Common Stock:

20,000 shares x $10 =

$200,000

30,000 shares x $10 =

300,000

Total

$500,000

c.

Paid-In Capital in Excess of Par

20,000 shares x ($12 − $10) =

$ 40,000

30,000 shares x ($15 − $10) =

150,000

Total

$190,000

d. Total Paid-In Capital:

Common Stock $500,000

Paid-In Capital in Excess of Par 190,000

Total $690,000

e. Total Assets: Cash $690,000

f.

General Journal

Date

Account Titles

Debit

Credit

3/1

Cash

240,000

Common Stock

200,000

Paid-In Capital in Excess of Par

40,000

5/2

Cash

450,000

Common Stock

300,000

11-79

Paid-In Capital in Excess of Par

150,000

11-80

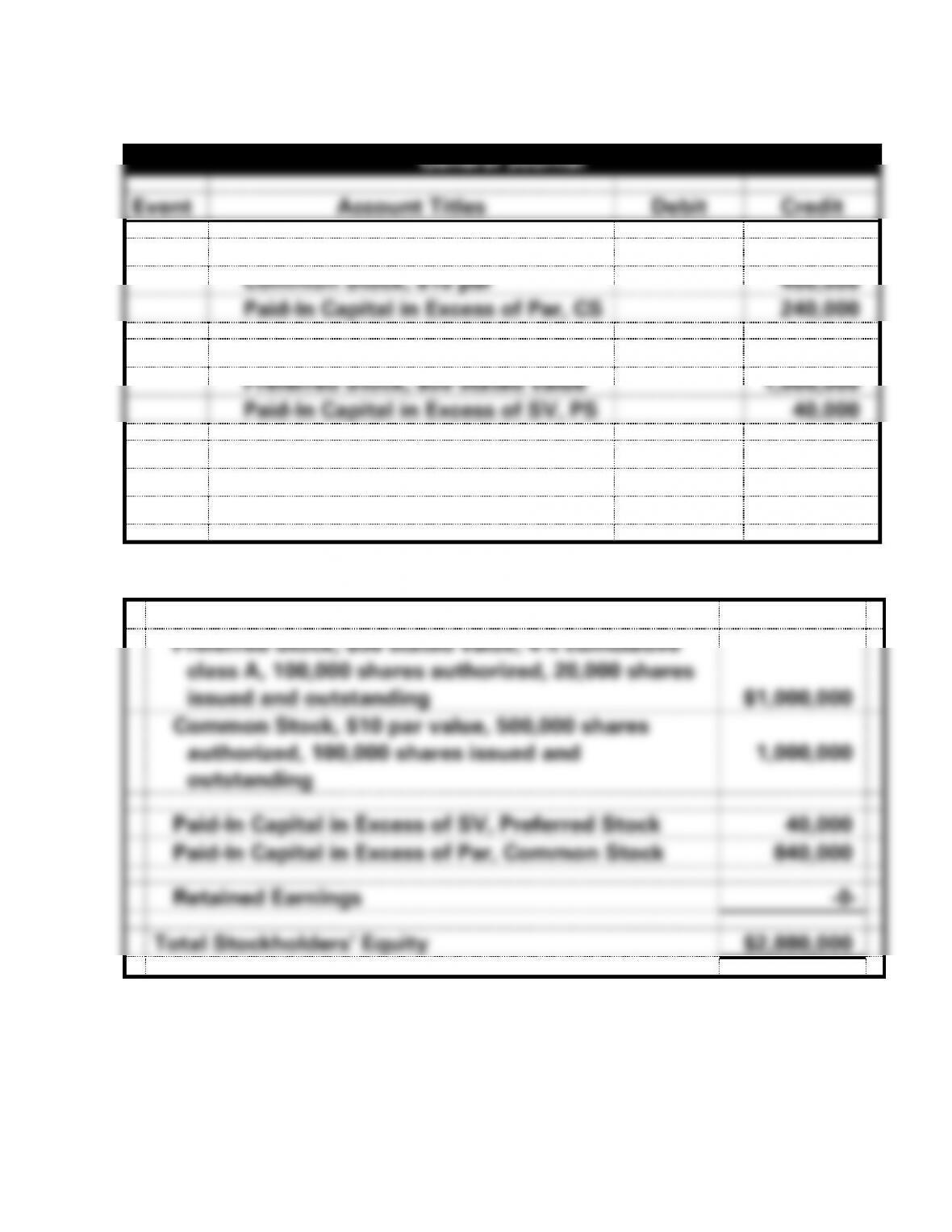

EXERCISE 11-5B

a.

General Journal

Event

Account Titles

Debit

Credit

1.

Cash (40,000 x $16)

640,000

Common Stock, $10 par

400,000

Paid-In Capital in Excess of Par, CS

240,000

2.

Cash (20,000 x $52)

1,040,000

Preferred Stock, $50 stated value

1,000,000

Paid-In Capital in Excess of SV, PS

40,000

3.

Cash (60,000 x $20)

1,200,000

Common Stock, $10 par

600,000

Paid-In Capital in Excess of Par, CS

600,000

b.

