11–60

PROBLEM 11-22A (cont.)

c.

Brice Company

December 31, 2016

Stockholders’ Equity

Preferred Stock, $20 par value, 6%, 8,000

shares issued and outstanding

$160,000

Common Stock, no par value, 88,000 shares

issued and outstanding

448,000

Total Paid-In Capital

$608,000

Retained Earnings

10,400

Total Stockholders’ Equity

$618,400

factors.

11–61

PROBLEM 11-23A

a.

Sun Corporation

General Journal

Date

Account Titles

Debit

Credit

2016

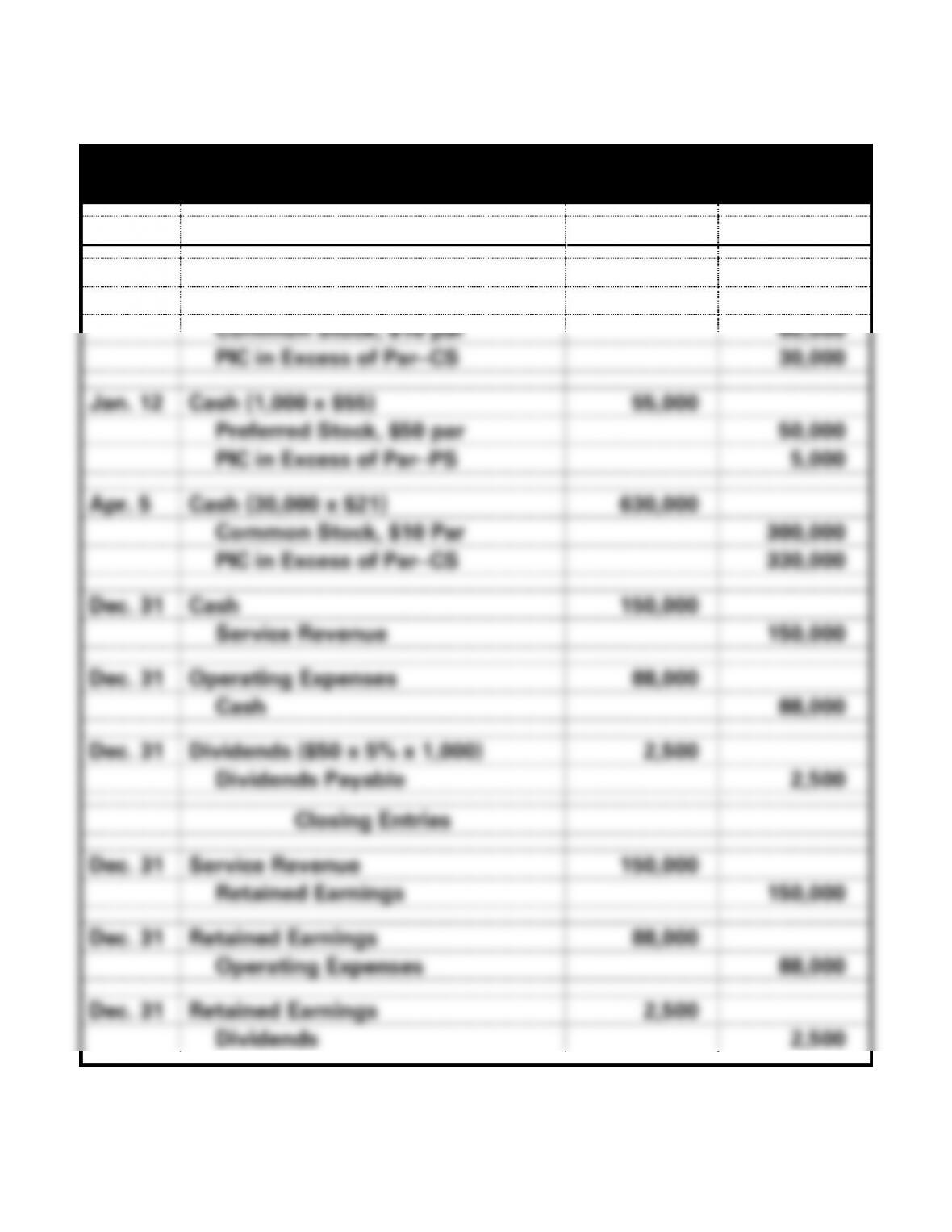

Jan. 5

Cash (6,000 x $15)

90,000

Common Stock, $10 par

60,000

PIC in Excess of Par−CS

30,000

Jan. 12

Cash (1,000 x $55)

55,000

Preferred Stock, $50 par

50,000

PIC in Excess of Par−PS

5,000

Apr. 5

Cash (30,000 x $21)

630,000

Common Stock, $10 Par

300,000

PIC in Excess of Par−CS

330,000

Dec. 31

Cash

150,000

Service Revenue

150,000

Dec. 31

Operating Expenses

88,000

Cash

88,000

Dec. 31

Dividends ($50 x 5% x 1,000)

2,500

Dividends Payable

2,500

Closing Entries

Dec. 31

Service Revenue

150,000

Retained Earnings

150,000

Dec. 31

Retained Earnings

88,000

Operating Expenses

88,000

Dec. 31

Retained Earnings

2,500

Dividends

2,500

11–62

PROBLEM 11-23A a. (cont.)

