5-6

ANSWERS TO QUESTIONS – CHAPTER 5

1. (1.) Specific Identification – The inventory cost flow method that

(2.) First In, First Out – The inventory cost flow method that assumes

that the first items purchased are the first items sold for the

purpose of computing cost of goods sold and inventory.

2. One advantage of the specific identification method is that both the

inventory account and cost of goods sold reflect the actual amounts on

3. FIFO allocates the cost of the first units purchased to the first units

sold; consequently, in a period of rising prices, this would produce a

turnover.

4. LIFO allocates the cost of the last units purchased to the first units sold;

consequently, in a period of rising prices, this would produce a lower

5-7

5. In an inflationary period, i.e., a period where prices are consistently

rising, FIFO will produce the highest amount of income. This is true

6. In an inflationary period, FIFO will produce the largest amount of total

assets. (Refer to the discussion for Question 5.) The unsold items,

7. Flow of costs refers to the assumption that is made for the purpose of

determining the cost of inventory items that are sold when preparing

financial statements. The cost flow assumption that a business makes

8. In a world where there is no income tax, the choice of cost flow

method would not affect the statement of cash flows because it is

simply allocating some of the cost of inventory purchased to expense

5-8

9. Key Company (first year of operations):

Beginning inventory $ -0–

Merchandise purchased 1,000 units @ $25 25,000

10. The amount of cost of goods sold for Key Company will be different

using different cost flow assumptions because the units purchased

during the second year have a different cost than those purchased the

previous year.

11. Since the prices of the inventory are increasing, it may be

advantageous to use FIFO for financial statement purposes because it

5-9

consequently the net income and income tax paid will be lower. Since

method.

12. In an inflationary period, for a business subject to income tax, LIFO

13. A deflationary period, i.e., a period of falling prices, would produce

results opposite of those for an inflationary period. FIFO would

14. “Lower of cost or market” is an accounting convention that helps to

reduce overstating inventory (assets) when the market value of certain

15. For merchandise that has declined in value, the “lower-of–cost-or–

16. In certain situations it is not possible or practical to take a complete

inventory. One such situation is when the inventory or part of it has

been destroyed by some disaster or similar event. Another situation

17. It is generally easier to manipulate net income when a periodic

5-10

The only measurement available is the amount of inventory still on

hand. There is no control over the amount that was sold, damaged, or

stolen. In addition, if the inventory is counted wrong or priced wrong,

19. When using the periodic method, ending inventory that is overstated

at the end of 2016, but is corrected at the end of 2017 will result in the

following:

2016 Income Statement:

20. The inventory turnover tells the user how many times on average

21. Discount merchandisers such as Walmart and Kmart should have a

5-11

EXERCISE 5-1A

a. LIFO

c. FIFO

d. LIFO

e. FIFO

5-12

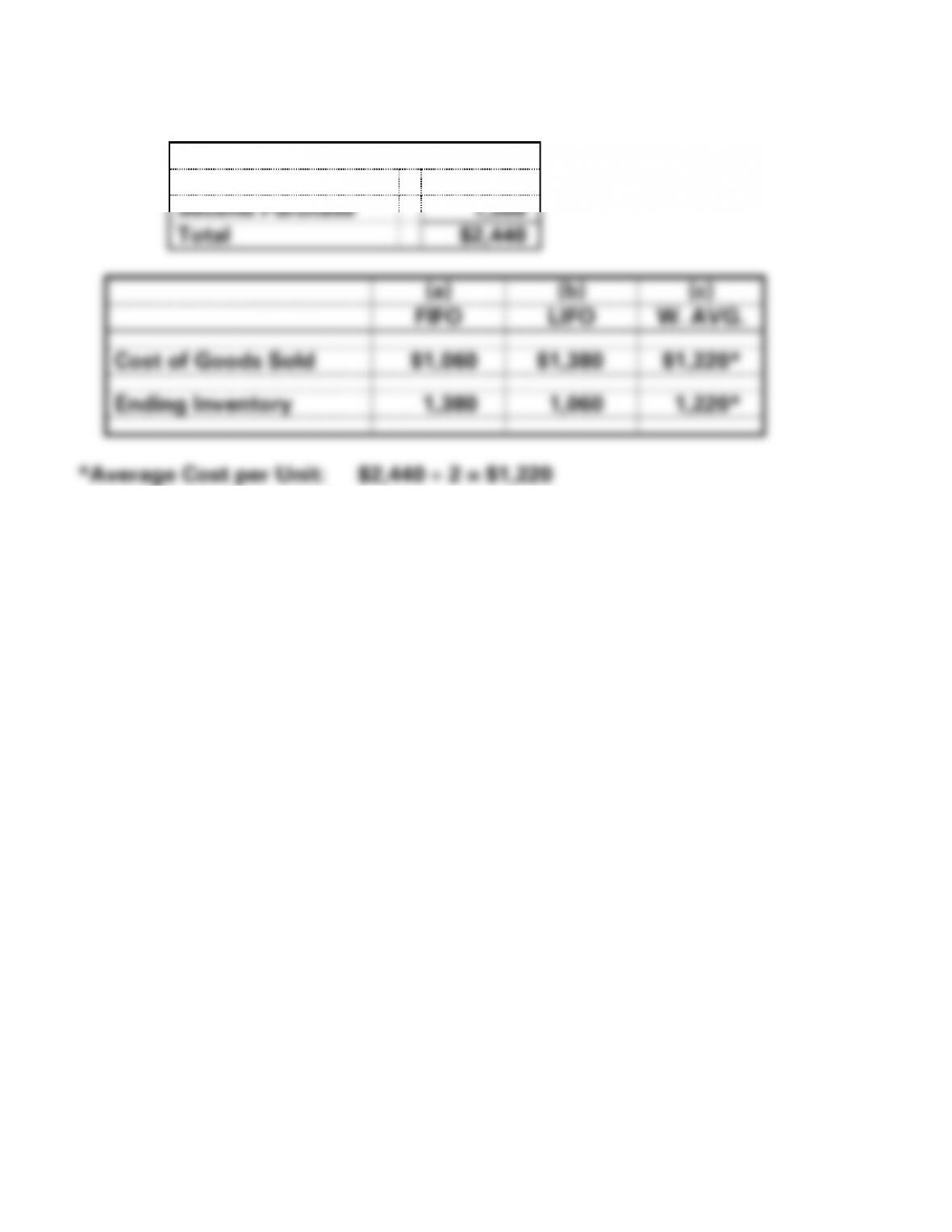

EXERCISE 5-2A

Jones Co.