Stockholders’ Equity:

Preferred Stock, $50 stated value, 4% cumulative

class A, 100,000 shares authorized, 20,000 shares

issued and outstanding

$1,000,000

Common Stock, $10 par value, 500,000 shares

authorized, 100,000 shares issued and

outstanding

1,000,000

Paid-In Capital in Excess of SV, Preferred Stock

40,000

Paid-In Capital in Excess of Par, Common Stock

840,000

Retained Earnings

-0-

Total Stockholders’ Equity

$2,880,000

11-81

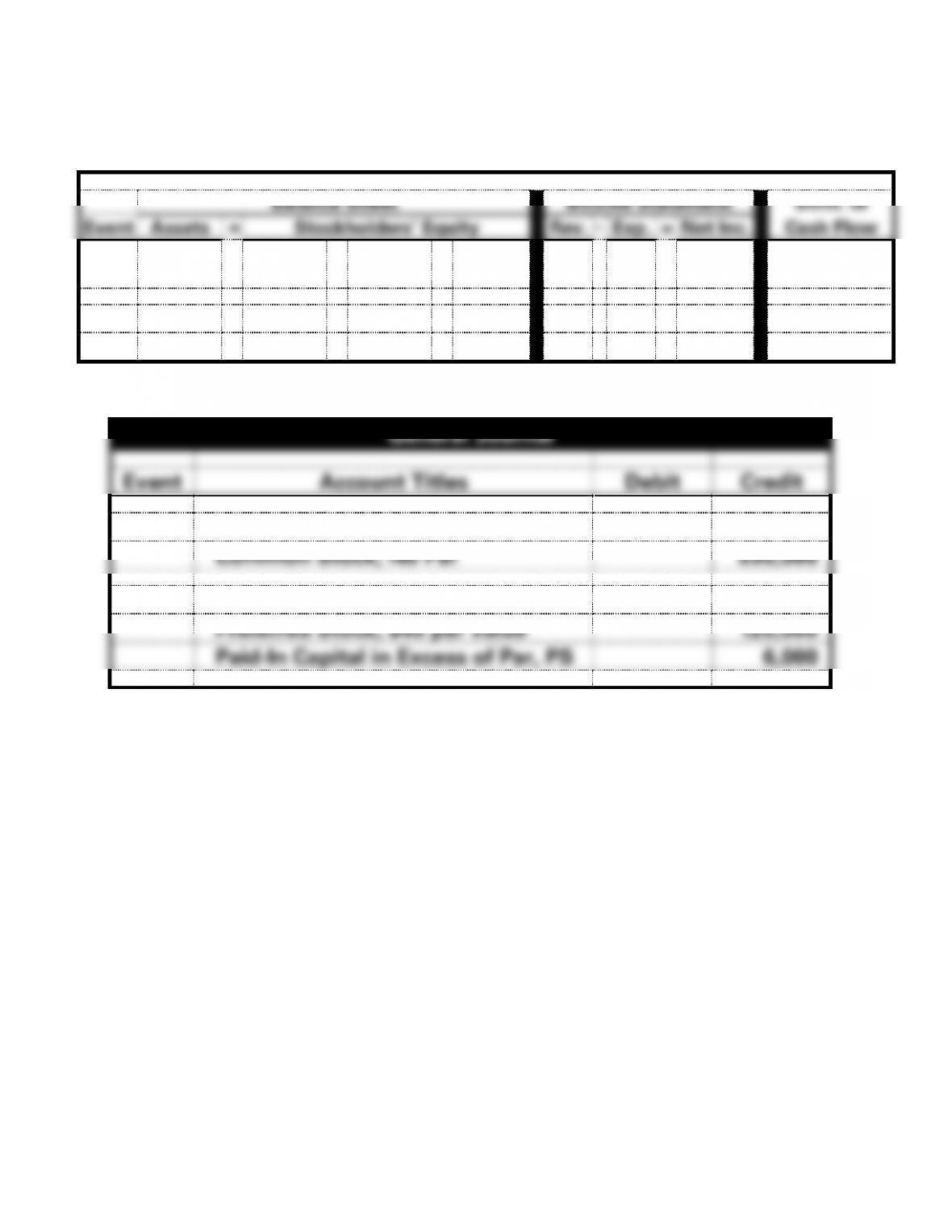

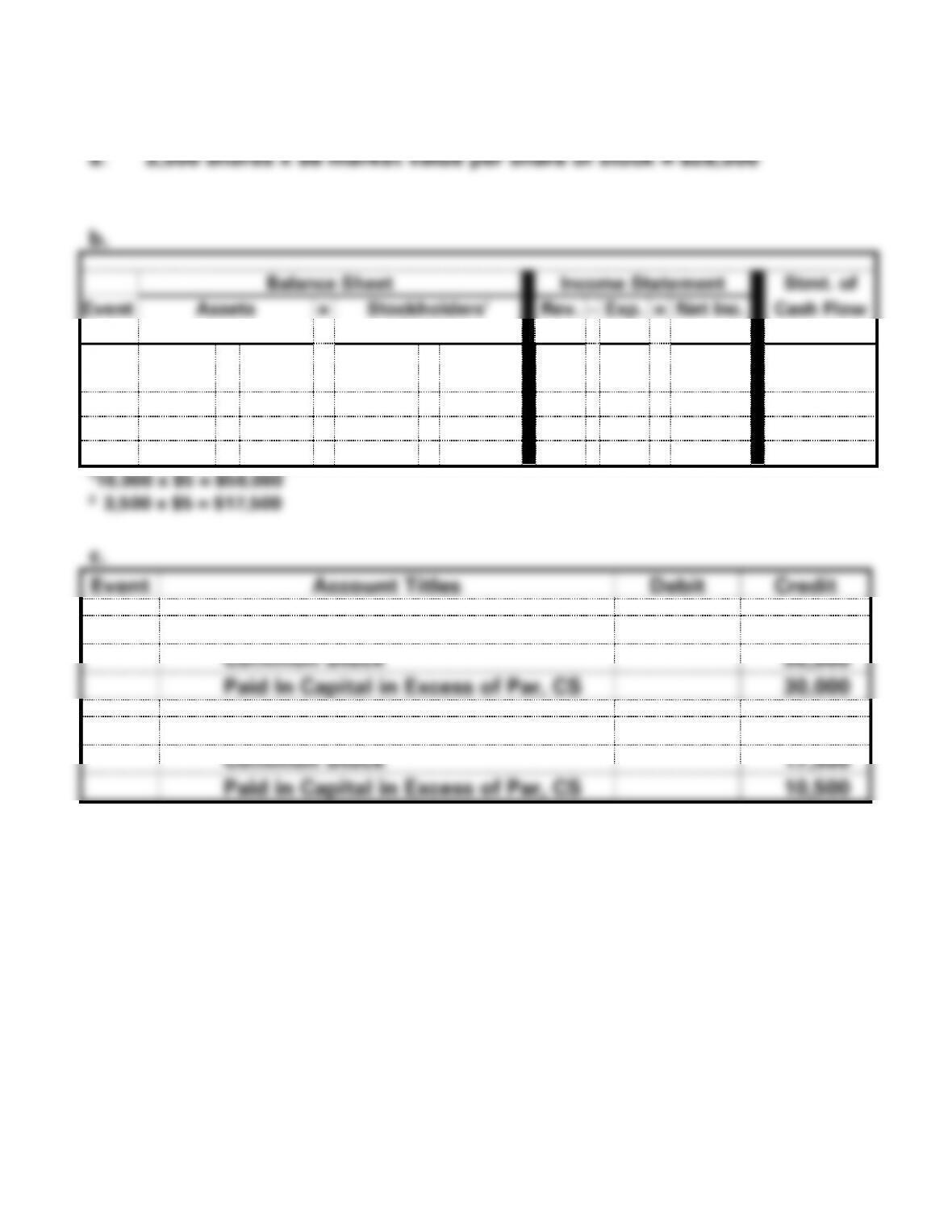

EXERCISE 11-6B

a.

Balance Sheet

Income Statement

Stmt. of

Event

Assets

=

Stockholders’ Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

Cash

=

Pref.

Stock

+

No-Par

C. Stock