Sun Corporation

General Journal

Date

Account Titles

Debit

Credit

2017

Feb. 15

Dividends Payable

2,500

Cash

2,500

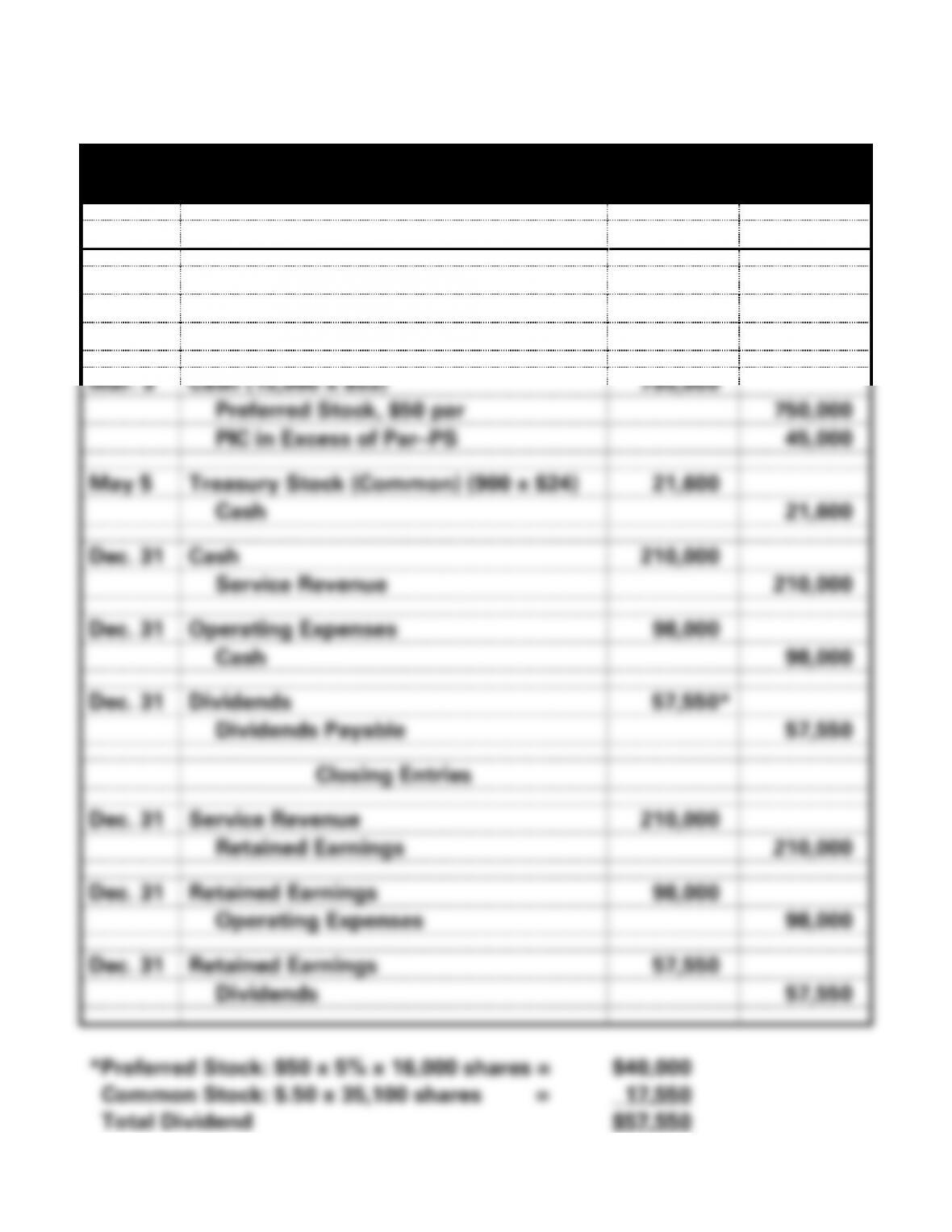

Mar. 3

Cash (15,000 x $53)

795,000

Preferred Stock, $50 par

750,000

PIC in Excess of Par−PS

45,000

May 5

Treasury Stock (Common) (900 x $24)

21,600

Cash

21,600

Dec. 31

Cash

210,000

Service Revenue

210,000

Dec. 31

Operating Expenses

98,000

Cash

98,000

Dec. 31

Dividends

57,550*

Dividends Payable

57,550

Closing Entries

Dec. 31

Service Revenue

210,000

Retained Earnings

210,000

Dec. 31

Retained Earnings

98,000

Operating Expenses

98,000

Dec. 31

Retained Earnings

57,550

Dividends

57,550

11–63

PROBLEM 11-23A a. (cont.)