First Purchase

$1,060

Second Purchase

1,380

Total

$2,440

(a)

(b)

(c)

FIFO

LIFO

W. AVG.

Cost of Goods Sold

$1,060

$1,380

$1,220*

Ending Inventory

1,380

1,060

1,220*

*Average Cost per Unit: $2,440 2 = $1,220

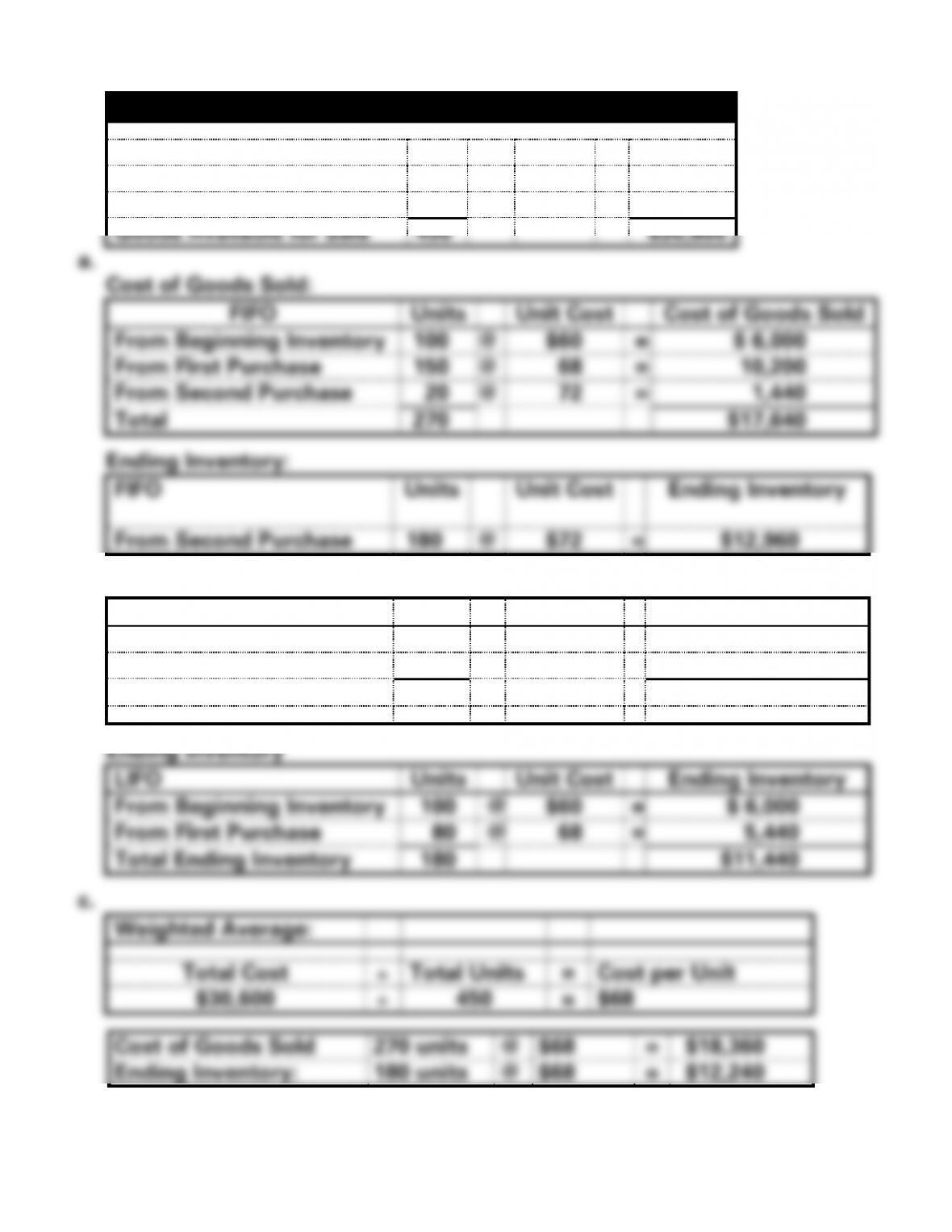

EXERCISE 5-3A

The Cortez Company Inventory Purchases

Beginning Inventory

100

@

$60

=

$ 6,000

First Purchase

150

@

68

=

10,200

Second Purchase

200

@

72

=

14,400

Goods Available for Sale

450

$30,600

a.

Cost of Goods Sold:

FIFO

Units

Unit Cost

Cost of Goods Sold

From Beginning Inventory

100

@

$60

=

$ 6,000

From First Purchase

150

@

68

=

10,200

From Second Purchase

20

@

72

=

1,440

Total

270

$17,640

From Second Purchase

180

=

Units

Unit Cost

Cost of Goods Sold

=

$14,400

@

68

=

$19,160

Units

Unit Cost

@

$60

=

@

68

=

Total Units

=

Cost per Unit

=

5-14

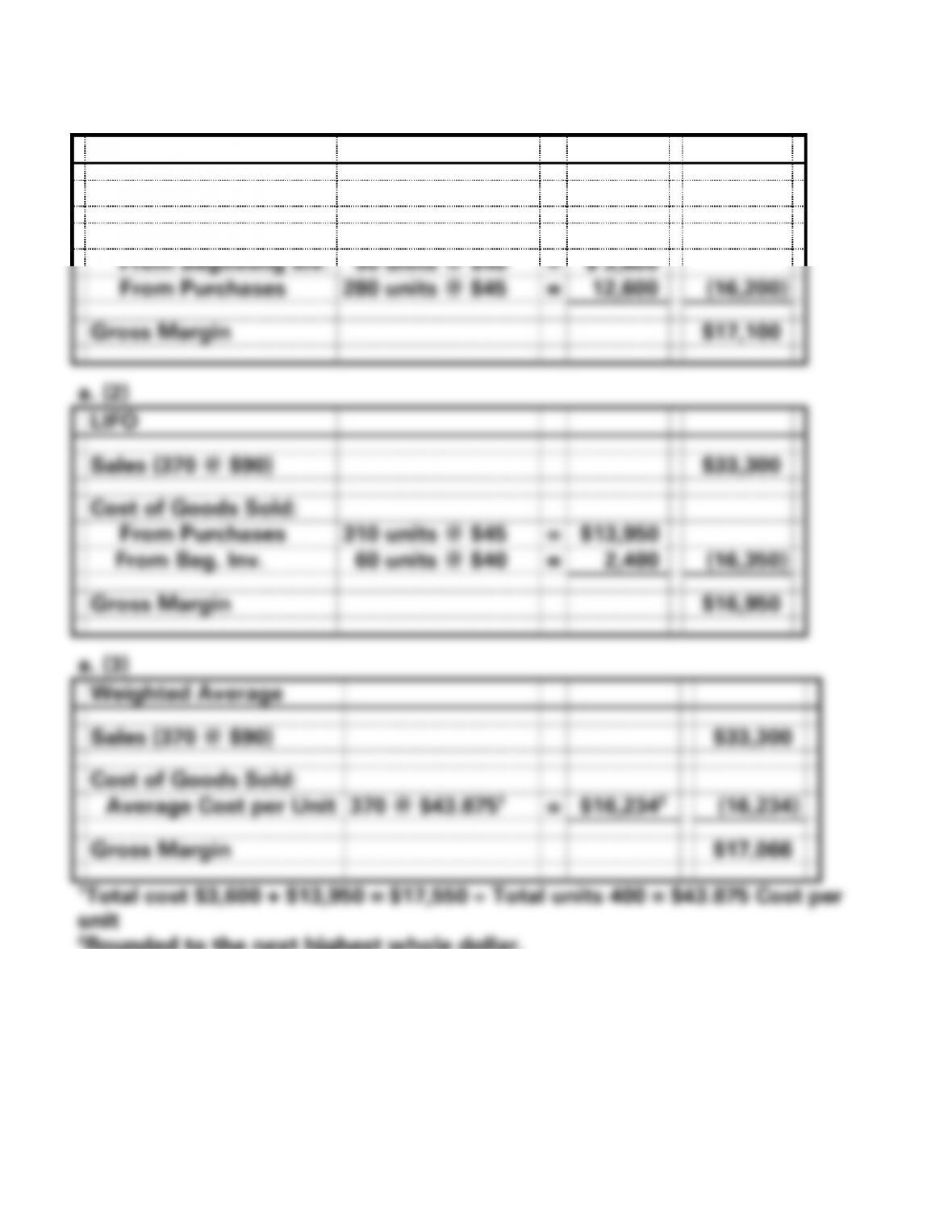

EXERCISE 5-4A

a. (1) Mason Company

FIFO

Sales (370 @ $90)

$33,300

Cost of Goods Sold:

From Beginning Inv.