+

PIC in

Excess

1.

250,000

=

NA

+

250,000

+

NA

NA

−

NA

=

NA

250,000 FA

2.

126,000

=

120,000

+

NA

+

6,000

NA

−

NA

=

NA

126,000 FA

b.

General Journal

Event

Account Titles

Debit

Credit

1.

Cash

250,000

Common Stock, No Par

250,000

2.

Cash

126,000

Preferred Stock, $40 par value

120,000

Paid-In Capital in Excess of Par, PS

6,000

EXERCISE 11-7B

EXERCISE 11-8B

a.

Earles Corporation

General Journal

Date

Account Titles

Debit

Credit

1.

Treasury Stock (4,000 x $30)

120,000

Cash

120,000

2.

Cash (2,500 x $35)

87,500

Treasury Stock (2,500 x $30)

75,000

Paid-In Capital in Excess of Cost, TS

12,500

11-84

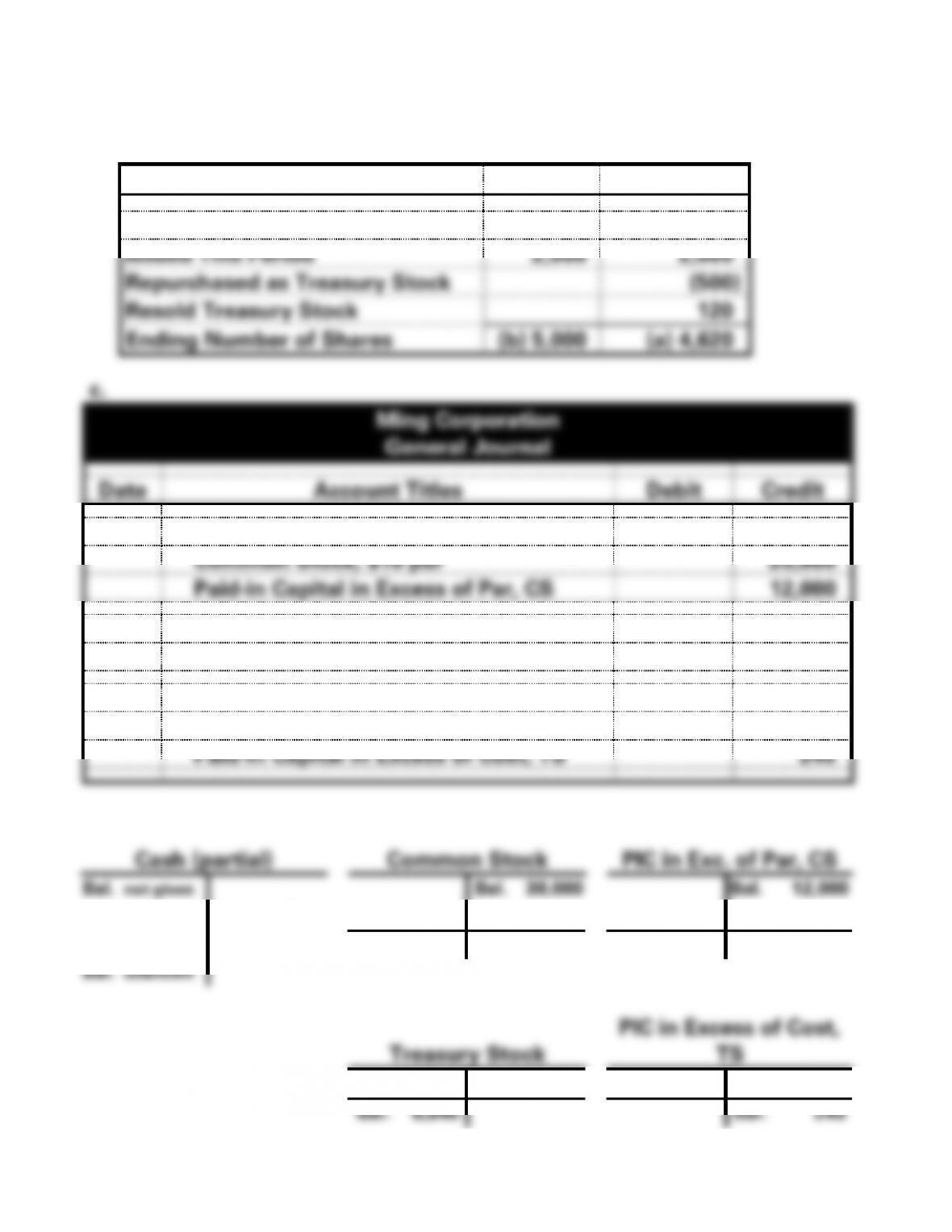

EXERCISE 11-9B

a. & b.