Sun Corporation T-Accounts for 2016

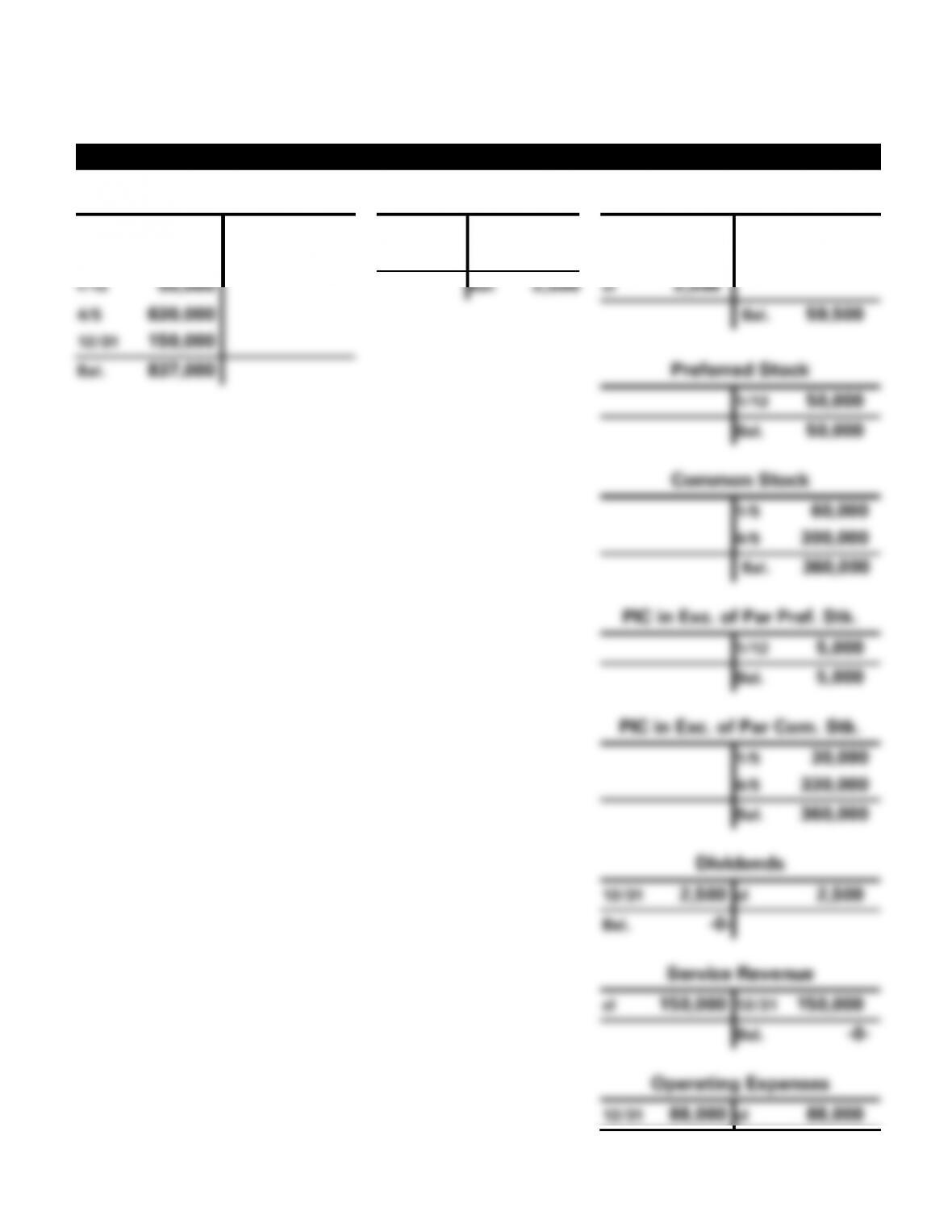

Cash

Dividends Payable

Retained Earnings

2016

2016

2016

1/5 90,000

12/31 88,000

12/31 2,500

cl 88,000

cl 150,000

1/12 55,000

Bal. 2,500

cl 2,500

4/5 630,000

Bal. 59,500

12/31 150,000

Bal. 837,000

Preferred Stock

1/12 50,000

Bal. 50,000

Common Stock

1/5 60,000

4/5 300,000

Bal. 360,000

PIC in Exc. of Par Pref. Stk.

1/12 5,000

Bal. 5,000

PIC in Exc. of Par Com. Stk.

1/5 30,000

4/5 330,000

Bal. 360,000

Dividends

12/31 2,500

cl 2,500

Bal. -0-

Service Revenue

cl 150,000

12/31 150,000

Bal. -0-

Operating Expenses

12/31 88,000

cl 88,000

11–64

Bal. -0-

11–65

PROBLEM 11-23A a. (cont.)

Sun Corporation T-Accounts for 2017

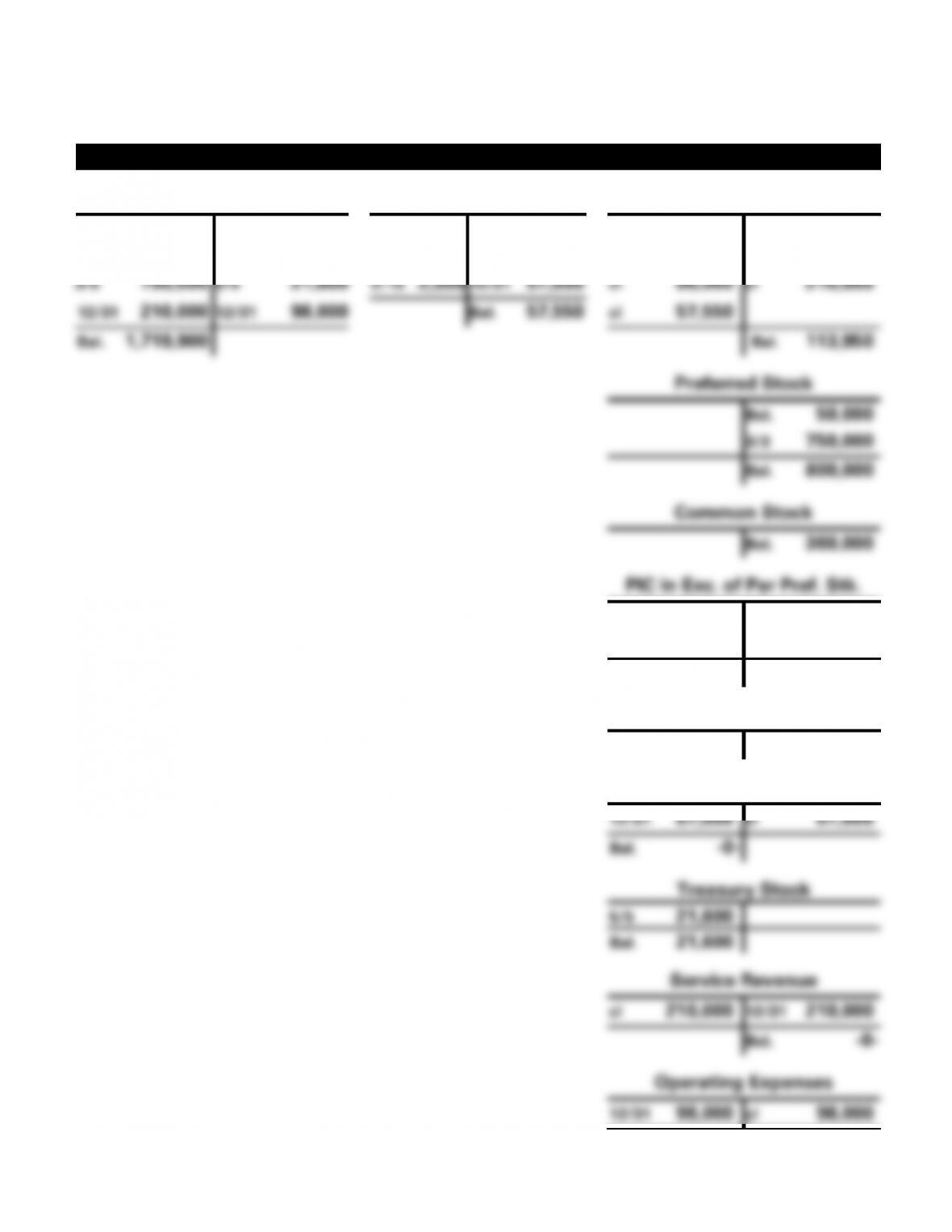

Cash

Dividends Payable

Retained Earnings

2017

2017

2017

Bal. 837,000

2/15 2,500

Bal. 2,500

Bal. 59,500

3/3 795,000

5/5 21,600

2/15 2,500

12/31 57,550

cl 98,000

cl 210,000

12/31 210,000

12/31 98,000

Bal. 57,550

cl 57,550

Bal. 1,719,900

Bal. 113,950

Preferred Stock

Bal. 50,000

3/3 750,000

Bal. 800,000

Common Stock

Bal. 360,000

PIC in Exc. of Par Pref. Stk.