90 units @ $40

=

$ 3,600

From Purchases

280 units @ $45

=

12,600

(16,200)

Gross Margin

$17,100

LIFO

Sales (370 @ $90)

$33,300

Cost of Goods Sold:

From Purchases

310 units @ $45

=

$13,950

From Beg. Inv.

60 units @ $40

=

2,400

(16,350)

Gross Margin

$16,950

Weighted Average

Sales (370 @ $90)

$33,300

Cost of Goods Sold:

Average Cost per Unit

370 @ $43.8751

=

$16,2342

(16,234)

Gross Margin

$17,066

5-15

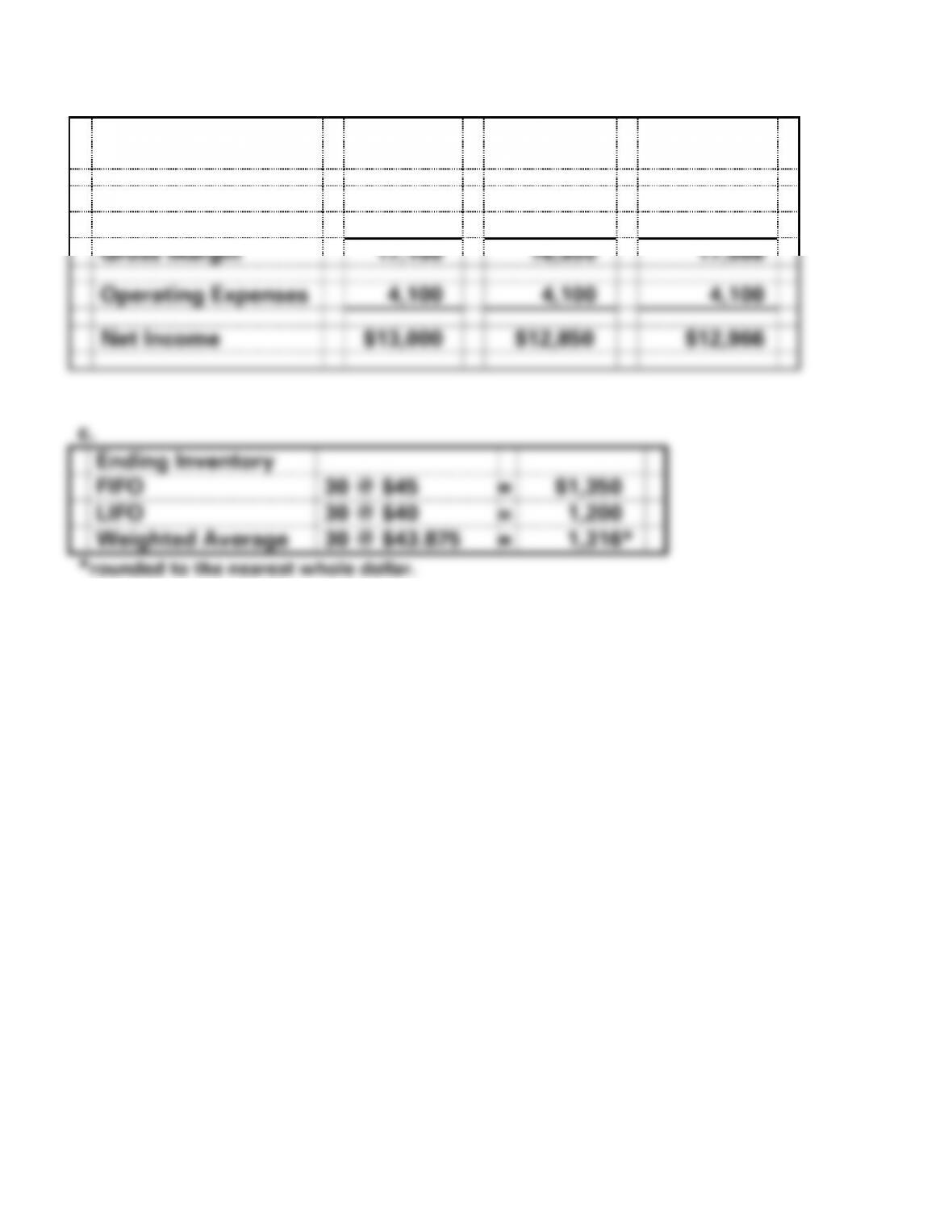

EXERCISE 5-4A (cont.)

b.

FIFO

LIFO

Weighted

Avg.

Sales

$33,300

$33,300

$33,300

Cost of Goods Sold

(16,200)

(16,350)

(16,234)

Gross Margin

17,100

16,950

17,066

Operating Expenses

4,100

4,100

4,100

Net Income

$13,000

$12,850

$12,966

c.