Common Stock

Issued

Outstanding

Beginning Number of Shares

3,000

3,000

Issued This Period

2,000

2,000

Repurchased as Treasury Stock

(500)

Resold Treasury Stock

120

Ending Number of Shares

(b) 5,000

(a) 4,620

c.

Ming Corporation

General Journal

Date

Account Titles

Debit

Credit

1.

Cash (2,000 x $16)

32,000

Common Stock, $10 par

20,000

Paid-in Capital in Excess of Par, CS

12,000

2.

Treasury Stock (500 x $18)

9,000

Cash

9,000

3.

Cash (120 x $20)

2,400

Treasury Stock (120 x $18)

2,160

Paid-In Capital in Excess of Cost, TS

240

Cash (partial)

Common Stock

PIC in Exc. of Par, CS

Bal. not given

Bal. 30,000

Bal. 12,000

1. 32,000

2. 9,000

1. 20,000

1. 12,000

3. 2,400

Bal. 50,000

Bal. 24,000

Bal. unknown

Treasury Stock

PIC in Excess of Cost,

TS

2. 9,000

3. 2,160

3. 240

Bal. 6,840

Bal. 240

11-85

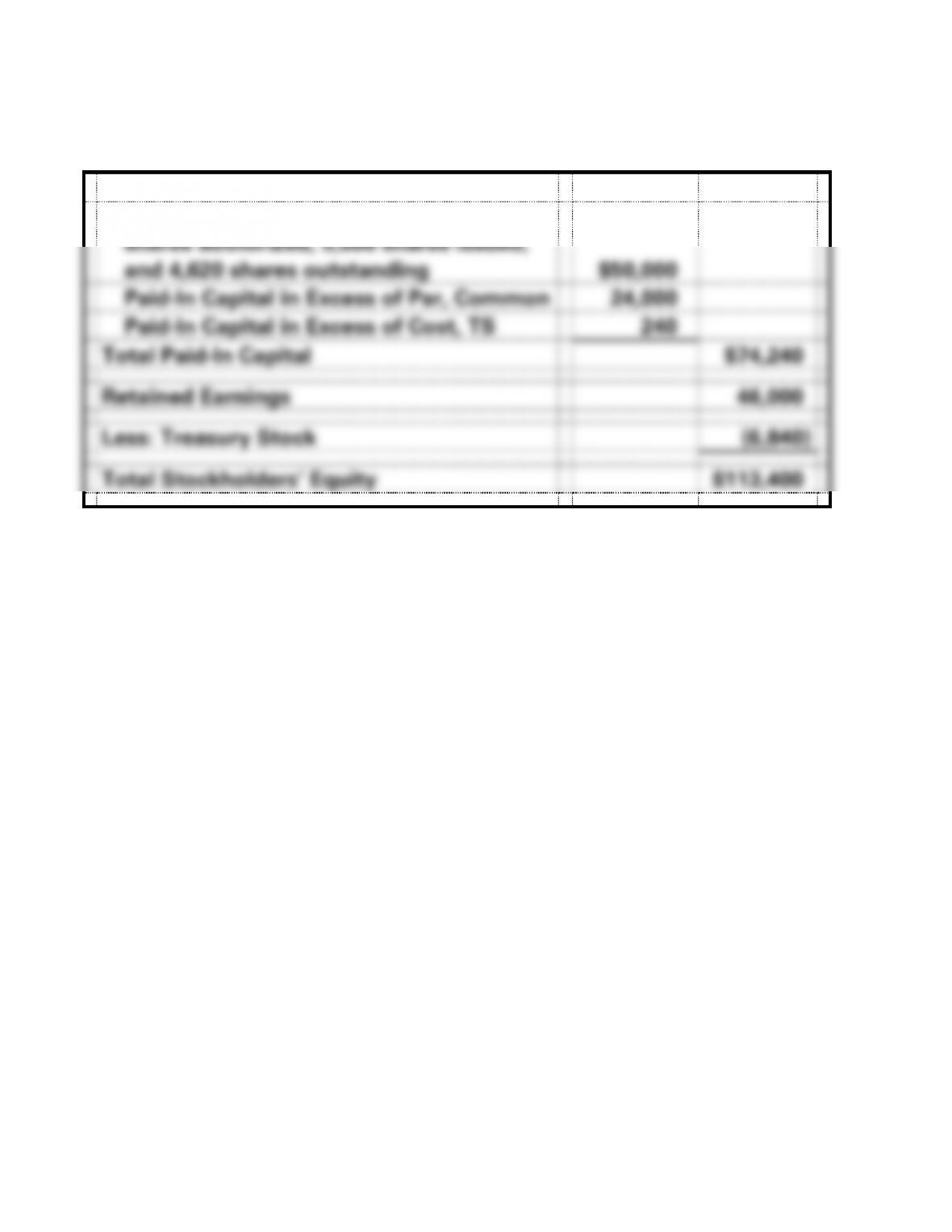

EXERCISE 11-9B (cont.)

d.