Bal. 5,000

3/3 45,000

Bal. 50,000

PIC in Exc. of Par Com. Stk.

Bal. 360,000

Dividends

12/31 57,550

cl 57,550

Bal. -0-

Treasury Stock

5/5 21,600

Bal. 21,600

Service Revenue

cl 210,000

12/31 210,000

Bal. -0-

Operating Expenses

12/31 98,000

cl 98,000

11–66

Bal. -0-

11–67

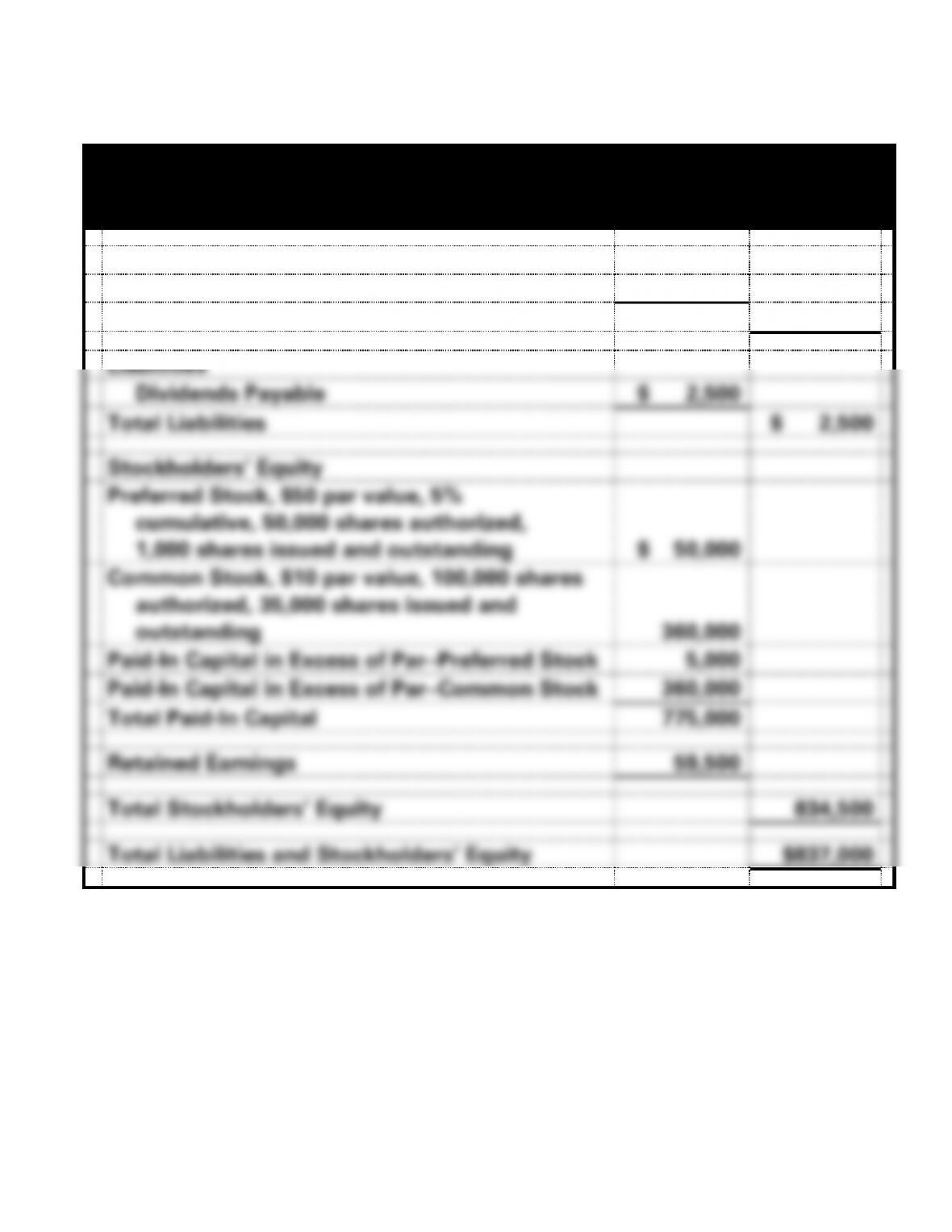

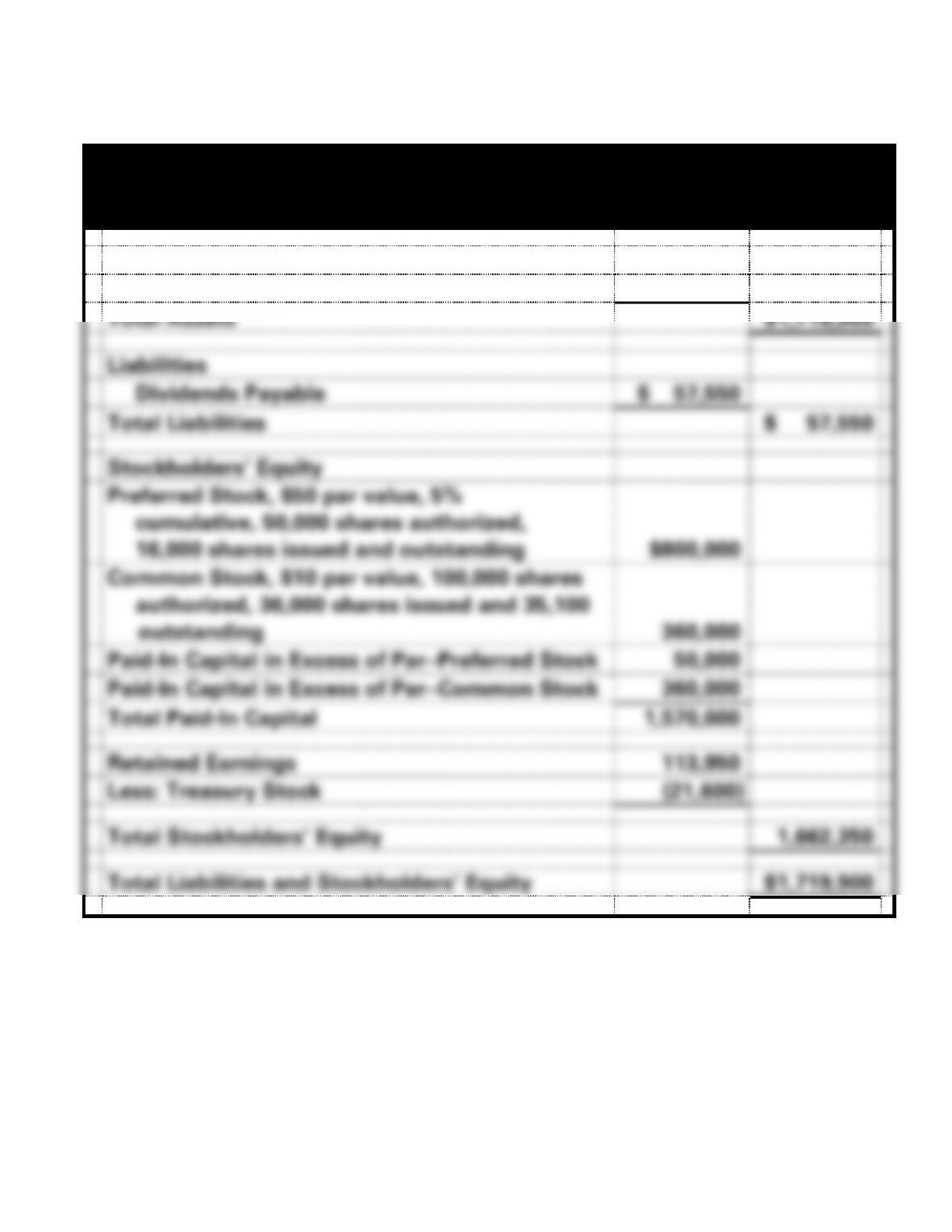

PROBLEM 11-23A (cont.)

b.

Sun Corporation

Balance Sheet

As of December 31, 2016

Assets

Cash

$837,000

Total Assets

$837,000

Liabilities

Dividends Payable

$ 2,500

Total Liabilities

$ 2,500

Stockholders’ Equity

Preferred Stock, $50 par value, 5%

cumulative, 50,000 shares authorized,

1,000 shares issued and outstanding

$ 50,000

Common Stock, $10 par value, 100,000 shares

authorized, 35,000 shares issued and

outstanding

360,000

Paid-In Capital in Excess of Par−Preferred Stock

5,000

Paid-In Capital in Excess of Par−Common Stock

360,000

Total Paid-In Capital

775,000

Retained Earnings

59,500

Total Stockholders’ Equity

834,500

Total Liabilities and Stockholders’ Equity

$837,000

11–68

PROBLEM 11-23A (cont.)

b.

Sun Corporation

Balance Sheet