Ending Inventory

FIFO

30 @ $45

=

$1,350

LIFO

30 @ $40

=

1,200

Weighted Average

30 @ $43.875

=

1,316*

5-16

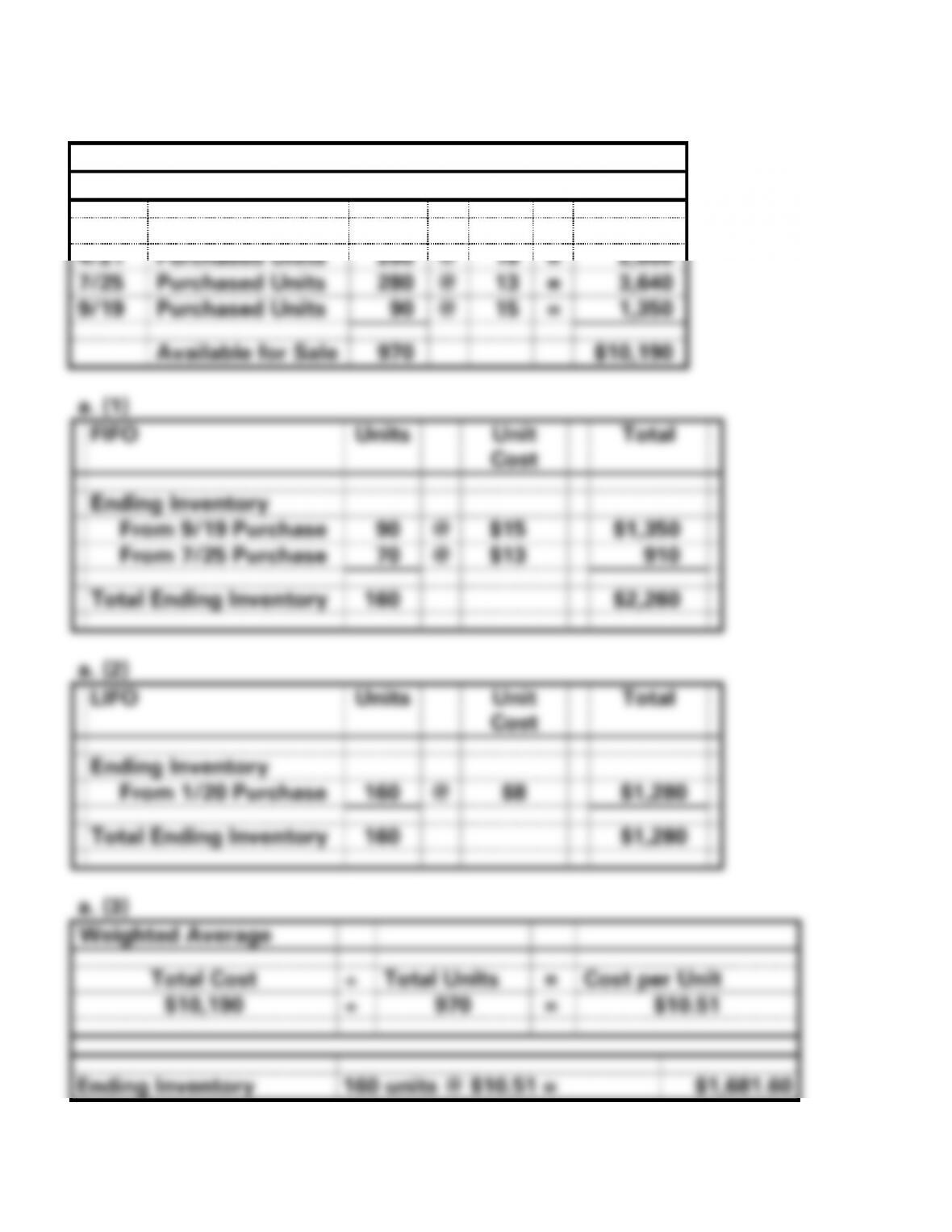

EXERCISE 5-5A

The Shirt Shop

Summary of Purchase Transactions

1/20

Purchased Units

400

@

$8

=

$3,200

4/21

Purchased Units

200

@

10

=

2,000

7/25

Purchased Units

280

@

13

=

3,640

9/19

Purchased Units

90

@

15

=

1,350

Available for Sale

970

$10,190

a. (1)

FIFO

Units

Unit

Cost

Total

Ending Inventory

From 9/19 Purchase

90

@

$15

$1,350

From 7/25 Purchase

70

@

$13

910

Total Ending Inventory

160

$2,260

a. (2)

LIFO

Units

Unit

Cost

Total

Ending Inventory

From 1/20 Purchase

160

@

$8

$1,280

Total Ending Inventory

160

$1,280

a. (3)

Weighted Average

Total Cost

Total Units

=

Cost per Unit

$10,190

970

=

$10.51

Ending Inventory

160 units @ $10.51 =

$1,681.60

*rounded

5-17

EXERCISE 5-5A (cont.)

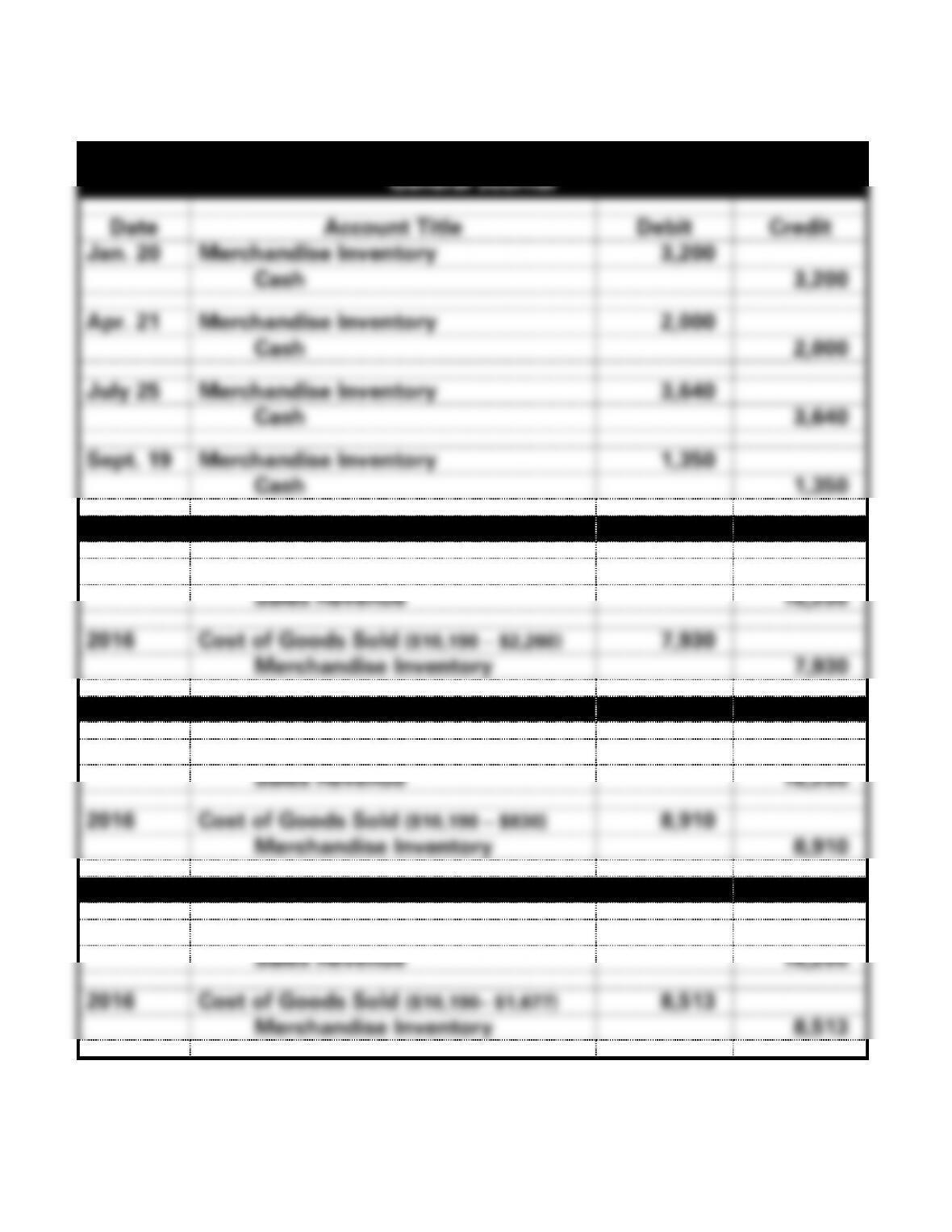

b.

Note: The purchase entries are the same for all three methods.