Stockholders’ Equity

Common Stock, $10 par value, 50,000

shares authorized, 5,000 shares issued,

and 4,620 shares outstanding

$50,000

Paid-In Capital in Excess of Par, Common

24,000

Paid-In Capital in Excess of Cost, TS

240

Total Paid-In Capital

$74,240

Retained Earnings

46,000

Less: Treasury Stock

(6,840)

Total Stockholders’ Equity

$113,400

11-86

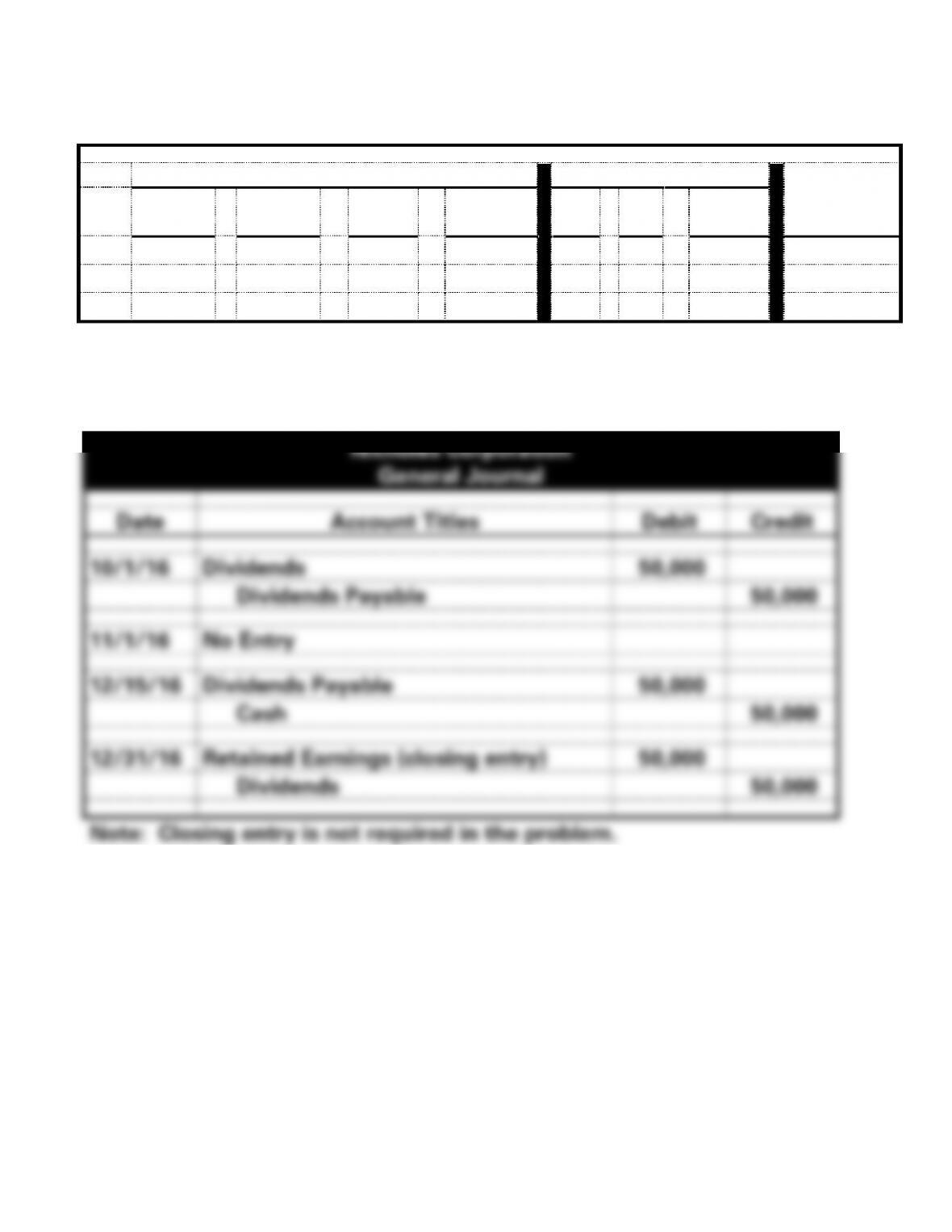

EXERCISE 11-10B

a.

Balance Sheet

Income Statement

Statement

Date

Assets

=

Liab.

+

Com.

Stk.

+

Ret. Ear.

Rev

−

Exp.

=

Net Inc.

of

Cash Flow

10/1

NA

=

50,000

+

NA

+

(50,000)

NA

−

NA

=

NA

NA

11/1

NA

=

NA

+

NA

+

NA

NA

−

NA

=

NA

NA

12/15

(50,000)

=

(50,000)

+

NA

+

NA

NA

−

NA

=

NA

(50,000) FA

b.

Nicholes Corporation

General Journal

Date

Account Titles

Debit

Credit

10/1/16

Dividends

50,000

Dividends Payable

50,000

11/1/16

No Entry

12/15/16

Dividends Payable

50,000

Cash

50,000

12/31/16

Retained Earnings (closing entry)

50,000

Dividends

50,000

Note: Closing entry is not required in the problem.