As of December 31, 2017

Assets

Cash

$1,719,900

Total Assets

$1,719,900

Liabilities

Dividends Payable

$ 57,550

Total Liabilities

$ 57,550

Stockholders’ Equity

Preferred Stock, $50 par value, 5%

cumulative, 50,000 shares authorized,

16,000 shares issued and outstanding

$800,000

Common Stock, $10 par value, 100,000 shares

authorized, 36,000 shares issued and 35,100

outstanding

360,000

Paid-In Capital in Excess of Par−Preferred Stock

50,000

Paid-In Capital in Excess of Par−Common Stock

360,000

Total Paid-In Capital

1,570,000

Retained Earnings

113,950

Less: Treasury Stock

(21,600)

Total Stockholders’ Equity

1,662,350

Total Liabilities and Stockholders’ Equity

$1,719,900

11–69

PROBLEM 11-23A (cont.)

c.

Schedule of Number of

Shares of Common Stock

Shares

Issued

Shares

Outstanding

2016

Jan. 5

6,000

6,000

Apr. 5

30,000

30,000

Totals

36000

36,000

2017

May 5

(900)

Totals

36,000

35,100

Shares issued and outstanding are the same for 2016. However, for 2017,

the 900 shares of treasury stock reduce the number of outstanding shares.

In 2017, there are 36,000 shares issued but only 35,100 outstanding.