The Shirt Shop

General Journal

Date

Account Title

Debit

Credit

Jan. 20

Merchandise Inventory

3,200

Cash

3,200

Apr. 21

Merchandise Inventory

2,000

Cash

2,000

July 25

Merchandise Inventory

3,640

Cash

3,640

Sept. 19

Merchandise Inventory

1,350

Cash

1,350

(1) FIFO Sales and Cost of Goods Sold

2016

Cash (810 x $20)

16,200

Sales Revenue

16,200

2016

Cost of Goods Sold ($10,190 − $2,260)

7,930

Merchandise Inventory

7,930

(2) LIFO Sales and Cost of Goods Sold

2016

Cash

16,200

Sales Revenue

16,200

2016

Cost of Goods Sold ($10,190 − $830)

8,910

Merchandise Inventory

8,910

(3) Weighted Average Sales and Cost of Goods Sold

2016

Cash

16,200

Sales Revenue

16,200

2016

Cost of Goods Sold ($10,190− $1,677)

8,513

Merchandise Inventory

8,513

5-18

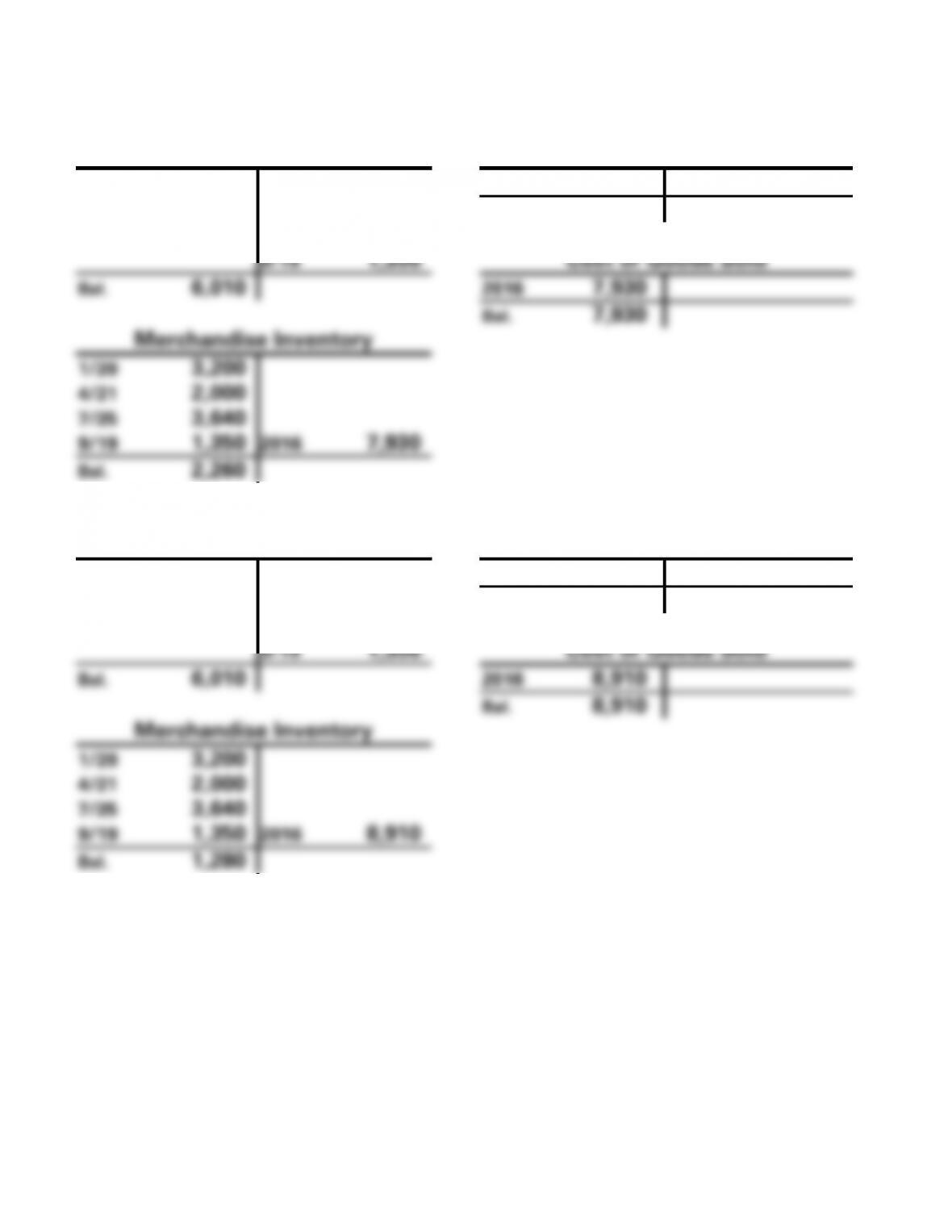

EXERCISE 5-5A b. (cont.)

(1) FIFO

Cash

Sales Revenue

2016 16,200

1/20 3,200

2016 16,200

4/21 2,000

Bal. 16,200

7/25 3,640

9/19 1,350

Cost of Goods Sold

Bal. 6,010

2016 7,930

Bal. 7,930

Merchandise Inventory

1/20 3,200

4/21 2,000

7/25 3,640

9/19 1,350

2016 7,930

Bal. 2,260

(2) LIFO

Cash

Sales Revenue

2016 16,200

1/20 3,200

2016 16,200

4/21 2,000

Bal. 16,200

7/25 3,640

9/19 1,350

Cost of Goods Sold

Bal. 6,010

2016 8,910

Bal. 8,910

Merchandise Inventory

1/20 3,200

4/21 2,000

7/25 3,640

9/19 1,350

2016 8,910

Bal. 1,280

5-19

EXERCISE 5-5A b. (cont.)

(3) Weighted Average

Cash

Sales Revenue

2016 16,200

1/20 3,200

2016 16,200

4/21 2,000

Bal. 16,200

7/25 3,640

9/19 1,350

Cost of Goods Sold

Bal. 6,010

2016 8,513

Bal. 8,513

Merchandise Inventory

1/20 3,200

4/21 2,000

7/25 3,640

9/19 1,350

2016 8,513

Bal. 1,677

5-20

EXERCISE 5-5A (cont.)

c.

FIFO

Sales (810 units @ $20)

$16,200

Cost of Goods Sold

Cost of Goods Avail. for Sale*

$10,190

Less: Ending Inventory

(2,260)

Cost of Goods Sold

(7,930)

Gross Margin

$ 8,270

LIFO

Sales (810 units @ $20)

$16,200

Cost of Goods Sold

Cost of Goods Avail. for Sale*

$10,190

Less: Ending Inventory

(1,280)

Cost of Goods Sold

(8,910)

Gross Margin

$ 7,290

*This amount is computed in the Summary of Purchase Transactions at the

beginning of the problem.

Difference in Gross Margin: $8,270 − $7,290 = $980

Note to Instructor: Cost of goods sold can be computed on a units-sold

basis rather than subtracting ending inventory from goods available for

sale.