11-87

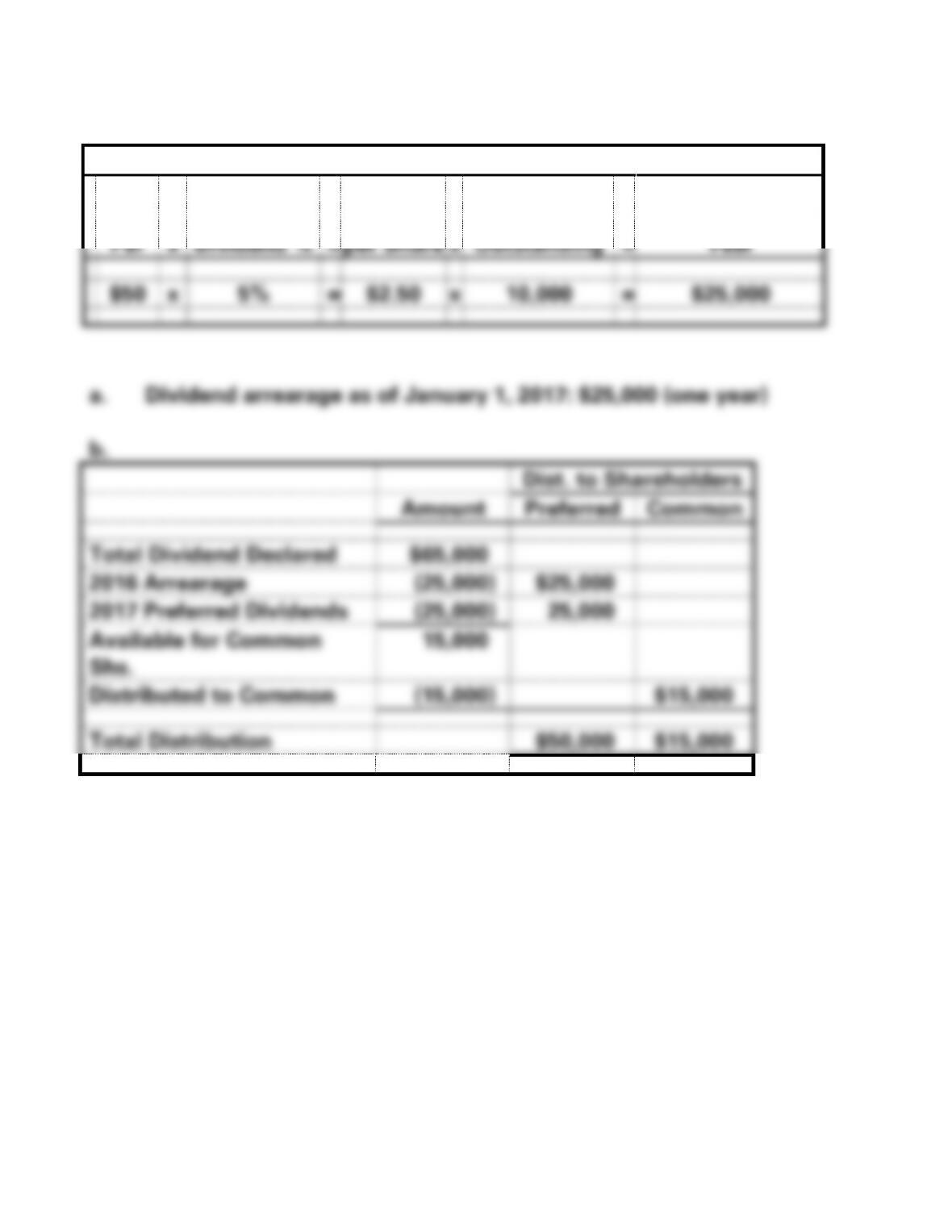

EXERCISE 11-11B

Computation of Preferred Dividends:

Par

x

Dividend %

=

Dividend

per Share

x

Number of

Shares

Outstanding

=

Total Preferred

Dividends for

Year

$50

x

5%

=

$2.50

x

10,000

=

$25,000

a. Dividend arrearage as of January 1, 2017: $25,000 (one year)

b.

Dist. to Shareholders

Amount

Preferred

Common

Total Dividend Declared

$65,000

2016 Arrearage

(25,000)

$25,000

2017 Preferred Dividends

(25,000)

25,000

Available for Common

Shs.

15,000

Distributed to Common

(15,000)

$15,000

Total Distribution

$50,000

$15,000

11-88

EXERCISE 11-12B

a.

Computation of Dividends to Be Paid:

Preferred Stock

$100 par value x 4% x 8,000 shares=

$32,000

Common Stock

$.5 x 200,000 shares =

100,000

Total Dividend

$132,000

11-89

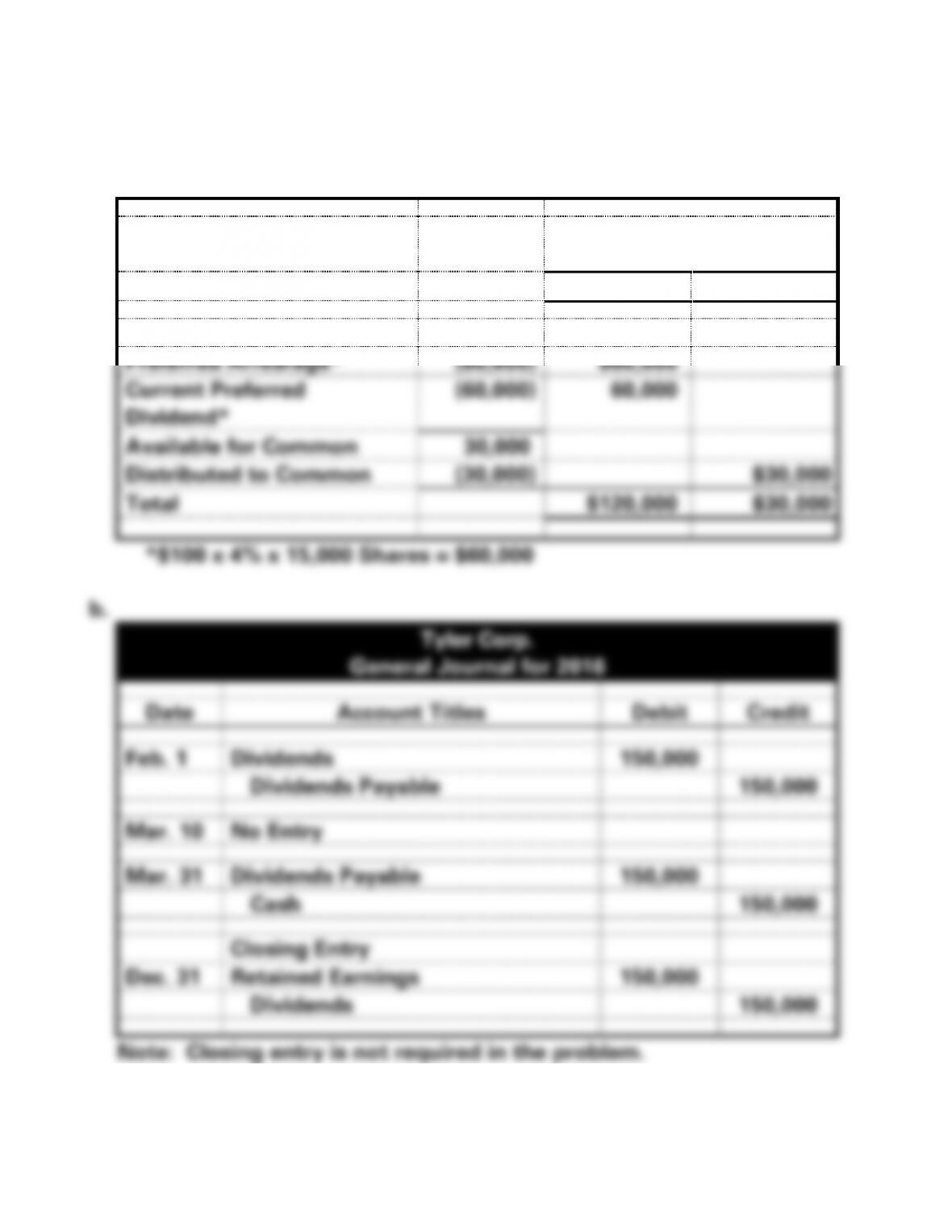

EXERCISE 11-13B

a. Distribution of Dividend:

Distributed to

Shareholders

Preferred

Common

Total Dividend Declared

$150,000

Preferred Arrearage*

(60,000)

$60,000

Current Preferred

Dividend*

(60,000)

60,000

Available for Common

30,000

Distributed to Common

(30,000)

$30,000

Total

$120,000

$30,000

*$100 x 4% x 15,000 Shares = $60,000

b.

Tyler Corp.

General Journal for 2016

Date

Account Titles

Debit

Credit

Feb. 1

Dividends

150,000

Dividends Payable

150,000

Mar. 10

No Entry

Mar. 31

Dividends Payable

150,000

Cash

150,000

Closing Entry

Dec. 31

Retained Earnings

150,000

Dividends

150,000

Note: Closing entry is not required in the problem.

11-90

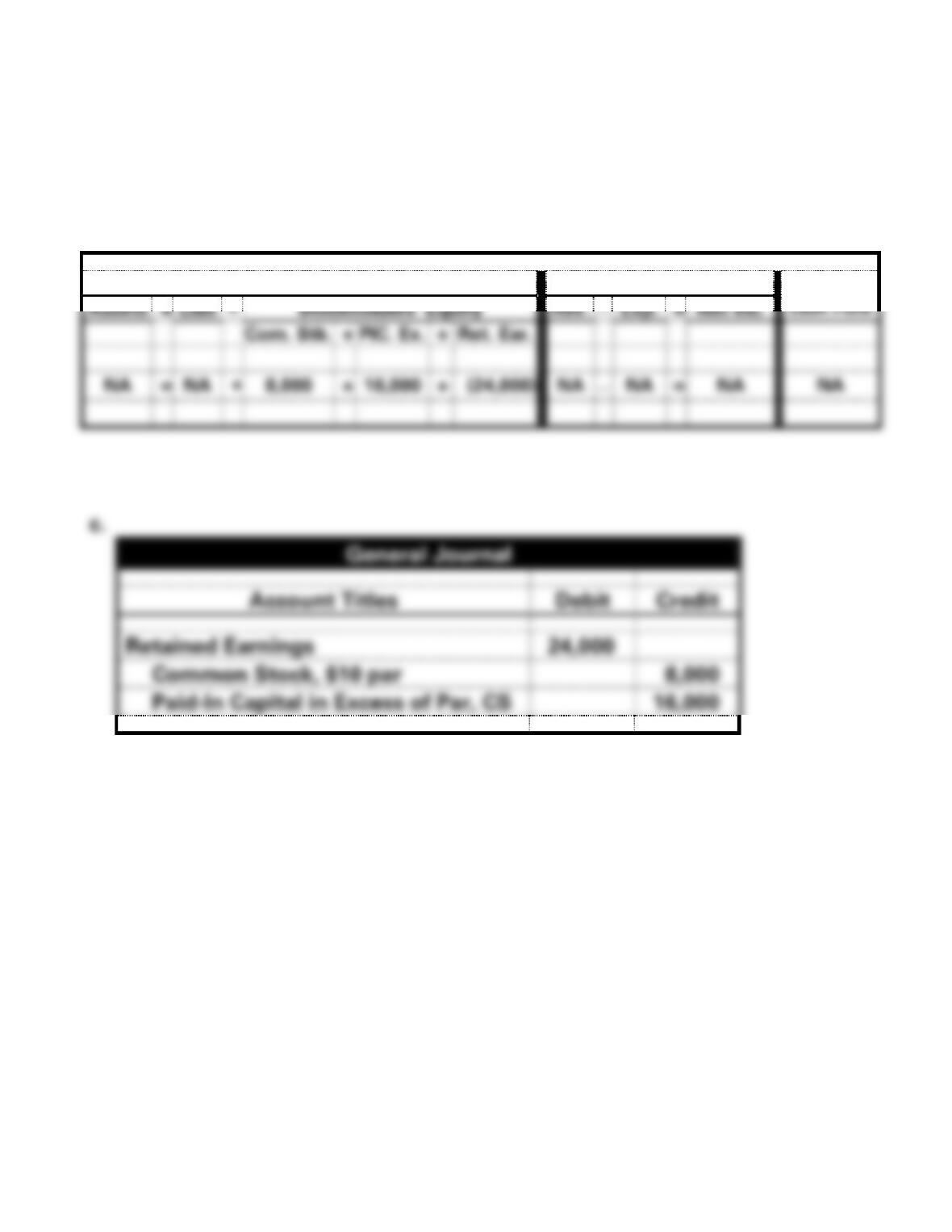

EXERCISE 11-14B

a. (20,000 shares x .04) = 800 shares; 800 shares x $30 = $24,000

b.

Balance Sheet

Income Statement

Stmt. of

Assets

=

Liab

+

Stockholders’ Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

Com. Stk.

+

PIC. Ex.

+

Ret. Ear.

NA

=

NA

+

8,000

+

16,000

+

(24,000)

NA

−

NA

=

NA

NA

c.