11–70

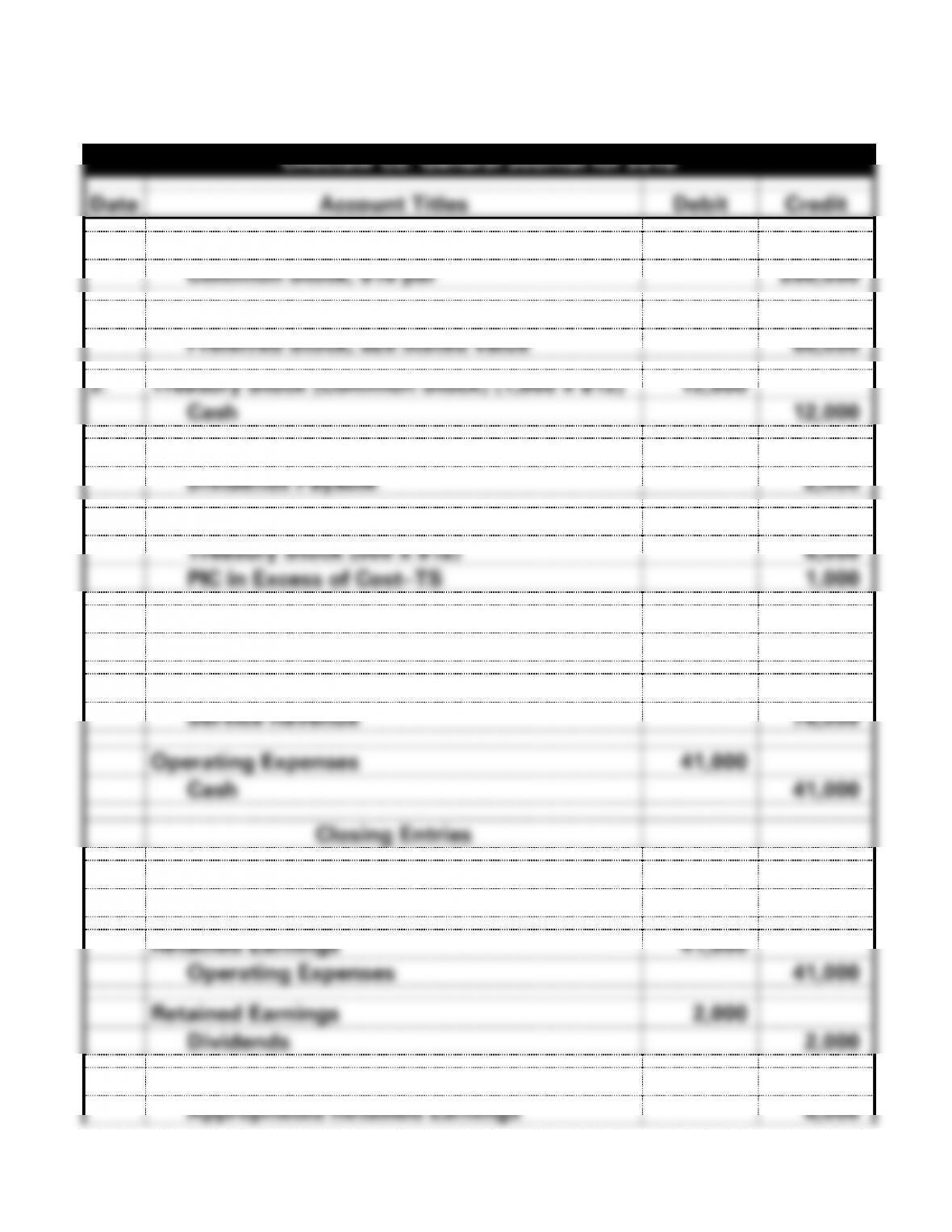

PROBLEM 11-24A

a.

Choctaw Co. General Journal for 2016

Date

Account Titles

Debit

Credit

1.

Cash (20,000 x $10)

200,000

Common Stock, $10 par

200,000

2.

Cash (3,000 x $20)

60,000

Preferred Stock, $20 stated value

60,000

3.

Treasury Stock (Common Stock) (1,000 x $12)

12,000

Cash

12,000

4.

Dividends

2,000

Dividends Payable

2,000

5.

Cash (500 x $14)

7,000

Treasury Stock (500 x $12)

6,000

PIC in Excess of Cost−TS

1,000

6.

Dividends Payable

2,000

Cash

2,000

7.

Cash

78,000

Service Revenue

78,000

Operating Expenses

41,000

Cash

41,000

Closing Entries

8.

Service Revenue

78,000

Retained Earnings

78,000

Retained Earnings

41,000

Operating Expenses

41,000

Retained Earnings

2,000

Dividends

2,000

9.