5-21

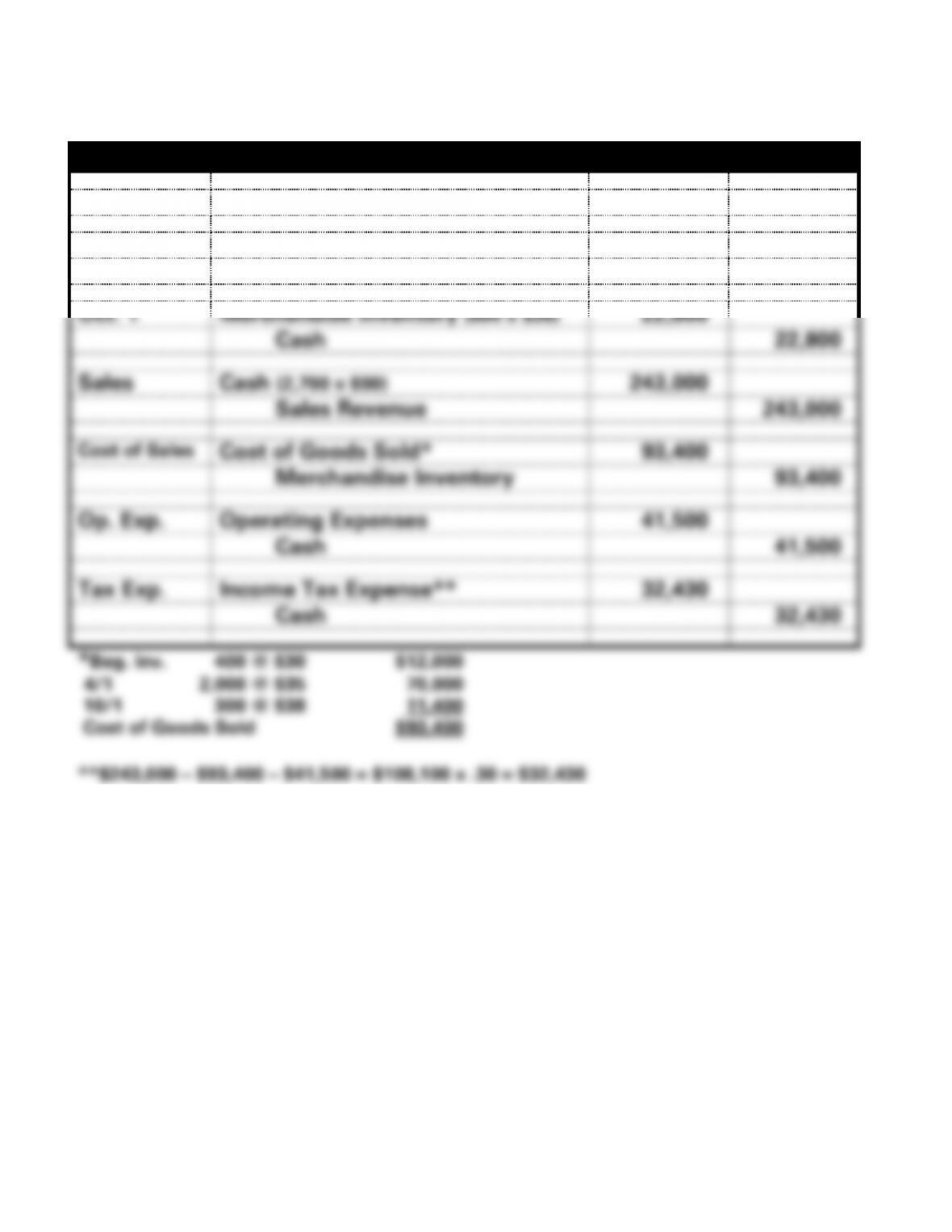

EXERCISE 5-6A

a. (1) FIFO

Date

Account Title

Debit

Credit

Apr. 1

Merchandise Inventory (2,000 x $35)

70,000

Cash

70,000

Oct. 1

Merchandise Inventory (600 x $38)

22,800

Cash

22,800

Sales

Cash (2,700 x $90)

243,000

Sales Revenue

243,000

Cost of Sales

Cost of Goods Sold*

93,400

Merchandise Inventory

93,400

Op. Exp.

Operating Expenses

41,500

Cash

41,500

Tax Exp.

Income Tax Expense**

32,430

Cash

32,430

*Beg. Inv. 400 @ $30 $12,000

4/1 2,000 @ $35 70,000

10/1 300 @ $38 11,400

Cost of Goods Sold $93,400

**$243,000 – $93,400 – $41,500 = $108,100 x .30 = $32,430

5-22

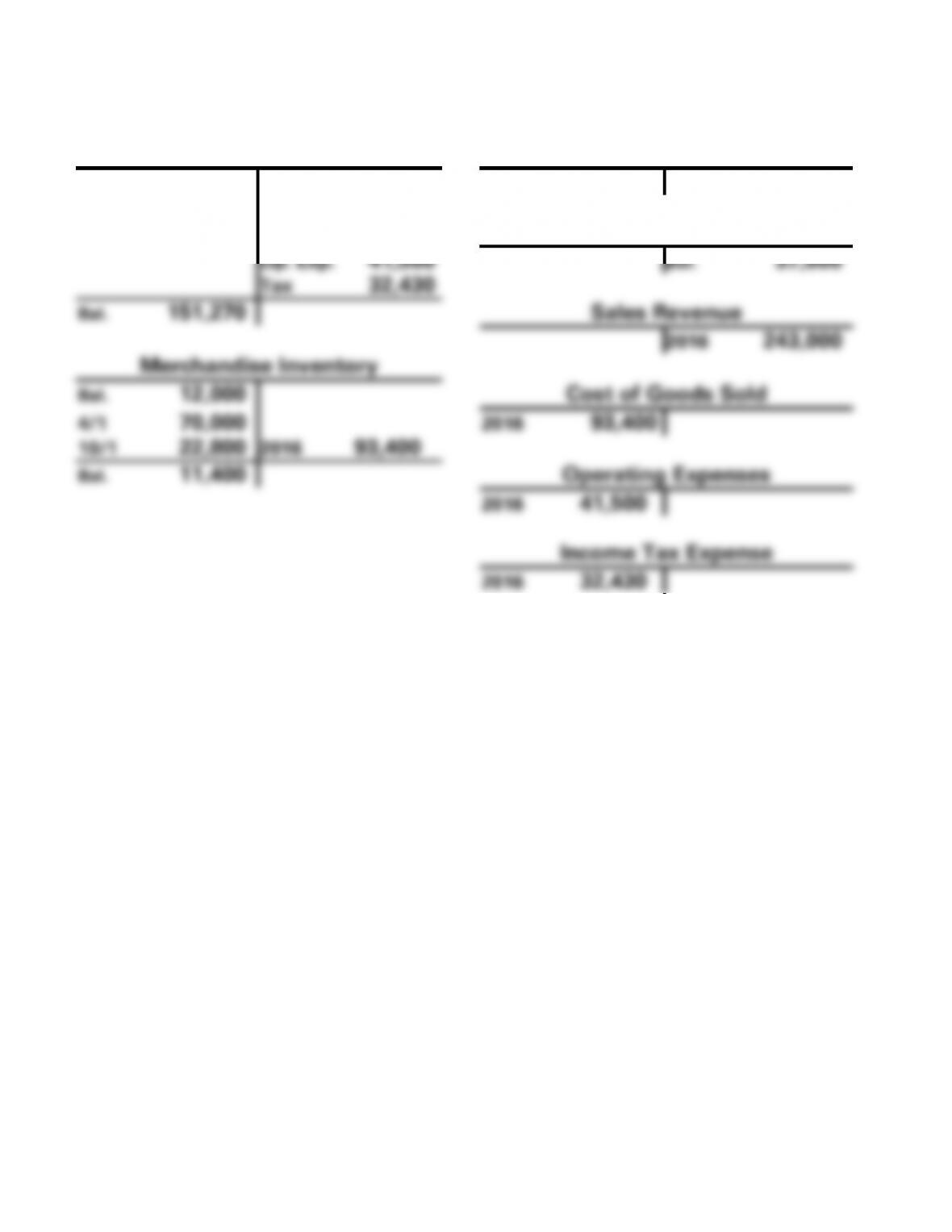

EXERCISE 5-6A a. (cont.)