General Journal

Account Titles

Debit

Credit

Retained Earnings

24,000

Common Stock, $10 par

8,000

Paid-In Capital in Excess of Par, CS

16,000

11-91

EXERCISE 11-15B

a. No formal entry would be made in the accounting records. A memo

entry would indicate the number of shares had tripled and the par

11-92

EXERCISE 11-16B

TCE should pursue the acquisition of the stock of National Mowers, Inc. A

11-93

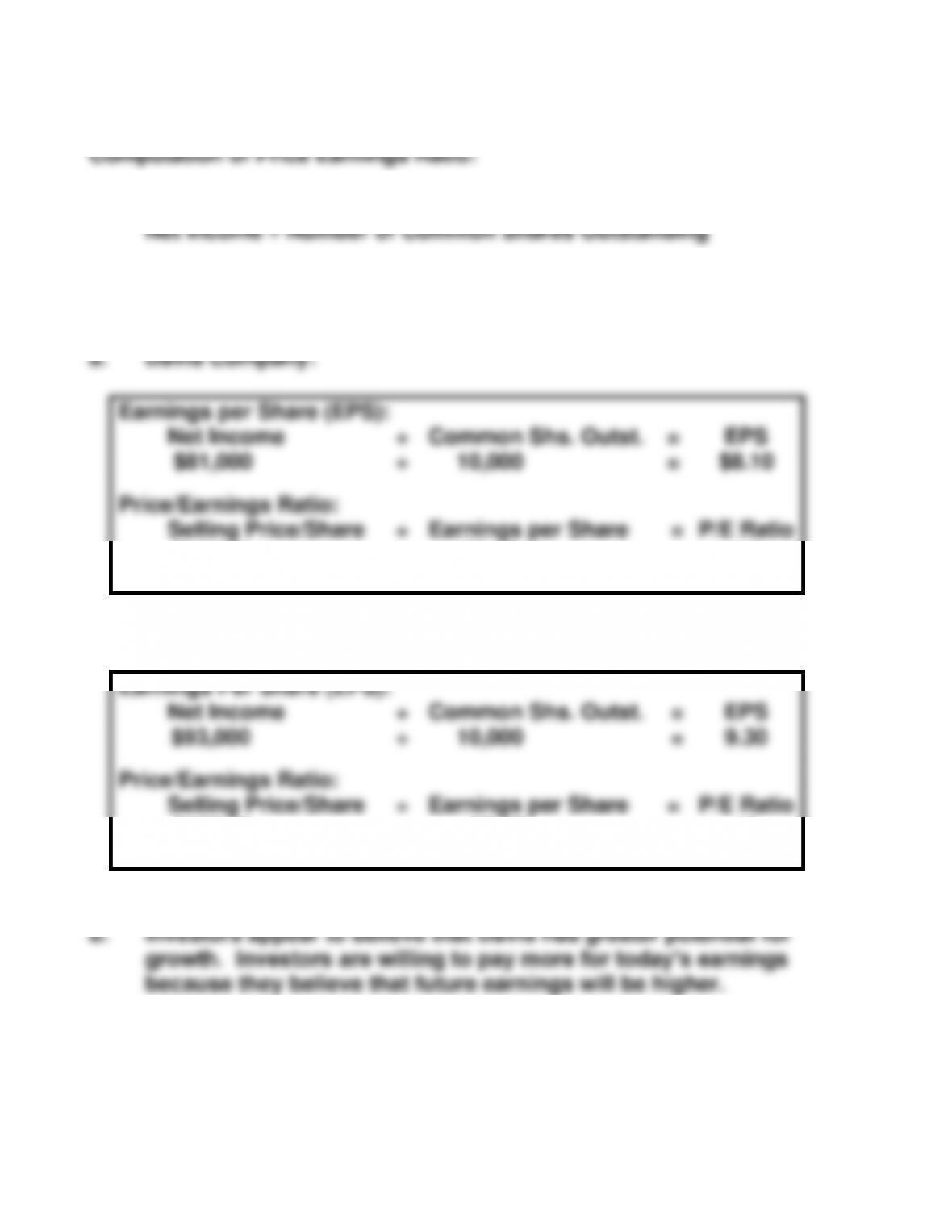

EXERCISE 11-17B

1. Compute Earnings per Share:

2. Compute Price Earnings Ratio:

Selling Price per Share Earnings per Share

Earnings per Share (EPS):

Net Income

÷

Common Shs. Outst.

=

EPS

$81,000

÷

10,000

=

$8.10

Price/Earnings Ratio:

Selling Price/Share

÷

Earnings per Share

=

P/E Ratio

$130.00

÷

$8.10

=

16

Royal Corporation:

Earnings Per Share (EPS):

Net Income

÷

Common Shs. Outst.

=

EPS

$93,000

÷

10,000

=

9.30

Price/Earnings Ratio:

Selling Price/Share

÷

Earnings per Share

=

P/E Ratio

$120.00

÷

$9.30

=

13

11-94

EXERCISE 11-18B

The P/E ratio is computed by dividing market value per share by earnings

PROBLEM 11-19B

Transactions

Cash Acquired from Owners

$120,000

Revenues

80,000

Expenses

56,000

Withdrawals/Distributions

5,000

11-96

PROBLEM 11-19B a. (cont.)

Best Auto Parts Company

Financial Statements

Balance Sheet

As of December 31, 2016

Assets

Cash

$139,000

Total Assets

$139,000

Liabilities

$ -0-

Equity

Smart, Capital

139,000

Total Liabilities and Equity

$139,000

Statement of Cash Flows

For the Year Ended December 31, 2016

Cash Flows From Operating Activities:

Receipts from Revenues

$ 80,000

Paid for Expenses

(56,000)

Net Cash Flow from Operating Activities

$ 24,000

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities:

Proceeds from Owner

$120,000

Paid for Owner Withdrawals

(5,000)

Net Cash Flow from Financing Activities

115,000

Net Change in Cash

139,000

Plus: Beginning Cash Balance

-0-

Ending Cash Balance

$139,000