Retained Earnings

8,000

Appropriated Retained Earnings

8,000

11–71

11–72

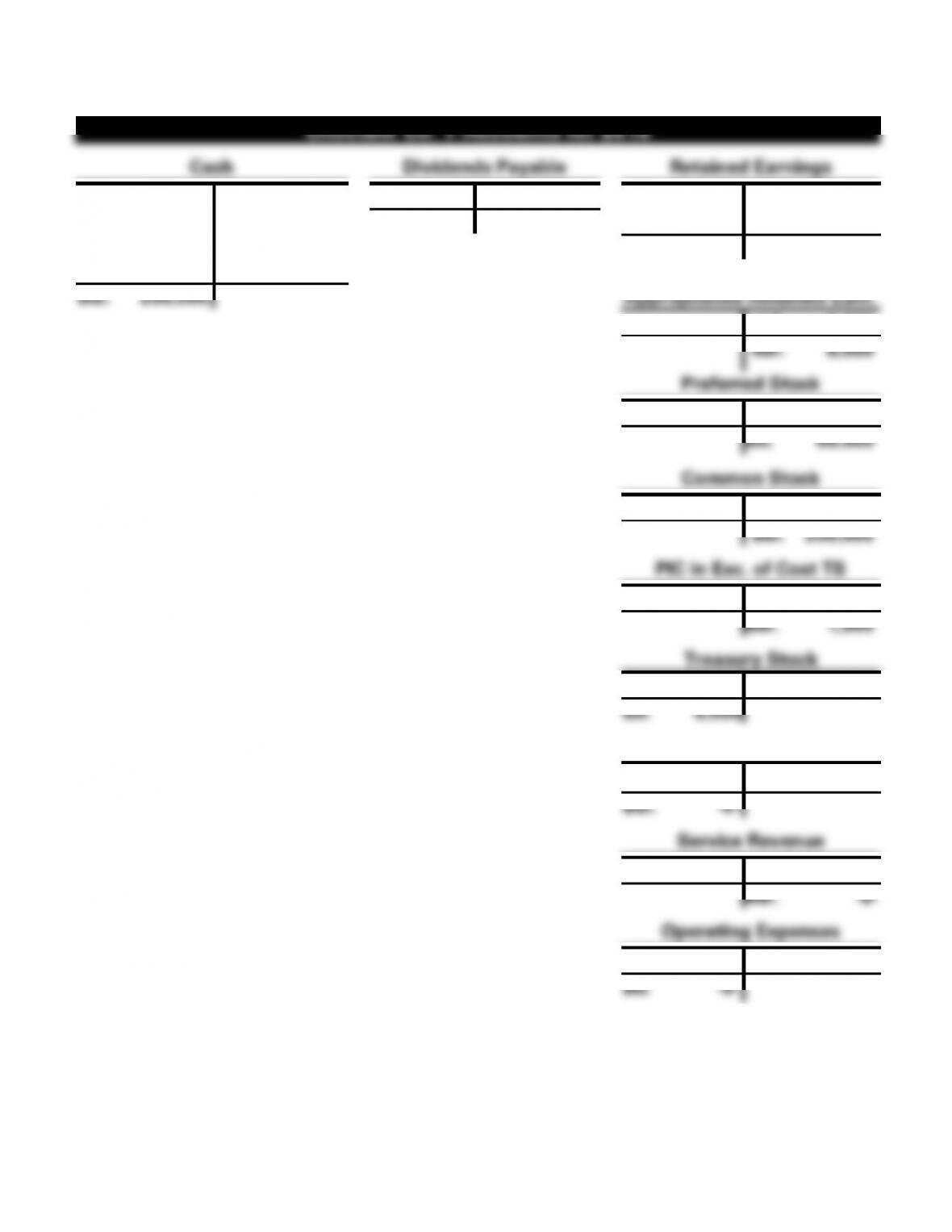

PROBLEM 11-24A a. (cont.)

Choctaw Co. T-Accounts for 2016

Cash

Dividends Payable

Retained Earnings

1. 200,000

3. 12,000

6. 2,000

4. 2,000

cl 8. 43,000

cl 8 78,000

2. 60,000

6. 2,000

Bal. -0-

cl 9. 8,000

5. 7,000

7. 41,000

Bal. 27,000

7. 78,000

Bal. 290,000

Appropriated Retained Earn.

cl 9. 8,000

Bal. 8,000

Preferred Stock

2. 60,000

Bal. 60,000

Common Stock

1. 200,000

Bal. 200,000

PIC in Exc. of Cost TS

5. 1,000

Bal. 1,000

Treasury Stock

3. 12,000

5. 6,000

Bal. 6,000

Dividends

4. 2,000

cl 8. 2,000

Bal. -0-

Service Revenue

cl 8. 78,000

7. 78,000

Bal. -0-

Operating Expenses

7. 41,000

cl 8. 41,000

Bal. -0-

11–73

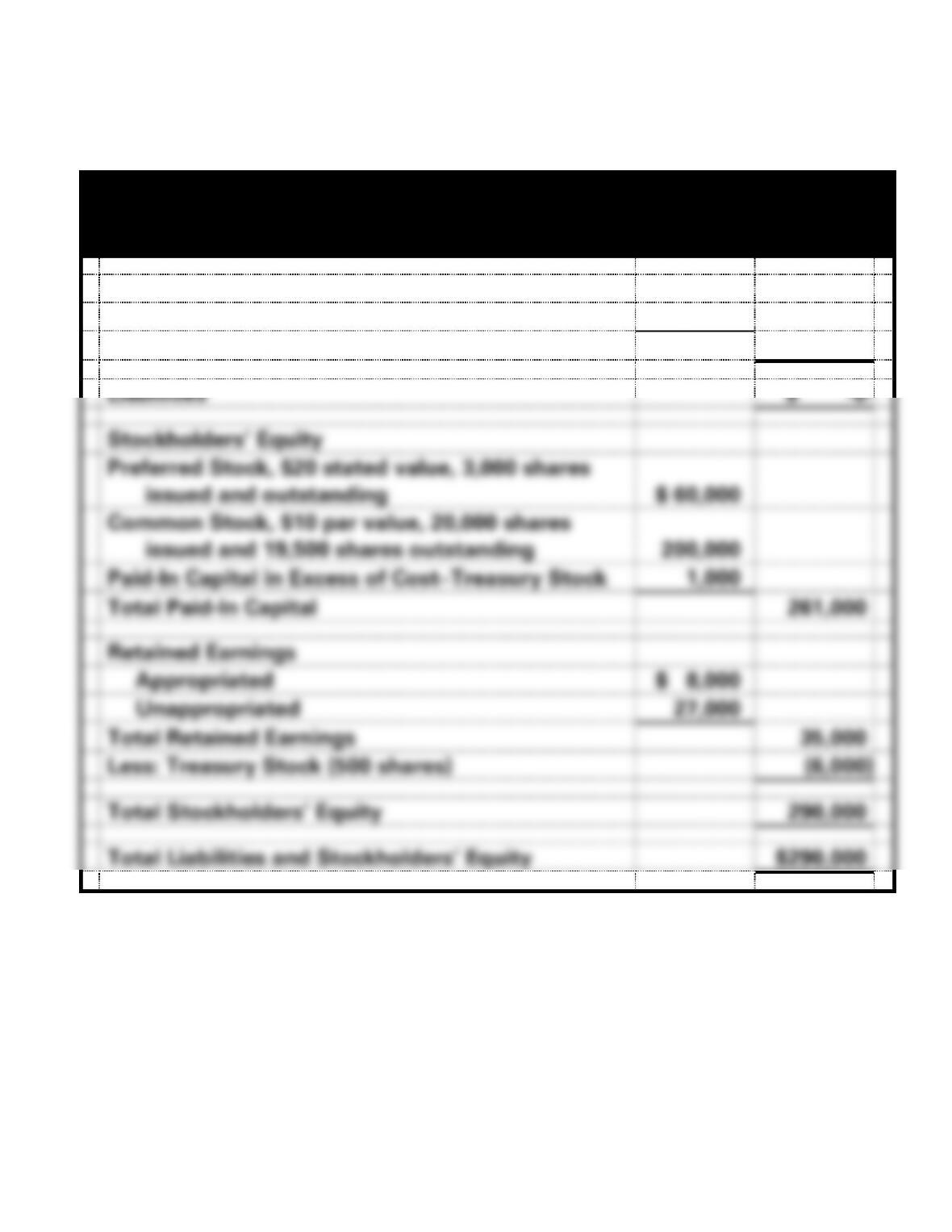

PROBLEM 11-24A (cont.)

b.