(1) FIFO

Cash

Common Stock

Bal. 75,000

Bal. 50,000

2016 243,000

4/1 70,000

10/1 22,800

Retained Earnings

Op. Exp. 41,500

Bal. 37,000

Tax 32,430

Bal. 151,270

Sales Revenue

2016 243,000

Merchandise Inventory

Bal. 12,000

Cost of Goods Sold

4/1 70,000

2016 93,400

10/1 22,800

2016 93,400

Bal. 11,400

Operating Expenses

2016 41,500

Income Tax Expense

2016 32,430

5-23

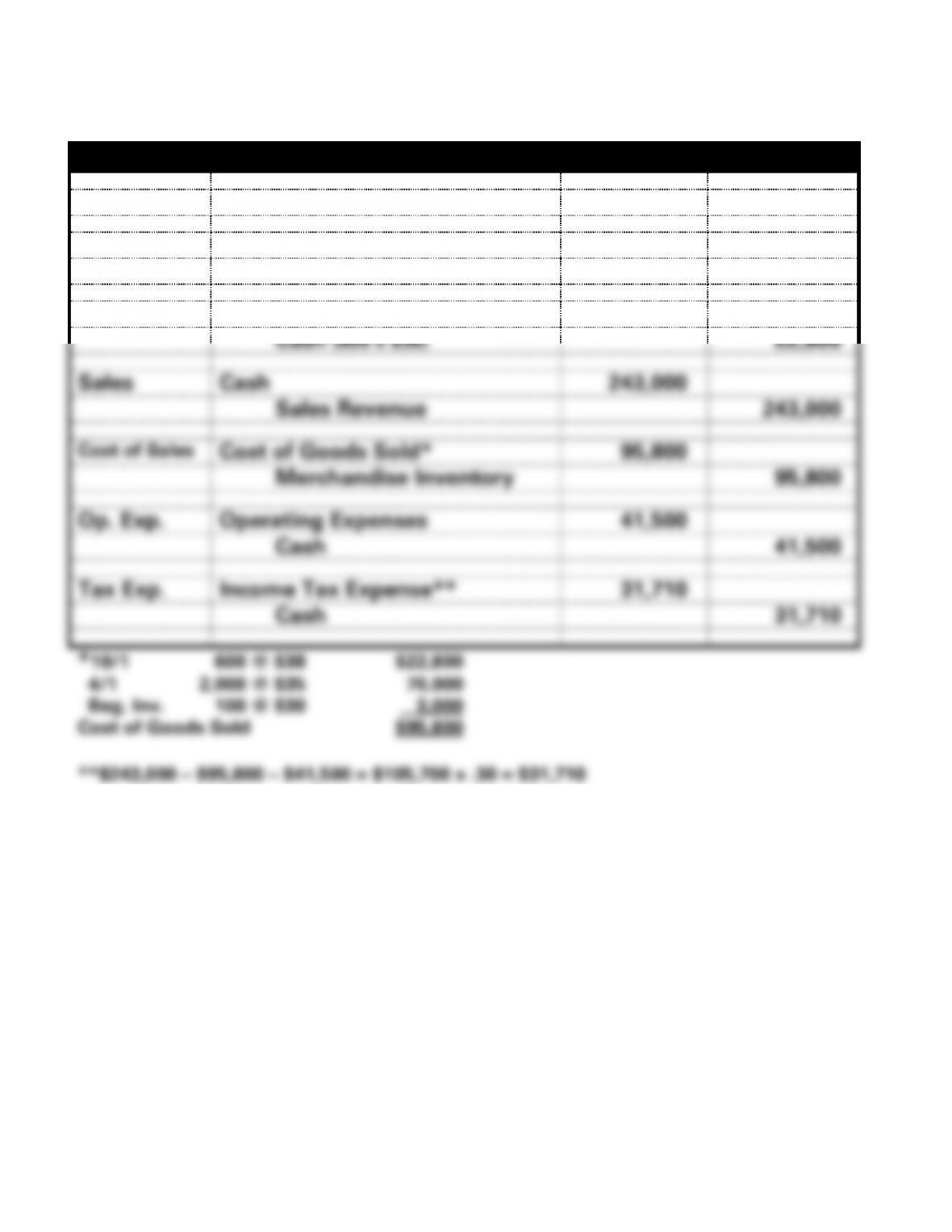

EXERCISE 5-6A a. (cont.)

(2) LIFO

Date

Account Title

Debit

Credit

Apr. 1

Merchandise Inventory

70,000

Cash (3,000 x $22)

70,000

Oct. 1

Merchandise Inventory

22,800

Cash (600 x $38)

22,800

Sales

Cash

243,000

Sales Revenue

243,000

Cost of Sales

Cost of Goods Sold*

95,800

Merchandise Inventory

95,800

Op. Exp.

Operating Expenses

41,500

Cash

41,500

Tax Exp.