Choctaw Co.

Balance Sheet

As of December 31, 2016

Assets

Cash

$290,000

Total Assets

$290,000

Liabilities

$ -0-

Stockholders’ Equity

Preferred Stock, $20 stated value, 3,000 shares

issued and outstanding

$ 60,000

Common Stock, $10 par value, 20,000 shares

issued and 19,500 shares outstanding

200,000

Paid-In Capital in Excess of Cost−Treasury Stock

1,000

Total Paid-In Capital

261,000

Retained Earnings

Appropriated

$ 8,000

Unappropriated

27,000

Total Retained Earnings

35,000

Less: Treasury Stock (500 shares)

(6,000)

Total Stockholders’ Equity

290,000

Total Liabilities and Stockholders’ Equity

$290,000

11-104

PROBLEM 11-25A

a. $200,000 10,000 shares = $20 per share

b. $20 par value per share x 6% = $1.20 per share

c. $1,000,000 + $500,000 = $1,500,000;

e. 1. 100,000 x 2 = 200,000 shares outstanding after the split.

2. No amount will be transferred from retained earnings.

3. Theoretically, the market price will be $21 ($42 2).

11-105

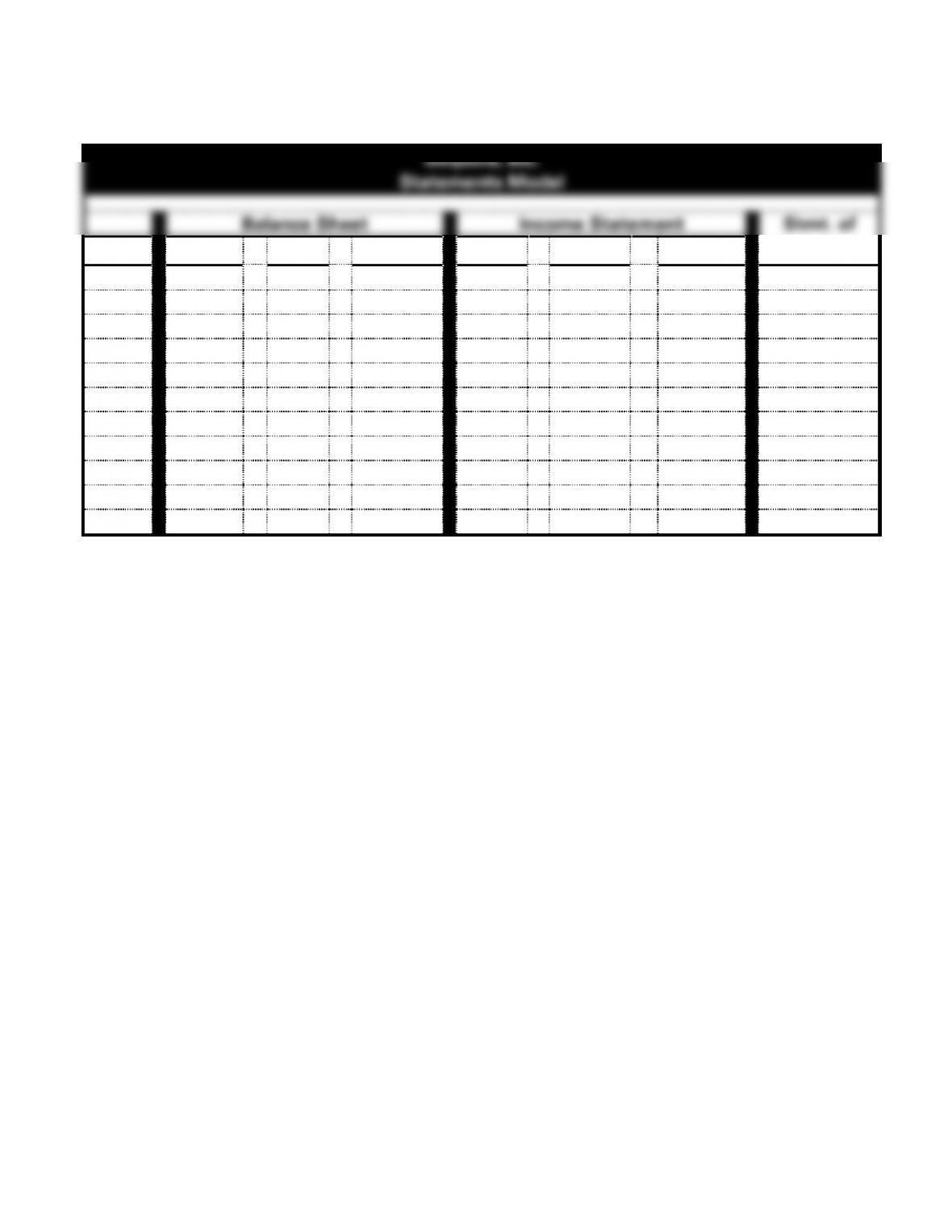

PROBLEM 11-26A

Sequoia, Inc.

Statements Model

Balance Sheet

Income Statement

Stmt. of

Event

Assets

=

Liab.

+

S. Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

1.

+

NA

+

NA

NA

NA

+ FA

2.

+

NA

+

NA

NA

NA

+ FA

3.

+

NA

+

NA

NA

NA

+ FA

4.

−

NA

−

NA

NA

NA

− FA

5.

+

NA

+

NA

NA

NA

+ FA

6.

NA

+

−

NA

NA

NA

NA

7.

NA

NA

NA

NA

NA

NA

NA

8.

NA

NA

+−

NA

NA

NA

NA

9.

NA

NA

+−

NA

NA

NA

NA

10.

−

−

NA

NA

NA

NA

− FA