Income Tax Expense**

31,710

Cash

31,710

*10/1 600 @ $38 $22,800

4/1 2,000 @ $35 70,000

Beg. Inv. 100 @ $30 3,000

Cost of Goods Sold $95,800

**$243,000 – $95,800 – $41,500 = $105,700 x .30 = $31,710

5-24

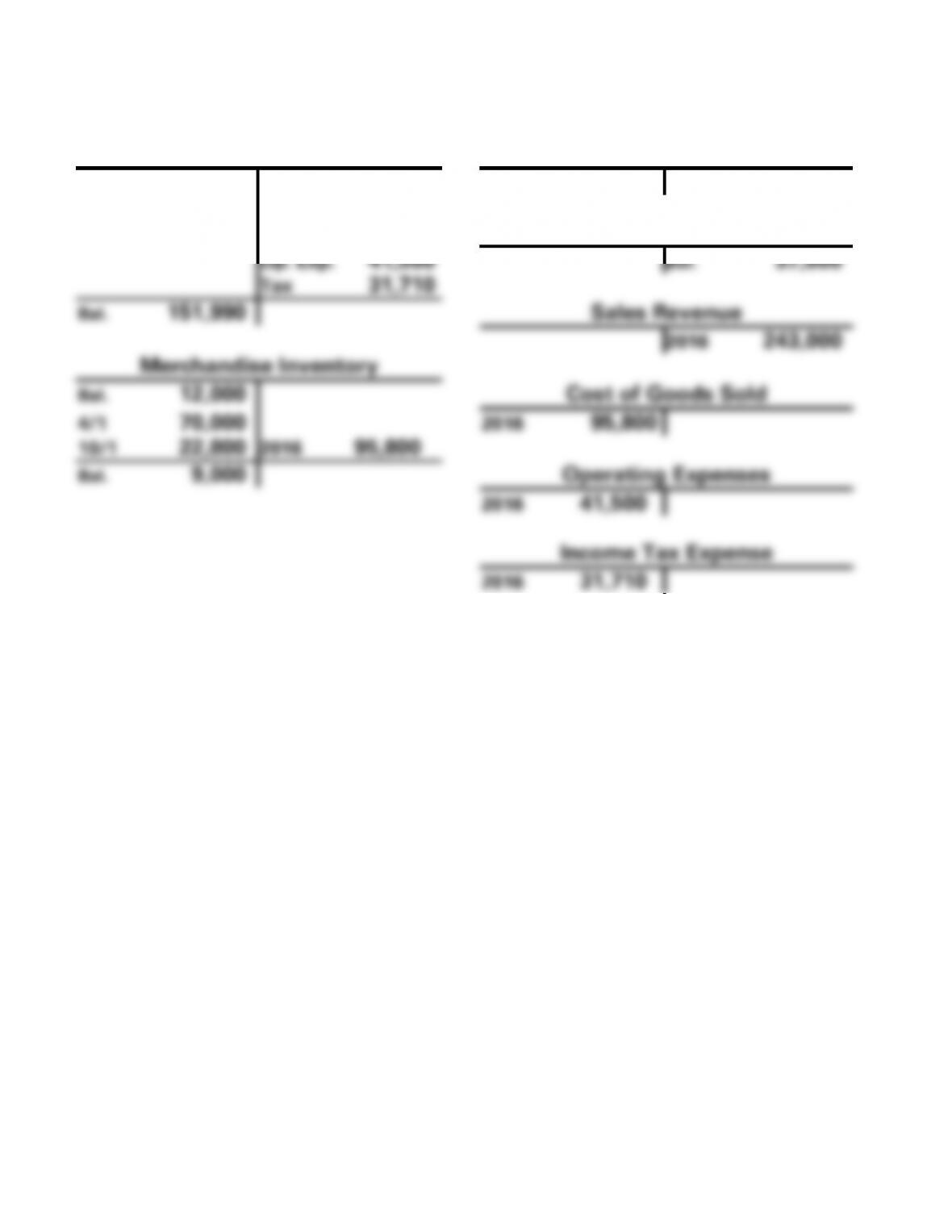

EXERCISE 5-6A a. (cont.)

(2) LIFO

Cash

Common Stock

Bal. 75,000

Bal. 50,000

2016 243,000

4/1 70,000

10/1 22,800

Retained Earnings

Op. Exp. 41,500

Bal. 37,000

Tax 31,710

Bal. 151,990

Sales Revenue

2016 243,000

Merchandise Inventory

Bal. 12,000

Cost of Goods Sold

4/1 70,000

2016 95,800

10/1 22,800

2016 95,800

Bal. 9,000

Operating Expenses

2016 41,500

Income Tax Expense

2016 31,710

5-25

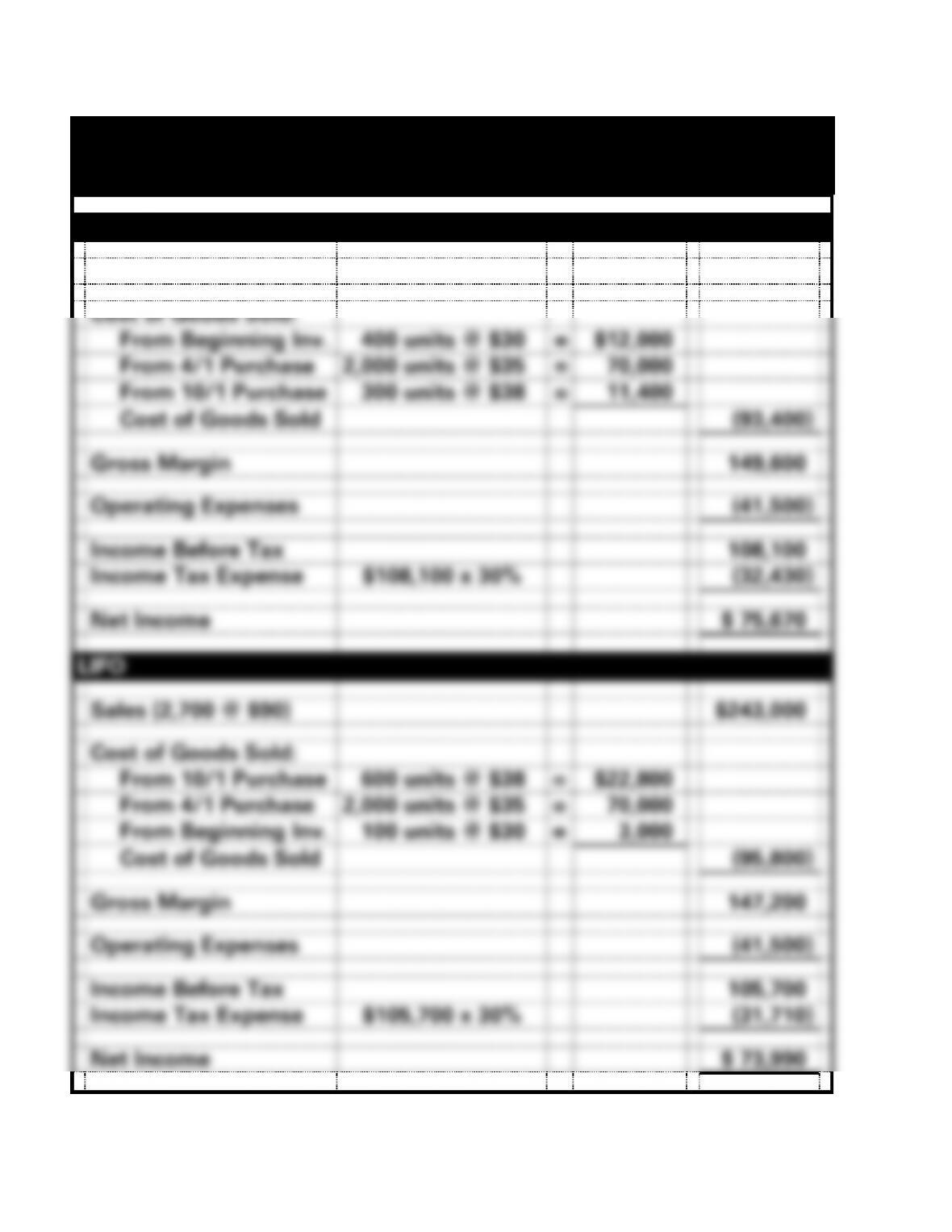

EXERCISE 5-6A (cont.)

b.

Parvin Company

Income Statements

For the Year Ended December 31, 2016

FIFO

Sales (2,700 @ $90)

$243,000

Cost of Goods Sold:

From Beginning Inv.

400 units @ $30

=

$12,000

From 4/1 Purchase

2,000 units @ $35

=

70,000

From 10/1 Purchase

300 units @ $38

=

11,400

Cost of Goods Sold

(93,400)

Gross Margin

149,600

Operating Expenses

(41,500)

Income Before Tax

108,100

Income Tax Expense

$108,100 x 30%

(32,430)

Net Income

$ 75,670

LIFO

Sales (2,700 @ $90)

$243,000

Cost of Goods Sold:

From 10/1 Purchase

600 units @ $38

=

$22,800

From 4/1 Purchase

2,000 units @ $35

=

70,000

From Beginning Inv.

100 units @ $30

=

3,000

Cost of Goods Sold

(95,800)

Gross Margin

147,200

Operating Expenses

(41,500)

Income Before Tax

105,700

Income Tax Expense

$105,700 x 30%

(31,710)

Net Income

$ 73,990